Sample Category Title

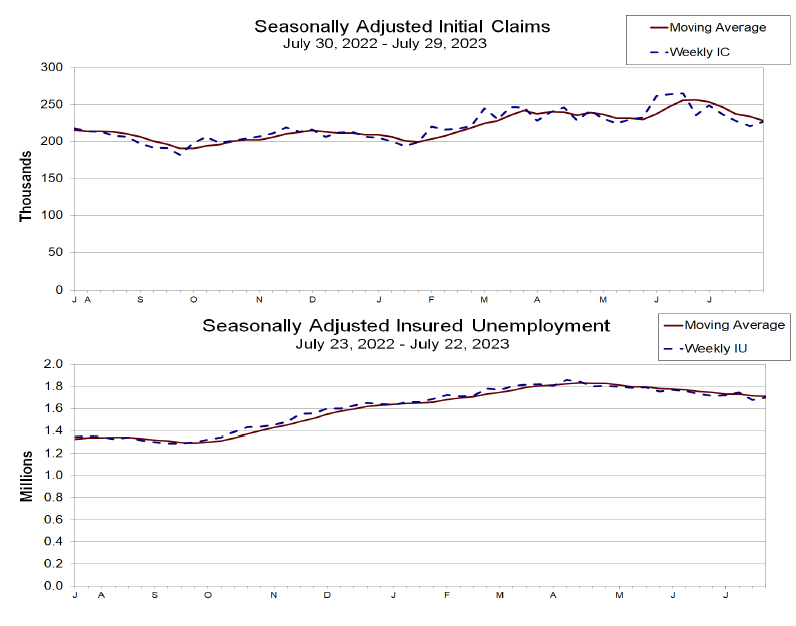

US initial jobless claims rose 6k to 227k

US initial jobless claims rose 6k to 227k in the week ending July 29, above expectation of 223k. Four-week moving average of initial claims dropped -5.5k to 228k.

Continuing claims rose 21k to 1700k in the week ending July 22. Four-week moving average of continuing claims dropped -4.5k to 1712k.

BoE hikes 25bps, softens hawkish bias slightly

BoE raises Bank rate by 25bps to 5.25% today. Two members, Jonathan Haskel and Catherine Mann voted for 50bps hike. Swati Dhingra voted for no change again. Six other MPC members vote for the decision.

Hawkish bias was somewhat softened slightly, as the language that "the MPC will adjust Bank Rate as necessary" was dropped. Nevertheless, the central bank maintained that "If there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required."

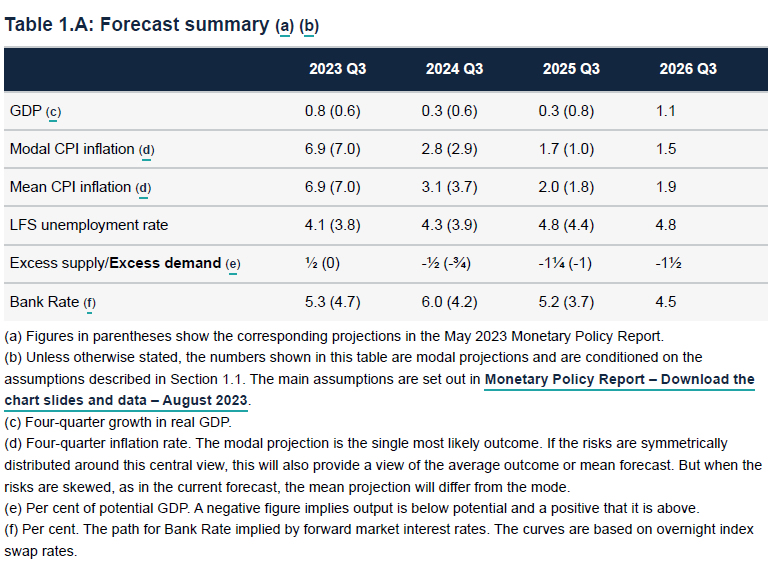

In the new economic forecast, modal CPI inflation was downgraded slightly from 7.0% to 6.9% in 2023 Q3, and from 2.9% to 2.8% in 2024 Q4. CPI forecast was upgraded from 1.0% to 1.7% in 2025 Q3.

(BOE) Bank Rate increased to 5.25%

Monetary Policy Summary, August 2023

The Bank of England's Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 2 August 2023, the MPC voted by a majority of 6–3 to increase Bank Rate by 0.25 percentage points, to 5.25%. Two members preferred to increase Bank Rate by 0.5 percentage points, to 5.5%, and one member preferred to maintain Bank Rate at 5%.

The Committee's updated projections for activity and inflation are set out in the accompanying August Monetary Policy Report. These are conditioned on a market-implied path for Bank Rate that rises to a peak of just over 6% and averages just under 5½% over the three-year forecast period, compared with an average of just over 4% for the equivalent period at the time of the May Report. The sterling effective exchange rate is around 4% higher than in the May Report.

