Sample Category Title

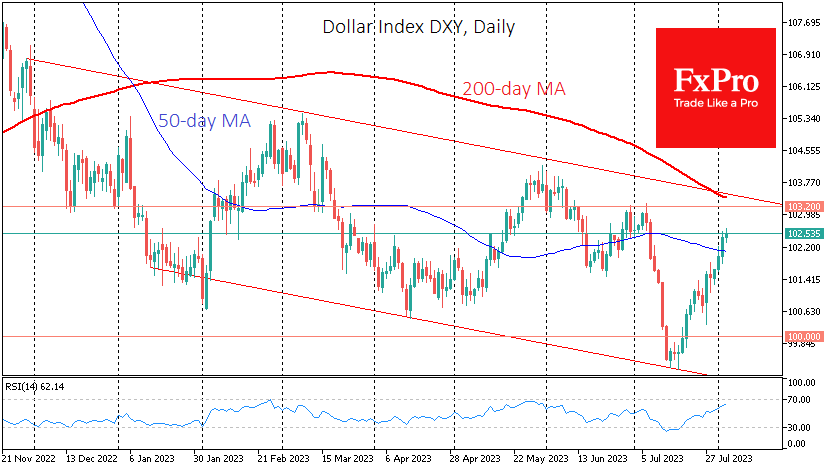

Dollar’s Ascent Could be the Start of a Long-Term Trend

The US dollar is continuing the rally that began in the middle of last month, benefiting from the caution in financial markets in recent days. Although the current rally has not yet brought the Dollar Index back to the levels seen before the massive sell-off in early July, the recent Dollar rally could become a long-term trend.

The Dollar has recently been supported by robust macro data, including yesterday’s ADP report of a 324k increase in private-sector employment. The largest weekly drop in commercial oil inventories also indicates domestic solid demand. The markets are now getting the message from the Fed that we don’t have to wait for a policy reversal soon and that rate hikes are not over yet.

The Fitch downgrade has breathed new life into the dollar rally. As a first step, investors are getting rid of the weakest assets in their portfolios by buying more liquid Treasuries and the dollar. If the US’s image is damaged, it may take months for the overhang of selling to reach the most protective instruments.

In 2011, the S&P downgrade of the U.S. triggered a multi-year rally in the dollar as other countries fared even worse, not to mention riskier corporate bonds.

Something similar could happen this time around. In that case, the 100 level on the dollar index could be a new stepping stone to start another multi-year rise. The levels of 80 from 1990 to 1995 and in 2014 and 90 from 2017 to 2021 played roughly the same role.

However, the long road must begin with the first step. The dollar index has been in a downward channel since last November, with its upper boundary now near 103.2, but to confirm a reversal, the dollar would need to climb above the previous local peak at 104.2.

The 200-day moving average is near 103.40, and a move up to it from the current 102.5 may be a much easier task than consolidating above it. But if it happens, the importance of this signal for FX and global markets must be emphasised.

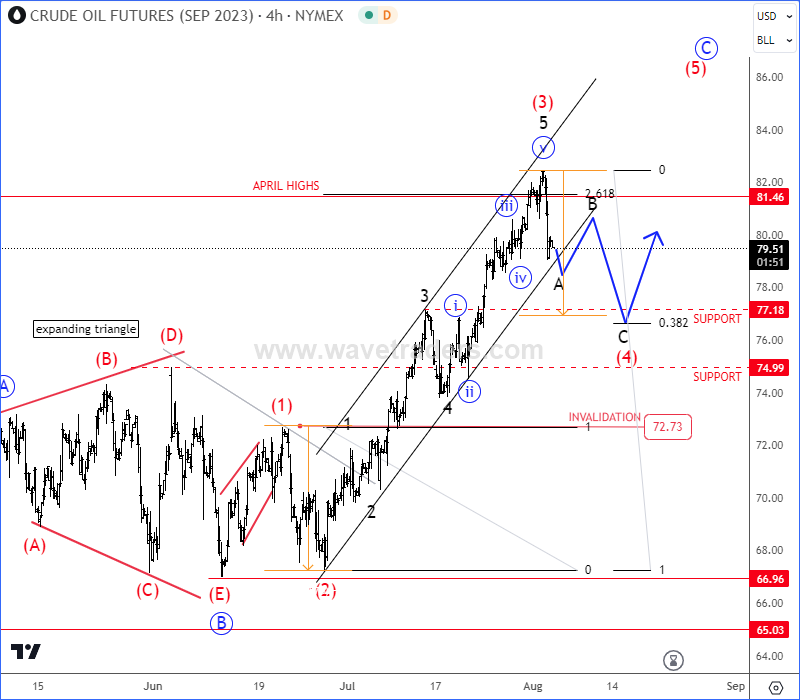

Crude Oil Slows Down for a New Correction

Crude oil faced strong drop and spike back in May, which can be also considered as the final leg of wave (5) of A, so we are aware of a higher degree A-B-C recovery after strong reversal up from the lows. After a completed wave A and expanding triangle in wave B, which is tricky, but still a bullish pattern that already sent prices higher, ideally within a five-wave bullish impulse into wave C. Now that came back to projected April highs for wave 5 of (3), we can see a new, higher degree A-B-C correction within wave (4) that can retest 77-75 support area before the uptrend for wave (5) resumes.

