Sample Category Title

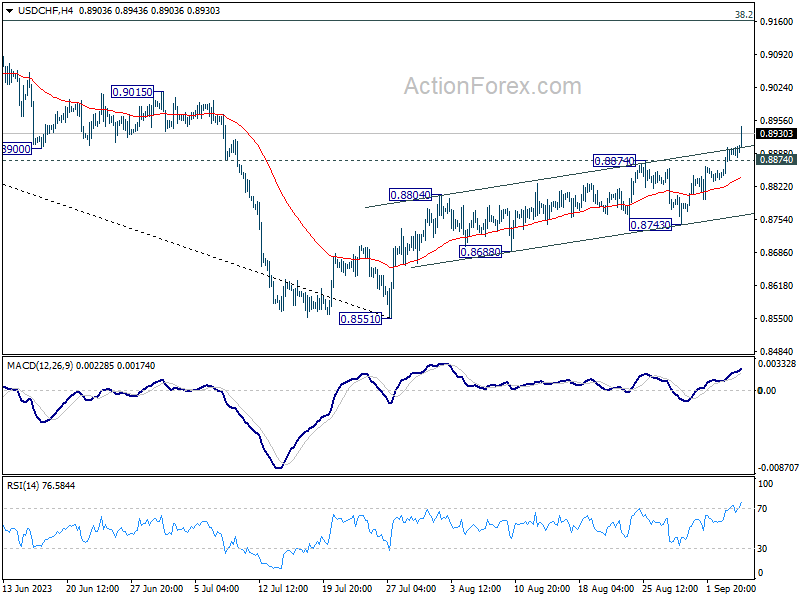

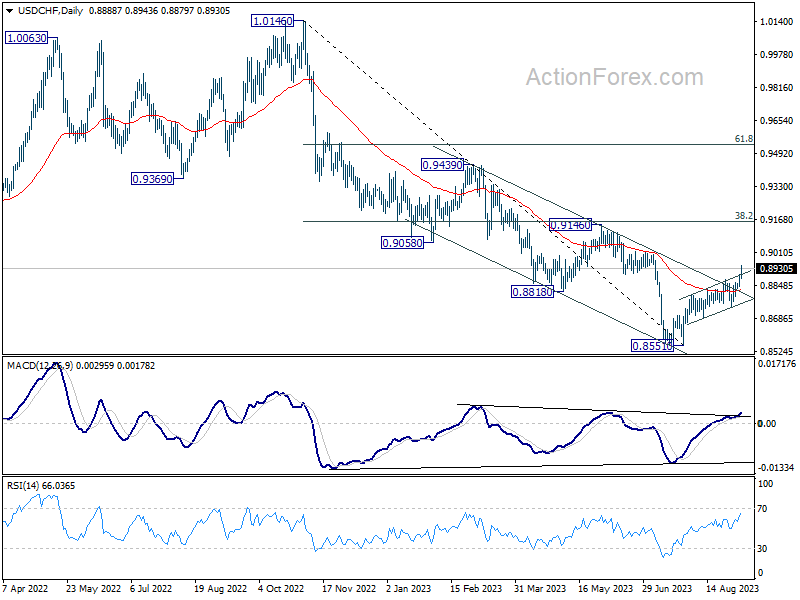

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8855; (P) 0.8879; (R1) 0.8919; More....

USD/CHF's rally from 0.8551 accelerates to as high as 0.8943 so far. Intraday bias stays on the upside. Current rise should target 0.9146 cluster resistance next. On the upside, below 0.8874 minor support will turn intraday bias neutral first. But risk will stay on the upside as long as 0.8743 support holds.

In the bigger picture, rebound from 0.8551 medium term bottom is currently seen as a correction to the downtrend from 1.0146 (2022 high). Further rally would be seen to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160). Strong resistance could be seen there to limit upside, at least on first attempt.

