Sample Category Title

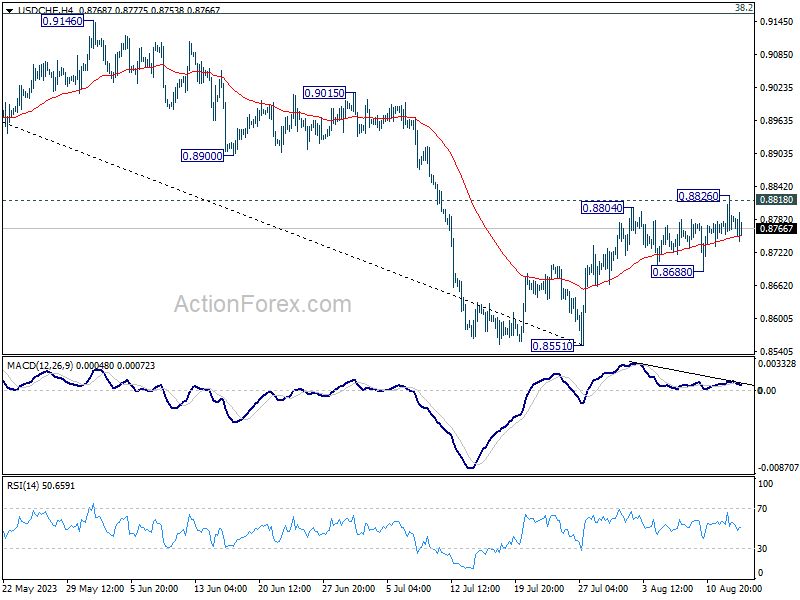

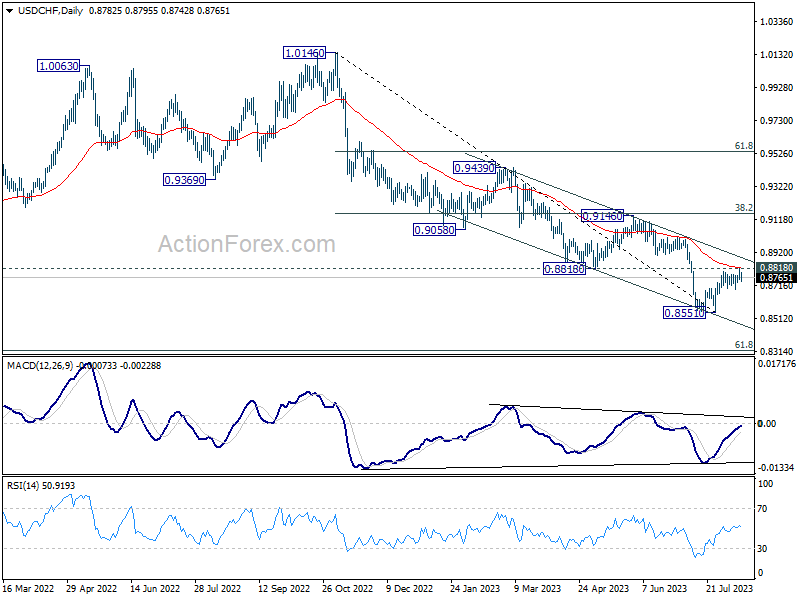

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8747; (P) 0.8787; (R1) 0.8823; More....

Intraday bias in USD/CHF stays neutral for the moment. On the upside, sustained trading above 0.8818 support turned resistance will carry larger bullish implication. Further rally should then be seen to 0.9146 cluster resistance next. However, break of 0.8688 support will indicate rejection by 0.8818, and turn bias back to the downside for retesting 0.8551 low.

In the bigger picture, a medium term bottom could be in place at 0.8551 already, on bullish convergence condition in D MACD. Sustained trading above 0.8818 will bring further rise to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160), even as a correction. Nevertheless, break of 0.8851 will resume the down trend from 1.0146 instead.

