Sample Category Title

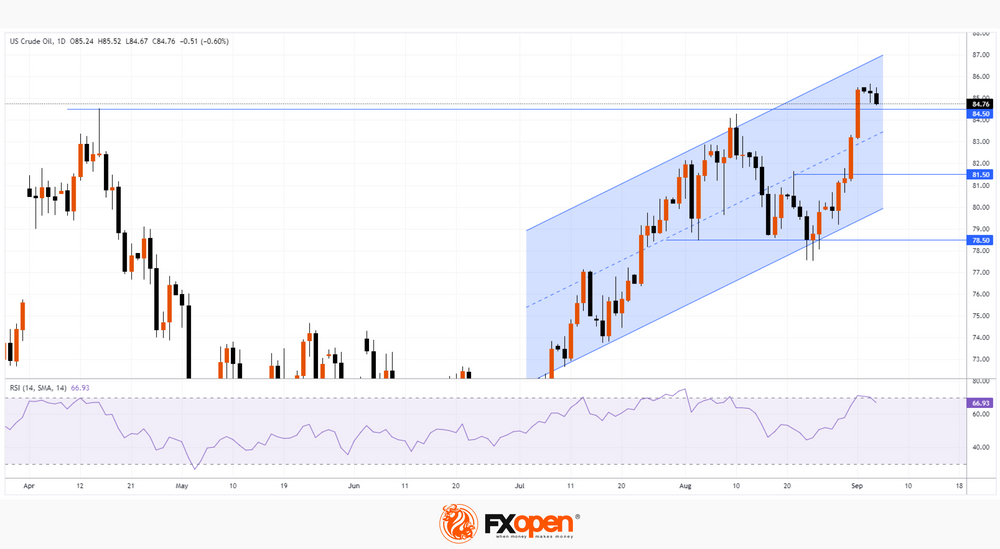

Price of Oil Sets Maximum of the Year

Yesterday, the price of WTI oil rose above USD 85.50 per barrel. This has not happened since November 2022.

On August 24, we wrote that the price of oil could find support for growth from the lower border of the rising channel, as well as from the level of USD 78.50. Since then, the price of WTI oil has risen by more than 9%. Fundamentally this contributed to:

→ the policy of limiting production by OPEC+ countries;

→ expectations that the Chinese economy will recover thanks to the incentives of the authorities.

According to Trafigura, a large company trading mainly in metals and energy resources, investment in the development of the oil industry is not enough, and a price of up to USD 88 can be considered fair in the current circumstances.

Bullish arguments:

→ the price of oil has not yet reached the upper limit of the rising channel, leaving the potential for updating the highs of the year;

→ the level at 81.50, which worked as a resistance, can now provide support;

→ support can also be provided by the median line of the uplink.

Bearish arguments:

→ rising oil prices are unfavorable for large economies, including the United States, which are struggling with high inflation. We can expect steps from governments aimed at lowering prices;

→ after 2 weeks of rapid growth (and especially on August 31 and September 1), a pullback would be a logical development for a market that is “overheated”. The RSI indicator indicates overbought.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

