Sample Category Title

Crypto Market Cools Down; XRP in Accumulation Phase

Market picture

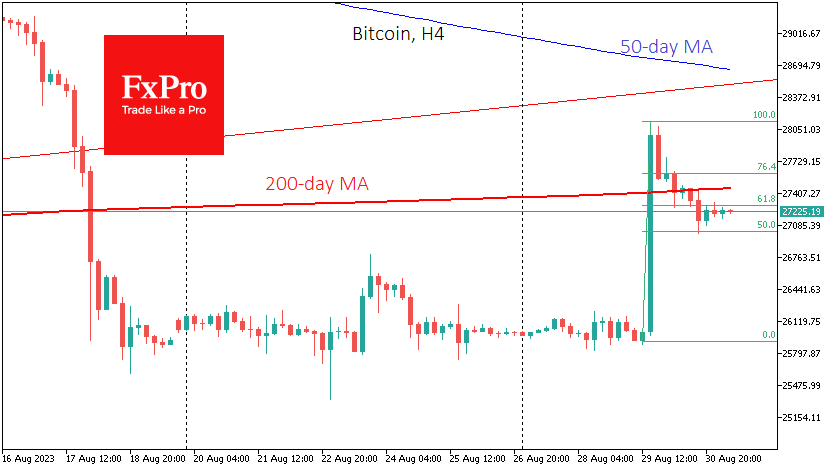

The crypto market is cooling after a surge in buying on the 29th, losing 0.8% over the past 24 hours to $1.085 trillion, but still almost 4% higher than before the jump. Crypto Fear and Greed Index has returned to neutral territory after a week and a half of wandering in “Fear”.

Bitcoin briefly dipped to $27K on Wednesday, about half of its initial jump from $26K to $28K and back below its 200-day and 200-week averages, despite the increased traction of risk in traditional markets. From the looks of it, the decisive trend battle won’t come until Friday evening at the earliest, with consolidation around current levels all the way through.

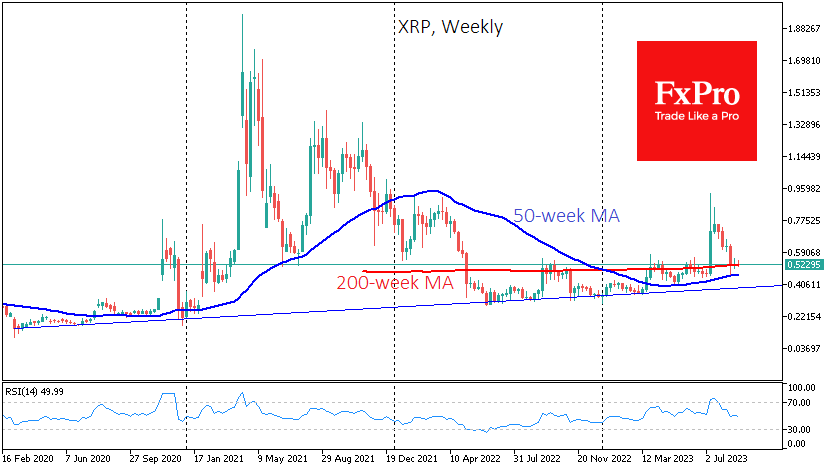

XRP has performed worse than the cryptocurrency market over the past few days, having erased almost all gains of its latest leap. On a weekly timeframe, long-term support appears to have been taken over by the 200-week average (now $0.516). A fortnight ago, the sell-off stopped at the 50-week average ($0.457). Both curves are well above the multi-year uptrend line, which now runs through $0.39. This dynamic could attract more speculators soon, with an upside potential of $0.60 or even $0.80.

News Background

According to Raul Pal, founder of Real Vision, ongoing Bitcoin consolidation could well end with a powerful spike. According to him, BTC is growing exponentially after periods of low volatility.

Bloomberg Intelligence suggests that stablecoins will be more popular than BTC in the short term.