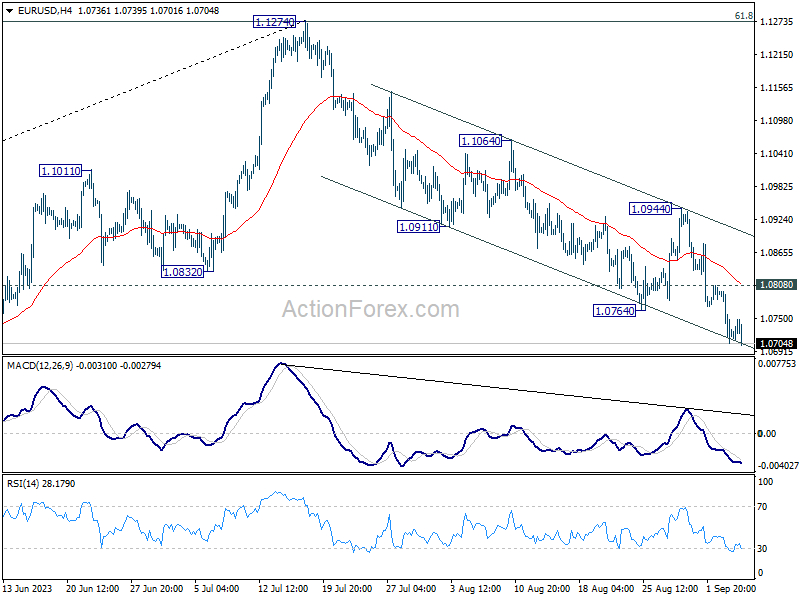

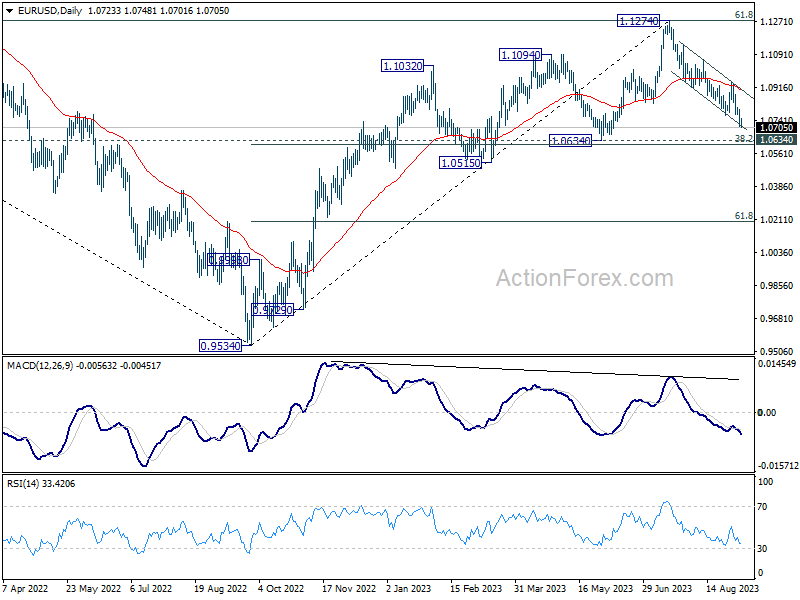

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0685; (P) 1.0744; (R1) 1.0781; More...

EUR/USD's fall from 1.1274 is in progress and intraday bias remains on the downside. Deeper decline would be seen to 1.0609/34 cluster support next. On the upside, above 1.0808 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.0944 resistance holds, in case of recovery.

In the bigger picture, fall from 1.1274 medium term top is seen as a correction to up trend from 0.9534 (2022 low). Deeper decline would be seen to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to bring rebound. Yet, medium term outlook will be neutral for now, as long as 1.1274 resistance holds. However, sustained break of 1.0609/34 will raise the chance of bearish trend reversal, and target 61.8% retracement at 1.0199.

