Sample Category Title

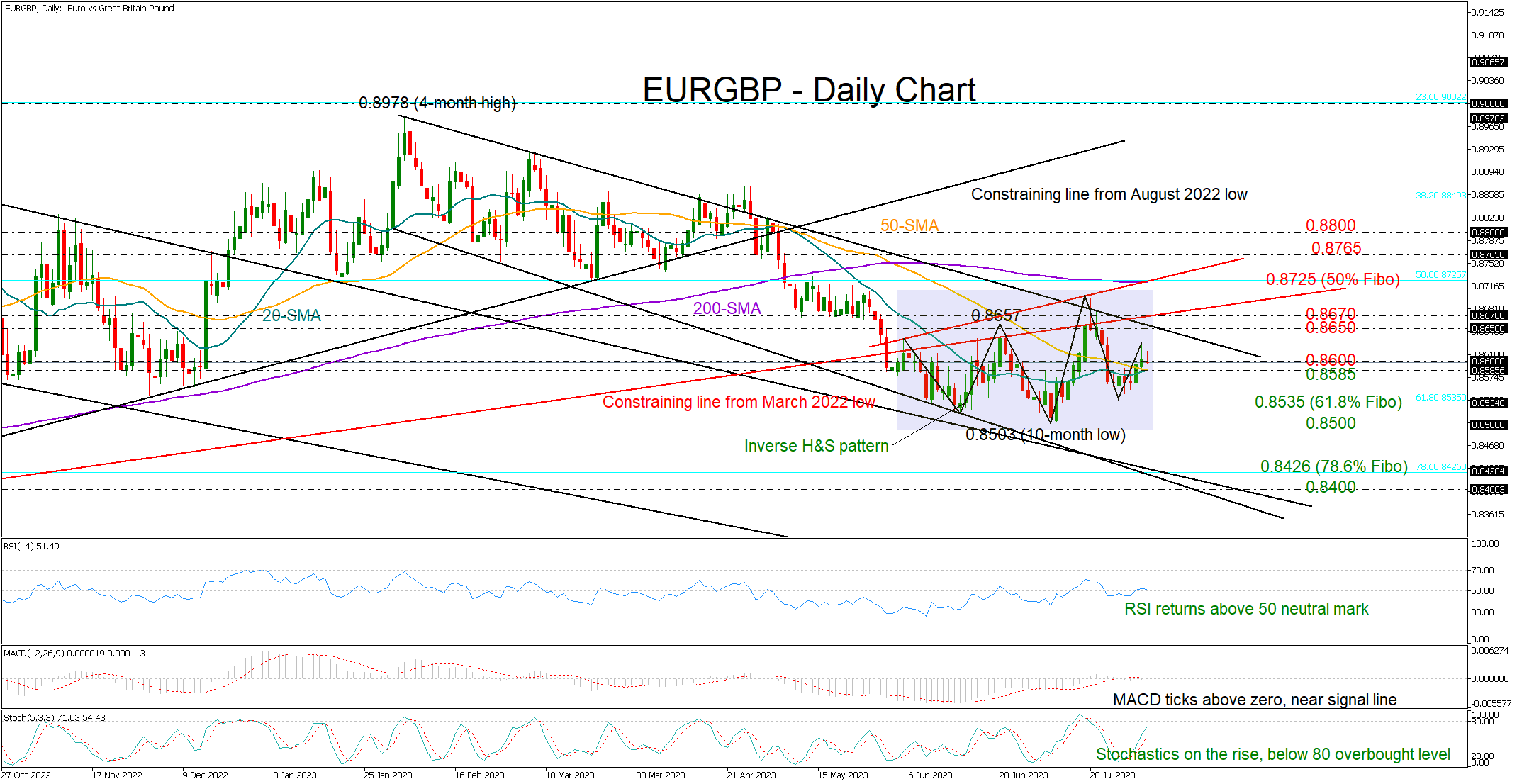

EURGBP Has a Nice Setup for a Bullish Reversal

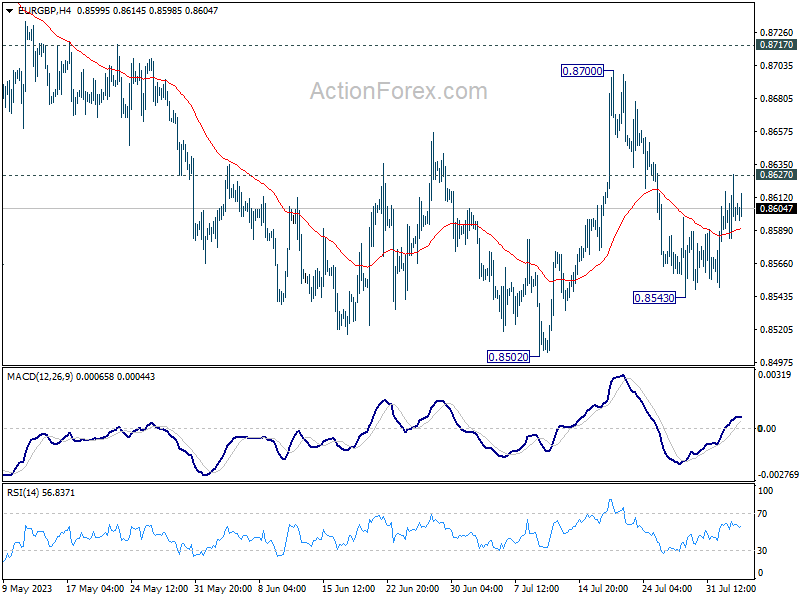

EURGBP keeps on maintaining a positive mood for the third consecutive day while confirming a higher low at 0.8543 ahead of the Bank of England's rate decision today at 11:00 GMT.

Specifically, the pair seems to be building the right shoulder of an inverse head and shoulders pattern (H&S), which theoretically is an encouraging sign that the previous downtrend to a ten-month low of 0.8503 is nearing its end. The 20- and 50-day simple moving averages (SMAs) are set to post their first bullish cross this year, and if that gets completed, the series of higher highs and higher lows in the short-term picture could gain extra credence.

In momentum indicators, the RSI has inched slightly above its 50 neutral mark and the stochastic oscillator has resumed its positive momentum. Meanwhile, the MACD has ticked above the zero line, but overall remains subdued.

Hence, buyers could sustain some caution until the price successfully enters the 0.8600 territory, and more importantly, closes above the 0.8650-0.8670 zone. Recovery efforts could be ruined due to the falling trendline from February's high and the broken ascending trendline from March 2022 low in this area. Should the pair breach that wall, the 200-day SMA, which overlaps with the 50% Fibonacci retracement of the 0.8201-0.9249 upleg, could be another headache at 0.8725. A decisive close higher from there would brighten the short-term outlook, shifting the spotlight to the 0.8765 barrier and then to the 0.8800 psychological mark.

In the event the price slips below its 20- and 50-day SMAs at 0.8585, the spotlight will again fall on the 0.8500-0.8535 key support area. Another step lower from there would point to a failed H&S bullish formation, activating a dynamic decline towards the 0.8400-0.8425 territory. The descending line from October 2022 and February 2023 are contained within that zone, while the 78.6% Fibonacci mark is in the neighborhood as well.