Company X, formerly known as Twitter, has obtained the necessary licence to provide cryptocurrency payment and trading services in the US. This is a positive sign for the future of crypto on the platform.

BlackRock has invested over $400 million in the shares of four mining companies, making it one of the largest lobbyists for the Bitcoin industry in the US.

During the SEC’s case against Binance, the regulator filed a sealed motion containing 35 exhibits, a statement from the agency’s trial counsel and a proposed order. The commission did not want the data submitted to the court to be made public, a rare occurrence according to legal experts.

The US Congress has proposed firing the head of the SEC following a court ruling that found Grayscale’s refusal to create a bitcoin ETF illegal.

NZD/USD Yawns as Business Confidence Improves

- New Zealand business confidence rises

- ADP Employment Change falls to 177,000

The New Zealand dollar is almost flat on Thursday, trading at 0.5958 in Europe.

New Zealand Business Confidence improves again

New Zealand’s ANZ Business Confidence index accelerated for a fourth straight month in August. The index improved to -3.7, up from -13.1 in July. Business Confidence has been in negative territory for 26 consecutive months, but the August print was the highest since June 2021. The consensus estimate stood at -1.9 and the New Zealand dollar didn’t react. If the upswing continues, we should see a positive reading in the next month or two, which would be a milestone and likely give a boost to the New Zealand dollar.

The business confidence report noted that inflation expectations dipped very slightly, from 5.14% to 5.06%. This is clearly incompatible with a 2% inflation target but the key question is whether the Reserve Bank of New Zealand will pause for a third straight time in October, in the hope that the benchmark rate of 5.50% will further cool the economy and push inflation lower.

The RBNZ doesn’t meet until October 4th, with only one tier-1 event prior to the meeting, which is GDP on September 20th. The central bank will also be keeping a close eye on events in China, where the economy has been deteriorating. On Thursday, China’s Manufacturing PMI rose in July to 49.7, up from 49.3 in June, but this marked a fifth straight contraction.

In the US, the markets await the non-farm payrolls release on Friday. The ADP employment report fell sharply to 177,000, down from an upwardly revised 371,000 and shy of the estimate of 195,000. The ADP release isn’t a reliable precursor to nonfarm payrolls but still attracts attention as investors hunt for clues ahead of the nonfarm payrolls release. The markets are expecting nonfarm payrolls to fall to 170,000 in August, compared to 187,000 in July.

NZD/USD Technical

- There is support at 0.5927 and 0.5866

- 0.5968 is a weak resistance line. Above, there is resistance at 0.6029

ECB Schnabel: Underlying price pressures remain stubbornly high

ECB Executive Board member Isabel Schnabel said in a speech that despite decline in headline inflation, largely due to unwinding of previous supply-side shocks, "underlying price pressures remain stubbornly high," with domestic factors now becoming the main drivers of inflation.

Given this backdrop, Schnabel emphasized the necessity of maintaining "sufficiently restrictive monetary policy" to steer inflation back to target. She advocated for a data-dependent approach, stating that the bank will continually assess whether current policy is effective in ensuring "a sustained and timely return of inflation to our 2% target."

To guide this assessment, Schnabel pointed to the need for a comprehensive risk analysis that looks beyond baseline inflation forecasts. This approach accounts for an "exceptionally large degree of uncertainty" in medium-term inflation projections, with risks on both the upside and downside.

Upside risks include stronger-than-expected growth in unit labor costs, firmer corporate pricing power, and the potential for new adverse supply-side shocks. Conversely, downside risks include possibility that impact of current monetary policy may become more pronounced over the medium term.

Notably, Schnabel also raised the issue of real risk-free rates, which have declined recently as investors reassess their expectations for economic growth and inflation. She warned that this decline could potentially "counteract" the ECB's efforts to control inflation effectively.

Fed Bostic said policy restrictive enough, warns against unnecessary economic pain

In a set of prepared remarks, Atlanta Fed President Raphael Bostic noted emphasizing that the current restrictive stance is appropriate. He urged for a cautious and patient approach, warning against the potential for "unnecessary economic pain" if the Fed tightens policy too aggressively.