Underlying quarterly GDP growth has been around 0.2% during the first half of this year. Bank staff expect a similar growth rate in the near term, reflecting more resilient household income and retail sales volumes, and most business surveys over recent months. Some more recent indicators show signs of weakening, however, including the July S&P Global/CIPS UK composite PMI.

The labour market remains tight but there are some indications that it is loosening. The LFS unemployment rate rose to 4.0% in the three months to May, somewhat higher than expected in the May Report, and the vacancies to unemployment ratio has continued to fall, although the latter still remains above historical averages.

Annual private sector regular pay growth increased to 7.7% in the three months to May, materially above expectations at the time of the May Report, and three-month on three-month growth in this measure of pay has picked up further. Earnings growth is nevertheless expected to decline in coming quarters, to around 6% by the end of this year, although there is uncertainty around this near-term outlook.

Twelve-month CPI inflation fell from 8.7% in May to 7.9% in June, lower than expected at the time of the Committee's previous meeting. Within this, core goods and services CPI inflation were both lower than expected, although the downside news in the latter, which is more likely to be informative about persistent inflationary pressures, was much smaller. Compared to the May Report projections, June CPI inflation was in line with expectations.

CPI inflation remains well above the 2% target. It is expected to fall significantly further, to around 5% by the end of the year, accounted for by lower energy, and to a lesser degree, food and core goods price inflation. Services price inflation, however, is projected to remain elevated at close to its current rate in the near term.

In the MPC's August most likely, or modal, projection conditioned on market interest rates, CPI inflation returns to the 2% target by 2025 Q2. It then falls below the target in the medium term, as an increasing degree of economic slack reduces domestic inflationary pressures, alongside declining external cost pressures. The Committee has decided in this forecast to bring some of the upside risks to inflation from persistence into its modal projection, pushing up on this inflation projection in the medium term relative to the May Report.

The Committee continues to judge that risks around the modal inflation forecast are skewed to the upside, albeit by less than in May, reflecting the possibility that the second-round effects of external cost shocks on inflation in wages and domestic prices take longer to unwind than they did to emerge. Mean CPI inflation, which incorporates these risks, is 2.0% and 1.9% at the two and three-year horizons respectively.

The MPC's remit is clear that the inflation target applies at all times, reflecting the primacy of price stability in the UK monetary policy framework. The framework recognises that there will be occasions when inflation will depart from the target as a result of shocks and disturbances. Monetary policy will ensure that CPI inflation returns to the 2% target sustainably in the medium term.

Recent data outturns have been mixed. However, some key indicators, notably wage growth, suggest that some of the risks from more persistent inflationary pressures may have begun to crystallise. At this meeting, the Committee voted to increase Bank Rate by 0.25 percentage points, to 5.25%.

Given the significant increase in Bank Rate since the start of this tightening cycle, the current monetary policy stance is restrictive. The MPC will continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including the tightness of labour market conditions and the behaviour of wage growth and services price inflation. If there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required. The MPC will ensure that Bank Rate is sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with its remit.

Minutes of the Monetary Policy Committee meeting ending on 2 August 2023

1: Before turning to its immediate policy decision, the Committee discussed: the international economy; monetary and financial conditions; demand and output; and supply, costs and prices. The latest data on these topics were set out in the accompanying August 2023 Monetary Policy Report.

2: The Committee discussed how inflation was evolving in other advanced economies, including in the euro area and the United States. Headline consumer price inflation had decreased significantly in these economies as commodity prices and energy prices had fallen back, and supply chain bottlenecks had dissipated. Core inflation had already peaked in the United States and appeared to be peaking in the euro area. Consumer goods price inflation was declining but services price inflation had remained strong. Several central banks had tightened monetary policy further and had noted that policy was dampening economic activity.

3: While UK-weighted global growth had proven resilient, some slowing was evident. For example, interest-sensitive components of demand such as housing investment in the United States, and housing and business investment in the euro area, had shown signs of weakness. Consumer spending, at least in the United States, had been more resilient, supported by the build-up of savings during the pandemic and the robustness of the labour market.

4: Advanced-economy labour markets generally remained tight, although the vacancies to unemployment ratio and wage growth in the United States had both started to fall. Wage growth remained strong in the euro area. It remained to be seen how quickly the more persistent components of inflation would fall back across economies, and there was a risk that underlying inflationary pressures could continue to persist even as headline measures fell towards their targets.

5: Regarding the latest developments in monetary and financial conditions, the Committee discussed evidence that interest rates in financial markets had been more sensitive to economic data outturns, particularly in the United Kingdom, than had been usual over the past decade. Market participants appeared to have placed more weight than usual on data outturns as leading indicators of inflation persistence. In the United Kingdom, respondents to the Bank's Market Participants Survey had continued to cite the evolution of wage growth, labour market tightness and services price inflation as the most important indicators when forming their expectations for the evolution of UK monetary policy, in line with the MPC's recent communications. Nevertheless, some of these series could be volatile from month to month.

