Sample Category Title

USD/CAD: A Hot Canadian Employment/Wage Report Sends the Loonie Higher

- BOC rate hike odds for the October 25th meeting rise from yesterday’s 23.9% to 28.8%

- Hours worked climbed to the highest level since February

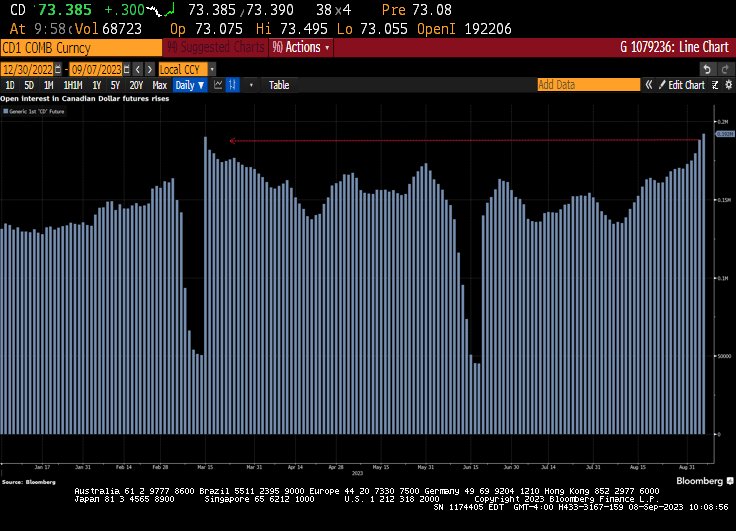

- CAD futures open interest rise to best levels since mid-March

Canada’s economy isn’t quite ready to cool. The latest Canadian employment report showed hiring bounced back in August, doubling expectations. The near 40,000 added jobs exceeded the 17,500 consensus estimate and proved that the prior month’s unexpected shedding of jobs was not the beginning of a new trend. The BOC will pay close attention to the wage growth acceleration of 5.2%, which was expected to soften to 4.7%. There is a lot of data before the October 25th BOC meeting, but it still seems like they’ve reached the terminal rate for this tightening cycle.

Open Interest in Canadian dollar futures

The Canadian dollar is the top performing G10 currency and that could continue given how the futures market is positioned. The last time open interest for Canadian dollar futures were at these levels was the middle of March, which was when USD/CAD started its decline from around the 1.37 level to the 1.3300 area.

Canadian Employment Highlights

Canada’s strong jobs report showed full-time employment rebounded from 1,700 to 32,200, while part-time work created 7,800 jobs, much better-than-the prior month’s decline of 8,100 positions. The unemployment rate held steady at 5.5%, which was better than the expected increase of 5.6%. The majority of the job gains stemmed from the professional and technical services, and construction. The regions that benefited the most were Alberta, British Columbia and Prince Edward Island. Nova Scotia was the only region that lost jobs. While the job gains are a positive sign, when you figure in population growth, this pace won’t cut it for keeping the unemployment rate steady. About 50,000 jobs per month would be needed to support a steady unemployment rate.

USD/CAD 60-minute chart

After breaking down below the 1.3650 level, bearish momentum is slowing down ahead of the 1.3600 level. If the start of next week does not include a risk averse start, the Canadian dollar could have a strong move here. Unless the uptrend line (which started in July) is broken substantially to the downside, the prevailing bullish trend may remain in place.

Sunset Market Commentary

Markets

Today’s empty eco calendar left plenty of room to further digest the PBOC’s regime shift in CNY fixings. They turn more tolerant to a weaker currency given the cyclical and structural headwinds the economy is facing. USD/CNY trades at the highest level since end 2007 (7.34). USD/JPY (147.40) is not impressed by Finance Minister Suzuki’s verbal intervention warning. USD/JPY 150, the previous line in the sand for strong action, comes closer step by step. Yesterday evening’s Wall Street risk off spilt to Asia and initially to Europe as well despite a decent start. The EuroStoxx 50 intensively tested the key 4200 support area which is the downside of the sideways trading band in place since May. A break didn’t occur with technical rebound action starting mid-way European dealings. Core bonds made a similar intraday U-turn though it started way faster. The new increase in the oil price ($89.5/b to $90.5/b) comes a good way in helping to explain the move. Changes on the German and the US yield curve are confined to +- 1 bp. The EUR/USD decline takes a breather, but at 1.07 no more than that. The dollar holds the upper hand in the current market environment. EUR/GBP is going nowhere neither at 0.8575. A report on jobs by KPMG and REC was overlooked. It signaled reduced activity across the UK during August with permanent placements falling at a rapid pace which was the sharpest in over three years while temp billings slipped into decline for the first time since July 2020. Nevertheless, competition for specific skills and the strong inflationary environment drove further increases in starting pay. The report adds to the picture scheduled by official data with the unemployment rate gradually picking increasing while wage growth accelerates. The Bank of England will likely take it as a sign to proceed slowly from here with markets expecting a final (or second-to-last) 25 bps rate hike.