Importantly, Bostic clarified that his endorsement for a patient approach should not be interpreted as support for easing monetary policy in the near term. He stated, "that does not mean I am for easing policy any time soon."

He argued that Fed must remain "resolute" in keeping policy tight until it is clear that inflation is moving towards the 2% target within a reasonable time frame. "I believe policy is already restrictive enough to get us there," he added.

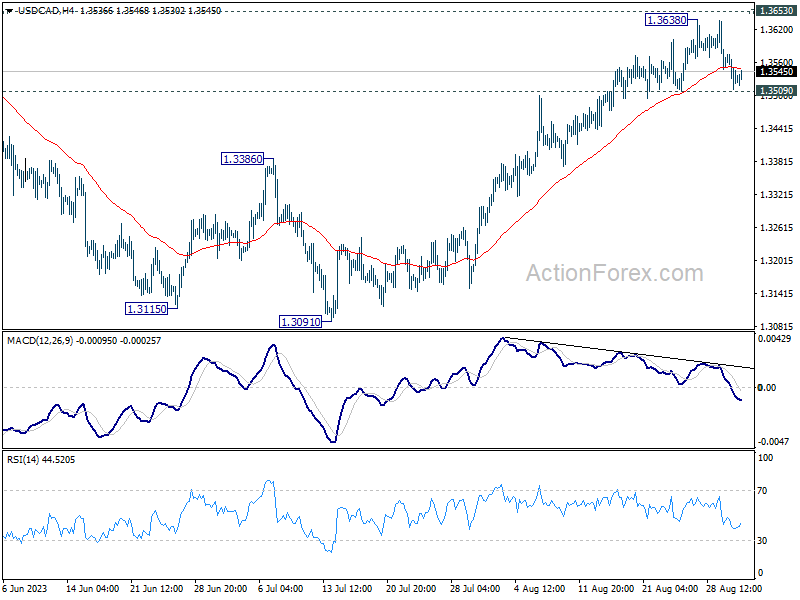

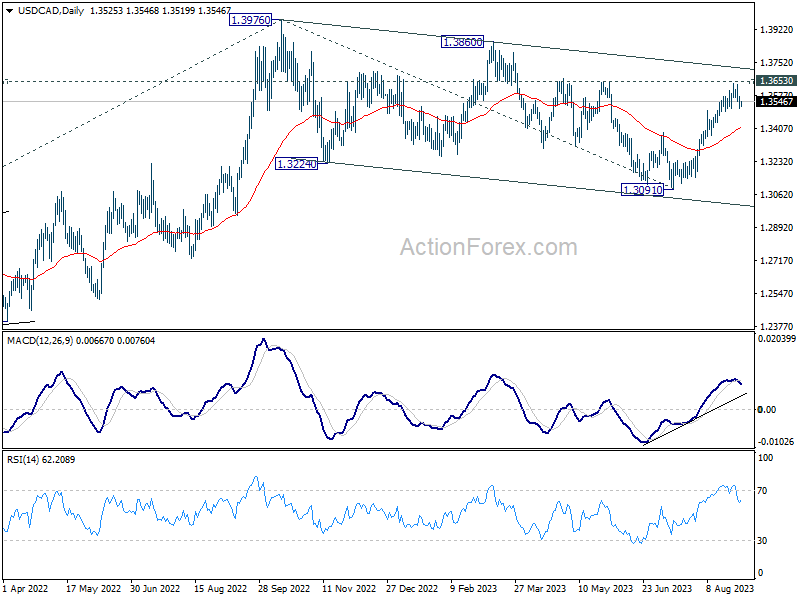

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3504; (P) 1.3541; (R1) 1.3568; More....

USD/CAD is staying in range of 1.3509/3638 and intraday bias stays neutral. Further rally is still expected with 1.3509 support intact. On the upside, decisive break of 1.3653 resistance there will confirm that correction from 1.3976 has completed, and target a test on this high. On the downside, however, break of 1.3509 support will indicate short term topping, and turn bias to the downside for some correction first.