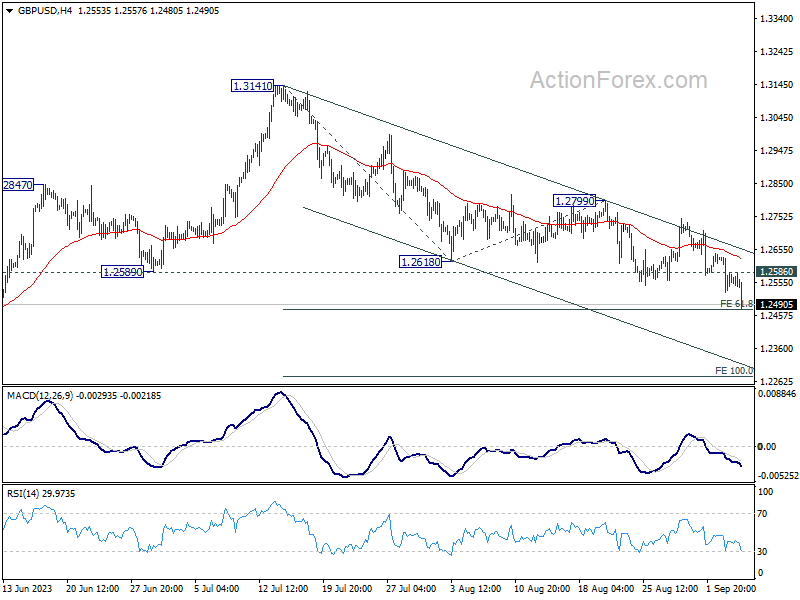

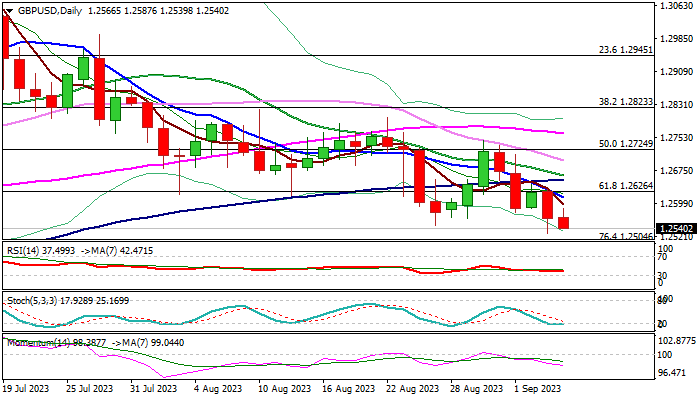

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2517; (P) 1.2577; (R1) 1.2625; More...

GBP/USD's decline continues today and hits as low as 1.2480 so far. Intraday bias remains on the downside. Firm break of 61.8% projection of 1.3141 to 1.2618 from 1.2799 at 1.2476 could prompt downside acceleration to 100% projection at 1.2276. On the upside, above 1.2586 minor resistance will turn intraday bias neutral first.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. But outlook will be neutral at best as long as 1.3141 resistance holds, and consolidation from there is set to extend, until further development.

Dollar Strengthens on Strong ISM Services; Canadian Dollar Steady After BoC Hold

Dollar is enjoying another rally, further solidifying its position as the strongest currency for the week so far, following an upbeat ISM Services report that well exceeded market expectations. The data affirms services sector's dominant role in driving US economy. Additionally, it highlighted a robust uptick in both employment and prices, arguing the specter of services-led inflation looks set to linger.

Canadian Dollar holds steady after BoC opts to keep interest rates unchanged, a move widely anticipated by the markets. While Loonie emerges as the second-strongest currency for the week, this appears to be more a function of weakness in other currencies rather than inherent strength.

Euro is showing signs of resilience, ranking as the third-strongest currency. It is making an attempt to reverse its position against both Sterling and Swiss Franc. Australian and New Zealand dollars, continue to lag as the weakest performers. Yen has experienced a slowdown in its recent selloff, aided by increased verbal intervention from Japanese authorities.

