Sample Category Title

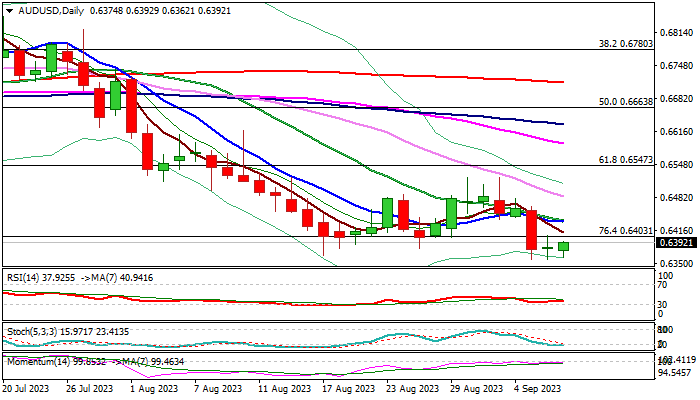

AUD/USD: Bears Pausing After Strong Fall on Tuesday

AUDUSD consolidation extends into second consecutive day, with the action so far holding between new 2023 low (0.6357 and broken Fibo 76.4% (0.6403).

Aussie dollar remains under pressure from firm US dollar, helped by better than expected US services PMI (Wednesday) and weekly jobless claims (today), as well as wide expectations that Fed will keep elevated interest rates for some time.

Unchanged RBA’s monetary policy for the third straight month also made Aussie less attractive for investors.

Near-term action remains weighed by Tuesday’s large bearish daily candle (down 1.2% for the day), along with MA’s in full bearish setup and 14-d momentum holding below the centreline, however, oversold stochastic suggests that the pair may hold in extended consolidation before larger bears resume.

Weekly close below cracked Fibo 76.4% of 0.6170/0.7157 (0.6403) would further strengthen negative structure and risk acceleration towards 0.6272 (3 Nov 2022 trough) and 0.6210 21 Oct low) which guard key support at 0.6170 (2022 low).

Daily Tenkan-sen (0.6439) should ideally cap upticks.

Res: 0.6403; 0.6439; 0.6483; 0.6522

Sup: 0.6357; 0.6272; 0.6210; 0.6170

Sunset Market Commentary

Markets

Markets this week are captured by an (admittedly mild) ‘by default risk-off bias’. The EuroStoxx 50 again cedes 0.35%. S&P opens 0.75% lower. The US being the exception to the rule, forward looking indicators in most major economies point to ongoing sluggish growth. At the same time there are few potential tools to restart a positive growth spiral. Monetary policy in the foreseeable future has to no role play in bailing out growth. In most developed countries this is also the case for fiscal policy. Higher oil prices are at risk of putting an additional burden on demand. China also isn’t in a position to play any role as locomotive for growth as it often did in the past. Today’s downward revision of EMU Q2 growth (from 0.3% Q/Q first estimate to 0.1% Q/Q) definitely is old news, but adds to anecdotic evidence. A lower contribution of net exports highlights the meagre underlying internal growth momentum. US jobless claims was the only ‘timely’ economic data series in for release. The outcome…? You guessed it. Claims declined further from 229k to 216k. It is a minor topic when the Fed will make up its mind on September 20. Next week’s August inflation data have the final say. Even so, it helped to block corrective setback in US yields (currently changing 1-2 bps across the curve). German bonds outperform with yields easing up to 4 bps (5-y). US economic outperformance combined with a risk-off make further USD gains a ‘no-brainer’. DXY jumps north of the 105 big figure. EUR/USD is at risk of losing 1.07. A bit remarkable, USD/JPY (147.17) fails to sustainably break recent peak levels in the 147.80 area. A soft BoE Decision Maker Panel survey (cf infra) triggered further Gilt outperformance. EUR/GBP briefly tested the 0.86 area, but with no follow-through gains yet (0.8584 currently).