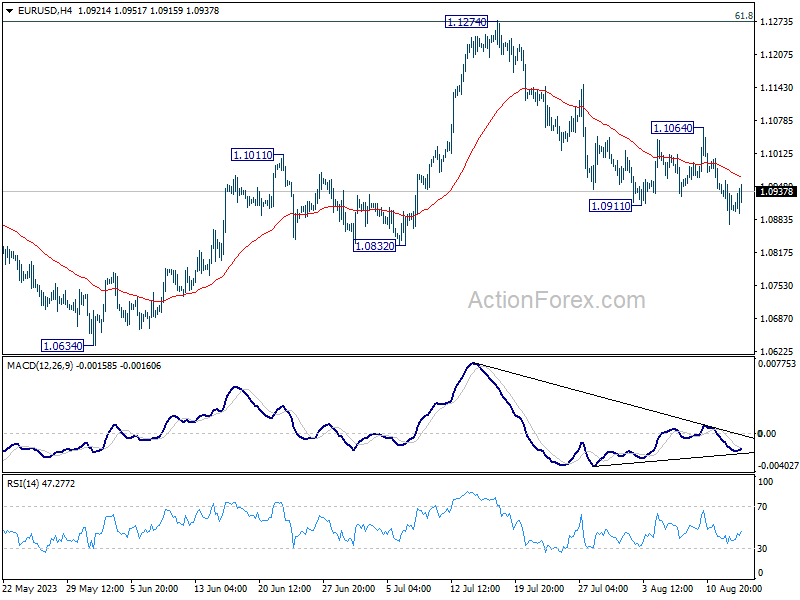

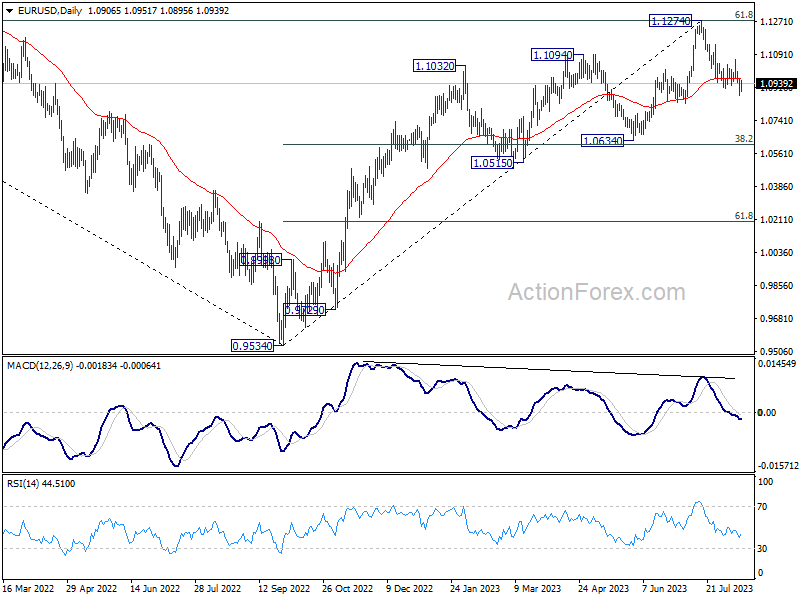

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0867; (P) 1.0914; (R1) 1.0952; More...

No change in EUR/USD's outlook as fall from 1.1064 is expected to continue with 1.1064 resistance intact. Sustained trading below 1.0832 support will target 1.0609/34 cluster support. On the upside, break of 1.1064 resistance is needed to indicate completion of the fall. Otherwise, outlook will stay cautiously bearish in case of recovery.

In the bigger picture, a medium term top could be formed at 1.1274, after failing to break through 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 decisively, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.0966) will bring deeper correction to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to set the range for consolidation.

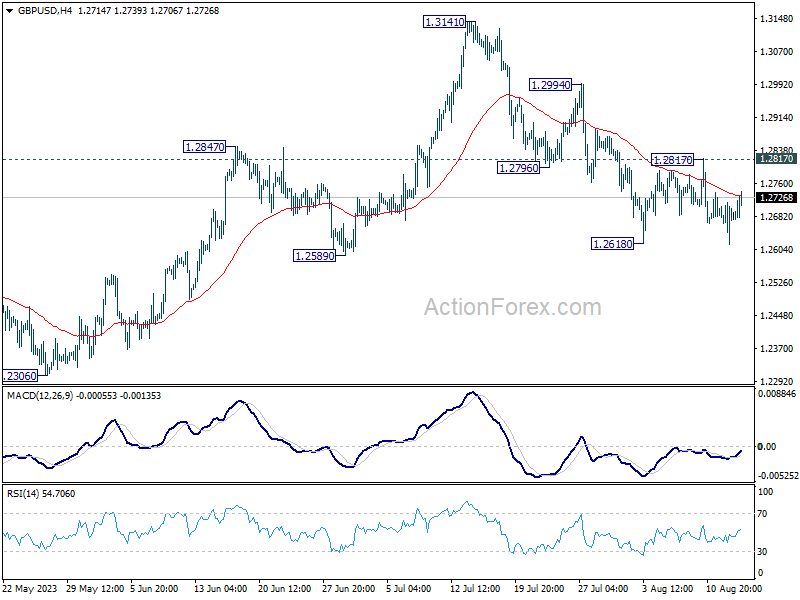

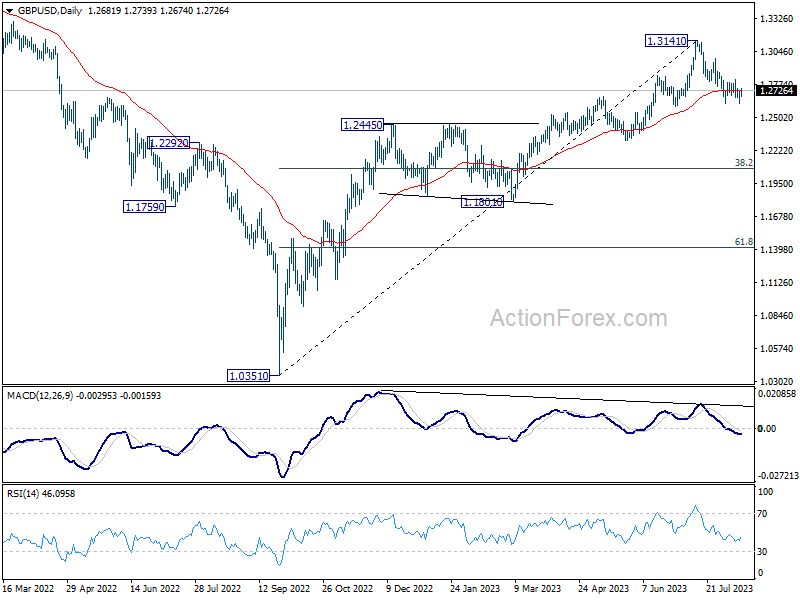

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2631; (P) 1.2673; (R1) 1.2729; More...

