Sample Category Title

Mild Risk-Off Sentiment, Dollar Dominates With Some Hesitation

Asian markets showcased a mild risk-off tone today, in the wake of lower closes in US markets overnight. However, the forex arena remains comparatively tranquil with major currency pairs and crosses largely confined within the previous day's trading range. Lingering apprehensions regarding a potential rate hike by the Fed have resurfaced following robust US services data. Yet, the odds of a subsequent rate increase in either November or December—assuming a pause this month—continue to oscillate around the 50% mark. This ambiguity is poised to persist unless the new economic projections by Fed provide a more definitive direction.

For the week, Dollar stands tall as the dominant currency. Nonetheless, there's a perceptible hesitation among buyers, suggesting a reluctance to propel the greenback any higher from its current position. Canadian Dollar trails closely as the second strongest, with Euro coming in third. On the flip side, Australian Dollar languishes at the bottom, feeling the pressure by lackluster Chinese trade figures. New Zealand Dollar and Yen aren't faring much better, positioned as the second and third weakest currencies respectively. Meanwhile, Sterling and Swiss Franc are presenting a mixed performance.

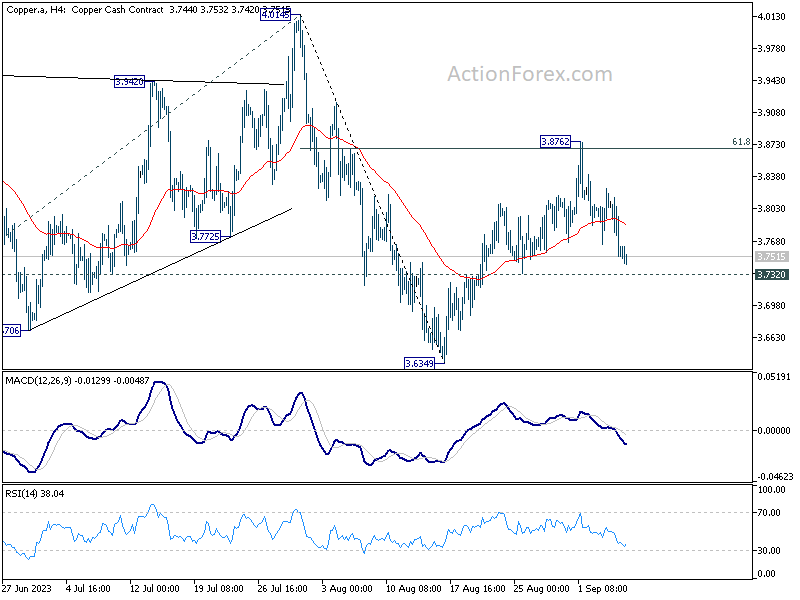

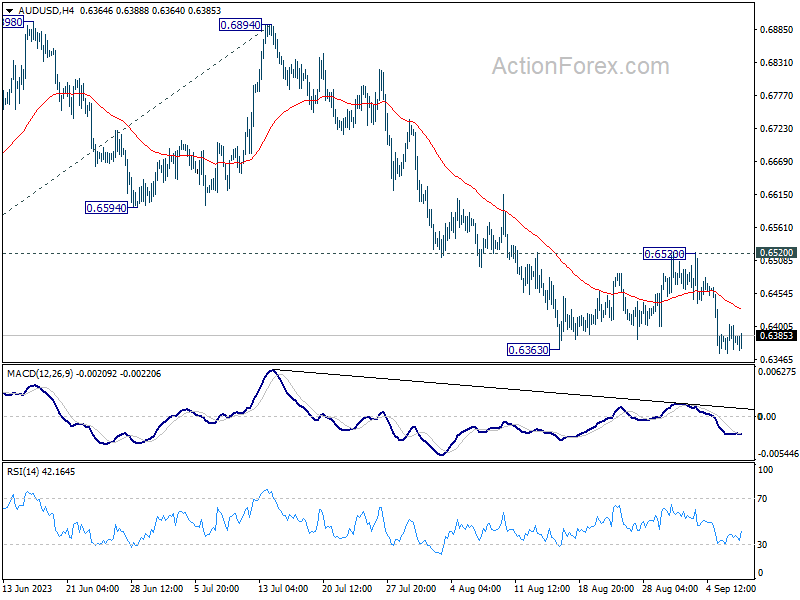

Technically, Copper's rebound from 3.6349 was admittedly stronger than expected. But the rejection by 61.8% retracement of 4.0145 to 3.3649 and the structure still argues that it's a corrective move. Break of 3.7320 support will indicate that fall from 4.015 is ready to resume through 3.6349. If realized, AUD/USD might follow and have enough momentum to move away from 0.6363 support finally.

In Asia, Nikkei closed down -0.73%. Hong Kong HSI is down -1.24%. China Shanghai SSE is down -1.06%. Singapore Strait Times is down -0.22%. Japan 10-year JGB yield is up 0.0042 at 0.660. Overnight, DOW dropped -0.57%. S&P 500 dropped -0.70%. NASDAQ dropped -1.06%. 10-year yield rose 0.022 to 4.290.

BoJ Nakagawa sees positive developments, but loose monetary policy still needed

BoJ Board member Junko Nakagawa struck a cautiously optimistic tone today about the Japanese economy, citing "positive developments" and "signs of change in corporate price and wage-setting behavior."

However, she was quick to note that the country has not yet achieved its price target "in a stable, sustainable fashion."

Nakagawa noted that there are chances inflation could accelerate beyond initial expectations. However, she also warned of the potential for inflation to decelerate once the pass-through effects of higher costs begin to moderate.

