Sample Category Title

RBNZ Review: Steady as She… Oh Wait!

- OCR remained at 5.5% as Westpac and the market had expected.

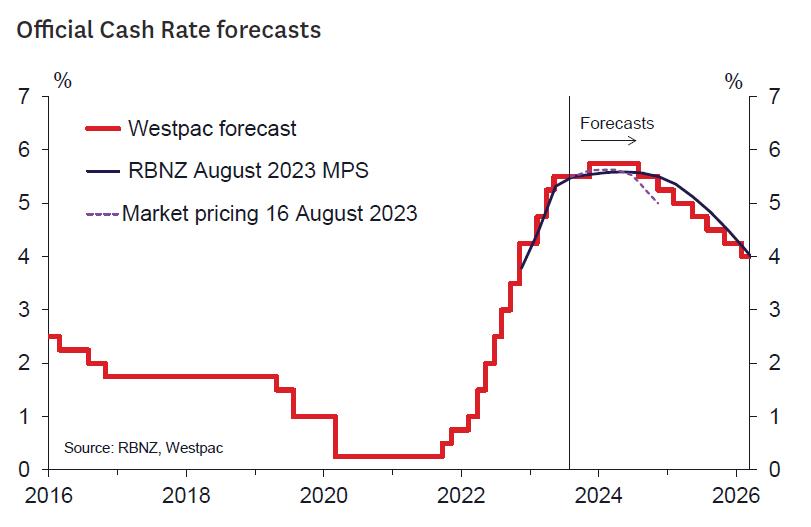

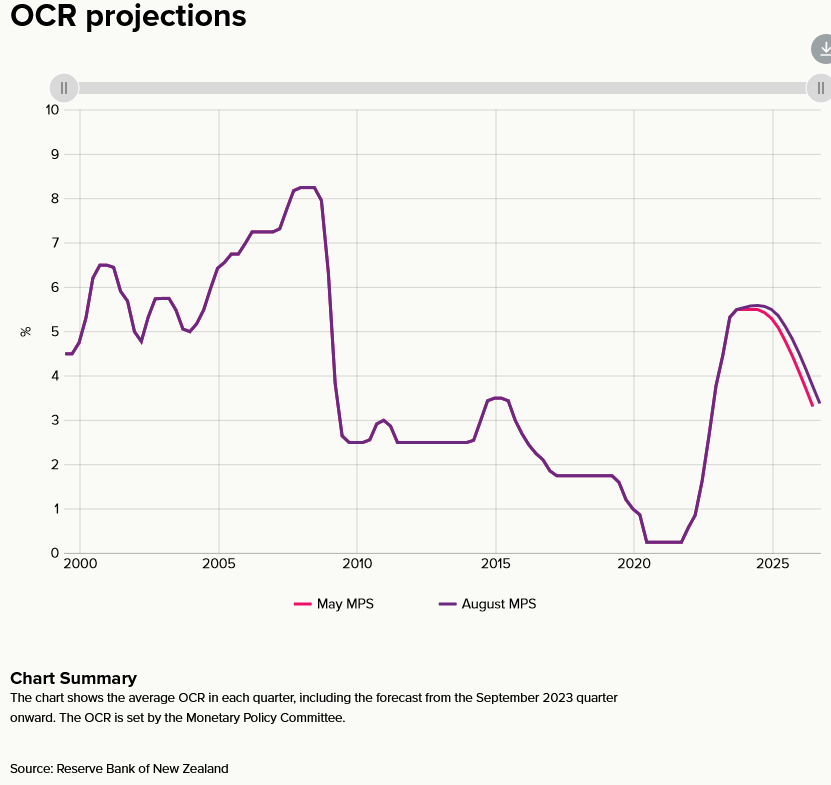

- The RBNZ's forecasts for near term growth have been revised up, and its OCR profile revised higher to 5.6% between December 2023 and June 2024, implying around a 40% chance of a further rate hike to 5.75%.

- The RBNZ has revised up its assumption for the neutral OCR by 25bps to 2.25%, lifting the OCR profile.

- The RBNZ's medium term CPI profile remained unchanged although with higher interest rates. CPI inflation still gets back inside the range September 2024, with risks seen as 'balanced'.

- Westpac retains its call for a 25bps increase in the OCR in November.

What happened?

The RBNZ left the OCR at 5.5% as widely expected. The overall tone of the Statement is a touch more hawkish than in the May Statement. In many respects the RBNZ's view on the balance of risks for inflation and interest rates is converging towards our own. That said, during the press conference, Governor Orr indicated that he remained "very comfortable" with the current OCR setting, suggesting that the MPC still has some ground to travel before they decide to implement the 25-basis point hike in the OCR that we continue to expect in November.

The OCR profile has been revised upwards. To some extent this has been driven by changes in technical assumptions around the longer-run "neutral OCR" which has been revised up by 25bps to 2.25%. This essentially means the RBNZ now sees the currently 5.5% level of the OCR as being slightly less restrictive than it previously thought. As a result, a higher forecast OCR track is now needed to keep forecast inflation heading back to target expeditiously.

Recent developments have also pushed the forecast for the OCR higher in the near term. The RBNZ now recognizes that house prices have bottomed out earlier than expected and that they will rise from here (the RBNZ retains a more conservative view on house prices than Westpac - they see price growth of 3% over 2024 versus our view of an almost 8% increase). The higher June quarter out-turn for non-tradables inflation also played a role, as has an upward revision in near term growth and labour market forecasts. All of this was foreshadowed in recent weeks by our MPS preview and Economic Overview.

The factors pushing up inflation pressures have been balanced by the weaker external outlook. Commodity prices have fallen significantly recently which is weighing on incomes and growth over the forecast horizon.

The risks.

