Sample Category Title

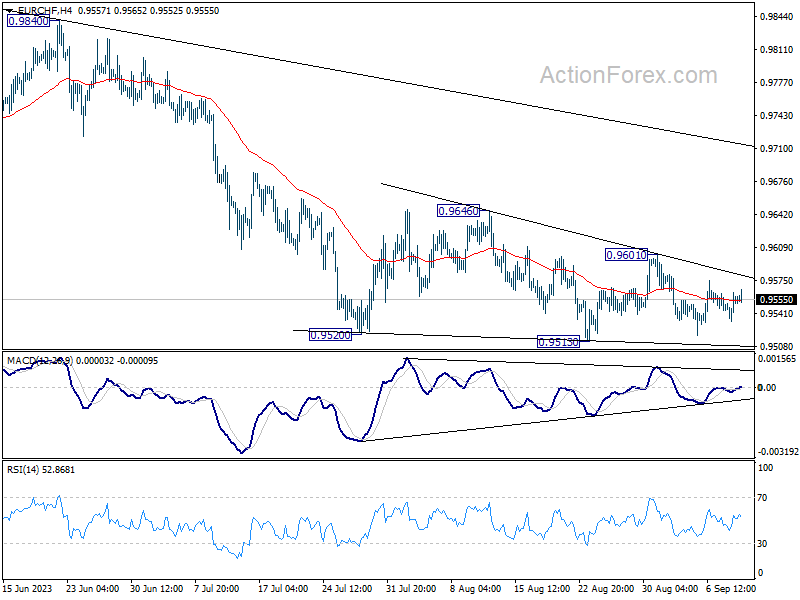

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9539; (P) 0.9552; (R1) 0.9569; More...

Range trading continues in EUR/CHF and intraday bias stays neutral. Outlook also remains bearish for now. On the downside, decisive break of 0.9513 will resume the decline from 1.0095, towards 0.9407 low. However, break of 0.9601 resistance will turn bias back to the upside for stronger rebound to 0.9646 resistance and above.

In the bigger picture, medium term outlook is staying bearish as the cross is capped well below falling 55 W EMA (now at 0.9818). Down trend from 1.2004 (2018 high) is in favor to continue. Sustained break of 0.9407 will target 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. For now, this will remain the favored case as long as 0.9670 support turned resistance holds, in case of strong rebound.

Aussie Recovery Likely Needs Help from US CPI

The Aussie hit 10-month lows last week but is finding a little support to start this week as the greenback falters. Australia’s jobs data will be closely watched but US CPI dominates the global calendar.

AUD/USD last week printed a low since November 2022 at 0.6357 but has showed glimmers of stability in recent sessions. It has been able to steady around 0.6400 despite the Chinese yuan falling to lows since 2007 against the US dollar, at 7.34 for the onshore yuan, 7.36 for the Hong Kong-traded yuan, (CNH).

The yuan fell every day last week but is starting this week on track to snap its losing streak. If China’s central bank – backed by US$3.2 trillion of FX reserves – is now looking to stabilise the yuan, it should be helpful for the Aussie’s tentative stabilisation. Still, China’s August activity data due Friday is not expected to inspire optimism over China’s economy.

The RBA has generally been less hawkish than over major central banks during the post-pandemic global tightening cycle. This remains the case following the RBA’s September meeting. The RBA repeated that “some further tightening of monetary policy may be required” but also introduced a new note of caution about China’s economy. Rates markets price around 40% chance of another rate rise.

Australia’s Q2 GDP data didn’t have a noticeable impact on the Aussie or interest rate expectations. The economy grew by a subdued 0.4%qtr, 2.1%yr. GDP per capita contracted -0.3% as population growth helped avoid a headline recession. Consumer spending was broadly flat but business investment was a positive surprise, increasing by 2.1%.

This week’s Australian data calendar remains worth watching, kicking off with September Westpac consumer sentiment and August NAB business confidence. Most market sensitive is the August labour force survey. After a surprising -15k dip in employment in July, a rebound is expected, Westpac on +40k, the median forecast +25k. We expect the unemployment rate to edge down to 3.6%. A surprise on the strong side might not have a big impact on the Aussie but a weak number would stoke talk of when the RBA might start cutting rates.

The global calendar focus this week is US August CPI. A rebound in gasoline prices is expected to push up annual inflation to 3.6% from 3.2%yr but CPI ex-food and energy will be key. Consensus is 4.3%yr versus 4.7%yr in July, the reading just a week ahead of the Fed policy meeting.