The policymaker underscored the need for BoJ to maintain its ultra-loose monetary policy for the time being, citing the prevailing economic uncertainty.

RBA Lowe cautions against complacency in managing inflation risks

In his final public speech as RBA Governor, Philip Lowe stated that for inflation to average around 2.5%, wage increases should typically align with productivity growth plus an additional 2.5%. He sees it as a "reasonable benchmark", even it's "not a hard and fast rule".

Lowe's recent attention has been particularly focused on the risk associated with the current period of high inflation. Specifically, he warned of the peril that "wages growth and profits running ahead of the rate that is consistent with a sustainable return of inflation to target."

In such a scenario, he cautioned, inflation would become "sticky," necessitating "tighter monetary policy and more economic pain later on."

Lowe acknowledged that recent data offers some level of comfort but emphasized the importance of remaining alert to these inflation risks. Rise in productivity growth, he noted, would be a welcome development as it would facilitate stronger growth in both nominal and real wages and profits.

China's exports and imports continue to contract, Yuan weakness persists

In August, China reported a fourth consecutive monthly contraction in exports, dropping -8.8% yoy to USD 284.9B. However, the contraction was narrower than market's expectation of a -9.5% yoy decline and an improvement from July's -14.5% yoy fall.

Imports also shrank by -7.3% yoy to USD 216.5B, beating expectations of -9.4% yoy decline and improving from July's -12.4% yoy drop. This marks a consistent trend of contracting imports every month in 2023 compared to the year-ago period.

Despite these figures beating expectations, trade surplus shrank from USD -80.6B to USD -68.4B, almost in line with expectation of USD -60.0B.

While the narrowing contraction in exports and imports could be seen as a mildly positive development, it doesn't significantly alter the broader narrative of economic cooling in China.

Offshore Chinese Yuan continued its decline today, sparking questions about the timing and intent of potential interventions by Chinese authorities.

USD/CNH's correction from 7.3491 should have completed at 7.2387 already. Rise from there is likely resuming the larger up trend 6.6971. From a pure technical perspective, USD/CNH should be ready to rise through 7.3745 (2022 high) to 61.8% projection of 6.8100 to 7.2853 from 7.1154 at 7.4091.