Summing up, a bullish trend reversal could happen for EURGBP, but buyers may require further motivation, such as a consistent rally above the 200-day SMA, to increase their market exposure.

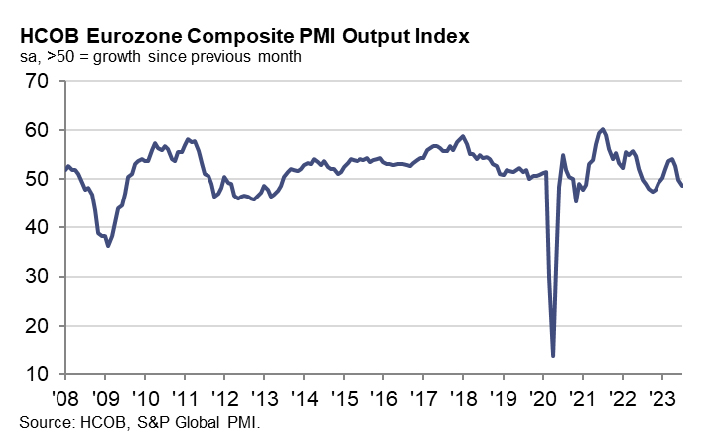

Eurozone PMI composite finalized at 48.6, off to a bad start in H2

Eurozone's PMI Services was finalized at a six-month low of 50.9 in July, a considerable drop from June's figure of 52.0. Moreover, PMI Composite was finalized at 48.6, descending from 49.9 in June, marking an eight-month low.

Turning attention to specific member states, PMI Composites revealed that Spain posted a 51.7, reflecting a six-month low. Ireland's index equaled 50.0, an eight-month low, while Italy and Germany saw similar eight-month lows of 48.9 and 48.5, respectively. However, France's PMI Composite showed the most significant contraction, falling to a staggering 32-month low of 46.6.

Reflecting on this troubling data, Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, stated: "The Eurozone is off to a bad start in the second half of the year. Economic output fell in July after stagnating the month before and showing generally solid growth during the first five months of the year."

He pointed out that manufacturing primarily drove this slump in activity, though the services sector also saw a slowdown. He noted, "In the services sector, a weak phase is heralded by the fall of the incoming new business index into contractionary territory."

De la Rubia also noted the divergent economic performance across Eurozone, with French service companies scaling back their activities significantly while Spanish companies continue to expand, albeit at a slower pace than in the first quarter.

