Sample Category Title

Aussie Dollar Remains in the Defensive

Markets

German bonds traded solo yesterday as US financial markets enjoyed a long weekend. They added between 2-4.3 bps in a move partially inspired by comments from ECB’s Wunsch. Unlike Wunsch, ECB president Lagarde at a London seminar yesterday did not reveal her preference for one or the other policy move at the September meeting. It remains a knife edge decision with money markets currently discounting only a 25% chance for a hike. The euro crept a little higher in an otherwise dull session. EUR/USD tried to recover the 1.08 a few times but in vain. EUR/GBP trended south to close at 0.855. Equities in Europe started off well thanks to a good Asian session. But gains of <1% gradually evaporated throughout the session. The likes of the EuroStoxx50 eventually finished flat (-0.06%).

Sentiment in the east meanwhile turned more gloomy compared to Monday. A weaker-than-expected Chinese services PMI (51.8, down from 54.1) underscores the fragile state of the economy, despite the range of measures (some yet to be implemented) taken by the government. Losses amount to 1.5% in Hong Kong. US Treasury yields on their first trading day add about as much as Bund yields did yesterday with changes varying from 1.8-2.9 bps. The US dollar catches a bid and shares the first place in the G10 landscape with the euro. EUR/USD as a result trades sideways sub 1.08. The Australian dollar underperforms with the status quo from the Reserve Bank of Australia not helping (see headline below).

After the Chinese PMIs and RBA decision, the focal point of the remaining economic releases shifts towards Europe. The ECB’s consumer inflation expectations survey is due today. It serves as important input, one of the last, to the September 14 policy meeting. Interest rate markets probably are still more sensitive to a downward surprise in a daily perspective. But we don’t think that it’ll dissuade the ECB from one more hike given stubborn (core) inflation. Sticking to the subject of prices, keep a close eye at oil. Brent has surged >20% since July and that may soon find its way in the m/m readings as well as dampen the current fabourable base effects in the y/y gauges. EUR/USD’s technical picture continues to look dire with the pair unable to depart from the lower bound of the upward sloping trading range. The dollar still holds the better card, making a break lower still look more likely than not. US money markets attach a (much) lower probability to a final Fed rate hike than their European counterparts do for the ECB (September or later). This provides the USD and (short-term) interest rate markets upward potential which could well materialize in case US data continues to show economic resilience.

News and views

Consumer price inflation in South Korea in August accelerated at a much faster pace than expected. Prices jumped 1.0% M/M, the biggest monthly gain since January 2017. The Y/Y measure printed at 3.4% Y/Y up from 2.3% Y/Y in July. The jump was mainly driven by an increase in oil prices since mid-July and unfavourable seasonal factors raising the cost of agricultural products. Food price rose 2.9% M/M . Transportation costs were 3.8% higher compared to the previous month. Core CPI excluding food and energy prices was unchanged at 3.3% Y/Y. The Bank of Korea in August kept its policy rate unchanged at 3.5% since January 2023. Today’s data will keep the BOK on alert and doesn’t leave room for a rate cut in the near future despite risks to the growth outlook. The won this morning is losing modest ground to USD/KRW 1325.4. This compared to levels of USD/KRW near 1257 mid-July and at YTD low (high for the won) at 1216 early February.

The Reserve Bank of Australia today as expected kept its policy rate unchanged at 4.1.%. According to the RBA ‘the higher interest rates are working to establish a more sustainable balance between supply and demand in the economy and will continue to do so’. This leaves the RBA further time to assess incoming data. The Australian economy is experiencing a period of below-trend growth and this is expected to continue for a while. Even so, conditions on the labour market remain tight. Monthly CPI in July continued to decline (4.9% Y/Y), but remains too high and will remain so for some time. The RBA forecast is for CPI inflation to continue to decline and to be back within the 2–3 per cent target range in late 2025. The RBA concludes that some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe. Today was the last meeting chaired by Governor Philip Lowe. Deputy Governor Michele Bullock will replace Lowe starting 18 September. The market reaction to the decision was modest. The 3-y government bond yield adds 1 bp (3.81%). The Aussie dollar remains in the defensive easing to AUD/USD 0.642, but most of this move already occurred before the RBA decision.