The Aussie cross rate with most at stake this week is probably AUD/EUR, with the ECB’s policy decision not at all clear. Markets price a 40% chance of another hike, to 4.00% deposit rate, while economists are split 26 to 23 in favour of no change in the Bloomberg survey. There is also the risk that ECB President Lagarde’s press conference sends the euro in a different direction from the initial response.

Event risk

Aust Sep Westpac consumer sentiment, Aug NAB business confidence, NZ Pre-election fiscal update, UK Jul unemployment and wages (Tue), UK Jul GDP, US Aug CPI (Wed), Aust Aug employment, ECB policy decision, US Aug retail sales (Thu), China Aug retail sales, industrial production, fixed asset investment, US Sep University of Michigan consumer sentiment, Sep NY Fed Empire State manufacturing survey (Fri)

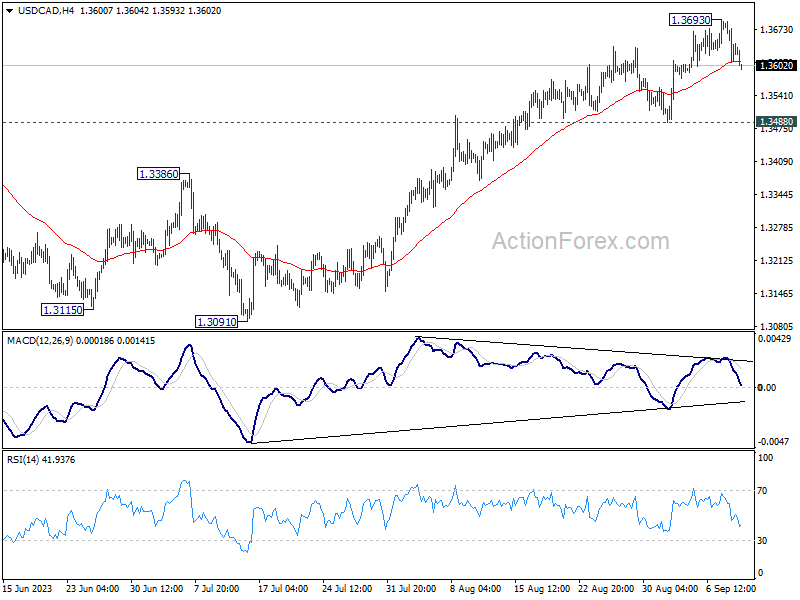

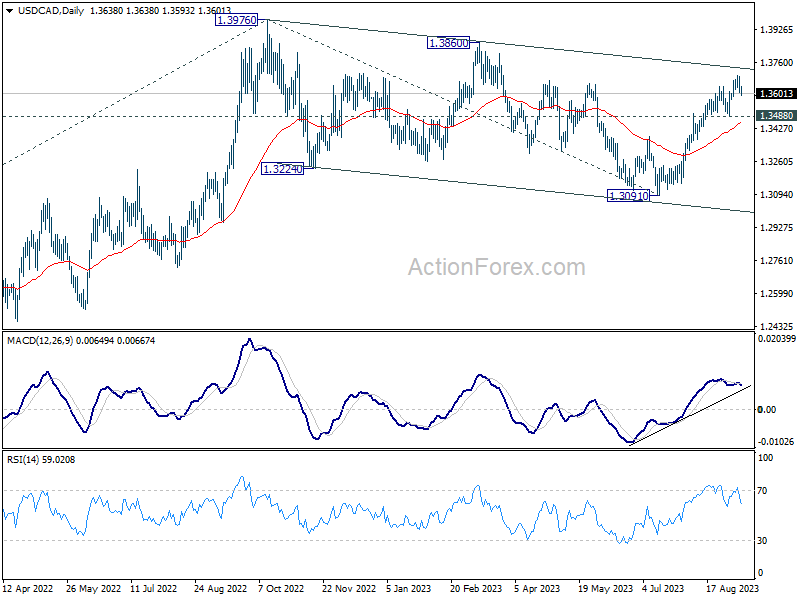

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3601; (P) 1.3647; (R1) 1.3685; More....

Intraday bias in USD/CAD stays neutral at this point. More consolidations could be seen below 1.3693 temporary top. But further rally is expected as long as 1.3488 support holds. Above 1.3693 will resume the rally from 1.3091 to 1.3860 resistance, and then 1.3976 high.

In the bigger picture, price actions from 1.3976 are viewed as a corrective pattern only. Upon completion, rise from 1.2005 (2021 low) would resume through 1.3976. Next target is 61.8% projection of 1.2005 to 1.3976 from 1.3091 at 1.4309. For now, this will remain the favored case as long as 55 D EMA (now at 1.3445) holds.