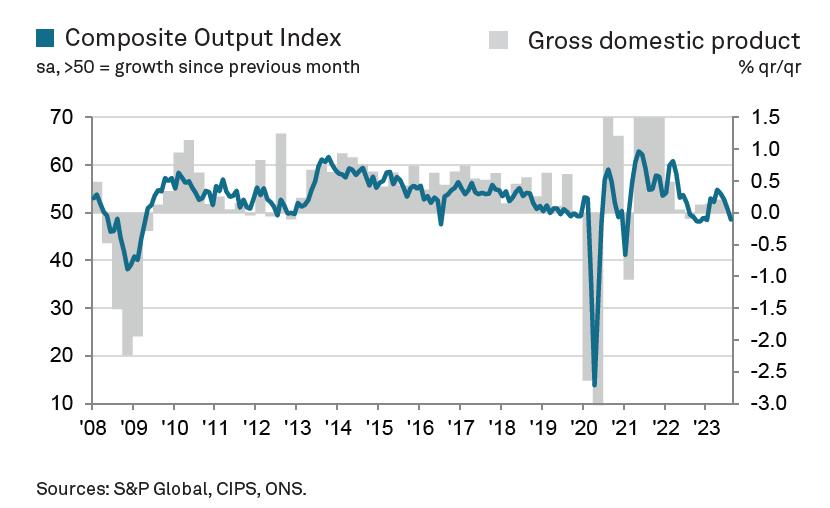

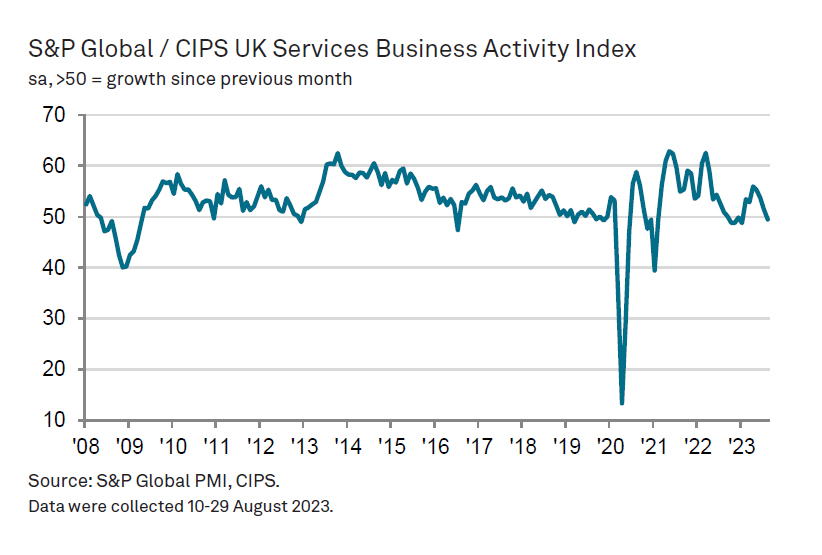

UK PMI services finalized at 49.5, faltering growth and sticky inflation

UK PMI Services was finalized at 49.5 in August, down from July's 51.5, and represents the lowest level since January. Furthermore, PMI Composite was finalized at 48.6, down from 50.8 in July, indicating the first contraction since the start of the year.

Tim Moore, Economics Director at S&P Global Market Intelligence, elaborated on the concerning developments. He noted that service sector businesses are "clearly feeling the impact of rising interest rates on client demand"

"Worries about the broader business climate also dampened spending in August," Moore said, adding that "faltering UK economic growth and sticky inflation" are contributing to more cautious outlook.

A key takeaway from the survey is the pace at which backlogs of work are decreasing—reported as the fastest in over three years. This suggests that businesses are scaling back their operations, perhaps in anticipation of tougher times ahead. The survey also highlighted cooling job market within service sector, as job creation dipped to its lowest point since March.

The report pointed out that competitive pressures may have started to curb inflation within the service economy. The latest round of price hikes was the slowest seen in two years, offering a glimmer of hope that inflation may stabilize or even decline in the near term.

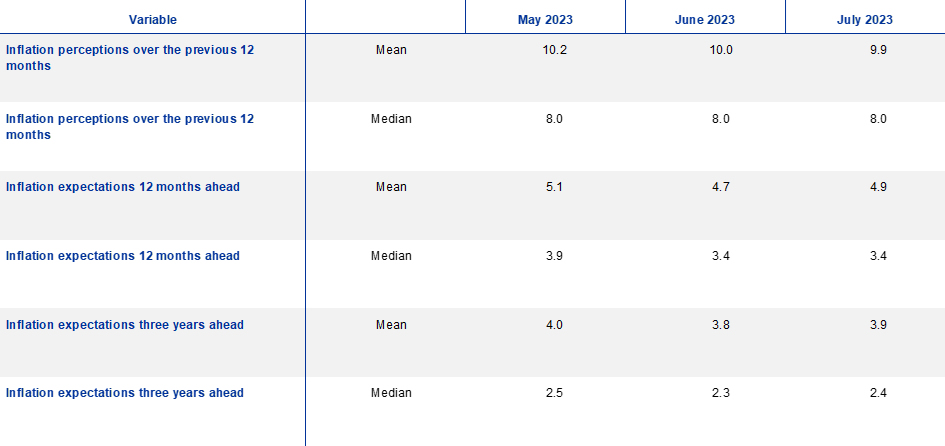

ECB consumer survey sees rising 3-yr inflation expectations, more pessimistic growth outlook