The RBNZ importantly has emphasized there are risks in both directions for the economy, inflation, and the OCR. The RBNZ has now moved to a more data-dependent approach – once again as we foreshadowed in our MPS preview. This is sensible and appropriate given the uncertainties out there. The Bank sees upside risks to growth and inflation in the near-term, with the unemployment rate now forecast to rise more slowly than in May. Looking towards the medium-term, the Bank emphasises downside risks to the growth and inflation outlook from the weaker external outlook, especially as regards China. This is unsurprisingly given recent negative trends in dairy prices. Indeed, following last night's auction, current dairy prices appear about 10% weaker than the Bank's assumed cycle low point. Overall, the RBNZ assessed that "the risks around the inflation projection remain balanced".

The bottom line – higher for longer.

The core message remains the same though. The RBNZ still sees an OCR of around the current level of 5.5% as sufficiently restrictive to bring inflation down over time. The OCR will need to remain at around these levels for longer than previously thought as the first easing comes either at the end of 2024 or early 2025 (compared to the September quarter 2024 in the May Statement).

Our view.

We continue to see a hike in the OCR to 5.75% in the November 2023 Monetary Policy Statement. Key indicators to watch, in order of importance, include:

- the September quarter CPI (where the RBNZ will be hoping to see tangible signs of core inflation measures decelerating – especially in non-tradables inflation),

- the September quarter labour market report (where the RBNZ will be watching the unemployment rate, employment growth, and wages indicators closely)

- business and consumer confidence indicators (to assess the extent that weaker commodity prices and farm incomes will flow through to broader economic growth)

- monthly housing market indicators (to check on the extent to which population growth pressures are leading to increased pricing pressures).

The RBNZ's economic projections.

Turning to the economic projections, following a weaker than expected March quarter, the RBNZ now estimates GDP growth of 0.5% in the June quarter – a sharp upgrade from the 0.2% contraction forecast in the May Statement. From that higher base, the RBNZ forecasts a slightly greater rate of contraction in the economy over the second half of this year. However, following the strong lift in employment reported in the June quarter, the RBNZ expects the unemployment rate to rise more slowly than in the May Statement, posing the risk that wage inflation may slow less quickly than projected previously. Specifically, the RBNZ now forecasts the unemployment rate to rise to 3.8% in the September quarter (previously 4.1%) and 4.4% in the December quarter (previously 4.6%). These revised forecasts address Westpac's previous concern that the RBNZ was overestimating the likely near-term loosening of the labour market.

Beyond this year, the RBNZ's projections point to a gradual pick-up in quarterly GDP growth but to rates that remain below the economy's 'potential' until the first half of 2025. In the detail, starting from a firmer base, the RBNZ has become more pessimistic about the outlook for growth in exports. However, this is balanced by a slightly more upbeat outlook for private consumption and a downward revision to forecast growth in imports. Cumulative GDP growth over 2024 and 2025 is slightly higher than in the May Statement, while projected growth in potential GDP has also been raised slightly. The bottom line is that, on average, activity is expected to track 1.7% below the economy's sustainable capacity, thus applying downward pressure on inflation. This is very similar (just 0.1% less) to what was projected in the May Statement. The unemployment rate is expected to reach a cyclical peak of 5.3% at the end of next year – 0.1% lower than forecast in May.

The RBNZ revised up its inflation forecasts – partly due to higher international oil prices although of more importance was the updated profile for non-tradables inflation. Nontradables inflation has been running hotter than the RBNZ had expected. In addition, measures of core inflation (which track the underlying trends in prices) indicate that price pressures have been easing only gradually two years after the OCR began rising. Consistent with those lingering domestic price pressures, the RBNZ has revised up its near-term forecast for non-tradables inflation.

The RBNZ has analysed the inflationary impact of migration and tentatively concluded that the inflationary impacts will be positive but lower than seen historically. More research is underway.

Looking at inflation two to three years ahead, which is the key focus for the RBNZ when setting monetary policy, the central bank's forecasts for inflation are largely unchanged. However, that's because the RBNZ has revised up its longer-term forecast for the OCR. In other words, the RBNZ now thinks that domestic inflation pressures are stronger than it previously assessed, and accordingly that higher interest rates are needed to get inflation back to target.

At those longer horizons, the RBNZ has also revised up its forecast for the long-run neutral OCR by 25bps. However, the longer term forecast for the actual OCR has been revised up by more than the neutral OCR has been (an additional 10 to 15bps). While that's not a big change, it helps to highlight the RBNZ thinks the risks for inflation have tilted upwards in recent months. Inflation still returns to the 1-3% target range in September 2024.

Reinforcing the stronger outlook for inflation pressures, the RBNZ has revised up its forecast for house prices. While the RBNZ had previously expected house prices to continue falling through the back part of the year, prices have instead flattened off in recent months. The RBNZ now forecasts house prices to rise by around 3% next year, and that will help to support household spending.

EUR/USD Extends Losses While USD/CHF Eyes Upside Break

EUR/USD started a fresh decline below the 1.0000 support. USD/CHF is rising and might aim a move toward the 0.8850 resistance.

Important Takeaways for EUR/USD and USD/CHF Analysis Today

- The Euro struggled to clear the 1.1040 resistance against the US Dollar.

- There is a major bearish trend line forming with resistance near 1.0920 on the hourly chart of EUR/USD at FXOpen.

- USD/CHF is gaining pace above the 0.8745 resistance zone.

- There is a key bullish trend line forming with support near 0.8760 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair failed to clear the 1.1040 resistance. The Euro started a fresh decline below the 1.0000 support against the US Dollar, as mentioned in the previous analysis.

There was a move below the 50-hour simple moving average and 1.0970. The bears were able to push the pair below the 1.0900 pivot level. The pair traded as low as 1.0874 and is currently attempting an upside correction.

There was a move above the 1.0900 level. Immediate resistance on the upside is near the 50-hour simple moving average at 1.0920. There is also a major bearish trend line forming with resistance near 1.0920. The trend line is close to the 23.6% Fib retracement level of the downward move from the1.1065 swing high to the 1.0874 low.