In Central Europe, investors are still trying to assess the impact of yesterday’s ‘unthinkable’ 75 bps rate cut of the National Bank of Poland (NBP). The zloty is ceding further ground as NBP governor Glapinski defends its move at the press conference. EUR/PLN jumps to 4.62 from 4.57 this morning. The fall-out on other currencies in the region is a bit mixed. Maybe a bit surprising, the Czech krona is feeling a bigger impact compared to the Hungarian forint. At EUR/CZK 24.39, the Czech currency is testing the weakest levels since December last year. The forint shows better resilience with EUR/HUF returning below to 390 mark (EUR/HUF 387.75). For now, the NBP rate cut didn’t change expectations on the MNB’s or CNB’s policy trajectory for the remainder of this year in a profound way (CNB first 25 bps rate cut in Q4, MNB policy rate near 11.00% year-end). It's a bit contradictory, but any further currency losses due to the NBP decision only complicates any MNB and CNB easing, as it might revive imported inflation.

News & Views

In the Bank of England’s monthly survey, UK companies in August said they expect to raise output prices by 4.4% over the next year. That’s down from 5.5% in July and sharply lower than the 6.7% peak in July 2022. It’s the slowest pace since November 2021. The BoE also started polling CPI inflation expectations since May of last year. Companies see consumer prices rising 4.8% next year and 3.2% three years ahead, down from 5.4% and 3.3% respectively in July. BoE Governor Bailey yesterday during his appearance before parliament said these inflation expectations “shapes a lot of our thinking about the direction of policy”. It shouldn’t come as a big surprise then that money markets have lowered bets for a 25 bps hike at the September meeting. They also no longer fully price in a total of 50 bps in additional tightening (to 5.75%). UK gilt yields lose more than 6 bps at the front end of the curve, outperforming global peers. An important caveat in the BoE’s survey of today, though, is wage growth. Companies’ expectations for the next 12 months remained unchanged at 5%. Combined with the share of firms reporting that hiring has become “much harder” having increased again (26.2%, up from 22.5%) suggests ongoing labour market tightness.

Germany’s Ifo institute today confirmed its June forecast of a 0.4% contraction this year. Unlike previously though, it does not expect a recovery in the second half of 2023 any longer. The reason it then didn’t lower its growth forecast is due to an upward revision from the statistics office to Q1 growth (-0.1% vs -0.3 prior). For 2024, GDP should expand 1.4% (-0.1 ppt compared to its previous forecast) while rising 1.2% in 2025. Private consumption is the bright spot. It forecasts a gradual recovery in 2023H2 amid rising disposable incomes & purchasing power due to easing inflation. Prices pressures are seen slowing to 6% in 2023 before falling to 2.6% and 1.9% in the two years after. Ifo’s head of forecasts said they expect the ECB’s first rate cut only at the end of next year.

