Sample Category Title

BoE to hike for sure, but by 25bps or 50bps?

BoE is widely expected to continue tightening today, though the extent of interest rate hike remains a point of contention. Markets currently slightly favor a 25 bps increment to 5.25%. However, a more aggressive 50bps hike to 5.50% cannot be entirely dismissed. The Bank's unexpected 50bps raise in June took markets by surprise, leading some economists to posit a strategic shift in the institution's response strategy. Conversely, CPI for June, which slowed more-than-expected to 7.9%, was perceived as a positive development by BoE policymakers, and could argue for a return to slowing tightening.

Regardless of today's decision, it is widely understood that this will not conclude the ongoing tightening cycle. Compared to ECB and Fed, BoE is anticipated to continue tightening for an extended period. Nonetheless, expectation of terminal rate has been fluctuating widely recently though, swinging from as high as 6.5% to 5.75% in a matter of weeks, suggesting a persisting uncertainty about the path ahead.

In addition to the anticipated rate decision, market observers will be closely watching two key aspects. First, today's voting could provide insight into the approach of MPC's newest member, Megan Greene, who recently succeeded known dove Silvana Tenreyro. If Greene presents a less dovish stance, Swati Dhingra may stand out as the only dissenter, making the vote an 8-1 majority.

Secondly, BoE is also set to release its new economic forecasts. Governor Andrew Bailey has repeatedly suggested that inflation is expected to decline fairly swiftly in the second half of the year, prompting keen interest in whether this prediction will still be reflected in the forthcoming projections.

Here are some readings on BoE:

- Will BoE Go Back to 25bps Interest Rate Increments?

