Sample Category Title

AUD/JPY Technical: Watch 92.80 Key Downside Trigger Level

- Weak medium-term momentum may kickstart a medium-term downtrend phase for AUD/JPY.

- Key short-term resistance stands at 93.70 with a potential downside trigger at 92.80.

Since its 19 June 2023 high of 97.67, the price actions of the AUD/JPY have continued to shape lower highs despite a retest and rebound on its key 200-day moving average after it printed an intraday low of 91.79 on 28 July 2023 ex-post Bank of Japan (BoJ)’s flexible yield curve control announcement on the 10-year Japanese Government Bond.

Technical analysis suggests that the AUD/JPY is now at heightened risk to evolve into a medium-term downtrend phase.

Challenging the 92.80 key downside trigger level

Fig 1: AUD/JPY medium-term trend as of 21 Aug 2023 (Source: TradingView, click to enlarge chart)

Last Friday, 18 August, AUD/JPY managed to stall its prior three days of decline at a key support/inflection level of 92.80 which is being defined by a confluence of elements; the former swing high areas of 26 January/14 February/21 February 2023, and medium-term ascending trendline from 24 March 2023 low of 86.06.

However, elements are not showing signs of any bullish reversal at this juncture with bearish momentum reading seen in the daily RSI oscillator as it inched lower from the 50 level and has not reached oversold condition.

Price actions oscillate within a minor descending channel

Fig 2: AUD/JPY minor short-term trend as of 21 Aug 2023 (Source: TradingView, click to enlarge chart)

The price actions of AUD/JPY have oscillated within a minor descending channel in place since 15 August 2023 minor swing high of 94.87 which suggested that further potential downside may materialize at least in the short-term horizon.

Watch the 93.70 key short-term pivotal resistance and a break below 92.80 near-term support exposes the next support at 92.00 (also the 200-day moving average) in the first step.

On the other hand, a clearance above 93.70 invalidates the bearish bias to see the next intermediate resistance at 94.90 (also the 50-day moving average).

Uncertainty on Policy Mix Keeps Yuan in Defensive

Markets

High profile technical levels eventually prevailed last Friday in a session absent of eco data, central bank speak or any other high-profile event. Core bonds ended off worst levels YTD after a surge higher in (US) real yields dominated most of August trading. It resulted in tests of cycle tops at the very long end (10y-30y) of US, but also German and UK yields. At 1.94%, the US 10-yr real yield had its highest weekly close since March 2009. A return of term premia (higher for even longer), credit risk (Fitch downgrade & public finances) and improved growth prospects (soft landing vs recession) all contributed. The lack of conviction of Friday’s core bond rebound suggests that the test of (yield) resistance levels remains ongoing. Higher real rates hurt risk sentiment. European stock markets lost around 0.5% again on Friday, but important support survived just for now. The picture remains fragile though, with EuroStoxx50 ending only just above 4200 and Asian risk sentiment this morning sluggish after Chinese data (see below). Main US stock indices ended around flat Friday, but the likes of the S&P 500 are clearly showing a topping out pattern, admittedly still withing the long term rising trend channel. First support kicks in at 4329. The dollar failed to really bank on the rater support with the trade weighted greenback testing, but for now not breaking, first resistance at 103.57. A real test of EUR/USD 1.0834 support didn’t occur yet. USD/JPY rallied from 138 mid-July to 146 currently. The Japanese ministry of Finance started its first FX interventions in almost 15 years around those levels last September. They later stepped it up around 150. The global context and unwillingness by the BoJ to really start normalizing monetary policy mean that JPY remains vulnerable.

Today’s eco calendar is empty apart from a Belgian OLO auction. The debt agency offers OLO 89 (0.1% Jun2030) and OLO 97 (3% Jun2033) for a combined €2.4-2.8bn. YTD, the debt agency already realized over 76% (€34.3bn) of its total OLO financing plan (€45bn). The bulk of this amount (€16bn) came from three syndicated deals. August global PMI’s (Wednesday) serve as distraction later this week going into Friday’s big event when Fed Chair Powell’s discusses the economic outlook at the US central bank’s high profile Jackson Hole symposium organized by the Kansas City Fed. Apart from guidance for the September meeting (no rate hike discounted), we look for clues on the neutral rate, the economic resilience and the disinflationary process. FOMC Minutes showed that for the majority of Fed members, the bar to hike rates another time is low given upside inflation risks.