However, this raises two crucial questions: when will the Chinese authorities step in to intervene in the currency markets, and what will be the nature of such intervention—i.e., whether they aim to set a floor for Yuan or merely slow its depreciation.

Looking ahead

Swiss foreign currency reserves, France trade balance, Italy retail sales, and Eurozone GDP revision will be release in European session.

Later in the day, Canada building permits and Ivey PMI, US jobless claims and non-farm productivity will be featured.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6358; (P) 0.6382; (R1) 0.6405; More...

Intraday bias in AUD/USD stays mildly on the downside for the moment. Current decline is part of the whole fall from 0.7156, next target is 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195. On the upside, break of 0.6520 resistance is needed to indicate short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

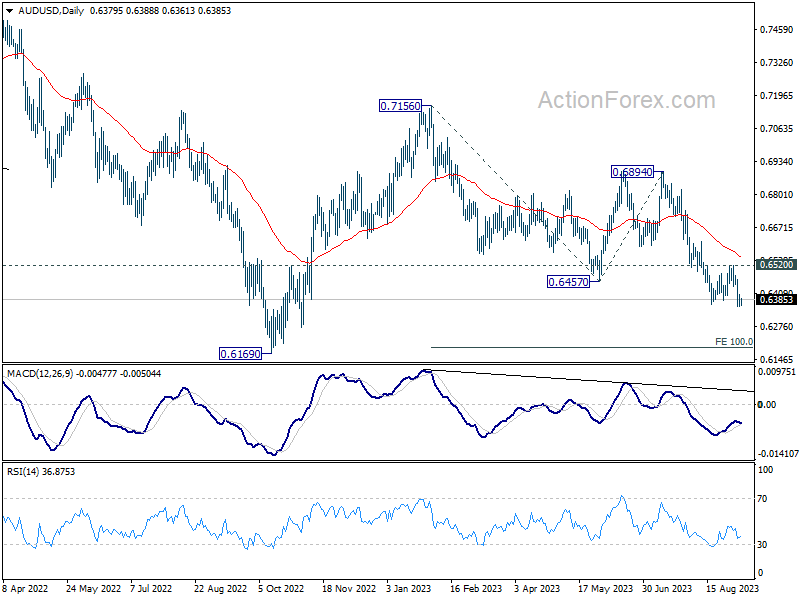

In the bigger picture, current development argues that the down trend from 0.8006 (2021 high) is still in progress. Decisive break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Manufacturing Sales Q2 | 0.20% | -2.80% | -2.50% | |

| 01:30 | AUD | Trade Balance (AUD) Jul | 8.04B | 10.05B | 11.32B | 10.27B |

| 03:00 | CNY | Trade Balance (USD) Aug | 68.4B | 68.0B | 80.6B | |

| 03:00 | CNY | Trade Balance (CNY) Aug | 488B | 494B | 576B | |

| 05:00 | JPY | Leading Economic Index Jul P | 107.6 | 107.9 | 109.1 | |

| 05:45 | CHF | Unemployment Rate Aug | 2.10% | 2.10% | 2.10% | |

| 06:00 | EUR | Germany Industrial Production M/M Jul | -0.80% | -0.40% | -1.50% | |

| 06:45 | EUR | France Trade Balance (EUR) Jul | -6.8B | -6.7B | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) Aug | 698B | |||

