Sample Category Title

ECB Preview: A Final Rate Hike, But Restrictive Policies Are Not Over

ECB Preview: A Final Rate Hike, But Restrictive Policies Are Not Over

- We expect the ECB to deliver a final 25bp rate hike during next week's ECB meeting due to still too strong inflation momentum and projected inflation above the target. We also expect an advancement of the end to full reinvestment process of PEPP currently guided for Dec 24 to be on the cards. Specifically, we expect ECB to 'task committees' for an announcement at the October meeting.

- The economic outlook has worsened since the July meeting, but the momentum in inflation is yet to show convincing dynamics, and given ECB's sole inflation mandate, we expect this inflation momentum to prevail. Currently, markets have put significant focus on the disinflationary impulse underway and the weaker growth outlook and therefore markets are only pricing 8bp of rate hikes for next week and 17bp of additional hikes altogether. A compromise in the governing council could be no hike and an acceleration of the balance sheet normalisation, but given the policy rate is the primary tool to calibrate its monetary policy stance, we expect a rate hike.

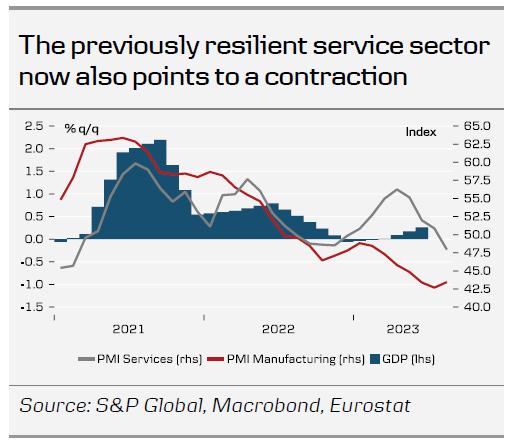

The service sector is now also in contraction

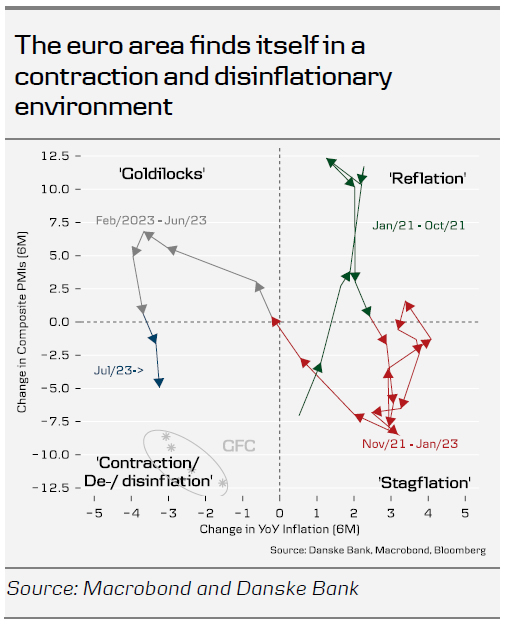

The euro area economy has fared better than expected this year, despite the previous energy crisis and inflation shock. Since the ECB meeting in July, the resilient service sector that kept the euro area activity buoyant, has shown signs of weakness with a below 50 PMI print in August. The PMIs showed that the ongoing demand conditions continued to worsen in August as new orders continued to decline. External demand is deteriorating due to challenges in the Chinese economy, while internal demand is yet to see the full impact of the ECB's monetary tightening. Consequently, we expect a lingering weakness in the euro area activity and specifically we expect a contraction in the euro area GDP in the second half of 2023 and foresee no meaningful rebound before next summer.

Sticky core inflation is a key upside risk to the inflation outlook

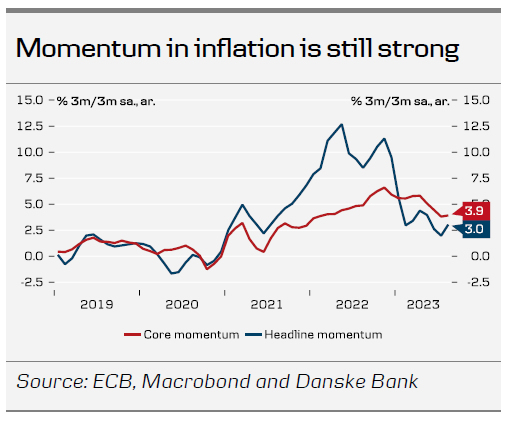

While the inflationary pressure has decreased sharply since last year, based on reviewing the headline figures, the underlying measures of inflation have shown a high degree of stickiness, which has consequently kept the ECB in a tightening mode. The drivers of inflation have shifted from external sources to internal pressures driven by increased wages and strong profit margins, a point that Lagarde also made recently. Wage pressures have been high, thanks to the remarkably strong labour market, despite significant monetary policy tightening. The July minutes referred to the 3m on 3m annualised headline inflation was 'about 2%' in June. Since then, that has picked up to 3% in August.

The strong labour market and large wage increases are keeping the pressure on core inflation which presents a challenge for the ECB. The momentum in core inflation is still high at 3.9% 3m/3m SAAR. The stickiness of core inflation is a key upside risk to the inflation outlook. On the positive side, service price inflation has ticked down in annual terms since the last ECB meeting, but it is still printing at 5.5%. The most recent business surveys show that the service sector is still increasing prices, although at a slower pace than previously.