News and Views

Chinese Banks announced to reduce the 1-year Loan Prime rate to 3.45% from 3.55%. The 5-year Loan Prime rate was kept unchanged at 4.20%. In both cases, the market expected a 15 bps reduction after the PBOC last week reduced the 1-year Medium-Term Lending Facility rate by a similar amount from 2.65% to 2.50%. The smaller than expected reduction in the bank rates leave markets in doubt on the degree of monetary support that Chinese authorities are prepared/able to put in place to revive economic activity in general and the ailing property sector in particular with deflationary tendencies also dampening activity. Uncertainty on the policy mix keeps the yuan in the defensive this morning with USD/CNY again jumping north 7.30 (7.3065) even as the PBOC set its daily fixing stronger than expected by market participants.

In a forecast published on Friday, the Czech Ministry of Finance downwardly revised growth for this and next year respectively to -0.2% (from 0.1%) and 2.3% (from 3.0%). Average inflation for this year was seen unchanged at 10.9%. The average predicted price rise for 2024 was slightly upwardly revised from 2.4% to 2.8%. At the same time, the Finance ministry forecasts a substantial improvement in the current account deficit. For this year, the Ministry sees a deficit of 1.7% and for next year of 0.6%. This compares to deficit forecasts of 3.5% and 1.9% respectively released in its April projections.

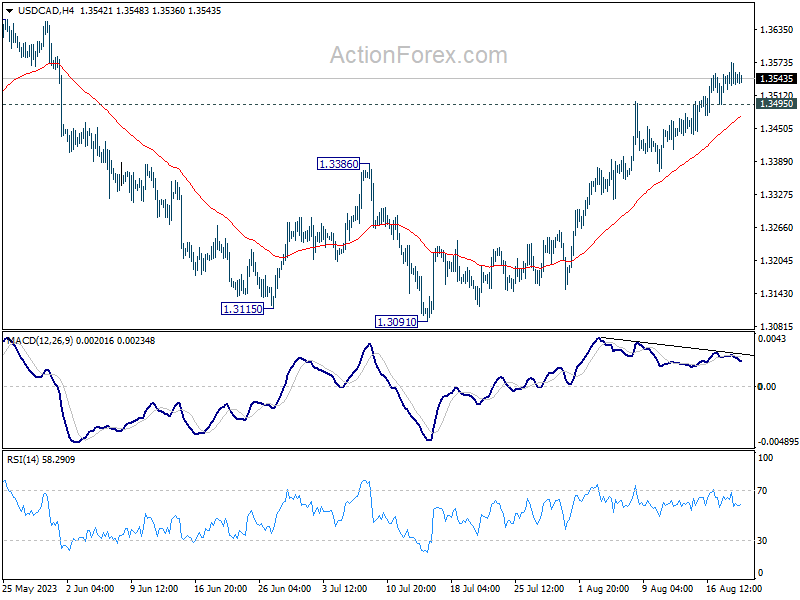

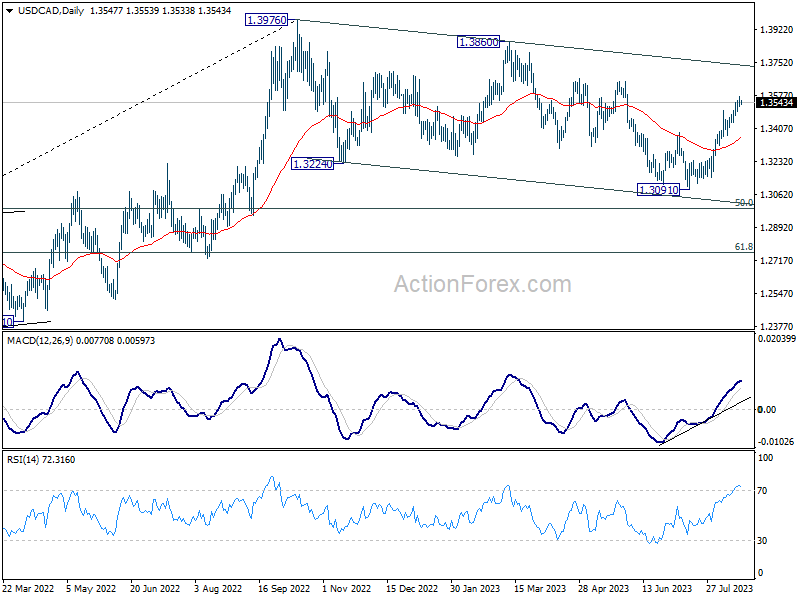

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3527; (P) 1.3551; (R1) 1.3577; More....