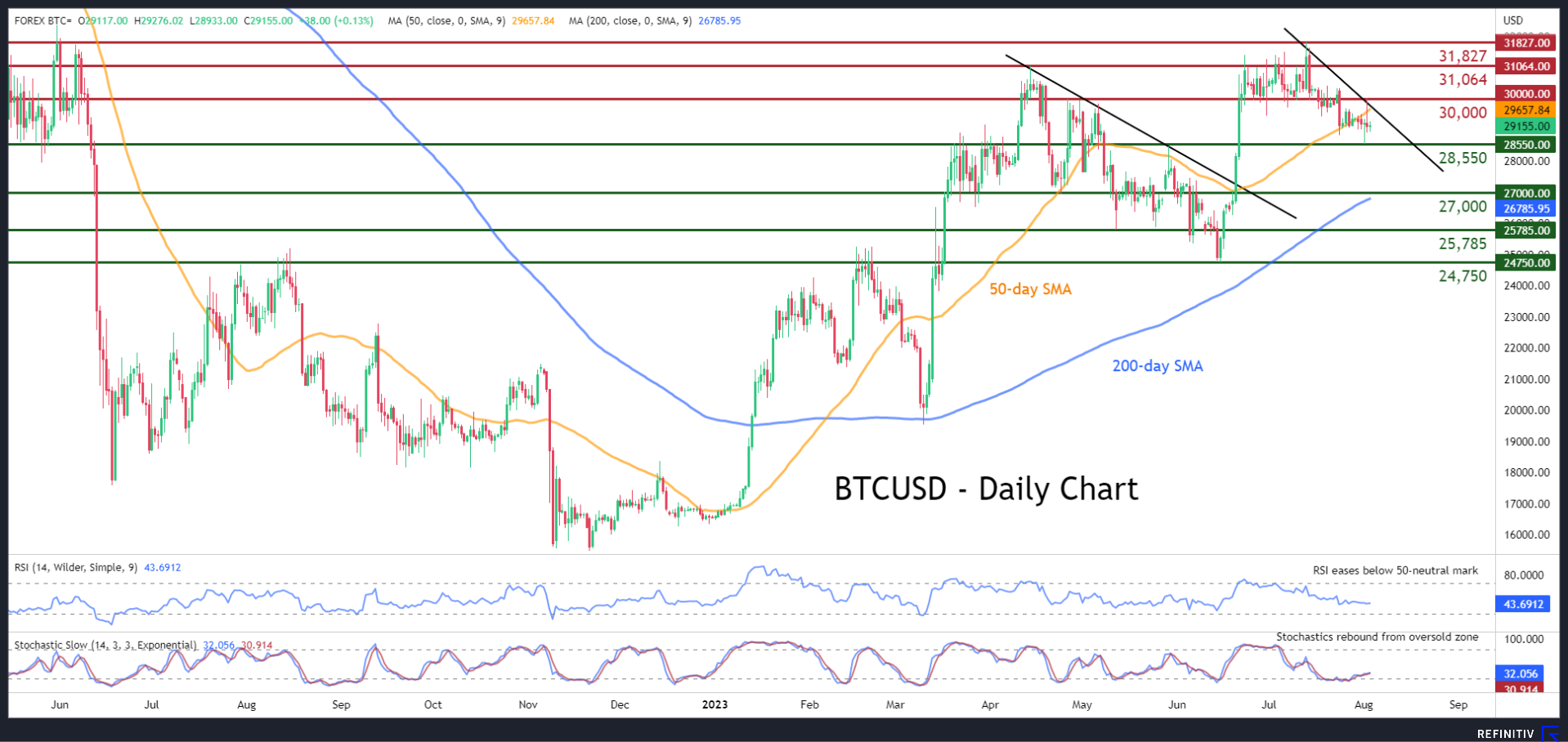

BTCUSD Retreats Below Ascending 50-day SMA

BTCUSD (Bitcoin) has been rangebound in the last few daily sessions following a mild pullback from its recent highs. Moreover, the king of cryptos has been gradually forming a structure of lower highs similar to the one observed during the April-June period, with the decline beneath the 50-day simple moving average (SMA) further darkening the outlook.

The momentum indicators currently suggest that the near-term risks are tilted to the downside. Specifically, the RSI is descending below the 50-neutral threshold, while the stochastics remain flat after a rebound from the oversold territory.

Should the bears try to push the price lower, the recent support of 28,550 could act as the first line of defence. If that barricade fails, the spotlight could turn to the April bottom of 27,000 before the May low of 25,785 gets tested. Further declines might then cease at the June low of 24,750.

On the flipside, if the price regains tractions and edges back higher, the $30,000 psychological mark could prove to be the first barricade for buyers to claim. A violation of that zone may open the door for the April peak of 31,064. Surpassing that region, the price could then challenge the 14-month high of 31,827.

Overall, BTCUSD has been rangebound in the last few sessions amid a broader short-term bearish pattern. For the bulls to regain confidence, the price needs to jump back above the 50-day SMA.