GBP/USD recovers notably today but stays below 1.2817 resistance. Intraday bias remains neutral at this point. On the downside, firm break of 1.2618, and sustained trading below 1.2678 resistance turned support will argue that it's already in a larger correction. Deeper decline would then be seen to 1.2306 support next. Nevertheless, break of 1.2817 minor resistance will indicate that the pull back has completed, and turn bias back to the upside for stronger rebound.

In the bigger picture, a medium term top could be in place at 1.3141 already, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.2723) should confirm this case, and bring deeper fall to 38.2% retracement of 1.0351 to 1.3141 at 1.2075, as a correction to up trend from 1.0351 (2022 low). For now, rise will stay mildly on the downside as long as 1.3141 resistance holds, in case of strong rebound.

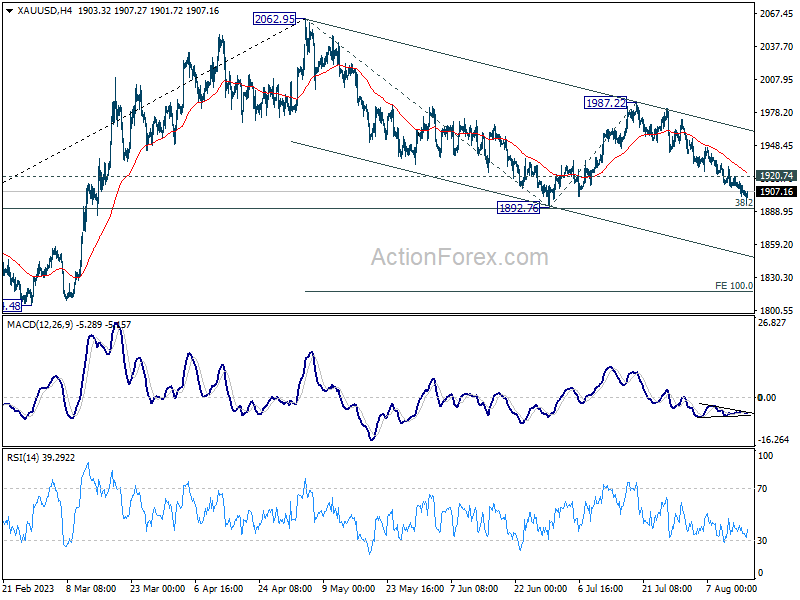

Sterling Jumps on Record Wages Growth, Gold Approaches Key Support

European major currencies are making a notable stride today, with Sterling at the forefront. The Pound ascent is attributed to the historic high recorded in UK regular wage growth. This surge adds further weight to BoE dilemma, pushing it to seriously consider additional monetary tightening in the upcoming month.

While Dollar is making efforts to recoup some of its recent losses, spurred by positive retail sales data surpassing expectations, its upward momentum is noticeably tepid. Canadian Dollar, despite higher than expected inflation figures, has largely been indifferent. This places it in tandem with Australian and New Zealand Dollars, both vying for the least impressive performance of the day. Floating somewhere in the midst, Japanese Yen presents a mixed bag—losing ground against Dollar and Europeans, yet holding its own versus commodity-linked currencies.

Technically, Gold is now approaching key support level at 1892.76 as the fall from 1987.22 extends. Strong rebound from current level, followed by break of 1920.74 minor resistance, will at least indicate some stabilization, with prospect for further rise back towards 1987.22 resistance. However, sustained break of 1892.76 will risk downside acceleration to 100% projection of 2062.95 to 1892.76 from 1987.22 at 1817.06. Under such a bearish scenario, this would likely serve as a green light for the Dollar to momentum, propelling it higher against other major rivals.

In Europe, at the time of writing, FTSE is down -1.20%. DAX is down -0.78%. CAC is down -0.88%. Germany 10-year yield is up 0.0528 at 2.691. Earlier in Asia, Nikkei rose 0.56%. Hong Kong HSI dropped -1.03%. China Shanghai SSE dropped -0.07%. Singapore Strait Times dropped -0.46%. Japan 10-year JGB yield rose 0.0131 to 0.632.

