Sample Category Title

Downside Risks on the Rise – Scenarios for Chinese Growth

- Financial stress is on the rise turning focus yet again on whether China is heading for a deeper financial and economic crisis.

- While we do see a rising risk of this happening (25% probability), our baseline scenario remains that China has the tools to avert such an outcome and will use them to the extend needed. Yet, due to the recent weak data and rise in financial stress we have revised down our forecast to 4.8% growth this year and 4.2% in 2024.

- We have lifted our forecast for both USD/CNH and EUR/CNH taking the new weaker growth outlook as well as rising risks into account. We now project USD/CNH to hit 7.60 in 12M up from 7.40 previously.

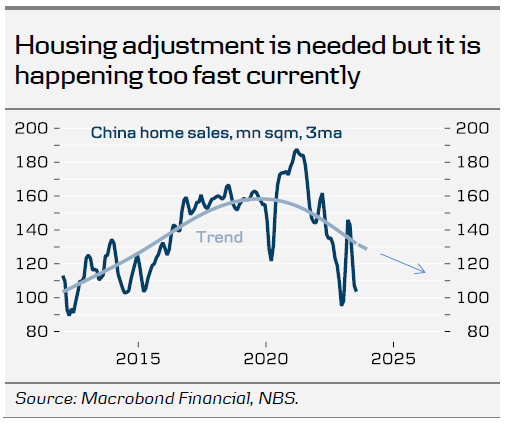

Headwinds on the rise again – lower GDP growth

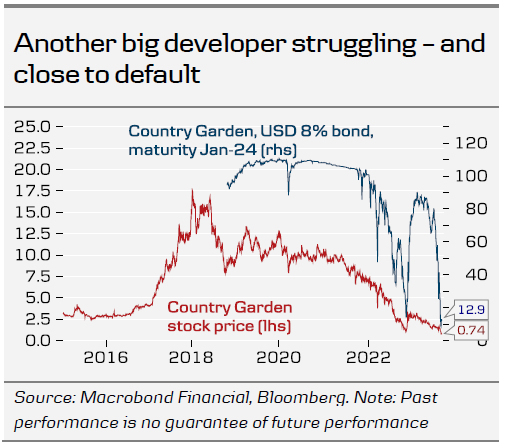

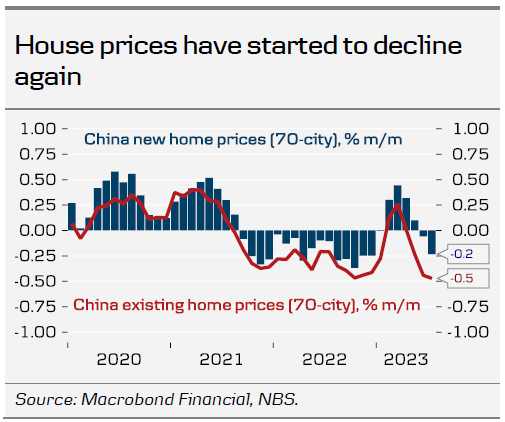

As we wrote about in China holiday wrap-up – part three: risks of a financial crisis resurface, 14 August, financial stress has increased lately with another major developer, Country Garden, at brink of default and contagion to the shadow banking system increasingly visible. On top of this economic data has disappointed across the board with both consumer spending, home sales and exports undershooting expectations. Taking these developments into account we revise down growth to 4.8% this and 4.2% next year.

In this baseline scenario we assume policy makers to step up stimulus as broadly signalled following the Politburo meeting in late July and to take more measures to improve financing channels for developers, lift home sales. We also expect them to provide the necessary lifelines to local governments and facilitate a restructuring of major shadow banking entities in distress, such as Zhongzi Enterprise Group. Our assumption is that they will still strive to reach the 5% target and do what is necessary to at least put a floor under growth so it does not fall below 4-4½%.

