Sample Category Title

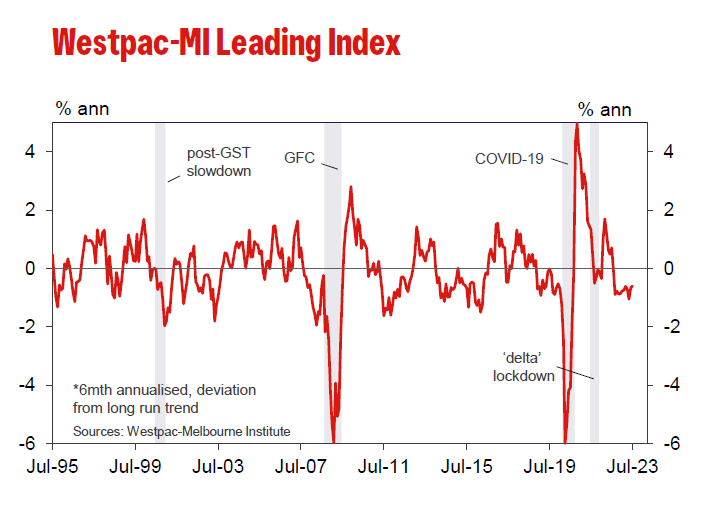

Australia’s Westpac leading index ticks up, but below-par growth set to persist

Australia's Westpac Leading Index figures reveals that growth rate has shown a marginal uptick, moving from -0.67% to -0.60% in July. But alarmingly, this marks the twelfth consecutive month in red, representing the longest stretch of such negative prints in a span of seven years, barring the COVID-affected period.

The subdued, below-par growth momentum witnessed throughout 2023 seems set to persist into the subsequent year. Westpac predicts deceleration in GDP growth to a mere 1% for the current year. Any potential rebound is anticipated to be minimal, with projections indicating a slight rise to 1.4% annually in 2024 – with the bulk of this growth concentrated towards the year-end.

Regarding RBA meeting on September 5, Westpac sets its expectations clear. The institution foresees cash rate remaining stable at 4.10%, denoting the zenith of this current tightening phase.

Referring the recent remarks of RBA Governor before the House of Representatives Standing Committee on Economics, the note emphasized, "Policy is now in a 'calibration' phase with small adjustments still possible if the data starts to show clear risks of a slower return to low inflation."

Nevertheless, given the evident frailty in growth momentum – as underscored by the most recent Leading Index update – coupled with the broader dynamics of price and wage inflation aligning with RBA's forecasts, "the threshold for additional tightening is high and unlikely to be met."

AUD/USD Dips Below 0.6500, FOMC Minutes Next

Key Highlights

- AUD/USD traded below the 0.6500 support zone.

- A major bearish trend line is forming with resistance near 0.6495 on the 4-hour chart.

- EUR/USD is consolidating losses near the 1.0900 zone.

- GBP/USD might face resistance near 1.2770 and 1.2800.

AUD/USD Technical Analysis

The Aussie Dollar started a fresh decline from well above 0.6720 against the US Dollar. AUD/USD traded below the 0.6620 support to move into a bearish zone.

Looking at the 4-hour chart, the pair settled below the 0.6550 level, the 100 simple moving average (red, 4 hours), and the 200 simple moving average (green, 4 hours).

The pair also traded below the 1.2500 support zone and tested 0.6425. A low is formed near 0.6428 and the pair is now consolidating losses. On the upside, an initial resistance is near the 0.6475 level. The first major resistance is near 0.6500.

There is also a major bearish trend line forming with resistance near 0.6495 on the same chart. A close above the 0.6500 resistance could start a decent increase.

In the stated case, the pair could rise toward the 0.6550 level. Any more gains could start a fresh increase toward the 0.6620 level.

Initial support is near the 0.6425 level. The next major support is near 0.6400, below which AUD/USD could gain bearish momentum. In the stated case, the pair could test the 0.6325 support.

Looking at EUR/USD, the pair is showing bearish signs and is currently consolidating losses near the 1.0900 level.