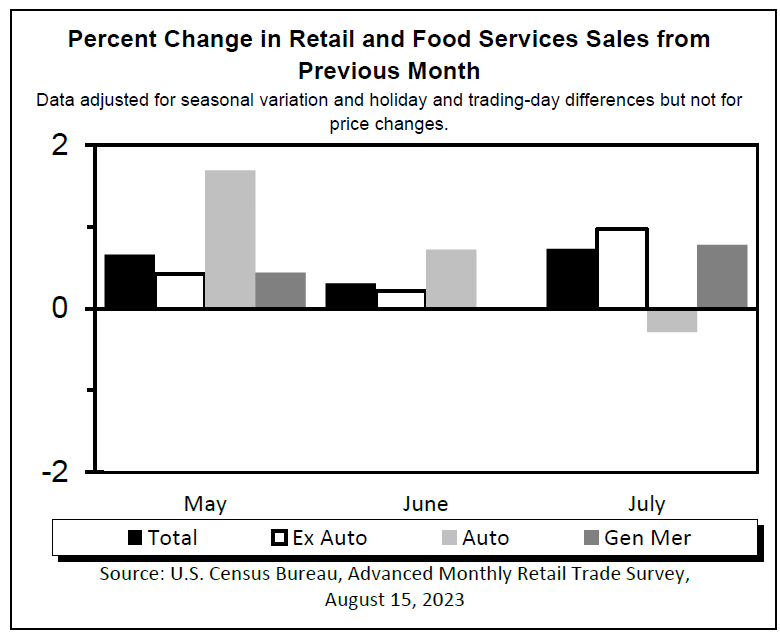

US retail sales rose 0.7% mom in Jul, ex-auto sales up 1.0% mom

US retail sales rose 0.7% mom to USD 696.4B in July, above expectation of 0.4% mom. Ex-auto sales rose 1.0% mom to USD 562.8B, above expectation of 0.4% mom. Ex-gasoline sales rose 0.8% mom to USD 644.0B. Ex-auto, gasoline sales rose 1.0% mom to USD 510.5B.

Total sales for May 2023 through July 2023 period were up 2.3% from the same period a year ago.

Canada CPI rose to 3.3% yoy in Jul, up 0.6% mom

Canadian inflation, measured by CPI, accelerated in July, posting a 0.6% mom increase, doubling expected rise of 0.3% mom. This upward tick, a substantial leap from June's 0.1% gain, was significantly influenced by higher travel tour prices.

On a year-on-year basis, July's CPI leapt from 2.8% yoy to 3.3% yoy , outpacing anticipated 3.0% yoy . A notable factor behind the rapid rise in the headline consumer inflation is base-year effect in gasoline prices. The previous year's steep decline in gasoline prices for July 2022, which saw a -9.2% drop, has ceased to affect the current 12-month trajectory.

Excluding gasoline, CPI rose 4.1% yoy, edging up from 4.0% yoy in June. Excluding energy, CPI decelerated to 4.2% yoy after 4.4% yoy increase in June.

CPI median slowed from 3.9% yoy to 3.7% yoy, matched expectations. CPI trimmed down from 3.7% yoy to 3.6% yoy, above expectation of 3.5% yoy. CPI common also fell from 5.1% yoy to 4.8% yoy, below expectation of 5.0% yoy.

German ZEW rose to -12.3, but current situation dived

August's ZEW Economic Sentiment Index for Germany showed an unexpected improvement, moving from -14.7 to -12.3, beating forecasted -15. However, the Current Situation index took a hit, declining sharply from -59.5 to -71.3—its lowest since October 2022 and below the predicted -63.

Conversely, Eurozone's ZEW Economic Sentiment took an optimistic turn, rising from -12.2 to -5.5, surpassing expected -12. Current Situation Index in the Eurozone also advanced, marking a rise of 2.3 points to -42.0.

ZEW President Professor Achim Wambach commented on the mixed results, noting, "The ZEW Indicator of Economic Sentiment remains in negative territory" but added that there's an anticipated "slight uptick in the economic situation by year-end."

However, he cautioned against over-optimism due to Germany's worsening current economic assessment. Highlighting external influences, Wambach mentioned that the prevailing sentiment suggests no further "interest rate hikes in the eurozone and the United States." He also pointed out a "significant increase" in US economic outlook, which positively impacts Germany's prospects.

UK payrolled employment rose 97k in Jul, unemployment rate at 4.2% in Jun

UK payrolled employment grew 97k, or 0.3% mom in July. June's figure was revised from -9k decrease to 47k increase. Median monthly pay rose 7.8% yoy compare with July 2022, down from prior month's 9.7% yoy. Claimant count rose 29.0k, above expectation of 19.6k.

In the three months to June, unemployment rate rose to 4.2%, above expectation of 4.0%. That's 0.3% higher than previous quarter. Employment rate rose 0.1% to 75.7%. Inactivity rate fell -0.1% to 20.9%. Average earnings including bonus rose 8.2% 3moy, above expectation of 7.3%. Average earnings excluding bonus rose 7.8% 3moy, above expectation of 7.4%, and hit the highest level on record.

China: Unexpected rate cut by PBOC aligns with disheartening July economic data

In an unexpected decision that took markets by surprise, PBoC announced a cut in key policy rates for the second time in a span of three months, just an hour before the release of July economic data that broadly fell short of market expectations.

PBOC lowered the rate on its one-year medium-term lending facility loans – valued at CNY 401B – to financial institutions by 15bps to 2.50% from the previous 2.65%. This significant move indicates the possibility of a reduction in China's benchmark loan prime rate in the upcoming week.

A closer look at the economic metrics for July reveals concerns. Industrial production grew at 3.7% yoy, underperforming against the anticipated 4.3% yoy and marking a slowdown from the 4.4% yoy of the previous month. Similarly, retail sales saw increase of just 2.5% yoy, lagging behind projected 4.2% yoy and decelerating from 3.1% yoy. This rate marks the slowest growth pace in sales since the decline observed in December 2022. Furthermore, fixed asset investment growth, year-to-date year-on-year, was recorded at 3.4%, falling short of 3.8% expectation.

Urban unemployment rate witnessed a slight increase, moving from 5.2% to 5.3%. Notably, NBS did not provide the usual age breakdown of unemployment figures. The spokesperson mentioned the suspension of youth unemployment data attributing it to societal and economic changes, and highlighted an ongoing reassessment of its data collection methodology. It's worth noting that in June, the youth unemployment rate (for ages 16-24) reached a record high of 21.3%

NBS also said in a statement, "We must intensify the role of macro policies in regulating the economy and make solid efforts to expand domestic demand, shore up confidence and prevent risks."