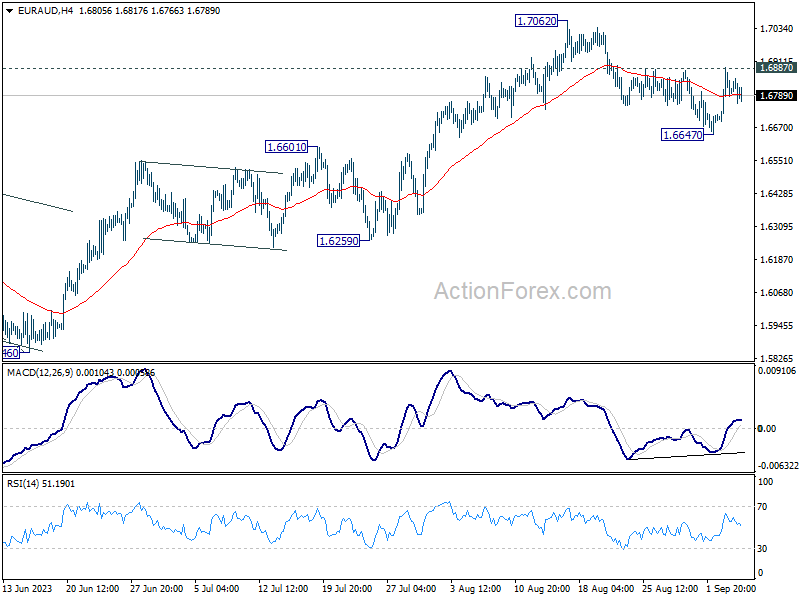

Looking ahead, EUR/AUD would be an intriguing pair to monitor, especially given Aussie's vulnerability to any negative surprises in the forthcoming Chinese trade balance data to be released at the upcoming Asian session. Moreover, rebounds in EUR/CHF and EUR/GBP could potentially bolster Euro in crosses.

Technically, firm break of 1.6887 resistance in EUR/AUD will confirm that correction from 1.7062 has completed. Further rally would then be seen through this resistance to resume larger up trend from 2022 low at 1.4281.

BoC stands pat, keeps hawkish bias

As anticipated, BoC keeps its overnight rate unchanged at 5.00%, alongside the Bank Rate at 5.25% and the deposit rate at 5.00%. Despite the steady rates, the tone of the announcement underscored ongoing concerns about inflation, coupled with a softer outlook on economic growth.

BoC explicitly stated that it remains "concerned about the persistence of underlying inflationary pressures," signaling a continued tightening bias. In its words, the central bank is "prepared to increase the policy interest rate further if needed," highlighting its willingness to act if inflation doesn't abate.

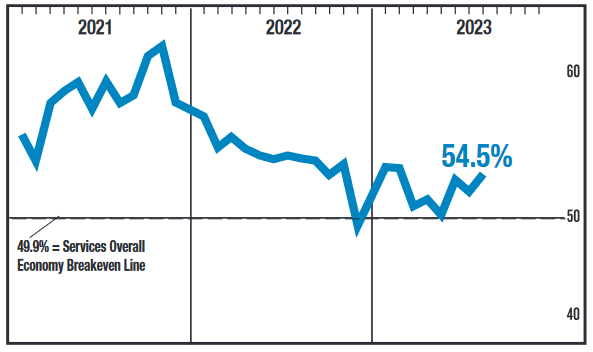

US ISM services rose to 54.5, employment and prices jump

US ISM Services PMI rose from 52.7 to 54.5 in August, comfortably above expectation of 52.6. Looking at some details, business activity/production ticked up from 57.1 to 57.3. New orders rose from 55.0 to 57.5. Employment rose strongly from 50.7 to 54.7. Prices also rose from 56.7 to 58.9.

ISM said: "The past relationship between the Services PMI and the overall economy indicates that the Services PMI for August (54.5 percent) corresponds to a 1.6-percent increase in real gross domestic product (GDP) on an annualized basis."

Fed's Collins advocates patience and holistic data assessment

Boston Fed President Susan Collins struck a note of caution and restraint in today's remarks, suggesting that while policy rates may be reaching their peak, further tightening could still be on the table, dependent on "holistic data assessment."

"This phase of our policy cycle requires patience, and holistic data assessment, while we stay the course," Collins asserted.

Collins emphasized the challenge of discerning meaningful trends in economic data, cautioning that "it is difficult to extract the signal from the noise."

"If the improvement is fleeting, further tightening could be warranted," she warned.

Most notably, Collins was reluctant to embrace the notion that recent improvements in economic indicators necessarily signal a taming of inflationary pressures.

"There are promising developments, but given the continued strength in demand, my view is that it is just too early to take the recent improvements as evidence that inflation is on a sustained path back to 2%," she said.

