Sample Category Title

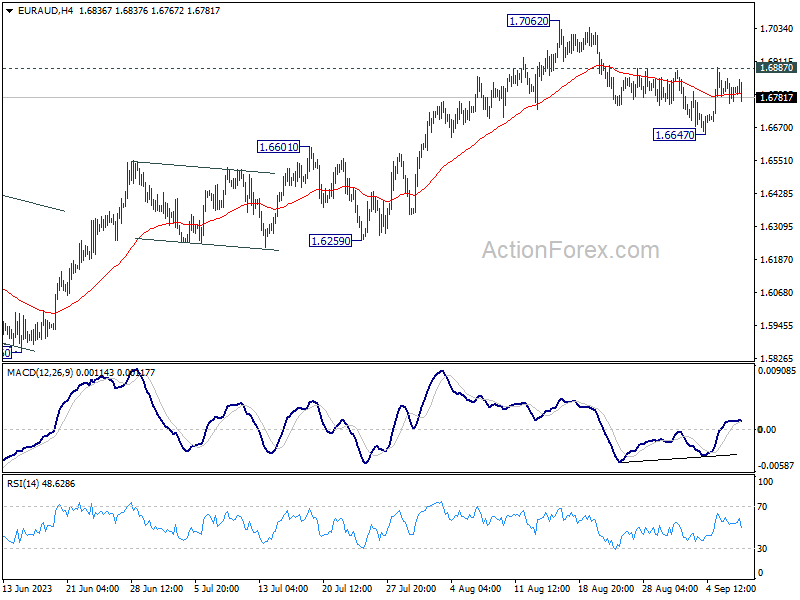

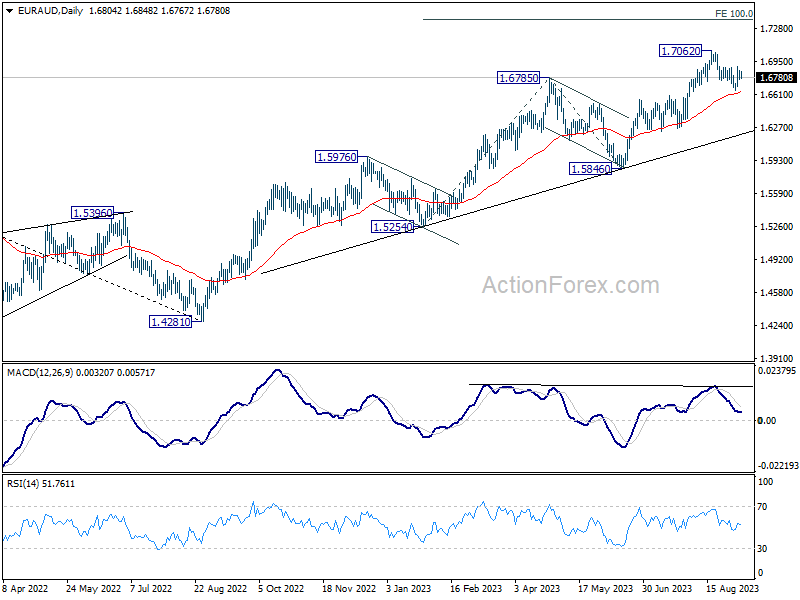

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6760; (P) 1.6807; (R1) 1.6853; More...

Intraday bias in EUR/AUD remains neutral at this point. On the upside, firm break of 1.6887 resistance should confirm that correction from 1.7062 has completed at 1.6647. Further rally should be seen through 1.7062 to 1.7377 projection level. On the downside, break of 1.6647 will extend the correction lower instead.

In the bigger picture, the rise from 1.4281 (2022 low) is in progress. Next target is 100% projection of 1.5254 to 1.6785 from 1.5846 at 1.7377. For now, outlook will stay bullish as long as 1.5846 support holds, even in case of deep pull back.