New staff projections will be closely watched

We will closely watch the ECB staff projections on the back of recent developments. Oil prices have ticked up since the last projection at the June meeting, and futures point to an upward revision of the technical assumptions on oil prices in both 2023 and 2024. On the other hand, natural gas futures are broadly in line with the expectations used in June. Both headline and core inflation have printed well above what the June projection exercise suggested. Headline has so far averaged 5.3% for the first two months of Q3 which is 0.6pp higher than the June exercise suggested. Similar comparison for core was 0.2pp higher at 5.4% so far in Q3. As a result the 2023 outlook may revised slightly higher. For policy guidance, we put more emphasis on the 2024 and 2025 outlook, where a strong labour market and real wage increases will support inflation across the region. However, the recent weakening of the service sector could lower the price pressure. In 2024, the ECB's latest projection of 3.0% y/y is slightly above the consensus of 2.6%. For 2025, inflation projections in June was 2.2% above the ECB's target.

Wage indicators have risen markedly as compensation per employee rose 5.2% in Q1, while negotiated wages rose 4.3% in Q2. Tomorrow, we get Q2 compensation per employee data, which is the last important data release before the meeting.

No hike in September will likely mean end of rate hike cycle.

Markets are currently pricing 8bp of rate hikes in for next week's meeting and 17bp to the peak rate. We only attach a slim probability of ECB skipping this meeting on a rate hike and then deliver one in October. Between the September and October meeting, the key new information we receive will be one inflation release, two PMI reports, a new bank lending survey and the SPF. Between the October meeting and December, we will receive plentiful of data including new staff projections, but for ECB to restart its hiking cycle in December after pausing for two meetings would require the euro area activity finds a new growth engine or we see a significant spike in inflation in our view. As a result, should ECB decide not to hike next week, we believe this is the end additional rate hikes. On the other hand, in our expectation of ECB hike next week, we expect ECB to keep an open door for further hikes, should it be needed – and this much relates to the inflation momentum.

ECB to pushback against expected easing of financial conditions

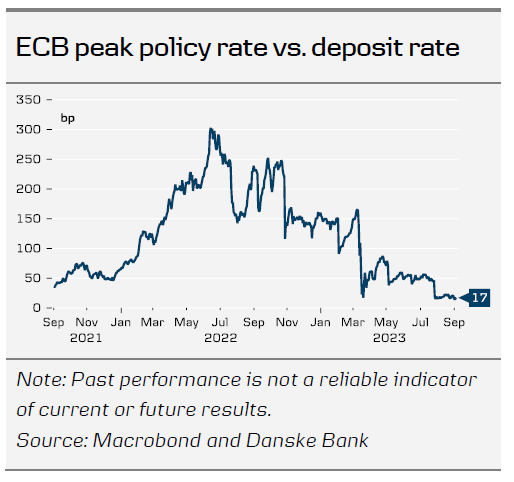

Shorter dated real forward rates in the euro area have shifted lower after the July meeting, implying an easing of the monetary policy stance. As Isabel Schnabel pointed out last week, markets are now pricing the real rates back to the levels we also observed at the February meeting, which are some c.20bp lower than at the July meeting. With the curve inversion in particular in the 2024 segment, we expect ECB to push back against an expectation of an imminent rate cut process and say it is premature to discuss rate cuts. ECB has put focus on the demand led inflation surge and hence to get inflation in line with the target, a sufficient restrictive monetary policy is required. We find the 2024 pricing of -70bp broadly fair. In our baseline scenario of ECB cutting 75bp next, we also highlight that risks are skewed to the topside on this.

Furthermore, a push back from ECB on the expected easing of financial conditions should also be seen in light of the expected inflation risk assessment being skewed to the upside. We find it challenging that ECB can pause at the current meeting with projected inflation in 2025 still above the 2% inflation target and a skewed inflation risk picture.

Advancing the end date of full PEPP reinvestments.

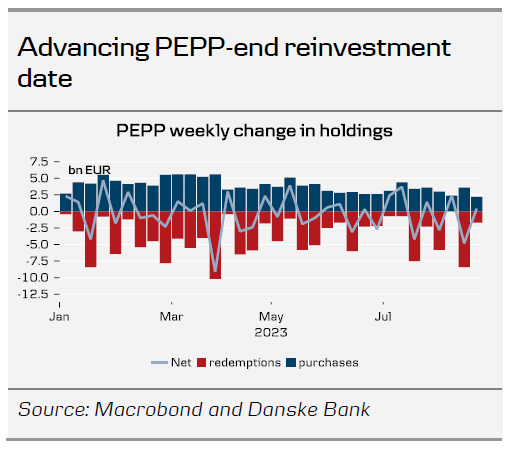

As we discussed in Reading the Markets EUR: Advancing the end to full PEPP reinvestments, 1 September, we expect the ECB to task committees to look into an advancement of the end to full PEPP reinvestments for a potential decision at the October meeting. We expect intentional vague language / guidance on ending PEPP reinvestments, which means that the ECB will have the flexibility to restart (even temporarily) reinvestments if it sees the need or if unfavourable market conditions persist, to continue its balance sheet normalisation. We expect an end to PEPP reinvestments to start from December this year. PEPP reinvestments averages EUR18bn/month currently.

Technical questions during the Q&A session

At the July meeting, ECB surprisingly announced a change the remuneration rate of the minimum reserve holdings starting on 20 September to be 0% (previously deposit rate). The upcoming change have been absorbed well by markets as anticipated, given that the MRR funds are 'locked' money and can't be used for investable means. We do not expect this to feature in the Q&A session.

