Sample Category Title

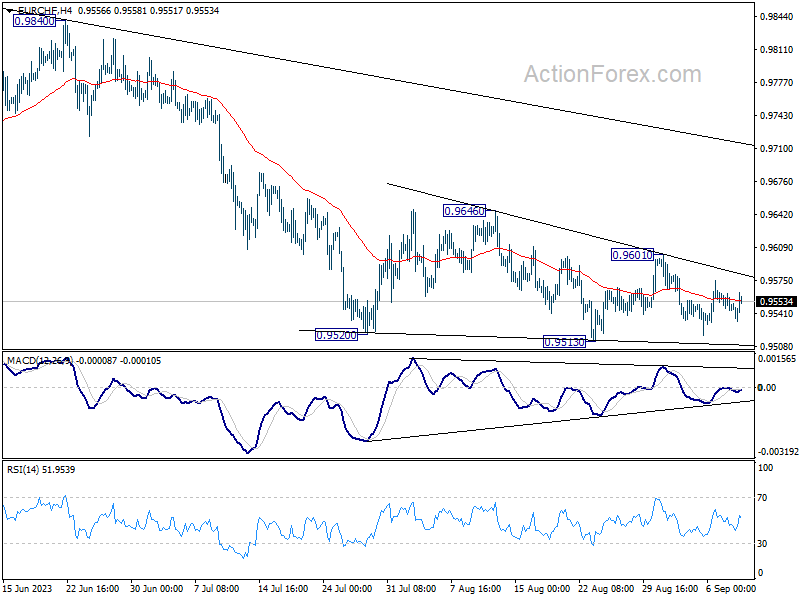

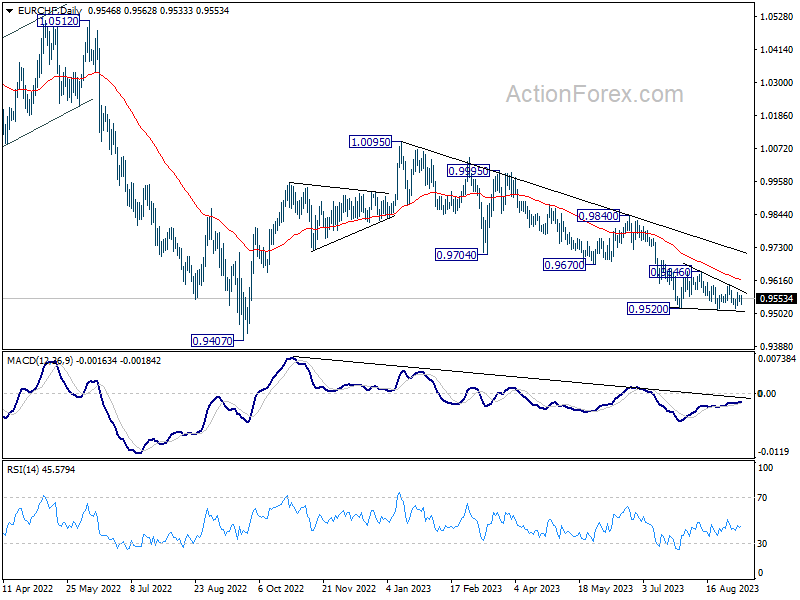

EUR/CHF Weekly Outlook

EUR/CHF's sideway trading continued last week and outlook is unchanged. Initial bias remains neutral this week first, and larger down trend is still in favor to continue. On the downside, decisive break of 0.9513 will resume the decline from 1.0095, towards 0.9407 low. However, break of 0.9601 resistance will turn bias back to the upside for stronger rebound to 0.9646 resistance and above.

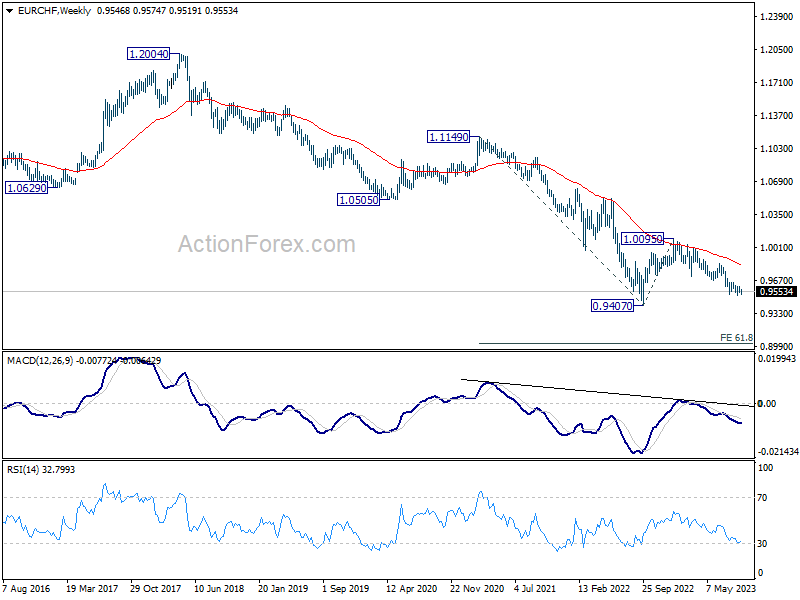

In the bigger picture, medium term outlook is staying bearish as the cross is capped well below falling 55 W EMA (now at 0.9818). Down trend from 1.2004 (2018 high) is in favor to continue. Sustained break of 0.9407 will target 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. For now, this will remain the favored case as long as 0.9670 support turned resistance holds, in case of strong rebound.

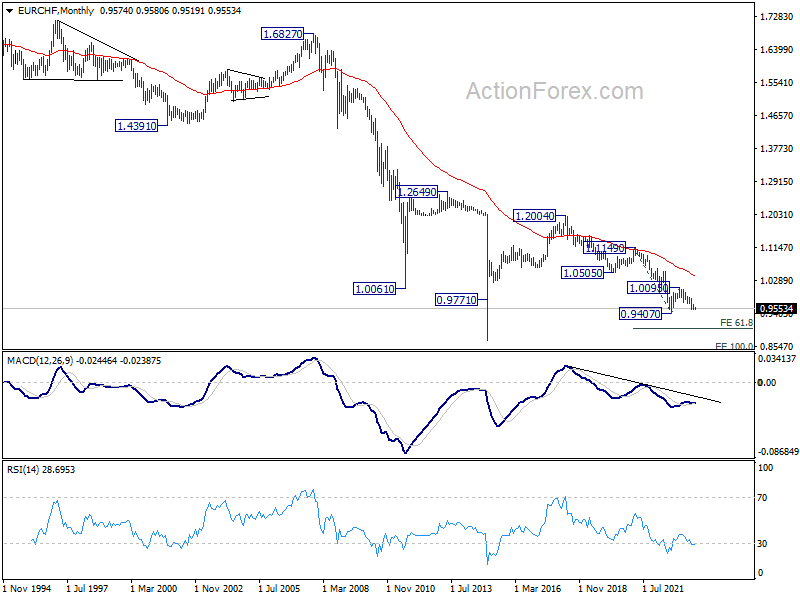

In the long term picture, outlook remains bearish as it's staying well below 55 M EMA (now at 1.0391). Break of 1.00095 resistance is needed to be the first sign of bottoming, or the multi-decade down trend is expected to continue.

Weekly Economic & Financial Commentary: China’s Economic Free Fall Continues

Summary

United States: Service Sector Continues to Support Growth

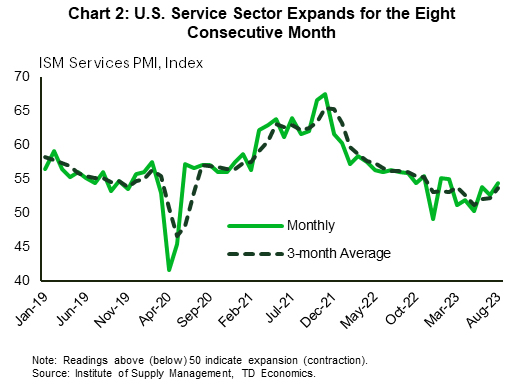

- During August, the ISM Services Index bested consensus expectations and rose to 54.5, hitting the highest reading since February. The monthly upturn highlights ongoing strength in the service sector and overall resilience of U.S. economic growth despite higher interest rates. An uptick in the prices paid component of ISM services index as well as this week's leg-up in oil prices are reminders of the obstacles ahead to fully tamp down inflation.