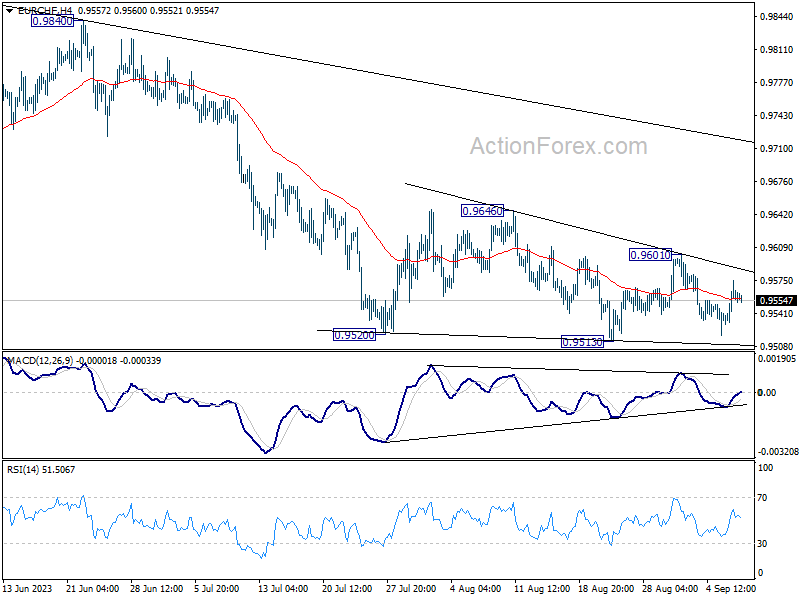

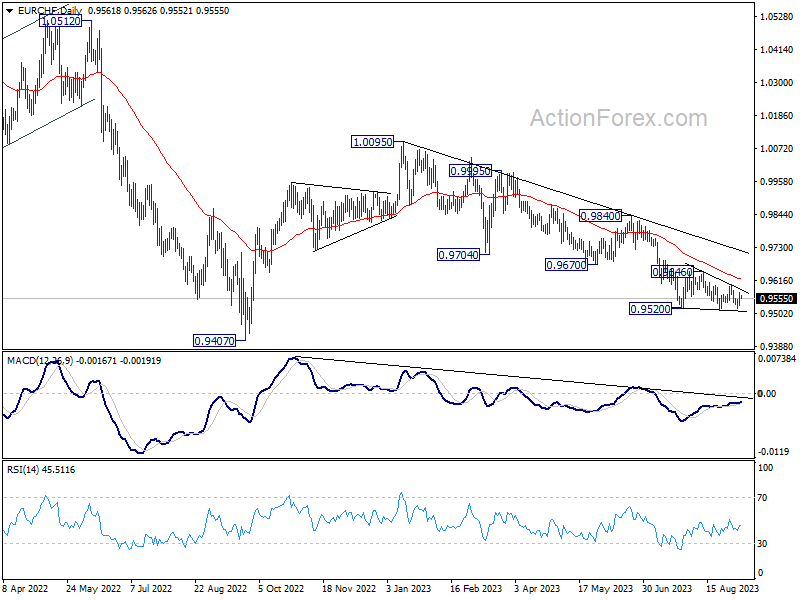

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9535; (P) 0.9556; (R1) 0.9579; More...

Range trading continues in EUR/CHF and intraday bias stays neutral for the moment. With 0.9601 resistance intact, larger down trend is still in favor to continue. On the downside, break of 0.9513 support will confirm this bearish case and target 0.9407 low. Nevertheless, break of 0.9601 resistance will turn bias back to the upside for stronger rebound to 0.9646 resistance and above.

In the bigger picture, medium term outlook is staying bearish as the pair is capped well below falling 55 W EMA (now at 0.9839). Down trend from 1.2004 (2018 high) is in favor to continue. Sustained break of 0.9407 will target 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. For now, this will remain the favored case as long as 0.9670 support turned resistance holds, in case of strong rebound.