| 08:00 | EUR | Italy Retail Sales M/M Jul | 0.20% | -0.20% | ||

| 09:00 | EUR | Eurozone GDP Q/Q Q2 | 0.30% | 0.30% | ||

| 12:30 | CAD | Building Permits M/M Jul | 7.50% | 6.10% | ||

| 12:30 | USD | Initial Jobless Claims (Sep 1) | 235K | 228K | ||

| 12:30 | USD | Nonfarm Productivity Q2 | 3.50% | 3.70% | ||

| 12:30 | USD | Unit Labor Costs Q2 | 1.80% | 1.60% | ||

| 14:00 | CAD | Ivey PMI Aug | 49.2 | 48.6 | ||

| 14:30 | USD | Natural Gas Storage | 38B | 32B | ||

| 15:00 | USD | Crude Oil Inventories | -1.8M | -10.6M |

Uncomfortably Strong US Outlook

Eurozone services PMI were disappointing in August, yet the ISM services index printed its strongest expansion across the Atlantic Ocean. The US ISM services index flirted with 55; employment, new orders, and ISM prices also showed significant progress last month. The strong ISM data bolstered the speculation that the Federal Reserve (Fed) could opt for another rate hike before the year end and keep the rates at restrictive levels for longer. The US 2-year yield advanced above 5%, the 10-year yield is around the 4.30% mark. Oh, and by the way, the US yield curve has been inverted since more than a year, but the resilience of the US economy continues surprising, and recession is nowhere around (at least in the data).

The US dollar index extends gains toward the 105 level. At 105.40, traders will decide whether the dollar deserves to reverse its yearly bearish trend, and step into a medium-term bullish configuration. Even though Fed’s Waller sounded happy and satisfied with last week’s weakish economic data – both for inflation and jobs – James Bullard said that the Fed should stick with a plan of one more hike this year. Maybe in November? For now, the market is positioned for no rate hike this year, but strong data and rising oil prices could change that expectation in the next few weeks. There is a growing chatter that the Fed could double its growth projection when it publishes an updated outlook later this month. I hope for the rest of the world that that does not happen!

Oil consolidates gains

Brent consolidates gains above $90pb, and US crude is at $87pb with little conviction from the bears to counter the positive trend after the latest API data showed around 5.5-mio-barrel fall in US inventories last week.

The US dollar’s appreciation adds an additional layer of complexity for the rest of the world, as not only crude prices rise, but the US dollar used to trade oil gains in value as well. Big Asian economies are reacting to the US dollar’s renewed strength. China defends its yuan by offering forceful guidance with its daily reference rate, while the Japanese issued a strong warning this week, threatening investors that if the USDJPY continued to rise, they would intervene. But in vain, the USDJPY 147.80 and consolidates above 147.50 this morning. However, the upside potential is clearly limited as the Japanese have been vocal about the fact that they won’t let the dollar-yen hit 150.

Elsewhere, the USDCAD advanced to the highest levels since March as the Bank of Canada (BoC) kept its policy rate unchanged at 5% as expected, Cable slipped below 1.25, while the selloff in the EURUSD slowed into the 1.07 support. What’s next? The European Central Bank (ECB) doves may have gotten ahead of themselves on the back of the recent weakness in economic data, but the fact that the softness in inflation is at jeopardy means that an ECB pause this month is not warranted. ECB’s Knot said that the markets are underestimating the chance of a rate hike next week. He reminded that a rate hike is ‘still a possibility’, just not a ‘certainty’. Peter Kazimir also said that one more rate hike should happen in Europe. Yes, the 11% slump in German exports make the ECB hawks sound less powerful, but you must keep somewhere in the back of your mind that economic weakness is needed to slow inflation – at least this is what the theory tells – therefore, the ECB hawks will fight for their last 25bp hike this month.

iPhones banned in Chinese offices

The S&P500 didn’t like the rising US yields and slipped below the 4500 level and the 50-DMA yesterday. Nasdaq 100 also fell 0.88%, as Apple dived more than 3.50% on a report that the Chinese government agencies banned staff from bringing iPhone and other foreign-branded devices into the office. This is now something new, the government employees were always expected not to bring iPhones to the office since the Trump-era trade war. But the news was perceived as further escalation of technology war between the US and China, amid other news including Huawei unveiling a new phone that is powered by a chip ‘that appears to be the most advanced version of China’s homegrown technology to date’ – as a demonstration of power that the US’ chip export ban is not holding the Chinese companies back from progressing. And the announcement came in the middle of US commerce secretary’s goodwill tour in China. Released this morning, Chinese trade data confirmed a 4th consecutive month of drop in Chinese exports. Although the drop itself was lower than expected, China’s share of US imports fell to the lowest levels since 2006.

