Sample Category Title

Has Euro/Dollar Entered Bearish Trend or Is It in Correction?

With economic numbers out of the Eurozone heightening recession concerns, and US data keep pointing to a superior US economy, the euro/dollar pair has been in a sliding mode recently.

ECB seen holding its fire next week

At the last ECB meeting, policymakers raised interest rates by a quarter point, but they did not commit to further moves, with President Lagarde replying with a “decisive maybe” when asked whether they are planning to hike again in September.

The fact that Lagarde sounded less hawkish than anticipated combined with a streak of data pointing to continued economic weakness made investors skeptical as to whether officials should raise rates again at next week’s gathering. Even after the preliminary CPI data for August revealed somewhat stickier-than-expected inflation, investors are assigning only a 30% probability for a hike.

However, with core inflation still resting well above the 2% target, no one can conclude that the Bank’s mission has been accomplished. And yet, traders are seeing only a 60% chance for another hike later this year, which probably means that they are more concerned about economic performance than high inflation at this stage.

Markets expect the Fed to stand pat as well

A September hike is not expected by the Fed either. After the last decision, where Powell signaled data dependency, investors became convinced that the Fed will also take the sidelines in September, with Powell’s Jackson Hole speech only raising the probability for a hike by November. This allowed the dollar to continue drifting north, whose engines were already receiving fuel due to concerns surrounding the performance of the Chinese economy.

Last week though, investors had second thoughts regarding the probability of another Fed hike as a streak of US data, including Friday’s employment report, pointed to a cooling US labor market. And still, the US dollar held strong against its European counterpart, confirming that apart from monetary policy developments, traders are increasingly paying attention to economic growth divergences as well. Taking that into account, heading into the September policy decisions, euro/dollar may be poised to continue drifting lower.

But language and signals could be key

Nonetheless, whether this will develop into a bigger downtrend that will extend beyond September is not crystal clear yet and what could clear the fog may be the ECB and Fed decisions on September 14 and 20, respectively.

Recent remarks by ECB officials and very high inflation in the Eurozone suggest that the ECB is very likely to leave the door to further hikes open next week, and if officials sound hawkish enough, the euro could rebound, even if no interest rate increase is delivered at that meeting.

But this could last for less than a week if the Fed appears equally hawkish on September 20, signaling that they are not done raising rates either. Yes, inflation in the US is lower than in the Euro area, but it is also above the 2% target, with the August PMIs pointing to rising input costs. Ergo, a hawkish Fed could keep any ECB-related gains in euro/dollar limited and bring the currency pair back under selling interest.

A break below 1.0665 could complete the reversal

Technically, the move that could confirm a bearish reversal may be a decisive break below the 1.0665 territory, which offered strong support during June. Such a dip would signal a lower low on bigger timeframes, initially targeting the 1.0530 area, the break of which could see scope for extensions all the way down to the low of November 30 at 1.0230.

For the pair to return in an uptrend mode, a break above 1.1070 may be needed, and this could become possible if the ECB ends up appearing more hawkish than the Fed.

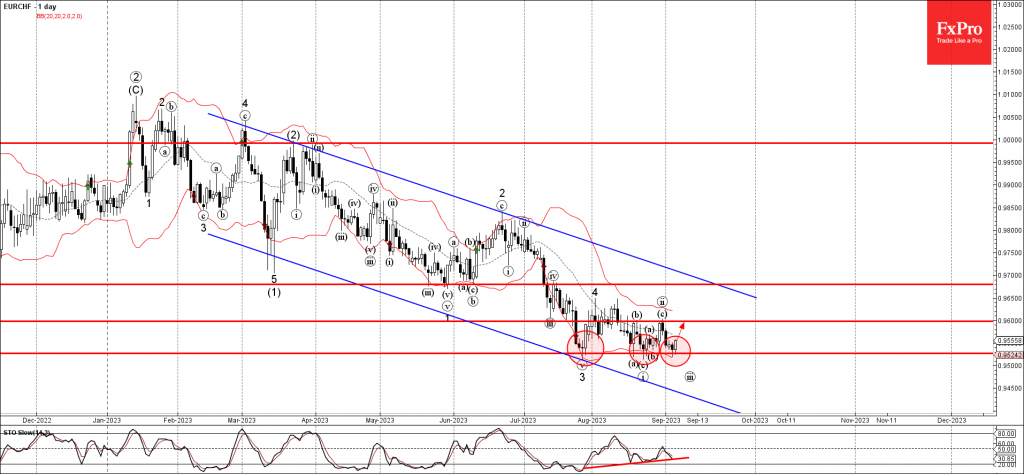

EURCHF Wave Analysis

- EURCHF reversed from pivotal support level 0.9525

- Likely to rise to resistance level 0.9600

EURCHF currency pair recently reversed up from the pivotal support level 0.9525 (which stopped the previous waves 3 and i), intersecting with the lower daily Bollinger Band.