Intraday bias in USD/CAD stays on the upside despite loss of upside momentum. Current rally would target 1.3653 resistance first. Decisive break there will confirm that correction from 1.3976 has completed, a target a test on this high. On the downside, below 1.3495 minor support will turn intraday bias neutral and bring consolidations first, before staging another rise.

In the bigger picture, price actions from 1.3976 are viewed as a corrective fall only. Upon completion, rise from 1.2005 (2021 low) would resume through 1.3976. Next target is 61.8% projection of 1.2005 to 1.3976 from 1.3091 at 1.4309. In case of another fall, downside should be contained by 61.8% retracement of 1.2005 to 1.3976 at 1.2758.

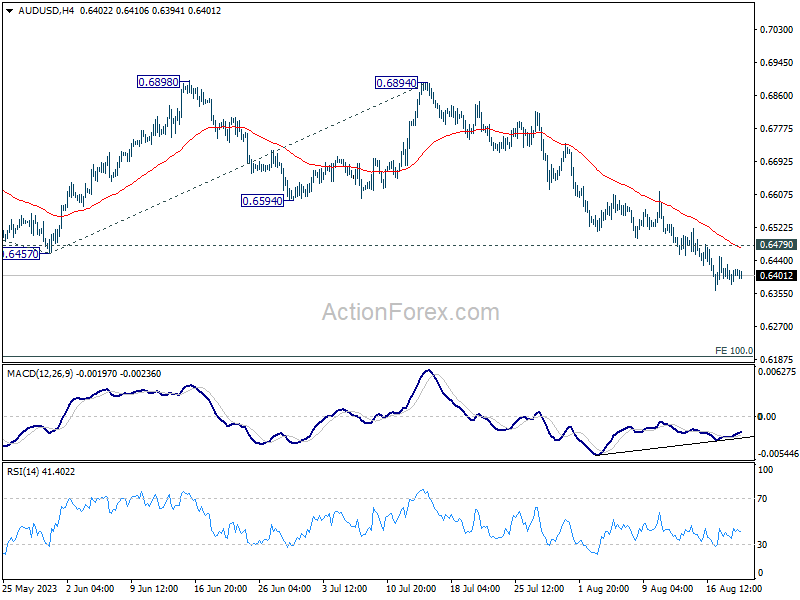

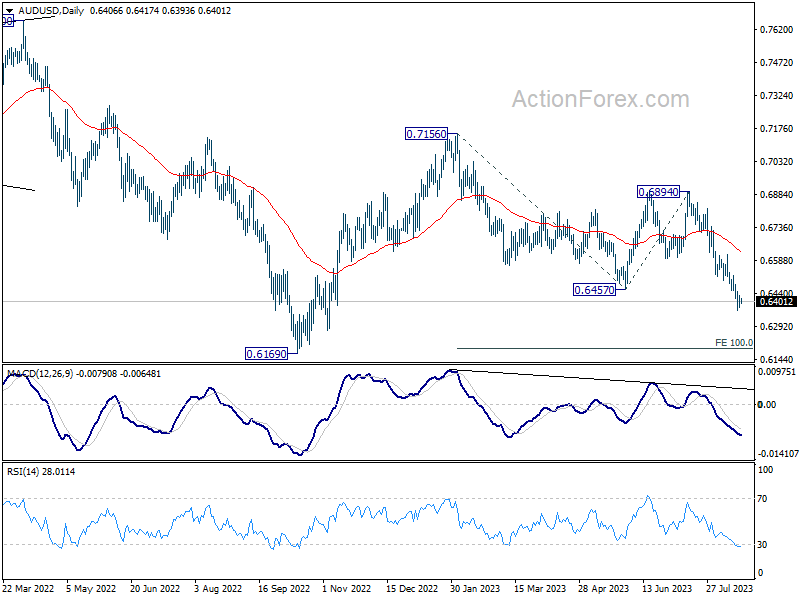

AUD/USD Daily Report

Daily Pivots: (S1) 0.6380; (P) 0.6404; (R1) 0.6430; More...