"The contrasting economic performance is making the already-difficult job for the ECB even more challenging," he added.

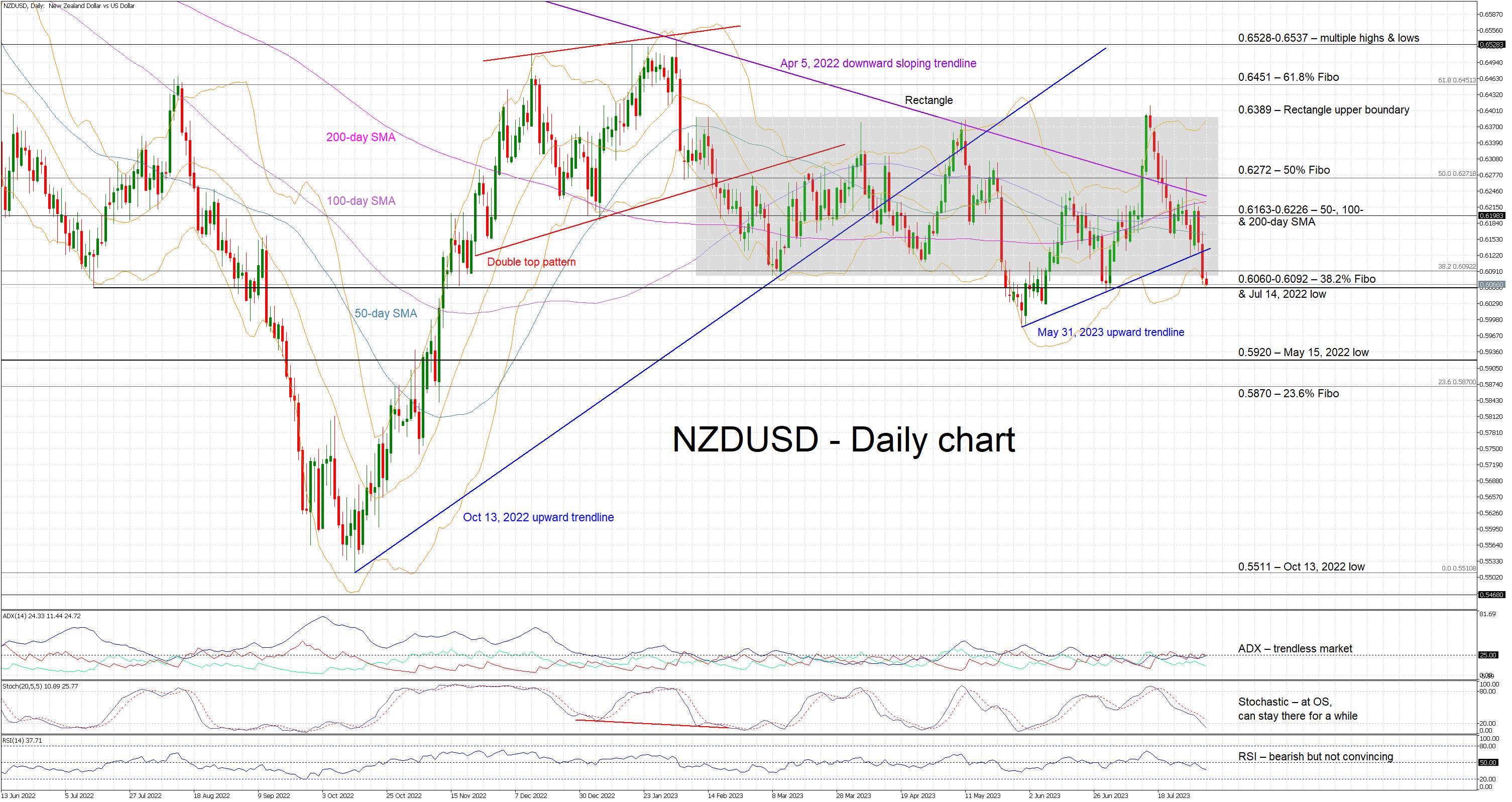

NZDUSD Bears Attempt Another Breakout

NZDUSD is recording another red candle as the bears are again trying to stage a breakout from the rectangle that has been in place since February 2023. This is actually the third breakout attempt since early June 2023. Interestingly, the first target of the bears appears to be to register a lower low, breaking the recent series of higher highs and higher lows developing since the May 31 local trough, and then stage a decisive downleg. Maybe, the continued convergence of the simple moving averages (SMAs) could play a role soon in the bears’ favour.

The momentum indicators are mostly on board with the current pullback. More specifically, the RSI is edging well below its 50-threshold and the stochastic oscillator has just returned to its oversold territory. It can stay there for a considerable amount of time, especially as its moving average is still above the 20-threshold level.