The upward reversal from the support level 0.9525 stopped the active short-term impulse wave iii from the end of August.

Given the strength of the support level 0.9525 and the triple bullish divergence on the daily Stochastic, EURCHF can be expected to rise toward the next resistance level 0.9600 (top of the previous waves ii and b).

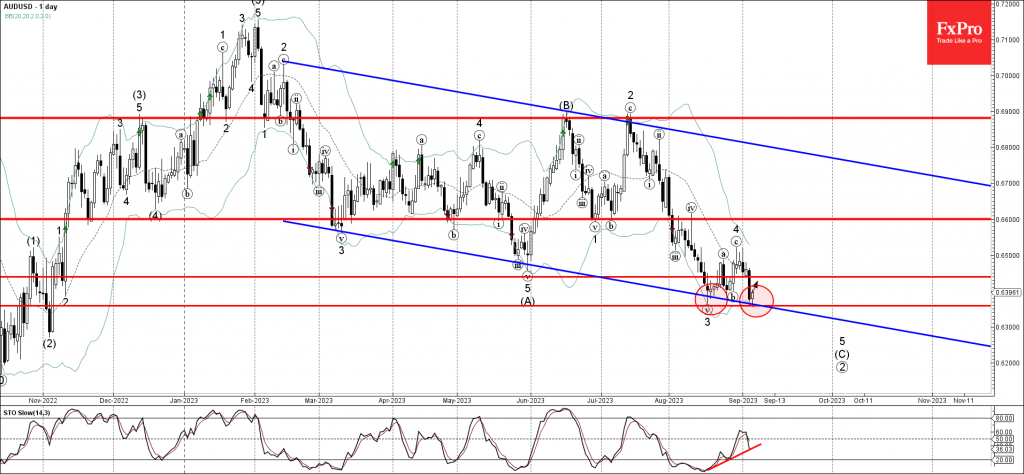

AUDUSD Wave Analysis

- AUDUSD reversed from key support level 0.6360

- Likely to rise to resistance level 0.6440

AUDUSD currency pair recently reversed up from the key support level 0.6360 (previous monthly low from August), intersecting with the support trendline of the wide weekly down channel from February.

The support level 0.6360 was further strengthened by the lower daily Bollinger Band.

Given the strength of the support level 0.6360 and the bullish divergence on the daily Stochastic, AUDUSD can be expected to rise further toward the next resistance level 0.6440.

ECB Kazimir prefers to hike next week, and take a breather thereafter

ECB Governing Council member Peter Kazimir offered two distinct pathways for the central bank's next move, strongly advocating for a 25 bps rate hike in the upcoming meeting next week.

Kazimir laid out the two scenarios: either to pause during the September meeting and opt for a "hopefully final" hike in October or December, or to proceed with a 25 basis point increase immediately, and "take a breather thereafter."

"The second option seems preferable, reasonable, to me," Kazimir emphatically stated. According to him, taking the latter route would be a "more straight forward and efficient solution," providing the markets with clearer signals. Furthermore, it would allow policymakers additional time to confirm that inflation is moving towards the 2% target in a sustainable manner.

Kazimir's recommendation comes at a time when there are increasing uncertainties surrounding the economic outlook. He acknowledged that "forecasts for inflation and economic growth are yet to be updated," but insisted on taking pre-emptive action. "It is, therefore, necessary to take one more step. As they say, better to be safe than sorry," he remarked.

Gold Returns to Bearish Area

Gold came under fresh selling pressure after rising as high as 1,952 in the first trading day of September, exiting the rising channel in the four-hour chart and pulling back into the May-August bearish channel.

The price is currently looking for a rebound around the 38.2% Fibonacci retracement of the 1,987-1,884 downtrend at 1,923, but the technical signals are not promising.

Although the stochastic oscillator is sending oversold signals, the falling RSI has yet to cross below 30, while the MACD has started a new negative cycle below zero and its red signal line. That keeps the bias on the bearish side, making a downfall to 1,910-1,915 likely. If the bears achieve a close below the 1,900 psychological mark, the focus will fall on the five-month low of 1,884.