News & Views

The Food Price Index of the Food and Agriculture Organization of the United Nations was down 2.1% in August from July, reversing the rebound registered last month and is currently 24% below its peak reached in March 2022. The drop reflected declines in the price indices for dairy products, vegetable oils, meat and cereals, while the sugar price index increased moderately. The Cereal Price Index declined 0.7% M/M to be down 14.1% Y/Y. Wheat prices fell 3.8%. Maize prices fell for the seventh consecutive month, hitting their lowest value since September 2020. By contrast, the Rice Price Index in August rose by 9.8% M/M to reach a 15-year nominal high, reflecting trade disruptions registered in the aftermath of India's July ban on rice exports. Vegetable oil prices declined 3.1% in August. The FAO Dairy Price Index (-4.0% M/M) registered the eighth consecutive monthly decline, to be 22.4% below its corresponding value last year. Meat prices also declined 4% M/M. The FAO Sugar Price Index rose 1.3% from July to be 34% higher compared to August last year. The increase in world sugar prices was mainly due to heightened concerns over the impact of the El Niño weather phenomenon on global production prospects. In India, below-average rains in August were detrimental to sugarcane crop development, while dry weather conditions in Thailand are expected to negatively affect the 2023/24 production. In Brazil, rains hampered field operations in some areas; however, the large crop currently being harvested limited the upward pressure on world sugar prices. The weakening of the Brazilian Real against the USD and lower ethanol prices also contributed to curbing the rise in world sugar prices. Still recent futures prices suggest upside price pressures might continue.

Canadian employment in August still rose at a solid/faster than expected pace. The economy added 39.9k jobs, double expectations, mainly driven by a rise in full time employment (32.2k). The unemployment rate remained unchanged at 5.5% (5.6% expected). Hourly wages for permanent employment unexpectedly accelerated from 5% to 5.2% while an easing to 4.7% was expected. At the same, the labour force continues to expand at a faster pace than employment. This reduces the employment rate from 62% to 61.9% and might slightly/gradually ease the tightness in the labour market. The Bank of Canada this week left its policy rate unchanged at 5% but showed ongoing concerns on persistent underlying inflation. Today’s wage data at least won’t help to ease this concern. The 2-yr CAD government bond yield rose 4 bps after the release. After touching the weakest level against the dollar since March yesterday; the loonie after the data strengthens from 1.3675 to test the 1.361 area.

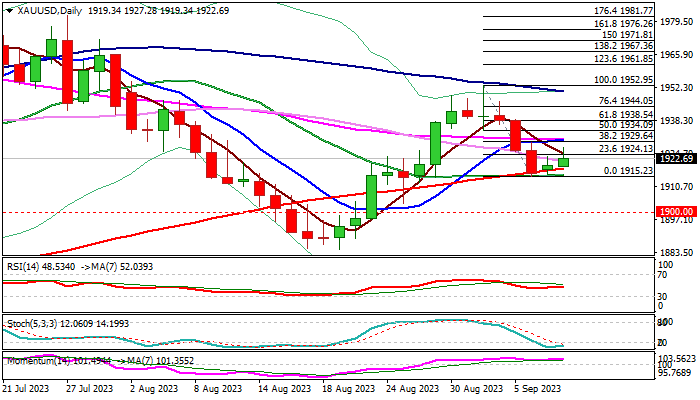

XAU/USD : Gold Price Regained Traction on Dovish Signals from Fed

Gold price rose further on Friday, extending recovery from $1915, where the higher base is forming after three-day fall found firm ground, after being contained by 200DMA.

