Sample Category Title

China’s Caixin PMI services fell to 51.8, waning economic momentum

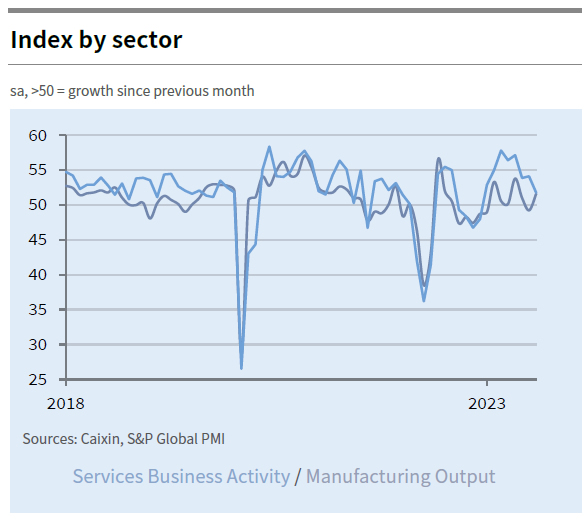

China Caixin PMI Services for August fell to 51.8, down from 54.1 in July and below market expectations of 53.6. This marks the lowest reading in eight months. According to Caixin, the softer performance was due to a slower increase in business activity and new orders. While employment continued to rise, input cost inflation reached a six-month low.

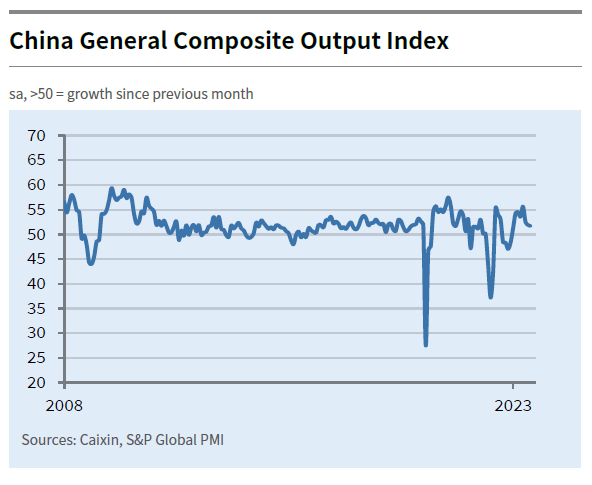

Composite Output Index, which includes both manufacturing and services sectors, slightly decreased from 51.9 to 51.7. Though it still indicates expansion, the rate of growth was the slowest since January this year. A milder expansion in services sector was partially offset by a modest uptick in factory production.

Wang Zhe, Senior Economist at Caixin Insight Group, attributed the lackluster performance to seasonal fluctuations, extreme weather conditions like high temperatures and flooding, and a complicated global economic environment. These factors are further exacerbated by weak domestic demand.

Wang also warned of the long-term challenges facing the Chinese economy, stating, "Looking ahead, seasonal impacts will gradually subside, but the problems of insufficient domestic demand and weak expectations may form a vicious cycle for a protracted period of time." He added that given the uncertainty in external demand, downward pressure on the economy may continue to intensify.

AUD/USD Under Downside Pressure Below 0.6510 as RBA Looms

- In the past three weeks, AUD/USD has been trading within a minor range configuration between 0.6510 and 0.6385.

- Price actions have been dictated primarily from external factors especially economic news flow out from China.

- Consensus is expecting another third consecutive month of no change in the policy cash rate at 4.1% in today’s RBA monetary policy decision.

- The medium-term trend of AUD/USD remains bearish below its 50-day moving average now acting as a resistance at 0.6600 and 0.6510 remains the key short-term resistance to watch.

Since its minor range swing low of 0.6338 printed on 17 August 2023, the price actions of AUD/USD have been primarily driven by external factors; especially economic news flow out from China as Australia’s commodities producers/trading firms are dependent on either direct or indirectly on the fortunes of the currently cash-stripped Chinese property developers.