6: The Committee discussed the near-term outlook for UK economic activity. Bank staff expected underlying quarterly GDP growth of 0.2% in 2023 Q2 and Q3, consistent with expectations at the time of the May Report. There had been continued resilience in household spending, supported by strength in both labour market activity and nominal wage growth, and consistent with a number of business surveys over recent months.

7: Set against that, the Committee noted that July indicators had been more mixed. There had been a decline in the flash S&P Global/CIPS UK composite PMI, which could be an early sign of less resilient growth, and lower consumer confidence. A greater number of contacts of the Bank's Agents had reported a slowing in the outlook for activity in the most recent period. Recent increases in market interest rates, and the subsequent media coverage of increasing mortgage costs, could have also contributed to the movements in these indicators.

8: The Committee discussed the balance in the economic outlook between the impact of higher rates weighing on consumer spending and business investment, against the upside impact on incomes from subsiding energy and food prices. Taken together, these factors suggested modestly positive underlying output growth for the second half of the year.

9: The Committee discussed recent news on indicators of UK inflation persistence. There were some signs that the labour market was loosening, although it remained tight in absolute terms. The LFS unemployment rate had risen to 4.0% in the three months to May, the vacancies to unemployment ratio had continued to decline, and recruitment difficulties appeared to be easing somewhat. However, annual private sector regular pay growth had increased further in May, and was materially stronger than had been expected in the May Report. Three-month on three-month growth in this measure of pay had picked up further.

10: Recent outturns in pay growth appeared to have been stronger than a standard model, based on productivity, short-term inflation expectations and a measure of economic slack, would have predicted. This could indicate greater second-round effects from the rise in inflation on wage growth after the terms of trade shock that had affected the economy. This suggested that the medium-term equilibrium rate of unemployment was likely to be higher. Wage growth was expected to remain strong in the near term, with the risk that there could be further upside surprises. Set against that, developments in some forward-looking indicators, such as the KPMG/REC UK Report on Jobs, implied that wage growth could slow more sharply than anticipated in the second half of 2023, although that survey's relationship with official earnings growth appeared to have weakened recently.

11: Twelve-month CPI inflation had eased to 7.9% in June, in line with the projection in the May Report, and reflecting a falling contribution from energy and, to a lesser extent, food prices. However, both core goods and services CPI inflation had been stronger than expected at the time of the May Report. Elevated goods price inflation continued to be broad-based across products, but slowing producer price inflation suggested that it could ease significantly towards the end of 2023. Services CPI inflation was projected to remain elevated in the near term. The MPC noted that its strength was likely to reflect resilience in demand, the strength of nominal pay growth and, to some extent, non-labour input costs, although some of the upside surprise had reflected components of services prices in which more idiosyncratic factors were likely to be at play.

The immediate policy decision

12: The MPC sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment.

13: The Committee discussed the evolution of key economic indicators since its previous meeting and the degree to which they had shown continued resilience. Underlying quarterly GDP growth had been around 0.2% during the first half of this year. Bank staff expected a similar growth rate in the near term, reflecting more resilient household income and retail sales volumes, and most business surveys over recent months. Some more recent indicators had shown signs of weakening, however, including the July S&P Global/CIPS UK composite PMI.

14: The labour market remained tight, but there were some indications that it was loosening. The LFS unemployment rate had risen to 4.0% in the three months to May and the vacancies to unemployment ratio had continued to fall, although the latter still remained above historical averages.

15: Annual private sector regular pay growth had increased to 7.7% in the three months to May, and three-month on three-month growth in this measure of pay had picked up further. Earnings growth was nevertheless expected to decline in coming quarters, to around 6% by the end of this year, although there was uncertainty around this near-term outlook.

16: Twelve-month CPI inflation had fallen from 8.7% in May to 7.9% in June, lower than expected at the time of the Committee's previous meeting. Within this, core goods and services CPI inflation had both been lower than expected, although the downside news in the latter, which was more likely to be informative about persistent inflationary pressures, had been much smaller.

17: As set out in the accompanying August Monetary Policy Report, CPI inflation was expected to fall significantly further, to around 5% by the end of the year, accounted for by lower energy, and to a lesser degree, food and core goods price inflation. Services price inflation, however, was projected to remain elevated at close to its current rate in the near term.

18: Past increases in Bank Rate, and the higher path of market interest rates on which the August Report forecast was conditioned, were expected to increasingly weigh on UK activity and inflation in coming quarters. Relative to the May projection, quarterly GDP growth was expected to be weaker throughout much of the forecast period, particularly during 2024 and at the beginning of 2025. An increasing degree of economic slack was expected to emerge after the middle of next year and the unemployment rate was projected to rise to just under 5% by 2026 Q3. Both aggregate spare capacity and unemployment increased by somewhat more in the Committee's latest projections than in the May Report, reflecting the weaker path of GDP.

19: In the MPC's August most likely, or modal, projection conditioned on market interest rates, CPI inflation returned to the 2% target by 2025 Q2. It then fell below the target in the medium term, as an increasing degree of economic slack reduced domestic inflationary pressures, alongside declining external cost pressures. The Committee had decided in this forecast to bring some of the upside risks to inflation from persistence into its modal projection, pushing up on this inflation projection in the medium term relative to the May Report.