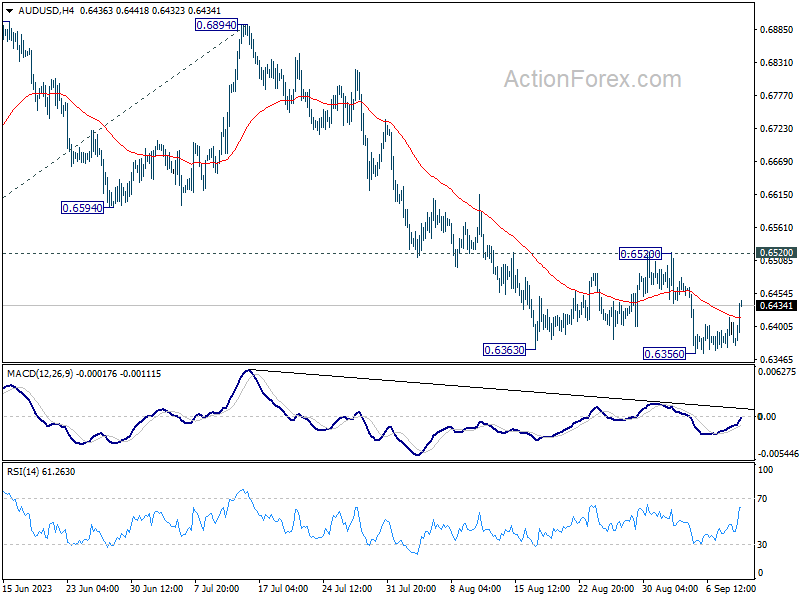

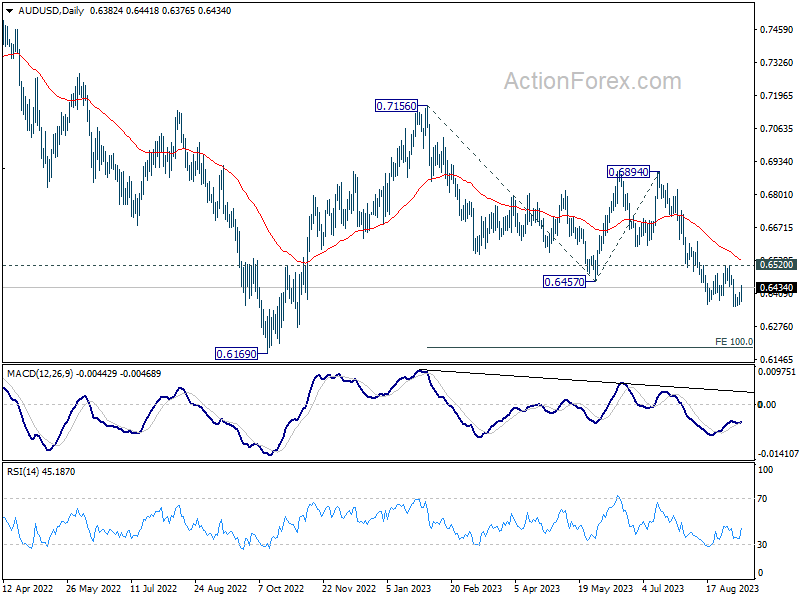

AUD/USD Daily Report

Daily Pivots: (S1) 0.6358; (P) 0.6386; (R1) 0.6406; More...

AUD/USD's recovery from 0.6356 extends higher today but stays well below 0.6520 resistance. Intraday bias remains neutral and further decline is still expected. On the downside, break of 0.6356 will resume larger fall to 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195.

In the bigger picture, current development argues that the down trend from 0.8006 (2021 high) is still in progress. Decisive break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.