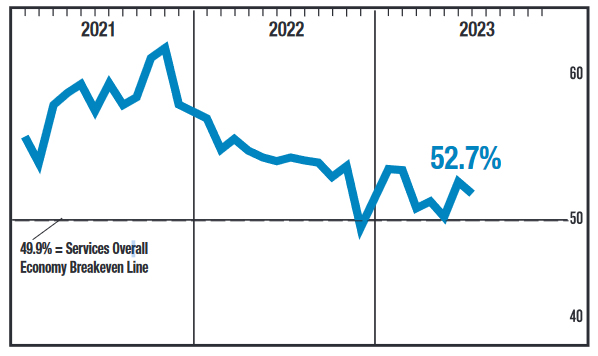

US ISM services fell to 52.7 in Jul, corresponds to 1% annualized GDP growth

US ISM Services PMI dropped from 53.9 to 52.7 in July, slightly below expectation of 53.0. Looking at some details, business activity/production dropped from 59.2 to 57.1. New orders dropped from 55.5 to 55.0. Employment dropped from 53.1 to 55.9. Prices rose from 54.1 to 56.8.

ISM said: "The past relationship between the Services PMI® and the overall economy indicates that the Services PMI® for July (52.7 percent) corresponds to a 1-percent increase in real gross domestic product (GDP) on an annualized basis."

Sunset Market Commentary

Markets

The Bank of England board raised interest rates by 25 bps to 5.25% in a 6-3 split decision. Two members favoured a continuation at the 50 bps clip while one wanted to keep the policy rate unchanged. The BoE acknowledged but downplayed the bigger than expected June CPI decline (to 7.9%). New forecasts based on a policy rate hitting 6% showed inflation still being at 5% by the end of this year and not hitting the 2% target before 2025Q2! The upward inflation revision compared to the May forecast, when a peak policy rate of “only” 4.75% was used, comes as the BoE decided to bring some of the inflation risks effectively into the projection. One of them includes increasing pay gains. Private sector pay growth increased to 7.7% y/y in the three months to May, materially above the May expectations. This follows a still tight labour market, even if some signs of easing begin to emerge. Quarterly GDP growth has been around 0.2% during 2023H1 and a similar growth rate may occur in the near term. Here too, signs of weakness arise, with the BoE specifically mentioning the July PMIs. In terms of further tightening, the BoE retains guidance that more hikes follow in case of more evidence of persistent inflationary pressures. It added a phrase stating that “The MPC will ensure that Bank Rate is sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with its remit.” Hello, higher for longer.

UK money markets still fully discount two more rate hikes over the course of this year/beginning of the next. UK short term rates collapsed 10 bps after the decision as some braced for another 50 bps move before cutting losses in half. The pound loses ground, though the bulk of that move happened in the run-up to the meeting. EUR/GBP tested the 0.865 zone, up from the low 0.86 area. Ahead of the BoE, there was some talk of the central bank stepping up the balance sheet reduction as indicated by the likes of Ramsden. Instead, it only said it would decide over the year ahead amount (Oct 23 – Sep 24) at the September meeting. In other markets, the core bond/UST and equity sell-off continued. US yields extend yesterday’s ascent by adding 3.6 (2-y)-11 (30-y) bps. Fed’s Barkin saw in the June CPI signs of a soft landing, supporting the yield rally at the long end of the curve. Germany adds up to 6 bps. EUR/USD whipsawed around opening levels of 1.094. The Japanese yen outperforms. Economic data today included marginally weaker than expected weekly jobless claims (227k vs 221k), a sharper than anticipated uptick in Q2 nonfarm productivity (3.7% vs 2.2%), causing unit labor costs to rise less than estimated (1.6% vs 2.5%). The US services ISM is scheduled for release after wrapping up this report.

News & Views

Swiss inflation fell in July. The monthly pace turned to a negative -0.1%, making the yearly figure ease from 1.7% to 1.6%. Core inflation dropped 0.2% m/m, falling to 1.7% vs. an unchanged 1.8% analyst estimate. The Swiss Federal Statistics Office said reduced prices for clothing and footwear were among the reasons for the decline. Prices for air transport and international package holidays fell too while prices for supplementary accommodation and the hire of private means of transport increased. Services inflation as a whole eased further, from 1.7% to 1.5%. The headline gauge has been within the central bank’s 0-2% target range for a second month straight now. However, the Swiss National Bank expects price pressures to rebound by the end of the year amid a wave of rent increases. SNB president Jordan said a September rate hike is therefore “most likely” to bring inflation permanently below 2%. EUR/CHF weakens to 0.957 today though that has mainly to do with the general risk aversion.

Turkish disinflation came to a halt in July. Price pressures reaccelerated from 38.21% to 47.83% on a searing 9.49% m/m pace. Core inflation picked up too, from 47.33% to 56.09%. All measures topped expectations. Transportation costs jumped the most as a result from last month’s introduced tax hikes on fuel. The government also raised taxes on several other essential goods as it sought to finance Erdogan’s expensive pre-election pledges including one month of free natural gas. This complemented ongoing weakness in the Turkish lira, fueling inflation further. The Turkish central bank expects the current bout of rising price pressures to end only by mid-2024, project at around 60%. It is currently in the process of gradually lifting the policy rate, having brought it from 8.5% to 17.5% currently. Its next meeting is August 24. The Turkish lira today holds steady at record low levels around EUR/TRY 29.56 and USD/TRY 26.98.