Weaker dollar on end-of-week profit taking contributed to fresh strength, as the metal benefited from rather neutral stance of Fed policymakers.

Fed officials referred to cooling inflation and quite good shape of the economy, while the latest data showed that labor demand is coming down and unemployment is rising, suggesting that the central bank will likely stay on hold in September’s policy meeting.

Technical picture on daily chart remains bullishly aligned as positive momentum is strong, RSI heading north and stochastic is about to emerge from oversold territory, though MA’s are in mixed setup.

Fresh strength cracked initial resistance at $1924 (Fibo 23.6% of $1952/$1915) but needs more work at the upside and sustained break above $1930 zone Fibo 38.2% / converged 10/55DMA’s) to generate reversal signal and open way for stronger advance.

Near-term bias is expected to remain with bulls while the price action stays above 200DMA, while next week’s daily cloud twist is also expected to be magnetic.

Res: 1930; 1938; 1940; 1948.

Sup: 1918; 1915; 1902; 1892.

Euro Edges Higher, German CPI Unchanged

- German inflation dips to 6.1%

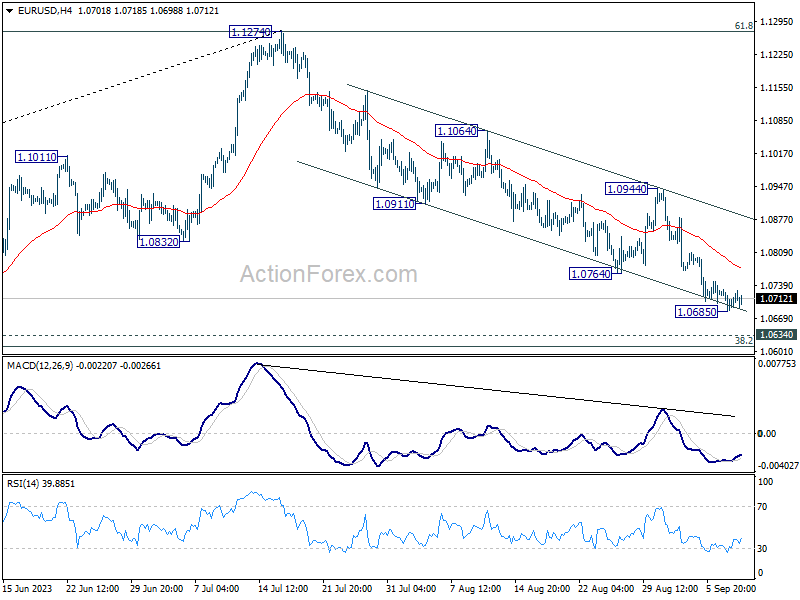

The data calendar is light on Friday and EUR/USD is trading at 1.0707 in Europe, up 0.09%. There are no tier-1 events out of the eurozone or the US, which means we can expect subdued movement from the euro for the remainder of the day.

The euro is poised to record a losing week for an eighth straight time. The euro has plunged about 500 points during that time, as the US dollar thrives over concerns that the Fed may have to keep hiking in response to the resilient labour market. The currency continues to struggle at 3-month lows and there aren’t any encouraging signs that the downturn is about to change.

The economic outlook in the eurozone remains weak. Recent eurozone numbers have been soft and Germany hasn’t resembled the locomotive which could always be trusted to lift the eurozone economy. German PMIs pointed to contraction in the services and manufacturing sectors in August, and today’s inflation report was a reminder that the largest economy in Europe is grappling with high inflation and weak growth.

German CPI remained unchanged in August for a third straight month. On a yearly basis, CPI was confirmed at 6.1% y/y, down a notch from 6.2%, while core CPI remained unchanged at 5.5% y/y. Food and energy prices rose but there was a bit of good news as services inflation ticked lower to 5.1%, down from 5.2% in July.

The ECB meets next week and it remains unclear what Lagarde & Co. will decide. Inflation, which is at 5.3%, remains much higher than the ECB target of 2%. The ECB wants to lower inflation but further rate increases could tip the weak economy into a recession. The markets have priced in a pause at the September meeting at around 70%, which means that a rate hike still remains on the table despite weak economic conditions..

EUR/USD Technical

- EUR/USD is testing resistance at 1.0716. Above, there is resistance at 1.0831

- There is support at 1.0658 and 1.0593

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0677; (P) 1.0705; (R1) 1.0723; More...