- Bank of England Preview – Topside Risk to EUR/GBP With a Return to 25bp Steps

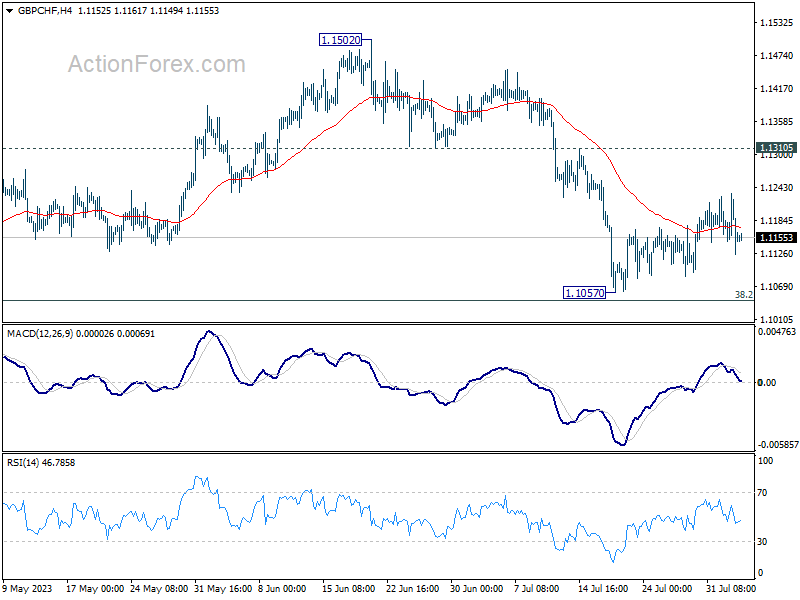

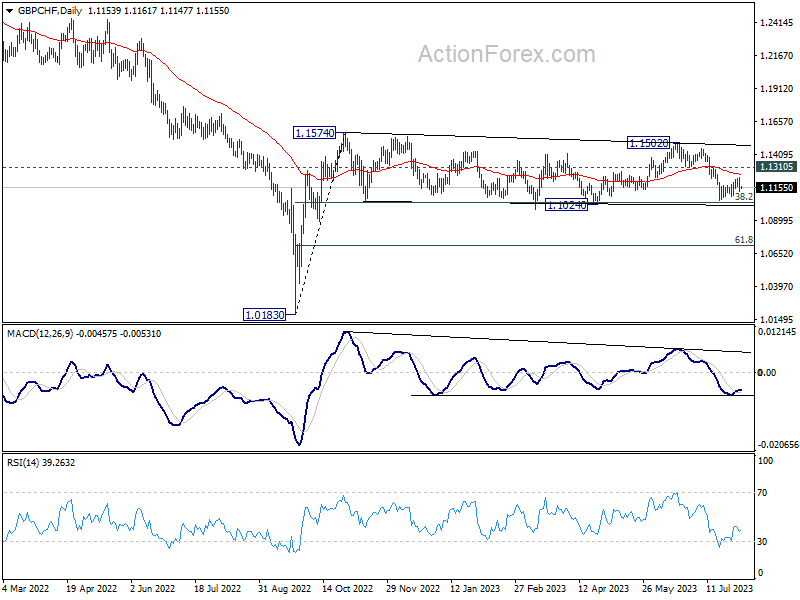

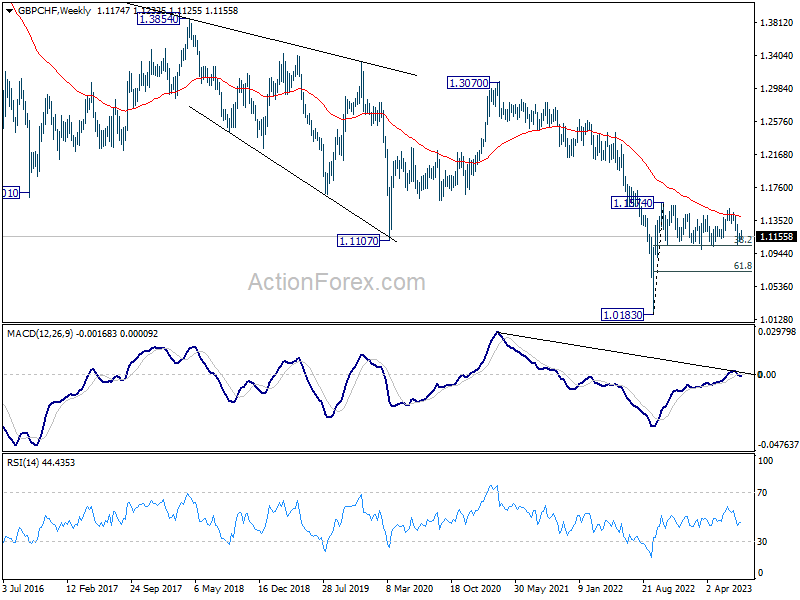

GBP/CHF's technical picture is mixed for now, with some dovish favor. From the near term angle, recovery from 1.1057 is clearly corrective looking, favoring a downside breakout. But the pair has been trading in medium term range of 1.1024/1574 since last October, keeping it neutral-at-worst. Yet, prior rejection by 55 W EMA is keeping the long term outlook bearish to neutral-at-best.

Still, further fall is more likely than not as long as 1.3105 support turned resistance zone. Decisive break of 1.1024 will bring deeper decline to 38.2% 1.0183 to 1.1574 at 1.0714 in rather quick manner. Let's see how GBP/CHF would reaction to today's BoE announcement.