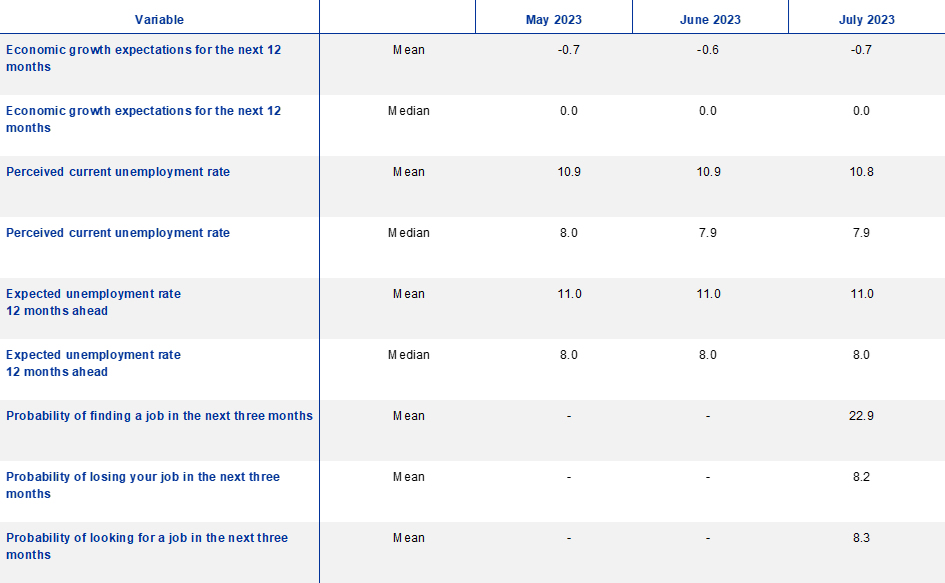

ECB has just released its Consumer Expectations Survey for July 2023, offering an inside look into how consumers are viewing the economic outlook.

Most notably, median expectations for inflation over the next year remained static at 3.4%. Even more telling is that forecast for inflation three years out saw a marginal uptick, moving to 2.4% from 2.3% recorded.

On the other hand, mean economic growth expectations for the next 12 months turned a bit more pessimistic, registering at -0.7% as compared to -0.6% in June.

In terms of employment, expectations for unemployment rate a year from now remained stable at 11.0%. Consumers perceive the current unemployment rate to be 10.8%, suggesting an expectation of a broadly stable labor market.

Market Caution Returns On China Woes

Asian markets were painted red on Tuesday with Chinese stocks leading losses as disappointing PMI services data fuelled concerns over the nation’s sluggish economic recovery.

European futures are pointing to a negative open amid the souring sentiment with investors focusing on final PMI data across the region, as well as a speech by ECB President Christine Lagarde. In the currency space, the dollar is advancing across the G10 space amid the cautious mood while Aussie bears are on a tear after the Reserve Bank of Australia kept rates on hold for a third time in the final meeting under Governor Philip Lowe. Regarding commodities, oil is hovering around levels not seen since November amid OPEC+ supply cuts while gold waits for a fresh fundamental spark.

Despite US markets being closed on Monday for the Labour Day holiday, this promises to be another eventful few days for global markets in the build-up to numerous central bank meetings in the weeks’ ahead. All eyes will be on the Bank of Canada rate decision on Wednesday which is expected to conclude with rates remaining at 5% amid the softening labour market and GDP growth.

Commodity Spotlight – Gold

Gold wobbled around $1935 on Tuesday morning, pressured by a stronger dollar and rising Treasury yields. Despite the choppy price action witnessed last Friday following the mixed US jobs report, gold seems to be searching for a fresh fundamental catalyst to trigger its next significant move. In the meantime, the precious metal is showing signs of exhaustion on the daily charts with weakness below the 50-day SMA opening a path back toward $1920. Should the $1935 level prove to be reliable support, prices could retest the 100-day SMA around $1953.

ECB Lane emphasizes need for timely return to 2% inflation

In an interview with The Currency, ECB Chief Economist Philip Lane offered some guarded optimism about the inflationary environment in Eurozone, despite acknowledging that the current inflation rate is a lofty 5.3%. Lane was keen to highlight a "welcome development" in the latest data, pointing to a slight easing in both goods and services inflation as potentially indicative of changing momentum.

Lane emphasized ECB's ongoing challenge of steering inflation rate back to its 2% target. "What is a timely manner?" Lane posed, elaborating that the goal is to return to 2% "sufficiently quickly that everyone understands that the current inflation episode is time-limited."

He underscored the importance of convincing the public that this is a "temporary inflation episode," and that they should not alter their longer-term behavior in anticipation of persistently high inflation rates. The key objective here is to prevent inflation expectations from becoming unanchored.