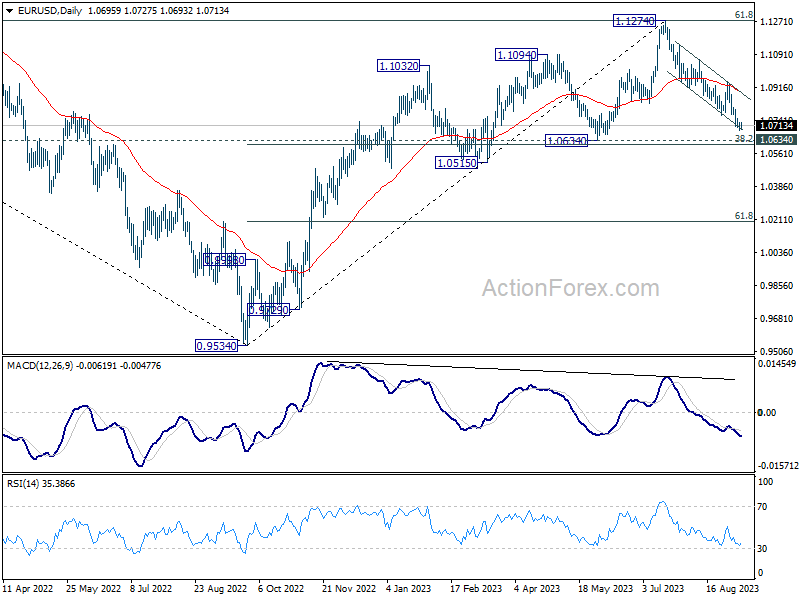

Intraday bias in EUR/USD stays neutral for consolidation above 1.0685 temporary low. Stronger recovery cannot be ruled out, but outlook will stay bearish as long as 1.0944 resistance holds. Below 1.0685 will resume the fall from 1.1274 to 1.0609/34 cluster support.

In the bigger picture, fall from 1.1274 medium term top is seen as a correction to up trend from 0.9534 (2022 low). Deeper decline would be seen to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to bring rebound. Yet, medium term outlook will be neutral for now, as long as 1.1274 resistance holds. However, sustained break of 1.0609/34 will raise the chance of bearish trend reversal, and target 61.8% retracement at 1.0199.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2441; (P) 1.2476; (R1) 1.2506; More...

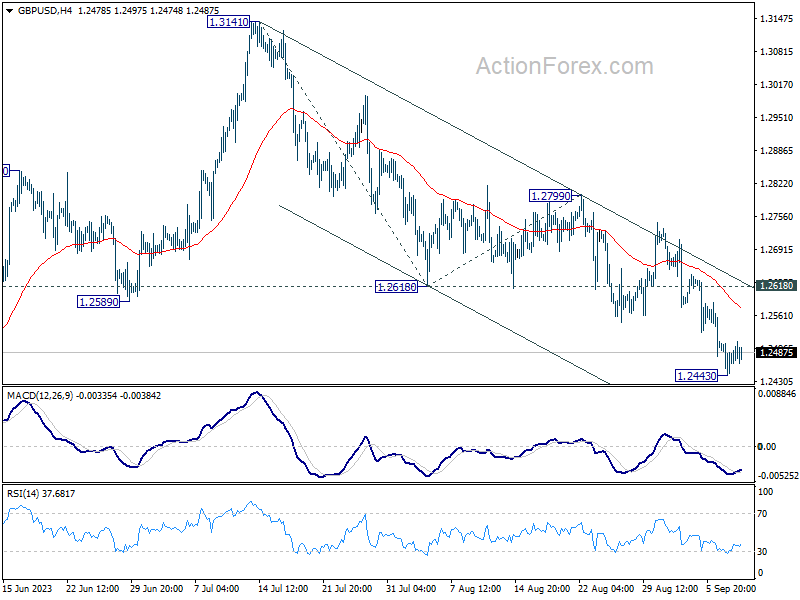

No change in GBP/USD's outlook as consolidation continues above 1.2443 temporary low. Stronger recovery cannot be ruled out. But upside should be limited by 1.2618 support turned resistance. Below 1.2443 will resume the fall from 1.3141 to 100% projection of 1.3141 to 1.2618 from 1.2799 at 1.2276.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. But outlook will be neutral at best as long as 1.3141 resistance holds, and consolidation from there is set to extend, until further development.