20: The Committee continued to judge that the risks around the modal inflation forecast were skewed to the upside, albeit by less than in May, reflecting the possibility that the second-round effects of external cost shocks on inflation in wages and domestic prices might take longer to unwind than they did to emerge. Mean CPI inflation, which incorporated these risks, was 2.0% and 1.9% at the two and three-year horizons respectively.

21: The MPC noted that the significant increases in Bank Rate since December 2021, and the move up across the yield curve as a whole over the same period, had tightened the overall stance of monetary policy, restricting demand relative to supply. These effects were likely to continue to build over coming quarters, as was shown in the MPC's August modal and mean projections.

22: The MPC's remit was clear that the inflation target applied at all times, reflecting the primacy of price stability in the UK monetary policy framework. The framework recognised that there would be occasions when inflation would depart from the target as a result of shocks and disturbances. Monetary policy would ensure that CPI inflation returned to the 2% target sustainably in the medium term.

23: Monetary policy was also acting to ensure that longer-term inflation expectations were anchored at the 2% target. Most indicators of household and corporate inflation expectations had tended to decline since the MPC's previous meeting, while medium-term inflation compensation measures in financial markets had risen slightly and had remained above their long-term averages.

24: Six members judged that a 0.25 percentage point increase in Bank Rate, to 5.25%, was warranted at this meeting. Recent data outturns had been mixed. However, some key indicators, notably wage growth, had surprised significantly on the upside. This could indicate that the medium-term equilibrium rate of unemployment had risen, and that some of the risks of greater persistence in broader domestic inflationary pressures had crystallised. Set against that, the unemployment rate had increased a little and the vacancies to unemployment ratio had decreased further since the previous MPC meeting. The most recent indicators of slowing activity needed to be weighed against the surprising resilience of activity over a number of quarters, and it was too early to conclude that the economy was at or very close to a significant turning point. Although the monetary stance was weighing on economic activity, a 0.25 percentage point increase in Bank Rate at this meeting was necessary to address the risks from greater inflation persistence.

25: Two members judged that a 0.5 percentage point increase in Bank Rate, to 5.5%, was warranted at this meeting. For these members, it was important to lean more actively against inflation persistence, which, as described in the August Report, successive forecasts had under-predicted. These members noted the continued tightness in the labour market: while the vacancies to unemployment ratio was falling, it was still well above long-run average levels. Further, high-frequency private sector wage growth measures had continued to trend upwards, consistent with the possibility that the equilibrium unemployment rate had risen. Key metrics including both core and services CPI inflation had continued to remain high. For these members, a forceful increase in Bank Rate at this meeting would help to bring inflation back to the 2% target sustainably in the medium term, and to reduce the risks of a more costly tightening later.

26: One member preferred to leave Bank Rate unchanged at 5% at this meeting. As the policy stance had become increasingly restrictive, there was no longer a strong case for further tightening on risk management grounds. Instead, the risks of overtightening had continued to build, increasing the likelihood of output losses and volatility that would require sharper reversals of policy. Lags in the effects of monetary policy meant that sizeable impacts from past and recent rate increases were still to come through, particularly from cumulative impacts on housing costs. Recent news in components of consumer and producer price inflation strongly indicated a downward trajectory for CPI inflation. Wage inflation had been strongest in business services, while real wages had fallen in most other industries, covering three-quarters of all employees. Given the restrictive policy stance, pay growth was likely to slow as inflation in salient items eased over this year and as the labour market continued to loosen further.

27: Given the significant increase in Bank Rate since the start of this tightening cycle, the current monetary policy stance was restrictive. The MPC would continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including the tightness of labour market conditions and the behaviour of wage growth and services price inflation. If there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required. The MPC would ensure that Bank Rate was sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with its remit.

28: The Chair invited the Committee to vote on the proposition that:

- Bank Rate should be increased by 0.25 percentage points, to 5.25%.

29: Six members (Andrew Bailey, Ben Broadbent, Jon Cunliffe, Megan Greene, Huw Pill and Dave Ramsden) voted in favour of the proposition. Three members voted against the proposition. Two members (Jonathan Haskel and Catherine L Mann) preferred to increase Bank Rate by 0.5 percentage points, to 5.5%. Swati Dhingra preferred to maintain Bank Rate at 5%.

Operational considerations

30: On 2 August 2023, the total stock of assets held for monetary policy purposes was £786 billion, comprising £785 billion of UK government bond purchases and £0.8 billion of sterling non‐financial investment‐grade corporate bond purchases.

31: As discussed in Box A in the August Monetary Policy Report, the Committee would vote on the target for gilt stock reduction over the 12-month period from October 2023 to September 2024 at its September 2023 meeting.

32: The following members of the Committee were present:

- Andrew Bailey, Chair

- Ben Broadbent

- Jon Cunliffe

- Swati Dhingra

- Megan Greene

- Jonathan Haskel

- Catherine L Mann

- Huw Pill

- Dave Ramsden

Sam Beckett was present as the Treasury representative.