In the bigger picture, price actions from 1.3976 are viewed as a corrective pattern only. Upon completion, rise from 1.2005 (2021 low) would resume through 1.3976. Next target is 61.8% projection of 1.2005 to 1.3976 from 1.3091 at 1.4309. For now, this will remain the favored case as long as 55 D EMA (now at 1.3409) holds.

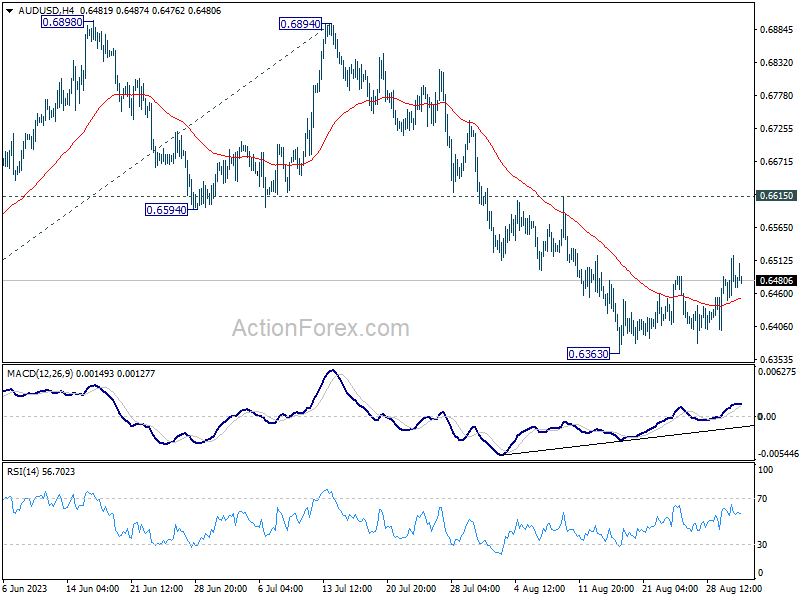

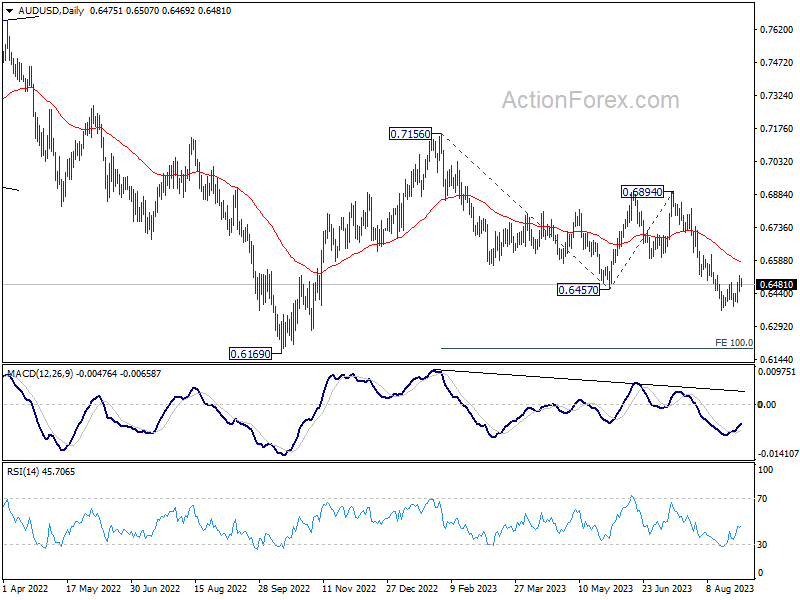

AUD/USD Daily Report

Daily Pivots: (S1) 0.6443; (P) 0.6482; (R1) 0.6515; More...

AUD/USD is extending the consolidation from 0.6363 and intraday bias remains neutral. Stronger recovery cannot be ruled out, but upside should be limited by 0.6615 resistance. Break of 0.6363 will resume larger fall from 0.7156 to 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195.