Strong ISM Data Highlights Resilient US Economy

Market movers today

The most important data release today is the euro area wage figures (compensation per employee) for Q2 2023. This is ECBs favourite wage measure and today's release is the last important data point before the ECB monetary policy meeting next Thursday.

Compensation per employee rose markedly in Q1 at 5.4% y/y, which was well above ECB Chief Economic Lane's previous (rough) estimate of 3% being the level corresponding to the inflation target. We have already received Q2 wage figures from the euro area countries where wage growth slowed in France, Italy and Spain but increased in Germany compared to the first quarter. In the latest projection from June, the ECB expected compensation per employee to average 5.3 in 2023.

We also get the final euro area 2023 Q2 national account figures. GDP rose 0.3% q/q according to the first estimate and we expect the final data to confirm this. The final data will reveal a breakdown of the GDP figures, which will give interesting insights into the growth composition.

The 60 second overview

Stronger-than-expected ISM services for august reaffirmed the US outperformance narrative, adding broad support to the USD. US ISM services for August printed at 54.5, the highest reading since February with business activity, price pressures and employment growth picking up. Consensus was anticipating ISM Services to signal weakening growth, but the surprising pick-up was broad-based across different sub-indices, with both current and future activity indicators signalling accelerating growth. Markets reacted by sending 2-year US Treasury yield 4-5bp higher and US stocks lower. While we highlight the volatility in ISM figures, we note that it is a clear signal that the US is not on the brink of a recession at least for now.

Bank of Canada (BoC) left policy rates unchanged as widely expected at yesterday's interim meeting. The BoC acknowledged that excess demand is easing but kept the open door for additional hikes if needed as it highlighted concerns of persistence in underlying inflation pressures. Overall, the communication was on the hawkish side with the BoC noting that there was "little recent downward momentum in underlying inflation" and that there is "risk that elevated inflation becomes entrenched".

Overnight, Chinese trade data for August came in close to expectation. Exports came in at -8.8% y/y (cons: 9.0%, prior: -14.5%) and imports slightly better than expected -7.3% y/y (cons: 9.0%, prior: -12.5%), In China, focus remains on the property sector and the faltering recovery, and while the big property developer Country Garden has avoided a default for now, the property sector remains a key source of strain on the economy.

Equities: Global equities lower yesterday with Japanese stocks being the bright spot. We saw a very interesting sentiment shift at 16:00 CET when US Non-Manufacturing data came out much stronger than expected and was showing the opposite picture of service PMIs. Yields were clearly higher on the number and equities lower. The worst performing sectors were tech, growth, and long duration stocks while defensives, insurance, and energy outperformed. In US yesterday, Dow -0.6%, S&P500 -0.7%, Nasdaq -1.1% and Russell 2000 -0.3%. Asian markets are lower this morning and the same goes for futures in the US and Europe.

FI: European yields rose across the board, led by the front end. Shorter-dated EGB yields rose through the day driven by hawkish ECB comments in the morning and the move was accelerated by surprisingly strong US ISM services release in the afternoon. In the end, the front end led sell-off saw 2y Germany up by almost 9bp on the day to above 3%. Intra-euro area spreads were relatively stable yesterday. Markets added 2bp to the September pricing (to 9bp), but took out 6bp of rate cuts in 2024 (to -63bp).

FX: EUR/USD remained in the 1.0700-1.0750 range during yesterday's session. Stronger-than-expected ISM services reaffirmed the US outperformance narrative, adding broad support to the USD. Despite the rise in Brent crude oil prices to levels above 90 USD/bbl NOK has done very little this week with EUR/NOK still trading around the 11.50 mark. EUR/GBP moved back closer to the 0.86 mark on dovish BoE remarks.