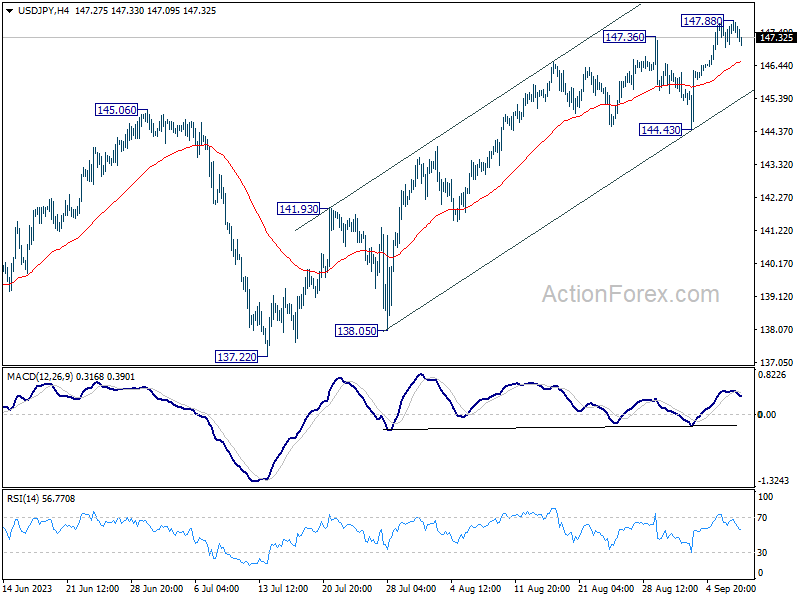

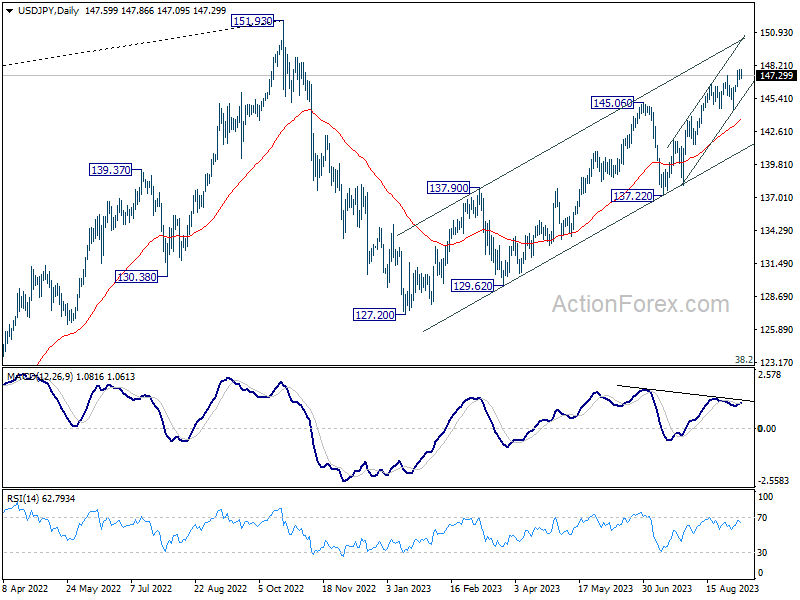

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.19; (P) 147.51; (R1) 147.99; More...

Intraday bias in USD/JPY is turned neutral with current retreat, and some consolidations could be seen. But near term outlook will stay bullish as long as 144.43 support holds. On the upside, above 147.88 will resume larger rally from 127.20, to retest 151.93 high.

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

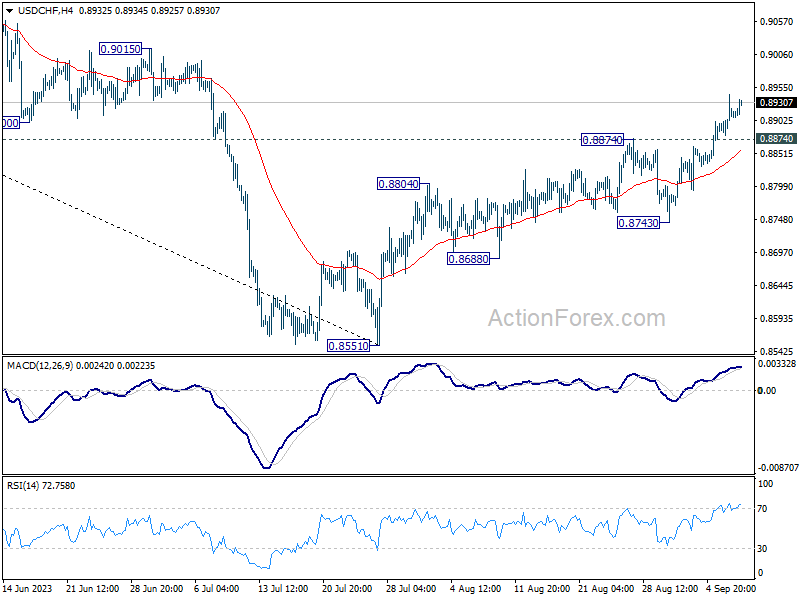

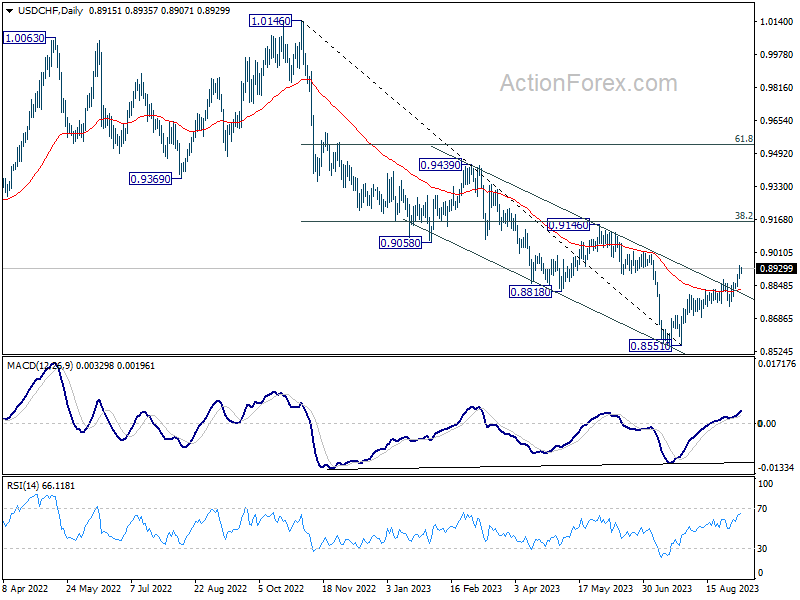

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8880; (P) 0.8912; (R1) 0.8944; More....