Japan's Q2 GDP grew 6% annualized, external demand drives growth

Japan witnessed a stellar performance in its Q2 GDP, registering a growth of 1.5% Qoq, a figure that comfortably surpassed the anticipated 0.8% qoq rise. In annualized terms, growth clocked in at 6.0%, notably higher than expected 3.1%. This rapid expansion marked the quickest pace since the October-December period of 2020 and signifies the third consecutive quarterly growth.

A significant driver of this growth was a 3.2% surge in exports during the quarter. The rejuvenation in external demand, particularly net exports, added a substantial 1.8% to the quarter's growth. The auto exports sector reaped benefits from the alleviation of supply disruptions, while a consistent uptick in international tourists bolstered the economy. On the flip side, imports dipped by -4.3% as energy and COVID vaccine imports declined.

A closer look at the domestic sector unveils a few challenges. Private consumption, a sector that constitutes over half of the economy, contracted by -0.5% on a quarterly basis. This resulted in domestic demand cutting -0.3% from growth. The mounting prices of regular commodities affected consumer spending negatively. Furthermore, sales of durable goods took a hit, which overshadowed the robust demand for services.

In terms of capital investment, the growth remained tepid, registering just a 0.03% increase. However, it's noteworthy that this was buoyed by spending related to software, marking its second successive quarter of rise.

RBA sees credible path back to inflation target with interest rate at present level

In the minutes from RBA's August 1 meeting, board members weighed the decision between raising cash rate by 25bps or maintaining its unchanged.

The board's inclination to hold the rate steady was rooted in their belief that prior tightening measures were "working as intended." Despite the full effects not yet being evident in the data, there were important signs, as "consumption had already slowed significantly", "labour market might be at a turning point", and "inflation was heading in the right direction".

The board observed a "credible path back to the inflation target with the cash rate staying at its present level." This assessment seemed to be "broadly in line with the staff's central forecasts." Solidifying their position, members collectively agreed that the reasons to "leave the cash rate unchanged at this meeting was the stronger one."

Meanwhile, they also acknowledged that "further tightening of monetary policy might be required" to consistently meet inflation goals. Such decisions will be driven by data trends and ongoing risk assessments.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2631; (P) 1.2673; (R1) 1.2729; More...

GBP/USD recovers notably today but stays below 1.2817 resistance. Intraday bias remains neutral at this point. On the downside, firm break of 1.2618, and sustained trading below 1.2678 resistance turned support will argue that it's already in a larger correction. Deeper decline would then be seen to 1.2306 support next. Nevertheless, break of 1.2817 minor resistance will indicate that the pull back has completed, and turn bias back to the upside for stronger rebound.

In the bigger picture, a medium term top could be in place at 1.3141 already, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.2723) should confirm this case, and bring deeper fall to 38.2% retracement of 1.0351 to 1.3141 at 1.2075, as a correction to up trend from 1.0351 (2022 low). For now, rise will stay mildly on the downside as long as 1.3141 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | GDP Q/Q Q2 P | 1.50% | 0.80% | 0.70% | |

| 23:50 | JPY | GDP Deflator Y/Y Q2 P | 3.40% | 3.80% | 2.00% | |

| 01:30 | AUD | RBA Meeting Minutes | ||||

| 01:30 | AUD | Wage Price Index Q/Q Q2 | 0.80% | 1.00% | 0.80% | |

| 02:00 | CNY | Industrial Production Y/Y Jul | 3.70% | 4.30% | 4.40% | |

| 02:00 | CNY | Retail Sales Y/Y Jul | 2.50% | 4.20% | 3.10% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Jul | 3.40% | 3.80% | 3.80% | |

| 04:30 | JPY | Industrial Production M/M Jun F | 2.40% | 2.00% | 2.00% | |

| 06:00 | GBP | Claimant Count Change Jul | 29.0K | 19.6K | 25.7K | 16.2K |

| 06:00 | GBP | ILO Unemployment Rate (3M) Jun | 4.20% | 4.00% | 4.00% | |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Jun | 8.20% | 7.30% | 6.90% | 7.20% |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jun | 7.80% | 7.40% | 7.30% | 7.50% |

| 06:30 | CHF | Producer and Import Prices M/M Jul | -0.10% | 0.20% | 0.00% | |

| 06:30 | CHF | Producer and Import Prices Y/Y Jul | -0.60% | -0.50% | -0.60% | |

| 09:00 | EUR | Germany ZEW Economic Sentiment Aug | -12.3 | -15 | -14.7 | |

| 09:00 | EUR | Germany ZEW Current Situation Aug | -71.3 | -63 | -59.5 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Aug | -5.5 | -12 | -12.2 | |