ECB Kazimir prefers to hike next week, and take a breather thereafter

ECB Governing Council member Peter Kazimir offered two distinct pathways for the central bank's next move, strongly advocating for a 25 bps rate hike in the upcoming meeting next week.

Kazimir laid out the two scenarios: either to pause during the September meeting and opt for a "hopefully final" hike in October or December, or to proceed with a 25 basis point increase immediately, and "take a breather thereafter."

"The second option seems preferable, reasonable, to me," Kazimir emphatically stated. According to him, taking the latter route would be a "more straight forward and efficient solution," providing the markets with clearer signals. Furthermore, it would allow policymakers additional time to confirm that inflation is moving towards the 2% target in a sustainable manner.

Kazimir's recommendation comes at a time when there are increasing uncertainties surrounding the economic outlook. He acknowledged that "forecasts for inflation and economic growth are yet to be updated," but insisted on taking pre-emptive action. "It is, therefore, necessary to take one more step. As they say, better to be safe than sorry," he remarked.

ECB Villeroy: Keeping rates sufficiently long counts more than hikes

ECB Governing Council member Francois Villeroy de Galhau refrained from detailing specific plans for the upcoming September 14 meeting. But he added, "I'm convinced we are close or very close to the high point of interest rates."

Also, "In our fight against inflation, maintaining rates for a sufficiently long period now counts for more than further significant rises", he said.

Villeroy also weighed in on inflation and economic growth trends, asserting that inflation passed its peak at the start of the year." He added that recent fluctuations in oil prices "should not change the underlying dis-inflationary trend." i

As for growth, Villeroy offered a measured outlook. "For the entire euro zone, we don't see a recession today," he noted. "The picture for France and the euro zone is slightly positive growth, slower growth," Villeroy added.

ECB Knot: A further hike still a possibility, but not a certainty

ECB Governing Council member Klaas Knot made it clear that reaching 2% inflation target by the end of 2025 is non-negotiable. "I continue to think that hitting our inflation target of 2% at the end of 2025 is the bare minimum we have to deliver," said Knot.

Knot didn't rule out the possibility of further tightening on at September 14 meeting. "We've reached the finessing phase of the tightening cycle," he noted. "Tightening—a further hike—is still a possibility, but not a certainty."

The ECB member also underscored the importance of wage growth in achieving the central bank's inflation target. According to him, "It's quite crucial in the disinflation process toward 2% by the end of 2025 that wage growth decelerates visibly."

Knot expressed concerns about current wage agreements, stating that they are "still pretty far off longer-run compatibility with a 2% inflation target plus half a percent productivity growth."

Eurozone retail sales down -0.2% mom in Jul, EU fell -0.3% mom

Eurozone retail sales volume fell -0.2% mom in July, matched expectations. Volume of retail trade decreased by -1.2% mom for automotive fuels, while it increased by 0.4% mom for food, drinks and tobacco and by 0.5% mom for non-food products.

EU retail sales decreased -0.3% mom. Among Member States for which data are available, the largest monthly decreases in the total retail trade volume were registered in Denmark and Ireland (both -2.3%), the Netherlands (-1.4%) and Luxembourg (-1.3%). The highest increases were observed in Portugal (+1.1%), Sweden (+1.0%) and Cyprus (+0.8%).

Japan's Kanda flags "high urgency" as Dollar bears 148 Yen

Japan's Vice Minister of Finance for International Affairs, Masato Kanda, issued a strong warning as Dollar approaches 148 yen, marking a high for this year.

Kanda stated, "We are closely monitoring the situation, with a high sense of urgency. If such moves continue, the government will take appropriate measures, and all options are on the table."

These remarks are the first significant warning since the Ten dropped below the 145-per-dollar mark in mid-August. Since then, Japanese authorities had been relatively silent.

With the declared "high sense of urgency", Japan has effectively put currency traders on alert for potential intervention or other policy moves. The "all options are on the table" comment raises the possibility of multiple policy actions, ranging from more verbal warnings to more market interventions to curb yen's fall.

Australia GDP grew 0.4% qoq on capital investment and services exports

Australia's GDP saw 0.4% qoq growth in Q2, aligning perfectly with market expectations. This marks the seventh consecutive quarter of economic growth for the nation. The economy exhibited resilience with a 3.4% annual growth rate for 2022-23 financial year, comfortably surpassing 10-year pre-pandemic average of 2.6%.