USD/CHF's rally from 0.8551 is still in progress and intraday bias stays on the upside. Further rally would be seen to 0.9146 cluster resistance next. On the upside, below 0.8874 minor support will turn intraday bias neutral first. But risk will stay on the upside as long as 0.8743 support holds.

In the bigger picture, rebound from 0.8551 medium term bottom is currently seen as a correction to the downtrend from 1.0146 (2022 high). Further rally would be seen to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160). Strong resistance could be seen there to limit upside, at least on first attempt.

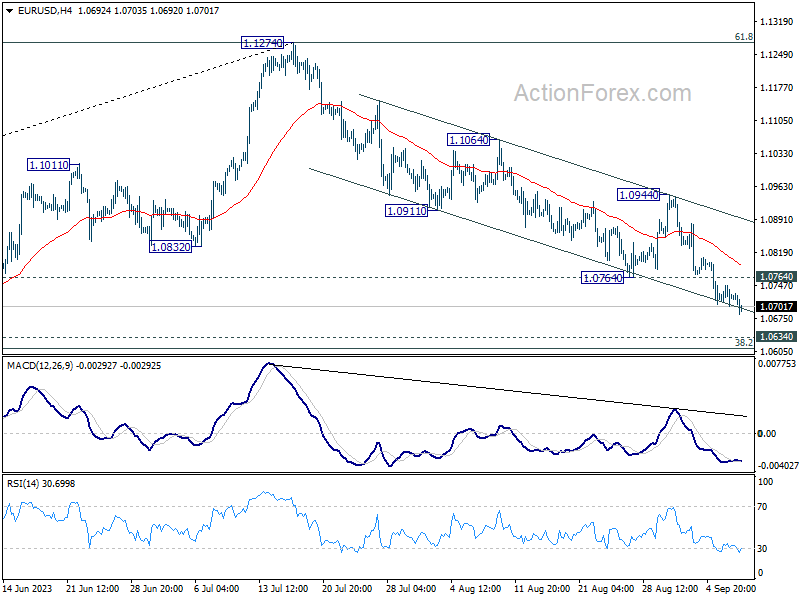

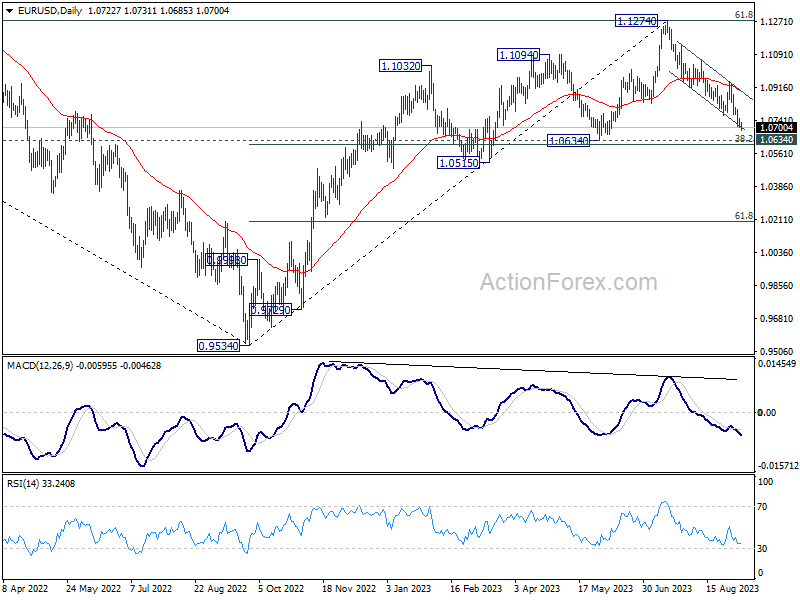

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0703; (P) 1.0726; (R1) 1.0749; More...