| 12:30 | CAD | Manufacturing Sales M/M Jun | -1.70% | -2.10% | 1.20% | |

| 12:30 | CAD | CPI M/M Jul | 0.60% | 0.30% | 0.10% | |

| 12:30 | CAD | CPI Y/Y Jul | 3.30% | 3.00% | 2.80% | |

| 12:30 | CAD | CPI Media Y/Y Jul | 3.70% | 3.70% | 3.90% | |

| 12:30 | CAD | CPI Trimmed Y/Y Jul | 3.60% | 3.50% | 3.70% | |

| 12:30 | CAD | CPI Common Y/Y Jul | 4.80% | 5.00% | 5.10% | |

| 12:30 | USD | Empire State Manufacturing Index Aug | -19 | -0.3 | 1.1 | |

| 12:30 | USD | Retail Sales M/M Jul | 0.70% | 0.40% | 0.20% | 0.30% |

| 12:30 | USD | Retail Sales ex Autos M/M Jul | 1.00% | 0.40% | 0.20% | |

| 12:30 | USD | Import Price Index M/M Jul | 0.40% | 0.20% | -0.20% | |

| 14:00 | USD | Business Inventories Jun | 0.20% | 0.20% | ||

| 14:00 | USD | NAHB Housing Market Index Aug | 56 | 56 |

US retail sales rose 0.7% mom in Jul, ex-auto sales up 1.0% mom

US retail sales rose 0.7% mom to USD 696.4B in July, above expectation of 0.4% mom. Ex-auto sales rose 1.0% mom to USD 562.8B, above expectation of 0.4% mom. Ex-gasoline sales rose 0.8% mom to USD 644.0B. Ex-auto, gasoline sales rose 1.0% mom to USD 510.5B.

Total sales for May 2023 through July 2023 period were up 2.3% from the same period a year ago.

Canada CPI rose to 3.3% yoy in Jul, up 0.6% mom

Canadian inflation, measured by CPI, accelerated in July, posting a 0.6% mom increase, doubling expected rise of 0.3% mom. This upward tick, a substantial leap from June's 0.1% gain, was significantly influenced by higher travel tour prices.

On a year-on-year basis, July's CPI leapt from 2.8% yoy to 3.3% yoy , outpacing anticipated 3.0% yoy . A notable factor behind the rapid rise in the headline consumer inflation is base-year effect in gasoline prices. The previous year's steep decline in gasoline prices for July 2022, which saw a -9.2% drop, has ceased to affect the current 12-month trajectory.

Excluding gasoline, CPI rose 4.1% yoy, edging up from 4.0% yoy in June. Excluding energy, CPI decelerated to 4.2% yoy after 4.4% yoy increase in June.

CPI median slowed from 3.9% yoy to 3.7% yoy, matched expectations. CPI trimmed down from 3.7% yoy to 3.6% yoy, above expectation of 3.5% yoy. CPI common also fell from 5.1% yoy to 4.8% yoy, below expectation of 5.0% yoy.

WTI Oil Technical: Time for a Potential Short-Term Pullback

- Recent bullish breakout from “Descending Wedge” has led to a 10% rally to reach a medium-term resistance zone of US$83.80/84.90.

- Technical elements are now advocating a potential corrective pull-back with supports coming in at US$79.80 and US$77.20.

- Today’s surprise three interest rate cuts by China’s central bank, PBoC has triggered a risk-off behaviour in cross-assets (FX, stock indices, commodities) via a negative reflexivity feedback loop.

The price actions of West Texas Oil (a proxy of WTI crude oil futures) have indeed shaped the bullish breakout from its “Descending Wedge” configuration on 24 July and rallied by +10% to print an intraday high of US$84.92 per barrel on last Thursday, 10 August which coincided with a medium-term resistance zone of US$83.80/84.90 (see daily chart).

Today, West Texas Oil has shed almost -1% intraday at this time of the writing to print an intraday low of $81.60 that recorded an accumulated loss of -3.7% in the past two sessions since Thursday, 10 August high of US$84.92.

The current weakness of oil has been in line with a broad-based risk-off behaviour seen in cross-assets today (FX, major stock indices & industrial metals commodities) attributed to the contagion fear in China’s financial system after a major trust fund failed to make timely payments to holders of its wealth management products that are backed by unsold properties of indebted property developers.

Today’s unexpected interest rate cut by China’s central bank, PBoC on its 1-year medium-term lending facility (MLF) interest rate by 15 basis points (bps), more than the previous 10 bps cut implemented in June to bring it down to 2.50%, its lowest level since late 2009. The 1-year MLF rate is a benchmark interest rate in China where PBoC provides a credit line to major commercial banks which in turn acts as a guide for another two benchmark interest rates that commercial banks charged to customers: the 1-year and 5-year loan prime rates.

Interestingly, PBoC enacted two more interest rate cuts today on the overnight standing lending facility (SLF) which was cut by 10 bps to 2.65% while the 7-day and 1-month SLF rates were cut by 10 bps each to 2.80% and 3.15% respectively.

Three interest rate cuts in a single day are considered a “rare” event in China given that the current guidance from China’s top policymakers is in favour of targeted stimulus policies to address the current economic growth slowdown rather than enacting “opening the liquidity floodgate” measures.

Hence, today’s surprise move on China’s more accommodative monetary policy stance is perceived as a heightened red alert on its financial system where trust firms’ default risks have risen that may trigger a systemic contagion which in turn created the negative reflexivity feedback loop seen today.

Daily RSI oscillator conditions suggest an imminent short-term pull-back

Fig 1: West Texas Oil medium-term trend as of 15 Aug 2023 (Source: TradingView, click to enlarge chart)

The daily RSI oscillator flashed a bearish divergence condition at its overbought region on 9 August 2023 which suggests that the medium-term upside momentum of West Texas Oil is overstretched, and its price actions face the risk of a corrective pull-back to retrace certain portions of the current 26% rally of its medium-term uptrend phase from 28 June 2023 low of US$66.95.