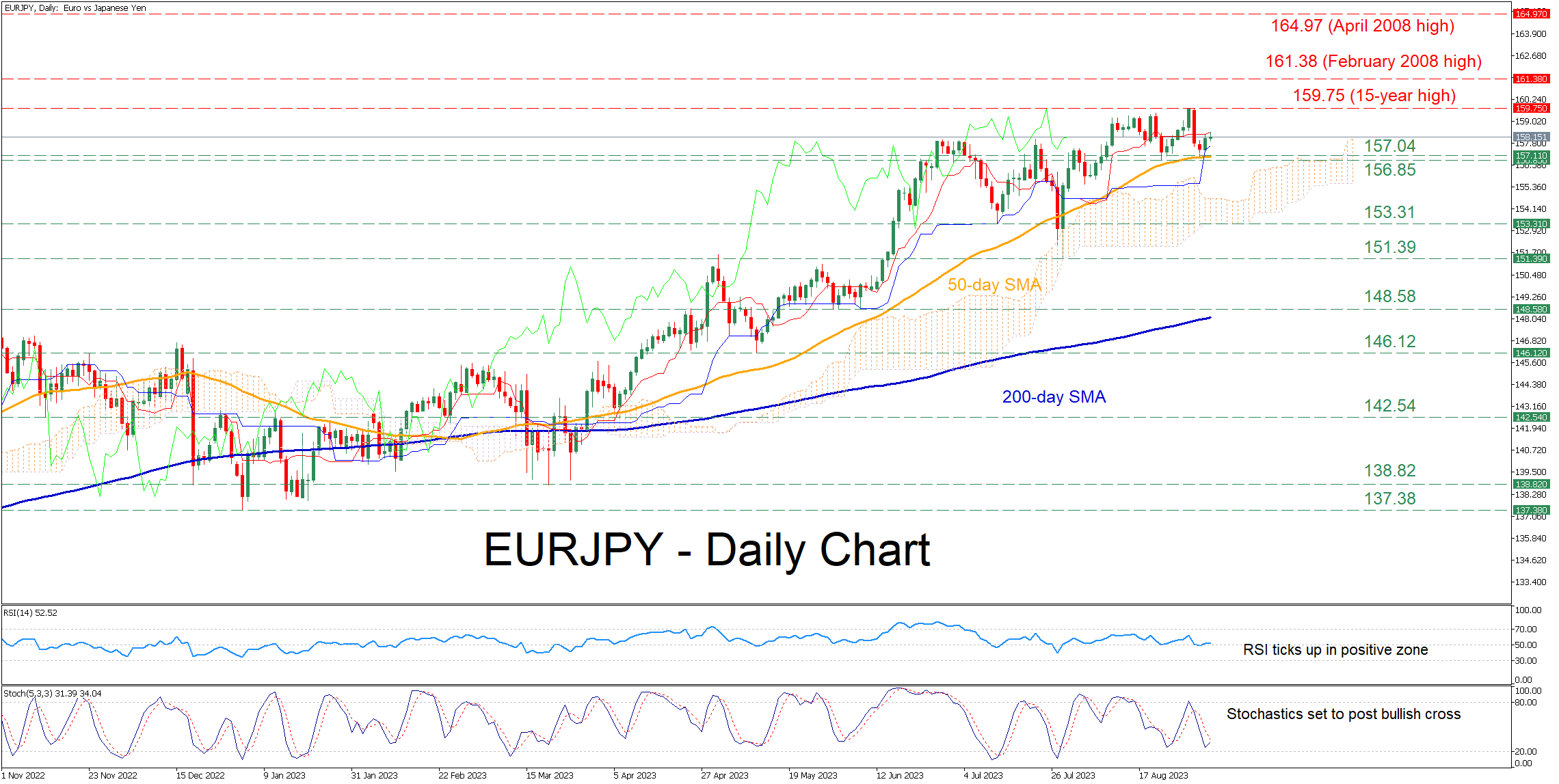

EURJPY Rebounds from 50-day SMA

EURJPY has been in a prolonged uptrend since the beginning of the year, posting a fresh 15-year peak of 159.75 on August 31. Although the pair experienced a pullback following its multi-year high, it managed to find its footing at the 50-day simple moving average (SMA) and recoup some losses.

The momentum indicators currently suggest that bullish forces are holding the upper hand. Specifically, the RSI is hovering above its 50-neutral mark, while the stochastic oscillator is set to post a bullish cross.