33: As permitted under the Bank of England Act 1998, as amended by the Bank of England and Financial Services Act 2016, David Roberts was also present on 26 and 28 July, as an observer for the purpose of exercising oversight functions in his role as a member of the Bank's Court of Directors.

ECB’s Panetta advocates for persistence over aggressiveness in monetary policy approach

ECB Executive Board member Fabio Panetta delivered a speech today, emphasizing the importance of "persistence" over "level" in executing the bank's monetary policy given the present economic context.

Panetta stated, "In the current context where policy rates are around the level necessary to deliver medium-term price stability, I will argue that monetary policy may operate not just by increasing rates but also by keeping the prevailing level of policy rates for longer. In other words, persistence matters as much as level."

The ECB official highlighted two primary approaches to the bank's disinflationary monetary policy: the 'level' approach, which involves raising the policy rate beyond its current position, risking a potential need for faster and earlier cuts, and the 'persistence' approach, which advocates for maintaining the policy rates at their prevailing level for an extended duration.

"Emphasizing persistence may be particularly valuable in the current situation," said Panetta, "where the policy rate is around the level necessary to deliver medium-term price stability, the risk of a de-anchoring of inflation expectations is low, inflation risks are balanced, and economic activity is weak."

He warned against the pitfalls of an aggressive rate hike strategy, stating that it "might amplify the risk associated with overtightening, which could subsequently require rates to be cut hastily in a deteriorating economic environment."

By contrast, Panetta argued, the 'persistence' element allows for greater flexibility, granting the central bank more time to assess the effects of its past policies and fine-tune its stance as new information emerges.

He added that by underlining the importance of this 'breathing space', stating, "This is crucial given that – as I said before – the transmission of our monetary policy may actually turn out to be stronger than our projections indicate."

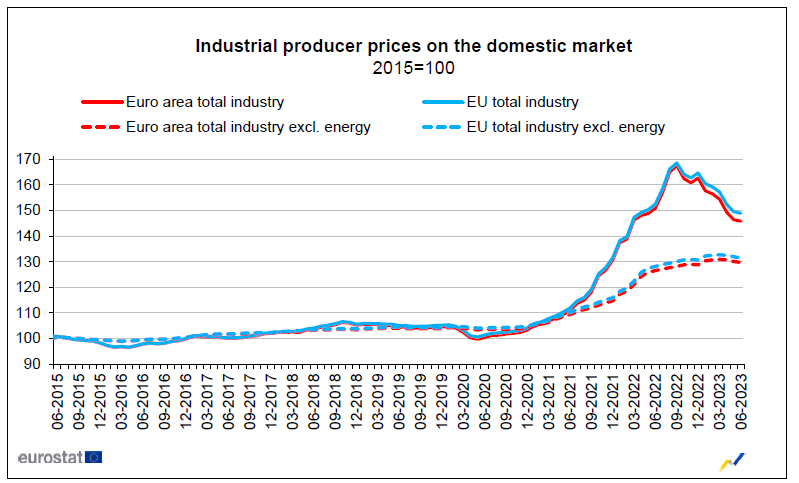

Eurozone PPI down -0.3% mom, -3.4% yoy in June

Eurozone PPI was down -0.3% mom, -3.4% yoy in June, versus expectation of -0.2% mom, -3.1% yoy. For the month, industrial producer prices decreased by -0.7% for intermediate goods and by -0.5% in the energy sector, while prices remained stable for durable consumer goods and for non-durable consumer goods, and prices increased by 0.1% for capital goods. Prices in total industry excluding energy decreased by -0.3%.

EU PPI was down -0.3% mom, -2.4% yoy. The largest monthly decreases in industrial producer prices were recorded in Hungary (-2.5%), Bulgaria and Latvia (both -2.4%) and Belgium (-2.2%), while the highest increases were observed in Ireland (+4.0), Croatia (+1.3%) and Sweden (+1.2%).

GBP/USD Exchange Rate Falls to a Month’s Minimum

Yesterday and today, the GBP/USD rate fell below 1.27 for the first time since July 6. A number of factors contributed to this:

- strengthening of the US dollar index due to downgrading of the US credit rating by Fitch;

- strong data on the ADP labor market — the number of jobs in the US, excluding the agricultural sector, increased by more than 300k over the month;

- market expectation of news from the Bank of England, which will publish its interest rate decision today at 14:00 GMT+3.

According to Reuters, forecasts for the UK economy are disappointing. Market participants expect a 14th rate hike by the Bank of England by 0.25%.

Technical analysis of the GBP/USD chart shows that:

- summer peaks formed an important head-and-shoulders pattern;

- the neckline, which can be drawn through the median line of the ascending channel, has already been broken after a weak rebound in the last days of July.

The pound, which looks weak against the US dollar, may be supported by:

- encouraging words from the head of the Bank of England;

- block of support formed in the area of 1.2600 from the low of June, the lower border of the channel and SMA (100).