Intraday bias in AUD/USD remains on the downside despite loss of downside momentum. Current fall should target 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195. On the upside, above 0.6479 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, current development argues that the down trend from 0.8006 (2021 high) is still in progress. Decisive break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.

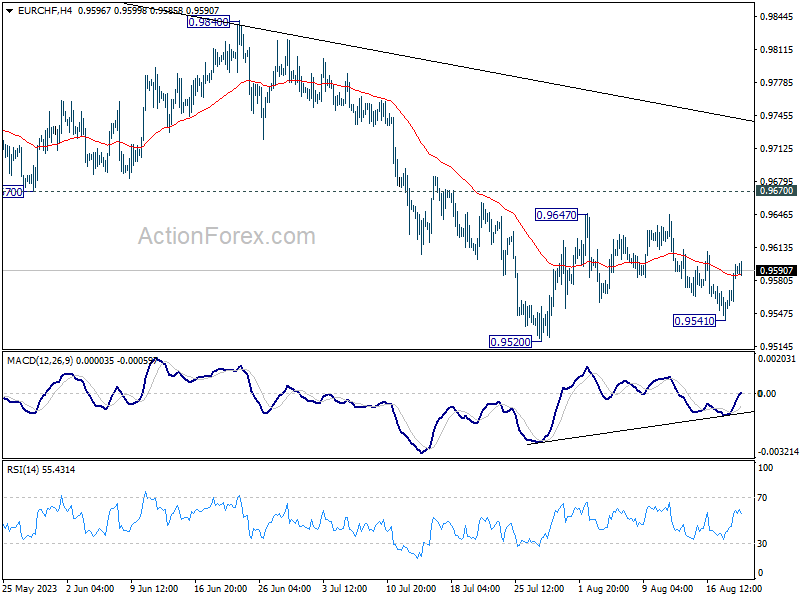

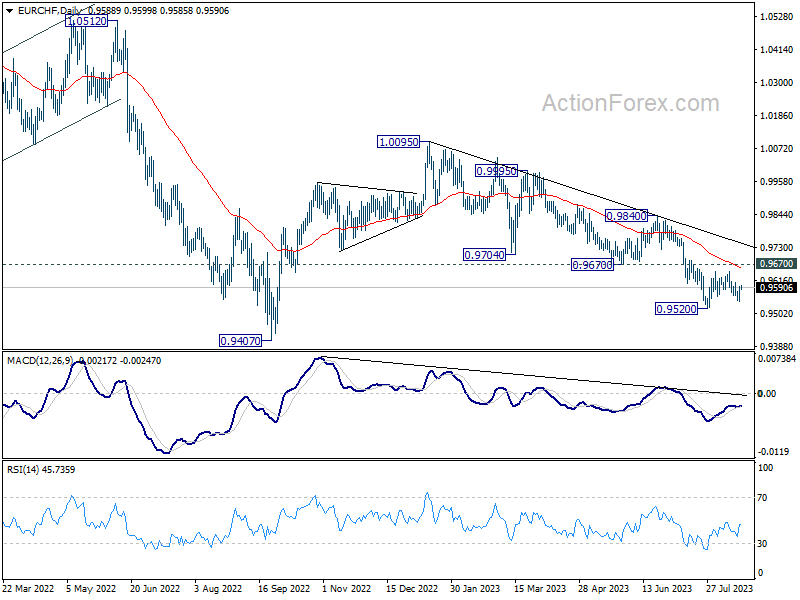

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9554; (P) 0.9576; (R1) 0.9616; More...

Intraday bias in EUR/CHF remains neutral as sideway trading continues. On the upside, break of 0.9647 will resume the rebound from 0.9520. Further sustained break of 0.9670 will be the first sign of bullish reversal and target 0.9840 resistance for confirmation. On the downside, break of 0.9520 will resume the whole fall from 1.0095 towards 0.9407 low.