Should the bears feel confident, they would first try to overcome the support set by the 0.6060-0.6092 range that is populated by the 38.2% Fibonacci retracement and the July 14, 2022 low respectively. They would then have the chance of recording a lower low and push NZDUSD below the 2023 of 0.5984, setting their eyes on the May 15, 2022 low at 0.5920.

On the flip side, the Average Directional Movement Index (ADX) is a tad below its 25-threshold and thus pointing to a range-trading market. This probably helps the bulls to remain calm as they plan their counterattack. Defending the 0.6060-0.6092 area would be significant from a short-term perspective, potentially giving them the necessary boost to lead NZDUSD higher towards the 0.6163-0.6226 range. This is defined by the 50-, 100- and 200-day SMAs and hence could prove much tougher to crack.

To conclude, NZDUSD bears remain focused on recording a decisive breakout as they are currently working their way through a strong support area that the bulls appear ready to defend.

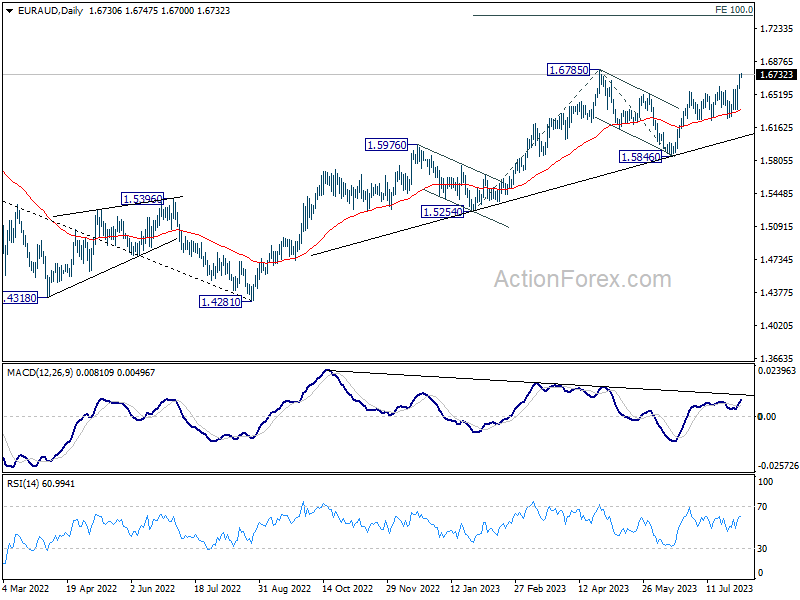

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6633; (P) 1.6683; (R1) 1.6780; More...

Intraday bias in EUR/AUD stays on the upside for retesting 1.6785 high. Decisive break there will resume larger up trend to 1.7377 projection level next. On the downside, break of 1.6587 minor support will delay the bullish case and turn intraday bias neutral first.

In the bigger picture, with 38.2% retracement of 1.4281 to 1.6785 at 1.5828 intact, rally from 1.4281 is still in progress. Firm break of 1.6785 will confirm rise resumption. Next target is 100% projection of 1.5254 to 1.6785 from 1.5846 at 1.7377. On the other hand, rejection by 1.6785 will extend the corrective pattern with another fall leg. But outlook will stay bullish as long as 1.5828 holds.

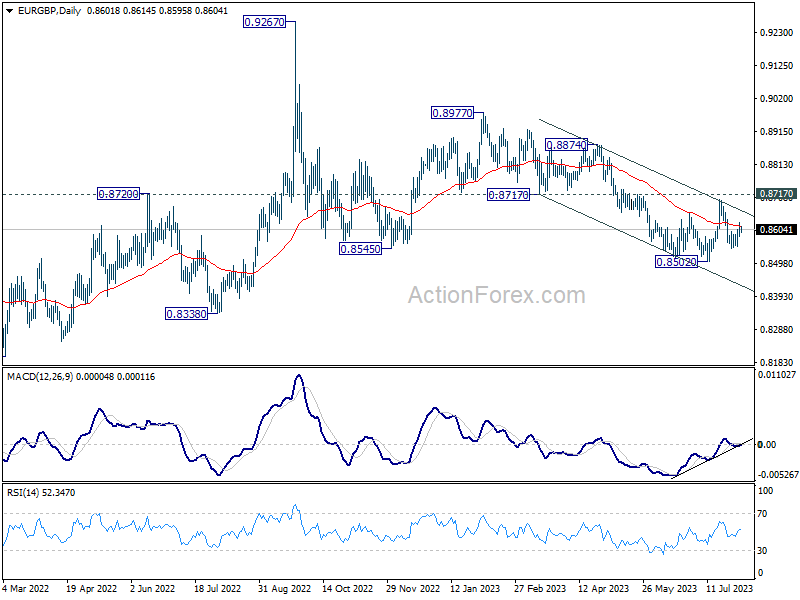

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8584; (P) 0.8606; (R1) 0.8629; More...