Economic Releases

- Euro Zone Gross Domestic Product Q2 2023 (Preliminary) (QoQ) - Forecast 0.6%, versus 0.6% previous.

- FOMC Meeting Minutes.

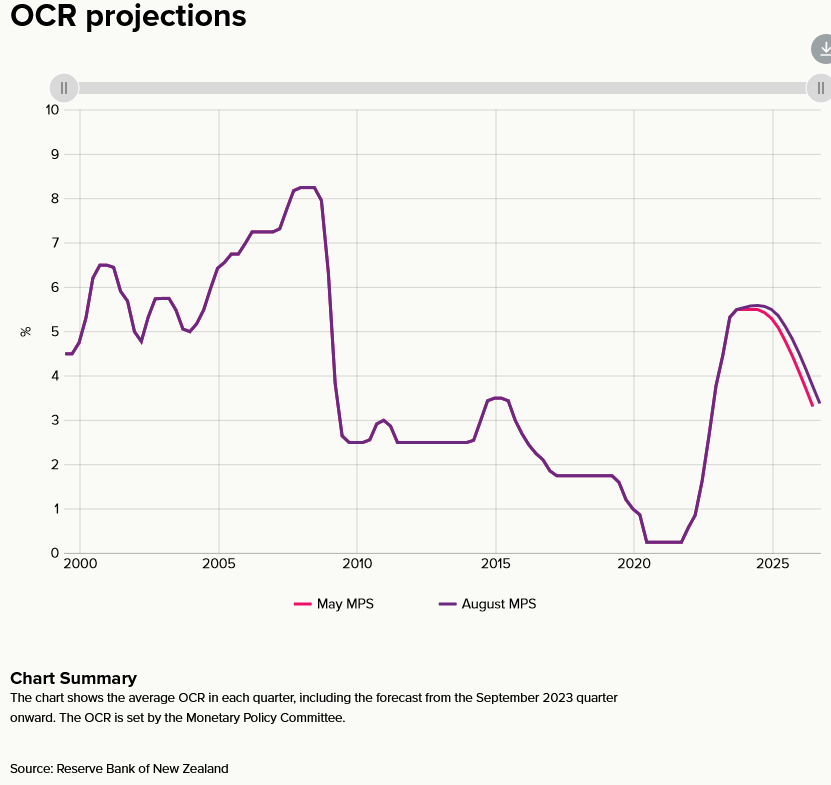

RBNZ on hold, OCR to stay high for longer

RBNZ has decided to maintain OCR unchanged at 5.50% again, aligning with broad market expectations. Making its stance clear, the bank asserted that the "OCR needs to stay at restrictive levels for the foreseeable future."

Reflecting a neutral stance, the central bank emphasized its confidence in the current monetary policy, "that with interest rates remaining at a restrictive level for some time, consumer price inflation will return to within its target range of 1 to 3% per annum, while supporting maximum sustainable employment."

Adding depth to its economic perspective, "The nominal neutral OCR has increased by 25 basis points to 2.25% within the projections," the Committee noted. They were in consensus that the existing OCR level was contractionary, asserting that it's effectively curbing domestic spending as intended.

Shifting the lens to future projections, the forecasts in the Monetary Policy Statement hint at the OCR potentially reaching a peak of 5.6% in the first quarter of 2024. This marks a slight shift from the earlier prediction of 5.5% in Q3 2023, hinting at the possibility of an additional rate hike. As for subsequent rate cut expectations are now set for the second quarter of 2025, a slight delay from the previously anticipated period between Q4 2024 and Q1 2025.

(RBNZ) Official Cash Rate remains at 5.5%

The Monetary Policy Committee today agreed to maintain the Official Cash Rate (OCR) at 5.5%.

The current level of interest rates is constraining spending and hence inflation pressure, as anticipated and required. The Committee agreed that the OCR needs to stay at restrictive levels for the foreseeable future to ensure annual consumer price inflation returns to the 1 to 3% target range, while supporting maximum sustainable employment.

The New Zealand economy is evolving broadly as anticipated. Activity continues to slow in parts of the economy that are more sensitive to interest rates. Labour shortages are easing as overall demand softens and immigration adds to labour resources. Headline inflation and inflation expectations have declined, but measures of core inflation remain too high.