In the past week, the AUD/USD has rallied as expected and hit the 0.6510 countertrend rebound resistance, it printed an intraday high of 0.6522 last Wednesday, 30 August before upside momentum fizzled out to trade back down within its minor range configuration in place since 17 August 2023.

In the past two trading sessions, the price actions of AUD/USD have been whipsawed around its downward-slopping 20-day moving average as we await the outcome of the key RBA monetary policy decision out later today at 0430 GMT.

Today’s RBA monetary policy meeting will be the last one chaired by the current Governor Phillip Lowe before he hands over the reins to Michele Bullock, an RBA “lifer” since 1985. In the run-up to today’s meeting, the consensus is expecting another third consecutive month of no change in the policy cash rate at 4.1% as the recently released monthly CPI indicator for July has slowed to 4.9% y/y from 5.4% y/y in June, its slowest pace of increase since February 2022 and below consensus of 5.2% y/y.

Interestingly, the ASX 30-day interbank cash rate futures on the September 2023 contract have indicated a 14% chance of a 25-basis point cut on the cash rate to 3.85% for today’s RBA meeting based on data as of 4 September 2023. That’s a slight increase in odds from a 12% chance of a 25-bps rate cut inferred a week ago.

Let’s now examine the AUD/USD from the lens of technical analysis.

Medium-term momentum remains bearish

Fig 1: AUD/USD medium-term trend as of 5 Sep 2023 (Source: TradingView, click to enlarge chart)

Since the bearish breakdown of the AUD/USD below its former medium-term ascending trendline support from the 13 Oct 2022 swing low on 11 August 2023, its price actions have continued to thread lower below its downward-sloping 50-day moving average now acting as a key medium-term resistance at 0.6600 which also confluences with the former swing low of 29 June/6 July 2023 where the bulls got rejected on 4 August and 10 August 2023 after attempts to break above it.

Also, the daily RSI indicator, a measurement of momentum has managed to stage a retreat right after a retest on former parallel ascending support now turns pull-back resistance right below the 50 level in the past week which indicates the revival of medium-term bearish momentum that advocates further potential downside pressure in the price actions of AUD/USD going forward.

0.6510 is the key short-term resistance to watch on the AUD/USD

Fig 2: AUD/USD minor short-term trend as of 5 Sep 2023 (Source: TradingView, click to enlarge chart)

If the 0.6510 key short-term pivotal resistance is not surpassed to the upside and a breakdown below the intermediate minor support of 0.6440, the AUD/USD may see a further slide to retest the minor range support of 0.6385. Thereafter, a break with a daily close below 0.6385 may kickstart another leg of a potential impulsive down move sequence within its medium-term downtrend phase to expose the next support at 0.6310 in the first step.

On the flip side, a clearance above 0.6510 negates the bearish tone for a squeeze-up to see the 0.6600 medium-term resistance next.

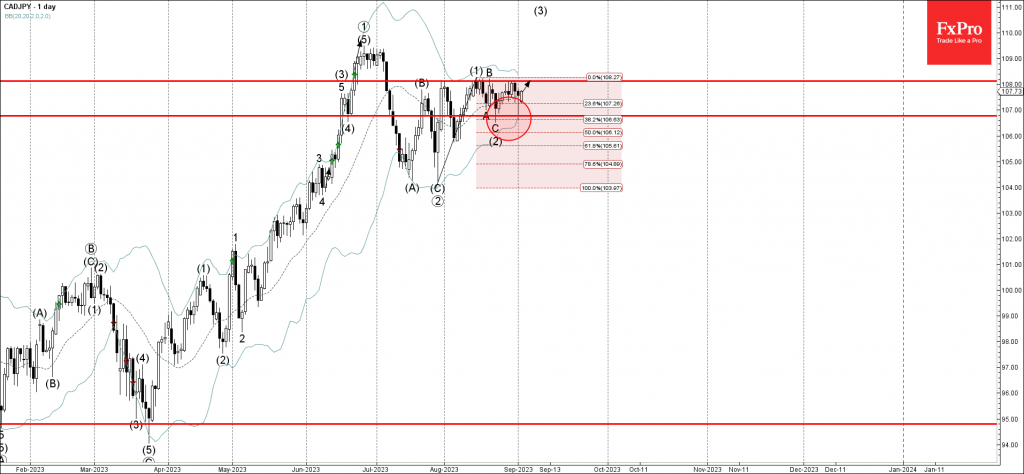

CADJPY Wave Analysis

- CADJPY reversed from support level 106.75

- Likely to rise to resistance level 108.00

CADJPY currency pair recently reversed up from the key support level 106.75 (which stopped the previous waves A and (2)), coinciding with the lower daily Bollinger Band and the 38.2% Fibonacci correction of the upward impulse from the end of July.