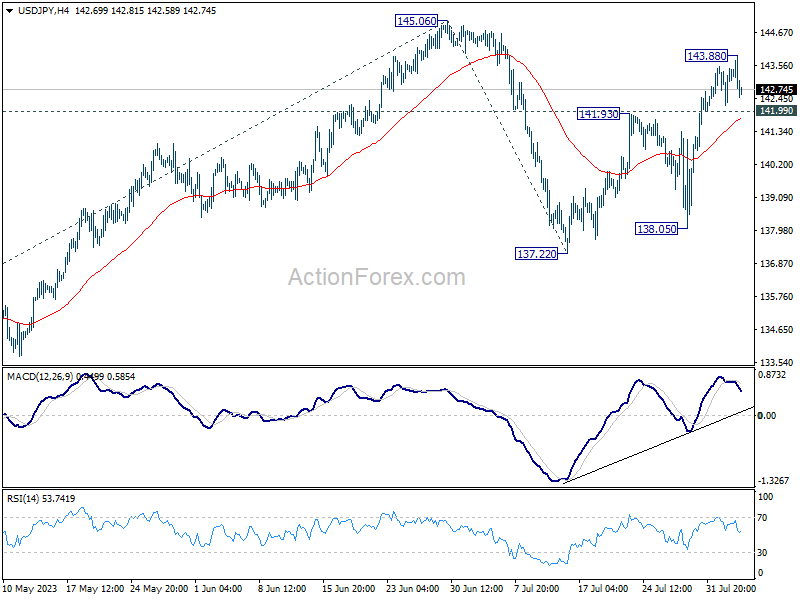

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.56; (P) 143.01; (R1) 143.79; More...

Intraday bias in USD/JPY neutral with current retreat. On the upside, above 143.88 will target a retest on 145.60 resistance first. Decisive break there will resume whole rally from 172.20. Next target is 61.8% projection of 129.62 to 145.06 from 137.22 at 146.76. However, sustained trading below 55 4H EMA (now at 141.77) will turn bias back to the downside for 137.22/138.05 support zone instead.

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

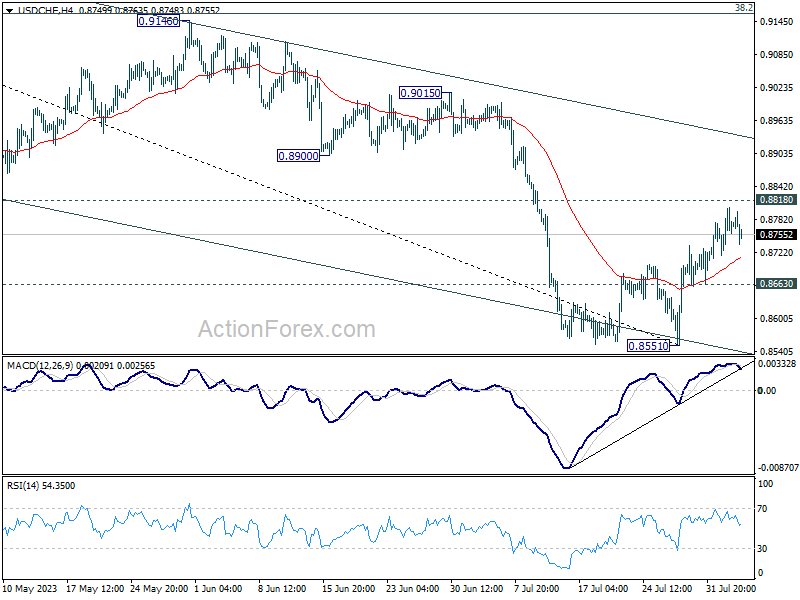

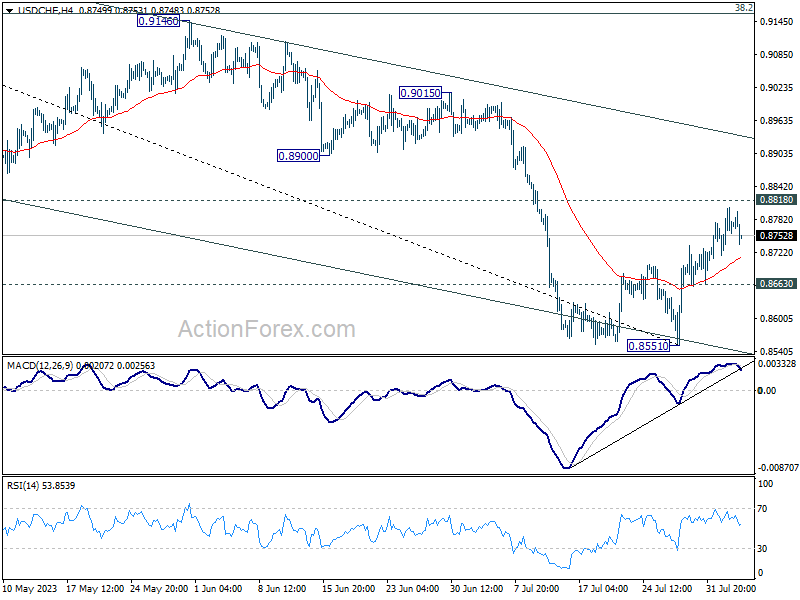

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8727; (P) 0.8766; (R1) 0.8814; More....

Intraday bias in USD/CHF is turned neutral as it lost momentum ahead of 0.8818 support turned resistance. As noted before, rejection by 0.8818 will maintain near term bearishness. Further break of 0.8863 minor support will turn bias back to the downside for retesting 0.8551. Nevertheless, decisive break of 0.8818 will carry larger bullish implication, and target 0.9146 cluster resistance.