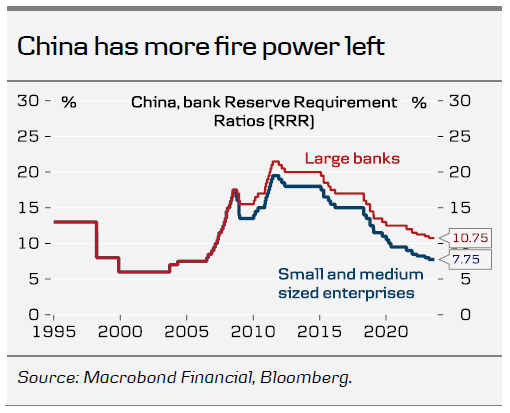

So which tools does the Chinese government have at its disposal to fight this crisis? First, it can follow through on the "forceful stimulus" it already vowed to do in late July in order to lift demand for private consumption, housing and infrastructure investments, see China holiday wrap-up – part 2: Stimulus and private sector plan lift Chinese markets, 28 July. Second, it can increase funding channels for developers. On Friday, PBOC and financial regulators met with bank executives telling them to direct more lending to support an economic recovery. It suggests policy makers are increasingly concerned about the recent financial stress and as the big lenders are state-owned they have some control over the amount of lending. Third, they can cut Reserve Requirement Ratios (RRR) for banks to free up more liquidity to buy credit bonds and increase lending. The RRR for small and medium sized banks is 7.75% while it is 10.75% for large banks. Fourth, like in developed economies China could opt for quantitative easing (QE) with PBOC buying bonds directly in the market. This would serve as a strong signal that they step in as lender of last resort. Why are they not doing it yet? Probably because the other tools have not been exhausted yet and they would rather cut RRR and let state banks do the buying.

Why are policy makers not already doing more?

That is a question often asked these days and it is also what causes concern to us. There are several options.

First, we do not know yet if they actually are preparing to do bigger stimulus but are just slow in implementation as the slowdown during spring came as a surprise. The policy signal from the Politburo in July did suggest a more forceful response. But the action has been underwhelming so far with only moderate rate cuts of 10-15bp. Still, it could be that they are brewing on other tools instead as they are concerned about cutting rates too much as it could add to the downward pressure on the yuan, which they are currently defending via stronger fixings and state banks selling dollars in the market. The jury is still out on how much stimulus is actually planned.

Second, it seems clear that Chinese policy makers have learned from the past mistakes of providing too much stimulus in a fairly uncontrolled manner as was the case in 2008-09. It led to a severe hangover with rising debt levels and wasteful investments. The risk is, though, that the pendulum has swung too much in the other direction and they don't do enough to get ahead of the curve and turn the economy around.

Third, Chinese leaders seem very keen on weaning the Chinese economy off the 'addiction' to a strong housing market, which has made many sectors over-reliant on continued growth in this sector. Households have 60% of their wealth in the sector. Developers have been riding the market with rising leverage for years and absorbed capital that would have been put to better use in the 'real economy'. Local governments depend on land sales for a large chunk of their revenues. And ordinary businesses have sometimes bought property just to use it as collateral for loans and for investment. This is not sustainable and policy makers may see the situation as a necessary pain to adjust to a new world where capital is allocated to more efficient sectors, not least high-tech manufacturing and tech. The risk is, though, that the whole economy crashes if Chinese leaders let the adjustment happen too fast. Also, it undermines their attempt to restore consumer confidence and make consumers a key driver of overall demand. So they will likely step in with more support but they will probably not do more than is absolutely necessary.

Risk scenarios – financial stress escalates triggering deeper crisis

With the fine balancing act of on the one hand finally getting rid of moral hazard and the economy's 'housing addiction' and on the other hand not triggering a deeper crisis, there is a risk that policy makers miscalculate and fall too far behind the curve so that the financial snowball that is rolling now gets too big to stop.

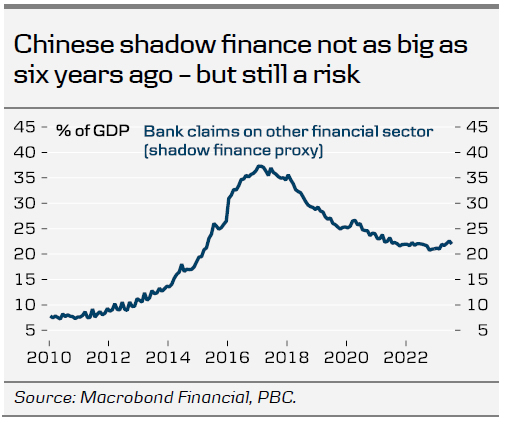

One way this could happen, would for example be if financial confidence in Wealth Management Products (WMP's) erodes sharply and causes a 'bank run' on these savings products. WMP's are basically a kind of deposits held in shadow banks that yield a higher rate than in ordinary banks, but also has much higher risk. Any losses are transferred directly to the depositor (buyer of the WMP) rather than the 'bank', but often times buyers of the products are not alert to this feature. If money is pulled out of the system rapidly, the financial stress could become so high that the government is unable to stop it – at least initially. The shadow banking system is already showing cracks and a few more bad stories could risk triggering a run on the system. One problem in these products is a classic maturity mismatch as they can be exited with short notice (3 months for example) but they finance loans with longer maturities – and with some of them being loans to developers. If the money is pulled out, it would not only hurt developers but also other companies that get funding through these products. It could thus trigger defaults more broadly as it cascades through the economy. On a positive side, shadow banking does not play as big a role as 6-7 years ago as the government realized the risks and started a crackdown. But it is still close to 25% of GDP. And in combination with other risks, such as those from local government debt (around 50% of GDP), and a possible deeper housing slump, the situation warrants close monitoring.