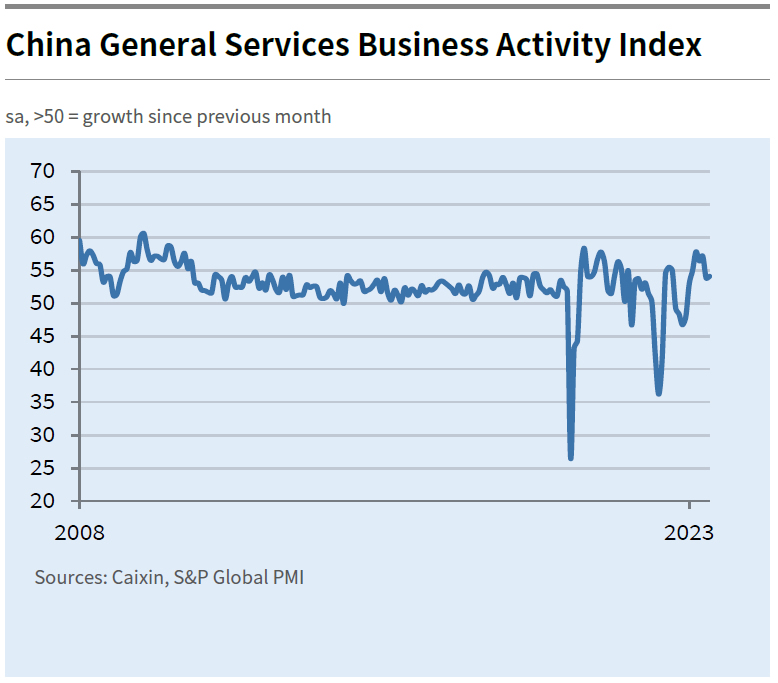

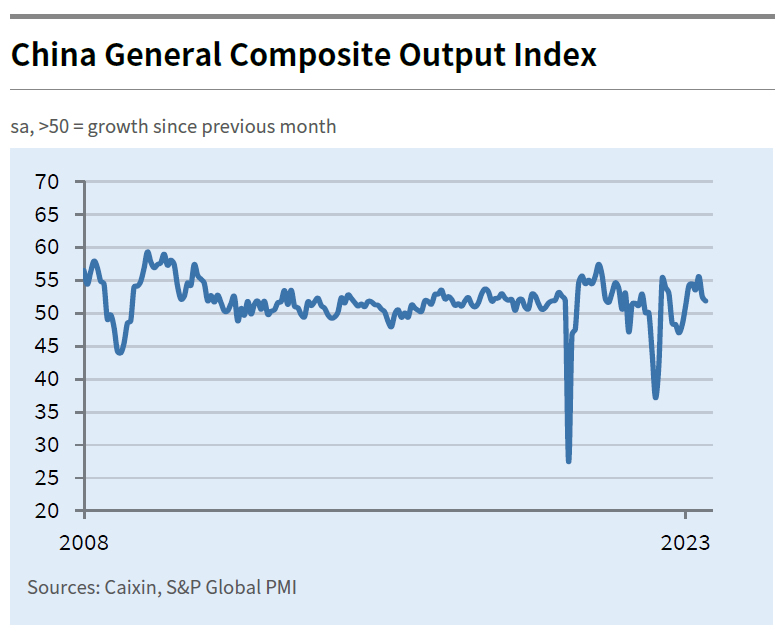

China’s Caixin PMI composite fell to 51.9, lowest since Jan

China's Caixin PMI Services increased slightly from 53.9 to 54.1 in July, surpassing the anticipated figure of 52.5. However, this reading fell short of the 55.5 average seen over the previous six months. Concurrently, PMI Composite dropped from 52.5 to 51.9, its lowest mark since January.

Commenting on the latest figures, Wang Zhe, a Senior Economist at Caixin Insight Group, expressed that the uneven recovery of the service and manufacturing industries remains a prominent concern. He noted, "Although the manufacturing sector was a drag, the steady expansion of the services industry still helped overall output, demand, and employment remain in positive territory."

The contraction in exports appeared pronounced, and while input costs saw a slight uptick, output prices registered a minor drop. Despite these challenges, expectations for future output remained on the optimistic side, though this metric recorded a new low since November.

On the broader economic landscape, Wang Zhe noted, "Although the data for industrial production and investment in June showed some signs of recovery, macroeconomic growth remained sluggish, and considerable downward pressure on the economy persisted."

Turning to policy recommendations, he emphasized the need for employment guarantees, stabilization of expectations, and boosting household income. He further argued that "At present, monetary policy only has a limited effect on boosting supply. An expansionary fiscal policy that targets demand should be prioritized."