However, it wasn't all good news: nominal GDP dropped by -1.2% qoq in the June quarter. GDP implicit price deflator also fell -1.5%, primarily due to -7.9% decline in terms of trade. Export prices fell by -8.2%, exceeding -0.3% fall in import prices. Despite this, domestic price growth remained stable at 1.2%, buoyed by increases in household rents, food prices, and the cost of capital goods, which escalated due to Australian Dollar's depreciation.

The positive quarterly GDP numbers were largely driven by two key factors: capital investment and the exports of services. Total gross fixed capital formation surged by 2.4%, reflecting growth in both public and private investment sectors.

Services exports soared 12.1%, with a significant push coming from 18.5% uptick in travel services.

Net trade in goods added 0.5% to GDP, with 2.5% rise in goods exports led mainly by mining commodities.

Household spending, on the other hand, remained rather muted, contributing just 0.1T to the GDP growth with modest 0.1% increase.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2517; (P) 1.2577; (R1) 1.2625; More...

GBP/USD's decline continues today and hits as low as 1.2480 so far. Intraday bias remains on the downside. Firm break of 61.8% projection of 1.3141 to 1.2618 from 1.2799 at 1.2476 could prompt downside acceleration to 100% projection at 1.2276. On the upside, above 1.2586 minor resistance will turn intraday bias neutral first.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. But outlook will be neutral at best as long as 1.3141 resistance holds, and consolidation from there is set to extend, until further development.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | GDP Q/Q Q2 | 0.40% | 0.40% | 0.20% | |

| 06:00 | EUR | Germany Factory Orders M/M Jul | -11.70% | -4.30% | 7.00% | |

| 08:30 | GBP | Construction PMI Aug | 50.8 | 49.8 | 51.7 | |

| 09:00 | EUR | Eurozone Retail Sales M/M Jul | -0.20% | -0.20% | -0.30% | 0.20% |

| 12:30 | CAD | Labor Productivity Q/Q Q2 | -0.60% | -0.10% | -0.60% | |

| 12:30 | CAD | Trade Balance (CAD) Jul | -1.0B | -3.5B | -3.7B | |

| 12:30 | USD | Trade Balance (USD) Jul | -65.0B | -67.9B | -65.5B | -63.7B |

| 13:45 | USD | Services PMI Aug F | 50.5 | 51 | 51 | |

| 14:00 | USD | ISM Services PMI Aug | 54.5 | 52.6 | 52.7 | |

| 14:00 | CAD | BoC Interest Rate Decision | 5.00% | 5.00% | 5.00% | |

| 18:00 | USD | Fed's Beige Book |

US ISM services rose to 54.5, employment and prices jump

US ISM Services PMI rose from 52.7 to 54.5 in August, comfortably above expectation of 52.6. Looking at some details, business activity/production ticked up from 57.1 to 57.3. New orders rose from 55.0 to 57.5. Employment rose strongly from 50.7 to 54.7. Prices also rose from 56.7 to 58.9.

ISM said: "The past relationship between the Services PMI and the overall economy indicates that the Services PMI for August (54.5 percent) corresponds to a 1.6-percent increase in real gross domestic product (GDP) on an annualized basis."

BoC stands pat, keeps hawkish bias

As anticipated, BoC keeps its overnight rate unchanged at 5.00%, alongside the Bank Rate at 5.25% and the deposit rate at 5.00%. Despite the steady rates, the tone of the announcement underscored ongoing concerns about inflation, coupled with a softer outlook on economic growth.

BoC explicitly stated that it remains "concerned about the persistence of underlying inflationary pressures," signaling a continued tightening bias. In its words, the central bank is "prepared to increase the policy interest rate further if needed," highlighting its willingness to act if inflation doesn't abate.

(BOC) Bank of Canada maintains policy rate, continues quantitative tightening

The Bank of Canada today held its target for the overnight rate at 5%, with the Bank Rate at 5¼% and the deposit rate at 5%. The Bank is also continuing its policy of quantitative tightening.