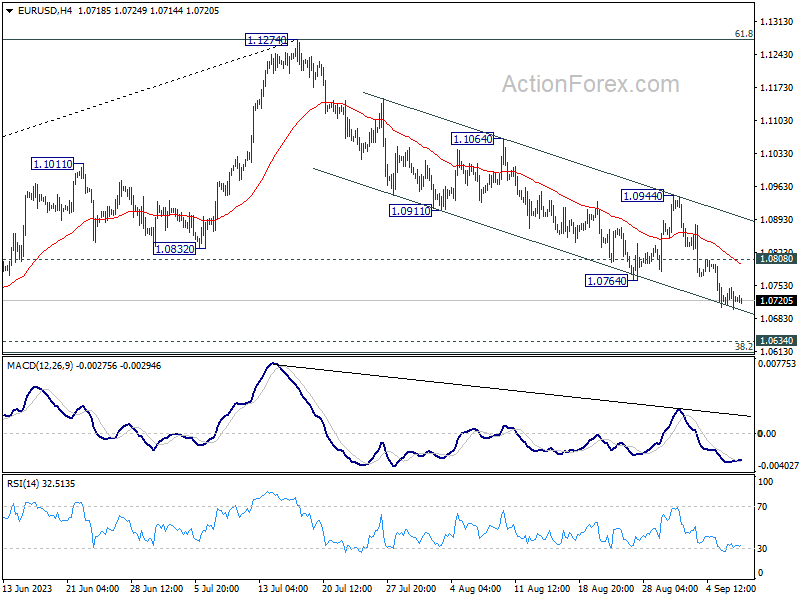

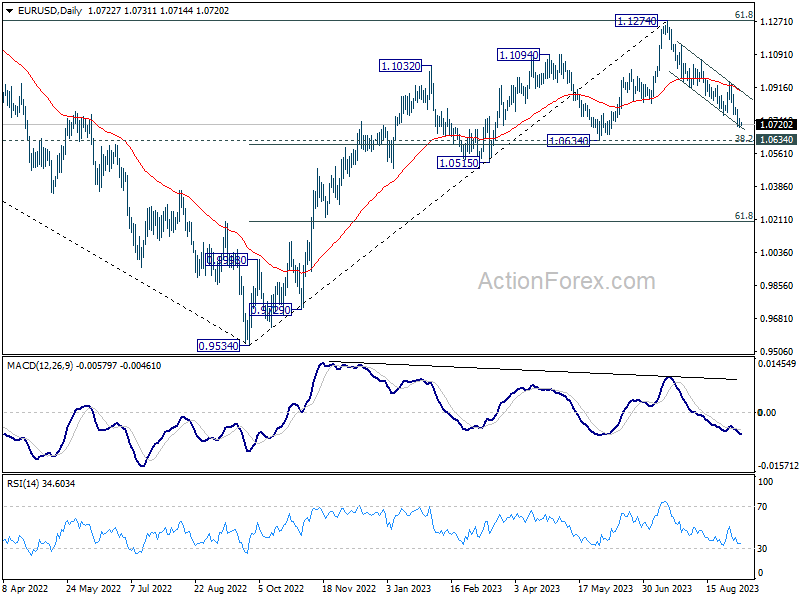

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0703; (P) 1.0726; (R1) 1.0749; More...

Intraday bias in EUR/USD stays on the downside for the moment. Deeper decline would be seen to 1.0609/34 cluster support next. On the upside, above 1.0808 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.0944 resistance holds, in case of recovery.

In the bigger picture, fall from 1.1274 medium term top is seen as a correction to up trend from 0.9534 (2022 low). Deeper decline would be seen to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to bring rebound. Yet, medium term outlook will be neutral for now, as long as 1.1274 resistance holds. However, sustained break of 1.0609/34 will raise the chance of bearish trend reversal, and target 61.8% retracement at 1.0199.