Alternatively, the bulls may fight for a bounce above the simple moving averages and the 23.6% Fibonacci of 1,936. A penetration higher could immediately stall near the broken rising channel at 1,943. If the recovery survives above the 61.8% Fibonacci and the 1,950 mark, the precious metal could accelerate towards the 1,970 resistance.

All in all, gold is at risk of falling back to the 1,900 area. Yet, as the technical indicators start to identify oversold conditions, the bulls might be around the corner.

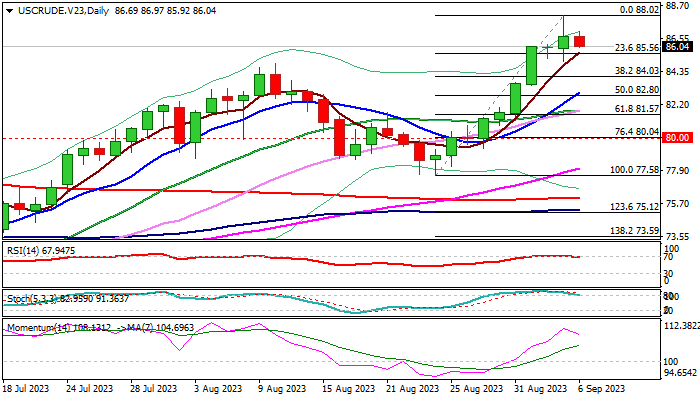

WTI Oil Outlook: Extended Production Cuts to Further Underpin Price

WTI oil price edged lower in early Wednesday’s trading, after advancing 0.9% on Tuesday and hitting new 2023 high ($88.02), underpinned by decision of Saudi Arabia and Russia to extend its voluntarily output cuts in the fourth quarter.

The decision for extended supply reduction is expected to keep the oil market tight, although the positive impact on the price was partially offset by signals that two key oil producers will be reviewing its decision on a monthly basis.

Persisting demand concerns also weigh on oil price as recent weaker than expected global economic data warn that the EU and US economies feel stronger negative impact from high borrowing cost, while economic growth in China, world’s biggest oil importer, is still to gain desired pace in post-Covid recovery.

Short-term picture is overall positive, but overbought conditions on daily chart (14-d momentum and RSI are about to reverse from overbought territory) is likely to trigger some profit taking and push the price lower.

Tuesday’s daily candle with long both shadows generated initial indecision signal, which may add to the scenario of pullback.

Dips should ideally find footstep above $84.00 zone (Fibo 38.2% of $77.58/$88.02 upleg) to mark a healthy condition ahead of fresh push higher, with deeper dips not to exceed $82.80 (50% retracement / rising 10DMA) to keep larger bulls intact, for push through the recent top and acceleration towards psychological $90 barrier.

Conversely, violation of $82.80 pivot would risk deeper correction and expose strong supports at $80.00 (psychological) and $78.70 (top of rising and thickening daily cloud).

Release of US crude inventories reports (API due today and EIA on Wednesday) are also expected to provide fresh signals.

Res: 88.02; 90.00; 93.72; 94.53.

Sup: 85.56; 85.00; 84.03; 82.80.

USD/CAD Rises to 22-Week High, BoC Decision Looms

- Bank of Canada expected to hold rates at 5.0%

- US to release ISM Services PMI

USD/CAD is trading quietly in Europe at 1.3651, up 0.06%. I expect to see stronger movement in the North American session, with the Bank of Canada making its rate announcement and the US releasing the ISM Services PMI which is expected to show little change.

Bank of Canada widely expected to hold rates

The Bank of Canada is virtually certain to hold rates at today’s meeting, with just a 6% probability of a rate hike, according to the TMX Group. That would leave the benchmark cash rate at an even 5.0%.

BoC Governor Macklem would certainly like to call it quits on the central bank’s aggressive tightening cycle and perhaps he can look for advice from his peers at the Federal Reserve and the Reserve Bank of Australia. Both the US and Australian economies have seen inflation fall significantly, but Jerome Powell at the Fed and Peter Lowe at the RBA have sent the markets a hawkish message that inflation isn’t beaten and the door is open for further rate hikes if necessary. The markets have taken a more dovish stance and are already looking ahead to possible rate cuts.