The upward reversal from the support level 106.75 continues the active intermediate impulse wave (3) from the middle of August.

Given the clear daily uptrend and the strong yen sales, CADJPY can be expected to rise further toward the next resistance level 108.00 (top of the previous waves (1) and B).

Brent Oil on an Upward Trajectory: A Comprehensive Overview

The price of Brent crude oil is showing positive momentum, stabilizing at approximately $88.57 per barrel as of Monday. The market sentiment is predominantly bullish.

This upward trend is supported by encouraging economic data from both China and the United States. Specifically, China's business activity outperformed expectations in August, lending some optimism to projections for oil demand. However, it's worth noting that the strength of the U.S. dollar could act as a moderating factor on crude oil price gains.

In terms of supply, Baker Hughes' recent statistics reveal that the count of active oil rigs in the U.S. remains stable at 512 units. Meanwhile, Canada saw a minor decline, with one rig going offline, bringing its total to 114 units.

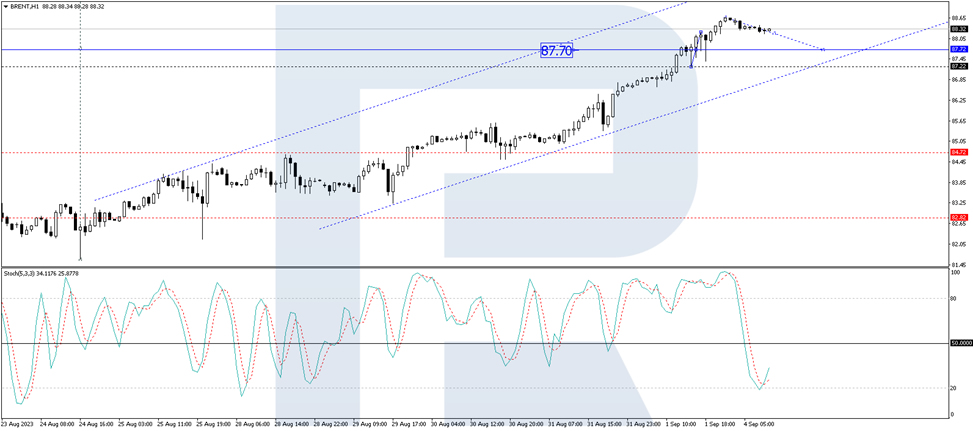

Technical Analysis of Brent Oil

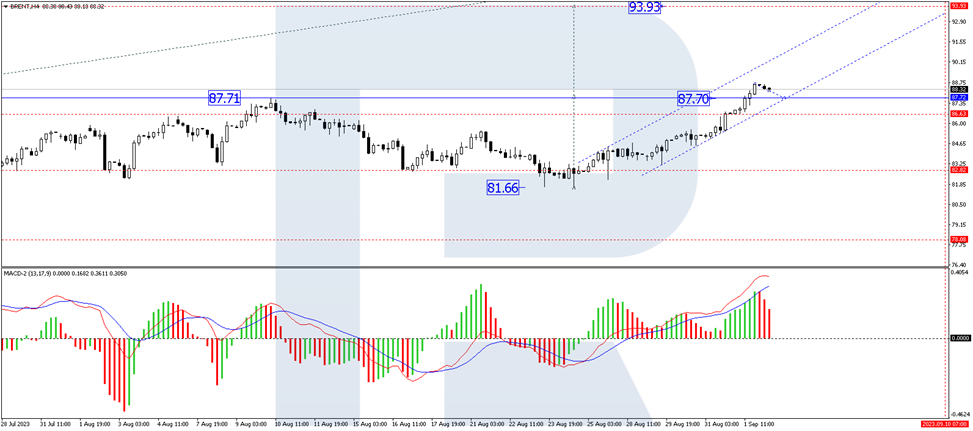

On the 4-hour chart for Brent, the price trajectory suggests robust growth. This upward movement can be interpreted as targeting a level of $93.93. Once this price target is achieved, a price correction to $87.70 is anticipated, potentially accompanied by a retest from above. Subsequently, analysts expect the price to climb to the initial target of $104.00. The Moving Average Convergence Divergence (MACD) indicator corroborates this outlook, with its signal line directed sharply upward, indicating the possibility of reaching new highs.

On the 1-hour chart, Brent has already seen a surge to $87.70, and a consolidation pattern has emerged around this price point. A breakout above this level has set the stage for an extension to $90.00, from where the upward trend could potentially continue to $93.93. The Stochastic oscillator lends technical support to this scenario; its signal line has bounced off the 20-point level and is advancing toward 50. Should it surpass this level, further upward movement to 80 is highly likely.

In summary, both short-term and medium-term technical indicators suggest that Brent oil prices are poised for further gains, although external economic factors could introduce some volatility.

A Slow Start to the Week as Germany Continues to Display Weakness

Not the most thrilling start to the week, with the US bank holiday naturally bringing with it a more peaceful opening session but markets in Europe have started fairly well.

Perhaps there's some carryover from last week - I'm still surprised at the lack of uplift from the jobs report - or the prospect of a stimulus-induced boost to China's economy. Or maybe there's nothing much at all behind the small gains in Europe and we're just getting back into the swing of post-summer break trading.