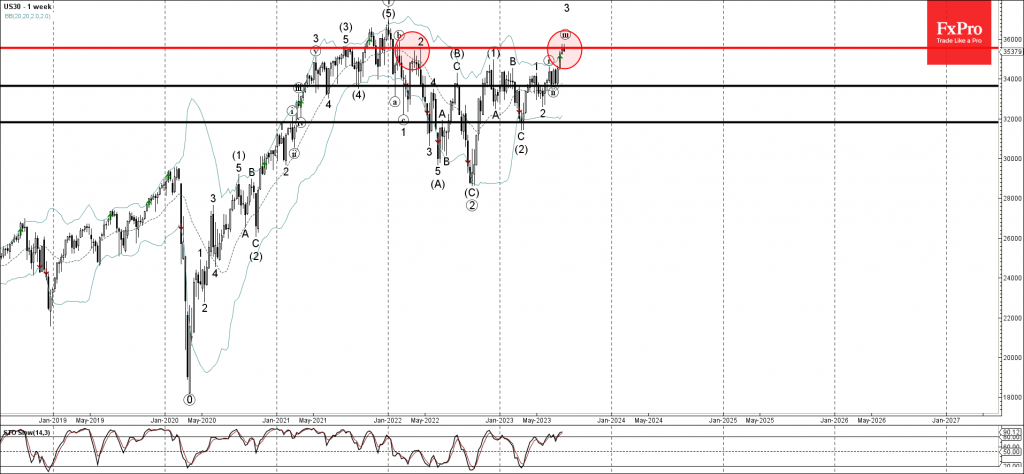

Dow Jones index Wave Analysis

- Dow Jones index reversed from major resistance level 35550.00

- Likely to fall to support at 34675.00

Dow Jones index recently reversed down strongly from the major resistance level 35550.00, which reversed the price multiple times from the start of 2022.

The resistance level 35550.00 was strengthened by the upper daily and weekly Bollinger Bands.

Given the strength of the resistance level 35550.00 and the overbought daily Stochastic increase the probability the index will fall further to the next support at 34675.00.

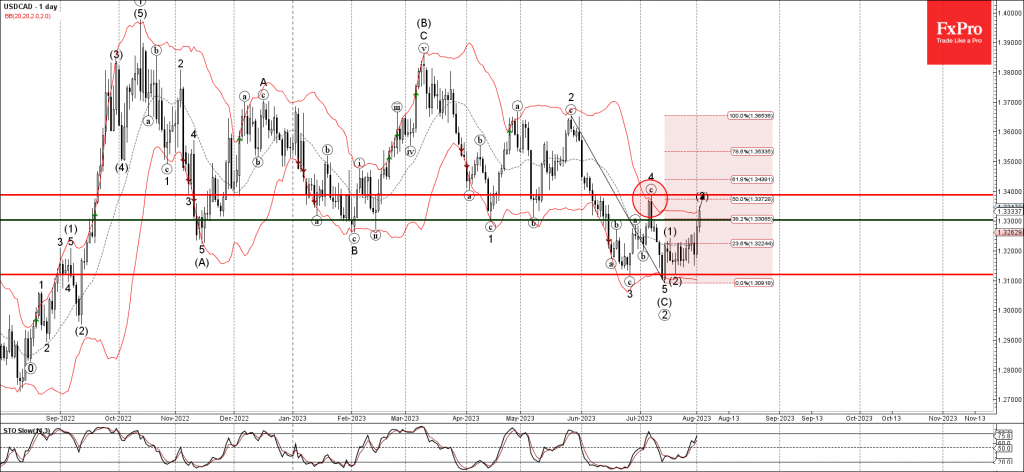

USDCAD Wave Analysis

- USDCAD broke resistance level 1.3300

- Likely to rise to resistance level 1.3400

USDCAD currency pair recently broke the resistance level 1.3300 intersecting with the 61.8% Fibonacci correction of the previous downward impulse from May.

The breakout of the resistance level 1.3300 accelerated the active intermediate impulse wave (3).

Given the clear daily uptrend, USDCAD currency pair can be expected to rise further toward the next resistance level 1.3400 (previous monthly high from July and the target for the completion of the active impulse wave (3)).