Intraday bias in EUR/GBP stays neutral first as recovery lost momentum after hitting 0.8627. On the downside, below 0.8543 will target a test on 0.8502 low. Decisive break there will resume larger decline from 0.8977. On the upside, above 0.8627 minor resistance will turn bias back to the upside for 0.8700, and possibly further to 0.8717 key support turned resistance.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Firm break of 0.8717 support turned resistance will argue that it has completed with three waves down to 0.8502. Further break of 0.8977 will bring retest of 0.9267 high. Nevertheless, rejection by 0.8717, followed by break of 0.8502 will resume the decline towards 0.8201 (2022 low).

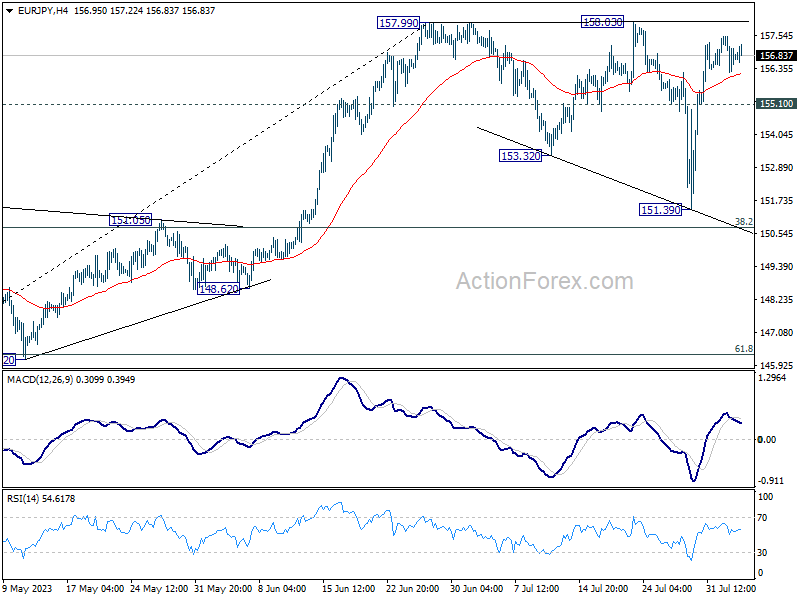

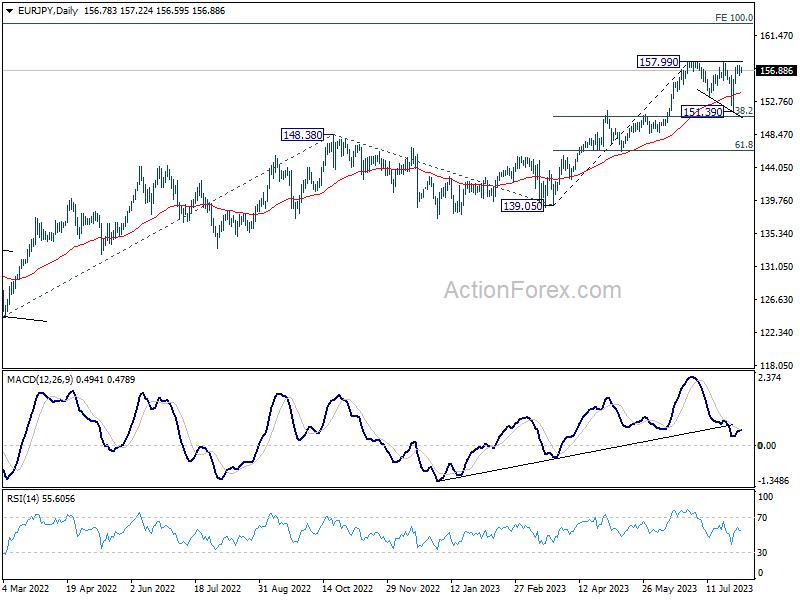

EUR/JPY Daily Outlook

Daily Pivots: (S1) 156.19; (P) 156.85; (R1) 157.43; More....

Intraday bias in EUR/JPY remains neutral for the moment, and outlook is unchanged. On the upside, decisive break of 157.99/158.03 will resume larger up trend to 162.82 projection level next. However, break of 155.10 will extend the corrective pattern from 157.99 with another falling leg instead.

In the bigger picture, as long as 151.60 resistance turned support holds, rise from 114.42 (2020 low) is in progress. On resumption, next target is 100% projection of 124.37 to 148.38 from 138.81 at 162.82. Nevertheless, sustained break of 151.60 will argue that larger correction is already underway. Deeper decline would be seen to 55 W EMA (now at 145.56).