In the bigger picture, medium term outlook is staying bearish as the pair is capped well below falling 55 W EMA (now at 0.9849). Down trend from 1.2004 (2018 high) is in favor to continue. Sustained break of 0.9407 will target 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. For now, this will remain the favored case as long as 0.9840 resistance holds, in case of strong rebound.

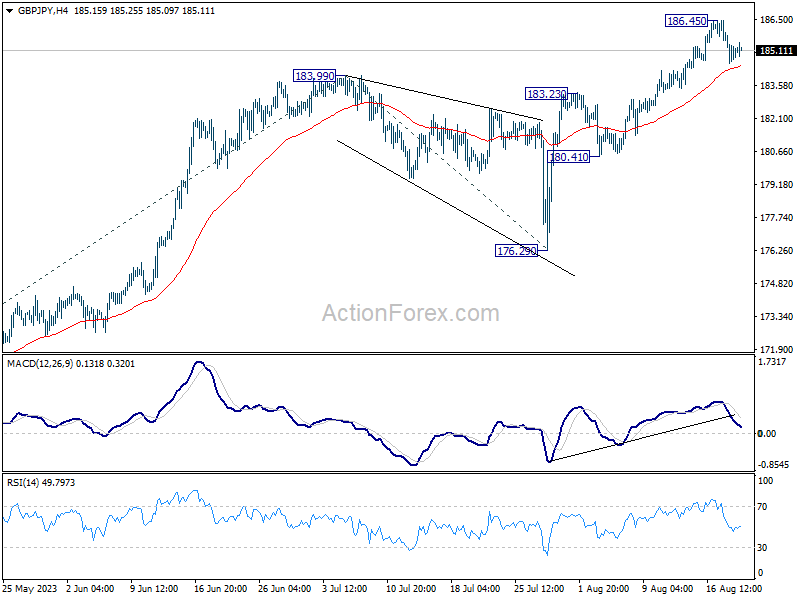

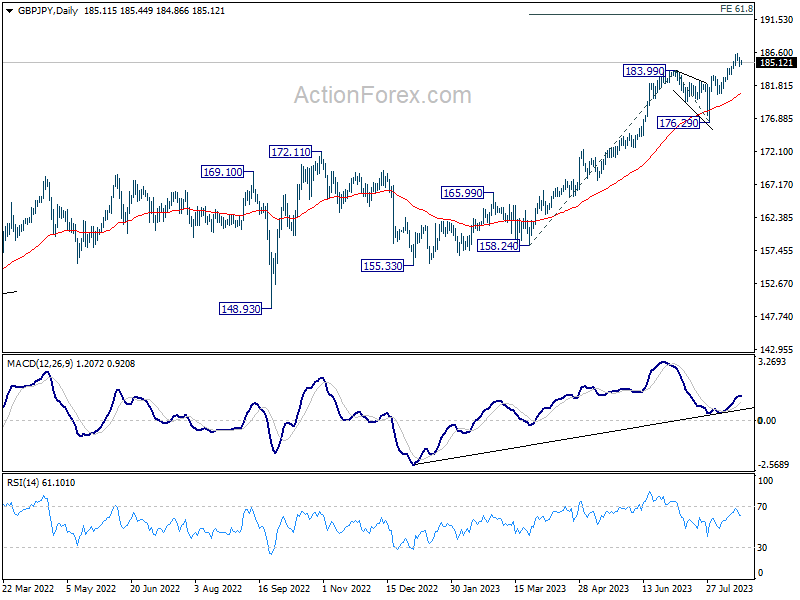

GBP/JPY Daily Outlook

Daily Pivots: (S1) 184.50; (P) 185.22; (R1) 185.89; More...

Intraday bias in GBP/JPY stays mildly on the downside at this point. Pull back from 186.45 would target 183.23 resistance turned support. Nevertheless, on the upside, break 186.45 will resume larger up trend to 61.8% projection of 158.24 to 183.99 from 176.29 at 192.20.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Next target is 195.86 (2015 high). This will now remain the favored case as long as 176.29 support holds, even in case of deeper pull back.