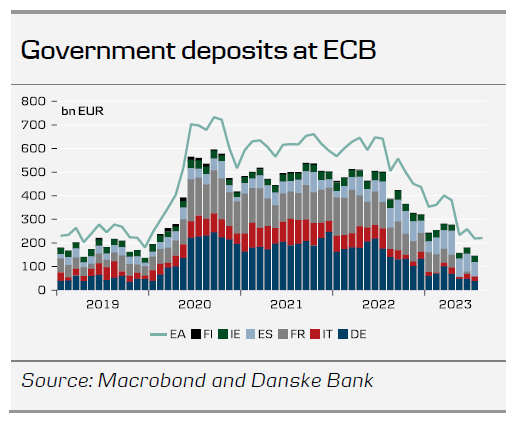

After the Bundesbank's (BuBa) unilaterally changed the rate on the government deposits from 1 October we expect Lagarde to get questions of whether a common decision will follow the BuBa change will be coming up. As of 1 October, the BuBa will no longer pay €STR-20bp but 0% on government deposits and the change was made possible effective from May where the ECB allowed the NCBs to decide the interest rate on the deposits concerned. We highlight that Spain (around EUR62bn) and Ireland (around EUR26bn) still have significant government deposits. Italy has 'only' EUR19bn.

A hike will likely broadly boost the EUR

Given the market pricing, a 25bp rate hike from the ECB will likely prompt a knee-jerk reaction higher in EUR/USD by 1-2 figures almost regardless of the rhetoric on the press conference and the sequential growth outlook priced by markets.

Since mid-July, EUR/USD has been on a downward trajectory breaking below 1.0750. Generally, the theme of US outperformance has been dominating despite the US jobs report showing a more balanced labour market and wage growth cooling. In addition, weak growth prospects overseas, especially in the euro area and China have likely also been beneficial for the greenback in tandem with the domestic strength in the US economy leading to upward pressure on US yields, lately driven by improving signs in the manufacturing sector (although the sector is still in contractionary territory). The DXY USD index recently hit the highest level since March this year.

Going forward, we remain bearish on EUR/USD, although relative rates could boost the cross in the near-term if the ECB hikes. The growth outlook looks rather bleak in the euro area, and we are likely yet to see the full effect of ECB's monetary policy tightening. On the other hand, the resilience of the US economy looks to be broadly continuing. Even though growth and inflation are declining in both regions, especially the former seems to be fading faster in the euro area. With central banks nearing peak policy rates, growth differentials increasingly appear to drive the cross. Hence, we maintain our strategic case for a lower EUR/USD, as we deem the US economy will remain on a relative stronger footing. We continue to forecast the cross at 1.06/.1.03 in 6/12M.

With Clouds Gathering Over the UK Economy, What’s Next for Pound?

Although the Bank of England is expected to keep raising rates for a while longer, the pound has lost decent ground lately against its US counterpart as traders seem to have been paying growing attention to growth dynamics. With underlying inflation more than three times the BoE’s 2% objective, will BoE policymakers stay keen to continue pressing the hike button or will they turn to a more cautious stance in order to safeguard the local economy?

BoE slows down, but underlying inflation remains high

BoE policymakers decided to slow their tightening efforts at the August gathering, raising interest rates by 25bps, a smaller hike than July’s half-point increment, with Governor Bailey noting that he didn’t think there was a case for another 50bps hike. This hurt market expectations regarding the BoE’s future course of action and weighed on the pound, which was already struggling against its US counterpart due to data suggesting that the US remains in better shape than other major economies.

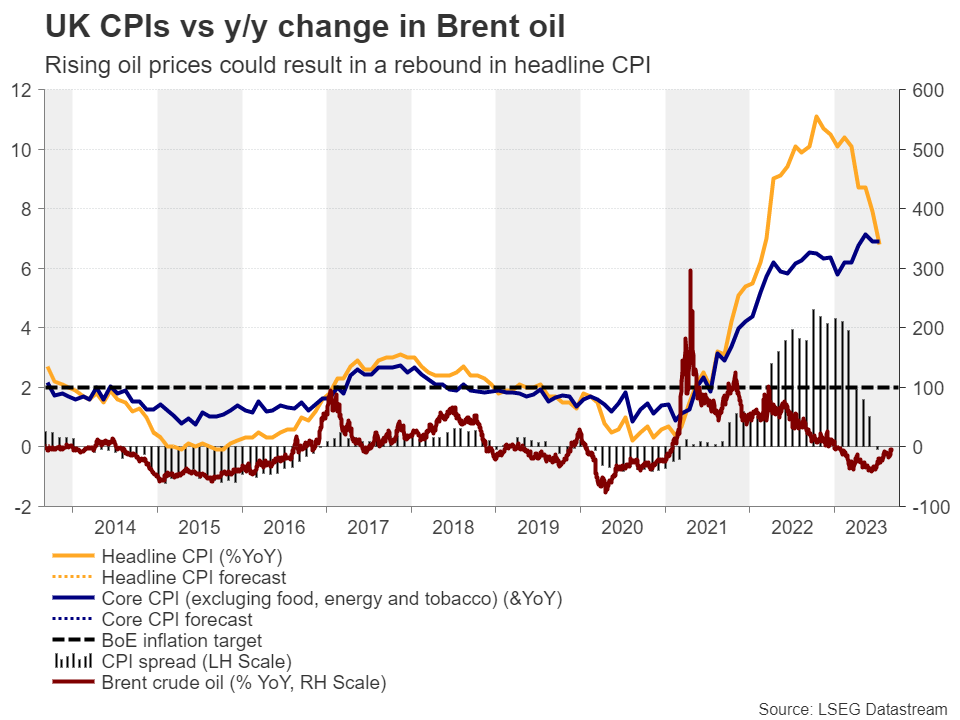

After the decision, GDP data showed that the economy grew somewhat instead of stagnating as the forecast suggested, with industrial and manufacturing production proving much stronger than expected in June. What’s more, despite the economy losing jobs and the unemployment rate rising to 4.2% in June from 4.0%, wages excluding bonuses accelerated by a full percentage point, adding to the already elevated inflation concerns. And as if all this was not enough, the CPI data revealed that the core CPI rate held steady at 6.9% y/y in July, suggesting that the decent slowdown in the headline print was due to volatile items like food and energy. With oil prices extending their recovery during August, a rebound in the headline rate in coming months cannot be ruled out.