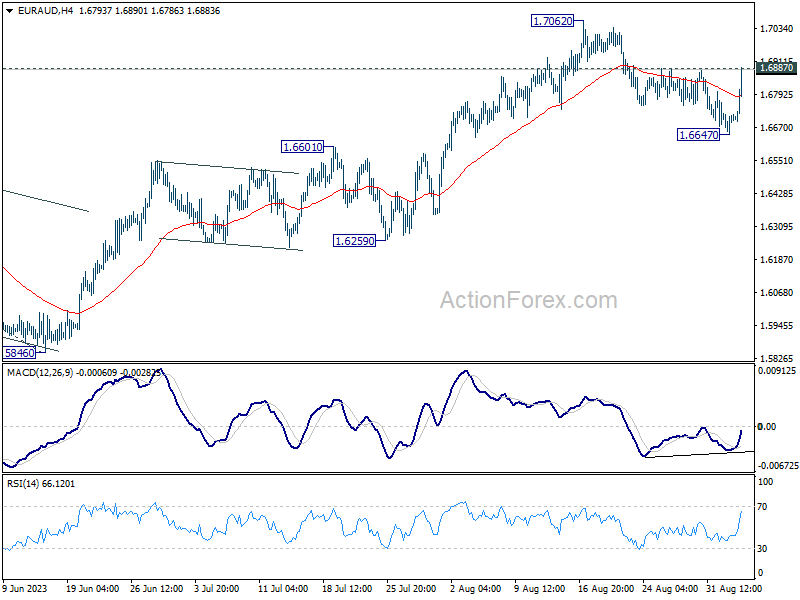

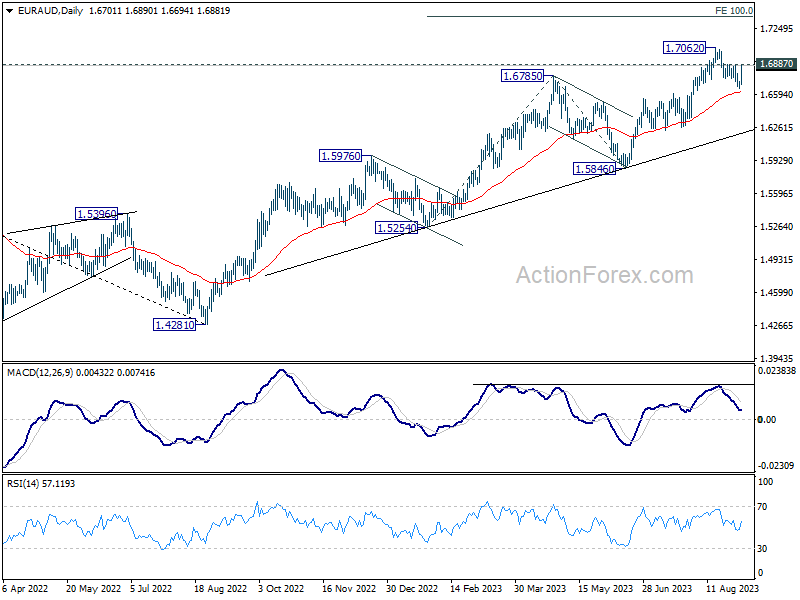

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6664; (P) 1.6695; (R1) 1.6740; More...

Immediate focus is now on 1.7887 resistance will today's rebound. Firm break there should confirm that correction from 1.7062 has completed at 1.6647. Further rally should be seen through 1.7062 to 1.7377 projection level. On the downside, break of 1.6647 will extend the correction lower instead.

In the bigger picture, the rise from 1.4281 (2022 low) is in progress. Next target is 100% projection of 1.5254 to 1.6785 from 1.5846 at 1.7377. For now, outlook will stay bullish as long as 1.5846 support holds, even in case of deep pull back.