In a financial crisis scenario, growth could drop much further in the short term, but policy makers would likely step in as 'lender of last resort' via PBOC and state banks to avoid a continued significant credit crunch. Stimulus would also be scaled up markedly. Nevertheless short term pain would likely be felt across the economy before the government's rescue action would have its' impact. A bit like the European debt crisis where the ECB refused to step in as lender of last resort until it threatened the whole euro system, and they stated they 'would do whatever it takes'. From there on the crises was more or less over. Why did the ECB wait so long? Same reason as in China. Moral hazard issues suggesting that you should only come to the rescue when there is no other option. Investors need to bear pain along the way to avoid too much risk taking again in the future.

It is hard to put numbers on these things as it could unravel in many ways but to give a sense of what we think of, we see both a 'mild crisis scenario' being possible where growth drops down to 3% for 6-9 months before the rescue action turns things around and a 'hard crisis scenario' that leads to outright negative growth for around 6-9 months. Currently we put the probability of a 'mild crisis scenario' at 15% and a 'hard crisis scenario' at 10% with a total risk of some crisis scenario summing up to 25%.

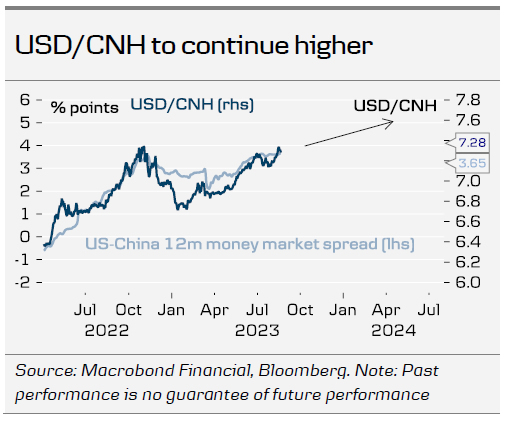

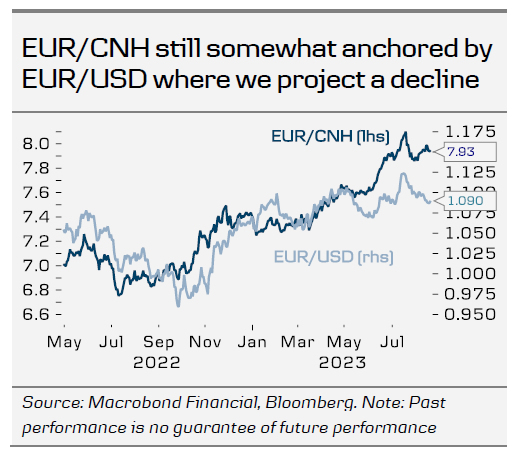

USD/CNH to continue higher

Based on the downward revision to our baseline growth scenario, we now also see USD/CNH moving even higher than in our current forecast as monetary policy divergence continues and downside risks weigh on the CNH. We now look for the cross to reach 7.70 in 12M (previously 7.40). For EUR/CNH, it implies a broadly flat level around 7.95 for the next 6-12 months based on our projection of a further decline in EUR/USD. The risk is skewed to the upside, though, as we see a higher probability of Chinese activity surprising to the downside still adding more downside on the CNH.