Globally, economic growth remains below trend and headline inflation has eased for most of our trading partners. Core inflation remains high in many countries. Weakening global economic growth is putting downward pressure on New Zealand export prices.

The imbalance between demand and supply is moderating in the New Zealand economy. However, a prolonged period of subdued spending growth is still required to better match the supply capacity of the economy and reduce inflation pressure.

In the near term, there is a risk that activity and inflation measures do not slow as much as expected. Over the medium-term, a greater slowdown in global economic demand, particularly in China, could weigh more on commodity prices and overall New Zealand export revenue.

The Committee is confident that with interest rates remaining at a restrictive level for some time, consumer price inflation will return to within its target range of 1 to 3% per annum, while supporting maximum sustainable employment.

Media contact

James Weir

Senior Adviser External Stakeholders

Phone:+64 4 471 3962 Mobile: 021 103 1622

Email: James.Weir@rbnz.govt.nz

Summary record of meeting

The Monetary Policy Committee discussed recent developments in the New Zealand economy. The Committee agreed that monetary conditions are restricting spending and reducing inflationary pressure as anticipated. While supply constraints in the economy continue to ease, inflation remains too high. Spending needs to remain subdued to better match the economy's ability to supply goods and services, so that consumer price inflation returns to its target range.

Global economic growth remains below trend for most of our trading partners. While global growth was resilient across the first half of the year this is beginning to fade, particularly in China. Globally, headline inflation has declined but core inflation remains high in many countries. The Committee noted that regional divergences in the moderation of core inflation are beginning to emerge.

New Zealand's export volumes over the last quarter were more resilient than expected due to favourable agricultural growing conditions in some regions. However, export revenues are expected to ease, in line with weakening global demand. A decline in global commodity prices has seen prices for New Zealand's exports moderate.

The Committee noted that tight monetary conditions continue to constrain domestic spending. The slowdown in economic activity is most notable in the parts of the economy that are more sensitive to interest rates. The Committee judged that with monetary conditions remaining restrictive, they expect to see further declines in consumption per capita and for GDP growth to be subdued over coming quarters.

Annual CPI inflation declined to 6.0% in the June quarter, with tradables inflation declining more than non-tradables inflation. Most measures of inflation expectations have declined alongside the fall in headline inflation. However, measures of core inflation remain near their recent highs.

The Committee discussed the labour market and agreed that capacity pressures have begun to ease. Recent net immigration has increased labour supply, helping to alleviate some labour market shortages. Employment growth remains resilient. The Committee noted that most measures of annual wage inflation have begun to ease.

The Committee noted that the estimate of the nominal neutral OCR has increased by 25 basis points to 2.25% within the projections, consistent with the Reserve Bank's indicator suite. The Committee agreed that the current level of the OCR remains contractionary and is constraining domestic spending as needed.

The Committee discussed the increase in the current account deficit and noted that this is primarily due to reduced services exports stemming from the COVID-19 pandemic as well as excess domestic demand. The current account deficit is expected to steadily narrow. Members noted that net foreign liabilities have declined over recent years and that risks associated with funding the deficit were low, as most foreign debt is hedged against foreign exchange risk.

The Committee discussed the recent strong growth in net immigration. The overall impact on demand and inflation pressure remains uncertain. Members noted that the current increase in net immigration may be less inflationary than previous increases, due to both changes to the composition of migrants and in the context of a tight domestic labour market.

The Committee noted that house prices appear to have stabilised. Members agreed that the current projection for house prices was reasonably balanced, remaining around estimates of sustainable levels. The Committee agreed that house price changes have an impact on household wealth. However, members agreed the willingness to consume out of wealth can vary and may be lower in the current context of high debt servicing costs.

The Committee discussed the balance of risks for inflation, output, and employment. Members noted that current projections are for subdued GDP growth, rather than a sharp downturn.

In discussing near-term risks, members considered upside risks to activity and inflation. Members discussed the impact of recent administered price increases – for example, council rates and excise tax – on headline inflation for the September quarter and noted that this could pose a risk to inflation expectations. Members also discussed risks around a slower easing in the labour market resulting in wage inflation taking longer to decline.