August was far from encouraging and the narrative appeared to follow quickly behind - interest rates will stay higher for longer, recessions are coming for us all etc. There may have been too much read into trade of the last month - I may be proven wrong - but I suspect we'll know over the next couple of weeks how much that will show to be the case.

The economic data today has been minor both in terms of numbers and impact/interest. German exports slumped again which won't come as a surprise to many given how they've performed for so long, teetering on recession and maybe so again. Global trade has suffered considerably and Germany seemingly particularly so, with China's sluggish demand clearly not helping.

Oil steady today but momentum remains with the rally

Oil prices are a little flat today after rallying another 5% last week. Brent hit a new high for 2023 in the process and, despite paring earlier gains today, there still appears to be plenty of momentum in the rally.

That there is still plenty of momentum so close to $90 a barrel may suggest we could see a strong push to break above which would represent a big shift in the market dynamic in quite a short period of time.

Saudi Arabia and Russia have been managing additional voluntary cuts on a monthly basis and could withdraw them at any point but I can't imagine they'll be in any rush and risk sending the price tumbling again.

Gold remains short of key technical resistance

Gold has been a little choppy today but nothing has really changed since Friday. It continues to trade a little shy of $1,950 after trying to break above in the immediate aftermath of the US jobs report. That it failed to hold above here was perhaps a little surprising - it couldn't have really delivered more for Fed doves - and maybe a bearish signal; a show of significant resistance.

It's failed around here for four days now and there are a combination of technical resistance levels that could be pushing back. Perhaps the rebound of the last couple of weeks has run out of steam.

ECB Lagarde: Effective communications to remain of paramount importance

In a speech today, ECB President Christine Lagarde emphasized two key reasons for the need of effective communications by central banks: "high inflation and high levels of attention on inflation."

According to Lagarde, "While inflation is now falling, effective communication is likely to remain of paramount importance even after the current inflation spike is over," she said.

Lagarde also highlighted the critical role that central banks play in anchoring inflation expectations. As various economic factors, such as relative price changes, come into play, it becomes even more important for central banks to maintain public confidence in their ability to ensure price stability.

The focus on inflation presents both an opportunity and a risk for central banks, Lagarde pointed out. On the one hand, the heightened public awareness around inflation could lead to unstable inflation expectations, posing a significant challenge for policy-makers. On the other hand, this increased attention gives central banks a valuable opportunity to communicate their commitment to price stability and to anchor public expectations.