In the bigger picture, down trend from 1.0146 is seen as in progress as long as 0.8188 support turned resistance holds. Next target is 61.8% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.8317. However, sustained break of 0.8818 should indicate medium term bottoming, and bring stronger rise back to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160), even as a correction.

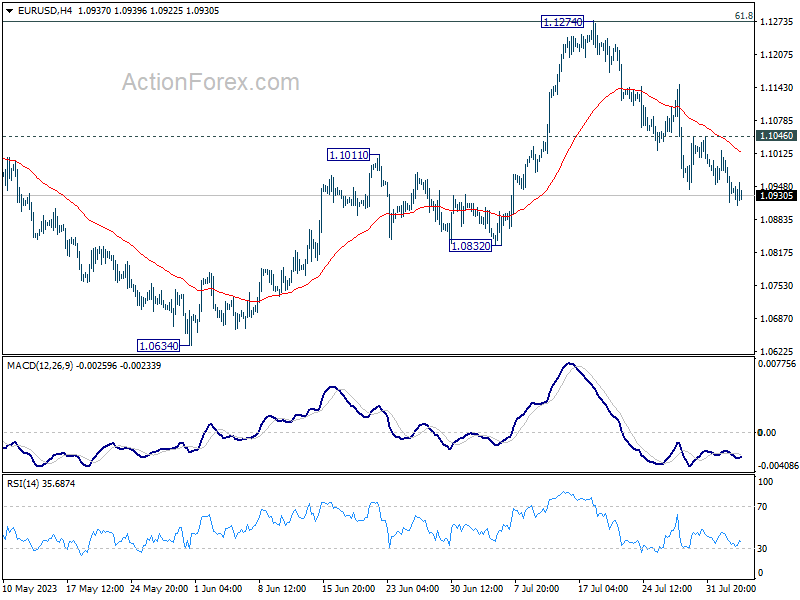

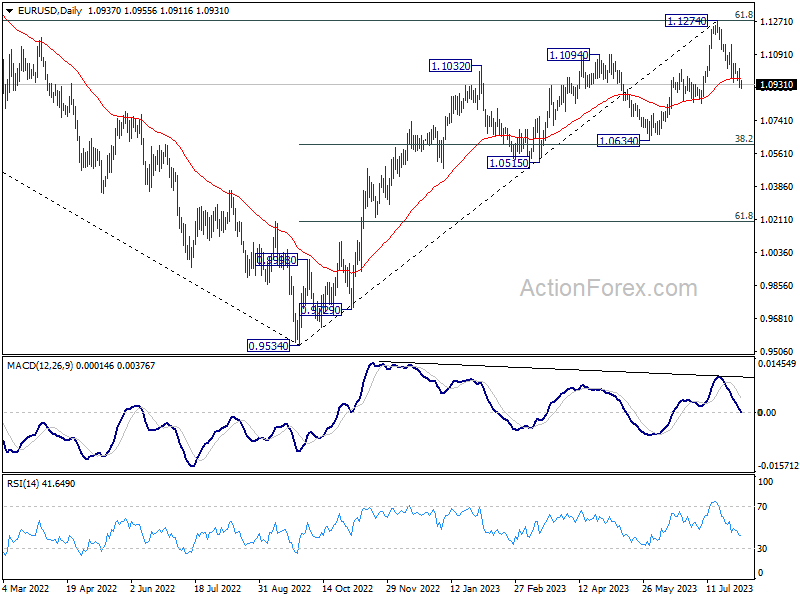

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0897; (P) 1.0959; (R1) 1.0999; More...

Intraday bias in EUR/USD remains on the downside at tis point. Current fall from 1.1274 would target 1.0832 support. Sustained trading below there will target 1.0609/34 cluster support. On the upside, however, break of 1.1046 resistance will turn bias back to the upside for stronger rebound instead.

In the bigger picture, a medium term top could be formed at 1.1274, after failing to break through 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 decisively, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.0963) will bring deeper correction to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to set the range for consolidation.