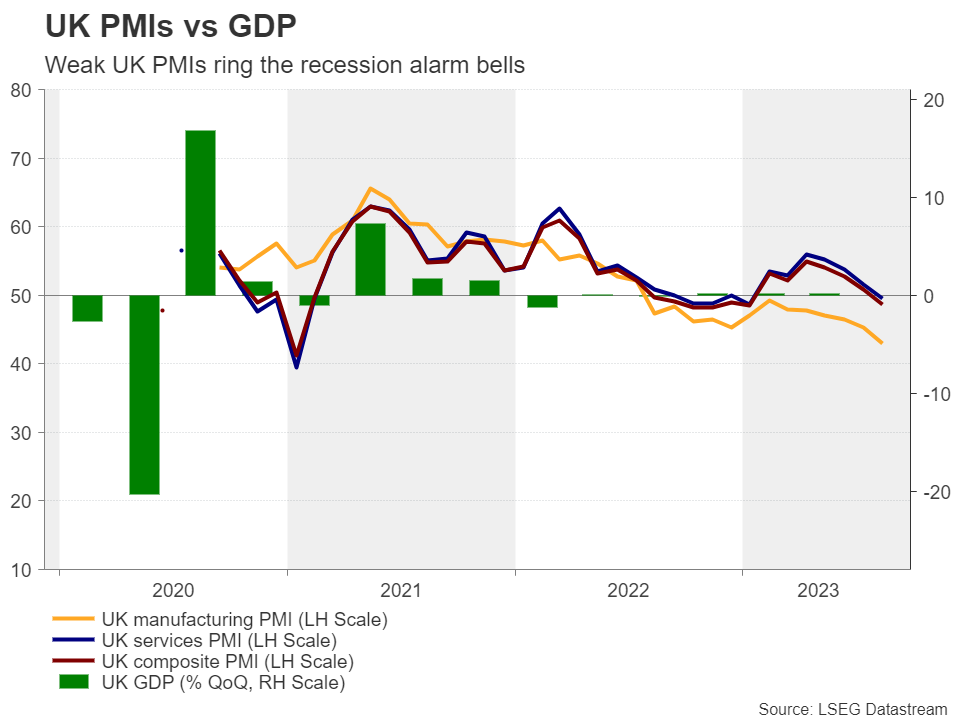

Ugly UK PMIs leave the BoE with a dilemma

All these numbers suggest that the BoE should stay the course and continue raising rates in order to bring ultra-sticky inflation to heel. However, the PMIs for August painted an ugly picture, with the composite PMI slipping into contractionary territory for the first time since January, heightening recession fears and leaving the BoE with a dilemma: continue raising rates and risk further damaging the economy or take a breather and risk allowing inflation to get out of control?

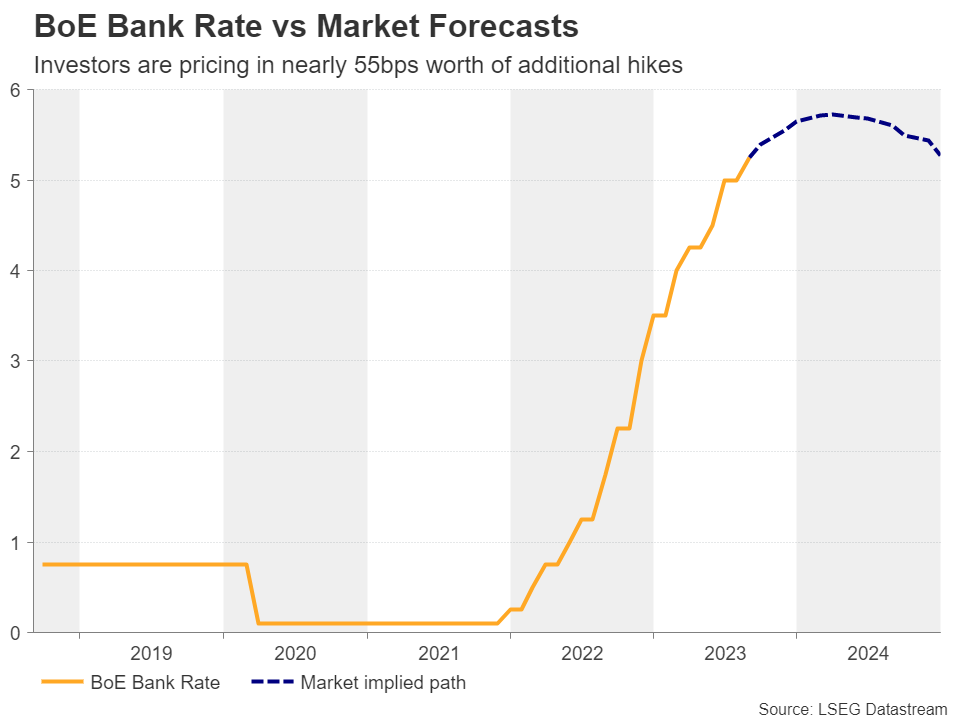

Just last week, remarks by Chief Economist Hew Pill revealed that he is in favor of keeping rates at current levels for longer rather than continuing to raise them and start cutting when they conclude the job is done. In other words, he may be willing to vote to keep interest rates on hold at the upcoming gathering on September 21. Still, the market is assigning an 83% probability for a 25bps hike that gathering, while it is fully pricing in another one by February.