EUR/USD's decline from 1.1274 is still in progress and intraday bias stays on the downside. Next target is 1.0609/34 cluster support. On the upside, above 1.0764 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.0944 resistance holds, in case of recovery.

In the bigger picture, fall from 1.1274 medium term top is seen as a correction to up trend from 0.9534 (2022 low). Deeper decline would be seen to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to bring rebound. Yet, medium term outlook will be neutral for now, as long as 1.1274 resistance holds. However, sustained break of 1.0609/34 will raise the chance of bearish trend reversal, and target 61.8% retracement at 1.0199.

USD/JPY Testing 148 Resistance, Higher One is at 150

Notice that USDJPY made a sharp drop from 2022 highs, a clear impulse that suggests we have a top in place of a higher degree wave V. As such, the current rise from 126 can be temporary, but it s a complex and deep movement but can be corrective still. Looking at the daily charts; the important key Fib resistance is at 78.6%, while the important channel line stands near 142.00 which certainly has to be broken for a bearish trend.

Looking at the 4h time frame, this can be an ongoing fifth wave of a fith that is now at frist resistance at 148, while second higher protection is at 150, which can be tested if price move will extend. So in both cases keep in mind that this five-wave rise from 137.00 can come to an end and that sooner or later bears will show up with a minimum three-wave bearish reversal.

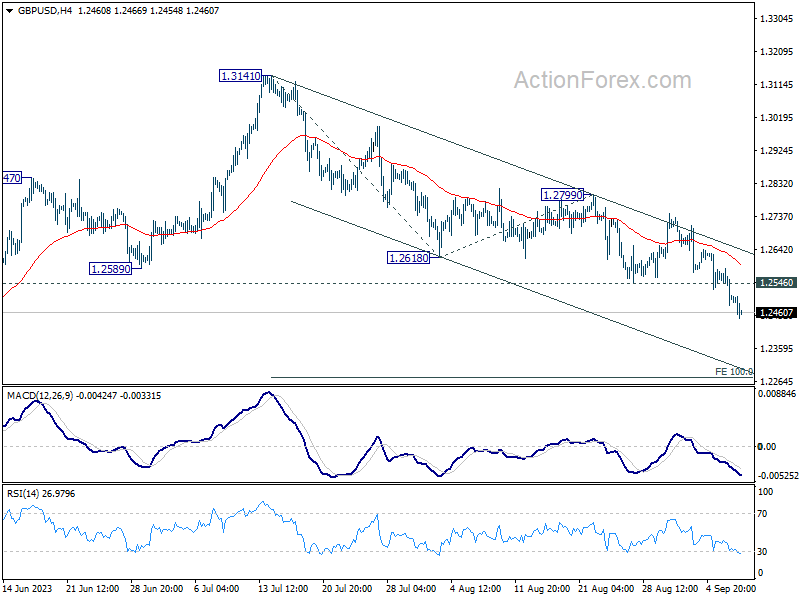

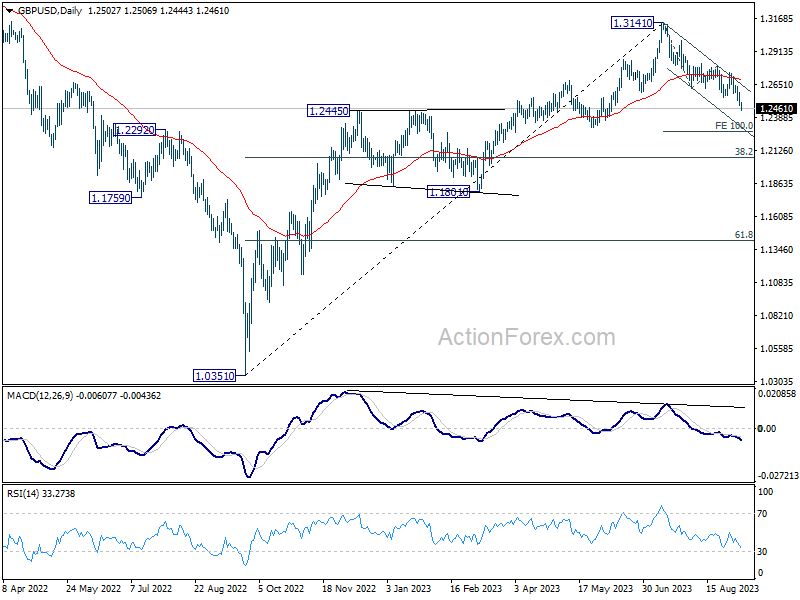

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2463; (P) 1.2526; (R1) 1.2569; More...