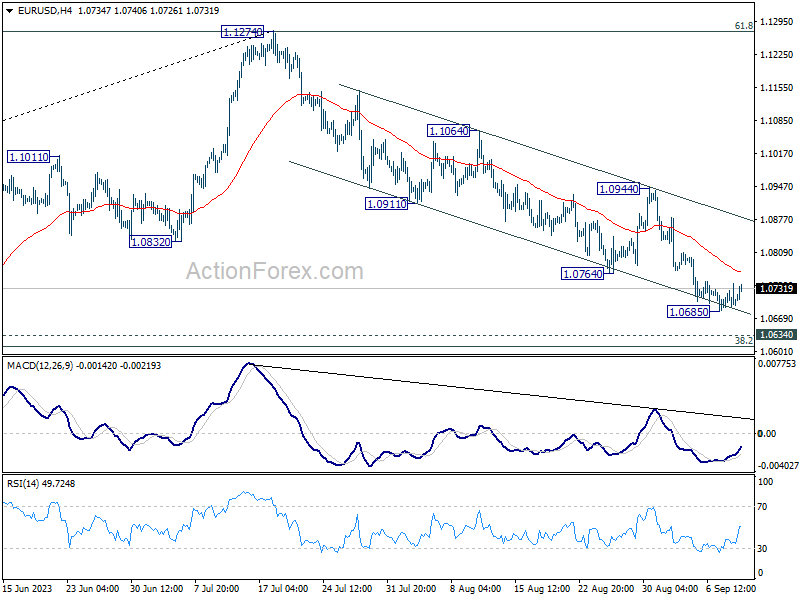

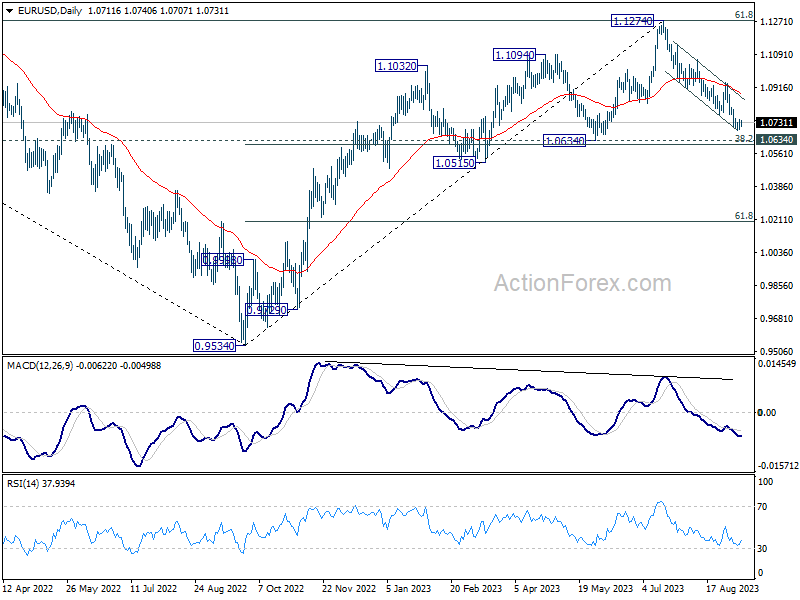

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0681; (P) 1.0713; (R1) 1.0731; More...

Intraday bias in EUR/USD remains neutral as consolidations continue above 1.0685 temporary low. Outlook will stay bearish as long as 1.0944 resistance holds. On the downside, below 1.0685 will resume the fall from 1.1274 to 1.0609/34 cluster support zone next.

In the bigger picture, fall from 1.1274 medium term top is seen as a correction to up trend from 0.9534 (2022 low). Strong support could be seen from 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609) to bring rebound, at least on first attempt. Break of 1.0944 will indicate the start of the second leg, and target retest of 1.1274. However, sustained break of 1.0609/0634 will raise the chance of bearish trend reversal, and target 61.8% retracement at 1.0199.