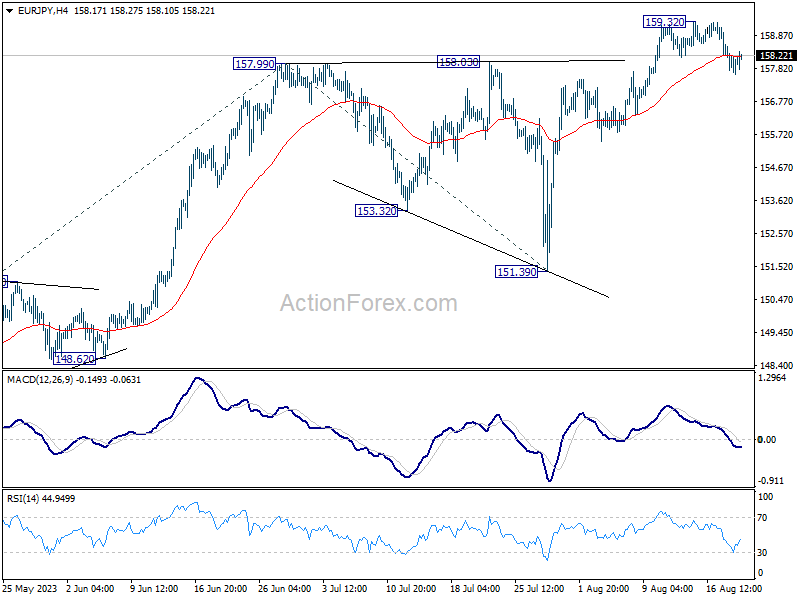

EUR/JPY Daily Outlook

Daily Pivots: (S1) 157.66; (P) 158.12 (R1) 158.59; More....

Intraday bias in EUR/JPY stays mildly on the upside at this point. Pull back from 159.32 could extend to 55 D EMA (now at 155.42). On the upside, though, break of 159.32 will resume larger up trend to 61.8% projection of 139.05 to 157.99 from 151.39 at 163.09 next.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 100% projection of 124.37 to 148.38 from 139.05 at 163.06. Sustained break there will pave the way to retest long term resistance at 169.96. This will now remain the favored case as long as 151.39 support holds, even in case of deep pull back.