The first major resistance is near the 50% Fib retracement level of the downward move from the1.1065 swing high to the 1.0874 low at 1.0970. An upside break above the 1.0970 level might send the pair toward the 1.1040 resistance. Any more gains might open the doors for a move toward the 1.1070 level.

On the downside, immediate support on the EUR/USD chart is seen near 1.0900. The next major support is near the 1.0875 level. A downside break below the 1.0875 support could send the pair toward the 1.0800 level.

USD/CHF Technical Analysis

On the hourly chart of USD/CHF at FXOpen, the pair started a decent increase from the 0.8700 support. The US Dollar gained climbed above the 0.8745 resistance zone against the Swiss Franc.

A base is formed above 0.8745 and the pair is now showing positive signs. It is trading near the 50% Fib retracement level of the downward move from the 0.8827 swing high to the 0.8744 swing low and above the 50-hour simple moving average.

On the upside, the pair is now facing resistance near 0.8785. The next major resistance is near the 76.4% Fib retracement level of the downward move from the 0.8827 swing high to the 0.8744 swing low at 0.8810.

If there is a clear break above the 0.8810 resistance zone and the RSI climbs above 60, the pair could start another increase. In the stated case, it could test 0.8850.

On the downside, immediate support on the USD/CHF chart is near the 50-hour simple moving average at 0.8775. The first major support is near a key bullish trend line at 0.8760. The next major support is near the 0.8745 level. Any more losses may possibly open the doors for a move toward the 0.8700 level or even 0.8680 in the near term.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

GBP/USD Daily Outlook

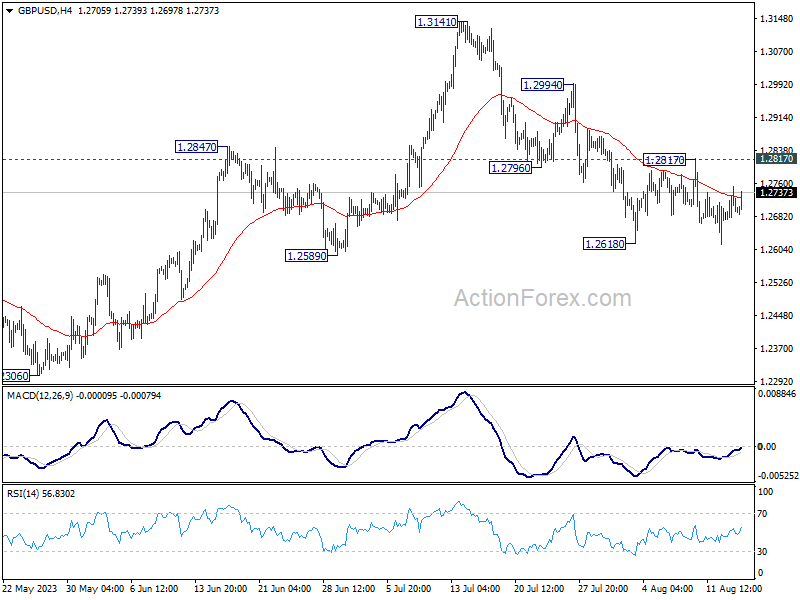

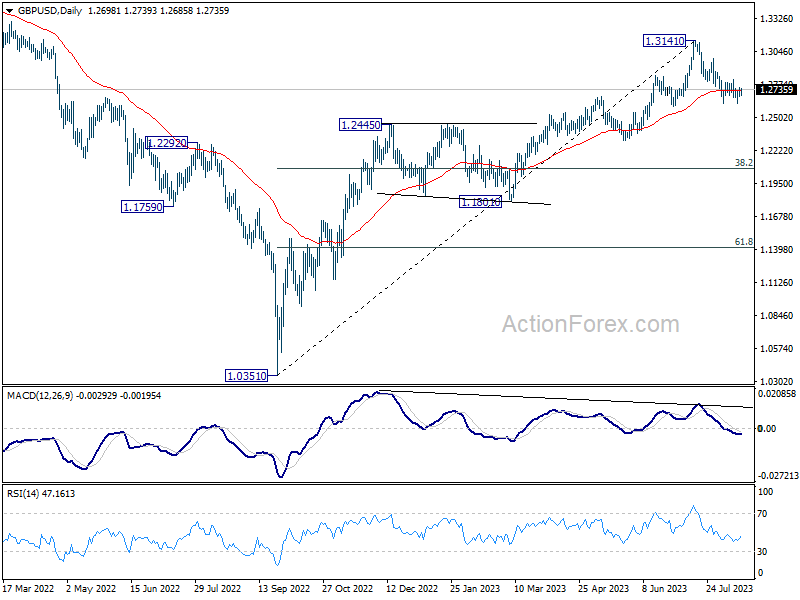

Daily Pivots: (S1) 1.2668; (P) 1.2711; (R1) 1.2746; More...

GBP/USD is staying in established range despite today's recovery. Intraday bias remains neutral for the moment. On the downside, firm break of 1.2618, and sustained trading below 1.2678 resistance turned support will argue that it's already in a larger correction. Deeper decline would then be seen to 1.2306 support next. Nevertheless, break of 1.2817 minor resistance will indicate that the pull back has completed, and turn bias back to the upside for stronger rebound.

In the bigger picture, a medium term top could be in place at 1.3141 already, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.2723) should confirm this case, and bring deeper fall to 38.2% retracement of 1.0351 to 1.3141 at 1.2075, as a correction to up trend from 1.0351 (2022 low). For now, rise will stay mildly on the downside as long as 1.3141 resistance holds, in case of strong rebound.