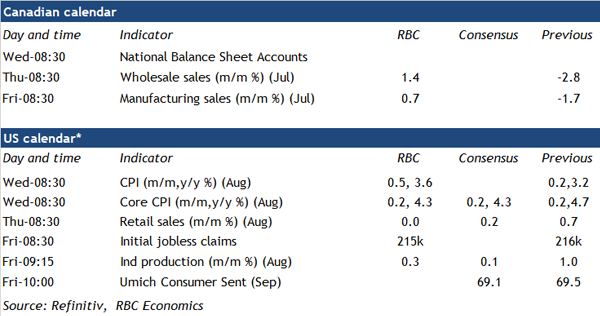

- Next week: CPI (Wed), Retail Sales (Thu), Industrial Production (Fri)

International: China's Economic Free Fall Continues

- This week, new data revealed China's economic slowdown is still in effect and a bottom has yet to be reached. China's August Caixin PMI indices showed a more robust deceleration in the services sector than expected. Service sector problems reflect Chinese households' unwillingness to spend and a preference to save, which not even the lifting of Zero-COVID policies has been able to alter.

- Next week: Brazil CPI (Tue), Argentina CPI (Thu), ECB Decision (Thu)

Interest Rate Watch: If the Fed Is Done, How Long Will We Be on Hold?

- Comments this week from N.Y. Fed President Williams suggested monetary policy is in a "good place" and Chicago Fed President Goolsbee said the Fed was "rapidly approaching the time when our argument is not going to be about how high should the rates go." These remarks are tacitly signaling the end of the tightening cycle. If that is indeed the case, we explore how the length of time the Fed stays on hold could be consequential.

Credit Market Insights: Fed's Beige Book Reveals Continued Uncertainty on the Outlook

- This week, the Federal Reserve released its September Beige Book, covering economic conditions across the country for the months of July and August. For the most part, economic growth was steady and generally unchanged from the previous period.

Topic of the Week: US Open Highlights Consumers' Hunger for Experiences

- Tennis fans have been converging on Queens, New York to catch the U.S. Open. Resale prices for tickets are higher than ever, but consumers appear more willing to pay up to witness this event.

The Weekly Bottom Line: Higher for Longer Seems Surer

U.S. Highlights

- Hard economic data was thin on the ground over the Labor Day shortened week, with survey indicators and Fed speakers grabbing attention.

- A slew of Federal Reserve speakers hint that the central bank may skip a rate hike at the next meeting, as the Beige Book (the Fed’s survey of economic conditions) suggests that the economy closed out the summer on a modest note.

- Oil markets were also on the move, after Saudi & Russian supply cuts were extended. Higher energy prices are a challenge to the needed cooling in inflation.

Canadian Highlights

- As widely anticipated, the BoC remained on hold, keeping the overnight lending rate at 5% while keeping the door open for another hike.

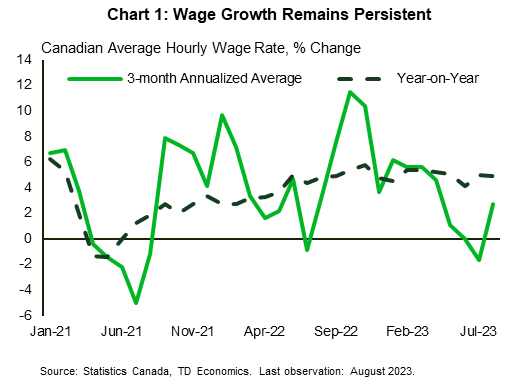

- The labour market moved towards greater balance in August with job gains not keeping pace with population growth, although wage growth remains too strong.

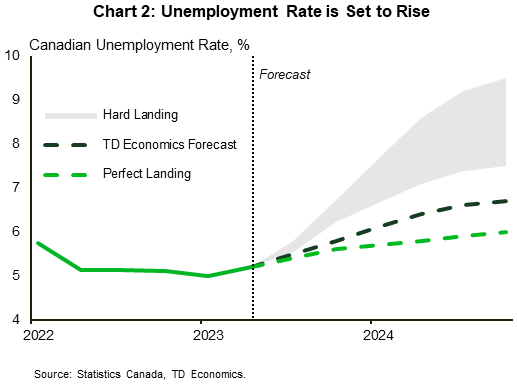

- The Bank of Canada needs to see more softness in the labour market to put a permanent end to this tightening cycle. We expect this to manifest more clearly by the October decision.

U.S. – Higher for Longer Seems Surer

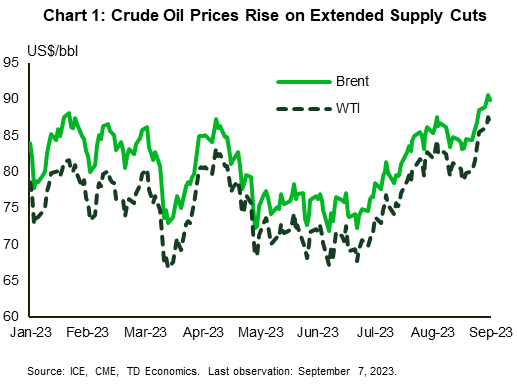

Hard economic data was thin on the ground over the Labor Day shortened week, with survey indicators and Fed speakers the main highlights on the calendar. Crude oil markets were also a bit livelier after Saudi Arabia and Russia both announced extensions to their supply cuts through to the end of the year.

Since July, Saudi Arabia has voluntary removed 1 million barrels per day (b/d) of crude from global oil markets. While the measure was cited to be temporary, it was already extended to September, with this week’s announcement extending it once again. Russia added their own export reduction of 300,000 b/d. On the day of the announcement, Brent crude, the international benchmark, rose 1.2% to close at $90.04 – exceeding $90 a barrel for the first time this year (Chart 1). Prices have since given back some of the gain, but the general move higher in oil prices over the past few weeks is likely to threaten efforts to tame inflation.

On that front, this week featured a full roster of Fed speakers. Governor Waller was also in the news making more dovish than usual statements. He noted that data showing a cooling job market meant the Fed should “proceed carefully”, and does not necessitate an imminent rate hike. Bostic echoed these sentiments. Logan noted that it could be appropriate’ to skip an interest-rate increase in September. Williams left whether the Fed would hike again as an open question, while Goolsbee, hinting at a higher for longer stance, sees a “golden opportunity” for the Fed to tame inflation without triggering a recession. All speakers emphasized that the Fed will be paying close attention to the data.

The Fed’s latest survey of economic conditions, the Beige Book, noted that the U.S. economy grew at a modest pace during July and August, relative to slight growth in the previous report. This was bolstered by a final bout of pent-up demand for leisure activities. Outside of leisure travel and a rise in auto sales due to better inventory, nonessential retail sales slowed. Job growth was generally subdued nationwide with wage growth elevated but expected to moderate in the months ahead. Prices for consumer goods fell faster than in many other categories. Demand for manufactured goods waned while the supply constrained single-family housing market continued to be challenged by higher financing costs and rising insurance premiums.

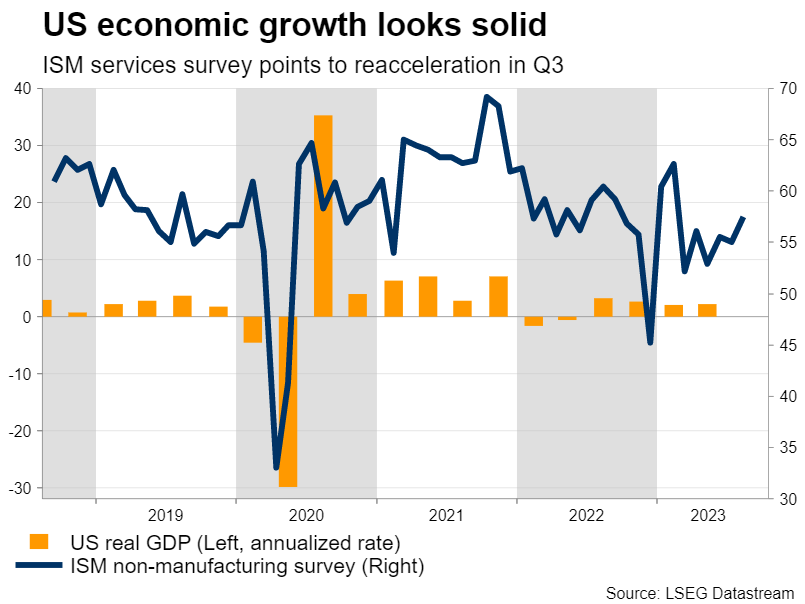

The ISM services index surprised to the upside this week, reaching a six-month high of 54.5 in August (Chart 2). The survey continued to highlight a service sector that is still in expansion mode, with survey respondents expressing positive sentiments about business and economic conditions. Beneath the headline, the positive details were an increase in business activity (+0.2 pts), new orders (+2.5 pts), and employment (+4.0 pts).