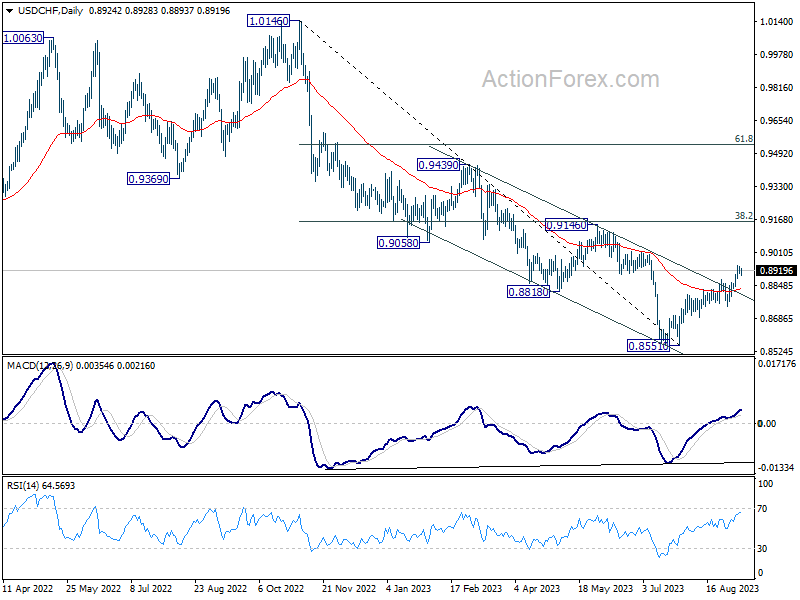

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8911; (P) 0.8926; (R1) 0.8942; More....

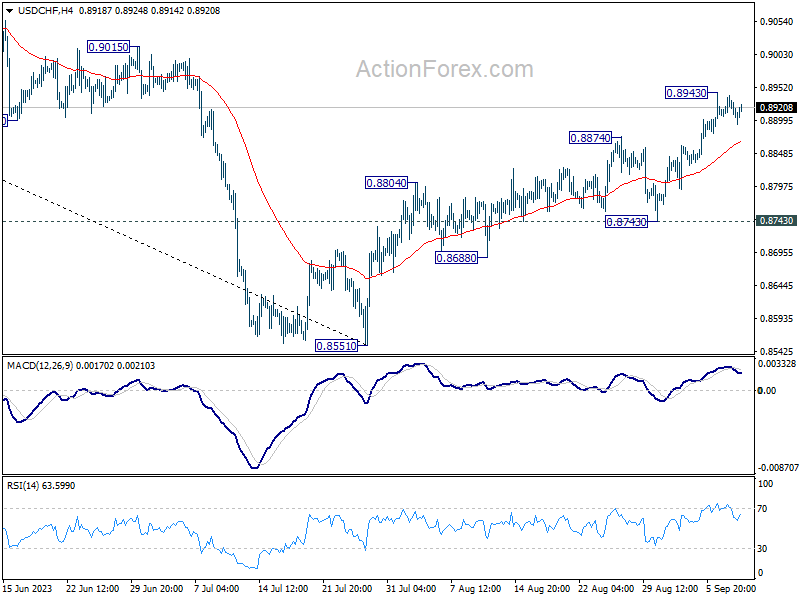

No change in USD/CHF's outlook as consolidations continue below 0.8943 temporary top. Another retreat cannot be ruled out. But further rally is expected as long as 0.8743 support holds. On the upside, above 0.8943 will resume the rally from 0.8551 to 0.9146 cluster resistance next.

In the bigger picture, rebound from 0.8551 medium term bottom is currently seen as a correction to the downtrend from 1.0146 (2022 high). Further rally would be seen to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160). Strong resistance could be seen there to limit upside, at least on first attempt.