Sunset Market Commentary

Markets

Trading took a slow start today with US investors absent (Labour Day) and the European eco calendar empty. German Bunds lost a few ticks at the start of trading, catching up with Friday’s post-payrolls losses for US Treasuries and taking into account comments by ECB Wunsch who said that it’s too early to talk about a rate hike stop adding that the ECB might need more to fight very persistent underlying inflation. Dovish ECB Centeno later balanced the comments by suggesting that there is a risk of doing too much on rates. The different views show that the jury is still out on the September decision. Money markets see a 25% probability of a September rate hike (our preferred scenario) . German yields today add 2.5 bps to 4 bps with the belly of the curve underperforming the wings. EUR/USD gains a few ticks, trying to regain EUR/USD 1.08. European stocks markets opened strong on the back of positive Asian momentum (more Chinese stimulus), but pare gains to currently +0.25% on average.

The Belgian debt agency updated its borrowing requirements and funding plan after announcing the “by far most successful issuance” ever. They raised €21.9bn via a fiscally-friendly 1-yr State Note for the retail customer. Renewed issuance of the 1-yr State Note in December 2023 is possible, but not mentioned. The outstanding amount of Treasury Certificates is now expected to decline by €13.46bn, whereas previously an increase of €1bn was expected. The net change in other short-term debt and financial assets will equally decline, and would amount to -€4.37bn. The Treasury’s cash reserves will structurally increase by some €9bn. The 2023 gross borrowing requirement was revised downwards by €2bn to €49.07bn with the OLO funding need lowered from €45bn to €42.1bn (€33.79bn or 80% of which already done). Because of this favorable position, the November OLO auction will be cancelled. Since the announcement of the 1-yr State Note, the German/Belgian 10-yr yield spread narrowed from around 67 bps mid-August to 62 bps currently. That’s the tightest since March of this year. The French/Belgian 10-yr yield spread narrowed from 13 bps to 9 bps over the past fortnight.

News & Views

Turkish inflation printed substantially higher than expected in August at 9.09% M/M and 58,94% Y/Y, compared with 9.49% M/M and 47.83% Y/Y in July. Markets expected a more modest rise of about 6.50% M/M. In a monthly perspective, the rise was driven by transportation costs (16.61%), furnishes and household equipment (+9.36%) and food an non-alcoholic beverages (+8.48%). The latter has a 25.4% weight in the expenditure basket. Core inflation ex energy, food and beverages, tobacco and gold also accelerated more than expected to 8.89% M/M and 64.85% Y/Y. The rise in inflation comes after president Erdogan after elections allowed for a change in the CBRT’s unorthodox monetary policy (reducing interest rates while at the same time taking non-monetary policy measures to limit the decline of the lira). In a subsequent move to a more orthodox/market-oriented policy, the lira lost more than 25% against the dollar since end May even as the CBRT raised its policy rate from 8.50% end May to 25.00% in August. Today’s data put pressure on the central bank to continue its tightening cycle on September 21. The lira depreciated modestly against the dollar, from USD/TRY 26.73 on Friday to 26.775 currently.

Czech nominal wages in the April/June quarter rose 1.5% Q/Q to be up 7.7% Y/Y, down from 8.7% in the first quarter. However, as consumer price inflation during that period rose by 11.1%, real wages still declined -3.1% Y/Y from 6.6% Y/Y in Q1. The volume of wages increased by 8.3% and the number of employees increased by 0.6%. In its summer forecast, the CNB expected nominal wage growth in Q2 at 8.6% Y/Y, 8.7% in Q3 and 8.8% in Q4. So current data suggest that wage pressures in the country are slower than the CNB anticipated. This could support the case for the CNB to cut its policy rate (7%) in the final quarter of this year. The koruna today declined slightly to EUR/CZK 24.11.

Britain’s Economy: Balancing Act Amidst Gloomy Metrics and Resilient FTSE 100

Recent headlines are painting a grim picture for the UK economy, with concerns of a looming recession fueled by disheartening metrics. Both house prices and factory production figures have taken a hit, raising concerns about the nation's financial health. However, amid these gloomy indicators, the FTSE 100 index stands strong, showcasing the complexity of the economic landscape.