The tone of the economic news this week is likely to keep policymakers in a wait and see mode. Consumers are keeping the service sector humming along, even as the labor market cools. All good news for the Fed, but higher energy prices remain a wildcard that will require close monitoring so as not to undo the progress on inflation thus far.

Canada – Finding a Balance

There was no surprise in the Bank of Canada's announcement this Wednesday. As widely anticipated, the benchmark overnight lending rate remained at 5%. In the wake of the decision, the market implied policy rate moved lower by roughly 10 basis points over the week. This shift put more pressure on Canadian dollar. When measured in U.S. currency, the loonie got cheaper by almost one cent. The loonie is down nearly three cents since the BoC's July interest rate announcement.

This was the second pause in this tightening cycle, but this time, the BoC did not characterize it as such. The tone of the message remained hawkish, with Governor Macklem reiterating his loud promise "to take further action", if needed. Indeed, the first time the Bank went on hold earlier in the year markets resolved that rate cuts won't be too long in coming. This helped ease financial conditions enough to reinvigorate the housing market and consumer spending in the first quarter.

Fifty basis points of hikes later, the risk of overtightening is higher as weakness in economic activity is more convincing. Recent readings of GDP, retail trade and home sales provide compelling evidence that demand is moderating. Nonetheless, the labour market continues to give mixed signals. August's headline employment gain at 40K new jobs was twice as high as expected by the consensus, but the pace of employment growth is lower than population growth, leading to a slight rise in the unemployment rate – at least at the second decimal place.

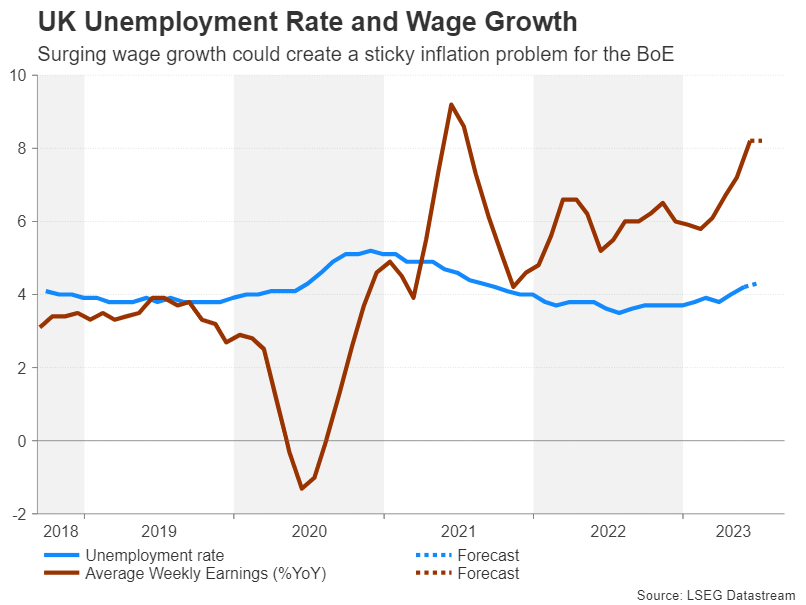

Meanwhile, headline wage growth eased slightly in August (on a year-on -year basis). The three-month annualized average change in wages did pick up, but still points to a cooler pace of wage gains in the months ahead (Chart 1). Overall, the pace remains too strong for broad inflation to move to its target. Additionally, when coupled with a decline in productivity, high wage growth means unit labour costs are rising for businesses. In a strong demand environment, businesses may pass this onto consumers, keeping inflation up, or they may cut costs by reducing investment or shedding workers.

Persistent wage pressure remains the most unfading signal of an unbalanced labour market. Still, we expect it to move to a lower trajectory as employees' ability to negotiate a pay raise diminishes as job vacancies become scant. As outlined in our recent report, the job market has reached an inflection point, setting a path for the unemployment rate to rise to 6.7% over the next year, slightly overshooting the level required to balance the market (Chart 2).

All told, while the market odds of another rate hike are lower, the Bank of Canada will need to see more softness the labour market and continued slowing in economic momentum through the rest of this year to remain on the sidelines. Until the Bank meets again on October 25th, we will have several economic releases, including two more inflation reports. By then, we expect the progress in rebalancing demand and supply in the economy will manifest more clearly, putting a permanent end to the tightening cycle.

U.S. Inflation Expected to Rise in August on Soaring Gasoline Prices

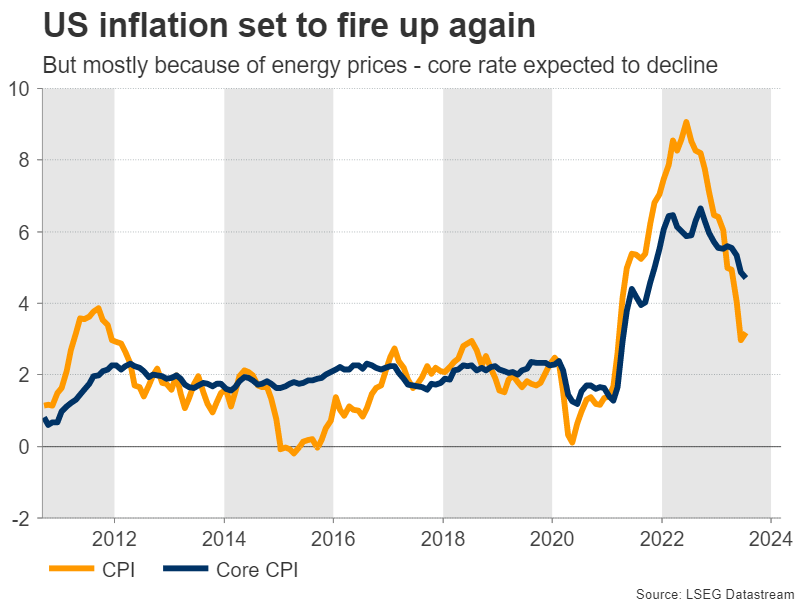

The U.S. Federal Reserve will be on the lookout for signs that broader inflation trends continued to slow down in August—even as energy prices spiked. We expect headline CPI to tick up to 3.6% year-over-year in August, up from 3.2% in July. This increase is almost entirely explained by higher global energy prices. Gasoline prices rose more than 10% month-over-month (on a seasonally adjusted basis) between July in August. And energy prices as a whole likely reported their steepest month-over-month growth since mid-2022.

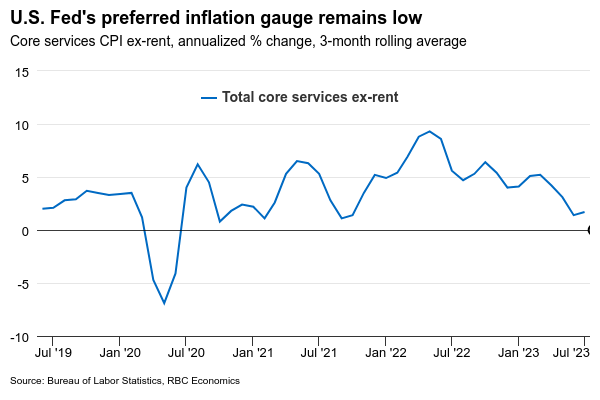

Aside from energy, U.S. price pressures have eased substantially in recent months. Food price growth has moderated sharply and we look for ‘core’ (ex-food & energy) price growth to slow to 4.3% year-over-year in August from 4.7% the month before. That will drop the measure further below a 6.6% peak in September last year. Month-over-month increases in the Fed’s preferred “supercore” measure (CPI services excluding rent) have been running below a 2% annualized rate for the last four months. But inflation pressures won’t stay that low if surging economic growth data and firm labour markets don’t show further signs of softness. But the economic backdrop abroad is slowing, job openings and quit rates continue to decline, and ‘excess’ savings that cushioned households from the blow of higher prices and interest rates are now largely depleted. We continue to look for U.S. economic growth to soften in the coming months—preventing a re-acceleration of broader inflation pressures.