This stands in a sharp contrast to the 55% probability seen for only another quarter point hike by the Fed and yet, the pound is on the back foot against the US dollar, confirming the narrative that traders are turning their gaze to growth dynamics. Despite the latest streak of data pointing to a slowdown in the US, the overall picture still suggests that the world’s largest economy is in a healthier state.

Like the September gatherings of all the major central banks, the BoE’s meeting on September 21 may prove pivotal with regards to the pound’s fate. Even if the Bank decides to press the hike button, if the decision is a close call and/or the decision has a dovish flavor, with hints that the peak of interest rates will be lower than the market currently anticipates, the pound is likely to continue to suffer. The opposite may be true if the Bank highlights the stickiness of inflation and appears ready to do whatever it takes to bring it to heel.

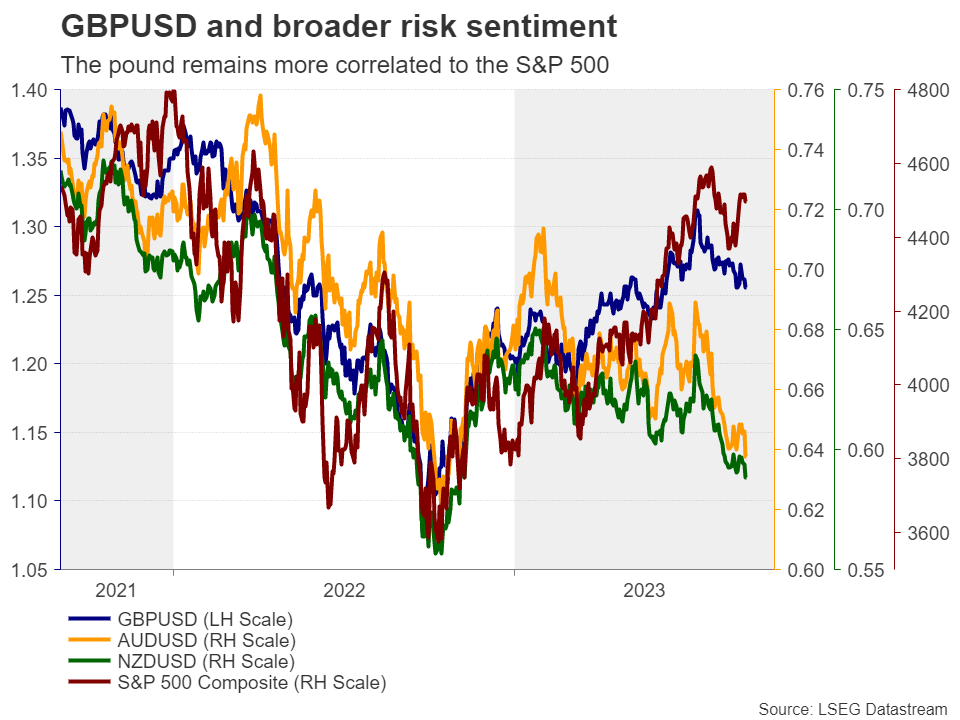

Equities have the pound’s back

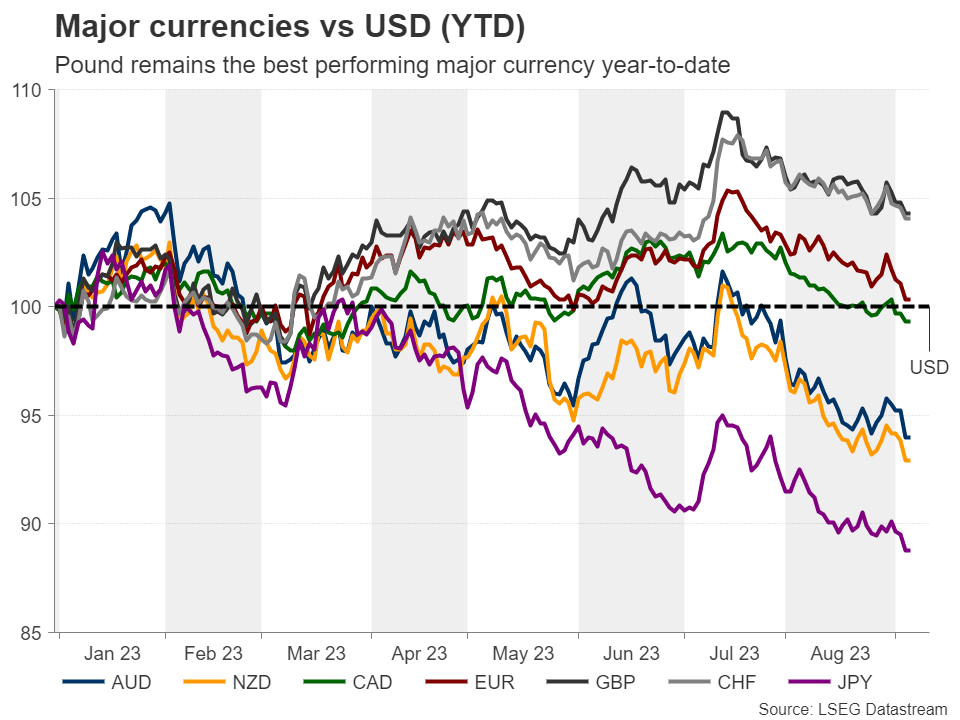

Despite its latest slide, the pound remains the best performing major currency – almost tied with the franc – since the turn of the year, and it is among the ones that lost the least ground since the US dollar staged a comeback. Apart from the fact that the BoE is still seen delivering more hikes than other major central banks, the pound may be also receiving support from its close correlation to the stock market.