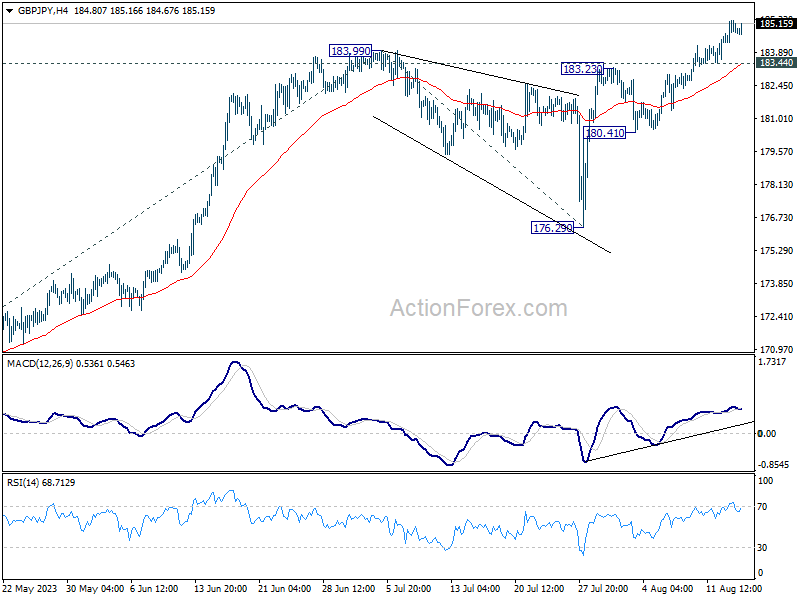

GBP/JPY Daily Outlook

Daily Pivots: (S1) 184.42; (P) 184.88; (R1) 185.40; More...

Intraday bias in GBP/JPY remains on the upside for the moment. Current up trend should extend to 61.8% projection of 158.24 to 183.99 from 176.29 at 192.20. On the downside, below 183.44 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Next target is 195.86 (2015 high). This will now remain the favored case as long as 176.29 support holds, even in case of deeper pull back.

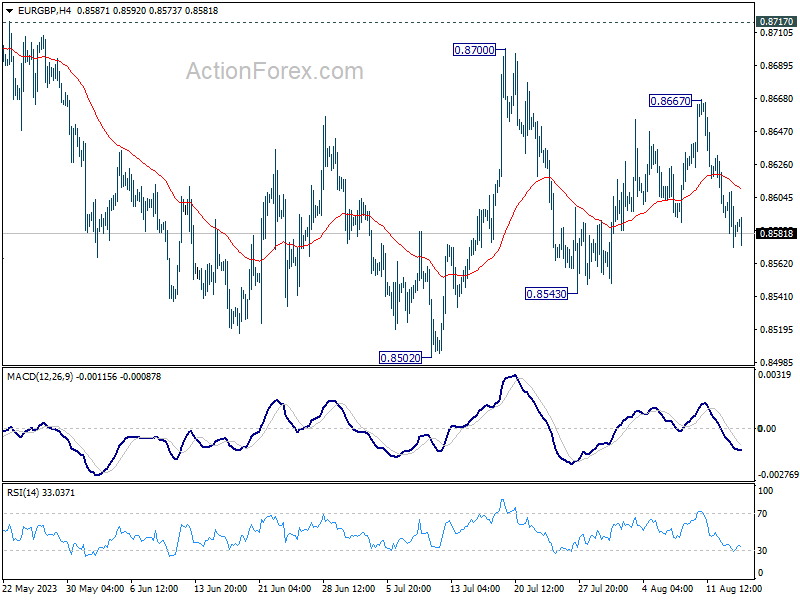

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8569; (P) 0.8589; (R1) 0.8605; More...

EUR/GBP dips mildly mildly today but stays in established range. Outlook is unchanged. On the downside, below 0.8543 will target a test on 0.8502 low. Decisive break there will resume larger decline from 0.8977. On the upside firm break of 0.8717 resistance will suggest larger reversal and target 0.8874 resistance next.

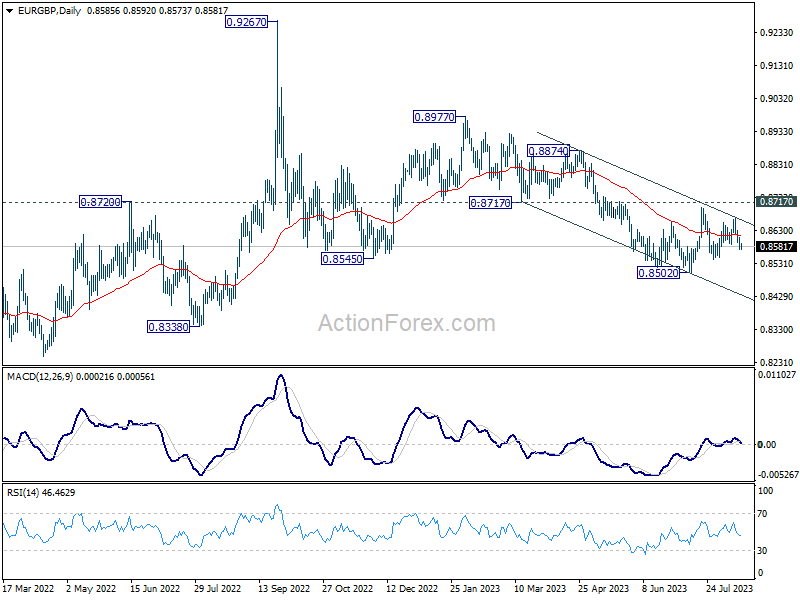

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Firm break of 0.8717 support turned resistance will argue that it has completed with three waves down to 0.8502. Further break of 0.8977 will bring retest of 0.9267 high. Nevertheless, rejection by 0.8717, followed by break of 0.8502 will resume the decline towards 0.8201 (2022 low).

Sterling a Touch Higher after UK CPI, Dollar Stays Resilient

In the wake of UK CPI data, Sterling slightly higher, but lacks clear buying momentum. As BoE had anticipated, headline inflation demonstrated pronounced deceleration. Concurrently, the evident surge in services inflation dovetails seamlessly with the week's unprecedented data on wage growth. Given these dynamics, BoE is primed for another rate hike in the coming month, with indicators suggesting a consistent tightening trajectory. Nonetheless, pinpointing the exact juncture for the peak rate remains a matter of speculation.