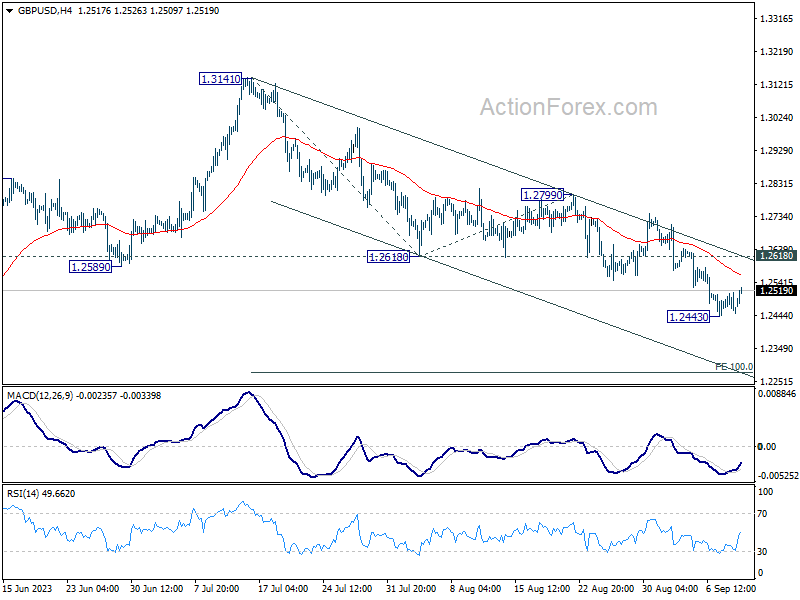

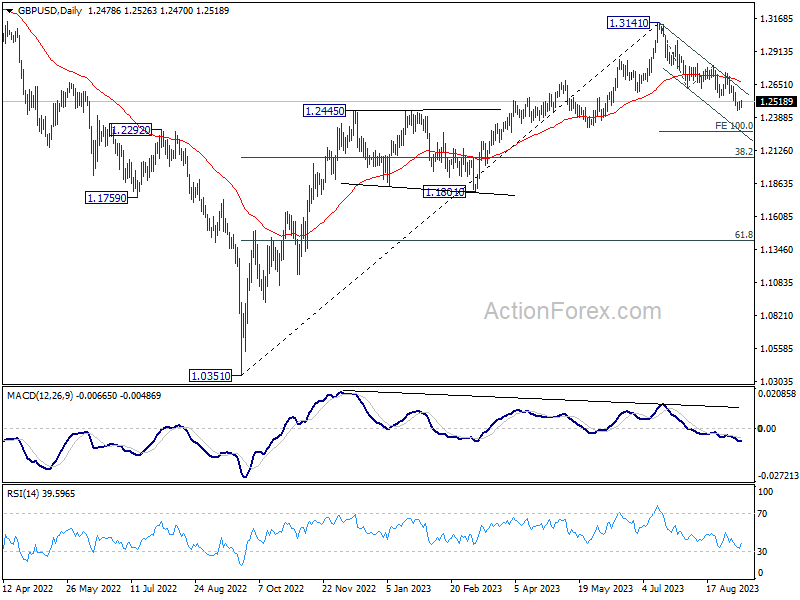

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2441; (P) 1.2478; (R1) 1.2504; More...

Intraday bias in GBP/USD remains neutral for consolidation above 1.2443 temporary low. Upside of recovery should be limited by 1.2618 support turned resistance to bring another fall. Break of 1.2443 will resume the decline from 1.3141 and target 100% projection of 1.3141 to 1.2618 from 1.2799 at 1.2276.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. But outlook will be neutral at best as long as 1.3141 resistance holds, and consolidation from there is set to extend, until further development.