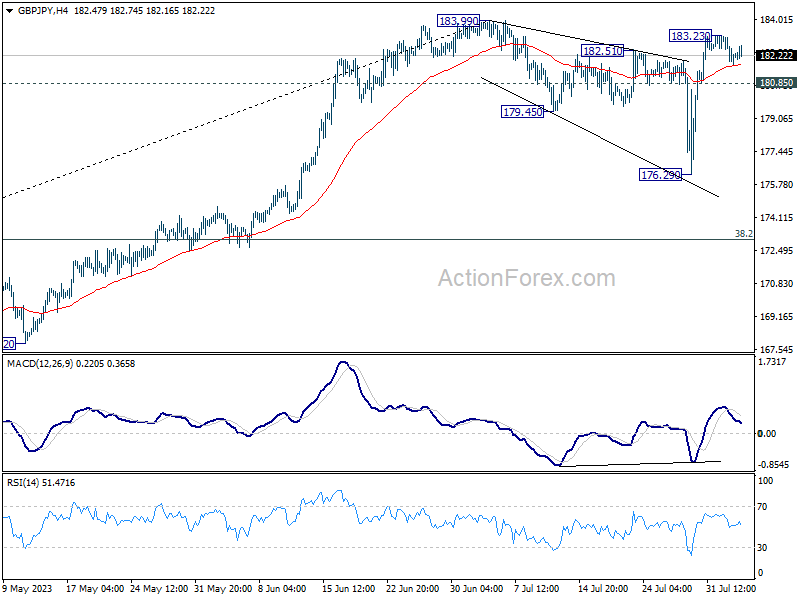

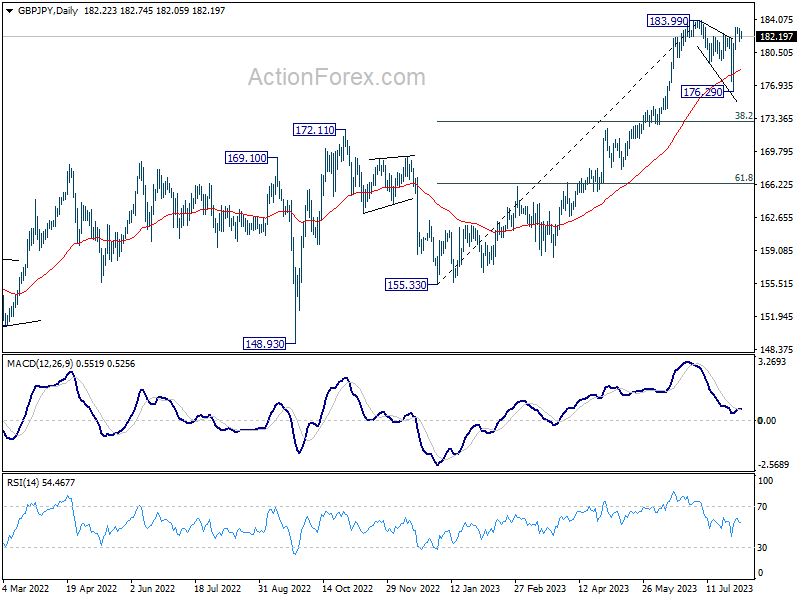

GBP/JPY Daily Outlook

Daily Pivots: (S1) 181.54; (P) 182.40; (R1) 183.03; More...

Intraday bias in GBP/JPY remains neutral at this point, but outlook is unchanged. Corrective pattern from 183.99 should have completed with three waves down to 176.29. Above 183.23 will target 183.99 resistance first. Decisive break there will resume larger up trend. However, break of 180.85 will turn bias to the downside to extend the corrective pattern from 183.99 with another falling leg.

In the bigger picture, as long as 172.11 resistance turned support holds, up trend from 123.94 (2020 low) is expected to continue through 183.99 at a later stage, towards 195.86 (2015 high). Nevertheless, firm break of 172.11 will argue that larger correction is already underway.