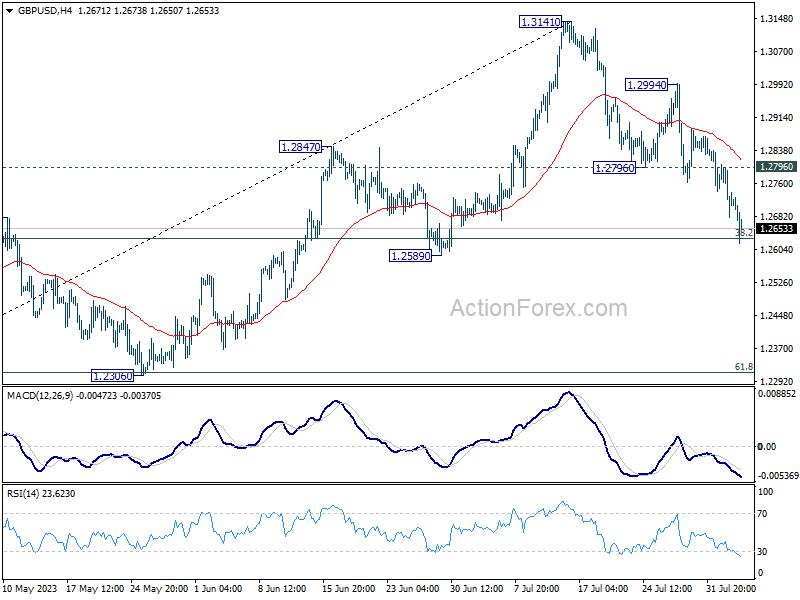

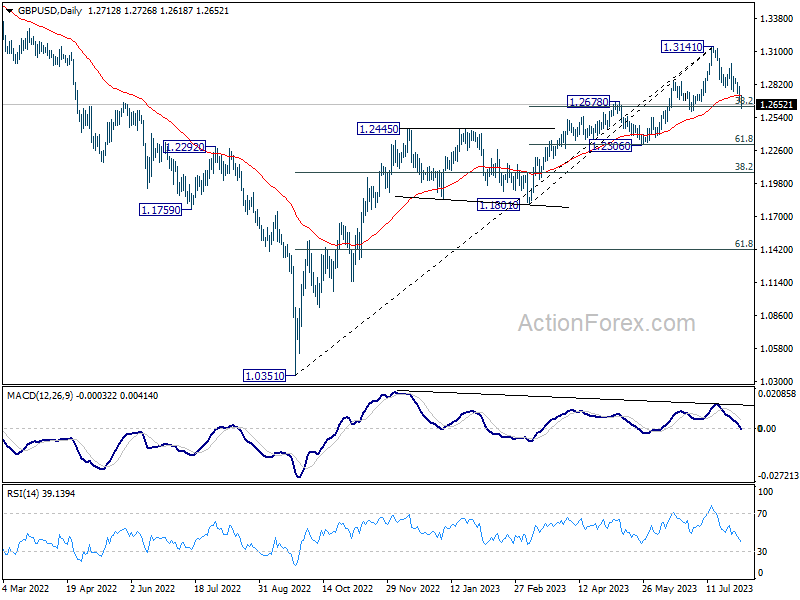

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2659; (P) 1.2732; (R1) 1.2784; More...

GBP/USD's decline from 1.3141 extends to as low as 1.2618 so far today, and met 38.2% retracement of 1.1801 to 1.3141 at 1.2629 already. There is no sign of bottoming yet and intraday bias remains on the downside. Sustained trading below 1.2678 support turned resistance will argue that it's already in a larger correction and target 1.2306 support next. Nevertheless, strong rebound from current level, followed by break of 1.2796 resistance, will retain near term bullishness and turn bias back to the upside.

In the bigger picture, the firm break of 55 D EMA (now at 1.2723) is raising the chance of medium term topping at 1.3141. This is also supported by bearish divergence condition in D MACD. Sustained trading below 1.2678 will indicate that fall from 1.3141 is at least correcting whole up trend from 1.0351, with risk of bearish reversal. Deeper fall would be seen back to 38.2% retracement of 1.0351 to 1.3141 at 1.2075.

Sterling Suffers as BoE Treads Cautiously with 25bps Rate Hike; Dollar Maintains Weekly Lead

Sterling falls significantly today following BoE's decision to raise interest rates by only 25bps. This cautious, along with Governor Andrew Bailey's clear indication that a 50bps hike was not on the table, has resulted in substantial pressure on the Pound. Meanwhile, currency markets remain mixed elsewhere, with Canadian and US Dollar on the softer side, while Japanese Yen stages a recovery. Swiss Franc and Euro have seen some uplift due to purchases against the faltering Pound. Australian and New Zealand Dollars have exhibited mixed behavior.

Despite a slight pullback in early US trading today, Dollar remains the top performer for the week. Euro and Swiss Franc follow closely, buoyed by Sterling's downfall. The Pound currently holds the position of the second-worst performer, only outdone by Australian Dollar's weakness, but has already overtaken New Zealand dollar.

Technically, USD/CHF has been losing upside momentum as seen in 4 H MACD, as it approached 0.8818 support turned resistance. Rejection by 0.8818 will retain near term bearishness in the pair. Further break of 0.8863 support will indicate that larger down trend is resume to resume through 0.8551 low. If realized, that would be an early indicate of completion of Dollar's near term rebound.

In Europe, at the time of writing, FTSE is down -0.66%. DAX is down -0.91%. CAC is down -0.76%. Germany 10-year yield is up 0.490 at 2.584. Earlier in Asia, Nikkei dropped -1.68%. Hong Kong HSI dropped -0.49%. China Shanghai SSE rose 0.58%. Singapore Strait Times dropped -0.63%. Japan 10-year JGB yield rose 0.0257 to 0.654.

In Europe, at the time of writing, FTSE is down -0.66%. DAX is down -0.91%. CAC is down -0.76%. Germany 10-year yield is up 0.490 at 2.584. Earlier in Asia, Nikkei dropped -1.68%. Hong Kong HSI dropped -0.49%. China Shanghai SSE rose 0.58%. Singapore Strait Times dropped -0.63%. Japan 10-year JGB yield rose 0.0257 to 0.654.

US initial jobless claims rose 6k to 227k

US initial jobless claims rose 6k to 227k in the week ending July 29, above expectation of 223k. Four-week moving average of initial claims dropped -5.5k to 228k.