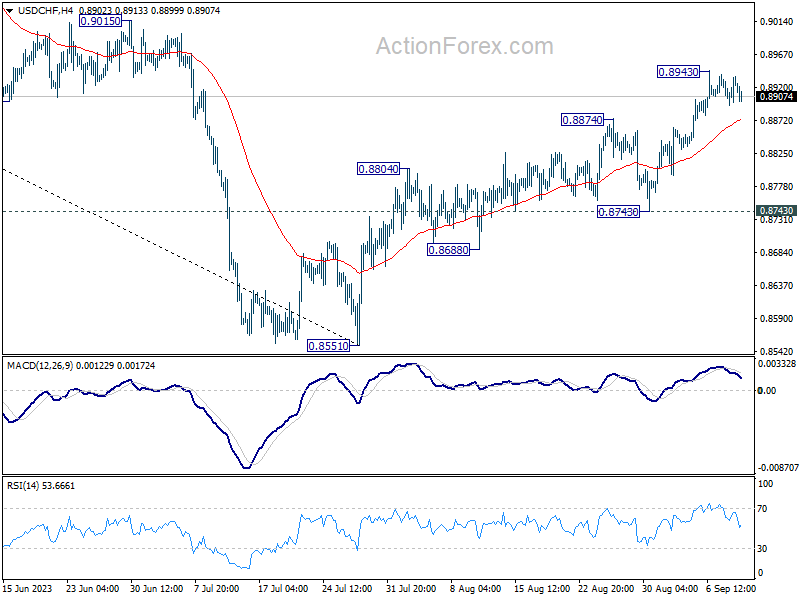

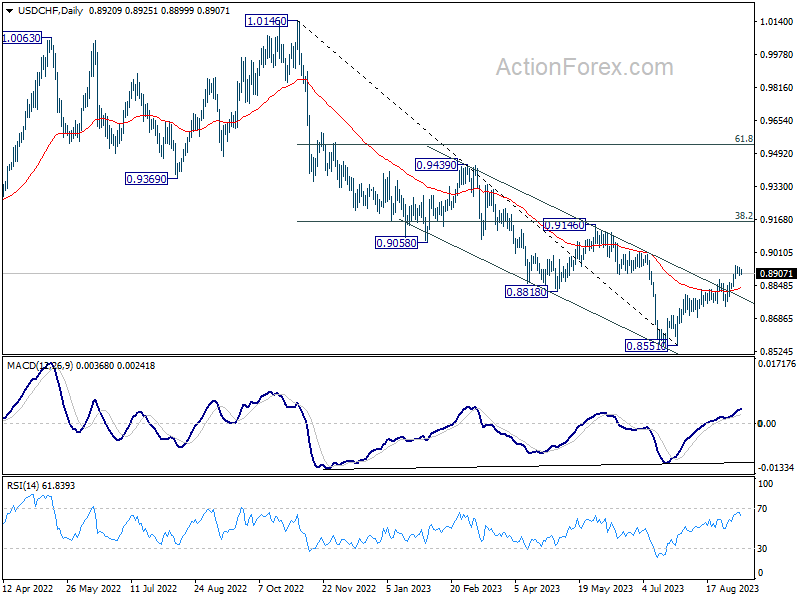

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8904; (P) 0.8921; (R1) 0.8946; More....

Intraday bias in USD/CHF remains neutral as consolidation from 0.8943 temporary top is extending. While deeper pull back cannot be ruled out, downside should be contained above 0.8743 support to bring another rally. Break of 0.8943 will extend the rise from 0.8551 to 0.9146 cluster resistance.

In the bigger picture, rebound from 0.8551 medium term bottom is currently seen as a correction to the downtrend from 1.0146 (2022 high). Further rally would be seen to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160). Strong resistance could be seen there to limit upside, at least on first attempt.

A Busy Week Ahead

The S&P 500 ended last week on a meagre positive note, as the selloff in Apple shares slowed. Apple will be unveiling the new iPhone15 after the Chinese storm. Last week’s selloff was certainly exaggerated. Once the Chinese dust settles, Apple’s performance will continue to depend on the overall sentiment regarding the tech stocks, which will in return, depend on the Federal Reserve (Fed) expectations, the rates, energy prices, Chinese property crisis, deflation risks, and how that mix affects the global price dynamics.

China announced this morning that consumer prices rose by 0.1% y-o-y in August, slower than 0.2% penciled in by analysts and after recording its first drop in over two years of 0.3% a month earlier. Core inflation, excluding food and energy prices, rose 0.8% y-o-y, at the same speed as in July, and remained at the fastest pace since January. The numbers remain alarmingly low, and the recent stimulus measures announced by the government did little to boost investors’ appetite. The CSI 300 was thoroughly sold on the rallies following stimulus news. And the yuan continued trending lower against the US dollar.

The US dollar is under a decent selling pressure this morning, particularly against the yen, after comments from the Bank of Japan (BoJ) Governor Ueda were interpreted as being ‘hawkish’. Ueda said that ‘there may be sufficient information by the year-end to judge if wages will continue to rise’, and that will help them decide whether they would end the super-loose monetary policy and step out of the negative rate territory. The remarks were disputably hawkish, to be honest, but given how negatively diverged the Japanese monetary policy is, any hint that the negative rates could end one day boosts hope. The 10-year JGB yield jumped 5bp to 70bp on the news, and the USDJPY fell to 146.30. The USDJPY has a limited upside potential as the Japanese officials have been crystal clear last week that a further selloff would be countered by direct intervention. But the pair has plenty of room to drop significantly, when the BoJ finally decides to jump and leave the negative rates behind.

This week, the US inflation numbers will give the dollar a fresh direction, and hopefully a softish one. The headline inflation is expected to tick higher from 3.2% to 3.6% in August, on the back of rising energy prices, while core inflation may have eased from 4.7% to 4.3%. ‘We’ve gotten monetary policy in a very good place’ said the NY Fed President Williams last week. Indeed, the Fed hiked the rates by more than 500bp and shed its balance sheet by $1 trillion, while keeping the GDP around 2%, as inflation eased significantly from the 9% peak last summer to around 3% this summer. But crude oil cheapened by more than 40% between last summer and this spring, and the prices are now up by nearly 30% since then. The Fed will likely hold fire when it meets this month, but nothing is less sure for the November meeting. This week’s inflation data will be played in terms of November expectations.

For the European Central Bank (ECB), the base case scenario is a no rate hike at this week’s monetary policy meeting, but the European policymakers could announce a 25bp hike despite the latest weakness in economic data. The EURUSD is slightly better bid this morning, expect consolidation and minor correction toward the 200-DMA, 1.0823, into the meeting. The ECB, unlike the Fed, is not worried about surprising the market, on one side or the other. A no rate hike – even if it’s a hawkish pause - could push the EURUSD to below 1.0615, the major 38.2% Fibonacci retracement, into a medium term bearish trend whereas a 25bp hike should trigger a rally toward the 1.09 level.