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

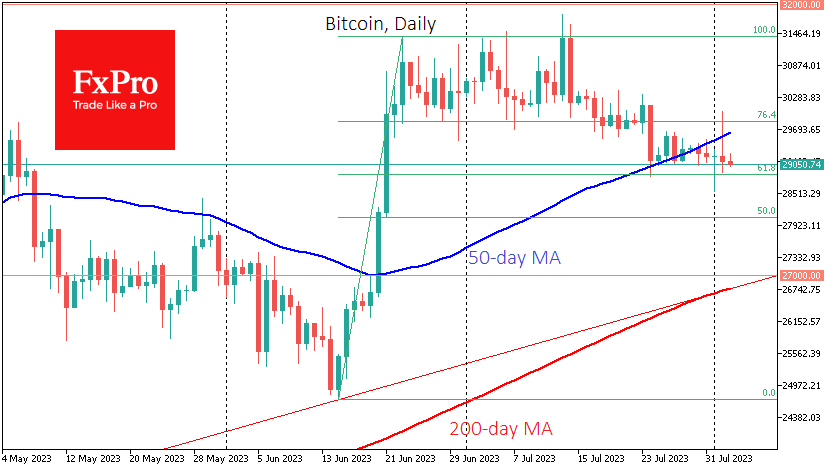

Bitcoin’s Continued Slide Down

Market picture

The crypto market cap fell 1.6% in 24 hours to $1.166 trillion. Risk assets in traditional markets came under pressure as the accumulated overheating in equities (especially in techs) accompanied a trigger – Fitch’s cut of the US rating.

The initial flight of speculators into Bitcoin proved to be short-lived. Bitcoin closed Wednesday down 0.5%, losing over 3.1% from its peak at the start of the day, and failed to get back above the 50-day average. This is another bearish signal in addition to the sequence of downward daily candles. So far, Bitcoin has managed to avoid accelerating the sell-off, but it looks like it’s only a matter of time before it does.

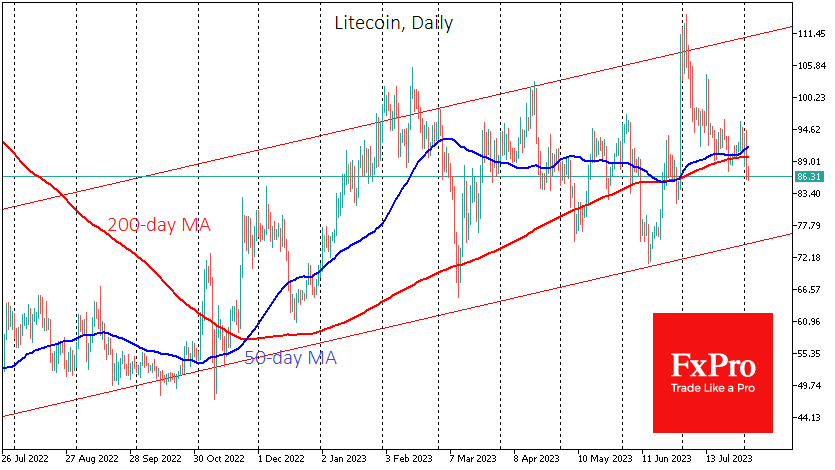

On Wednesday, the Litecoin (LTC) network saw its third halving. The reward per block was reduced to 6.25 LTC. So far, 87.5% of the total LTC supply has been mined. The altcoin reacted with a decline and hit new month lows at around $86. This drop sent the coin below the 50 and 200-day averages, raising the question of a long-term trend change and opening the way down to $77-80.

News Background

Trading activity in the Bitcoin spot market has weakened to its lowest since November 2020, Santiment noted. Major players have so far refrained from entering exchanges, and this trend may continue in August.

MicroStrategy founder Michael Saylor said the company had bought an additional 467 BTC worth $14.4 million in July. As of 31 July, MicroStrategy owns 152,800 BTC worth approximately $4.53 billion at $29,672.

BlackRock’s filing to launch a bitcoin ETF is part of an “adoption cycle” that will allow the first cryptocurrency to hit record highs, Galaxy Digital CEO Mike Novogratz said. The head of BlackRock believed in Bitcoin, he said, and that’s the most important thing that has happened in the crypto market this year.

The chances of the US Securities and Exchange Commission (SEC) approving a bitcoin-ETF application have risen to 65 per cent, Bloomberg analyst James Seyffarth said. Two weeks earlier, he estimated this probability at 50%; a few months ago – at 1%.