Globally, Dollar, although exhibiting a subdued tone today, is firmly positioned as one of the week's frontrunners, second only to the Pound. On the other end of the spectrum, Australian Dollar finds itself grappling with the week's underwhelming performance. This downturn is attributed to an amalgamation of bearish trends emerging from China and a continued dip in Copper prices. On the other hand, New Zealand Dollar is mixed, with help from today's post-RBNZ recovery. In the meantime, Canadian Dollar and Yen are charting the next in line for weaker performances, with Euro and Swiss Franc portraying a mixed picture for the time being.

Technically, WTI crude oil is in notable pull back this week. With D MACD crossed below signal line, a short term top should be in place at 84.91, after hitting 161.8% projection of 63.67 to 74.74 from 66.94 at 84.85. Break of 78.72 support will likely bring deeper pull back through 55 D EMA (now at 77.09) to 74.74 resistance turned support. Such a pronounced dip in WTI might resonate with a broader risk-off sentiment, possibly in tandem with a significant dip in equities. Such a scenario could pave the way for an invigorated US Dollar.

In Asia, Nikkei closed down -1.46%. Hong Kong HSI is down -1.38%. China Shanghai SSE is down -0.64%. Singapore Strait Times is down -0.66%. Japan 10-year JGB yield dropped -0.0094 to 0.622. Overnight, DOW dropped -1.02%. S&P 500 dropped -1.16%. NASDAQ dropped -1.14%. 10-year yield rose 0.037 to 4.221.

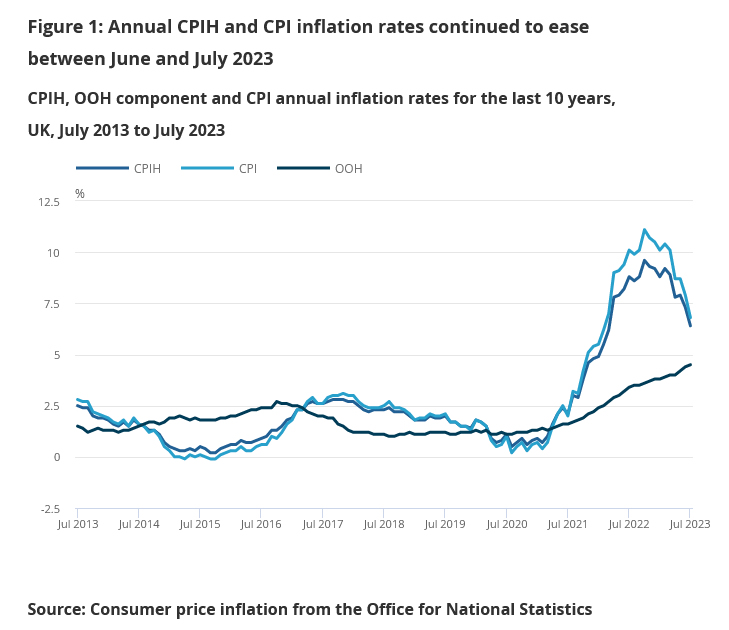

UK CPI slowed to 6.8% in Jul, services inflation hit highest since 1992

July saw a marked deceleration in UK's CPI, falling from 7.9% yoy to 6.8% yoy , precisely in line with market expectations. Core CPI, which strips out variables like energy, food, alcohol, and tobacco, stood unchanged at 6.9% yoy, above the expected 6.8%.

CPI figures pertaining to goods showed a noticeable slowdown, dropping from 8.5% yoy to 6.1% yoy. On the flip side, CPI services ramped up from 7.2% yoy to 7.4% yoy , registering its peak since the staggering 9.5% yoy rate observed in March 1992.

On a month-to-month analysis for July, CPI receded by -0.4%, a figure slightly above than forecasted decline of -0.5%. Core CPI saw a monthly rise of 0.3% mom. While the CPI for goods plunged by -1.7% mom. , services CPI exhibited an increase, registering growth of 1.0% mom. .

Office for National Statistics remarked, "The slowdown in the annual CPI rate into July 2023 was driven by downward contributions to change from 8 of the 12 divisions."

Notably, housing and household services emerged as the primary sectors applying downward pressure. Expanding on this, ONS stated, "Within this division, the downward effect came mainly from gas and electricity."

RBNZ on hold, OCR to stay high for longer

RBNZ has decided to maintain OCR unchanged at 5.50% again, aligning with broad market expectations. Making its stance clear, the bank asserted that the "OCR needs to stay at restrictive levels for the foreseeable future."

Reflecting a neutral stance, the central bank emphasized its confidence in the current monetary policy, "that with interest rates remaining at a restrictive level for some time, consumer price inflation will return to within its target range of 1 to 3% per annum, while supporting maximum sustainable employment."

Adding depth to its economic perspective, "The nominal neutral OCR has increased by 25 basis points to 2.25% within the projections," the Committee noted. They were in consensus that the existing OCR level was contractionary, asserting that it's effectively curbing domestic spending as intended.

Shifting the lens to future projections, the forecasts in the Monetary Policy Statement hint at the OCR potentially reaching a peak of 5.6% in the first quarter of 2024. This marks a slight shift from the earlier prediction of 5.5% in Q3 2023, hinting at the possibility of an additional rate hike. As for subsequent rate cut expectations are now set for the second quarter of 2025, a slight delay from the previously anticipated period between Q4 2024 and Q1 2025.

Australia's Westpac leading index ticks up, but below-par growth set to persist

Australia's Westpac Leading Index figures reveals that growth rate has shown a marginal uptick, moving from -0.67% to -0.60% in July. But alarmingly, this marks the twelfth consecutive month in red, representing the longest stretch of such negative prints in a span of seven years, barring the COVID-affected period.