- According to StatCan’s advance estimates for July, “core” wholesale sales rose by 1.4%, higher motor vehicle and parts sales (+5.8%) contributed to this, offsetting lower sales in machinery, equipment and supplies.

- Manufacturing sales ticked up 0.7% in July according to the flash estimate, primarily driven by petroleum and coal product, food, and primary metal subsectors. Industrial prices in the manufacturing sector rose more than that (seasonally adjusted) in July, suggesting that sales declined excluding price impacts.

- U.S. retail sales likely remain unchanged in August, following a 0.7% uptick in the prior month. This expected slowdown in growth is mainly due to a 4.5% decline in unit auto sales in August. Excluding autos, we expect sales edged up by 0.3% although largely due to a price-related increase in sales at gas stations.

- We expect that U.S. industrial production inched up 0.3% in August, decelerating from a 1% increase in July. Most of this growth was drive by the manufacturing sector, where hours worked rose.

- Canadian household net wealth likely rose in Q2 with an increase in house prices and stronger equity markets pushing asset values up more than debt levels. A surge in household disposable incomes in Q2 likely pushed the debt-to-income ratio lower and left the debt servicing ratio little-changed despite further increases in debt payments. Signs that labour markets softened into Q3 mean that positive income boost is unlikely to be repeated in the near-term.

Summary 9/11 – 9/15

Monday, Sep 11, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y Jul | 2.50% | 2.40% |

| 06:00 | JPY | Machine Tool Orders Y/Y Aug P | -19.80% | |

| 08:00 | EUR | Italy Industrial Output M/M Jul | -0.30% | 0.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y Jul | |

| Forecast: 2.50% | Previous: 2.40% | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Aug P | |

| Forecast: | Previous: -19.80% | ||

| 08:00 | EUR | Italy Industrial Output M/M Jul | |

| Forecast: -0.30% | Previous: 0.50% | ||

Tuesday, Sep 12, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Westpac Consumer Confidence Sep | -0.40% | |

| 01:30 | AUD | NAB Business Conditions Aug | 10 | |

| 01:30 | AUD | NAB Business Confidence Aug | 2 | |

| 06:00 | GBP | Claimant Count Change Aug | 29K | |

| 06:00 | GBP | ILO Unemployment Rate (3M) Jul | 4.30% | 4.20% |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jul | 7.60% | 7.80% |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Jul | 8.20% | 8.20% |

| 09:00 | EUR | Germany ZEW Economic Sentiment Sep | -15 | -12.3 |

| 09:00 | EUR | Germany ZEW Current Situation Sep | -75 | -71.3 |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Sep | -6.2 | -5.5 |

| 10:00 | USD | NFIB Business Optimism Index Aug | 91.6 | 91.9 |

| 23:50 | JPY | PPI Y/Y Aug | 3.20% | 3.60% |

| 23:50 | JPY | BSI Large Manufacturing Conditions Q3 | 0.2 | -0.4 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Westpac Consumer Confidence Sep | |

| Forecast: | Previous: -0.40% | ||

| 01:30 | AUD | NAB Business Conditions Aug | |

| Forecast: | Previous: 10 | ||

| 01:30 | AUD | NAB Business Confidence Aug | |

| Forecast: | Previous: 2 | ||

| 06:00 | GBP | Claimant Count Change Aug | |

| Forecast: | Previous: 29K | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) Jul | |

| Forecast: 4.30% | Previous: 4.20% | ||

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jul | |

| Forecast: 7.60% | Previous: 7.80% | ||

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Jul | |

| Forecast: 8.20% | Previous: 8.20% | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment Sep | |

| Forecast: -15 | Previous: -12.3 | ||

| 09:00 | EUR | Germany ZEW Current Situation Sep | |

| Forecast: -75 | Previous: -71.3 | ||

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Sep | |

| Forecast: -6.2 | Previous: -5.5 | ||

| 10:00 | USD | NFIB Business Optimism Index Aug | |

| Forecast: 91.6 | Previous: 91.9 | ||

| 23:50 | JPY | PPI Y/Y Aug | |

| Forecast: 3.20% | Previous: 3.60% | ||

| 23:50 | JPY | BSI Large Manufacturing Conditions Q3 | |

| Forecast: 0.2 | Previous: -0.4 | ||

Wednesday, Sep 13, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:00 | GBP | GDP M/M Jul | -0.20% | 0.50% |

| 06:00 | GBP | Industrial Production M/M Jul | -0.50% | 1.80% |

| 06:00 | GBP | Industrial Production Y/Y Jul | 0.70% | |

| 06:00 | GBP | Manufacturing Production M/M Jul | -0.90% | 2.40% |

| 06:00 | GBP | Manufacturing Production Y/Y Jul | 3.10% | |

| 06:00 | GBP | Goods Trade Balance (GBP) Jul | -15.9B | -15.5B |

| 09:00 | EUR | Eurozone Industrial Production M/M Jul | -0.70% | 0.50% |

| 11:00 | GBP | NIESR GDP Estimate Aug | 0.30% | |

| 11:00 | USD | MBA Mortgage Applications (Sep 8) | -2.90% | |

| 12:30 | USD | CPI M/M Aug | 0.60% | 0.20% |

| 12:30 | USD | CPI Y/Y Aug | 3.60% | 3.20% |

| 12:30 | USD | CPI Core M/M Aug | 0.20% | 0.20% |

| 12:30 | USD | CPI Core Y/Y Aug | 4.70% | |

| 14:30 | USD | Crude Oil Inventories | -6.3M | |

| 23:50 | JPY | Machinery Orders M/M Jul | -0.70% | 2.70% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:00 | GBP | GDP M/M Jul | |

| Forecast: -0.20% | Previous: 0.50% | ||

| 06:00 | GBP | Industrial Production M/M Jul | |

| Forecast: -0.50% | Previous: 1.80% | ||

| 06:00 | GBP | Industrial Production Y/Y Jul | |

| Forecast: | Previous: 0.70% | ||

| 06:00 | GBP | Manufacturing Production M/M Jul | |

| Forecast: -0.90% | Previous: 2.40% | ||

| 06:00 | GBP | Manufacturing Production Y/Y Jul | |

| Forecast: | Previous: 3.10% | ||

| 06:00 | GBP | Goods Trade Balance (GBP) Jul | |

| Forecast: -15.9B | Previous: -15.5B | ||

| 09:00 | EUR | Eurozone Industrial Production M/M Jul | |

| Forecast: -0.70% | Previous: 0.50% | ||

| 11:00 | GBP | NIESR GDP Estimate Aug | |

| Forecast: | Previous: 0.30% | ||

| 11:00 | USD | MBA Mortgage Applications (Sep 8) | |

| Forecast: | Previous: -2.90% | ||

| 12:30 | USD | CPI M/M Aug | |

| Forecast: 0.60% | Previous: 0.20% | ||

| 12:30 | USD | CPI Y/Y Aug | |

| Forecast: 3.60% | Previous: 3.20% | ||

| 12:30 | USD | CPI Core M/M Aug | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 12:30 | USD | CPI Core Y/Y Aug | |

| Forecast: | Previous: 4.70% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -6.3M | ||

| 23:50 | JPY | Machinery Orders M/M Jul | |

| Forecast: -0.70% | Previous: 2.70% | ||

Thursday, Sep 14, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | AUD | Consumer Inflation Expectations Sep | 4.90% | |

| 01:30 | AUD | Employment Change Aug | 24.3K | -14.6K |

| 01:30 | AUD | Unemployment Rate s.a. Aug | 3.70% | 3.70% |

| 04:30 | JPY | Industrial Production M/M Jul F | -2.00% | -2.00% |

| 06:30 | CHF | Producer and Import Prices M/M Aug | 0.10% | -0.10% |

| 06:30 | CHF | Producer and Import Prices Y/Y Aug | -0.60% | |

| 12:15 | EUR | ECB Main Refinancing Rate | 4.25% | 4.25% |

| 12:30 | CAD | Wholesale Sales M/M Jul | -2.00% | -2.80% |

| 12:30 | USD | Retail Sales M/M Aug | 0.20% | 0.70% |

| 12:30 | USD | Retail Sales ex Autos M/M Aug | 0.40% | 1.00% |

| 12:30 | USD | PPI M/M Aug | 0.40% | 0.30% |

| 12:30 | USD | PPI Y/Y Aug | 0.80% | |

| 12:30 | USD | PPI Core M/M Aug | 0.20% | 0.30% |

| 12:30 | USD | PPI Core Y/Y Aug | 2.40% | |

| 12:30 | USD | Initial Jobless Claims (Sep 8) | 229K | 216K |

| 12:45 | EUR | ECB Press Conference | ||

| 14:00 | USD | Business Inventories Jul | 0.10% | 0.00% |

| 14:30 | USD | Natural Gas Storage | 33B | |

| 22:30 | NZD | Business NZ PMI Aug | 46.3 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | AUD | Consumer Inflation Expectations Sep | |