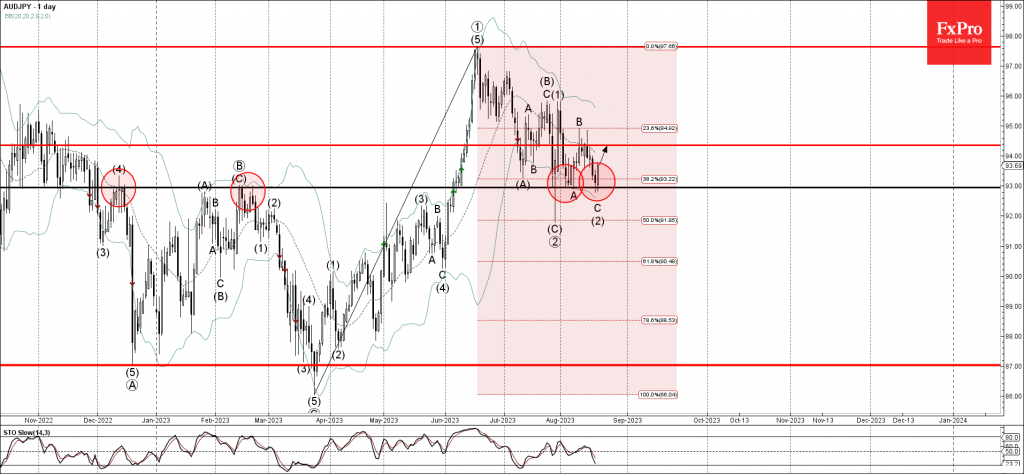

AUDJPY Wave Analysis

- AUDJPY reversed from support level 93.00

- Likely to rise to resistance level 94.35

AUDJPY currency pair recently reversed up from the support level 93.00 (which has been reversing the price from the end of July), coinciding with the lower daily Bollinger Band and the 38.2% Fibonacci correction of the sharp upward impulse from March.

The upward reversal from the support level 93.00 is likely to form the daily Japanese candlesticks reversal pattern Morning Star.

Given the strong yen sales, AUDJPY currency pair can be expected to rise further toward the next resistance level 94.35.

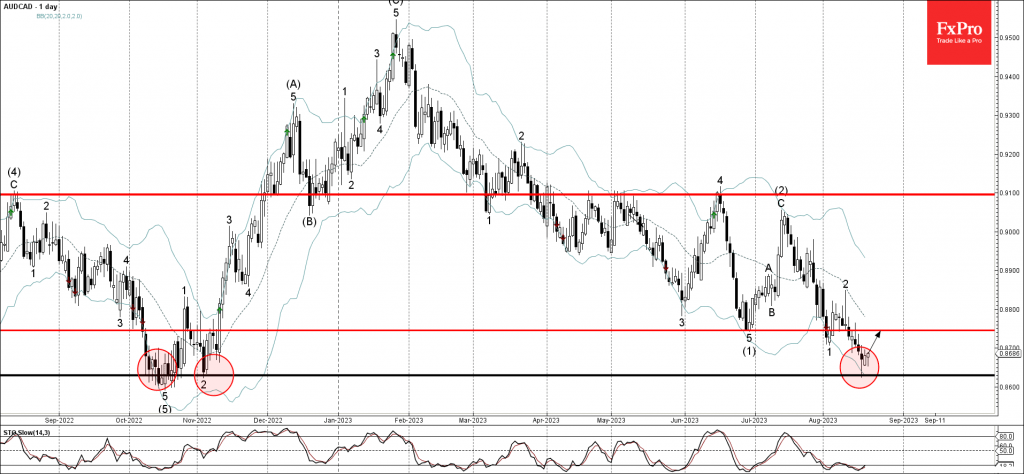

AUDCAD Wave Analysis

- AUDCAD reversed from support level 0.8630

- Likely to rise to resistance level 0.8745

AUDCAD currency pair recently reversed up from the major long-term support level 0.8630 (former strong support from October and November), coinciding with the lower daily Bollinger Band.

The upward reversal from the support level 0.8630 created the daily Japanese candlesticks reversal pattern Hammer.

Given the strength of the support level 0.8630 and the oversold daily Stochastic, AUDCAD currency pair can be expected to rise further toward the next resistance level 0.8745.

EUR/USD: The Jackson Hole Dollar Playbook

- 2-year Treasury yield rises 3.7bps to 4.979% (supports Fed’s higher for longer push)

- Dollar softens as risk appetite tentatively returns following last week’s stock market rout

- Fed Chair Powell to speak at Jackson Hole Symposium on Friday

The fate of the dollar will not solely depend on what Fed Chair Powell says at Jackson, but on several other factors. Will Nvidia’s earnings reignite the AI trade and provide much needed relief to tech stocks? How much additional support will we see from China? Is ECB President Lagarde ready to show which way she is leaning towards for the September meeting? Finally, will the global flash PMIs show that rate hiking cycles are starting to bring down the service sector?

Fed Chair Powell will be trying to avoid a policy mistake here. The annual Jackson Hole gathering will undoubtedly emphasize the need for policymakers to keep rates higher for longer. Powell might stick to his hopes of a soft landing, while hinting that eventually rates will be able to come down. It seems the majority of Wall Street is expecting Powell to deliver a hawkish hold, but any signs that the Fed is concerned about disorderly markets could end up supporting the case that the Fed will cut rates early next year.