Continuing claims rose 21k to 1700k in the week ending July 22. Four-week moving average of continuing claims dropped -4.5k to 1712k.

BoE hikes 25bps, softens hawkish bias slightly

BoE raises Bank rate by 25bps to 5.25% today. Two members, Jonathan Haskel and Catherine Mann voted for 50bps hike. Swati Dhingra voted for no change again. Six other MPC members vote for the decision.

Hawkish bias was somewhat softened slightly, as the language that "the MPC will adjust Bank Rate as necessary" was dropped. Nevertheless, the central bank maintained that "If there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required."

In the new economic forecast, modal CPI inflation was downgraded slightly from 7.0% to 6.9% in 2023 Q3, and from 2.9% to 2.8% in 2024 Q4. CPI forecast was upgraded from 1.0% to 1.7% in 2025 Q3.

UK PMI composite finalized at 50.8, economy to flatline at best

UK PMI Services was finalized at 51.5 in July, down from June's 53.7. PMI Composite was finalized at 50.8, down from June's 52.8, sparking concerns over the possibility of an economic stagnation in the coming months.

Tim Moore, Economics Director at S&P Global Market Intelligence: "The loss of momentum signalled by service providers in July suggests that the UK economy is set to flatline at best in the coming months.

"There were sporadic reports that subdued demand had led to more competitive pricing and the pass through of lower fuel costs, which contributed to a slowdown in output charge inflation to its second-lowest since August 2021.

"However, there was no let-up in pressure on business expenses as the rate of input cost inflation was virtually unchanged from that seen on average in the second quarter of 2023.

"Survey respondents widely commented on strong cost pressures due to higher salary payments in July, which will add to concerns among policymakers that sticky inflation and stagnant growth will prove a persistent challenge for the UK economy during the second half of the year."

ECB's Panetta advocates for persistence over aggressiveness in monetary policy approach

ECB Executive Board member Fabio Panetta delivered a speech today, emphasizing the importance of "persistence" over "level" in executing the bank's monetary policy given the present economic context.

Panetta stated, "In the current context where policy rates are around the level necessary to deliver medium-term price stability, I will argue that monetary policy may operate not just by increasing rates but also by keeping the prevailing level of policy rates for longer. In other words, persistence matters as much as level."

The ECB official highlighted two primary approaches to the bank's disinflationary monetary policy: the 'level' approach, which involves raising the policy rate beyond its current position, risking a potential need for faster and earlier cuts, and the 'persistence' approach, which advocates for maintaining the policy rates at their prevailing level for an extended duration.

"Emphasizing persistence may be particularly valuable in the current situation," said Panetta, "where the policy rate is around the level necessary to deliver medium-term price stability, the risk of a de-anchoring of inflation expectations is low, inflation risks are balanced, and economic activity is weak."

He warned against the pitfalls of an aggressive rate hike strategy, stating that it "might amplify the risk associated with overtightening, which could subsequently require rates to be cut hastily in a deteriorating economic environment."

By contrast, Panetta argued, the 'persistence' element allows for greater flexibility, granting the central bank more time to assess the effects of its past policies and fine-tune its stance as new information emerges.

He added that by underlining the importance of this 'breathing space', stating, "This is crucial given that – as I said before – the transmission of our monetary policy may actually turn out to be stronger than our projections indicate."

Eurozone PPI down -0.3% mom, -3.4% yoy in June

Eurozone PPI was down -0.3% mom, -3.4% yoy in June, versus expectation of -0.2% mom, -3.1% yoy. For the month, industrial producer prices decreased by -0.7% for intermediate goods and by -0.5% in the energy sector, while prices remained stable for durable consumer goods and for non-durable consumer goods, and prices increased by 0.1% for capital goods. Prices in total industry excluding energy decreased by -0.3%.

EU PPI was down -0.3% mom, -2.4% yoy. The largest monthly decreases in industrial producer prices were recorded in Hungary (-2.5%), Bulgaria and Latvia (both -2.4%) and Belgium (-2.2%), while the highest increases were observed in Ireland (+4.0), Croatia (+1.3%) and Sweden (+1.2%).

Eurozone PMI composite finalized at 48.6, off to a bad start in H2

Eurozone's PMI Services was finalized at a six-month low of 50.9 in July, a considerable drop from June's figure of 52.0. Moreover, PMI Composite was finalized at 48.6, descending from 49.9 in June, marking an eight-month low.

Turning attention to specific member states, PMI Composites revealed that Spain posted a 51.7, reflecting a six-month low. Ireland's index equaled 50.0, an eight-month low, while Italy and Germany saw similar eight-month lows of 48.9 and 48.5, respectively. However, France's PMI Composite showed the most significant contraction, falling to a staggering 32-month low of 46.6.

Reflecting on this troubling data, Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, stated: "The Eurozone is off to a bad start in the second half of the year. Economic output fell in July after stagnating the month before and showing generally solid growth during the first five months of the year."

He pointed out that manufacturing primarily drove this slump in activity, though the services sector also saw a slowdown. He noted, "In the services sector, a weak phase is heralded by the fall of the incoming new business index into contractionary territory."

De la Rubia also noted the divergent economic performance across Eurozone, with French service companies scaling back their activities significantly while Spanish companies continue to expand, albeit at a slower pace than in the first quarter.

"The contrasting economic performance is making the already-difficult job for the ECB even more challenging," he added.