| Forecast: | Previous: 4.90% | ||

| 01:30 | AUD | Employment Change Aug | |

| Forecast: 24.3K | Previous: -14.6K | ||

| 01:30 | AUD | Unemployment Rate s.a. Aug | |

| Forecast: 3.70% | Previous: 3.70% | ||

| 04:30 | JPY | Industrial Production M/M Jul F | |

| Forecast: -2.00% | Previous: -2.00% | ||

| 06:30 | CHF | Producer and Import Prices M/M Aug | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 06:30 | CHF | Producer and Import Prices Y/Y Aug | |

| Forecast: | Previous: -0.60% | ||

| 12:15 | EUR | ECB Main Refinancing Rate | |

| Forecast: 4.25% | Previous: 4.25% | ||

| 12:30 | CAD | Wholesale Sales M/M Jul | |

| Forecast: -2.00% | Previous: -2.80% | ||

| 12:30 | USD | Retail Sales M/M Aug | |

| Forecast: 0.20% | Previous: 0.70% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Aug | |

| Forecast: 0.40% | Previous: 1.00% | ||

| 12:30 | USD | PPI M/M Aug | |

| Forecast: 0.40% | Previous: 0.30% | ||

| 12:30 | USD | PPI Y/Y Aug | |

| Forecast: | Previous: 0.80% | ||

| 12:30 | USD | PPI Core M/M Aug | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 12:30 | USD | PPI Core Y/Y Aug | |

| Forecast: | Previous: 2.40% | ||

| 12:30 | USD | Initial Jobless Claims (Sep 8) | |

| Forecast: 229K | Previous: 216K | ||

| 12:45 | EUR | ECB Press Conference | |

| Forecast: | Previous: | ||

| 14:00 | USD | Business Inventories Jul | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 33B | ||

| 22:30 | NZD | Business NZ PMI Aug | |

| Forecast: | Previous: 46.3 | ||

Friday, Sep 15, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 02:00 | CNY | Industrial Production Y/Y Aug | 4.00% | 3.70% |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Aug | 3.30% | 3.40% |

| 02:00 | CNY | Retail Sales Y/Y Aug | 3.00% | 2.50% |

| 04:30 | JPY | Tertiary Industry Index M/M Jul | 0.20% | -0.40% |

| 08:30 | GBP | Consumer Inflation Expectations | 3.50% | |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Jul | 13.5B | 12.5B |

| 12:30 | CAD | Manufacturing Sales M/M Jul | -1.70% | |

| 12:30 | USD | Empire State Manufacturing Sep | -10 | -19 |

| 12:30 | USD | Import Price Index M/M Aug | 0.40% | |

| 13:15 | USD | Industrial Production M/M Aug | 0.20% | 1.00% |

| 13:15 | USD | Capacity Utilization Aug | 79.30% | 79.30% |

| 14:00 | USD | Michigan Consumer Sentiment Index Sep P | 69.5 | 69.5 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 02:00 | CNY | Industrial Production Y/Y Aug | |

| Forecast: 4.00% | Previous: 3.70% | ||

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Aug | |

| Forecast: 3.30% | Previous: 3.40% | ||

| 02:00 | CNY | Retail Sales Y/Y Aug | |

| Forecast: 3.00% | Previous: 2.50% | ||

| 04:30 | JPY | Tertiary Industry Index M/M Jul | |

| Forecast: 0.20% | Previous: -0.40% | ||

| 08:30 | GBP | Consumer Inflation Expectations | |

| Forecast: | Previous: 3.50% | ||

| 09:00 | EUR | Eurozone Trade Balance (EUR) Jul | |

| Forecast: 13.5B | Previous: 12.5B | ||

| 12:30 | CAD | Manufacturing Sales M/M Jul | |

| Forecast: | Previous: -1.70% | ||

| 12:30 | USD | Empire State Manufacturing Sep | |

| Forecast: -10 | Previous: -19 | ||

| 12:30 | USD | Import Price Index M/M Aug | |

| Forecast: | Previous: 0.40% | ||

| 13:15 | USD | Industrial Production M/M Aug | |

| Forecast: 0.20% | Previous: 1.00% | ||

| 13:15 | USD | Capacity Utilization Aug | |

| Forecast: 79.30% | Previous: 79.30% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Sep P | |

| Forecast: 69.5 | Previous: 69.5 | ||

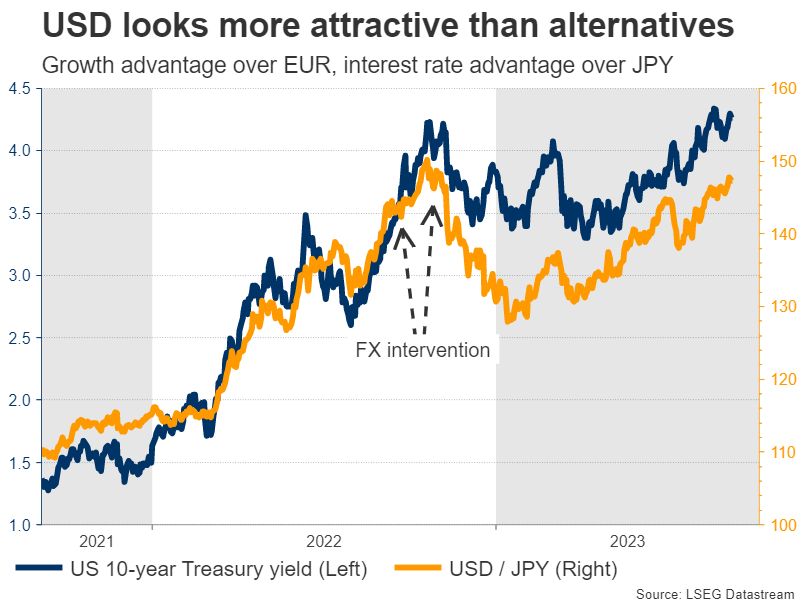

US Inflation Data Could Add Fuel to Dollar’s Resurgence

The US dollar has gone on a tear in recent weeks amid signs that the US economy remains resilient, in contrast to Europe and China that are rapidly losing steam. Whether this rally continues or suffers a setback will depend on the latest CPI report on Wednesday at 12:30 GMT. Overall though, the outlook for the dollar seems quite bright.

American strength

A range of incoming indicators continue to reaffirm the power of the US economy. The labor market is still in great shape and with inflation cooling off, real wage growth has returned to positive territory, which is a blessing for American consumers if it is sustained.

Meanwhile, the housing market has defied the negative pressure exerted by sky-high borrowing costs and has instead enjoyed an impressive recovery. Thanks to a national supply shortage, home prices as measured by the Case-Shiller price index almost hit new record highs in June, a trend that almost certainly persisted over the summer.

Add it all together and it seems US economic growth is reaccelerating. The economy grew by 2.1% year-over-year in the second quarter and the Atlanta Fed GDPNow model points to an annualized growth rate of 5.6% this quarter.

In contrast, both the Eurozone and China are slowing down at an alarming pace. Euro area GDP grew only 0.5% y/y in the second quarter, and business surveys suggest the situation will get worse moving forward, putting the risk of a mild recession on the radar. Likewise, China is dealing with the crises in its manufacturing and property sectors, which have sapped growth.