If the latest bounce extends, the bulls might initially attack the 15-year high of 159.75. Breaking above that zone, the pair could storm to fresh multi-year peaks, where the February 2008 high of 161.38 may curb further advances. Failing to halt there, the price might then ascend to challenge the April 2008 high of 164.97.

On the flipside, should the price reverse back lower, any declines could cease at the 157.04-156.85 range defined by the two latest support levels, while its upper end coincides with the 50-day SMA. A violation of that zone could trigger a retreat towards 153.31. Even lower, the July low of 151.39 may prove to be a tough hurdle for the price to overcome.

In brief, EURJPY regained traction following its unsuccessful test of the 50-day SMA. Can the latest recovery resume and enable the pair to revisit recent highs?

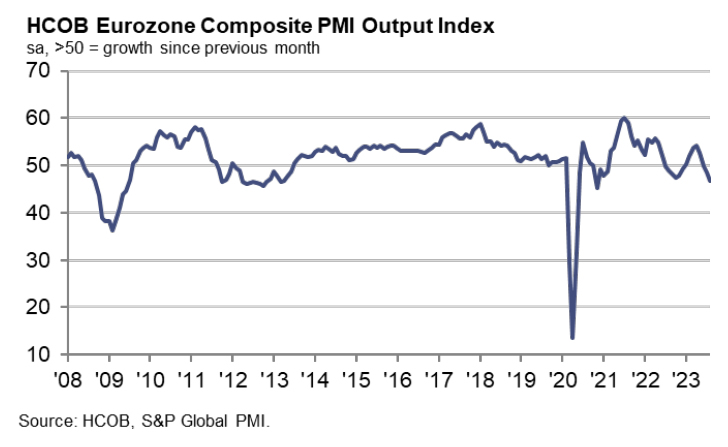

Eurozone PMI services finalized at 47.9, Q3 GDP to contract -0.1%

Eurozone is grappling with weakening economic indicators, as PMI Services for August (final) slipped to a 30-month low of 47.9, down from July's reading of 50.9. Composite PMI, which combines services and manufacturing data, also sank to a 33-month low of 46.7, down from July's 48.6.

The fall in PMI scores was particularly evident in Germany (44.6) and France (46.0), which reported 39-month and 33-month lows, respectively. On the other hand, Ireland managed to score a 4-month high of 52.6, showing some resilience amid the general downturn.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, provided a sobering analysis. "The disappointing numbers contributed to a downward revision of our GDP nowcast, which stands now at -0.1% for the third quarter," he said. According to de la Rubia, the services sector, a stabilizer for Eurozone economy, has turned into a "drag".

Furthermore, he noted that input price increases have surprisingly accelerated, questioning the outlook for rapidly decreasing inflation. Employers are also becoming cautious about expanding their workforces, hinting that job cuts could be on the horizon.

JP225 Cash Index Bulls’ Determination in Question

The JP225 cash index is trying to register its fourth consecutive green candle but the rally seems to have halted temporarily at the June 16, 2023 downward sloping trendline. This is the third time that this trendline appears to limit the bulls’ appetite, allowing the formation of a bearish series of lower lows and lower highs.

In the meantime, the momentum indicators remain mostly on the bulls’ side. The RSI has made a higher high, but it appears to be moving sideways now. Additionally, the Average Directional Movement Index (ADX) is hovering comfortably above its 25-threshold, and thus signaling the presence of a bullish trend in the market. More interestingly, the stochastic oscillator has just entered its overbought territory, still holding a good gap from its moving average. However, this move could be a very early signal that the current rally could be close to its completion. In addition, a developing bearish divergence is casting a shadow over the recent JP225 index advance.

Should the bulls remain committed in continuing the rally, they would try to break above the June 16, 2023 downward sloping trendline. If successful, they would then have the chance to make a higher high and potentially test the June 16, 2023 high at 34,006.

On the other hand, the bears are trying to stage a reversal. They could try to defend the June 16, 2023 trendline, push the JP225 cash index below the 50-day simple moving average (SMA) and towards the 31,665-31,764 range. This region is populated by the 23.6% Fibonacci retracement level of the March 8, 2022 – June 16, 2023 uptrend and the 100-day SMA, and if broken it would give the bears the chance to record the lowest print since June 3, 2023.

To sum up, the JP225 index bulls are in control but the stochastic oscillator’s recent moves are raising questions on the viability of the current upside move.

RBA Board Left the Cash Rate Unchanged at 4.1%

The Governor’s decision statement was widely anticipated including maintaining the soft tightening bias.