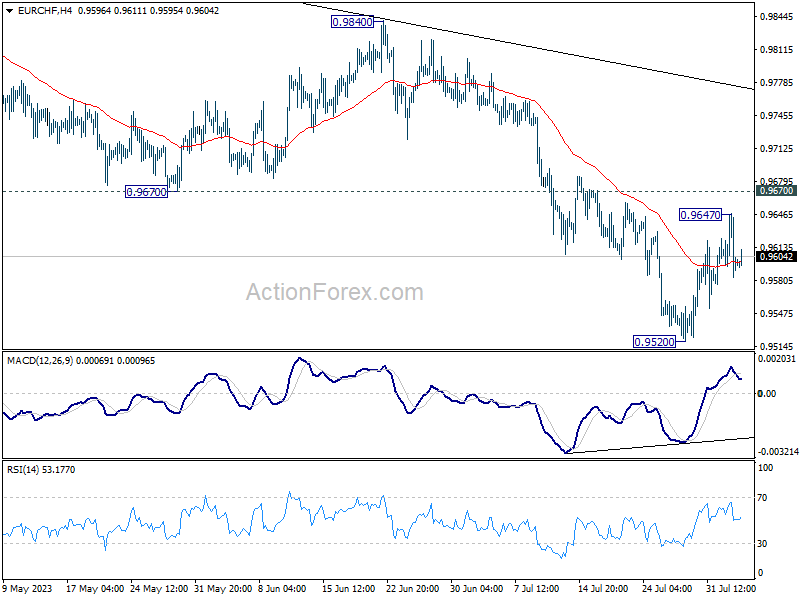

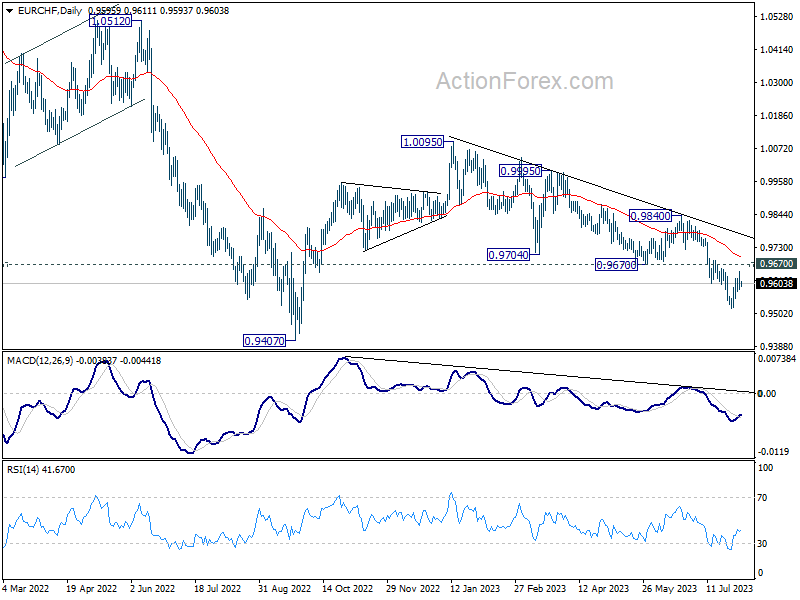

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9573; (P) 0.9611; (R1) 0.9637; More...

Intraday bias in EUR/CHF is turned neutral with 4H MACD crossed below signal line. Also, with 0.9670 support turned resistance intact, near term outlook stays bearish for further decline. Break of 0.9520 will resume the fall from 1.0095 towards 0.9407 low. Nevertheless, sustained break of 0.9670 will be the first sign of bullish reversal and target 0.9840 resistance for confirmation.

In the bigger picture, medium term outlook is staying bearish as the pair is capped well below falling 55 W EMA (now at 0.9876). Down trend from 1.2004 (2018 high) is in favor to continue. Sustained break of 0.9407 will target 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. For now, this will remain the favored case as long as 0.9840 resistance holds, in case of strong rebound.

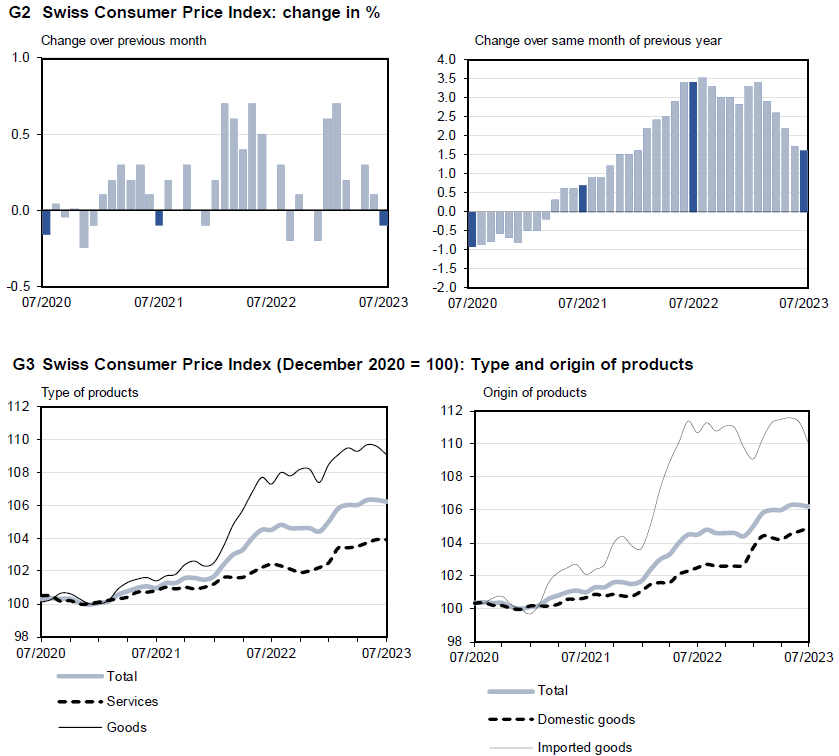

Swiss CPI slowed to 1.6% yoy in Jul, core CPI down to 1.7% yoy

Swiss CPI fell -0.1% mom in July, matched expectations. Core CPI (excluding fresh and seasonal products, energy and fuel) was down -0.2% mom. Domestic products prices rose 0.2% mom while imported product prices dropped -1.2% mom.