Macklem appears to face the same challenge of acknowledging that rate hikes have cooled the economy and curbed inflation while sounding credible about keeping open the option of further rate hikes. Last week’s GDP report indicated that the economy contracted by 0.2%, compared to the BoC’s forecast of 1.5% growth. The BoC has hiked repeatedly in order to lower inflation but there are concerns that the rate hikes in June and July may have tilted the risk toward a recession.

The Federal Reserve is widely expected to pause at the September 20th meeting. The pause could signal that rates have finally peaked, although don’t expect any Fed members to publicly state that the rate-tightening cycle is over.

Federal Reserve Governor Christopher Waller said on Tuesday that the Fed can afford to “proceed carefully” with rate hikes, given that inflation has been falling, and if the downtrend continues, “we are in pretty good condition”.

USD/CAD Technical

- USD/CAD tested resistance at 1.3657 earlier. The next resistance line is 1.3721

- 1.3573 and 1.3509 are providing support

Australian Dollar Steadies After Solid GDP

- Australian GDP unchanged at 0.4%

- RBA holds rates at 4.10%

The Australian dollar has edged higher on Wednesday, after sustaining sharp losses a day earlier. In the European session, AUD/USD is trading at 0.6391, up 0.19%.

Australia’s GDP holds steady in Q2

The Australian economy grew by 0.4% q/q in the second quarter, unchanged from the upwardly revised reading in the first quarter and matching the consensus. On an annualized basis, GDP expanded 2.1% in the second quarter, compared to an upwardly revised 2.4% in the previous quarter.

The GDP data didn’t knock anyone off their seats, but Australia’s economy has now posted growth for seven straight quarters despite weak global economic conditions. Still, household consumption was weak, falling from 0.3% to 0.1% and the household savings ratio fell from 3.6% to 3.2%. These lower readings reflect the squeeze that higher interest rates and inflation are having on households.

The Reserve Bank of Australia held rates at 4.10% on Tuesday, as expected. The RBA has maintained rates for three straight months and Governor Lowe’s swan song included the usual rhetoric about inflation remaining too high and the door remained open for further rate hikes if needed. The markets are more dovish than the RBA and have priced in a 70% chance of no further hikes from the RBA, with cuts likely to begin in late 2024.

The Federal Reserve is widely expected to pause at the September 20th meeting. The benchmark cash rate is currently in a range of 5.25%-5.50%, and a pause could signal that rates have finally peaked, although don’t expect any Fed members to publicly state that the rate-tightening cycle is over.

Inflation hasn’t been beaten and core CPI, which is a better gauge of underlying inflation than headline CPI, rose 4.2% in July, about double the Fed’s target of 2%. Federal Reserve Governor Christopher Waller said on Monday that the Fed can afford to “proceed carefully” with rate hikes, given that inflation has been falling, and if the downtrend continues, “we are in pretty good condition”.

AUD/USD Technical

- AUD/USD tested resistance at 0.6395 earlier. Above, there is resistance at 0.6458

- There is support at 0.6325 and 0.6274

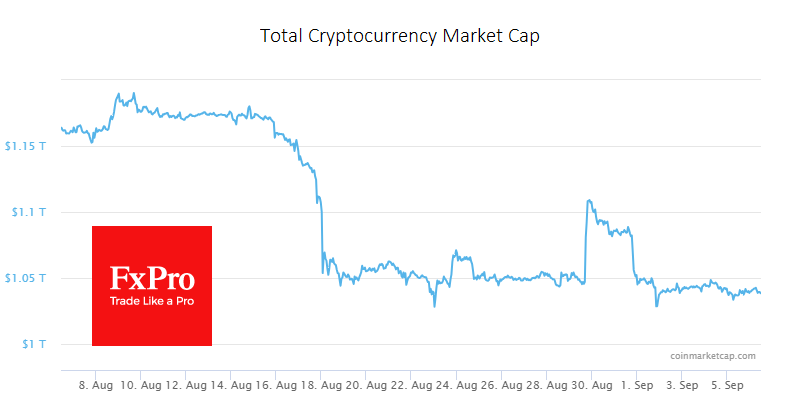

Speculators Have Lost Interest in the Crypto Market

Market picture

Crypto is out of volatility mode, moving in a narrow range of around $1.04 trillion over the last 24 hours, with little change in the total cap. This could be another pause before a new step down the ladder, as we have seen since July, or a preparation for further growth. We are now leaning towards the first option.