As risk-linked currencies, the aussie and the kiwi also used to have a positive correlation with Wall Street, but due to Australia’s and New Zealand’s strong trade ties with China, these currencies are now better reflecting the concerns surrounding the performance of the world’s second largest economy. Having also in mind that both the RBA and the RBNZ seem to have concluded their tightening cycles, according to market pricing, the pound may be destined to continue outperforming those currencies. In other words, even if sterling suffers for a while longer against the US dollar, the pound/aussie and pound/kiwi pairs may be destined to continue drifting north.

Pound/kiwi pulled back after hitting the 2.1585 barrier, but it continues to trade above the uptrend line drawn from the low of February 2. This points to a positive outlook and should the bulls regain control, they could aim for another test at 2.1585, or the high of March 9, 2020, at 2.1680. A break higher could see scope for advances towards the psychological round number of 2.2000, also marked by the peak of May 26, 2016. For a bearish reversal to start being examined, the pair may need to drop below the key support zone of 2.0910.

BoC Hits (Hopeful) Pause on Rate Hikes

The Bank of Canada decided to pause the hiking cycle and left the overnight rate unchanged at 5% in today’s announcement, in line with our and markets’ pre-meeting expectations.

The BoC (also as expected) kept the option open to hike further if necessary down the road. Inflation has slowed substantially but the central bank's own preferred 'core' measures are still running persistently above the 2% target. Wage growth is still high and near-term CPI growth rates are likely to rise in the near-term with oil prices higher in recent weeks.

But interest rates are already at levels that the central bank views as 'restrictive' enough to put downward pressure on economic growth and inflation pressures over time. And today's decision followed a slew of softer economic data releases that suggest the lagged growth headwinds from the 475 bp cumulative rate hikes since March 2022 are building.

The unemployment rate in Canada rose by half a percentage point from April to July. And GDP edged lower in Q2 alongside a soft early estimate for July that's tracking potentially a second consecutive quarterly decline in Q3. That GDP data is substantially softer than the 1.5% (annualized) increase in each of Q2 and Q3 that the BoC assumed in July.

Bottom line: The BoC remains highly data-dependent and won't hesitate to push interest rates higher if necessary to return inflation to the 2% target rate. And there are two additional labour market reports and two additional inflation reports before the next scheduled decision in October. But we continue to expect that the recent soft-patch in economic data will continue, and look for the overnight rate to hold where it is through the end of this year

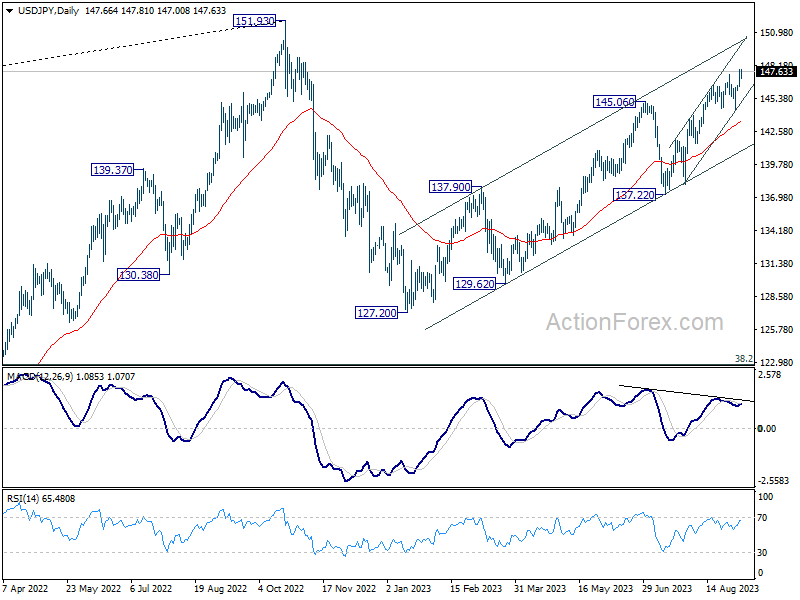

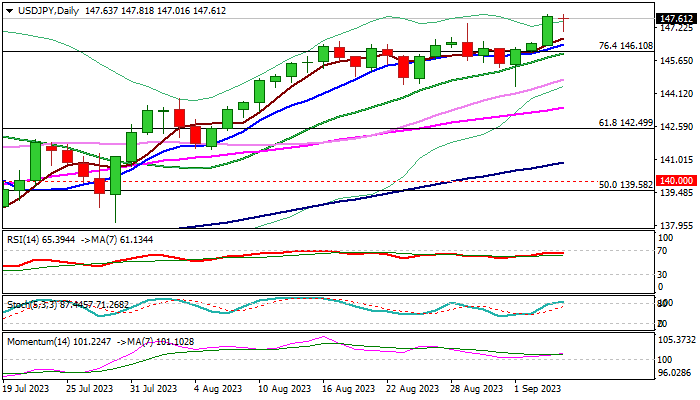

USD/JPY: Bulls Remain in Play Despite Intervention Fears

USD/JPY bulls are taking a breather after three-day rally which accelerated to new 2023 high on Tuesday (the pair was up 0.9% for the day).