The subdued, below-par growth momentum witnessed throughout 2023 seems set to persist into the subsequent year. Westpac predicts deceleration in GDP growth to a mere 1% for the current year. Any potential rebound is anticipated to be minimal, with projections indicating a slight rise to 1.4% annually in 2024 – with the bulk of this growth concentrated towards the year-end.

Regarding RBA meeting on September 5, Westpac sets its expectations clear. The institution foresees cash rate remaining stable at 4.10%, denoting the zenith of this current tightening phase.

Referring the recent remarks of RBA Governor before the House of Representatives Standing Committee on Economics, the note emphasized, "Policy is now in a 'calibration' phase with small adjustments still possible if the data starts to show clear risks of a slower return to low inflation."

Nevertheless, given the evident frailty in growth momentum – as underscored by the most recent Leading Index update – coupled with the broader dynamics of price and wage inflation aligning with RBA's forecasts, "the threshold for additional tightening is high and unlikely to be met."

Looking ahead

Eurozone GDP revision and industrial production will be released in European session. Later in the day, housing data from Canada and US will be release. US will also release industrial production, and FOMC minutes.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8569; (P) 0.8589; (R1) 0.8605; More...

EUR/GBP dips mildly mildly today but stays in established range. Outlook is unchanged. On the downside, below 0.8543 will target a test on 0.8502 low. Decisive break there will resume larger decline from 0.8977. On the upside firm break of 0.8717 resistance will suggest larger reversal and target 0.8874 resistance next.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Firm break of 0.8717 support turned resistance will argue that it has completed with three waves down to 0.8502. Further break of 0.8977 will bring retest of 0.9267 high. Nevertheless, rejection by 0.8717, followed by break of 0.8502 will resume the decline towards 0.8201 (2022 low).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Westpac Leading Index M/M Jul | 0.00% | 0.12% | ||

| 02:00 | NZD | RBNZ Interest Rate Decision | 5.50% | 5.50% | 5.50% | |

| 03:00 | NZD | RBNZ Press Conference | ||||

| 06:00 | GBP | CPI M/M Jul | -0.40% | -0.50% | 0.10% | |

| 06:00 | GBP | CPI Y/Y Jul | 6.80% | 6.80% | 7.90% | |

| 06:00 | GBP | Core CPI Y/Y Jul | 6.90% | 6.80% | 6.90% | |

| 06:00 | GBP | RPI M/M Jul | -0.60% | -0.70% | 0.30% | |

| 06:00 | GBP | RPI Y/Y Jul | 9.00% | 9.00% | 10.70% | |

| 06:00 | GBP | PPI Input M/M Jul | -0.40% | 0.00% | -1.30% | |

| 06:00 | GBP | PPI Input Y/Y Jul | -3.30% | -5.10% | -2.70% | -2.90% |

| 06:00 | GBP | PPI Output M/M Jul | 0.10% | -0.40% | -0.30% | -0.20% |

| 06:00 | GBP | PPI Output Y/Y Jul | -0.80% | -1.20% | 0.10% | 0.30% |

| 06:00 | GBP | PPI Core Output M/M Jul | 0.10% | -0.30% | -0.20% | |

| 06:00 | GBP | PPI Core Output Y/Y Jul | 2.30% | 1.60% | 3.00% | 3.10% |

| 09:00 | EUR | Eurozone GDP Q/Q Q2 P | 0.30% | 0.30% | ||

| 09:00 | EUR | Employment Change Q/Q Q2 P | 0.40% | 0.60% | ||

| 09:00 | EUR | Eurozone Industrial Production M/M Jun | 0.10% | 0.20% | ||

| 12:15 | CAD | Housing Starts Y/Y Jul | 260K | 281.4K | ||

| 12:30 | CAD | Wholesale Sales M/M Jun | -4.40% | 3.50% | ||

| 12:30 | USD | Housing Starts Jul | 1.45M | 1.43M | ||

| 12:30 | USD | Building Permits Jul | 1.47M | 1.44M | ||

| 13:15 | USD | Industrial Production M/M Jul | 0.30% | -0.50% | ||

| 13:15 | USD | Capacity Utilization Jul | 79.00% | 78.90% | ||

| 14:30 | USD | Crude Oil Inventories | -2.4M | 5.9M | ||

| 18:00 | USD | FOMC Minutes |

Resilient US Retail Sales Fuel Inflation Expectations, Fed Hawks

The Americans continue spending and that’s bad news for the entire world. Announced yesterday the July retail sales data came in better-than-expected in the US. Sales grew 0.7% on a monthly basis and more than 3% on a yearly basis - the biggest figure since January, when sales soared by 3% as well. Amazon’s Prime day apparently helped boost online sales, while demand for bigger items including furniture and auto parts declined. But all in all, the American consumer spent 3% more compared to a year ago, Home Depot reported small earnings beat yesterday and its CEO confirmed that ‘fears of a recession have largely subsided, and the consumer is generally healthy... while adding that ‘uncertainties remain’. Uncertainties remain, yes, but the resilience of the US consumer spending sapped investor sentiment by fueling inflation expectations and Federal Reserve (Fed) hawks, yet again. The US 2-year yield spiked above the 5% mark, but bounced lower, certainly helped by a big drop in Empire State manufacturing in August, the 10-year yield flirted with 4.30%, while major stock indices fell. The S&P500 closed below the 50-DMA, which stands at 4446, Nasdaq 100 remained offered below its own 50-DMA, at 15175, while Russell 200 slipped below the 50-DMA.

In the FX, the strength of the US consumer spending is reflected as a stronger US dollar across the board. The US dollar index remains bid, while Cable bulls resist to the bears around the 1.27, and above the 200-DMA, which stands near 1.2620, as the data released yesterday showed that wages in Britain accelerated at a record pace. Happily, this morning’s inflation data poured some cold water on the fire, as the CPI fell from 7.9% to 6.8% in July, as expected, yet core inflation remained steady at 6.9%, while the core PPI came in higher than expected. On the food front, grocery prices also fell more than 2 percentage points to 12.7%. But 12.7% is still a very high number. As a result, odds for a 50bp hike at the Bank of England’s (BoE) September meeting is given a 1 over 3 chance, the 2-year gilt yield is back above 5%, and looks like it’s there to stay, as the peak BoE rate is seen at 6%.