Credit: Risk-off hit markets on Wednesday, dragging down credits along with equities. Itrax Main widened 1.9bp to close at 71.8bp, while Itrax Xover widened 8.9bp to close at 402.2bp. Assa Abloy's three tranche EUR benchmark deal hit primary markets on Wednesday, with the 'A-' rated lock-maker ending up printing EUR1.8bn on very strong demand.

China’s exports and imports continue to contract, Yuan weakness persists

In August, China reported a fourth consecutive monthly contraction in exports, dropping -8.8% yoy to USD 284.9B. However, the contraction was narrower than market's expectation of a -9.5% yoy decline and an improvement from July's -14.5% yoy fall.

Imports also shrank by -7.3% yoy to USD 216.5B, beating expectations of -9.4% yoy decline and improving from July's -12.4% yoy drop. This marks a consistent trend of contracting imports every month in 2023 compared to the year-ago period.

Despite these figures beating expectations, trade surplus shrank from USD -80.6B to USD -68.4B, almost in line with expectation of USD -60.0B.

While the narrowing contraction in exports and imports could be seen as a mildly positive development, it doesn't significantly alter the broader narrative of economic cooling in China.

Offshore Chinese Yuan continued its decline today, sparking questions about the timing and intent of potential interventions by Chinese authorities.

USD/CNH's correction from 7.3491 should have completed at 7.2387 already. Rise from there is likely resuming the larger up trend 6.6971. From a pure technical perspective, USD/CNH should be ready to rise through 7.3745 (2022 high) to 61.8% projection of 6.8100 to 7.2853 from 7.1154 at 7.4091.

However, this raises two crucial questions: when will the Chinese authorities step in to intervene in the currency markets, and what will be the nature of such intervention—i.e., whether they aim to set a floor for Yuan or merely slow its depreciation.

RBA Lowe cautions against complacency in managing inflation risks

In his final public speech as RBA Governor, Philip Lowe stated that for inflation to average around 2.5%, wage increases should typically align with productivity growth plus an additional 2.5%. He sees it as a "reasonable benchmark", even it's "not a hard and fast rule".

Lowe's recent attention has been particularly focused on the risk associated with the current period of high inflation. Specifically, he warned of the peril that "wages growth and profits running ahead of the rate that is consistent with a sustainable return of inflation to target."

In such a scenario, he cautioned, inflation would become "sticky," necessitating "tighter monetary policy and more economic pain later on."

Lowe acknowledged that recent data offers some level of comfort but emphasized the importance of remaining alert to these inflation risks. Rise in productivity growth, he noted, would be a welcome development as it would facilitate stronger growth in both nominal and real wages and profits.

BoJ Nakagawa sees positive developments, but loose monetary policy still needed

BoJ Board member Junko Nakagawa struck a cautiously optimistic tone today about the Japanese economy, citing "positive developments" and "signs of change in corporate price and wage-setting behavior."

However, she was quick to note that the country has not yet achieved its price target "in a stable, sustainable fashion."

Nakagawa noted that there are chances inflation could accelerate beyond initial expectations. However, she also warned of the potential for inflation to decelerate once the pass-through effects of higher costs begin to moderate.

The policymaker underscored the need for BoJ to maintain its ultra-loose monetary policy for the time being, citing the prevailing economic uncertainty.