GBP/USD's decline continues today and intraday bias stays on the downside. Current fall from 1.3141 should target 100% projection of 1.3141 to 1.2618 from 1.2799 at 1.2276. On the upside, above 1.2546 minor resistance will turn intraday bias neutral and bring consolidations. But risk will stay on the downside as long as 1.2799 resistance holds, in case of recovery.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. But outlook will be neutral at best as long as 1.3141 resistance holds, and consolidation from there is set to extend, until further development.

Sterling in Distress Following BoE Survey, Euro and Franc also Soften

Sterling is under pronounced pressure in forex markets, trailing as the day's worst performer. This wave of selloff initiated yesterday following BoE Governor Andrew Bailey's articulation to the parliament, hinting that UK is "much nearer" to hitting the terminal interest rates. Further aggravating the downfall, a BoE survey rolled out today unveiled a stark decline in businesses' on-year inflation expectations, thus spotlighting intensified speculation over the path of BoE's tightening. Euro and Swiss Franc are also caught in this downward spiral, but slightly not as drastically as Sterling.

Contrary to European currencies, commodity currencies are witnessing a tepid recovery. But Australian and New Zealand Dollars remain unmoved from their positions as the weakest players of the week. Dollar retains its ground, drawing support from an encouraging jobless claims data release, while sustained buying momentum seems reserved primarily against European majors. Meanwhile, Yen is on recover, as part of near term consolidations.

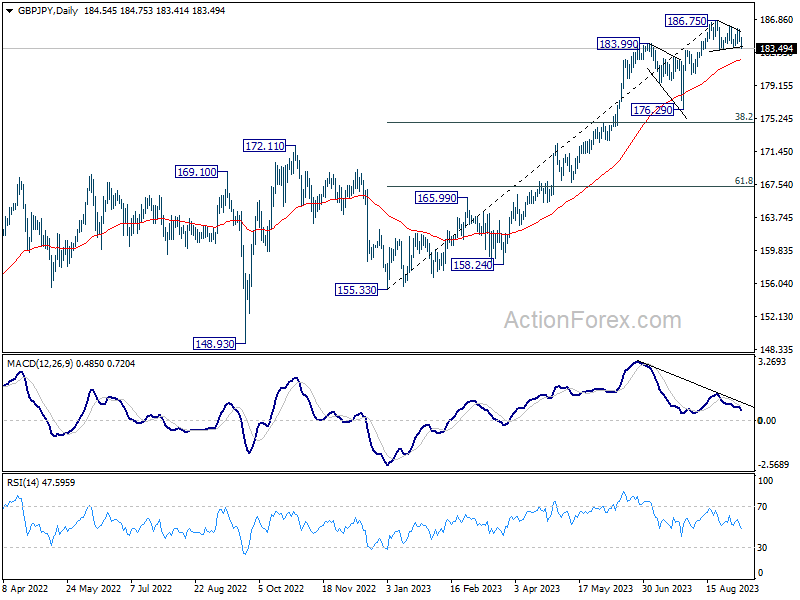

Technically, GBP/JPY's correction from 186.75 looks ready to extend lower with break of near term trend line support. Sustained trading below 183.51 support would target 55 D EMA (now at 182.16). A rebound might occur at this juncture, at least on the first attempt.

But look further ahead, there's a tangible possibility that GBP/JPY's decline from 186.75 represents a larger-scale correction to the uptrend from 155.33. The impending two weeks are critical, as employment and inflation data could essentially steer the dynamics, serving as precursors to BoE rate decision on September 21. Sustained break of 55 D EMA could pave the way to 176.29.

In Europe, at the time of writing, FTSE is up 0.03%. DAX is down -0.42%. CAC is down -0.18%. Germany 10-year yield is down -0.0398 at 2.617. Earlier in Asia, Nikkei dropped -0.75%. Hong Kong HSI fell -1.34%. China Shanghai SSE declined -1.13%. Singapore Strait Times rose 0.12%. Japan 10-year JGB yield rose 0.0021 to 0.658.