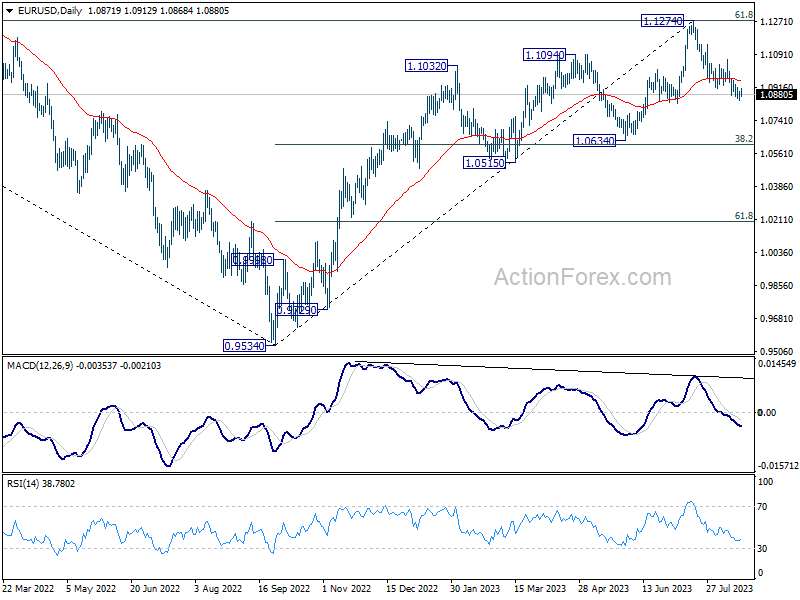

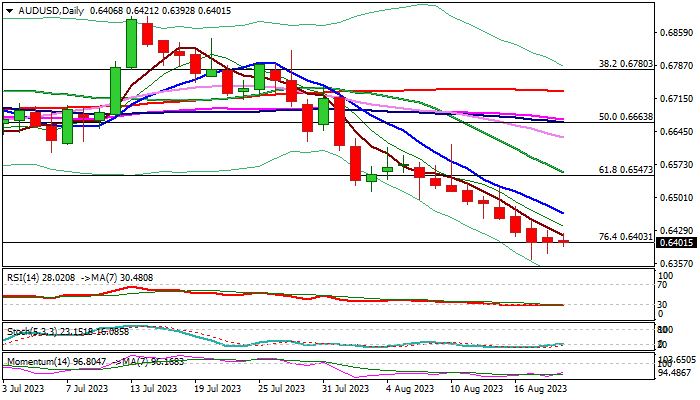

EUR/USD Daily Chart

The EUR/USD (a daily chart of which is shown) as of Monday (8/21/2023) is seeing its bearish trend cool ahead of the Jackson Hole Symposium. The euro’s slide had its eyes on the July low (1.0834), but that seems to be providing key support for now. If the bond market selloff remains intact, we might not have to wait for any fireworks from Jackson Hole speeches by both ECB’s Lagarde and Fed Chair Powell.

If euro-dollar sees a sharp plunge, key support will come from the 1.0740 to 1.07400 region. It is around that area that price could see the formation of a potential bullish ABCD pattern, which might target a key harmonic level of 350 pips.

The key story on Wall Street remains the movement with real yields. The yield on 10-year inflation-protected Treasuries rose above the 2% level, this is the first time it did that since 2009. Soft landing or not, some investors won’t be able to pass up getting paid over 5% on short-term debt they can hold for a few months.

If at the end of the week, the dollar’s rally is exhausted, upside could target the 1.0925 region. Only a daily close above the 1.1050 level would open the door for an extended euro rally.

AUD/USD: Initial Signals of Correction After Five-Week Bear-Run

Australian dollar edged higher on Monday and is on track for possible first bullish daily close in ten days, which may generate initial reversal signal.

Long tails of candles of past two days point to growing bids, with daily stochastic and RSI emerging from overbought territory and contributing to positive signals.

Larger downtrend of five weeks is looking for a breather, as Aussie dollar received fresh support from rising yuan and copper.

Triple failure to register daily close below cracked Fibo support at 0.6403 (76.4% of 0.6170/0.7157) signals formation of bear-trap pattern on daily chart which would also support recovery.

Today’s close above Friday’s high (0.6428) is seen as minimum requirement to keep alive hopes of recovery, with lift above daily Tenkan-sen / Fibo 23.6% of 0.6894/0.6364 (0.6489) to strengthen near-term structure for stronger recovery.

Caution on failure to clear Friday’s high which would signal extended narrow consolidation but will keep the downside vulnerable.