Crude Oil Price Rally Could Extend To $90

Key Highlights

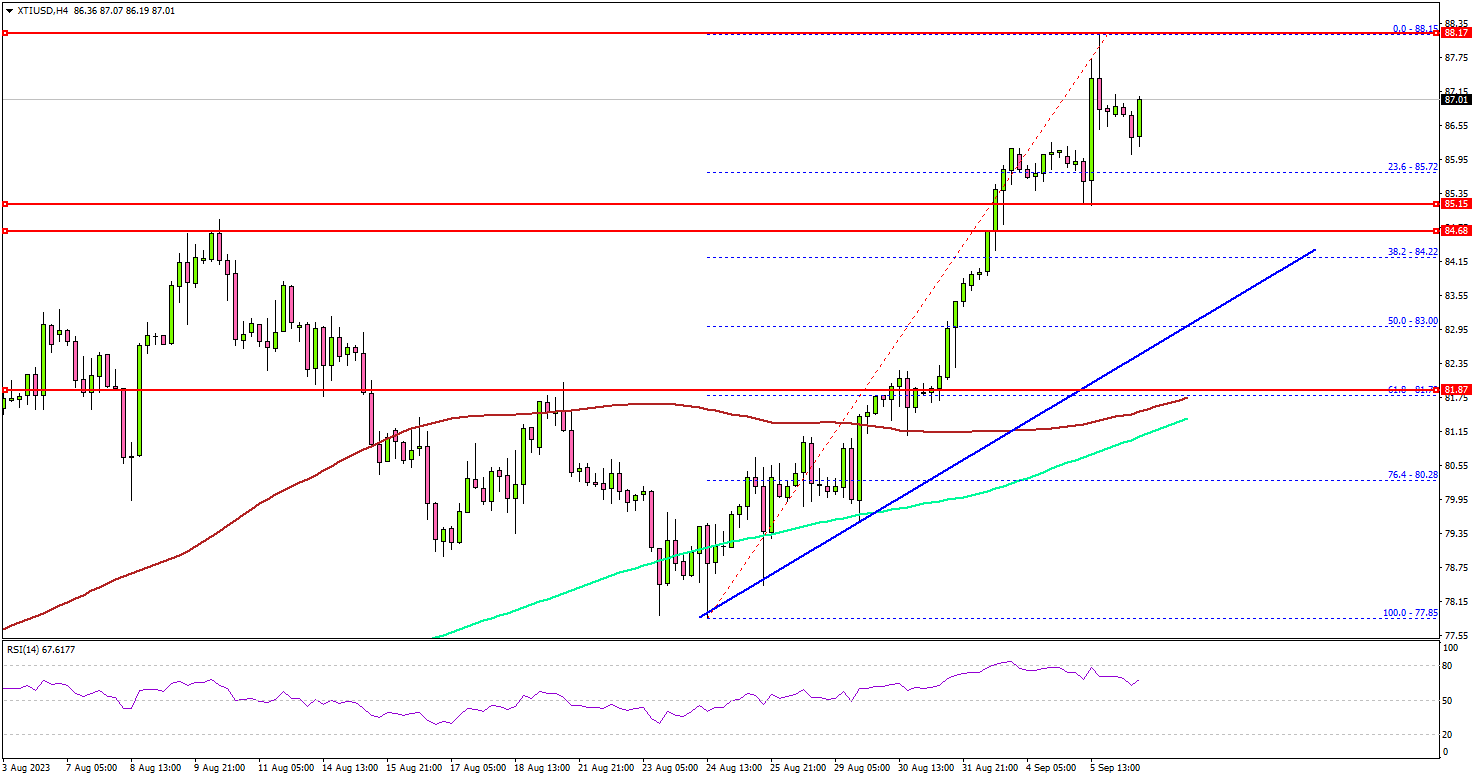

- Crude oil price is rising above the $84 and $85 resistance levels.

- A key bullish trend line is forming with support near $84.20 on the 4-hour chart.

- Gold prices might find a strong buying interest near $1,915.

- EUR/USD is consolidating losses below 1.0780.

Crude Oil Price Technical Analysis

Crude oil price started a steady increase after a close above $80 against the US Dollar. The price rallied above the $82 and $84 resistance levels.