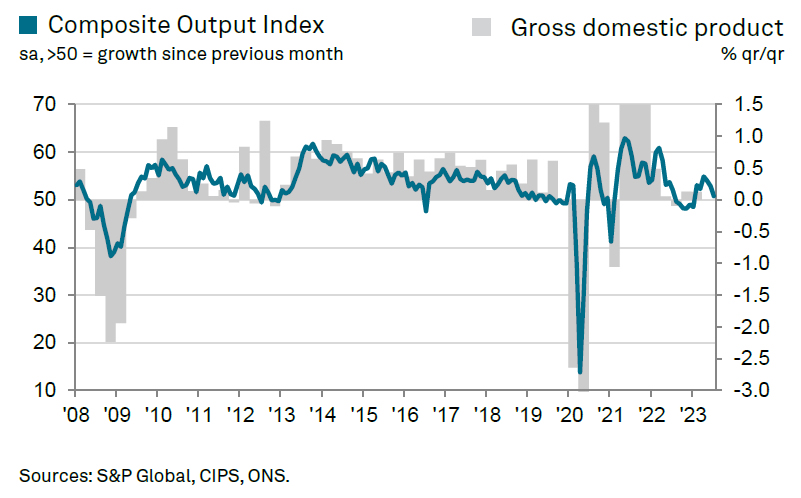

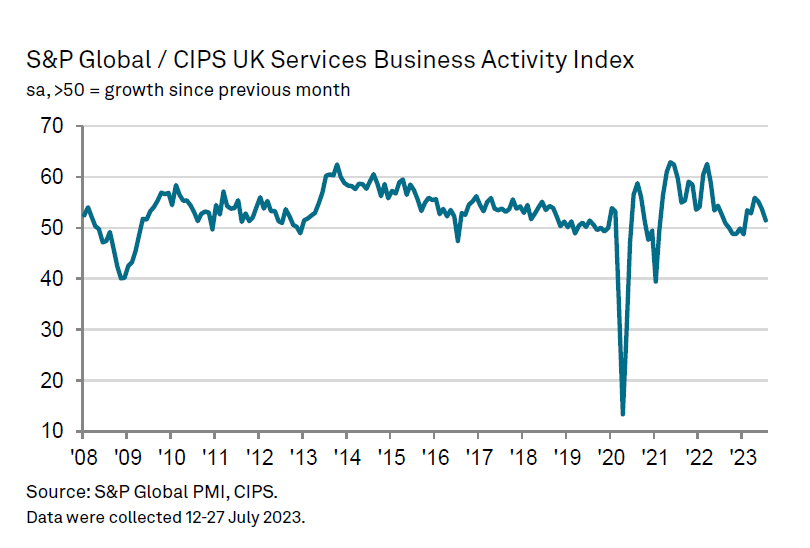

UK PMI composite finalized at 50.8, economy to flatline at best

UK PMI Services was finalized at 51.5 in July, down from June's 53.7. PMI Composite was finalized at 50.8, down from June's 52.8, sparking concerns over the possibility of an economic stagnation in the coming months.

Tim Moore, Economics Director at S&P Global Market Intelligence: "The loss of momentum signalled by service providers in July suggests that the UK economy is set to flatline at best in the coming months.

"There were sporadic reports that subdued demand had led to more competitive pricing and the pass through of lower fuel costs, which contributed to a slowdown in output charge inflation to its second-lowest since August 2021.

"However, there was no let-up in pressure on business expenses as the rate of input cost inflation was virtually unchanged from that seen on average in the second quarter of 2023.

"Survey respondents widely commented on strong cost pressures due to higher salary payments in July, which will add to concerns among policymakers that sticky inflation and stagnant growth will prove a persistent challenge for the UK economy during the second half of the year."

British Pound Under Pressure Ahead of Bank of England Decision

- BoE expected to raise rates at Thursday meeting

- Money markets are split over extent of rate hike

The British pound is slightly lower on Thursday. In the European session, GBP/USD is trading at 1.2885, down 0.19%. The pound has been struggling and is down 1.26% this week.

BoE expected to raise rates

The Bank of England meets later today and policy makers have a tough decision on their hands. Will they raise rates by 25 basis points or be more aggressive and deliver a 50-bp hike? The BoE has raised rates 13 consecutive times since December 2021 and is widely expected to continue hiking at today’s meeting.

The money markets have priced in a 25-bp increase at 62%, with a 38% chance of a 50-bp hike. That means the meeting is live and we could see some volatility from the pound following the rate announcement. The BoE’s decision may well depend on whether inflation is moving downwards fast enough. Headline CPI fell to 7.9% in June, down from 8.7%. Core CPI has been stickier and was unchanged in June at 6.9%.

The BoE is well aware that its tightening is causing plenty of pain for consumers, but inflation remains public enemy number one, and there is a great deal of distance before inflation is brought down closer to the 2% target. Can the BoE afford to raise by just 25-bp or is a second consecutive hike of 50-bp needed? The BoE has played its cards close to the chest and that is likely the reason we are seeing the split amongst investors as to how high a raise we’ll see later today..