Res: 0.6428; 0.6453; 0.6489; 0.6521.

Sup: 0.6378; 0.6364; 0.6272; 0.6170.

Sunset Market Commentary

Markets:

After a risk-off trend almost uninterruptedly set the tone for global trading since end July, little/no news this time proved good enough to trigger a cautious countermove in equities and in FX. US and European markets even ignored a fragile sentiment in Asia after Chinese banks reduced lending rates less than expected, proving less support to the economy than hoped for. The EuroStoxx 50 rebounds about 0.7% (was 1%+ earlier intraday), avoiding a new attack on the key 4200 support area. Similar story in the US with the S&P 500 staying away from the 4328 June correction low. Except for technical considerations, we saw few obvious drivers for the rebound. The (European) rebound - in part driven by energy stocks mirroring higher oil (Brent $85.7/b) and natural gas prices - calls for caution on the sustainability of the move. The bid for equities at least wasn’t driven by a congruent rebound in core bonds. They remained under modest pressure from the start of trading. US yields are rising between 3.5 bps (2-y) and 7 bps (30-y). The US 30-y yield is touching the highest levels since mid-2011. The US 10-y yield is only a whisker away from the 4.335% cycle top. The 10-y real yield (1.99%) nears the 2% psychological barrier. The real yield last surpassed this level in March 2009! At least another good reason to stay cautious on a sustained risk rebound. German/EMU yields lagged the rise in US yields earlier this month but today joined the US move with Bund yields adding between 4 bps (2-y) and 6.5 bps (10-y). Market focus this week evidently is on Fed Chair Powell’s speech at the Jackson Hole symposium on Friday. For European markets we also keep a close eye at Wednesday’s preliminary August PMI’s. The June and July EMU indices for sure were highly disappointing. Still, question remains whether the current slowdown in European growth is enough to bring (services/core) inflation back under control. A positive surprise for the August PMI’s (or the IFO) could in this context wrongfoot investors, reinforce the higher for longer narrative and might even revive more outspoken market anticipation of a September ECB rate hike.

The dollar rally slows on FX markets. DXY trades marginally lower at 103.3. The euro today outperforms after a long-drawn EUR/USD decline earlier this month. The pair tries to regain the 1.09 big figure, creating some breathing space to prevent an immediate attack on the 1.0834 key support. However, the battle isn’t over yet. The combination of a risk-on sentiment an higher US/EMU yields reveals ongoing yen vulnerability. Trading north of 159, EUR/JPY is again nearing last week’s top of 159.36, the weakest level of the yen against the single currency since 2008! USD/JPY (145.9) also keeps last week’s top (146.46) within reach with the psychological 150/the 2022 top at 151.95 seen as a likely level for more decisive BOJ action. No clear directional trend for sterling today even as Gilts both outperform Treasuries and Bunds (yields rising less than 2 bps). Cable (GBP/USD 1.275) gains marginally. EUR/GBP reversed early gains to trade in the 0.855 area.

News & Views:

The German Bundesbank expects Europe’s largest economy to probably stagnate again in Q3 as high interest rates and weak global demand weigh. The German economy continues to be in a weak phase as the country has it hard to overcome the manufacturing-induced slump with momentum in construction also sluggish. At the same time, stable employment, robust wage gains and retreating inflation will help private consumption recover. Increased inflation expectations and a possible recurrence of energy price shocks harbor upside risks for the price outlook together with strong wage growth which is set to remain beyond the turn of the year.

The Belgian debt agency raised a combined €2.8bn by tapping OLO 89 (€1.225bn 0.1% Jun2030) and OLO 97 (€1.575bn 3% Jun2033). The amount sold was the maximum on offer with an auction bid cover of 1.73. Thanks to today’s auction, the Belgian debt agency already raised €37.1bn of this year’s planned €45bn (82.5%). The bulk of this amount was raised via three syndicated deals earlier this year (totaling €16bn).