Across the Channel, the 10-year bund yield is also pushing higher near a decade high, and all eyes are on the European GDP and industrial production data this morning. The European economy is weakening due to the rising rates, tightening credit conditions and high energy prices, but the fact that the labour market remains tight in Europe as well remains a major concern for inflation expectations for the European Central Bank (ECB), which will let the economy sink further if it doesn’t take further control over inflation. Therefore, the EURUSD will certainly react negatively to a weak European data set today, and the pair could re-test the minor 23.6% Fibonacci retracement level, at 1.0870, but figures more or less in line with expectations should not change the ECB’s hawkish tilt. The problem is, there is nothing the ECB could do - other than restricting financial conditions - regarding the energy and gas prices – which move parallel to completely external factors like the Ukrainian war and labour strikes in Australia. In this sense, the Dutch TTF futures were again up by 12% yesterday, while US crude tanked near the $80pb level, pressured lower by 1. the surprise Chinese rate cut’s inability to spark interest in risk assets, 2. news that China’s imports of sanctioned Iranian hit a record high of 1.5mbpd this month - that oil trading at around $10 discount to Brent and 3. the latest data from the API hinting at an almost 7mio barrel decline in US crude inventories last week. The more official EIA data is due today, and the consensus is a 2.4 mio barrel fall. US crude could well slip below the $80pb on slow growth concerns, but Saudis will fight to keep the price above $80pb in the medium run.

Back to the inflation talk, the recent rise in energy and food prices is concerning for the euro area’s inflation in the next readings. Therefore, the falling inflation trend remains in jeopardy, as the discussion of an ECB pause on rate increases.

The Reserve Bank of New Zealand (RBNZ) held its cash rate unchanged for the 2nd consecutive month but warned that there is a risk that activity and inflation measures do not slow as much as expected, and that they won’t be cutting rates until the Q1 of 2025. The kiwi extended losses against the greenback, but the selloff remained contained.

Due today, the FOMC minutes will likely show that the Fed officials remain cautious despite the latest fall in inflation numbers, for the same reasons: rising energy and food prices that are sometimes driven by geopolitical events and that the Fed could only watch and adopt. The Fed is expected to hold fire on its rates in the September meeting, but nothing is less guaranteed than the end of the tightening cycle before the year end.

Market Sentiment Remains Cautious

Market movers today

Following up on yesterday's inflation data from Sweden which came in well in line with expectations, this morning the Prospera inflation expectations survey is due.

In the UK, consensus expects inflation to moderate from 7.9% y/y in June to 6.7% in July.

In the US, we get housing data and industrial production for July, but main focus will be on the FOMC minutes released this evening.

There, the focus will naturally be on how the participants saw the balance of risks regarding the potential future rate hikes.

The 60 second overview

US: July retail sales data surprised to the upside, as nominal sales rose by 0.7% m/m (consensus 0.4%) and control group sales (excl. cars, gasoline, food services and building materials) were up by 1.0% m/m (consensus 0.5%). Amazon Prime Day in mid-July likely contributed to the pick-up, as non-store sales rose by 1.9% m/m, while demand for 'big ticket' items such as cars, furniture and electronics declined. Overall, this could reflect still resilient but slightly more cautious consumer demand. On the leading data front, NY Fed's Empire manufacturing survey and NAHB housing market index declined after strong readings earlier in summer. While the former has been very volatile over the past year, it is among the first manufacturing indicators released for August. Nevertheless, in the evening, the Fed's Kashkari was not ready to close the door for further rates hikes, even if he did caution that there 'could be more slowdown still in the pipeline'. We stick to our view that the Fed is already done hiking for now.

China: Following the latest string of weak macro releases, data published overnight showed that Chinese housing prices had declined by 0.2% m/m (-0.1% y/y) in July. Housing sales volumes have remained low this year, in line with broader economic activity, and despite the central government's efforts to stimulate the economy. Catch up with our latest thoughts on China in China holiday wrap-up - part 3 - Risks of a financial crisis resurface, 14 August.

RBNZ: The Reserve Bank of New Zealand kept the Official Cash Rate unchanged at 5.50% in its meeting overnight, in line with market expectations. New Zealand's core inflation pressures moderated in the latest Q2 reading, and yesterday's Q3 households' expectation survey showed a clear downtick in 1-2 year inflation expectations. In line with earlier communication, RBNZ continued to signal that rates would be maintained at the current level for now, although the rate path was adjusted slightly higher. The updated path now points towards a slight risk of another hike, and a later turn towards cutting rates (early 2025, compared to late 2024), which supported NZD/USD modestly overnight.

Equities: Chinese growth worries lingered into the session and overshadowed strong US retail sales data. Equities were pulled -1% lower in Europe and US in a risk-off session. All sectors were lower but value cyclicals suffered the most; such as banks, materials or energy. The latter with a clear connection to China worries. The underperformance of banks related to cautious comments from Fitch on the sector's credit rating. Little distinction between small caps or large caps, value or growth. VIX rose to 16.5 which is a low level but the highest obtained since summer. US futures are unchanged this morning.

FI: Global yields rose during most of yesterday's session, though some of the move was reversed in the afternoon. Yields promptly surged following the release of the stronger-than-expected US retail sales figures for July, briefly pushing the 2Y US treasury yield above 5%. However, the move quickly reversed without a clear trigger, probably partly explained by some short covering activity in markets. The 10Y US Treasury yield ended up by 2bp, while the 10Y German yield rose 4bp throughout the day. In both markets, the 2s10s curve bear steepened throughout the day.

FX: Scandies remained under pressure yesterday on the back of weak global risk sentiment. USD was about unchanged vis-à-vis majors following stronger-than expected US retail sales. The sell-off in CNH continues to grab attention. USD/CNH rose above the 7.30 yesterday after PBOC cut rates.