The decision by the Reserve Bank Board to hold the cash rate at 4.1% was seen as a near certainty by most market commentators.

While the Board considered two options in August – ‘on hold’ or a 0.25% rate increase –the Minutes from that meeting showed a clear preference for the ‘on hold’ option without the qualifications seen in July which the Minutes to that meeting described as a ‘finely balanced’ decision.

Since the August Board meeting there has been: further evidence of an easing in wage pressures; some softening in the labour market; a further fall in inflation as measured by the monthly inflation indicator; and more timely indicators pointing to weak consumer spending. There has also been extensive coverage of the problems now being faced by the Chinese property sector.

There were few significant changes in the Governor decision statement relative to the August meeting. Where there were shifts, these were broadly consistent with the encouraging data developments listed above.

The Governor is even more confident about the inflation trajectory, noting: “Inflation in Australia has passed its peak and the monthly indicator in July showed a further decline.”

Commentary on the labour market was a little more relaxed: “… conditions in the labour market remain tight” – softened a touch from last month’s “very tight”.

He also made note of risks around the China story: “… there is increased uncertainty around the outlook for the Chinese economy due to ongoing stresses in the property market.”

As we predicted in our pre-meeting note, despite rising confidence that the inflation target will be achieved, the statement retained the warning that “Some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe.”

The Board will be aware of the volatile Australian dollar and any indication that it was dropping its tightening bias would only add further downward pressure to the currency. It is already dealing with the uncertainties in China and the market’s discomfort with the official forecast for inflation to only reach 2.8% by end 2025 – only just within the band nearly three and a half years after the tightening cycle began.

Following the decision to keep rates on hold in August, Westpac called the end of the tightening cycle with the next move likely to be a rate cut cycle from August next year.

We believe that the likely ongoing weakness in spending and the continuing reduction in inflation is likely to close any window for further ‘insurance’ to assist with the return to target.

The Governor’s statement today certainly supports that view.

RBA Remains on Hold, Chinese Sluggish Recovery Continues, UK Retail Sales Bounce Back

The Australian dollar fell further this morning despite the RBA holding interest rates steady and warning that further tightening may be necessary.

The central bank warned that while inflation is declining, a strong labour market and economy remain a risk. What's more, persistent services price inflation which is being seen in other countries could be another potential upside risk in Australia in the future.

Markets aren't buying the hawkish warning though and continue to price in a 70% chance of no further increases from the RBA, with cuts then likely to start late next year. This will almost certainly change repeatedly over the months ahead but as things stand, clear progress is being made on inflation and the central bank has no desire to needlessly crash the economy.

Chinese services PMI slips amid an ongoing sluggish recovery

Australia's biggest trading partner, China, is continuing its sluggish recovery this year with the latest Caixin services PMI slipping back to 51.8 from 54.1 and well below forecasts. As we saw in the official survey data last week, it highlights the economy is struggling from both weak internal and external demand.

Measures to support the economy have been limited and targeted so far and there's little to suggest that approach is going to change in the foreseeable future. The PMI data may be contributing to the weaker performance in China and Hong Kong overnight and the uninspiring start in Europe.

UK retail sales promising but headwinds remain

UK retail sales bounced back in August after a disappointing performance in July, likely hampered by the weather. The rebound is encouraging but there are a number of things to consider from inflation to one-off events like the success of the Lionesses in the World Cup in boosting activity.

On the plus side, inflation is falling and wage growth will likely surpass it for the rest of the year but there's no guarantee that will lead to an increase in spending. Higher interest rates will mean higher mortgage costs, and perhaps paying down debt and more cautious spending activity in the run-up to Christmas. Household spending has remained resilient though and that's encouraging.

Chinese PMI may have contributed to halt in Oil rally

Oil prices are steady for a second day after another strong performance last week. Brent continues to trade close to $90 and despite the slow start this week, momentum remains with the rally. The Chinese data this morning may have stood in the way of further gains so far today but it will be interesting to see whether it can add to recent gains after rising to 2023 highs in recent weeks.

Gold continues to consolidate after the US jobs report

Gold has slipped back from $1,950 in recent days, still struggling in the aftermath of the US jobs report which could have been a bullish catalyst for it. Instead, it's consolidated just below these levels and it's hard to say whether that is bullish or bearish. A consolidation of this kind could be argued to be technically bullish but the failure to progress after that jobs report is a little odd and perhaps even a bearish signal.