House Prices and Factory Production: A Double Whammy?

Recent reports suggest that the UK's housing market has experienced its largest annual drop in prices since the global financial crisis of the late 2000s. Simultaneously, factory production figures indicate a notable slump, leading some to draw comparisons to the economic turmoil of that era.

This double blow has sent shockwaves through the media, with sensationalist journalism warning of an impending recession. While these figures are undoubtedly concerning, it's essential to consider the broader economic context.

The British Pound's Response

The British Pound has reacted to these negative indicators by depreciating against the US Dollar. The Dollar, despite the US's high debt-to-GDP ratio and recent debt ceiling increases, has maintained its strength thanks to controlled inflation and robust output and productivity.

The Pound's dip against the Dollar reflects concerns over the UK's economic prospects. However, it's important to note that currency markets can be sensitive and reactive, often amplifying sentiment, which may not always align with the underlying economic health.

Indicative pricing only

FTSE 100 Index: A Contrary Tale

Amid the turbulent economic news, the FTSE 100 index tells a different story. It has remained resilient and stood at 7,503 as the London trading session began. This index represents some of the UK's largest blue-chip companies, and its robust performance indicates confidence in their prospects.

A Complex Economic Landscape

The stark contrast between the Pound's depreciation and the FTSE 100's stability highlights the complexity of the UK's economic landscape. While the media has periodically sounded the alarm about a UK recession over the past two years, the nation has managed to avoid a full-blown economic downturn.

Despite challenges such as soaring energy prices, a cost of living crisis, inflation touching double digits, and multiple interest rate hikes, a recession has not materialised. This resilience could be attributed to various factors, including government policies, consumer behaviour, and global economic conditions.

Conclusion: Uncertain Path Ahead

As headlines oscillate between economic optimism and pessimism, it's evident that the path forward for the UK's economy remains uncertain. While warning signs are present, historical precedent has shown that economic resilience and adaptability are also prominent features of the British economic landscape.

The outcome could indeed "go either way," as the interplay of domestic and international factors continues to shape Britain's economic future. In this dynamic environment, cautious optimism may be the order of the day, with a keen eye on economic indicators and policy responses.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

RBA Expected to Pause, US Nonfarm Payrolls Rises Slightly

- RBA expected to pause

- US nonfarm payrolls rise slightly to 187,000

The Australian dollar has started the week with slight gains. In Monday’s European session, AUD/USD is trading at 0.6464, up 0.21%.

RBA expected to pause

The Reserve Bank of Australia is expected to hold interest rates at 4.10% when it meets on Tuesday and a rate hike would be a huge surprise. The central bank has paused for two straight meetings and the odds of a third pause stand at 86%, according to the ASX RBA rate tracker.

The most important factor in RBA rate policy is of course inflation. In July, CPI fell to 4.9% y/y, down from 5.4% y/y and better than the consensus of 5.2% y/y. Inflation is moving in the right direction and has dropped to its lowest level since February 2022.

A third straight pause from the RBA will likely raise expectations that the current rate-tightening cycle is done but I don’t believe we’re at that point just yet. This is Governor Lowe’s final meeting and he is expected to keep the door open to further rate hikes. Incoming Governor Bullock stated last week that the RBA “may still need to raise rates again”, adding that the Bank will make its rate decisions based on the data. The RBA isn’t anywhere near declaring victory over inflation and has projected that inflation will not fall back within the 2%-3% inflation target until late 2025.

The week wrapped up with the US employment report for August. The Fed will be pleased as nonfarm payrolls remained below 200,00 for a third straight month, rising from a revised 157,000 to 187,000. Wage growth fell to 0.2% in August, down from 0.4% in July and below the consensus of 0.3%. The data cements a rate hold at the September 20th meeting, barring a huge surprise from the CPI report a week prior to the rate meeting.

AUD/USD Technical

- AUD/USD is testing resistance at 0.6458. Above, there is resistance at 0.6516

- There is support at 0.6395 and 0.6337