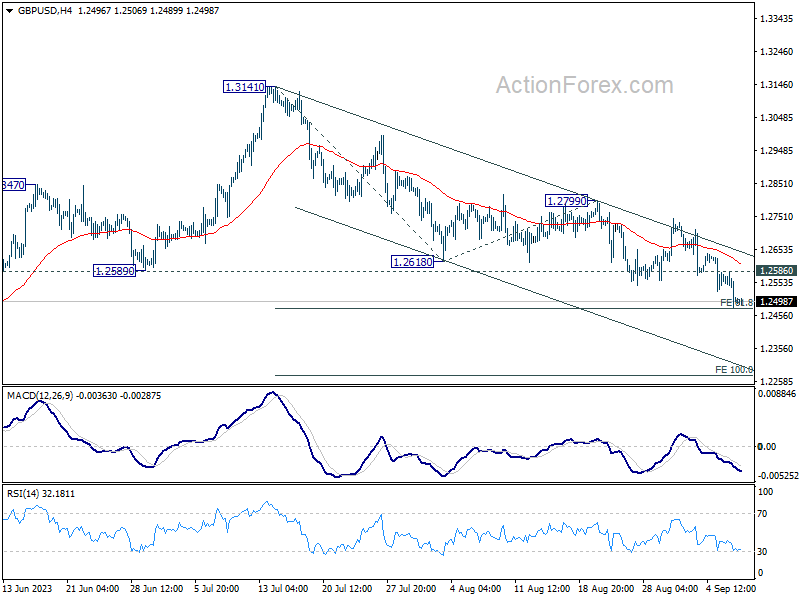

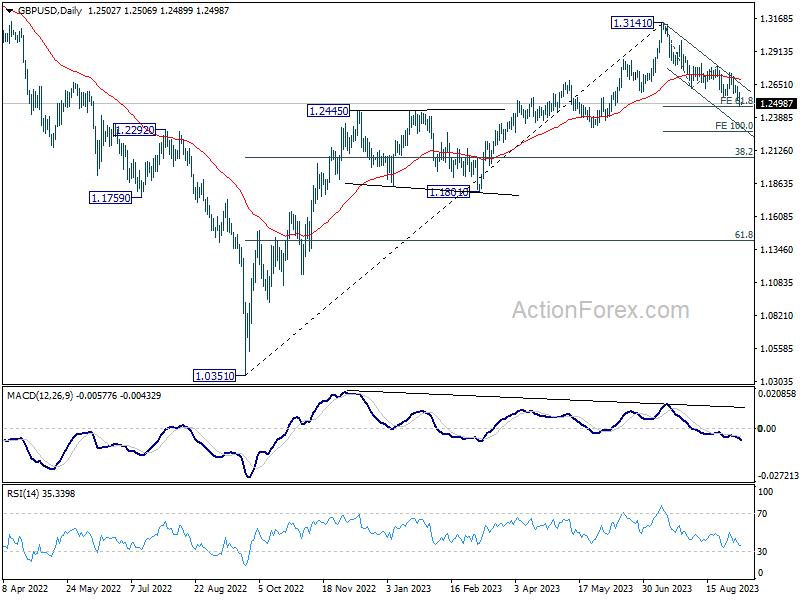

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2463; (P) 1.2526; (R1) 1.2569; More...

Intraday bias in GBP/USD stays on the downside at this point. Firm break of 61.8% projection of 1.3141 to 1.2618 from 1.2799 at 1.2476 could prompt downside acceleration to 100% projection at 1.2276. On the upside, above 1.2586 minor resistance will turn intraday bias neutral first.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. But outlook will be neutral at best as long as 1.3141 resistance holds, and consolidation from there is set to extend, until further development.