Inflation report

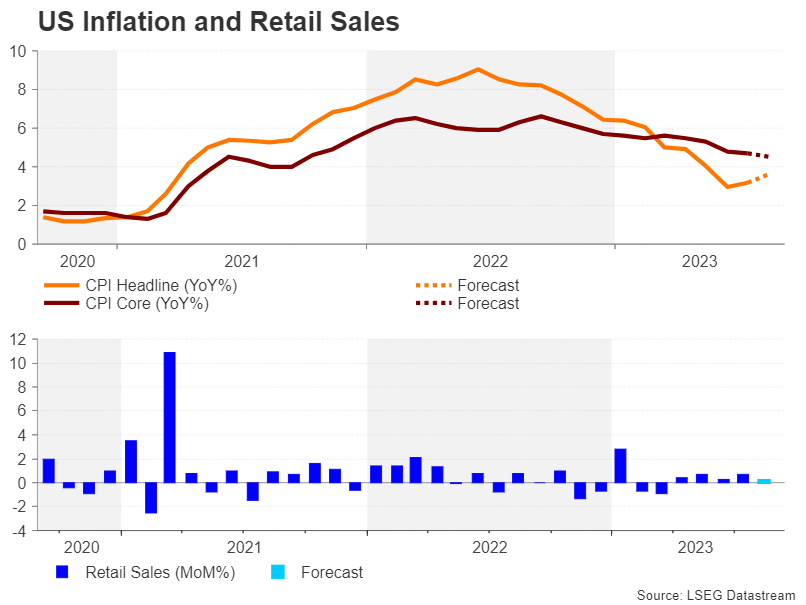

Turning to the upcoming releases, inflation as measured by the CPI rate is expected to have risen in August, partly because of the spike in energy prices. In monthly terms, the headline CPI rate is anticipated at 0.5%, which would push the yearly rate up to 3.5% from 3.2% in July.

However, the core rate that excludes energy and food items is projected to have risen only by 0.2% on the month. That would translate into a decline in the yearly rate, mostly because of base effects. Since a very hot print from August 2022 will now drop out of the 12-month CPI calculation and will be replaced by a colder print, that will mechanically push the yearly rate down.

Therefore, it's a mixed bag and the market reaction will boil down to any surprises in these numbers. In this sense, the risk of an upside CPI surprise seems greater, as the prices paid components of both the ISM surveys rose sharply during the month.

Arguing the same point is the Cleveland Fed's inflation nowcast model, which points to monthly prints of 0.79% and 0.38% for the headline and core CPI rates respectively, far above official forecasts. Admittedly, this is a narrow model, so it's difficult to put much weight on it. Still, it is one of the only real-time inflation trackers available.

Looking at the charts, an upside CPI surprise could push euro/dollar lower towards the crucial region of 1.0630, a violation of which would shift the technical outlook to negative. On the other hand, the most important area to watch in case of a CPI miss is 1.0760, which acted both as support and resistance this year.

Big picture

All told, the US economy and by extension the dollar seem much more attractive than any alternatives at this point. Europe and China are battling a severe slowdown, the Japanese yen has been devastated by rate differentials, and the British pound is trading like a proxy for equity markets, leaving it vulnerable to any shifts in risk appetite.

The US dollar stands in antithesis to all this. It offers a combination of solid economic growth, high interest rates, and safe haven qualities thanks to its reserve currency status, making it an 'all weather currency'.

If these elements remain in play while the global economy continues to struggle, that would leave plenty of scope for the dollar to extend its rally.

Week Ahead – ECB Rate Hike Hangs in the Balance; US CPI Could Edge Up Again

The European Central Bank is headed for a crunch rate decision next week amid rising recession risks and the job on inflation not yet done. It’s going to be a big week for the US dollar as well, as the CPI and retail sales reports are due before the Fed’s September meeting. There’s a barrage of UK data that will keep the pound on its toes before the next Bank of England decision, while the market mood will also be swayed by some key economic indicators out of China, as fears about the health of the world’s second largest economy persist.

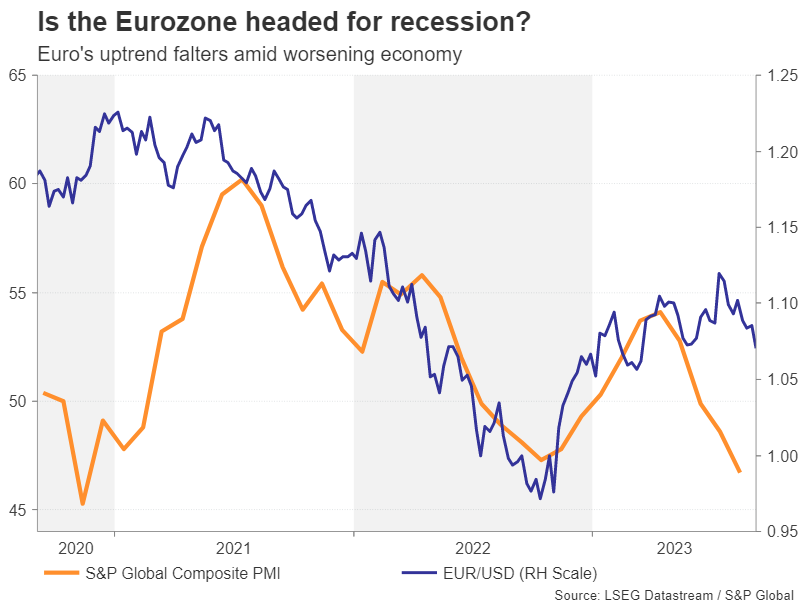

Recession fears come back to haunt the euro

After an impressive uptrend that stretched almost 10 months, the euro’s fortunes took a turn for the worst this summer. A massive rebound in the US dollar has been one of the thorns on the euro’s side. Another is the deteriorating outlook for the Eurozone economy. Following an aggressive tightening campaign that has taken everyone by surprise, borrowing costs in the euro area now stand at their highest since the single currency’s inception. Add to that the weakening demand in Europe’s key export markets, it’s no wonder that growth is faltering. Germany in particular has been hit hard by the sharp slowdown in China and the ZEW economic sentiment index out on Tuesday could underscore all the gloom.

Moreover, the bad news keeps getting worse. Second quarter GDP growth just got revised down to 0.1% from 0.3% q/q, reviving recession angst, while the latest PMI readings show the downturn deepened in August. There could be more negative news from July industrial production figures due on Wednesday.

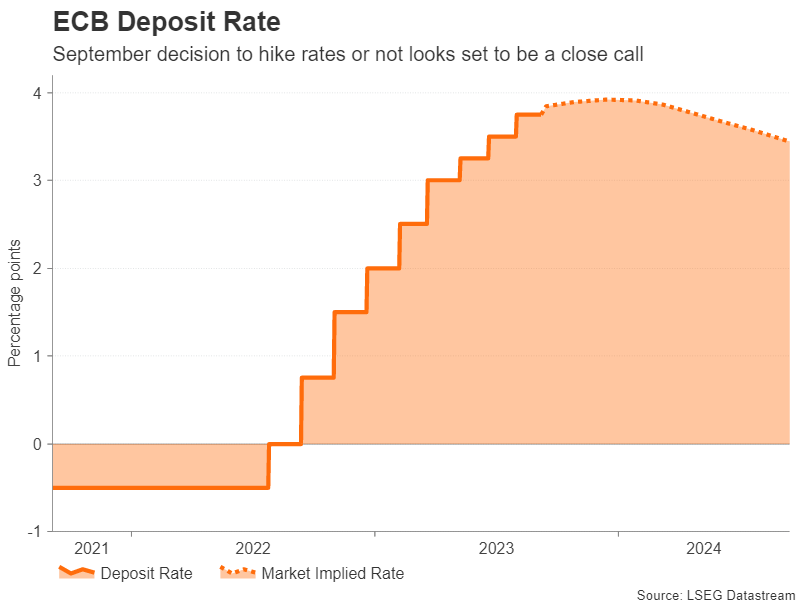

Will the ECB surprise with a 25-bps hike?

All this could give ECB policymakers enough cause for concern to pause interest rates for the first time since June 2022 when they meet on Thursday. The consensus among economists and in money markets is for the ECB to keep its deposit rate unchanged at 3.75%.

However, investors still see a sizeable probability of about 35% that the ECB will hike by 25 basis points in September. After all, core inflation that strips out food, energy, alcohol and tobacco has barely fallen this year, while CPI that excludes only food and energy remains fairly elevated at 6.2% y/y. Whilst there is very good reason to believe that inflation will moderate further over the coming months, the hawks among the Governing Council may push for one further hike for reassurance before agreeing to a pause.

If the ECB decides not to raise rates, a hawkish hold seems almost certain. Hence, there is scope for some limited upside correction in euro/dollar. However, no amount of hawkish rhetoric or even a positive spin on the economy by President Lagarde will be able to save the euro when there are stagflation clouds hanging over it.

US CPI & retail sales could reinforce higher for longer bets

The Fed doesn’t meet until September 19-20 – that’s almost two months since the July FOMC – and after an uneventful Jackson Hole, markets are badly in need for some fresh policy guidance. Before then however, investors will be treated to the August CPI and retail sales prints.