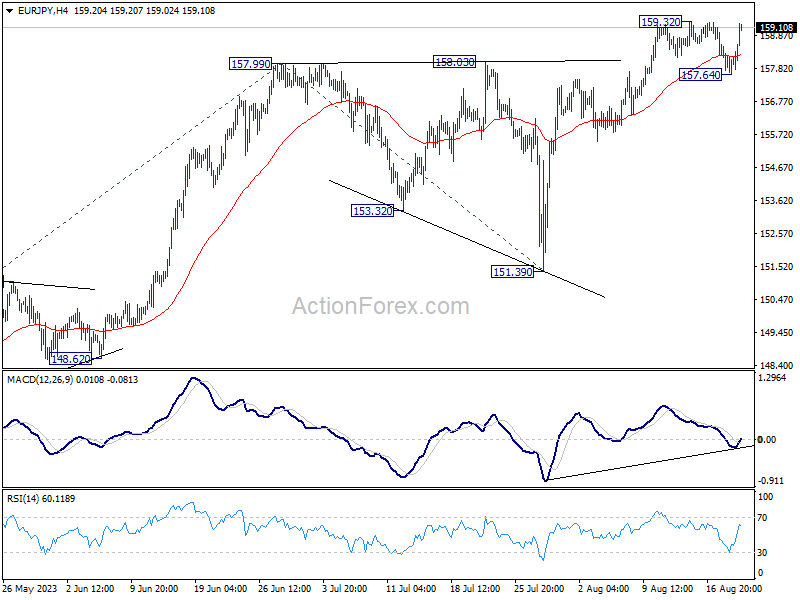

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 157.66; (P) 158.12 (R1) 158.59; More....

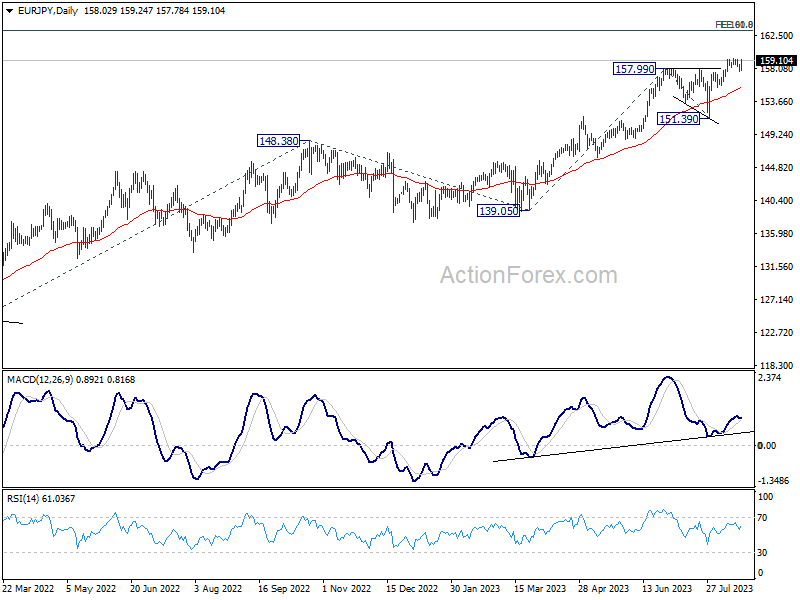

Intraday bias in EUR/JPY is turned neutral first with today's recovery. On the upside, decisive break of 159.32 will resume larger up trend, and target 61.8% projection of 139.05 to 157.99 from 151.39 at 163.09 next. On the downside, however, break of 157.64 will turn bias back to the downside for deeper correction.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 100% projection of 124.37 to 148.38 from 139.05 at 163.06. Sustained break there will pave the way to retest long term resistance at 169.96. This will now remain the favored case as long as 151.39 support holds, even in case of deep pull back.

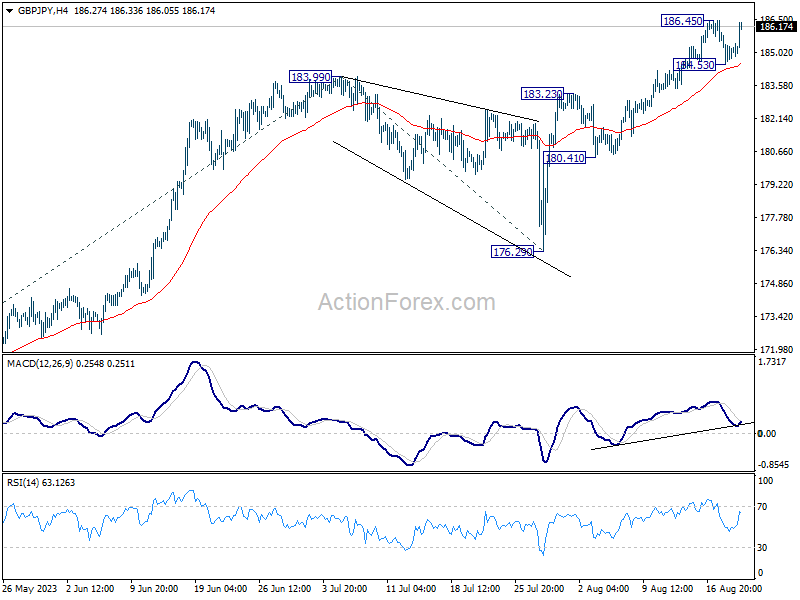

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 184.50; (P) 185.22; (R1) 185.89; More...