GBP/USD Technical

- There is resistance at 1.2744 and 1.2870

- 1.2637 and 1.2511 are providing support

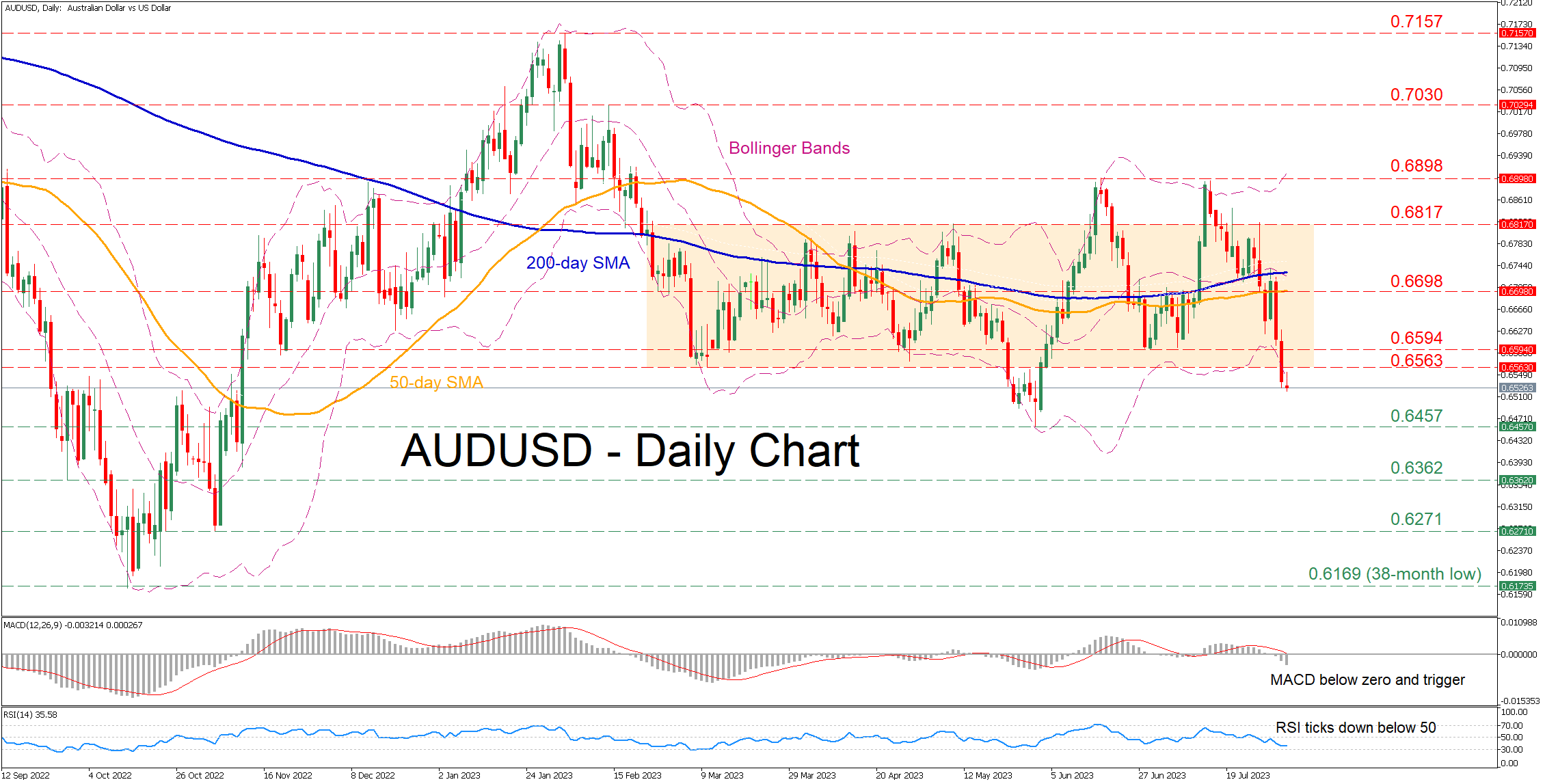

AUDUSD Extends Retreat Below Rectangle, 2023 Lows in Sight

AUDUSD has been in a steady decline after its latest bullish breakout from the rectangle encountered resistance at 0.6898, validating a double top pattern. Moreover, in the near term, the pair has exited the sideways pattern to the downside, while its break beneath both the 50- and 200-day simple moving averages (SMAs) has painted a gloomy technical picture.

The momentum indicators currently suggest that bearish forces are intensifying. Specifically, the RSI is negatively charged below its 50-neutral mark, while the MACD is declining further below zero and its red signal line.

Should the retreat resume, the price could initially test the 2023 bottom of 0.6457. Slicing through that region, the pair might descend towards levels not seen in months, where the September 2022 low of 0.6362 could curb further downside attempts. A break below the latter could open the door for the November 2022 low of 0.6271.

Alternatively, if the pair manages to halt its decline and storm back higher, the previous support regions of 0.6563 and 0.6584 could prove to be the first hurdles for the bulls to conquer. Surpassing the latter, the price might challenge the 50-day SMA, currently at 0.6698. Further advances might then cease at 0.6817, which is the upper border of the rectangle.

In brief, AUDUSD has dipped below its rangebound pattern amid intensifying negative momentum. A failure to re-enter the range could lead to more severe losses, but traders should not rule out a potential rebound as the pair is approaching oversold conditions.