In the bigger picture, current development argues that the down trend from 0.8006 (2021 high) is still in progress. Decisive break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.

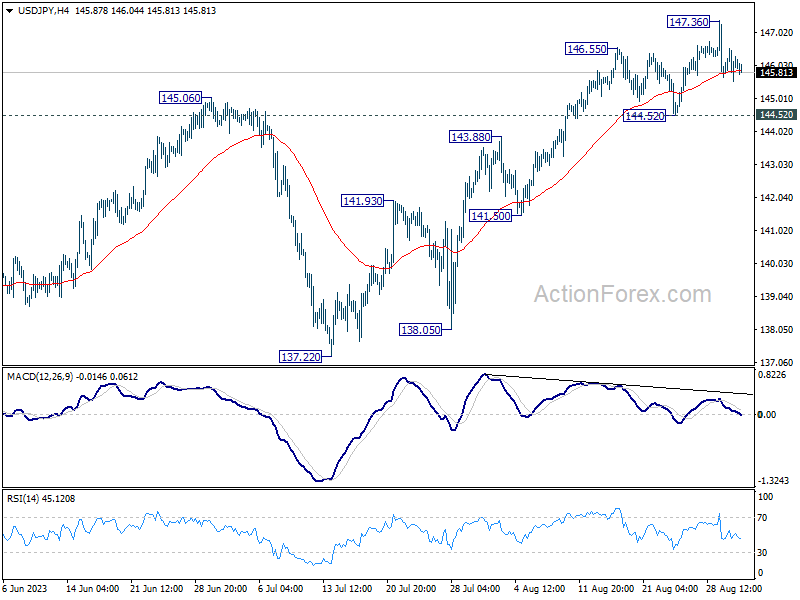

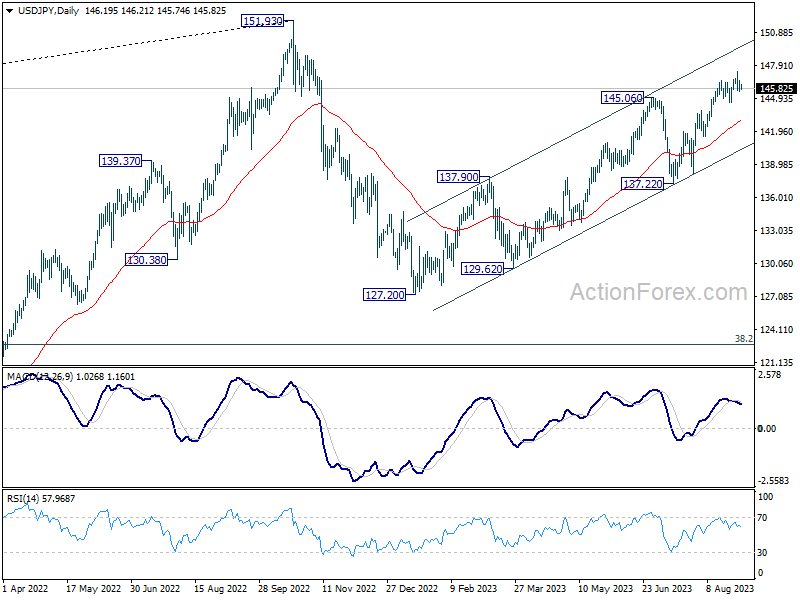

USD/JPY Daily Outlook

Daily Pivots: (S1) 145.70; (P) 146.12; (R1) 146.68; More...

USD/JPY is extending the consolidation from 147.36 and intraday bias remains neutral. As long as 144.52 support holds, further rally remains in favor. Above 147.36 will resume the rise from 127.20 to retest 151.93 high. On the downside, however, firm break of 144.52 should confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 142.96).