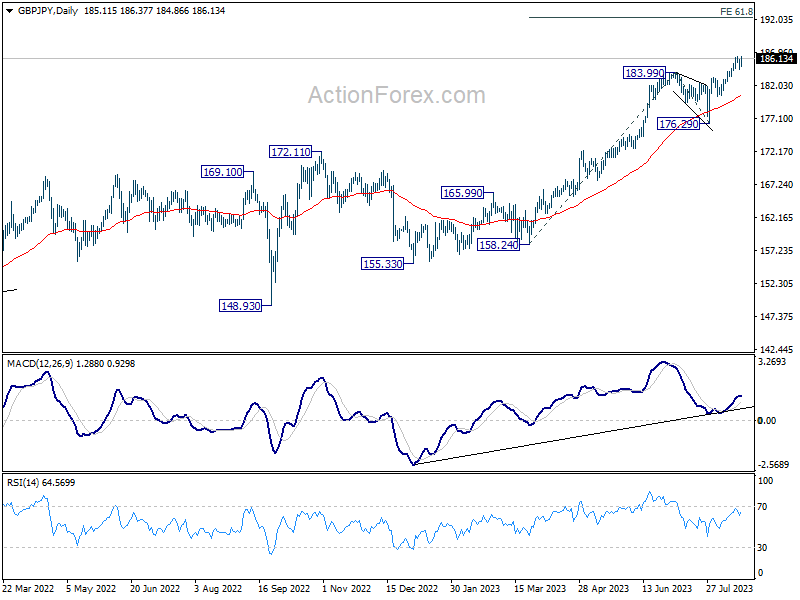

Intraday bias in GBP/JPY is turned neutral first with today's recovery. On the upside, decisive break of 186.45 will resume larger up trend to 61.8% projection of 158.24 to 183.99 from 176.29 at 192.20. On the downside, below 184.53 will bring another corrective fall to 183.23 resistance turned support, and possibly below.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Next target is 195.86 (2015 high). This will now remain the favored case as long as 176.29 support holds, even in case of deeper pull back.

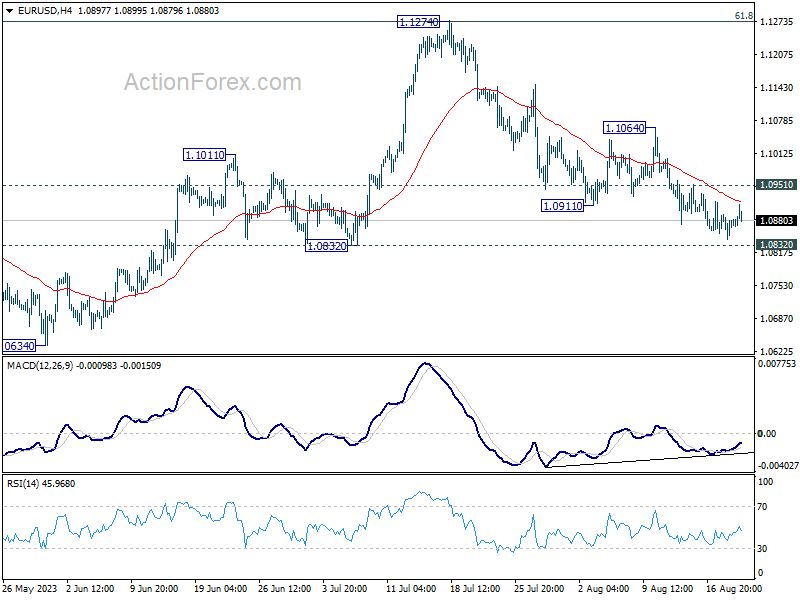

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0847; (P) 1.0871; (R1) 1.0896; More...

Intraday bias in EUR/USD stays neutral at this point. On the downside, decisive break of 1.0832 support will resume the fall from 1.1274 and target 1.0609/34 cluster support next. On the upside, above 1.0951 minor resistance will turn intraday bias to the upside for stronger recovery.

In the bigger picture, a medium term top should be formed at 1.1274, after failing to break through 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 decisively, on bearish divergence condition in D MACD. Fall from there is seen as a correction to the uptrend from 0.9534 (2022 low). Deeper decline would be seen to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to set the range for consolidation. Yet, medium term outlook will be neutral for now, as long as 1.1274 resistance holds.