First up is CPI inflation on Wednesday. The consumer price index inched up in July for the first time in more than a year, rising by 3.2% year-on-year. Expectations are for a further uptick in August to 3.6%. Core CPI on the other hand could edge slightly lower from 4.7%. So unless there’s a beat in both of those figures or a shock large miss, the reaction in the bond and equity markets might be muted.

If the CPI report turns out broadly neutral, attention will swiftly turn to Thursday’s producer price index and retail sales numbers. The unexpectedly strong consumer spending in the third quarter is possibly the single biggest factor that could prompt the Fed to press the hike button in September or November. The retail sales readings will therefore be watched carefully.

Following a 0.7% m/m rise in July, retail sales are forecast to have grown at a more moderate pace of 0.2% in August.

Other releases will include the Empire State manufacturing index, industrial output and the University of Michigan’s preliminary consumer sentiment survey, all on Friday.

The odds for a 25-bps rate increase by November were boosted after the upbeat ISM services PMI and they could firm further if the upcoming week’s data is overall solid. The dollar is already trading at six-month highs so if the US economy continues to shine the brightest among its peers, there could be more gains in store.

Will UK jobs and GDP data come to the pound’s aid?

Out of all the major central banks, the Bank of England is widely seen as having the furthest to go in interest rate hikes. That’s been the key driver for sterling this year when, until recently, it topped the FX league for best performers before being toppled by the Swiss franc. The reason why the pound lost its crown is because the ‘further to go’ distance has suddenly shrunk and the BoE may only raise rates a couple more times.

This repricing quickened after Governor Andrew Bailey hinted that policymakers are “much nearer” the end of the tightening cycles. A deepening slump in the UK housing market might explain why Bailey is becoming more jittery about overtightening.

Nevertheless, the British economy has proven to be somewhat more resilient than the Eurozone’s and next week’s data could further support this view. Employment numbers for July are due on Tuesday, which will include a vital update on wage growth. UK pay growth accelerated to an astoundingly high 8.2% y/y in the three months to June. At the very least, high wage growth looks set to prevent the Bank from cutting rates anytime soon even if it decides to go on pause early.

On Wednesday, the focus will be on the July GDP estimate, with industrial production and trade figures also on cue.

Sterling could recoup some of its recent losses should the incoming data ease concerns about stagflation or a recession.

Aussie weighed by Chinese and domestic woes

Down under, another battered currency will be looking for a data boost. The Australian dollar has had a rough ride lately amid a stalling economic recovery in China and the Reserve Bank of Australia not committing to any further rate hikes.

Domestic employment numbers will be important for the aussie on Tuesday after stronger-than-expected GDP growth in the second quarter cast doubt on the RBA’s overcaution on the economy. Any rebound in jobs growth in August could thus provide the aussie a bit of a lift.

However, traders might pay more attention to China’s monthly releases on industrial output, retail sales and investment due on Friday. Although growth momentum is expected to have remained sluggish in August by China’s standards, the forecasts point to some improvement. Should that turn out to be the case, risk sentiment is likely to be buoyed, helping the aussie to bounce back from 10-month lows.

Weekly Focus – All Eyes on the ECB Next Week

This week, we published our latest economic forecasts for both Nordic and global economies in Nordic Outlook - Divergent fortunes, 5 September. The outlook for the euro area remains weak, and we think the economy is headed for a slight contraction towards the end of the year. In the US, we have lifted our growth forecast for this year (1.9%) due to more upbeat investment outlook, but still look for clearly below-trend growth towards 2024 on weakening consumption (+0.6%). And while Chinese authorities have recently rolled out increasing number of stimulus measures, we expect growth to remain below the official target at 4.8% in 2023 and 4.2% in 2024.

The divergent outlook was reflected in this week's mixed data releases as well. Euro area Sentix index signalled further weakening in investor confidence in early September, while China's Caixin Services PMI confirmed the slowdown in the official NBS measure released earlier. In contrast, US ISM Services index defied weaker signals from PMIs, and rose sharply against expectations (54.5; from 52.7). Notably, the uptick was broad-based across subcomponents, including new orders, employment and prices paid.

The strong reading lifted UST yields, which were further boosted by initial jobless claims falling to the lowest levels since February. The fear of rates staying higher for longer weighed on equity sentiment and EUR/USD. We discussed the recent US labour market data and implications for the Fed in US Labour Market Monitor, 7 September.

Next week, the focus turns to the ECB meeting, where we anticipate a final 25bp hike. Markets remain divided between a hike and a pause, with the implied probability of the former hovering around 35-40%. This week, the Q2 compensation of employees, which is ECB's key measure for wage growth, continued to grow at a pace of 5.6% y/y, close to Q1 rate of 5.4%. The figure was slightly higher than ECB estimated for 2023 back in June (5.3%). This could provide support to the still elevated underlying core inflation, which we expect to fall below 3% only in H2 2024. Read our more detailed ECB Preview, 6 September and further details on data from Euro Area Macro Monitor, 7 September.

In the US, next week brings the final key data release ahead of the September FOMC meeting, including the August CPI. While the recent uptick in oil prices will likely lift the headline measure by 0.5% m/m, cooling wage pressures should translate into further easing in core services inflation, and we forecast another low core CPI print at 0.2% m/m. While both us and the markets remain convinced that the Fed will go on a pause in September, market pricing implies that the November meeting is essentially a coin-flip between a hike and a pause. The next meeting will provide some interest cues in the form of updated rate projections however, and a low CPI print could tilt some of the FOMC participants to revert their June call for one more hike later in the year.

Other data releases include US retail sales, where early card transaction data is pointing towards slowing real spending growth, especially when considering the higher gasoline prices. The Fed will keep an eye out for the preliminary University of Michigan survey as well, and if the declining trend on inflation expectations continued into September.

Week Ahead – US Inflation Key, ECB Ponders Rate Pause, UK Labor Market Data

US

This week is all about the US CPI report and retail sales data. If the US demand for goods didn’t weaken that much and if inflation heated up, rate hike expectations for the November meeting might become the consensus. The inflation report might not be as clear as headline inflation will obviously rise given the surge in gasoline prices, but core might deliver another subdued reading. Moderation with consumer spending will be the theme as Americans deal with higher energy prices, rising debt levels, and as confidence softens.

Investors will also pay close attention to the University of Michigan’s inflation expectations on Friday. The 1-year outlook for prices may drop from the 3.5% August reading. Fed speak will be nonexistent as the blackout period begins for the September 20th policy meeting.

Eurozone

The European Central Bank meets next week and it’s not clear at this stage what decision they will come to. Refinitiv is pricing in around a 65% chance of a hold, which may signal the end of the tightening cycle – not that the ECB would in any way suggest that at this stage – but expectations do differ. There’s every chance the committee will push through one more, at which point the data is expected to improve regardless making a Fed-style exit all the more difficult. Ultimately, it will likely come down to the projections which will be released alongside the decision. ZEW surveys aside, on Tuesday, the rest of the week is made up of tier-three data.

UK

Potentially a big week for the UK ahead of the next monetary policy meeting on 21 September. Andrew Bailey and his colleagues this past week hinted that the decision is in the balance and not the foregone conclusion many expect. Markets are pricing in a more than 70% chance of a hike and more than 50% of another after that by February. If what they said is true, then the labor market report on Tuesday could be hugely significant as further slack could give those on the fence the reassurances they need that past measures, among other things, are working and more may not be needed. Huw Pill also speaks on Monday while Catherine Mann will make an appearance in Canada on Tuesday. GDP on Wednesday could also be interesting, with the rest of the week made up of less influential releases.

Russia

The CBR is expected to leave the key rate unchanged at 12% on Friday. It hiked very aggressively at the last meeting – from 8.5% – so there is scope for another surprise, with inflation having risen again last month to 5.1%. The rouble has also been in steady decline after rebounding following the last announcement, to trade not far from its recent lows against the dollar.

South Africa

A relatively quiet week ahead, with manufacturing figures due on Monday and retail sales on Wednesday.

Turkey

The CBRT is desperately trying to get inflation under control again with successive large interest rate hikes. In response the currency has stopped making new lows but it has drifted lower again over the last couple of weeks since the surprisingly large last hike. It’s sitting not far from the pre-meeting lows now and inflation data this past week won’t have helped, rising to 58.94% annually. More rate hikes are likely on the way. Next week the focus is on unemployment and industrial production figures on Monday.