The Committee noted that the projections for government expenditure and revenue are predicated on Budget 2023 forecasts. Overall, real government consumption and investment spending as a share of potential GDP is projected to decline over the forecast horizon.

Over the medium term, the Committee discussed risks around the outlook for global growth and judged that these were skewed to the downside. A greater slowdown in global growth would likely see a fall in import prices. Members noted that weaker global demand, particularly from China, could weigh further on commodity prices and therefore on export revenues.

Members also discussed the risks around the lagged effect of previous monetary tightening on households and businesses. The average mortgage rate on outstanding loans is expected to rise from around 5% to near 6% by early 2024, and debt servicing costs as a share of income are still increasing.

Members discussed the risk to those parts of the economy most exposed to lower commodity or asset prices. The Committee agreed that the slowdown in economic activity will not be even across sectors of the economy, due to global factors and the varied impact of high domestic interest rates. In particular, the Committee noted that pockets of stress were beginning to emerge for some households, and the commercial property, agriculture, and construction sectors.

The Committee agreed that in the current circumstances, there is no material trade-off between meeting the Committee's inflation and employment objectives and maintaining the stability of the financial system. Members noted that debt levels are high in some parts of the economy and debt servicing costs have increased. While broad indicators of stress have increased, non-performing loans remain at low levels.

In discussing their Remit objectives, the Committee noted inflation is still expected to decline within the target band by the second half of 2024. The Committee agreed that the risks around the inflation projection remain balanced. Employment is above its maximum sustainable level, however, recent indicators show that labour market pressures continue to ease.

The Monetary Policy Committee discussed the appropriate stance of monetary policy. The Committee agreed that interest rates still need to remain at a restrictive level for the foreseeable future, to ensure annual consumer price inflation returns to the 1 to 3% target range while supporting maximum sustainable employment.

On Wednesday 16 August, the Committee reached a consensus to maintain the Official Cash Rate at 5.50%.

Attendees:

Reserve Bank members of MPC: Adrian Orr, Karen Silk, Christian Hawkesby, Paul Conway

External MPC members: Bob Buckle, Peter Harris, Caroline Saunders

Treasury Observer: Dominick Stephens

MPC Secretary: Kate Poskitt

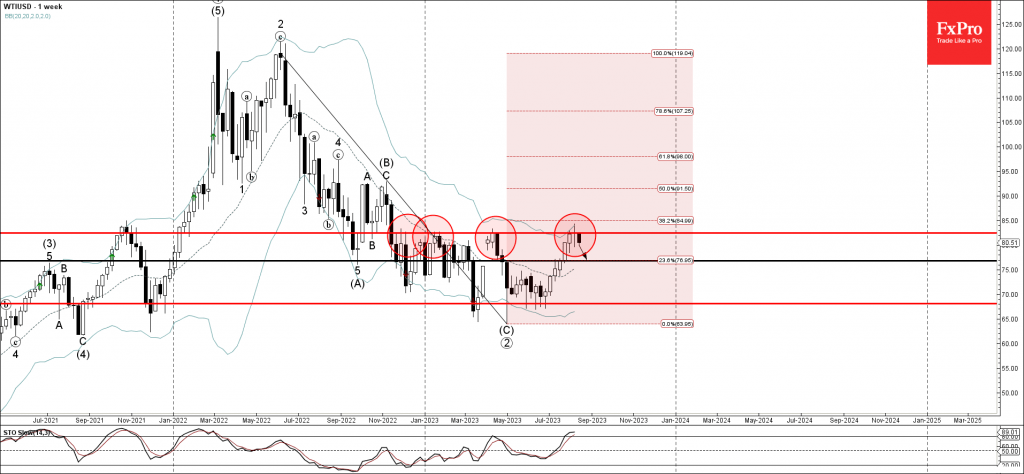

WTI Wave Analysis

- WTI reversed from resistance level 82.50

- Likely to fall to support level 76.80.

WTI crude oil recently reversed down from the major long-term resistance level 82.50 (which has been reversing the price from the end of last year).