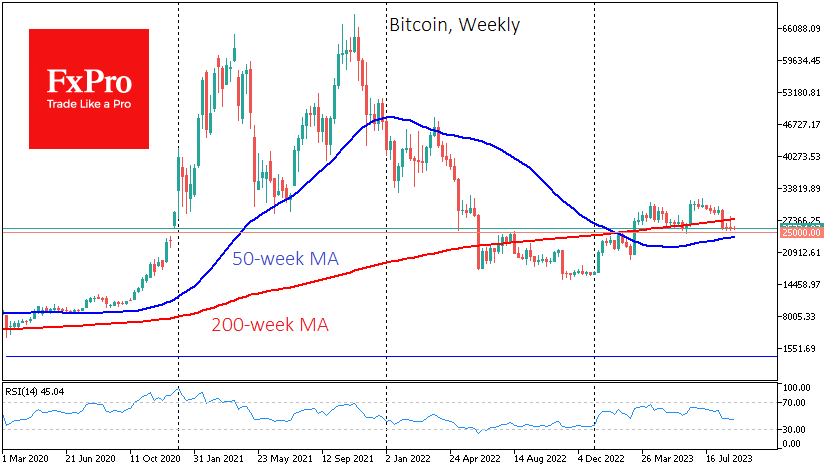

Bitcoin has stabilised around $25.7K, lower than it was at the end of last week. This dip looks like speculators trying to find demand to push the price higher. However, we believe that buyers will remain on the sidelines until the $25K level is reached. This has been the critical level for the last 14 months, and we do not expect a real bull-bear battle until this level is reached.

On the monthly timeframe, Bitcoin confirmed an overbought stochastic exit in August, which could be a sign of disappointment for the bulls, notes Fairlead Strategies. The signal generated often indicates the passing of a local top, as happened in late 2017 and early 2021.

News background

User activity on crypto exchanges is at its lowest since late 2022, according to CCData estimates. It said that the number of Bitcoin transactions on centralised exchanges has fallen by more than 60% since October last year.

Since 2022, lawyers, consultants and other professionals have made more than $700 million from the bankruptcy of five major crypto companies, including FTX, The New York Times calculated by analysing court records.

Payments giant Visa will launch payments in stablecoins based on the Solana blockchain. The company will start testing USDC on the Ethereum network in 2021. The choice of Solana is due to faster and cheaper transactions compared to the ETH blockchain.

Centralisation of nodes is one of Ethereum’s fundamental problems, but an ideal solution may only emerge in 10-20 years, said Vitalik Buterin, the platform’s co-founder. He says the answer lies in making nodes cheaper and easier to maintain.

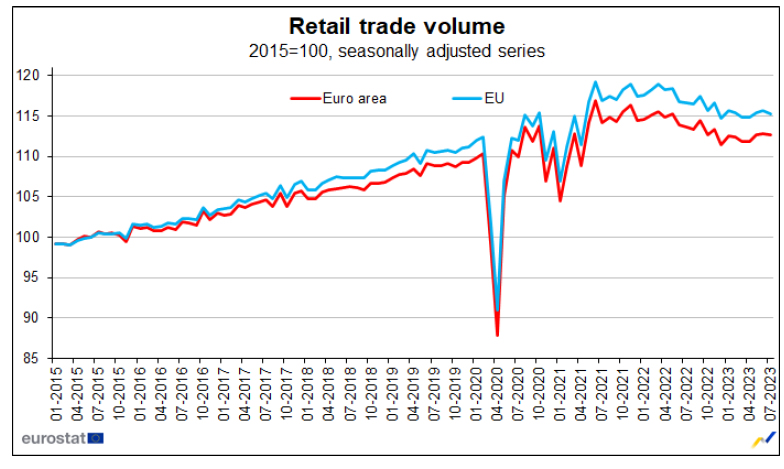

Eurozone retail sales down -0.2% mom in Jul, EU fell -0.3% mom

Eurozone retail sales volume fell -0.2% mom in July, matched expectations. Volume of retail trade decreased by -1.2% mom for automotive fuels, while it increased by 0.4% mom for food, drinks and tobacco and by 0.5% mom for non-food products.

EU retail sales decreased -0.3% mom. Among Member States for which data are available, the largest monthly decreases in the total retail trade volume were registered in Denmark and Ireland (both -2.3%), the Netherlands (-1.4%) and Luxembourg (-1.3%). The highest increases were observed in Portugal (+1.1%), Sweden (+1.0%) and Cyprus (+0.8%).