On the corporate calendar, ARM will go public this week, in what is going to be this year’s biggest IPO. The company is expected to price on the 13th of September with a price range of $47-51 per share, and will start trading on Nasdaq the following day. ARM is expected to be valued at around $52bn, roughly 20 times its last disclosed annual revenue on expectation that the chips needed to power the generative AI will make ARM a sunny to-go place. Hope it won’t be stormy.

Busy Week Ahead

Market movers today

A busy week starts off with inflation data from the Nordics. In Norway, strong wage growth continues to support broader inflation pressures, and we expect August core inflation to tick slightly higher to 6.6% y/y (from 6.4%). In Denmark, inflation likely remained more muted, we think headline prices rose 3.0% y/y in August.

In the euro area, the EU Commission will publish its economic forecast. In their latest forecast from May the Commission expected GDP growth at 1.1% in 2023 and 1.6% in 2024. We expect the forecasts to be revised down due to the weak Q2 GDP growth figures and the deterioration we have seen over the summer in both the manufacturing and the service sector. Headline inflation has come in slightly lower over the summer, so here we also expect a downward revision of the forecast for 2023 and 2024.

Later this week, the main focus will turn to the ECB meeting on Thursday. Both markets and analyst consensus remain divided between a pause and a 25bp hike, we still expect the ECB to opt for the latter, see more details from our ECB preview, 6 September.

On the data front, markets' will pay close attention to the US August CPI release on Wednesday. While higher energy prices likely lifted headline CPI by 0.5% m/m (3.6% y/y), we look for another low core CPI print at 0.2% m/m (4.3% y/y).

The 60 second overview

Markets: Global financial markets closed last week with subdued activity. The S&P index recorded a marginal uptick, while Europe's Stoxx 600 experienced a 0.2% gain, primarily bolstered by the performance of energy stocks, in tandem with the ongoing appreciation of oil prices. Concurrently, US Treasury yields registered an upward trajectory, lending support to the USD, which marked its eighth consecutive week of ascent - a streak not seen since 2005. This robust performance of the USD has increasingly captured the attention of policymakers in Japan and China, triggering deliberations about its potential impact on their respective economies. In China, consumer prices displayed a modest uptick of 0.1% y/y in August, a slight rebound from the 0.3% decline observed in July, aligning with consensus expectations. Although this shift marked an exit from deflationary territory, the persistent softness in pricing pressures is indicative of subdued demand conditions.

Elsewhere, Brent crude prices advanced by 0.8%, extending their weekly gains to over 2% - now at around $90 USD per barrel. This surge has propelled oil prices to their highest levels since November of the preceding year with Saudi Arabia's and Russia's announcement of an extension of supply cuts until year-end.

This morning, Asian markets are mixed. Futures point to a neutral open in Europe. In Japan, the JPY strengthened after Bank of Japan governor, Kazuo Ueda, hinted that the Japanese central bank could have enough information about wage dynamics by year-end - a key factor in deciding when to end its negative monetary policy rate. The yield on 10-year Japanese government bond rose above 0.7% for the first time since 2014 on the back of Ueda's comments.

Equities: Global equities marginally higher Friday in rather dull session. Energy stocks continued to do well while industrials and materials underperformed. Wait-and-see markets ahead of ECB and Fed meetings seems a little early but yields and monetary policy outlook plays and important role for equities. In US on Friday, Dow +0.2%, S&P500 +0.1%, Nasdaq +0.1% and Russell 2000 -0.2%. Action and focus on Asia this morning with a strong yen on the back of a shift in tone from Bank of Japan. Japanese 10-year yields are up 6bp and bank stocks massively outperformed on a day when Nikkei 225 is lower by 0.5%. US and European futures are in green this morning.

FI: It is going to be a busy week in terms of key economic data and central bank meetings. The main events are the US inflation for August on Wednesday, US retail sales for August on Thursday as well as the ECB meeting on Thursday. The core US inflation is expected to rise by 0.2% m/m. ECB is expected to raise rates by 25bp.

FX: EUR/USD is hovering around the 1.07 mark, as strong US data and general risk-off sentiment have weighed on the cross the past couple of months. USD/JPY is trading around the 147 mark, as elevated US yields still add support to the cross. EUR/GBP is just short of the 0.86 mark. EUR/SEK remained range-bound around 11.85-95 all of last week, consolidating in wait of the next trigger. EUR/NOK has been on a downward trajectory in September and is now trading around 11.45. The rally in EUR/DKK stalled on Friday - it traded slightly to the strong side of the 7.4604 central rate.