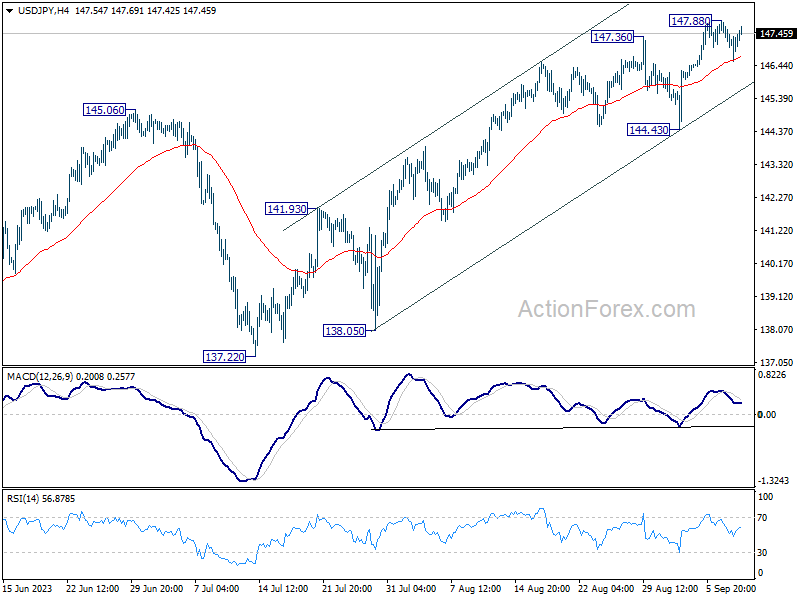

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.93; (P) 147.40; (R1) 147.76; More...

No change in USD/JPY's outlook as consolidation continues below 147.88. Intraday bias remains neutral first. While deeper retreat could be seen, outlook will stay bullish as long as 144.43 support holds. On the upside, above 147.88 will resume larger rally from 127.20, to retest 151.93 high.

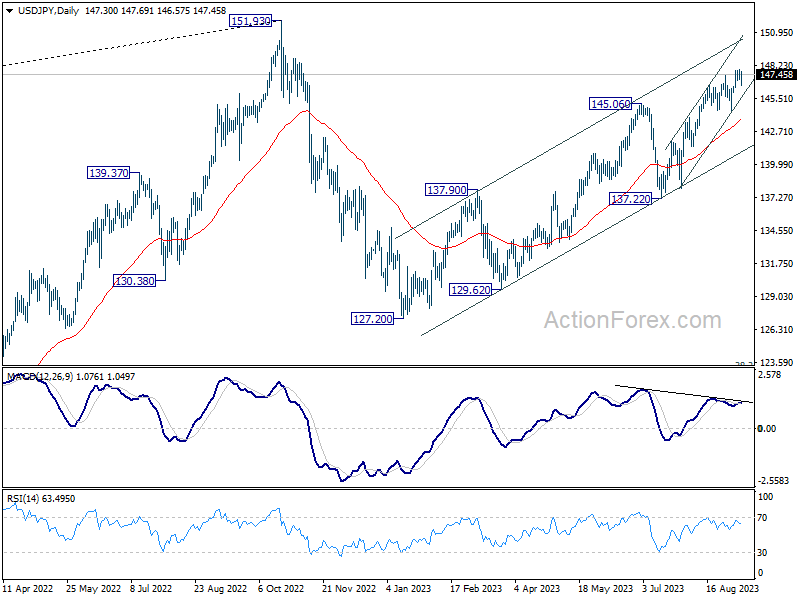

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

Canada’s Labour Market Bounces Back in August

The Canadian labour market added 39.9k positions in August, with full-time employment up 32.2k and part-time employment up 7.8k.

The unemployment rate was unchanged at 5.5% and the participation rate dropped 0.1 percentage point to 65.5%.

Employment by sector exhibited the rubber band effect, with gains in professional, scientific and technical services (+52k) and construction (+34k) offsetting losses in prior months. Same for educational services (-44k), which had strong gains prior.

Lastly, total hours worked were up 0.5% month-on-month and wages were up 4.9% year-on-year (vs 5.0% in July).

Key Implications

The job market is keeping everyone guessing. While the positive job gain provided an offset to weakness in prior months, the population boom (+103k!) is causing labour force growth (+54k) to outpace hiring. The number of unemployed workers has now grown by 137.6k over 2023. As we highlighted in our recent job market outlook, there are many ways the once high-flying labour market can come back down to earth. So far, it has been a smooth transition. But this will be no easy task, and we expect turbulence in the months ahead.