The resistance level 82.50 was strengthened by the upper daily Bollinger Band and the 38.2% Fibonacci correction of the previous downtrend from last year. Given the strength of the resistance level 82.50 and the overbought weekly Stochastic, WTI crude oil can be expected to fall further toward the next support level 76.80.

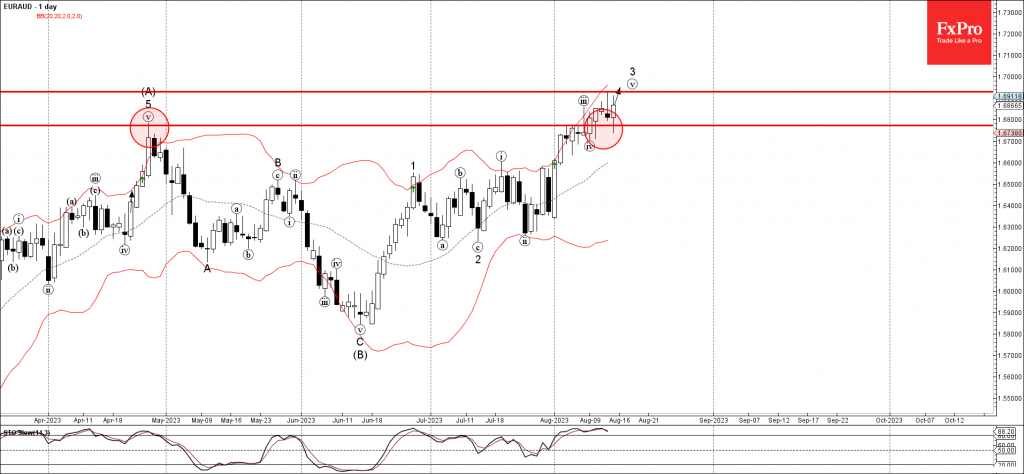

EURAUD Wave Analysis

- EURAUD reversed from support level 1.6770

- Likely to rise to resistance level 1.6930

EURAUD currency pair recently reversed up from the pivotal support level 1.6770 (former multi-month high from April).

The upward reversal from the support level 1.6770 continues the minor impulse waves v and 3, which belong to the intermediate impulse wave (C) from June.

Given the clear daily uptrend, EURAUD can be expected to rise further toward the next resistance level 1.6930, target for the completion of the active impulse waves v and 3.

Stocks Drop on China Jitters and as Global Bond Selloff Continues

US stocks remained heavy after a robust retail sales report sent yields higher and raised the odds that the Fed might not be done raising rates. A healthy consumer was supposed to drive soft landing calls, but too much consumer resilience will drive the Fed to keep rates higher for longer. This US retail sales report showed spending is picking up, especially given the upward revisions for June's report.

Equities were heavy in early trade as concerns grow that China is in a lot worse shape than initially thought. Ahead of some key data, the PBOC decided to be proactive and delivered a surprise rate cut. China cut the 1-year medium term lending rate facility from 2.65% to 2.50%, which was the steepest reduction since 2020. The data that followed the rate cut was uninspiring for the rest of the year and will force officials into delivering a lot more easing. Key Chinese industrial production, retail sales, and investment data all came in softer-than-expected.

UK

Record wage growth will keep the pressure on the BOE to deliver more tightening. The economy still has a tight labor market as companies need to pay their employees more money. The rise in the unemployment rate was due to more people returning to the workforce. Average pay excluding bonuses easily exceeded the consensus estimate of 7.4%, rising 7.8% in the three months through June from a year ago.

This hot wage data is giving the BOE hawks a win as they were right in calling for a half-point rate increase last meeting. The British pound is starting to look attractive again as it seems the BOE will easily be raising rates at both the September and November meetings.

Canadian CPI

The Canadian dollar rallied after the July inflation rose back the Bank of Canada’s inflation-control target range of 1% to 3%. This was not entirely hot as both core readings remained subdued. This report means that the BOC will remain data-dependent and that the odds of one more rate hike might be growing.