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

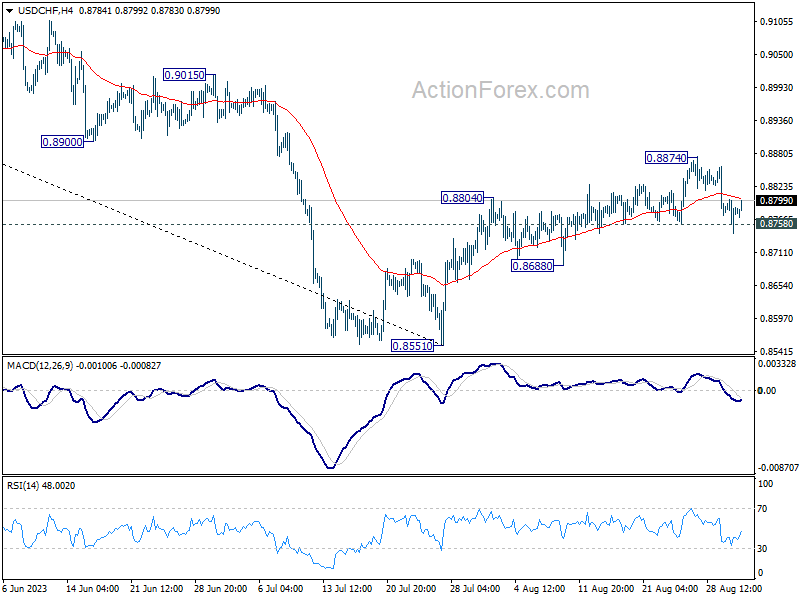

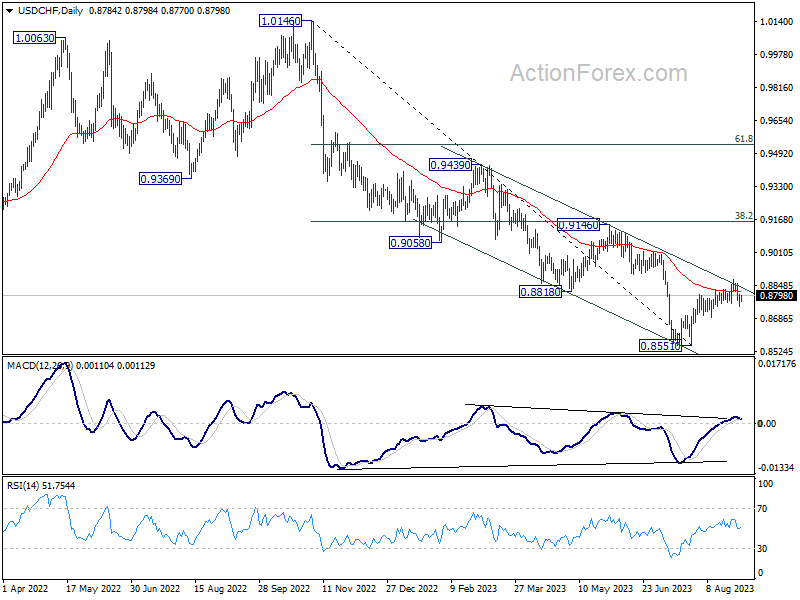

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8752; (P) 0.8778; (R1) 0.8811; More....

Focus stays on 0.8758 support in USD/CHF. Firm break there will argue that corrective rebound from 0.8551 has completed at 0.8874. Intraday bias will be turn back to the downside for 0.8688 support, and then 0.8551 low. Strong rebound from current level will retain near term bullishness though. Break of 0.8874 will resume the rise from 0.8551 to 0.9146 cluster resistance next.

In the bigger picture, rebound from 0.8551 medium term bottom is currently seen as a correction to the downtrend from 1.0146 (2022 high). Further rally would be seen to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160). Strong resistance could be seen there to limit upside, at least on first attempt. Nevertheless, medium term outlook is neutral at best as long as 0.8551 holds, until further developments.