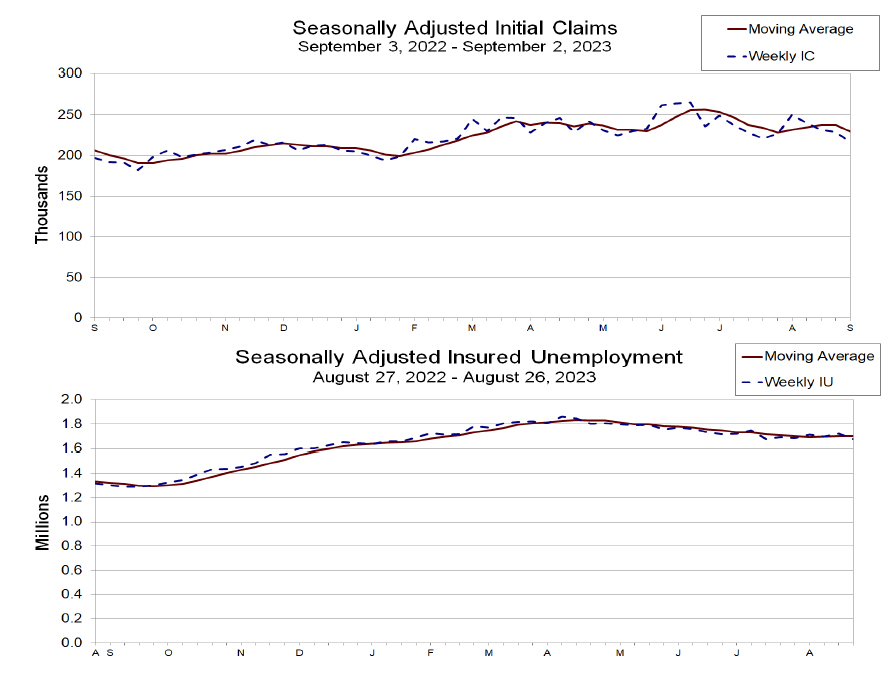

US jobless claims down to 216k, vs exp. 235k

US initial jobless claims fell -13k to 216k in the week ending September 2, better than expectation of 235k. Four-week moving average of initial claims dropped -8.5k to 229k.

Continuing claims dropped -40k to 1679k in the week ending August 26. Four-week moving average of continuing claims fell -1k to 1701.5k.

BoE Decision Maker Panel indicates easing inflation expectations

In the latest release of BoE Decision Maker Panel survey data for August, there is a tangible shift in business expectations pointing towards a decrease in both output price inflation and CPI inflation over the coming year, albeit with a lingering high degree of uncertainty.

According to the report, firms anticipate a fall in output price inflation over the next year, with the year-ahead output price inflation envisioned to be 4.9% in the three months leading up to August. This projection denotes a dip of -0.5% in comparison to the data gathered in the three months to July.

One-year ahead CPI inflation expectations lowered to 4.8% in August, a significant reduction from the 5.4% foreseen in July. Furthermore, when casting the net wider to encompass a three-year period, August data records a slight decrease to 3.2%, down by a marginal -0.1% from July's expectations.

In the realm of wage growth, there is a persistence of the previously noted trend with expectations for the year ahead holding steady at 5.0% in August. Despite this, it is essential to note that the figure is overshadowed by the realized wage growth reported at a higher 6.9% for both single month data and the cumulative data for the three months to August.

However, amidst these optimistic projections, businesses seem to be grappling with considerable uncertainty. A substantial 53% of firms expressed that they are facing high to very high levels of uncertainty, a statistic that has remained unchanged from July.

BoJ Nakagawa sees positive developments, but loose monetary policy still needed

BoJ Board member Junko Nakagawa struck a cautiously optimistic tone today about the Japanese economy, citing "positive developments" and "signs of change in corporate price and wage-setting behavior."

However, she was quick to note that the country has not yet achieved its price target "in a stable, sustainable fashion."

Nakagawa noted that there are chances inflation could accelerate beyond initial expectations. However, she also warned of the potential for inflation to decelerate once the pass-through effects of higher costs begin to moderate.

The policymaker underscored the need for BoJ to maintain its ultra-loose monetary policy for the time being, citing the prevailing economic uncertainty.