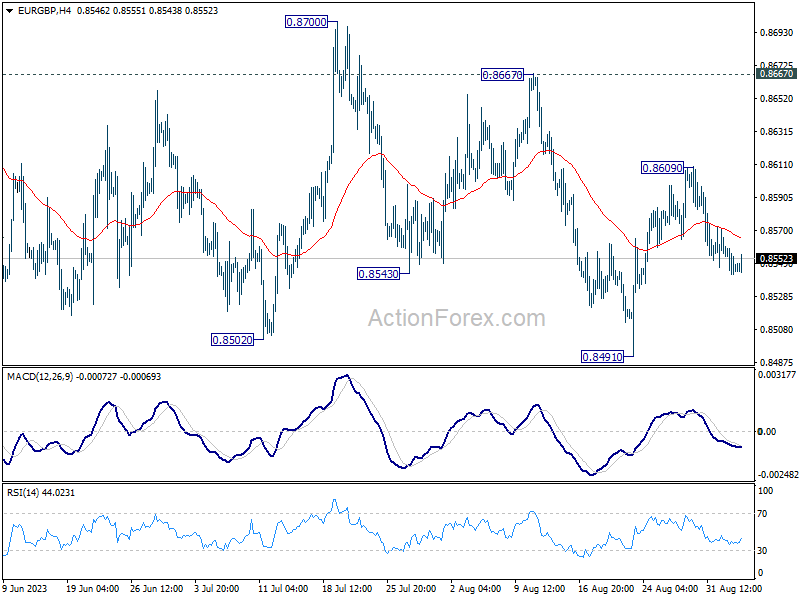

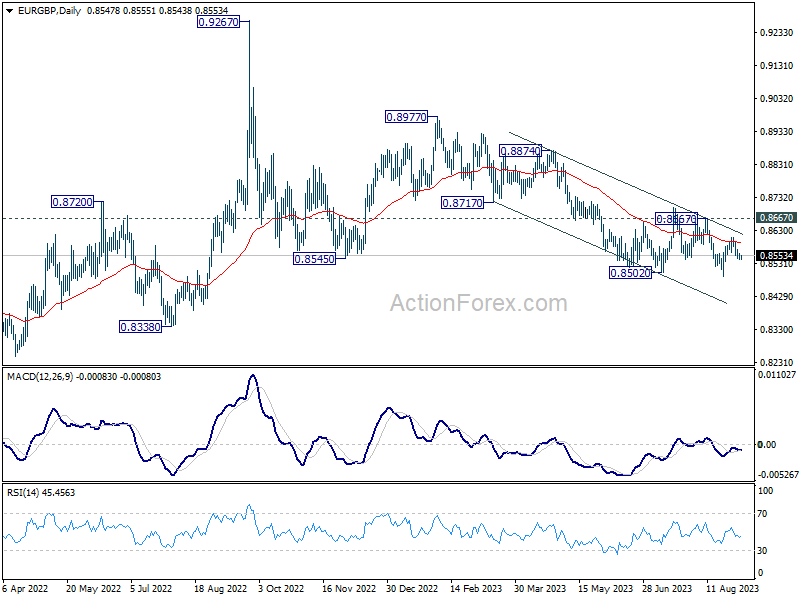

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8541; (P) 0.8552; (R1) 0.8559; More...

No change in EUR/GBP's outlook and intraday bias stays mildly on the downside. Deeper fall would be seen to retest 0.8491 low. Firm break there will resume larger down trend. On the upside, above 0.8609 minor resistance will bring another rebound. But in any case, outlook will stay bearish as long as 0.8667 resistance holds.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Further decline is in favor as long as 0.8667 resistance holds. Break of 0.8491 will resume the fall towards 0.8201 (2022 low).