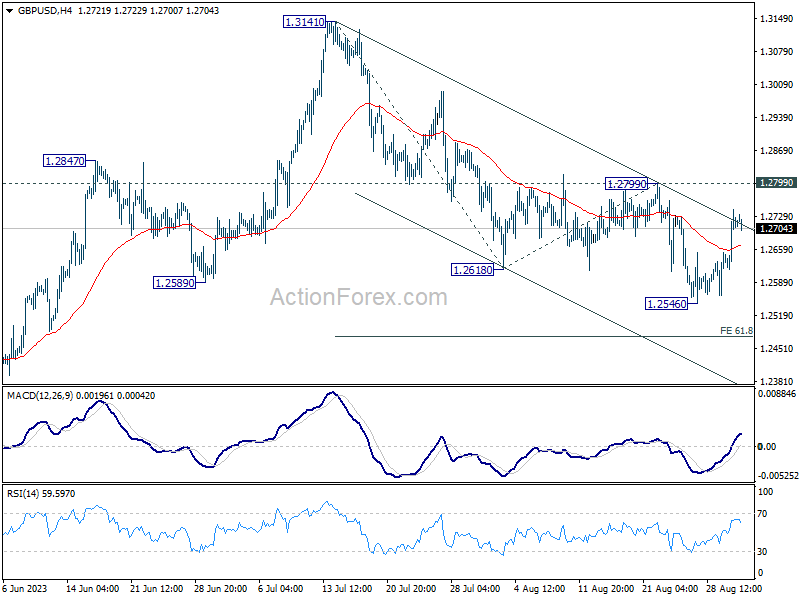

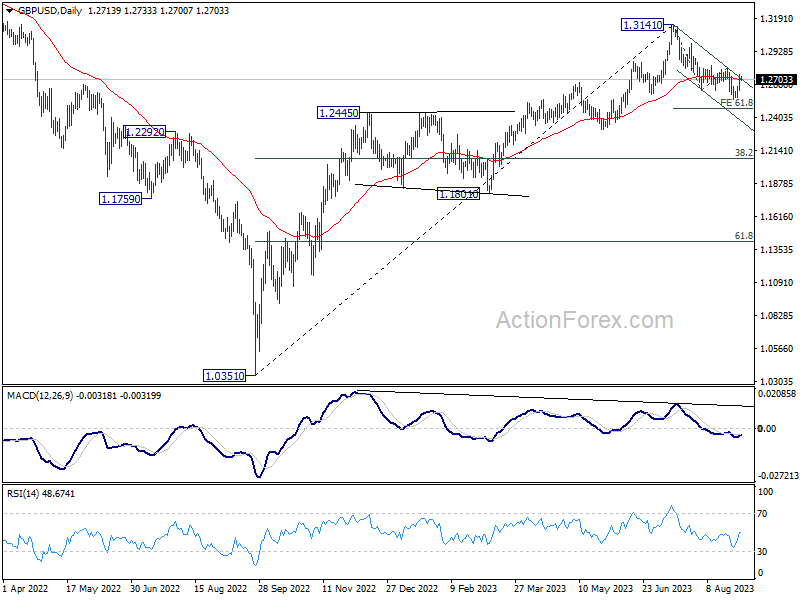

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2644; (P) 1.2696; (R1) 1.2772; More...

GBP/USD is staying in consolidation inside 1.2546/2799 and intraday bias remains neutral for the moment. On the downside, break of 1.2546 will resume whole fall from 1.3141 to 61.8% projection of 1.3141 to 1.2618 from 1.2799 at 1.2476. However, on the upside, firm break of 1.2799 will indicate that the correction from 1.3141 has completed with three waves down to 1.2546. Intraday bias will be turned back to the upside for retesting 1.3141.

In the bigger picture, for now, fall from 1.3141 medium term top is seen as a correction to up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3141 at 1.2075. Strong support would be seen there to bring rebound on first attempt. But outlook will be neutral at best as long as 1.3141 resistance holds, and consolidation from there is set to extend, until further development.