RBA Lowe cautions against complacency in managing inflation risks

In his final public speech as RBA Governor, Philip Lowe stated that for inflation to average around 2.5%, wage increases should typically align with productivity growth plus an additional 2.5%. He sees it as a "reasonable benchmark", even it's "not a hard and fast rule".

Lowe's recent attention has been particularly focused on the risk associated with the current period of high inflation. Specifically, he warned of the peril that "wages growth and profits running ahead of the rate that is consistent with a sustainable return of inflation to target."

In such a scenario, he cautioned, inflation would become "sticky," necessitating "tighter monetary policy and more economic pain later on."

Lowe acknowledged that recent data offers some level of comfort but emphasized the importance of remaining alert to these inflation risks. Rise in productivity growth, he noted, would be a welcome development as it would facilitate stronger growth in both nominal and real wages and profits.

China's exports and imports continue to contract

In August, China reported a fourth consecutive monthly contraction in exports, dropping -8.8% yoy to USD 284.9B. However, the contraction was narrower than market's expectation of a -9.5% yoy decline and an improvement from July's -14.5% yoy fall.

Imports also shrank by -7.3% yoy to USD 216.5B, beating expectations of -9.4% yoy decline and improving from July's -12.4% yoy drop. This marks a consistent trend of contracting imports every month in 2023 compared to the year-ago period.

Despite these figures beating expectations, trade surplus shrank from USD -80.6B to USD -68.4B, almost in line with expectation of USD -60.0B.

While the narrowing contraction in exports and imports could be seen as a mildly positive development, it doesn't significantly alter the broader narrative of economic cooling in China.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2463; (P) 1.2526; (R1) 1.2569; More...

GBP/USD's decline continues today and intraday bias stays on the downside. Current fall from 1.3141 should target 100% projection of 1.3141 to 1.2618 from 1.2799 at 1.2276. On the upside, above 1.2546 minor resistance will turn intraday bias neutral and bring consolidations. But risk will stay on the downside as long as 1.2799 resistance holds, in case of recovery.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. But outlook will be neutral at best as long as 1.3141 resistance holds, and consolidation from there is set to extend, until further development.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Manufacturing Sales Q2 | 0.20% | -2.80% | -2.50% | |

| 01:30 | AUD | Trade Balance (AUD) Jul | 8.04B | 10.05B | 11.32B | 10.27B |

| 03:00 | CNY | Trade Balance (USD) Aug | 68.4B | 68.0B | 80.6B | |

| 03:00 | CNY | Trade Balance (CNY) Aug | 488B | 494B | 576B | |

| 05:00 | JPY | Leading Economic Index Jul P | 107.6 | 107.9 | 109.1 | |

| 05:45 | CHF | Unemployment Rate Aug | 2.10% | 2.10% | 2.10% | |

| 06:00 | EUR | Germany Industrial Production M/M Jul | -0.80% | -0.40% | -1.50% | |

| 06:45 | EUR | France Trade Balance (EUR) Jul | -8.1B | -6.8B | -6.7B | -6.8B |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Aug | 694B | 698B | ||

| 08:00 | EUR | Italy Retail Sales M/M Jul | 0.40% | 0.20% | -0.20% | |

| 09:00 | EUR | Eurozone GDP Q/Q Q2 | 0.10% | 0.30% | 0.30% | |

| 12:30 | CAD | Building Permits M/M Jul | -1.50% | 7.50% | 6.10% | |

| 12:30 | USD | Initial Jobless Claims (Sep 1) | 216K | 235K | 228K | |

| 12:30 | USD | Nonfarm Productivity Q2 | 3.50% | 3.50% | 3.70% | |

| 12:30 | USD | Unit Labor Costs Q2 | 2.20% | 1.80% | 1.60% | |

| 14:00 | CAD | Ivey PMI Aug | 49.2 | 48.6 | ||

| 14:30 | USD | Natural Gas Storage | 38B | 32B | ||

| 15:00 | USD | Crude Oil Inventories | -1.8M | -10.6M |

US jobless claims down to 216k, vs exp. 235k

US initial jobless claims fell -13k to 216k in the week ending September 2, better than expectation of 235k. Four-week moving average of initial claims dropped -8.5k to 229k.

Continuing claims dropped -40k to 1679k in the week ending August 26. Four-week moving average of continuing claims fell -1k to 1701.5k.