Credit: The general risk-off tone we have seen in August continued yesterday with Xover closing at the widest level for the month so far, being out some 6.7bp to 411bp. ITraxx main widened 1.5bp to 71.7bp. In spite of this, the Nordic primary markets are showing signs of awakening post the summer lull with deals announced from both Wallenius Wilhelmsen, Sparebanken Sogn & Fjordane and Sparebanken Øst.

Nordic macro

Sweden: In Sweden, we get the monthly Prospera inflation expectations survey at 8.00 CET. This is the smaller survey where only money market participants respond, but is still important input for the Riksbank. The trend over the recent months has been a steady decline for the 1y horizon (CPIF 4.1% in July, down from a peak of 5.6% in Sep 2022) while the 2y and 5y horizons have remained more stable closer to 2% (2y 2.4% and 5y 2.2% in July). We would expect a similar pattern in this print, with the 1y horizon dropping further while 2y and 5y remain anchored close to the 2% target.

UK CPI slowed to 6.8% in Jul, services inflation hit highest since 1992

July saw a marked deceleration in UK's CPI, falling from 7.9% yoy to 6.8% yoy , precisely in line with market expectations. Core CPI, which strips out variables like energy, food, alcohol, and tobacco, stood unchanged at 6.9% yoy, above the expected 6.8%.

CPI figures pertaining to goods showed a noticeable slowdown, dropping from 8.5% yoy to 6.1% yoy. On the flip side, CPI services ramped up from 7.2% yoy to 7.4% yoy , registering its peak since the staggering 9.5% yoy rate observed in March 1992.

On a month-to-month analysis for July, CPI receded by -0.4%, a figure slightly above than forecasted decline of -0.5%. Core CPI saw a monthly rise of 0.3% mom. While the CPI for goods plunged by -1.7% mom. , services CPI exhibited an increase, registering growth of 1.0% mom. .

Office for National Statistics remarked, "The slowdown in the annual CPI rate into July 2023 was driven by downward contributions to change from 8 of the 12 divisions."

Notably, housing and household services emerged as the primary sectors applying downward pressure. Expanding on this, ONS stated, "Within this division, the downward effect came mainly from gas and electricity."

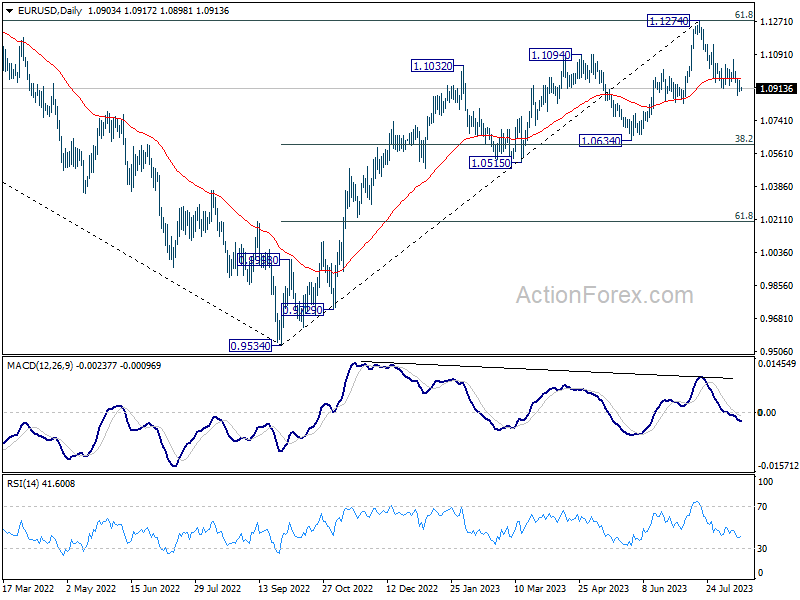

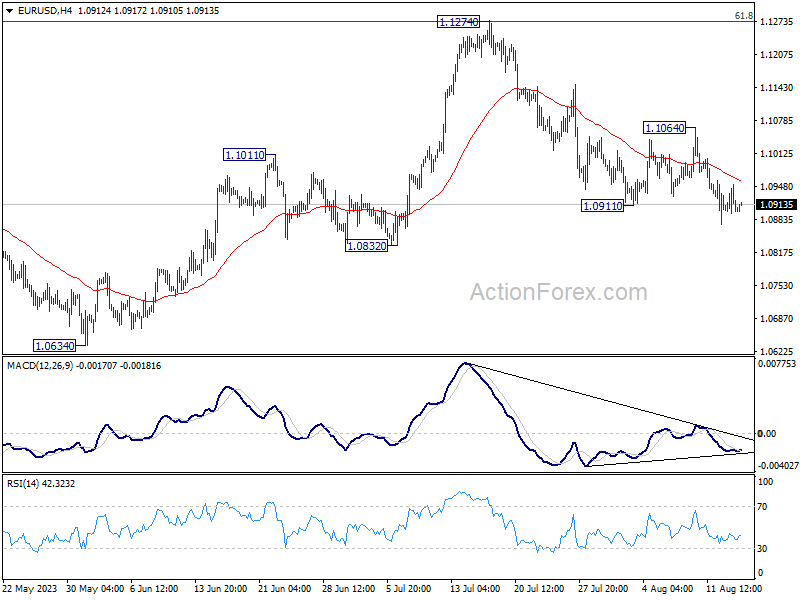

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0884; (P) 1.0919; (R1) 1.0939; More...

Intraday bias in EUR/USD stays on the downside for 1.0832 support. Decisive break there will extend the decline from 1.1274 to 1.0609/34 cluster support. On the upside, break of 1.1064 resistance is needed to indicate completion of the fall. Otherwise, outlook will stay cautiously bearish in case of recovery.

In the bigger picture, a medium term top could be formed at 1.1274, after failing to break through 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 decisively, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.0966) will bring deeper correction to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to set the range for consolidation.