Switzerland

A very quiet week to come, with PPI inflation the only economic release. We’ve been seeing some deflation in recent months in the PPI data which will be giving the SNB some comfort that price pressures are back under control. Another rate hike is no longer viewed as guaranteed, with markets slightly favoring a hold over the coming meetings but it is tight.

China

The much sought-after consumer and producers’ price inflation data for August will be released this Saturday where market participants will have a better gauge of the current deflationary conditions in China.

After a slight improvement in the two sub-components of August’s NBS Manufacturing PM where new orders and production rose to their highest level since March at 50.2 and 51.9 respectively coupled with an improvement in export growth for August that shrunk to a lesser magnitude of -8.8% y/y from -14.5% y/y in July, there are some signs of optimism that the recent eight months of deflationary pressures may have started to abate.

The August CPI is expected to inch back up to 0.2% y/y from -0.3% y/y in July and the PPI is forecast to shrink at a lesser magnitude of -3% y/y in August versus -4.4% in July. If the PPI turns out as expected, it will be the second consecutive month of improvement from a persistent loop of deflationary pressure in factory gate prices since November 2022.

Other key data to focus on will be new yuan loans and M2 money supply for August which will be released on Monday. It will provide a sense of whether China’s economy is slipping into a liquidity trap despite the current targeted monetary and fiscal stimulus measures enacted by policymakers.

Lastly, the housing price index, industrial production, retail sales, and the unemployment rate for August will be released on Friday with both retail sales and industrial production expected to show slight improvement; 2.8% y/y for retail sales over 2.5% y/y recorded in July, 4% y/y for industrial production versus 3.7% in July.

Market participants will be keeping a close eye on youth unemployment for August after July’s figure was temporarily suspended by the National Bureau of Statistics without any clear timeline for the suspension. The youth joblessness data in China is of key concern after the youth unemployment rate skyrocketed to a record high of 21.3% in June, around four times more than the national unemployment rate of 5.3%.

Lastly, China’s central bank, the PBoC, will announce its decision on a key benchmark interest rate, the 1-year medium-term lending facility rate on Friday and the expectation is no change at 2.50% after a prior cut of 15 basis points.

India

Inflation and balance of trade for August will be the focus for the coming week. Inflation data is released on Tuesday and is expected to dip slightly to 7% y/y from 7.44% in July, the highest since April 2022.

Balance of trade will be released on Friday and the expectation is for the deficit to widen slightly to -$21 billion from -$20.67 billion in July.

Australia

On Monday, the Westpac consumer confidence change for September is expected to improve to 0.6% m/m from a reading of -0.4% m/m in August, following three consecutive interest rate pauses from RBA.

The key employment change data for August will be released on Thursday with 24,300 jobs expected to be created, an improvement on the 14,600 reduction in July. Meanwhile, the unemployment rate is expected to slip to 3.6% from 3.7% in July.

New Zealand

Electronic retail card spending for August is due on Tuesday and is forecast to dip to 1.4% y/y from 2.2% in July. That would represent a declining trend in growth in the past five months.

Next up, food inflation for August will be released on Wednesday; its growth rate is expected to slow to 7.8% y/y from 9.6% in July. That would be the slowest growth in food inflation since June 2022.

Japan

A couple of key data points to note for the coming week. Firstly, the Reuters Tankan Index on manufacturers’ sentiment on Wednesday; after a big jump to +12 in August – its highest level recorded so far this year – sentiment is expected to taper off slightly to +10 for September.

Producers’ price index for August will be released on Wednesday and a slight dip is expected to 3.2% y/y from 3.6% in July.

Lastly, on Thursday, we will have data on machinery orders from July with the consensus expecting a further decline of 10.7% y/y from -5.8% in June.

Singapore

One key data to focus on is the balance of trade for August which will be out on Friday. The trade surplus is being expected to increase slightly to $7 billion from $6.49 billion in July. That would be the fourth consecutive month of expansion in the trade surplus.

Economic Calendar

Saturday, Sept. 9

Economic Data/Events

- China CPI, PPI

- G-20 summit in New Delhi: President Biden, UK PM Sunak and Saudi Crown Prince Mohammed bin Salman plan to attend

Sunday, Sept. 10

Economic Events

- Russia’s Eastern Economic Forum: North Korean leader Kim Jong Un to meet with Russian President Putin

- Russia holds regional elections, including in four occupied regions of Ukraine

Monday, Sept. 11

Economic Data/Events

- China aggregate financing

- Italy industrial production

- Japan M2 money stock

- Mexico industrial production

- South Africa manufacturing production

- Turkey current account, industrial production

- The EU releases an updated economic forecast

- BOE’s Mann speaks at Canadian Association for Business economics conference

- US Deputy Treasury Secretary Adeyemo addresses The Economic Club of New York

- Creditors of China’s Country Garden finish voting on requests to extend more bonds

- Thailand PM Thavisin to unveil economic measures at joint session of parliament

Tuesday, Sept. 12

Economic Data/Events

- Australia consumer confidence

- Germany ZEW survey

- India industrial production, CPI

- Mexico international reserves

- Spain CPI

- UK jobless claims, unemployment

- Apple unveils iPhone 15 line and next-generation smartwatches at “Wonderlust”

- New Zealand’s Treasury releases pre-election economic and fiscal update

Wednesday, Sept. 13

Economic Data/Events

- US August CPI M/M: 0.5%e v 0.2% prior; Y/Y: 3.6%e v 3.2% prior

- Eurozone industrial production

- India trade

- Japan PPI

- New Zealand food prices

- UK industrial production

- European Commission President von der Leyen delivers State of the EU speech at the European Parliament in Strasbourg.

- Tech leaders including Tesla’s Elon Musk and Meta Platforms’ Mark Zuckerberg attend a forum on the future of AI convened by Senator Chuck Schumer

Thursday, Sept. 14

Economic Data/Events

- US retail sales, PPI, business inventories, initial jobless claims

- Australia unemployment

- Eurozone ECB rate decision: Expected to deliver one last rate hike, bringing main refinancing rate to 4.50% and the deposit rate to 4.00%

- India wholesale prices

- Japan machinery orders, industrial production

- United Auto Workers union contract talks reach a pivotal moment that could shut down a major section of the US economy

- German Foreign Minister Baerbock to meet with US Secretary of State Blinken in DC

- Italian PM Meloni to attend Budapest Demographic Summit

Friday, Sept. 15

Economic Data/Events

- US industrial production, University of Michigan consumer sentiment, Empire manufacturing index

- Canada existing home sales

- China property prices, retail sales, industrial production

- France CPI

- Italy trade, CPI

- Japan tertiary index

- New Zealand PMI

- Poland CPI

- Russia rate decision

- Chinese financial institutions set to reduce foreign exchange deposits held in reserve

- Informal meeting of EU finance ministers in Spain

Sovereign Rating Updates

- Germany (Fitch)

- Belgium (S&P)

- Saudi Arabia (S&P)

- Spain (S&P)

- Greece (Moody’s)

- Netherlands (DBRS)

Crypto Sellers Losing Patience

Market Picture

It looks like sellers in cryptocurrencies are losing patience. The crypto market remains tightly pinned at $1.04 trillion in capitalisation. An attempt to break away and cross the $1.05 trillion mark has been met with heavy selling, and it’s well below the $1.1 trillion pivot late last month.

Similarly, Bitcoin is finding it increasingly difficult to keep its balance as it rises above $26.0K. The last such attempt on Friday morning was quickly thwarted, and BTCUSD is again trading near $25.8K.

Bitcoin’s technical picture on daily timeframes remains bearish, as the 50-day is approaching 200-day MA from above. The crossing (probably next week) can potentially trigger an impulsive sell-off, which is very dangerous in such a thin market.

Ethereum is trading near its 50- and 200-week averages and near its lows from March. This is a bearish disposition, especially given the strengthening dollar and pressure on US stock indices in the background.

News background

The Financial Stability Board and the International Monetary Fund recommended regulating digital assets. The initiative aims to bring together standards and different positions to mitigate cryptocurrency risks.

The Chicago Board Options Exchange (CBOE) filed applications with the US Securities and Exchange Commission (SEC) on behalf of Ark Invest and VanEck to launch spot ETFs on Ethereum.

Google has allowed advertising of blockchain-based games using NFT from 15 September if they are unrelated to gambling.

Meanwhile, Arkham Intelligence platform identified Grayscale Foundation wallets that hold more than $16bn worth of bitcoins.