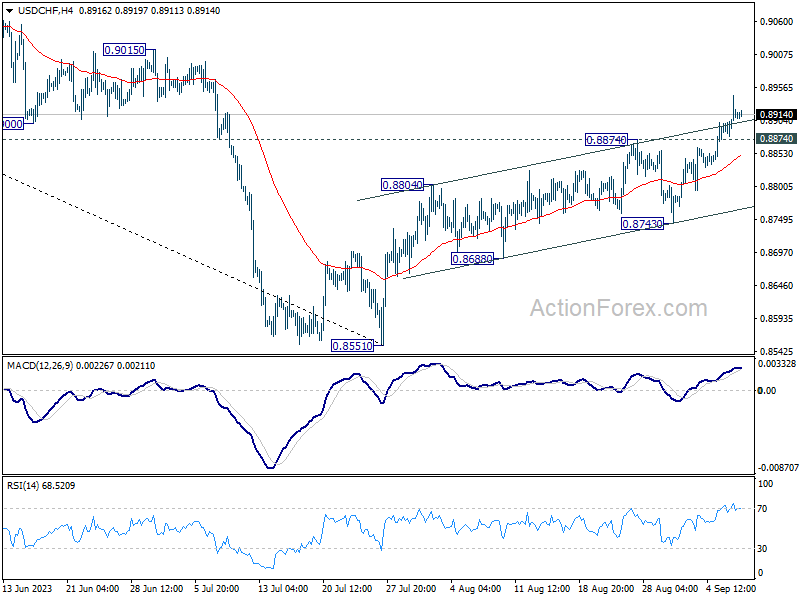

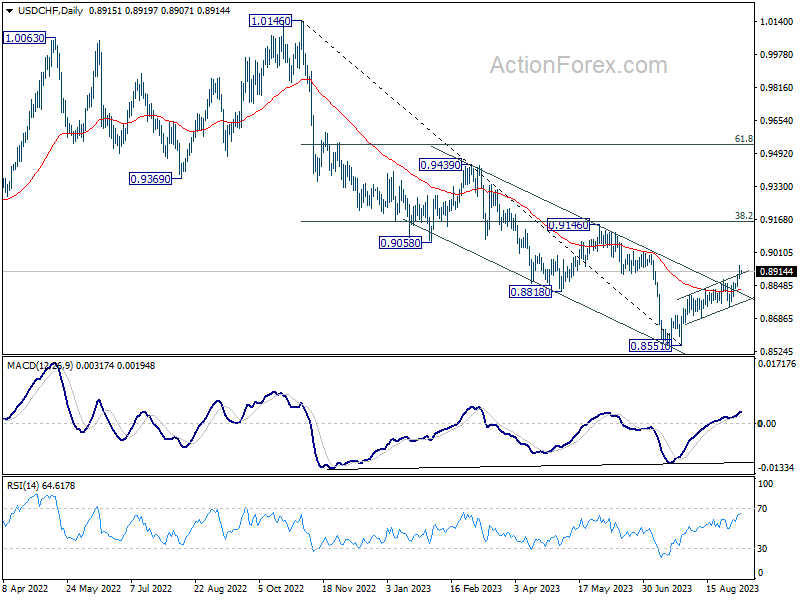

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8880; (P) 0.8912; (R1) 0.8944; More....

Intraday bias in USD/CHF stays on the upside for the moment. Current rise should target 0.9146 cluster resistance next. On the upside, below 0.8874 minor support will turn intraday bias neutral first. But risk will stay on the upside as long as 0.8743 support holds.

In the bigger picture, rebound from 0.8551 medium term bottom is currently seen as a correction to the downtrend from 1.0146 (2022 high). Further rally would be seen to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160). Strong resistance could be seen there to limit upside, at least on first attempt.

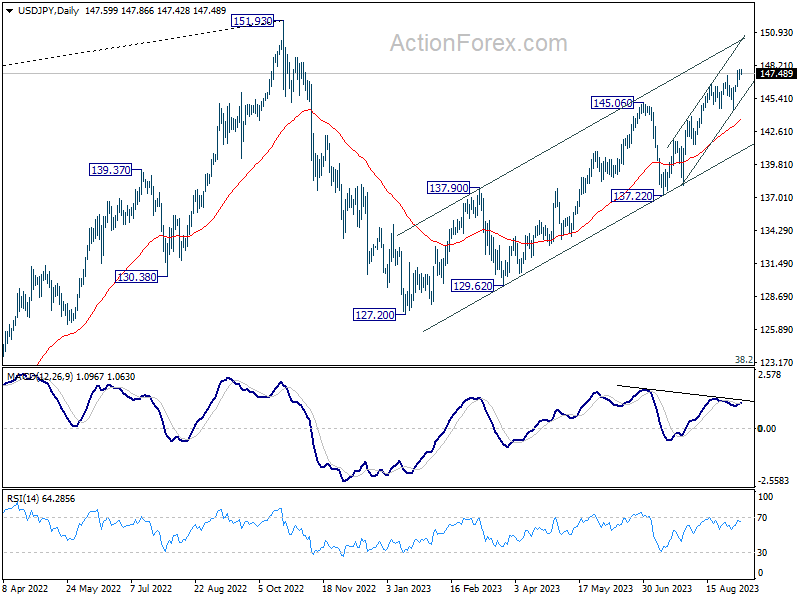

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.19; (P) 147.51; (R1) 147.99; More...

Intraday bias in USD/JPY stays on the upside for the moment. Current rally is part of the whole rise from 127.20, and should target a test on 151.93 high. On the downside, below 146.40 minor support will turn intraday bias neutral first. But near term outlook will stay bullish as long as 144.43 support holds, in case of retreat.