Traders remain cautious on looming intervention, as Japan’s authorities reiterated their readiness to intervene at any time to support weakening national currency, although larger bulls remain firmly in play, with signals of further advance seen on daily chart.

In addition, much better than expected US non-manufacturing PMI figures (Aug 54.5 at seven-month high vs July 52.7 and 52.5 f/c) adds to positive signals for dollar.

On the other hand, overbought conditions on daily chart may keep the pair in a narrow consolidation (ideally to be contained at 146.10 zone (daily Tenkan-sen / broken Fibo 76.4%, former strong resistance) to keep bulls in play and offer better buying opportunities.

Only acceleration through 144.60/40 zone (daily Kijun-sen / higher base) would sideline bulls and open way for deeper correction.

Res: 147.81; 148.84; 149.7; 150.00

Sup: 147.01 146.43; 146.10; 145.35

BoE Bailey signals near end of tightening cycle, shifts to data-driven stance

In today's parliamentary hearing, BoE Governor Andrew Bailey provided nuanced insights that suggest the central bank could be nearing the end of its interest rate-hiking cycle. While Bailey was cautious not to confirm that rates have peaked, he pointed to "current evidence" indicating the bank is "much nearer now to the top of the cycle."

Bailey asserted that many economic indicators are behaving as expected, signaling a likely continued—and quite marked—fall in inflation by year-end. Although he warned of a temporary uptick in the next data release due to year-on-year changes in fuel prices, he brushed off the development as non-central to the inflation trajectory.

Reflecting on BoE's recent shift in policy language, Bailey noted that the bank has moved from a posture of determining the "how much and over what time frame" of rate hikes to a more "evidence and data-driven" approach. He also emphasized that monetary policy is "now restricted in its impact," indicating a limited scope for further significant rate hikes.

Deputy Governor Jon Cunliffe also weighed in on inflation, noting the presence of "mixed signals." While pay growth and service price inflation remain strong, there are signs of "cooling in the labour market," he said, framing this as a focal point of discussions moving forward.

Bank of Canada Holds Policy Rate at 5%

The Bank of Canada maintained the overnight rate at 5.0%, while stating that it will continue with Quantitative Tightening (QT).

The bank highlighted the slowing in economic momentum stating, "the Canadian economy has entered a period of weaker growth, which is needed to relieve price pressures. Economic growth slowed sharply in the second quarter of 2023, with output contracting by 0.2% at an annualized rate. This reflected a marked weakening in consumption growth and a decline in housing activity."

On the persistence of high inflation, it stated that "recent CPI data indicate that inflationary pressures remain broad-based. After easing to 2.8% in June, CPI inflation moved up to 3.3% in July, averaging close to 3% in line with the Bank’s projection. With the recent increase in gasoline prices, CPI inflation is expected to be higher in the near term before easing again."

On the future path of policy, the Bank recognized that "excess demand in the economy is easing", but that it remains "prepared to increase the policy interest rate further if needed."

Key Implications

No surprises today as the BoC held the policy rate at 5%. With last week's GDP release showing a contraction in the second quarter, and growing signs of a cooling in the job market, there was little pressure for the BoC to keep raising rates. Our expectation is that this period of "weak economic growth" is set to continue over the rest of this year and into early 2024.

Although the BoC has moved back to the sidelines, it doesn't mean it will let up on its hawkish rhetoric. It needs to make sure that financial conditions remain tight for the economy to continue to slow. Markets are still in the 'will they, won't they' camp, with pricing for another hike around 50%. Given that the slowdown looks to continue, we think the bar for another hike has been raised.

ISM Index Shows Healthy Services Sector Expansion in August

The ISM Services PMI rose to 54.5 in August from 52.7 in July, handily beating the 52.5 reading consensus was expecting. This is the eighth consecutive month of expansion for the services sector.

The business activity sub-index firmed a more modest 0.2 percentage points (pp) to 57.3 in August.

The new orders index rose 2.5 pp to 57.5, the strongest print since February.

The prices paid component rose to 58.9. Despite the second consecutive uptick in price growth, the index is still lower than at any point between June 2020 and April 2023.

Supplier delivery times registered 48.5, up from 48.1 in July, while the backlog of orders index plummeted 10.3 points to 41.8.

The employment sub-component jumped 4.0 pp to 54.7.

Thirteen out of 18 industries expanded in August, down from fourteen in July.

Key Implications

After a bumpy few months, the services sector is showing renewed verve. The headline index has posted gains in two of the past three months and is approaching levels registered in January and February. That said, the expansion is not progressing at the same pace as in 2021 and 2022. Growth looks set to proceed at a more moderate pace as the new orders and business activity sub-indexes are both a touch below their respective ten-year averages.

While the expansion has slowed from the gangbusters pace in 2021 and 2022, healthy indications from the services sector are showing an economy that still has something left in the tank. Moreover, the growth is coming at a time that labor markets remain tight – putting a floor under wage growth.