Looking at the 4-hour chart of XTI/USD, the price surpassed $85 and settled above the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

Finally, it tested the $88.00 resistance zone. Recently, there was a minor downside correction below the $87 level. However, the bulls seem to be active above the $85.80 level. The 23.6% Fib retracement level of the upward move from the $77.85 swing low to the $88.15 high is also near $85.75.

The next major support sits near the $84.00 zone. There is also a key bullish trend line forming with support near $84.20 on the same chart.

Any more losses might call for a test of the $82 support zone in the coming days. On the upside, the price might face resistance near the $88 level. The next major resistance is near the $88.80 level, above which the price may perhaps accelerate higher. In the stated case, it could even visit the $90 resistance.

Looking at gold prices, there was a downside correction below the $1,930 level but the bulls might be active near $1,915.

Economic Releases to Watch Today

- Euro Zone Gross Domestic Product for Q2 2023 (QoQ) - Forecast 0.3%, versus 0.3% previous.

- Euro Zone Gross Domestic Product for Q2 2023 (YoY) - Forecast 0.6%, versus 0.6% previous.

- US Initial Jobless Claims - Forecast 234K, versus 228K previous.

Nikkei Futures (NKD) Looking to Extend Higher as an Impulse

Short term Elliott Wave view in Nikkei Futures (NKD) suggests the Index rallies as a 5 waves impulse structure from August 18, 2023 low. Up from August 18, wave ((i)) ended at 32285 and pullback in wave ((ii)) ended at 31555 as the 1 hour chart below shows. Up from wave ((ii)), wave i ended at 31850 and dips in wave ii ended at 31620. Index resumed higher in wave (iii) towards 32375 and wave iv ended at 32150. Final leg wave v ended at 32560. This completed wave (i) in higher degree.

Pullback in wave (ii) ended at 32200 and the Index then resumed higher in wave (iii) towards 33280. Dips in wave (iv) ended at 33015 as expanded flat. Expect the Index to end wave (v) of ((iii)) soon. Afterwards, it should pullback in wave ((iv)) to correct cycle from August 25 low before the rally resumes. Typically wave ((iv)) should pullback somewhere around 23.6 – 38.2 Fibonacci retracement of wave ((iii)). Near term, as far as pivot at 31549 low stays intact, expect wave ((iv)) pullback to find support in 3, 7, 11 swing for more upside in wave ((v)).

Nikkei Futures (NKD) 60 Minutes Elliott Wave Chart

Nikkei Elliott Wave Video

https://www.youtube.com/watch?v=tCi3ebXCcpo

GBP/USD – Sinks to Three-Month Low after BoE Monetary Policy Report Hearing

- Dovish BoE commentary weighs on the pound

- Two more rate hikes are still heavily priced in

- Major support below around the 200/233-day SMA band

The monetary policy report hearing can often be a much-hyped but ultimately anti-climactic event, with policymakers sticking to the script whenever possible and the Treasury Select Committee frequently blurring the lines between politics and central banking.

While that was probably largely true today, it was interesting that Governor Bailey and his colleagues share the view that there is no pre-determined outcome at the next meeting – hike or no hike – which isn’t something that can be said over much of the last couple of years.

A rate hike is still extremely likely at the next meeting on 21 September (82.8% priced in) and one more is still almost fully priced in, which is arguably a surprise based on today’s comments.

BoE Interest Rate Probabilities

Source – Refitiv Eikon

Sterling slides after dovish commentary

The pound clearly responded to the comments during the hearing, slipping against the dollar to a three-month low.

GBPUSD Daily

Source – OANDA on Trading View

What’s more, that was seemingly backed by momentum, with the stochastic and MACD both recording lower lows at the same time. It also confirmed the rebound off the 55/89-day simple moving average band last week which looked quite a bearish move at the time.

The focus now is on the 200/233-day SMA band, a break of which would further solidify the bearish appearance in the pair. This falls around 1.23-1.24, around the May lows and an area that was firm support in the second quarter of the year.