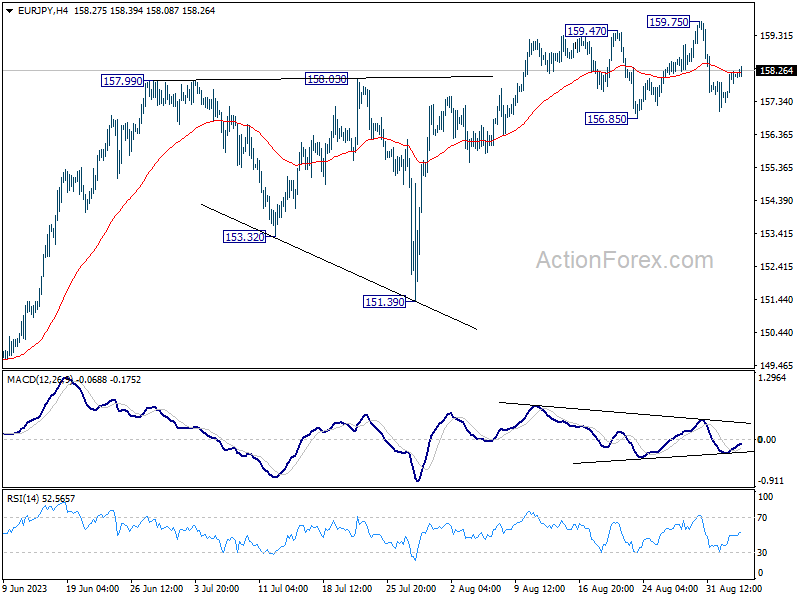

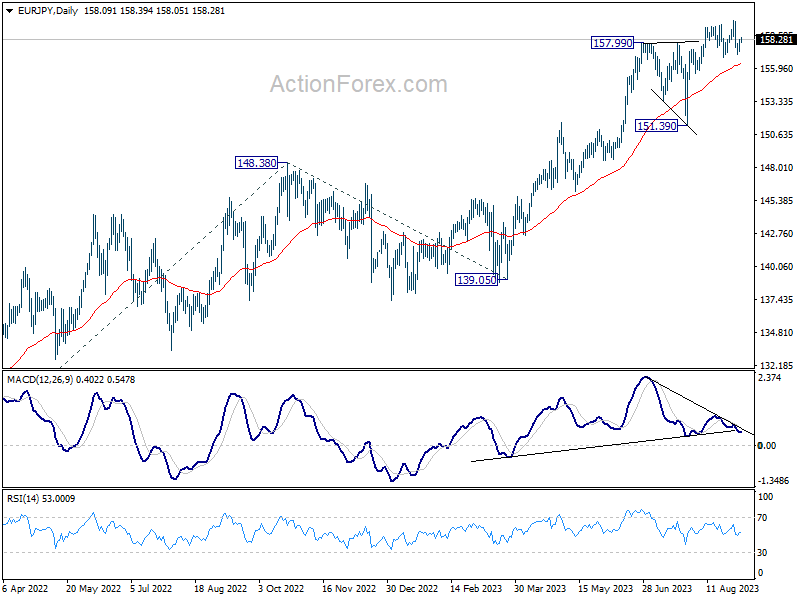

EUR/JPY Daily Outlook

Daily Pivots: (S1) 157.58; (P) 157.91; (R1) 158.50; More....

EUR/JPY is still extending the sideway consolidation pattern and intraday bias remains neutral. On the downside, break of 156.85 will turn bias back to the downside for 55 D EMA (now at 156.36) and possibly below. On the upside, break of 159.75 will resume larger up trend instead.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 100% projection of 124.37 to 148.38 from 139.05 at 163.06. Sustained break there will pave the way to retest long term resistance at 169.96. This will remain the favored case as long as 151.39 support holds, even in case of deep pull back.

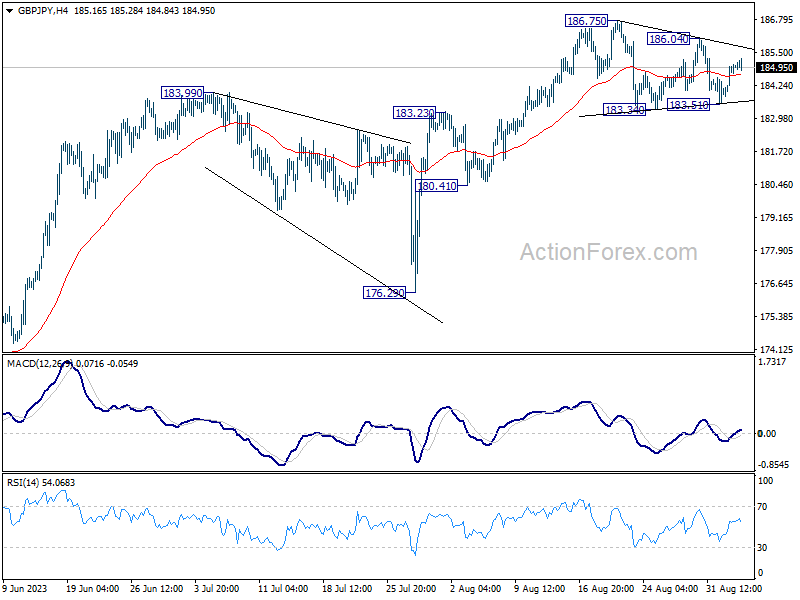

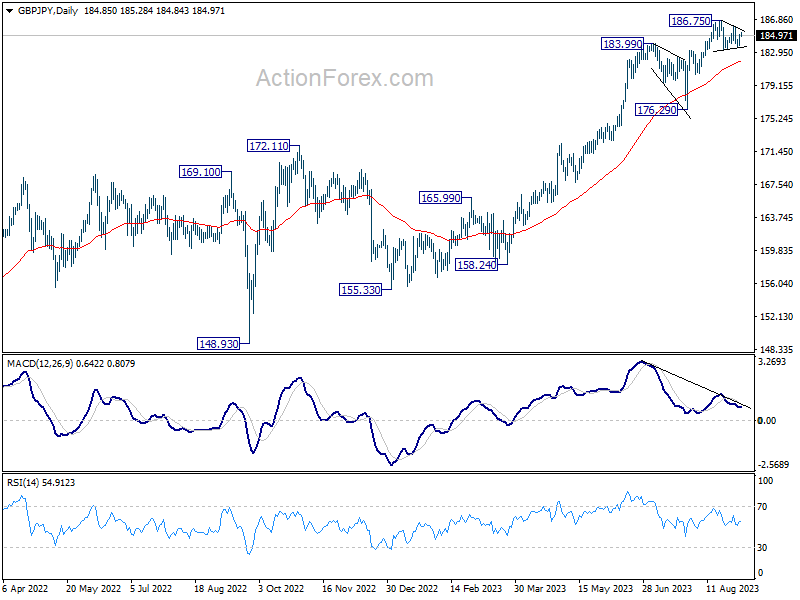

GBP/JPY Daily Outlook

Daily Pivots: (S1) 184.21; (P) 184.64; (R1) 185.44; More...

GBP/JPY is extending the consolidation pattern from 186.75 and intraday bias remains neutral. On the upside, above 186.04 will argue that larger up trend is ready to resume through 186.75. On the downside, however, break of 183.51 will bring deeper correction to 55 D EMA (now at 181.98).