Sunset Market Commentary

Markets

Uncertainty on the health/recovery of the Chinese economy and a higher oil price due to prologued production cuts from Saudi-Arabia and Russia cloud the global economic outlook and triggered a mild risk-off reaction on Asian markets. German June factory orders tumbled 11.7% M/M and at first sight only reinforced the view that the German/EMU economy was heading for even deeper trouble. However, it was mainly due to a big ticket (aerospace) order in June. Even so, European equities opened with losses of 0.5%+ and momentum remained fragile as trading continued. The Eurostoxx 50 currently loses about 0.65% .US indices opened about 0.25/0.3% lower. Oil stabilizes just below $90/b. This level risks reinforcing unwelcome stagflationary dynamics. ECB speakers gave some final guidance for next week’s policy meeting ahead of their black-out period. ECB’s Knot indicated that markets are underestimating the chances of a September rate hike. His Slovak colleague Kazimir said that it’s preferable for the ECB to raise the policy rate next week rather than taking a pause. Contrary to what happened yesterday, the German yield curve (re-)inverts slightly with the 2-yr yield rising 4 bps while the 30-yr eases 1 bp. US yields traded with changes of less than 1.5 bp across the curve ahead of the services ISM. It printed strong (54.5 from 52.7 vs 52.5 expected) with the 2-yr yield aiming at 5% again. The Fed later today also will publish the Beige Book preparing the September 20 policy decision.

The dollar took a breather ahead of the ISM. Afterwards, the greenback profited from the interest rate support with DXY easily holding above the 104.7 May top. The ongoing debate on a ECB rate hike next week initially helped to prevent aggressive further euro sales, but the dollar took the upper hand with the pair testing the 1.07 big figure. USD/JPY trades at 147.60, near the 10-month peak touched in overnight rating. Japanese Vice finance minister for foreign affairs warned that authorities are ready to take appropriate action. The verbal interventions are no game-changer to counter USD dominance. UK yields are mostly trading marginally lower as BoE’s Bailey and his colleagues are testifying before a committee of Parliament. First headlines indicate that BoE’s Bailey is confident that the disinflation process will continue. Sterling underperforms with EUR/GBP returning to the mid 0.85 area.

News & Views

In the most remarkable of U-turns, Turkish president Erdogan today said that tight monetary policy was needed to slow inflation. Since he silently sided with a hawkish turn at the central bank, it raised its policy rate from 8.5% to 25% over the space of three months. Over the past years, his stubborn view that lower rates are needed for low inflation pushed the country’s assets to edge. Today, he vowed a return to single digit price increases as his government presented economic targets for the next three years. New inflation forecasts suggest that this will happen in 2026 (8.5%) following 65% this year (up from 24.9%), 33% next year (from 13.8%) and 15.2% in 2025 (from 9.9%). Growth forecasts for this and next year stand at 4.4% and 4% respectively, down from 5% and 5.5%. The Turkish lira didn’t respond to today’s update an continues trading weak at EUR/TRY 28.80.

The National Bank of Poland cut its policy rate today by 75 bps from 6.75% to 6%. It was always going to be a close call as Polish central bank governor Glapinski tied the faith of a rate cut to Polish inflation dropping to single digits; a target narrowly missed last week (10.1% Y/Y). The statement will later today provide more clarity, but a significant loss of economic momentum is likely the official explanation with October elections being the unofficial one. While the market was split on whether or not the NBP would pull the trigger, no one was positioned for such a large move with Glapinski at the July press conference indicating a preference to move in smaller steps once the cutting cycle starts. Polish zloty swap rates tank up to 22.5 bps at the front end of the curve (2-yr) with the zloty selling off. EUR/PLN breaks through 4.50 resistance to currently change hands above 4.55%. Interestingly, other CEE currencies took a scare as well from the NBP signaling (?) function. EUR/HUF spikes above 390 with EUR/CZK testing the YTD highs around 24.30. We must add comments by CNB Prochazka earlier today who said that he couldn’t image the CNB lowering rates while the ECB would still be going up.

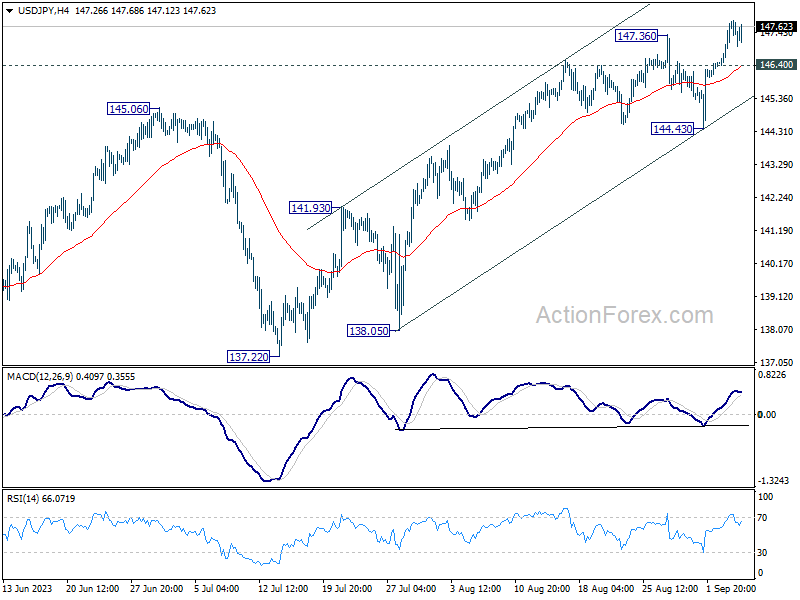

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.82; (P) 147.31; (R1) 148.22; More...

USD/JPY's rally is still in progress and stays on the upside. Current rally is part of the whole rise from 127.20, and should target a test on 151.93 high. On the downside, below 146.40 minor support will turn intraday bias neutral first. But near term outlook will stay bullish as long as 144.43 support holds, in case of retreat.

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.