A bearish breakdown below minor ascending channel support

Fig 2: West Texas Oil minor short-term trend as of 15 Aug 2023 (Source: TradingView, click to enlarge chart)

Today’s price actions of West Texas Oil have staged a bearish breakdown below its minor ascending channel support from the 28 June 2023 low.

Watch the US$83.80 key short-term pivotal resistance to maintain the short-term bearish tone to see the next support coming in at US$79.80 and a break below it exposes US$77.20 next (also the key 200-day moving average).

On the flip side, a clearance above US$83.80 invalidates the corrective pull-back scenario for a retest of the 10 August 2023 swing high area of US$84.90 and a clearance above it sees the next resistance coming in at US$87.00 (psychology level & Fibonacci extension).

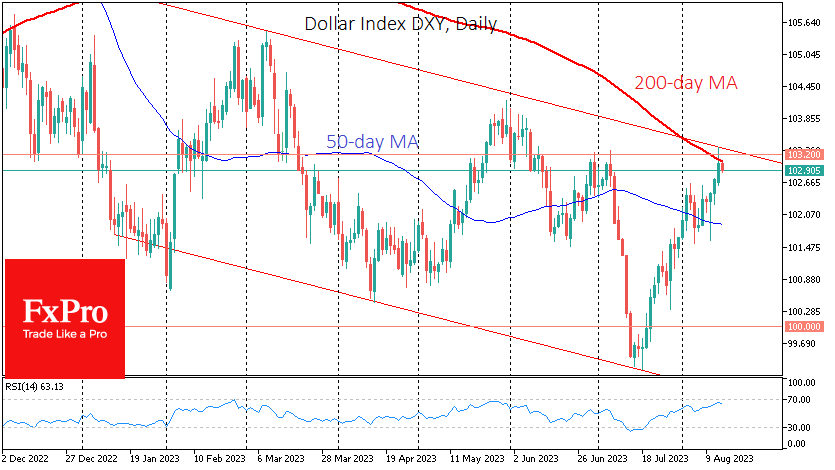

Dollar Trying to Break Bear Trend

The DXY has gained more than 3.8% over the past month, fully retracing its losses from five trading sessions in early July after the NFP. This retracement carries extra weight; a sharp upward or downward from current levels would be an essential trend indicator.

The Dollar Index is now approaching 103, where the local July highs, the 200-day MA and the upper boundary of the bearish corridor since last November are concentrated.

The downtrend was formed in the last quarter of last year when the Fed slowed the pace of its rate hikes following a decline in the annual price growth rate. Since then, inflation has continued to rise in other developed economies. As a result, the leading currency trade has been betting on a resumption of the dollar correction as the spread between US government bond yields and those of other major economies narrows.

This trend is now being tested as inflation in European countries has fallen at an accelerated pace. Meanwhile, economic data in the US is fuelling domestic inflation. As a result, yields on 10-year US government bonds are close to last year’s highs, fuelling interest relative to alternatives in other developed countries. These flows have contributed to the dollar’s rally over the past month.

The DXY has risen to the 200-day MA, a long-term trend indicator. Earlier this month, the dollar index consolidated above the 50-day MA, associated with a medium-term trend.

Further growth with consolidation above 103.2 will show that the downtrend has been broken and that the growth impulse to the 105.3-107.5 range will begin in the coming months.

Nevertheless, betting on further dollar growth seems premature before an upward reversal is confirmed. In the absence of such confirmation, the scenario of a continuation of the downtrend remains valid. The lower boundary of the working range is 4% below current levels, and the dollar could be there within a couple of months.

Therefore, the next few days will determine whether the dollar will decide to break its almost year-long downtrend or remain within its framework. Tomorrow’s release of the FOMC meeting minutes could provide an important clue as to the direction of travel. However, it is more likely that the dollar’s path will be determined at the end of next week during the Fed’s Jackson Hole symposium.

Australian Dollar Extends Losses as Wage Growth Falls

- Australian dollar extends losses

- Australia’s wage growth eases to 3.2%

- China’s retail sales decline

The Australian dollar hasn’t recorded a winning daily session in over a week and is in negative territory on Tuesday. In the European session, AUD/USD is trading at 0.6468, down 0.28%. On Monday, the Australian dollar dropped as low as 0.6453, its lowest level since early November 2022.

Australian wage growth eases in the second quarter

Australia’s wage growth ticked lower to 3.6% y/y in the second quarter, compared to 3.7% in Q1. Wages rose 0.8% q/q for a third straight quarter in Q2. The takeaway is that although wage growth remains high, we’re not seeing a rise. That is an encouraging sign for the Reserve Bank of Australia, as higher wages raise the possibility of a wage-price spiral, which would hurt the RBA’s efforts to reduce inflation.

The RBA has made its rate stance very clear, saying that rate hikes remain on the table but any decision will be based on economic data. Today’s wages report is unlikely to cause any shift at the RBA. The probability of a pause is currently 93%, compared to 95% prior to the wage growth release, according to the ASX RBA rate tracker.

Weak wage growth isn’t great news for households, who are seeing their purchasing power erode due to high inflation. The good news is that lower wage growth will make it easier for the RBA to start to trim rates if inflation cooperates and continues to fall.