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Next target is 195.86 (2015 high). This will remain the favored case as long as 176.29 support holds, even in case of deeper pull back.

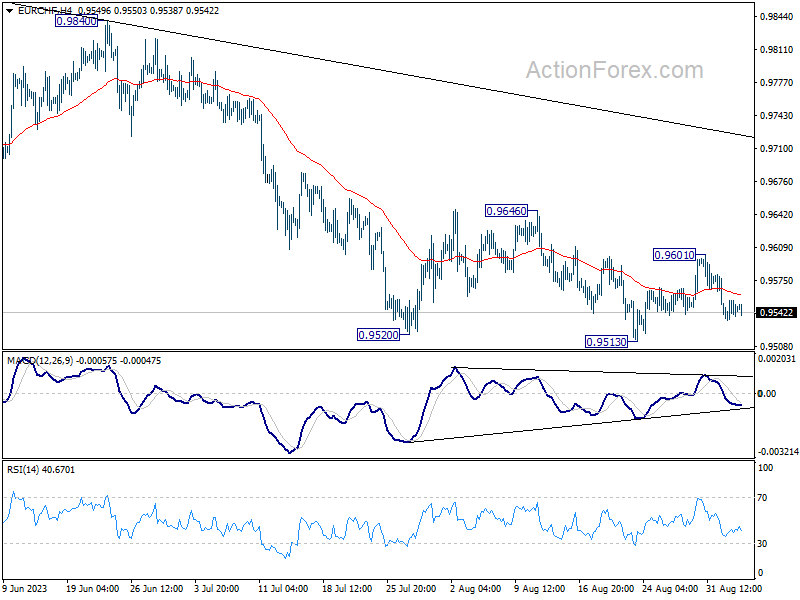

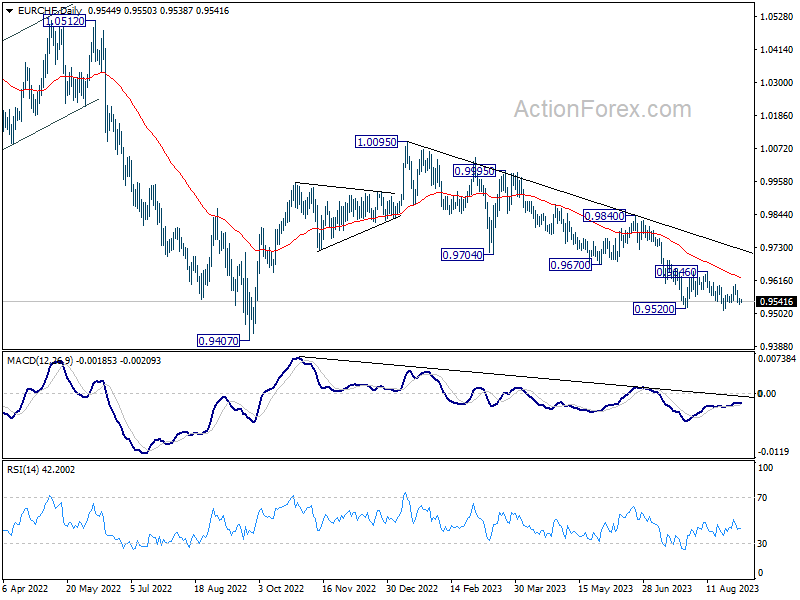

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9538; (P) 0.9547; (R1) 0.9559; More...

EUR/CHF is staying in range above 0.9513 and intraday bias stays neutral at this point. With 0.9601 resistance intact, larger down trend is still in favor to continue. On the downside, break of 0.9513 support will confirm this bearish case and target 0.9407 low. Nevertheless, break of 0.9601 resistance will turn bias back to the upside for stronger rebound to 0.9646 resistance and above.

In the bigger picture, medium term outlook is staying bearish as the pair is capped well below falling 55 W EMA (now at 0.9839). Down trend from 1.2004 (2018 high) is in favor to continue. Sustained break of 0.9407 will target 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. For now, this will remain the favored case as long as 0.9670 support turned resistance holds, in case of strong rebound.