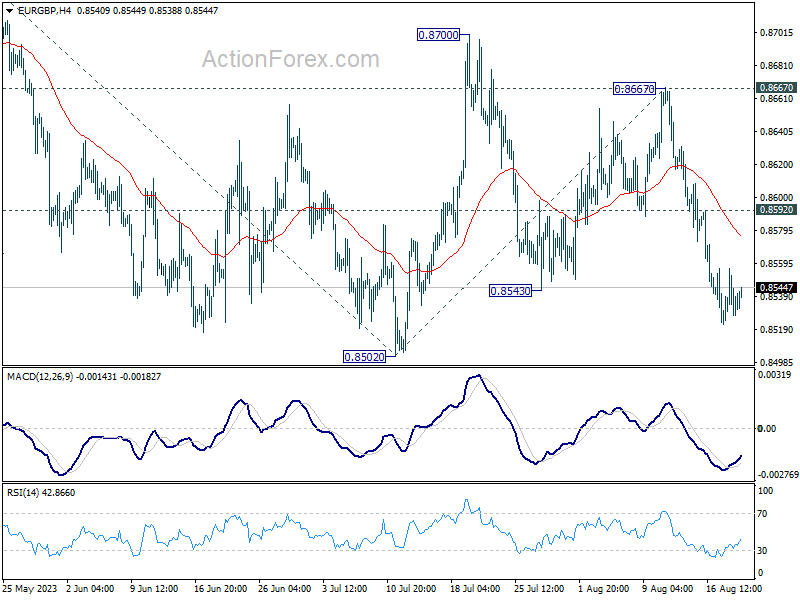

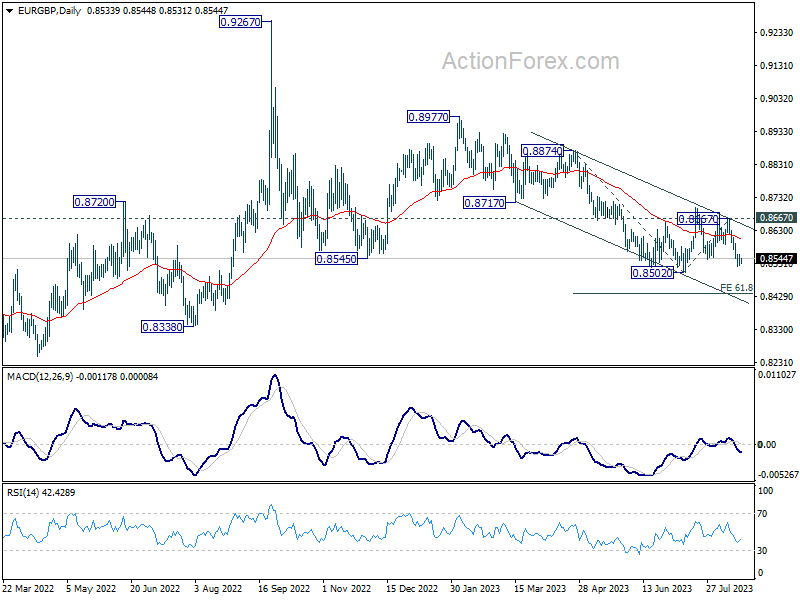

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8523; (P) 0.8540; (R1) 0.8555; More...

Intraday in EUR/GBP is turned neutral with current recovery, but further decline is expected with 0.8592 resistance holds. Decisive break of 0.8502 will resume larger down trend. Next target is 61.8% projection of 0.8874 to 0.8502 from 0.8667 at 0.8437. On the upside, above 0.8592 minor resistance will mix up the outlook and extend sideway trading from 0.8502.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Further decline is in favor as long as 0.8667 resistance holds. Break of 0.8502 will resume the fall towards 0.8201 (2022 low).

China Rate Cuts Remain Short of Expectations, Focus on Jackson Hole, BRICS

The week starts with weak appetite as Chinese banks cut loan rates less than expected; the 1-year LPR was cut by 10bp to a record low versus 15bp cut expected by analysts, while the 5-year LPR was left unchanged despite pressure from Beijing. Chinese banks’ decision to keep the 5-year rate steady is confusing for investors, in the middle of a property crisis. The Hang Seng index sank further into bear market, and the global risk sentiment is less than ideal as healthy economic data from the US, and darker clouds over China cast shadow on both stock and bond markets.

The US 10-year yield approached the highest levels since 2007, as the US 30-year yield hit the highest levels advanced towards levels last seen in 2011. The rising yields weigh on major stock indices. The S&P500 closed last week around 2% lower, and Nasdaq 100 lost 2.6% last week. Interestingly, the S&P500 has been down by around 3% since the beginning of this earnings season – while the earnings season was not that bad. Nearly 80% of the companies announced better-than-expected results and Refinitiv highlighted that the Q2 of 2023 had the highest rate of companies beating expectations since Q3 2021, and the earnings expectations rebounded to the highest levels since last October, when the major US indices bottomed out. This picture simply means that the fear of a further Fed tightening, prospects of higher interest rates, combined to the set of bad news from China simply didn’t let investors enjoy the better-than-expected earnings.

Jackson Hole and BRICS

This week, investors will have their eyes and ears on Federal Reserve (Fed) Chair Jerome Powell’s Jackson Hole speech due Friday. The chances are that he will keep his hawkish stance despite falling inflation. The minutes from the latest FOMC meeting highlighted ‘significant upside risks’ on inflation. This being said, the fear of decidedly hawkish Fed is already priced in, and if there is no more hawkish surprise from this week’s Jackson Hole meeting, tensions among investors could ease by next week, and give markets some breathing room.