Inflation in advanced economies has continued to come down, but with measures of core inflation still elevated, major central banks remain focused on restoring price stability. Global growth slowed in the second quarter of 2023, largely reflecting a significant deceleration in China. With ongoing weakness in the property sector undermining confidence, growth prospects in China have diminished. In the United States, growth was stronger than expected, led by robust consumer spending. In Europe, strength in the service sector supported growth, offsetting an ongoing contraction in manufacturing. Global bond yields have risen, reflecting higher real interest rates, and international oil prices are higher than was assumed in the July Monetary Policy Report (MPR).

The Canadian economy has entered a period of weaker growth, which is needed to relieve price pressures. Economic growth slowed sharply in the second quarter of 2023, with output contracting by 0.2% at an annualized rate. This reflected a marked weakening in consumption growth and a decline in housing activity, as well as the impact of wildfires in many regions of the country. Household credit growth slowed as the impact of higher rates restrained spending among a wider range of borrowers. Final domestic demand grew by 1% in the second quarter, supported by government spending and a boost to business investment. The tightness in the labour market has continued to ease gradually. However, wage growth has remained around 4% to 5%.

Recent CPI data indicate that inflationary pressures remain broad-based. After easing to 2.8% in June, CPI inflation moved up to 3.3% in July, averaging close to 3% in line with the Bank's projection. With the recent increase in gasoline prices, CPI inflation is expected to be higher in the near term before easing again. Year-over-year and three-month measures of core inflation are now both running at about 3.5%, indicating there has been little recent downward momentum in underlying inflation. The longer high inflation persists, the greater the risk that elevated inflation becomes entrenched, making it more difficult to restore price stability.

With recent evidence that excess demand in the economy is easing, and given the lagged effects of monetary policy, Governing Council decided to hold the policy interest rate at 5% and continue to normalize the Bank's balance sheet. However, Governing Council remains concerned about the persistence of underlying inflationary pressures, and is prepared to increase the policy interest rate further if needed. Governing Council will continue to assess the dynamics of core inflation and the outlook for CPI inflation. In particular, we will be evaluating whether the evolution of excess demand, inflation expectations, wage growth and corporate pricing behavior are consistent with achieving the 2% inflation target. The Bank remains resolute in its commitment to restoring price stability for Canadians.

Information note

The next scheduled date for announcing the overnight rate target is October 25, 2023. The Bank will publish its next full outlook for the economy and inflation, including risks to the projection, in the Monetary Policy Report at the same time.

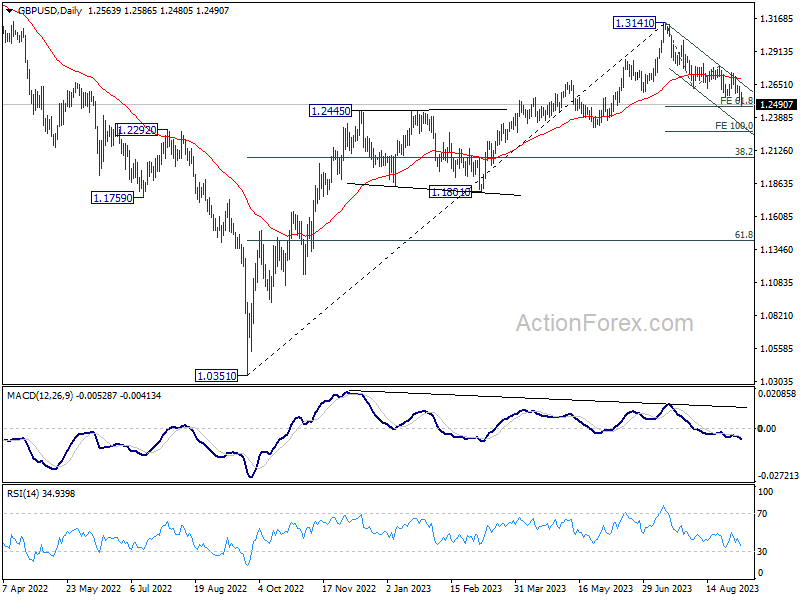

GBP/USD: Bears Hold Grip and Look for Signal of Bearish Continuation

GBPUSD remains at the back foot on Wednesday and holding just above new 11-week low at 1.2527, posted on Tuesday after 0.5% daily drop, which completed bearish engulfing pattern on daily chart, adding to negative near-term signals.