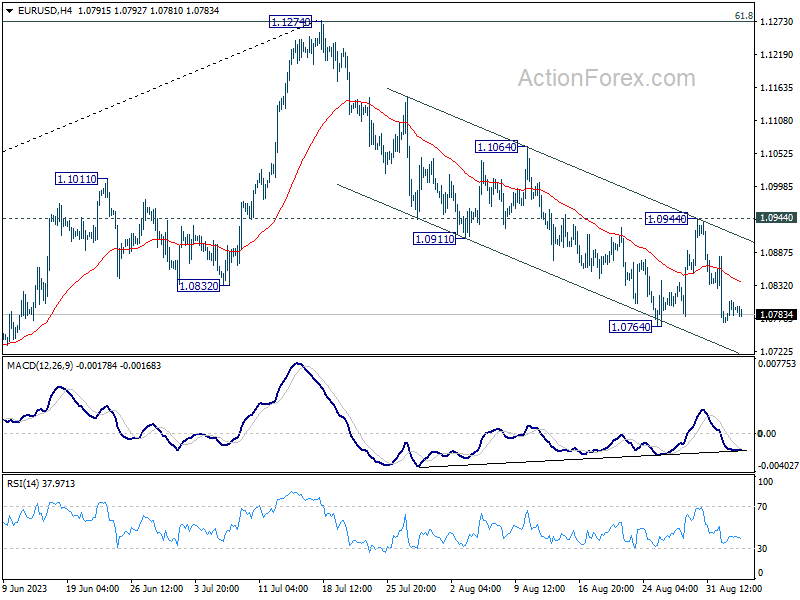

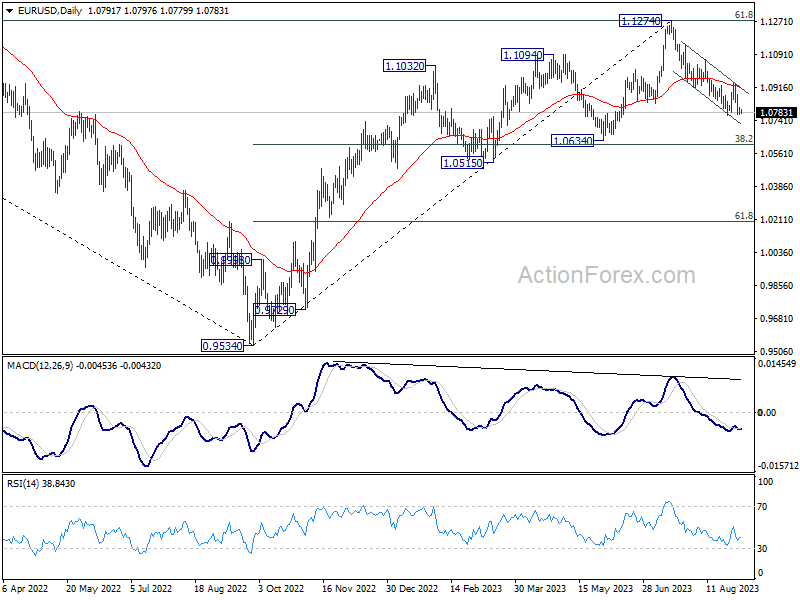

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0776; (P) 1.0793; (R1) 1.0813; More...

EUR/USD is staying in consolidation from 1.0764 and intraday bias stays neutral. Further decline is in favor with 1.0944 resistance intact. On the downside, firm break of 1.0764 support will resume whole decline from 1.1274 to 1.0609/34 cluster support next.

In the bigger picture, fall from 1.1274 medium term top is seen as a correction to up trend from 0.9534 (2022 low). Deeper decline would be seen to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to bring rebound. Yet, medium term outlook will be neutral for now, as long as 1.1274 resistance holds.