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

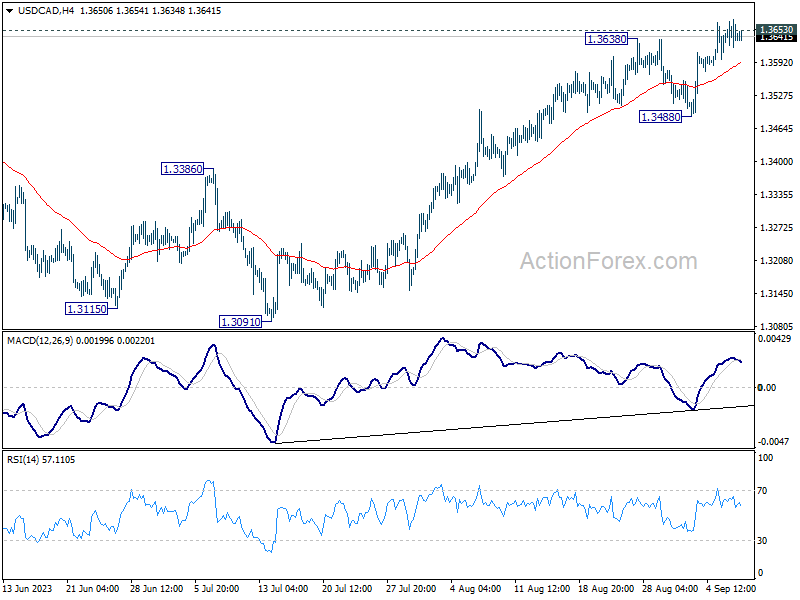

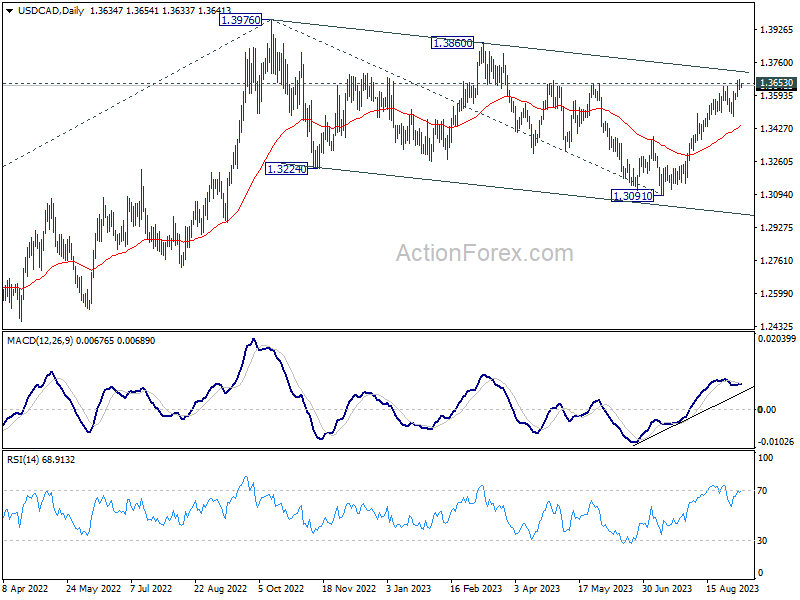

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3613; (P) 1.3645; (R1) 1.3667; More....

Intraday bias in USD/CAD stays on the upside at this point. Sustained break of 1.3653 should confirm that correction from 1.3976 has completed, and target a test on this high. For now, risk will stay on the upside as long as 1.3488 support holds, in case of retreat.

In the bigger picture, price actions from 1.3976 are viewed as a corrective pattern only. Upon completion, rise from 1.2005 (2021 low) would resume through 1.3976. Next target is 61.8% projection of 1.2005 to 1.3976 from 1.3091 at 1.4309. For now, this will remain the favored case as long as 55 D EMA (now at 1.3436) holds.

Nikkei 225 Technical: Bullish Breakout from 2-month Descending Range

- The Japanese Nikkei 225 has outperformed the rest of the world for the dreaded month of August where most global benchmark stock indices recorded their worst losses in three months.

- Since its 18 August 2023 low, it has recorded a gain of 6.1% as of yesterday, 6 September.

- 33,000 is the key short-term support to watch.

The price actions of the Japan 225 (JPY) Index (a proxy of the Nikkei 225 futures) have staged the expected rebound right above the 31,130 key medium-term support as highlighted in the prior report and hit the 32,810 resistance on 30 August 2023.

Thereafter, it continued to rally and staged a bullish breakout from a two-month descending range (“bullish flag” from 16 June 2023 high of 34,015) yesterday, 6 September within a major uptrend phase in place since 3 January 2023 low of 25,585.

All in all, it has gained by +6.1% from its 18 August 2023 swing low to yesterday’s 6 August US session close of 33,148. Also, for the dreaded month of August that negatively impacted almost all major benchmark stock indices, the Nikkei 225 cash index has outperformed the rest of the world with a monthly loss of -1.67% versus a wider monthly loss of -2.91% inflicted on the iShares MSCI All World Index exchange-traded fund over the same period.

Let’s now examine what’s in store for the Japan 225 (JPY) Index from the lens of technical analysis.

Medium-term momentum bullish breakout reinforces price actions breakout from 2-month range

Fig 1: Japan 225 medium-term trend as of 7 Sep 2023 (Source: TradingView, click to enlarge chart)

Prior to yesterday’s price actions’ bullish breakout above the descending range resistance, the daily RSI indicator, a gauge of momentum has staged an earlier bullish breakout on 4 September 2023 above its parallel descending resistance.