Gas Prices

European natural gas futures are surging as the risk for Australian LNG workers to strike grow. If talks collapse, the world could see about 10% of global LNG exports at risk. Europe has bolstered their inventories, but a hot end to summer could lead to a surge in cooling demand. Inventories are not a concern right now, but if we get further disruptions and if weather trends in the summer and winter lead to many spikes in demand, we could see natural gas surge significantly higher.

Jackson Hole

We are a week away from Jackson Hole and Wall Street is not expecting any major surprises. Fed Chair Powell will remain upbeat regarding the progress with bringing inflation down. July PCE data to be sticky and keep risk of one more hike on the table. Given the US economic resilience backdrop, the Fed will want to keep optionality here, so an end of tightening will not be signaled.

Oil

Crude prices continue to pullback after both disappointing Chinese industrial production data and the German ZEW survey that showed concerns with recovery are elevated. The oil market might remain tight, but most of the headlines are turning bearish for the demand side. Oil’s pullback might need to continue a while longer before buyers emerge.

Gold

Gold prices are falling as real yields continue to rise. Gold could be stuck in the house of pain a little while longer if the bond market selloff does not ease. The 30-year Treasury yield rising above 2% is a big red flag for some traders. We haven’t seen yields on the 30-year at these levels since 2011, which is making non-interest bearing gold less attractive even as China’s property market rattle markets.

Home Depot

Home Depot delivered mostly in-line results, but they were able to hold onto their guidance. Big ticket projects are under pressure, but small projects remain in demand. Share prices rose given the lowered May outlook was reaffirmed and after they set a $15 billion buyback.

Fed’s Kashkari feels good about falling inflation, but it’s still too high

Minneapolis Fed Neel Kashkari remarked at an event today, "Inflation is coming down. We have made progress and good progress. I feel good about that."

But it wasn't all accolades. Highlighting lingering concerns, Kashkari pointedly added, "It's still too high," making it clear that the current inflation rates, though improved, are not yet at Fed's comfort zone.

Kashkari also questioned, "Have we done enough to actually get inflation all the way back down to our 2% target. Or do we have to do more?"

This introspection underscores the broader debate within FOMC: whether the existing measures are adequate or if there's a need for further tightening action.

Canadian Dollar Steady Despite Rise in Inflation

- Canada’s inflation rises to 3.3%

- US retail sales climb 0.7%, core rate soars 1%

The Canadian dollar is showing limited movement on Tuesday. In the North American session, USD/CAD is trading at 1.3477, up 0.13%.

Canada’s inflation jumps

Canada released the July inflation report earlier today. CPI rose 3.3% y/y, up from 2.8% in June and above the consensus estimate of 3.0%. On a monthly basis, CPI was up 0.6% in June, compared to 0.1% in May and higher than the estimate of 0.3%.

The average of two of the Bank of Canada’s core measures came in at 3.65% y/y in June, a drop lower than the 3.7% gain in May. Core CPI, which is considered more reliable than headline CPI, remains uncomfortably high for the Bank of Canada.

The June inflation reading managed to fall within the BoC’s 1%-3% target, for the first time since March 2021. The rise in the July reading is a reminder that the fight against inflation is not over and it will be a challenge for the BoC to keep inflation below 3%.

The Bank of Canada holds its next meeting on September 6th. The BoC has said that its rate decisions will be based on the data, and the rise in July CPI could provide support for a rate hike at that meeting. Reuters reported that the money markets have raised the probability of a 25 basis point hike in September to 31% currently, up from 22% prior to the inflation report release.

Consumer spending remains resilient

In the US, retail sales for July surprised on the upside. Headline retail sales rose 0.7% m/m, above the June reading of 0.3% (upwardly revised from 0.2%). The core rate jumped 1.0%, blowing past the 0.2% gain in June. Both readings beat the consensus estimate of 0.4%. The Fed is widely expected to hold rates in September, but November is less clear-cut, with a 64% chance of a pause, a 32% likelihood of a 25-basis point hike and a 3% chance of a 50-bps increase.

USD/CAD Technical

- There is resistance at 1.3513 and 1.3580

- 1.3434 and 1.3367 are providing support