The RBA minutes, released today, indicated that the RBA viewed the risks to the economy as “finely balanced” between tightening too fast or allowing inflation to remain too high. In the end, the decision to pause was based on weaker economic growth and the “acute financial challenges” that some households faced due to rising rates.

China has posted a host of weak economic data, and the trend continued on Tuesday. Retail sales slowed to 2.5% y/y in July, down from 3.1% in June and well below the 4.5% consensus estimate. The unemployment rate ticked higher to 5.3% in July, up from 5.2% a month earlier. China’s central bank responded by cutting key policy rates today, in an attempt to kick-start the sputtering economy. The surprise move by the central bank has raised speculation that it could trim the 5-year lending prime rate (LPR) next week.

AUD/USD Technical

- AUD/USD is putting pressure on resistance at 0.6449. This is followed by support at 0.6402

- 0.6532 and 0.6579 are the next resistance lines

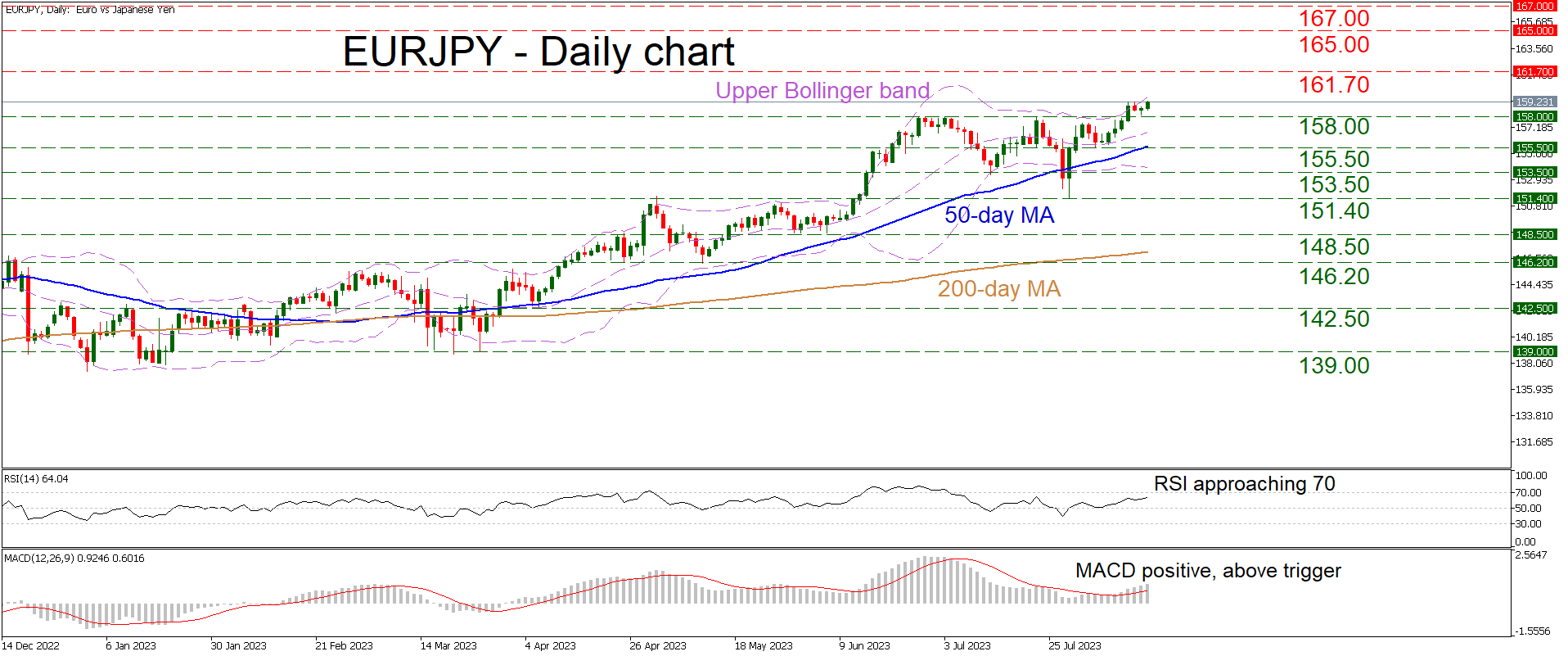

EURJPY Hits Fresh 15-Year High as Yen Gets Smoked

EURJPY has been grinding higher, hitting its best levels in 15 years earlier today. The series of higher highs and higher lows remains in place, keeping the pair in a clear uptrend.

As a testament to how powerful the rally has been, the pair is trading near its upper Bollinger band and well above its longer-term moving averages (MAs). Similarly, momentum indicators such as the RSI and the MACD are flashing bullish signals, although neither is at extreme levels yet.

Another push higher could encounter some resistance near the 161.70 area, defined by the inside swing high in February 2008. If the bulls charge ahead, the next region to give them trouble might be the 165.00 barrier, marked by the highs of April 2008. Even higher, the focus would shift to the 167.00 zone, which acted as support multiple times in the summer of 2008.

Now if sellers manage to retake the wheel, the first barrier to their drive lower would likely be the 158.00 territory, which served as resistance in recent weeks and might now provide support. Penetrating below that, the spotlight would fall on the 155.50 hurdle, which is roughly where the 50-day MA has converged as well.

All told, the picture remains decisively bullish. It would take a clean break below the recent low of 151.40 to change that.