These observations have indicated the medium-term upside momentum has resurfaced which in turn reduces the odds of a price action’s failure bullish breakout. Hence, it is likely that the Index has kickstarted a potential medium-term impulsive up-move sequence within its major uptrend phase in place since the 3 January 2023 low.

Price actions are retesting the 33,000 pull-back support

Fig 2: Japan 225 minor short-term trend as of 7 Sep 2023 (Source: TradingView, click to enlarge chart)

As seen on the shorter-term 1-hour chart, the price actions of the Japan 225 (JPY) Index have staged a pull-back and retested the former “descending range’ resistance now turns pull-back support at 33,000 which also confluences with the lower boundary of a minor ascending channel from 25 August 2023 low and upward sloping 5-day moving average.

Watch the 33,000 key short-term pivotal support to maintain the potential short-term bullish bias scenario to see the next intermediate resistance coming in at 33,490 (the upper boundary of the minor descending channel & the 1 August 2023 minor swing high) in the first step.

On the other hand, a break below 33,000 negates the bullish tone to expose the 50-day moving average now acting as a support at 32,510.

Dollar in General Trades a Tad Stronger

Markets

Several events coloured trading yesterday. The Polish central bank sent shockwaves through local and neighbouring markets after cutting the policy rate by the 75 bps that no one foresaw. The zloty and rates nosedived. Second: ECB’s Knot and Kazimir seized the final speaking opportunity ahead of the blackout period. The former said markets are underestimating of something happening (i.e. a rate hike) at the September meeting. Kazimir sees the need for one more move and added a September hike is preferable to a later increase. And finally, the US services ISM. The indicator unexpectedly rebounded from 52.7 to 54.5 on a pickup in new orders to an elevated 57.5, a sharp 4 point rise in employment to 54.7 and a high level of business activity (57.3). The prices paid subseries extended a recent revival to 58.9. The outcome supports once more both a final Fed rate increase as well as keeping policy restrictive for a significant period of time even as the Fed’s Beige Book suggested a slowdown in activity and hiring growth. US yields gained between 1.9-6.7 bps with the front underperforming. The 2-y retook the 5% barrier again. The ECB comments helped German yields leave the intraday lows. A second upleg followed in lockstep with the US. Net daily changes varied from 1.6 bps (30-y) to 7.7 bps (2-y). The dollar recouped losses after the ISM. EUR/USD closed at 1.0727, marginally up from 1.072. USD/JPY stabilized near the recent highs around 147.7. That DXY eked out a small gain still (north of the 104.7 resistance) had to do with the dollar appreciating against sterling. GBP/USD fell towards 1.25. Sterling was weak too (see below). EUR/GBP rebounded from 0.8533 to 0.8577.

Stocks yesterday were weighed down by the (real) yield increase (WS down 1% in tech) and sentiment remained grim in Asian dealings. China underperforms, losing about 1%. It’s currency is about to hit a new multi-year low (USD/CNY 7.324). The dollar in general trades a tad stronger. EUR/USD turns south to 1.072. The yen’s safe haven status prevents it from losing further territory. Core bonds trade with a small weakening bias. Today’s economic calendar has dried up. It only contains the US weekly jobless claims. The several ECB speeches due can’t touch on monetary policy. Those scheduled for the Fed may still do as the silence period only kicks in this Saturday. We expect core bond yields to at least hold on to their recent gains in what is probably a technically inspired session. The dollar retains the upper hand against the euro. EUR/USD is developing within a downward trend channel. 1.0635 is the next high profile support zone but without a specific trigger it should survive the day.

News & Views

The Bank of Canada (BoC) yesterday as expected left is policy rate unchanged at 5.0% and continues its quantitative tightening. The BoC saw the economy entering a period of weaker growth needed to slow prices pressures. Growth in the second quarter even turned negative (0.2% QoQa), reflecting a marked weakening in consumption growth and a decline in housing activity, as well as the impact of wildfires. The tightness in the labour market has continued to ease gradually, but wage growth remained around 4% to 5%. Still, the BoC assesses inflation as broad-based. CPI inflation moved back up to 3.3% in July and recent rise in oil prices might keep inflation higher in the short-term. Core inflation is running near 3.5% with little downward momentum recently. The decline in excess demand and assuming still lagging effects of monetary policy filtering through in the economy, the BoC left the rate unchanged. However, the Governing Council remains concerned about the persistence of underlying inflation and is prepared to increase the policy interest rate further if needed. The 2-y Canada government bond yield rose about 5 bps after the policy announcement, but that was mainly due to global factors. Markets still see slightly less than 50% for an additional hike later this year. The loonie closed the session little changed against the dollar (USD/CAD 1.3636).