EUR/USD’s Downside Limited from Daily Perspective

Markets

Weaker-than-expected August ADP job creation and a downward revision to (outdated) US Q2 growth & PCE (core) inflation triggered a kneejerk move higher in US Treasuries yesterday. Gains didn’t survive the day though and yields eventually ended only marginally lower at the front end of the curve. It suggests market caution going into Friday’s payrolls. It wouldn’t be the first time the official labour market snaps a streak of underwhelming data (JOLTS and US consumer confidence disappointed at face value on Tuesday). Inflation numbers released in Germany (slower easing than hoped for) and Spain (reacceleration) provided counterweight as well. Bunds underperformed but finished off the intraday lows. Yields rose between 2.5-3.5 bps across the curve. The euro as a result had the upper hand. EUR/USD rose from as low as 1.0855 to 1.0923. DXY (trade-weighted dollar) slipped towards the recently recovered resistance of 103.16 (23.6% recovery of the September 2022 – July 2023 decline). The Japanese yen failed to capitalize on USD weakness. USD/JPY even ended the day slightly higher at 146.24. It isn’t leaving the recent highs just yet. The British pound was the star performer in the G10 landscape. EUR/GBP dipped back below 0.86 even as gilts outperformed their German counterparts. Stocks traded choppy in Europe while eking out gains ranging between 0.11-0.54% on the major Wall Street exchanges. Asian dealings aren’t very informative either. Equity performance is mixed with China lagging regional peers. PMI business confidence in the country highlight the ongoing struggle despite a glimmer of hope for a manufacturing sector bottoming out (see below). The Chinese yuan is among the weaker currencies this morning. The yen gains a few ticks, regardless of BoJ’s Nakamura arguing against his hawkish colleague Tamura’s case laid out on Wednesday. Tamura said negative rates could potentially end early next year. But according to Nakamura “the sustainable and stable achievement of the 2% inflation target accompanied by wage growth isn’t in sight yet.” Other currencies including the US dollar as well as core bonds show little direction.

Today’s economic calendar is all about inflation. The July PCE (core) deflator is due in the US with consensus expecting 0.2% m/m growth that brings the yearly figure up from 3% to 3.3% (4.1% to 4.2%). We have a neutral bias on the outcome. But being the Fed’s preferred inflation gauge and looking at the price action earlier this week, markets are probably more sensitive to a downward surprise. European HICP is due too. Following the Spanish and German readings yesterday and the minor upward Dutch surprise this morning, risks to the 5.1% headline and 5.3% core consensus are tilted to the upside. While that’s priced in to some extent already, we do think it at least offers a floor for European yields in particular. It may also further shape expectations for a September ECB hike, which markets currently give a less than 50% chance. In similar reasoning EUR/USD’s downside is limited from a daily perspective. Several ECB and Fed speeches are scheduled for today as are the ECB’s meeting minutes of the July meeting. They serve as a wildcard for trading.

News and views

The official Chinese August composite PMI ticked up from 51.1 to 51.3 in August, ending a 4-month decline. Details showed a small improvement in manufacturing (49.7 from 49.3) compensating for a setback in non-manufacturing (51 from 51.5). Manufacturing details showed new orders in positive territory (>50) for the first time since March. Companies keep shedding jobs (48) while price gauges hint at building price pressure (input costs 56.5 from 52.4 & output costs 52 from 48.6). Details in the services sector were weaker with the decline in new orders accelerating (47.5 from 48.1) and employment below the 50-mark for a 6-month running. China’s government recently announced a number of measures to revamp the economy/consumer spending. The Chinese currency remains stuck around the USD/CNY multiyear low of 7.30.

New Zealand’s main opposition party – National Party – who leads in opinion polls ahead of the national October 14 vote, said that it would quickly overturn the ruling Labour Party’s change to the central bank’s mandate (RBNZ). During their current tenure, they expanded it from solely focusing on returning inflation to the 1%-3% objective to also achieving maximum sustainable employment. The National Party accuses Labour of economic mismanagement and blamed it for fueling rampant inflation. “We want to build confidence that the Reserve Bank will be focused on that inflation mandate. We don’t see it as something novel. We see it just as a return to what was the position prior to the current government.”