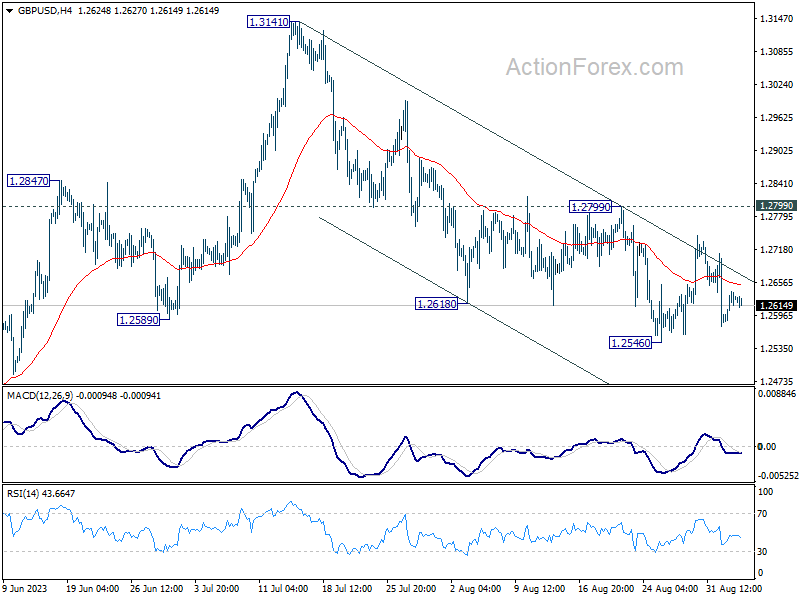

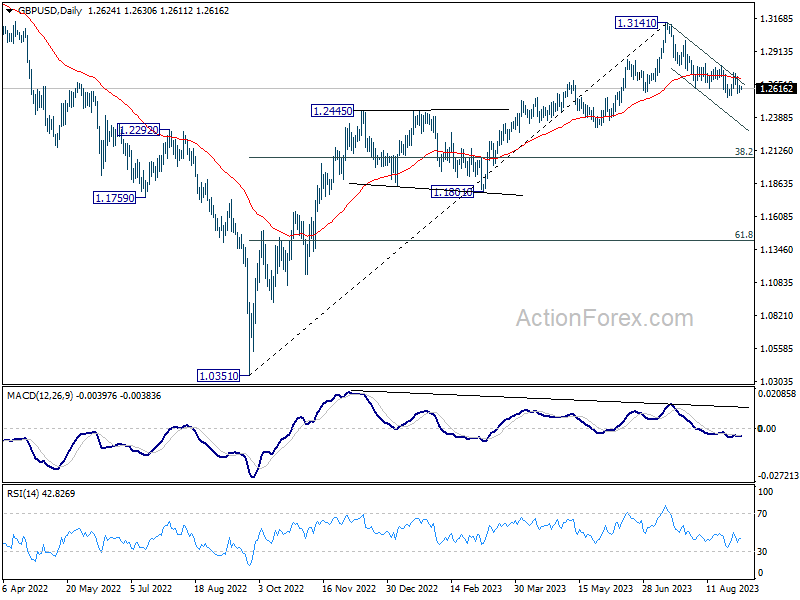

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2596; (P) 1.2620; (R1) 1.2652; More...

GBP/USD is staying in consolidation above 1.2546 and intraday bias stays neutral. Further decline is in favor with 1.2799 resistance intact. Break of 1.2546 will resume the fall from 1.3141. However, on the upside, firm break of 1.2799 will indicate that the correction from 1.3141 has completed. Intraday bias will be turned back to the upside for retesting 1.3141.

In the bigger picture, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. But outlook will be neutral at best as long as 1.3141 resistance holds, and consolidation from there is set to extend, until further development.

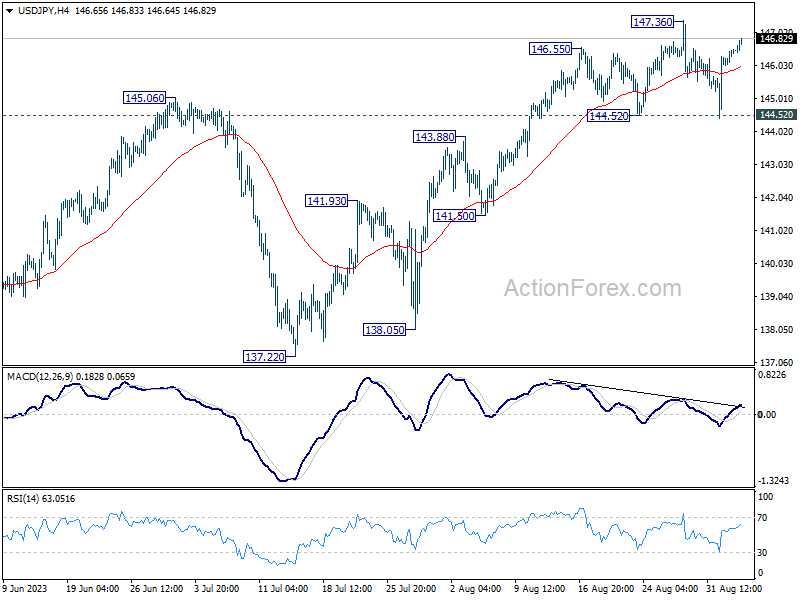

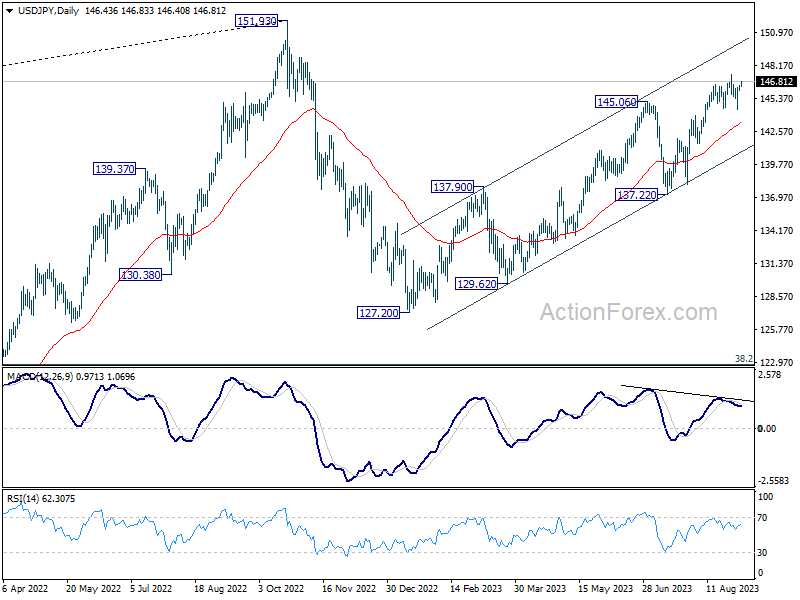

USD/JPY Daily Outlook

Daily Pivots: (S1) 146.18; (P) 146.34; (R1) 146.65; More...