Swiss CPI slowed to 1.6% yoy in Jul, core CPI down to 1.7% yoy

Swiss CPI fell -0.1% mom in July, matched expectations. Core CPI (excluding fresh and seasonal products, energy and fuel) was down -0.2% mom. Domestic products prices rose 0.2% mom while imported product prices dropped -1.2% mom.

Annually, CPI slowed from 1.7% yoy to 1.6% yoy, above expectation of 1.5% yoy. Core CPI decelerated from 1.8% yoy to 1.7% yoy. Domestic products prices was unchanged at 2.3% yoy. Imported products prices dropped further from -0.1% yoy to -0.6% yoy.

China's Caixin PMI composite fell to 51.9, lowest since Jan

China's Caixin PMI Services increased slightly from 53.9 to 54.1 in July, surpassing the anticipated figure of 52.5. However, this reading fell short of the 55.5 average seen over the previous six months. Concurrently, PMI Composite dropped from 52.5 to 51.9, its lowest mark since January.

Commenting on the latest figures, Wang Zhe, a Senior Economist at Caixin Insight Group, expressed that the uneven recovery of the service and manufacturing industries remains a prominent concern. He noted, "Although the manufacturing sector was a drag, the steady expansion of the services industry still helped overall output, demand, and employment remain in positive territory."

The contraction in exports appeared pronounced, and while input costs saw a slight uptick, output prices registered a minor drop. Despite these challenges, expectations for future output remained on the optimistic side, though this metric recorded a new low since November.

On the broader economic landscape, Wang Zhe noted, "Although the data for industrial production and investment in June showed some signs of recovery, macroeconomic growth remained sluggish, and considerable downward pressure on the economy persisted."

Turning to policy recommendations, he emphasized the need for employment guarantees, stabilization of expectations, and boosting household income. He further argued that "At present, monetary policy only has a limited effect on boosting supply. An expansionary fiscal policy that targets demand should be prioritized."

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2659; (P) 1.2732; (R1) 1.2784; More...

GBP/USD's decline from 1.3141 extends to as low as 1.2618 so far today, and met 38.2% retracement of 1.1801 to 1.3141 at 1.2629 already. There is no sign of bottoming yet and intraday bias remains on the downside. Sustained trading below 1.2678 support turned resistance will argue that it's already in a larger correction and target 1.2306 support next. Nevertheless, strong rebound from current level, followed by break of 1.2796 resistance, will retain near term bullishness and turn bias back to the upside.

In the bigger picture, the firm break of 55 D EMA (now at 1.2723) is raising the chance of medium term topping at 1.3141. This is also supported by bearish divergence condition in D MACD. Sustained trading below 1.2678 will indicate that fall from 1.3141 is at least correcting whole up trend from 1.0351, with risk of bearish reversal. Deeper fall would be seen back to 38.2% retracement of 1.0351 to 1.3141 at 1.2075.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) Jun | 11.32B | 10.50B | 11.79B | 10.50B |

| 01:45 | CNY | Caixin Services PMI Jul | 54.1 | 52.5 | 53.9 | |

| 06:00 | EUR | Germany Trade Balance (EUR) Jun | 18.7B | 15.5B | 14.4B | |

| 06:30 | CHF | CPI M/M Jul | -0.10% | -0.10% | 0.10% | |

| 06:30 | CHF | CPI Y/Y Jul | 1.60% | 1.50% | 1.70% | |

| 07:45 | EUR | Italy Services PMI Jul | 51.5 | 52.3 | 52.2 | |

| 07:50 | EUR | France Services PMI Jul F | 47.1 | 47.4 | 47.4 | |

| 07:55 | EUR | Germany Services PMI Jul F | 52.3 | 52 | 52 | |

| 08:00 | EUR | Italy Retail Sales M/M Jun | -0.20% | 0.00% | 0.70% | 0.60% |

| 08:00 | EUR | Eurozone Services PMI Jul F | 50.9 | 51.1 | 51.1 | |

| 08:30 | GBP | Services PMI Jul F | 51.5 | 51.5 | 51.5 | |

| 09:00 | EUR | Eurozone PPI M/M Jun | -0.40% | -0.20% | -1.90% | |

| 09:00 | EUR | Eurozone PPI Y/Y Jun | -3.40% | -3.10% | -1.50% | -1.60% |

| 11:00 | GBP | BoE Interest Rate Decision | 5.25% | 5.25% | 5.00% | |

| 11:00 | GBP | MPC Official Bank Rate Votes | 8--0--1 | 7--0--2 | 7--0--2 | |

| 11:30 | USD | Challenger Job Cuts Y/Y Jul | -8.20% | 25.20% | ||

| 12:30 | USD | Initial Jobless Claims (Jul 28) | 227K | 223K | 221K | |

| 12:30 | USD | Nonfarm Productivity Q2 P | 3.70% | 1.10% | -2.10% | |

| 12:30 | USD | Unit Labor Costs Q2 P | 1.60% | 2.70% | 4.20% | |

| 13:45 | USD | Services PMI Jul F | 52.4 | 52.4 | ||

| 14:00 | USD | ISM Services PMI Jul | 53 | 53.9 | ||

| 14:00 | USD | Factory Orders M/M Jun | 0.20% | 0.30% | ||

| 14:30 | USD | Natural Gas Storage | 18B | 16B |