Bank of Canada Governor Tiff Macklem spoke yesterday about the clear evidence that past interest rate hikes are working to slow the economy. While the evidence became a little less clear today, when we look under the surface, the story still holds. Consumer spending is slowing under the weight of 475bps in rate hikes over the last 18 months, and the real estate market is rolling over again after the BoC's June/July rate hikes. Given that markets are pricing a 50/50 chance of another BoC hike this year, it is clear that market participants are still looking for more evidence of an economic slowdown.

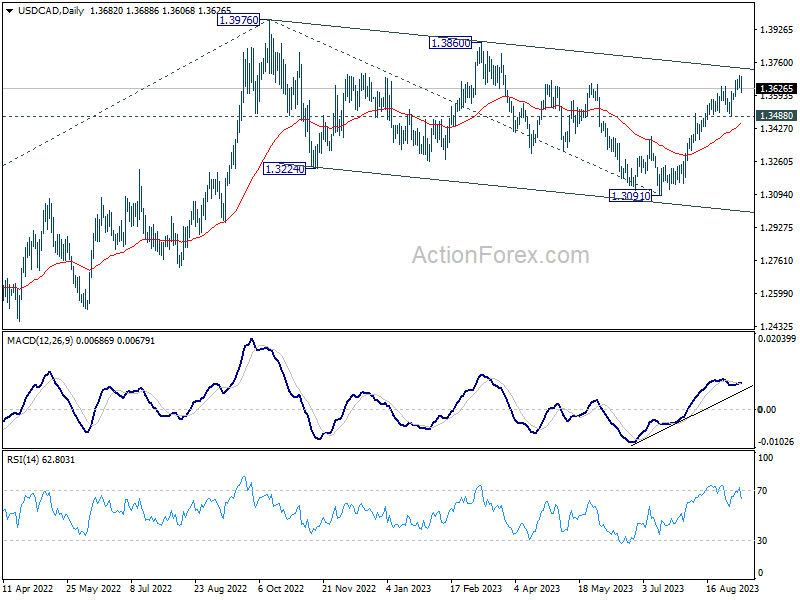

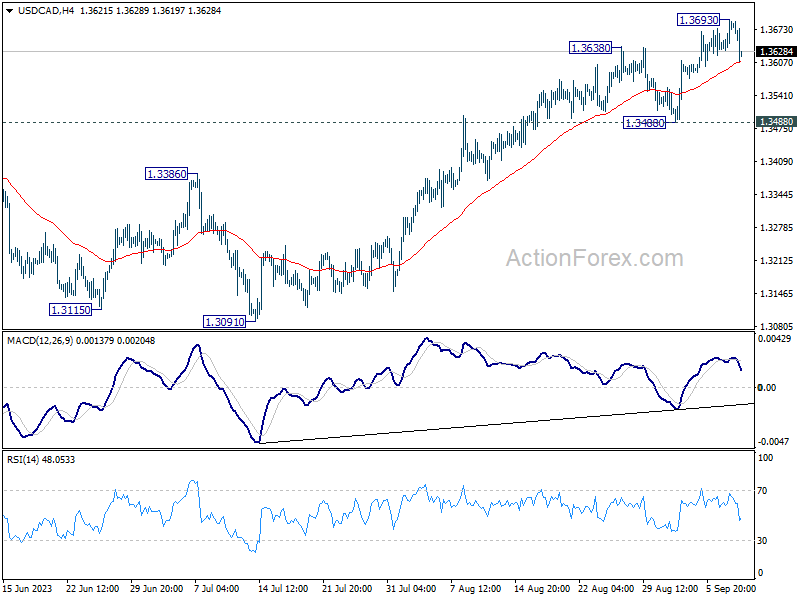

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3648; (P) 1.3671; (R1) 1.3711; More....

Intraday bias in USD/CAD is turned neutral with today's retreat, and some consolidations could be seen below 1.3693. But the favored case is still that correction from 1.3976 has completed at 1.3091. Further rally is expected as long as 1.3488 support holds. Above 1.3693 will resume the rally from 1.3091 to 1.3860 resistance, and then 1.3976 high.

In the bigger picture, price actions from 1.3976 are viewed as a corrective pattern only. Upon completion, rise from 1.2005 (2021 low) would resume through 1.3976. Next target is 61.8% projection of 1.2005 to 1.3976 from 1.3091 at 1.4309. For now, this will remain the favored case as long as 55 D EMA (now at 1.3436) holds.