USD/JPY is staying in consolidation from 147.36 and intraday bias remains neutral. On the upside, firm break of 137.36 will resume larger rally to retest 151.93 high. However, on the downside, firm break of 144.52 should confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 143.31) and possibly below.

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

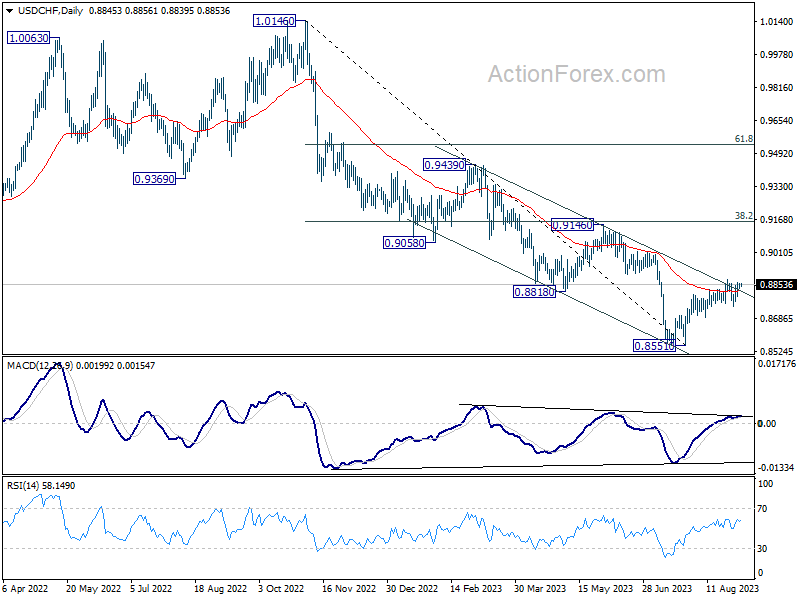

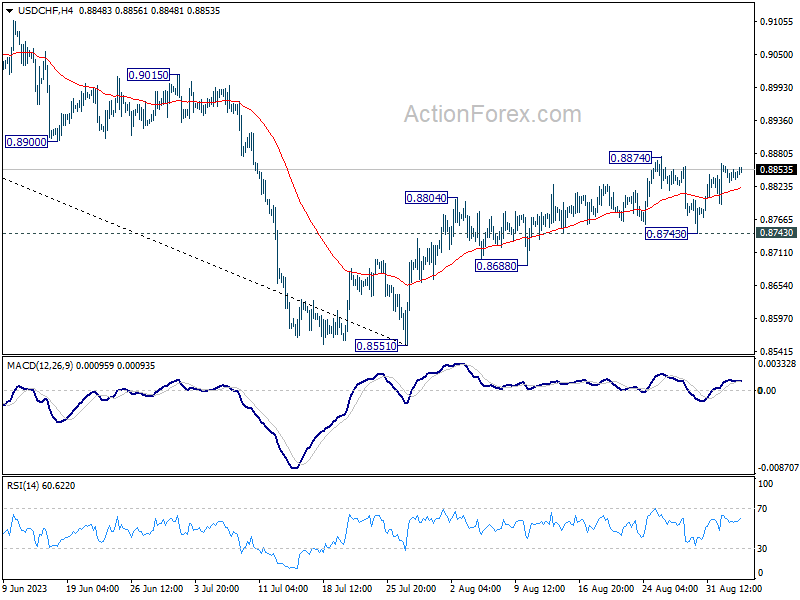

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8831; (P) 0.8847; (R1) 0.8860; More....

USD/CHF is staying in consolidation from 0.8874 and intraday bias remains neutral. On the upside, firm break of 0.8874 will resume the rise from 0.8551. Next target is 0.9146 cluster resistance. On the downside, though, break of 0.8743 minor support will argue that rebound from 0.8551 has completed, and bring retest of this low.

In the bigger picture, rebound from 0.8551 medium term bottom is currently seen as a correction to the downtrend from 1.0146 (2022 high). Further rally would be seen to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160). Strong resistance could be seen there to limit upside, at least on first attempt.