Elsewhere, BRICS summit will take place this week between 22nd and 24rd of August. What’s interesting with this summit is 1. A month ago, South Africa said that 40 more nations wanted to join BRICS, and 23 of them formally applied to become members including Saudi Arabia, Iran, and UAE. 2. They would like to drop US dollar and eventually start using member-state currencies to settle their trade terms between them, and 3. There are rumours that the BRICS countries could even issue a gold-based currency to replace the US dollar, as many nations are willing to free themselves from the risks of holding and using US dollars. Note that the rumours of a gold-based BRICS currency didn’t necessarily boost appetite in gold lately. The price of an ounce is, on the contrary, mainly driven by US yields. The rising US yields weigh on gold appetite by increasing the opportunity cost of holding the non-interest-bearing gold. The yellow metal slipped below its 200-DMA last week for the first time since December. A downside correction in the US yields could slow the selloff and encourage a minor positive correction but given the Fed’s undoubtful hawkish stance on its rate policy, gold bulls may need BRICS to say something about their currency plans. But I am afraid the latter might not be on the agenda of this week’s summit.

Modest Chinese Rate Cut

Market movers today

The week is off to a quiet start in terms of data releases with nothing significant in the calendar.

The big data event this week will be on Wednesday when flash PMIs are released for the Euro Area and the US (among others). This release may well set the tone ahead of the September rate meetings in the ECB and the Fed. Risks to growth are a large part of the case for those arguing against an ECB hike even though inflation remains high, following disappointing PMIs in July. For the US, hard data for July has been strong but soft indicators for August have been very mixed, with strong Philly Fed and weak Empire Manufacturing Index. Also a highlight for this week is the Fed's Jackson Hole Symposium Thursday to Saturday with Powell speaking on the economic outlook Friday.

The 60 second overview

Modest Chinese stimulus: The Peoples Bank of China (PBoC) cut the one-year loan prime rate (LPR) by 10 basis points to 3.45% this morning. Most new and outstanding loans are based on the one-year LPR. This comes after the PBoC unexpectedly cut its medium-term policy rate last week. The cut today was no surprise, although smaller than the 15bps expectation. It was a surprise however, that the five-year LPR, which affects mortgage prices, was left at 4.20%. This probably reflects concerns about a weaker yuan, which has had a tough year. USD/CNY increased somewhat when markets opened.

Euro area inflation: On Friday, the final HICP data looked to confirm what country figures already implied. There seems to be no temporary holiday factors, like tourism, that can explain the continued high core price pressures in July. Hotel prices or package holidays have not been off the charts. It looks like a broad based service price pressure, which supports our call for another ECB hike in September.

Japan: On Friday, we also got Japanese inflation data for July. Core inflation (excluding food and energy) increased to 2.7% from 2.6% in June highlighting some inflation stickiness. Price momentum has been weaker for a few months now though, as food and energy prices have been the key inflation drivers this far. Coupled with a disappointing wage print in June and weak domestic demand in the national account data, the pressure on the BoJ to begin tightening has eased somewhat since the July policy tweak. Overall we see good chances of another tweak to the yield curve control in one of the three remaining meetings for this year. The September meeting, however, is starting to look like a non-event.

Equities: Global equities lower again Friday, though with some more optimism in the US cash session. The turn towards defensive and energy continued without any macro drivers or news out of China to change the recent narrative. In US on Friday, Dow +0.1%, S&P 500 -0.01%, Nasdaq -0.2% and Russell 2000 +0.5%. This week starting basically as the previous one with huge focus on China's property sector, some small policy adjustments and falling equities. Outside China, a more upbeat tone with most indices being higher. US and European futures are close to unchanged this morning.

FI: Concerns on China sent global yields lower on Friday from the open by 8-9bp in the 10y area. The 5 to 10y area outperformed the short end and the long end of the curve. After the market open reaction, the rest of the day was mostly side-ways trading. This week, focus turns towards PMIs and the Fed's annual conference in Jackson Hole with Powell and Lagarde both speaking on Friday.

FX: Friday, and last week in general, saw NOK and SEK underperforming other G10 currencies and they have now lost 8% and 7%, respectively vs USD since the troughs in mid-July. EUR/USD has been on a downward trajectory the past month and is currently trading below 1.09. Focus this week is on Jackson Hole speeches including Jerome Powell's on Friday.

Credit: Last Friday completed a full week of daily widening in credit spreads. Itraxx Main widened 1.6bp to 78.1bp while Xover widened 5.9bp to 430.2bp. The weak tone throughout last week was carried by increased anxiety around the Chinese economy and hawkish signals from central banks. A theme that also drove equities wider. In spite of the bearish backdrop, we saw several primary issues during the week, indicating that the markets are not, by any means, in panic mode.