Bear-leg off 1.2746 (Aug 30 lower top) is attempting to complete a failure swing pattern on daily chart, to signal continuation of larger downtrend from 1.3141 (2023 high, posted on July 13) towards initial target at 1.2504 (Fibo 76.4% of 1.2307/1.3141) and 200DMA (1.2423) in extension).

Daily MA’s in predominantly bearish configuration and 14-d momentum sliding deep in the negative territory, contribute to bearish near-term outlook.

Sterling received a mild support from slightly better than expected UK Aug construction PMI, awaiting fresh signals from the speech of BoE Governor Bailey and US Aug non-Manufacturing PMI, which may deflate pound on better than expected Aug numbers.

Res: 1.2587; 1.2626; 1.2665; 1.2724.

Sup: 1.2527; 1.2504; 1.2423; 1.2368.

Euro Steady Higher Despite Soft German, Eurozone Data, US Services PMI Next

- German factory orders slide by 11.7%

- Eurozone retail sales decline by 0.2%

- EUR/USD inches higher

The euro has steadied on Wednesday, following sharp losses a day earlier. In the European session, EUR/USD is trading at 1.0731, up 0.09%.

The euro can’t seem to find its footing and has fallen about 200 basis points since August 31st. On Tuesday, the euro dropped to a low of 1.0706, its lowest level since early June.

German factory orders, eurozone retail sales decline

The eurozone economy is in trouble and Germany, the largest country in the bloc, has also seen its powerhouse economy deteriorate. The manufacturing sector has been mired in decline for months, and the services sector, which had shown prolonged expansion and has carried the eurozone and German economies on its back, fell into contraction territory in August.

The news didn’t get any better on Wednesday, as German factory orders and eurozone retail sales headed lower. German factory orders plunged by 11.7% m/m in July, compared to a consensus of -4.0%. This followed an upwardly revised gain of 7.6% in June. This was the steepest decline since April 2020.

In the eurozone, retail sales decreased by 0.2% m/m in July, down from an upwardly revised 0.2% gain in June and below the consensus of -0.1%. On a yearly basis, retail sales was unchanged in July at -1.0%, slightly better than the consensus of -1.2%. Retail sales have not posted a gain in ten months, pointing to prolonged weakness in consumer spending.

The ECB meets next week and ECB President Lagarde hasn’t shown her cards as to whether the central bank will hike or hold. The host of soft data out of Germany and the eurozone is providing support for the doves, who are concerned about a recession. The hawks remain fixated on pushing inflation closer to the 2% target, even at the price of a recession. The final decision could go right to the wire – currently, the odds of a quarter-point hike stand at 32% and a hold at 68%.

In the US, it’s a relatively quiet week on the data calendar, with only two key events – ISM Services PMI later today for August and unemployment claims on Thursday. The services sector has been in expansion over the past three years with just one exception, but growth has been modest for much of 2023. The consensus for the August PMI stands at 52.5, close to the July reading of 52.7 points. The 50.0 level separates contraction from expansion.

EUR/USD Technical

- EUR/USD is testing support at 1.0716. Below, there is support at 1.0658

- There is resistance at 1.0831 and 1.0889

Fed’s Collins advocates patience and holistic data assessment

Boston Fed President Susan Collins struck a note of caution and restraint in todays remarks, suggesting that while policy rates may be reaching their peak, further tightening could still be on the table, dependent on "holistic data assessment."

"This phase of our policy cycle requires patience, and holistic data assessment, while we stay the course," Collins asserted.

Collins emphasized the challenge of discerning meaningful trends in economic data, cautioning that "it is difficult to extract the signal from the noise."

"If the improvement is fleeting, further tightening could be warranted," she warned.

Most notably, Collins was reluctant to embrace the notion that recent improvements in economic indicators necessarily signal a taming of inflationary pressures.

"There are promising developments, but given the continued strength in demand, my view is that it is just too early to take the recent improvements as evidence that inflation is on a sustained path back to 2%," she said.