Annually, CPI slowed from 1.7% yoy to 1.6% yoy, above expectation of 1.5% yoy. Core CPI decelerated from 1.8% yoy to 1.7% yoy. Domestic products prices was unchanged at 2.3% yoy. Imported products prices dropped further from -0.1% yoy to -0.6% yoy.

Bank of Japan Intervened With Unscheduled Bond Buying Program

Markets

Bunds and US Treasuries parted ways yesterday. Yields on the latter surged more than 8 bps at the long end of the curve. That had little to do with the Fitch rating downgrade, though it was related to one reasons for the decision: the deterioration fiscal situation. US Treasury for the first time in over two years raised the amount on offer for several tenors in the August-October quarter. Next week’s mid-month refinancing operation for example will be $7bn higher ($103bn in total) than in the first month of the previous quarter. In addition, shortly before the announcement ADP’s employment report crushed a 190k consensus by adding 324k new jobs in July. Meanwhile, market talk is moving from a “soft landing” to “no landing” at all in the US. German yields, by contrast, fell 1.8 (30-y) to 6 (2-y) bps. They did close well off intraday lows though, especially longer maturities. Yield differentials as well as a sour equity mood (EuroStoxx50 -1.6%, Wall Street ended more than 2% lower in case of the Nasdaq) favoured the US dollar over the euro. EUR/USD extended its recent correction towards 1.094 after having traded north of 1.10 in earlier dealings. The trade-weighted dollar index closed around 102.59, the highest since early July. Risk-off also supported the yen while currencies with a riskier profile (AUD, NZD, SEK, NOK) suffered. Sterling too declined but managed a close off the lows. EUR/GBP ended north of 0.86.

The Bank of Japan for a second time this week intervened with an unscheduled bond buying programme. That happened as the 10-y moved beyond 0.65%. It is still trading around that level currently. The yen loses marginally even as sentiment is mixed, at best. Japan underperforms (-1.3%). EUR/USD stabilizes around yesterday’s closing levels. US yields extend their ascent. The 10-y yield tested 4.09% resistance yesterday but is now moving past that important level. Apart from intermediate resistance at 4.24%, it was the final hurdle before a return to the 4.33% cycle high. The drop in core bonds isn’t a UST exclusive. Bund yields are set for a higher open as well. 2.55-2.58% serves as an important level in the 10-y yield. Today’s economic calendar could be of importance in sustaining that move as well as the recent dollar comeback. The US services ISM is expected to ease from 53.9 to 53. Strong demand (new orders in June picked up three points) at least suggests no imminent collapse in activity. The Bank of England also convenes today. The jury is still out whether the central bank will make use of one lower-than-expected June CPI reading to ease the tightening pace from 50 to 25 bps. There is also growing talk of a potential speedier rundown of the balance sheet. If the BoE opts for that, it will probably complement a 25 bps rate hike (to 5.25%).

News and views

Brazil’s central bank declared the fight against inflation over by cutting the policy rate yesterday 50 bps to 13.25%. The dovish shift came as inflation eased from a 12.1% peak in April 2022 to 3.2% in June this year. That’s below this year’s 3.25% target. The steep deceleration was the result of the central bank acting swiftly on the post Covid-19 inflation surge. It started hiking early in 2021. By contrast, the likes of the Fed and ECB only began in March and July 2022. The Banco de Brasil together with other Latin American counterparts were lauded for their quick response of which they are now reaping the benefits. The central bank said that if the scenario evolves as expected, more rate reductions of the same magnitude will follow. Analysts and markets were leaning more towards a 25 bps rate reduction, so there might be some price adjustment in the Brazilian real when market reopens today. USD/BRL started bottoming out end of July after hitting the 4.70 barrier. A first meaningful resistance pops up at 4.90.

Spain’s ERC leader Aragones said the socialist PSOE should not take support from Catalonia’s separatist parties to form a new government for granted. Its his first interview after the July national elections yielded no clear majority for the left nor the right blocs. That made the likes of the ERC and Junts kingmakers in the government formation. ERC supported Sanchez’ PSOE in the last parliament, Junts didn’t. But this time around, Sanchez needs them both. Aragones wants further talks on Catalonia’s political future, cut the region’s contributions to the national public fincanes and to take control of local train services. Junts for its part demands a referendum on independence and amnesty for all separatists facing legal charges related to the failed 2017 independence bid.