In a hearing before the Treasury Committee of the UK Parliament, Bank of England Governor Bailey and two other colleagues kept a mild tone on further policy tightening. According to the BoE governor, the bank is near the top of the hiking cycle. Inflation recently has dropped and Bailey indicated that recent indictors are signaling that the fall inflation will continue. He also argued that a substantial amount of transmission still has to come as this process apparently has longer lags than initially expected. The market still sees two additional 25 bps rate hikes going into next year. However, a new 25 bps step at the September 21 meeting is no longer fully discounted. Sterling weakened during the hearing with EUR/GBP jumping back higher to close at 0.8577, up from the 0.8530.

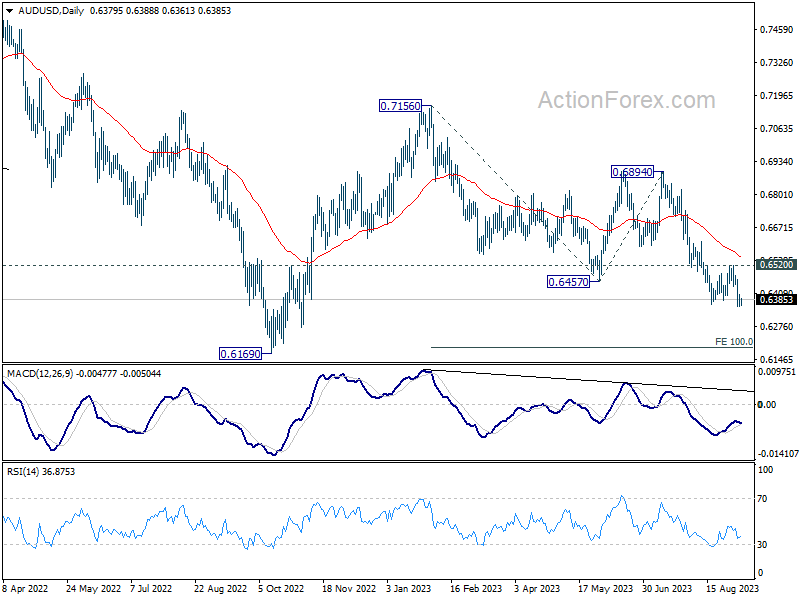

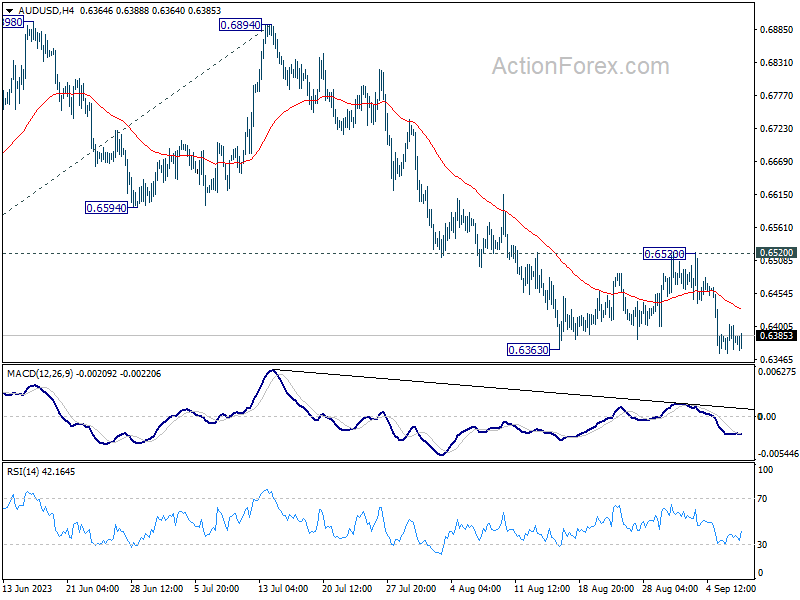

AUD/USD Daily Report

Daily Pivots: (S1) 0.6358; (P) 0.6382; (R1) 0.6405; More...

Intraday bias in AUD/USD stays mildly on the downside for the moment. Current decline is part of the whole fall from 0.7156, next target is 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195. On the upside, break of 0.6520 resistance is needed to indicate short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, current development argues that the down trend from 0.8006 (2021 high) is still in progress. Decisive break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.