Credit: The week ended on a positive note with US markets rallying after a relatively slow European session. Credit markets followed suit and Itrax Main tightened 1.1bp to close at 70.9bp, while Itrax Xover tightened 3.5bp to close at 399.5bp. The usual Friday-lull returned to primary markets, which were relatively calm despite the slightly improved risk sentiment.

Nordic macro

Norwegian core inflation has been volatile in recent months, driven largely by food prices. These climbed far less in July than last year, which may mean that they come down more cautiously than normal in August. There are also signs that the biggest price hikes may now be behind us, and producer prices on food have slowed in recent months. On the other hand, we expect services inflation to remain high due to stronger wage growth, and airfares look likely to rise further. We therefore expect core inflation to climb to 6.6% y/y in August.

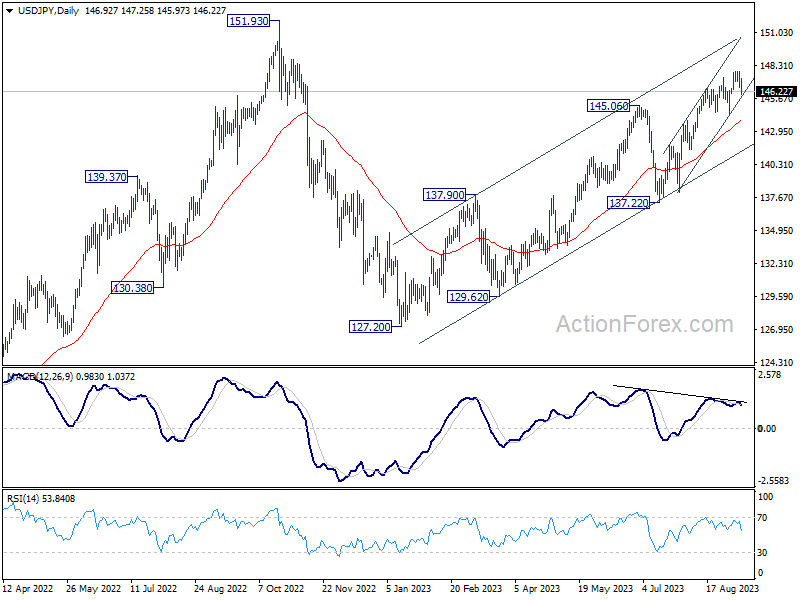

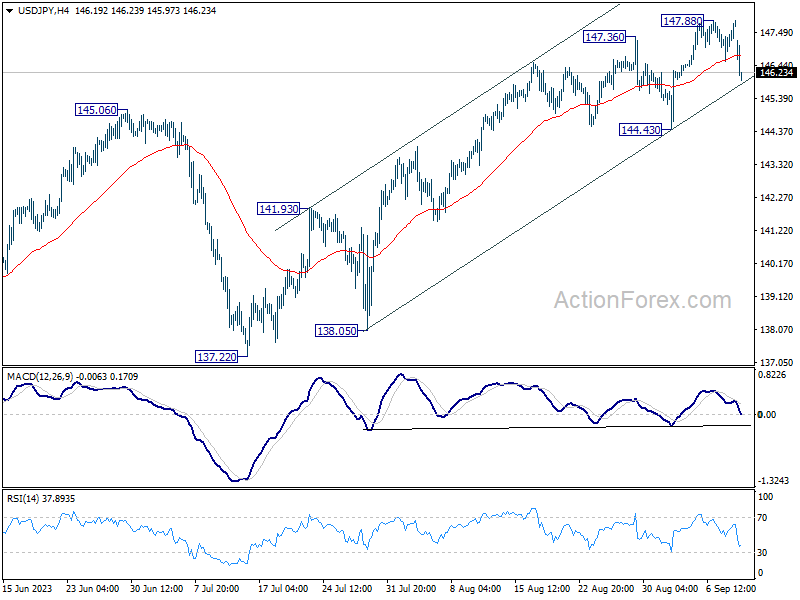

USD/JPY Daily Outlook

Daily Pivots: (S1) 146.93; (P) 147.40; (R1) 147.76; More...

USD/JPY dips notably today, but stays well above 144.43 support. Intraday bias remains neutral at this point, as consolidation from 147.88 could extend. But outlook remains bullish with 144.43 support intact. On the upside, above 147.88 will resume larger rise from 127.20, to retest 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by break of 137.22 support will indicate that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.