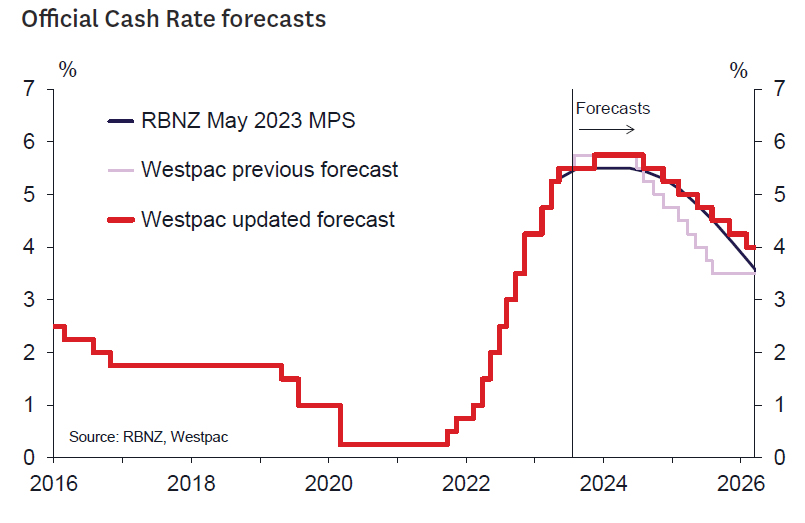

RBNZ to Hold in August; But a Hike Still Likely Before Year End

- We continue to see the RBNZ raising the cash rate to 5.75%, but in November instead of August.

- Evidence has accumulated suggesting persistent inflation pressures as feared.

- The economy is slowing from a very overheated position but is still growing.

- Even so, recent data have likely not been strong enough to overcome the RBNZ's strong bias to keep the OCR at 5.5%

- We think the theme of economic resilience and sticky inflation will persist and will eventually force the RBNZ to act.

- With the current sticky domestic inflation pressures likely to ease only gradually, we see a slow rate reduction cycle beginning in the second half of 2024.

Since May 2023, we have had the view that the RBNZ would need to tighten policy further to ensure a timely fall of inflation to the 1-3% target range. This view was predicated on a sense that current very high rates of inflation would be slow to recede and that risks to the inflation outlook were tilted to a slower-than-needed fall. Strong net migration was seen as supporting both the housing market and the economy right at the time the RBNZ would have hoped that growth would be quickly slowing and providing much needed disinflationary impetus.

In large part, the accumulated evidence has supported our view. While GDP in the March quarter was somewhat weaker than expected, we also can see tangible signs that strong migration is supporting the economy. The housing market has exhibited strength compared to the relatively dire predictions of commentators earlier this year. Business and consumer confidence have bottomed out and are staging a tentative recovery, which is unusual if the end of the tightening cycle has been reached. The labour market has been a particular area of strength. Employment growth has remained strong in defiance of concerns of a recessionary economy. Large numbers of migrants have found jobs in a labour market that, while better balanced than a year ago, remains tight. The strong labour market has meant that household incomes have continue to grow strongly, leaning against the considerable disinflationary impact of the RBNZ's 525 bps of interest rate increases delivered in recent years.

The June quarter CPI provided a timely reminder of upside risks to the inflation outlook. While annual headline inflation fell to 6%, in line with projections, lower imported inflation masked widespread and unexpectedly strong home grown non-tradables inflation. Non-tradables inflation is the part of inflation most impacted by RBNZ policy and fell only slightly to 6.6%. More generally, overall inflation remains far north of the promised land of the 1-3% target range. However, this strong and potentially concerning data needed to overcome the RBNZ's very strong bias to keep the OCR steady at 5.5% until the second half of next year. A high hurdle was in place, and we don't see the evidence as sufficient to move the RBNZ in August.

We retain confidence that recent trends will continue. The economy will likely continue to be supported by ongoing strong migration, the housing market will continue to strengthen, and inflation will only slowly moderate at current interest rates. We continue to doubt the economy will experience outright recession in the second half of 2023 as forecast by the RBNZ (although risks from the concerning situation in China and weaker agricultural commodity prices warrant keeping a close eye on that element of the forecast). But the data probably won't be sufficient to budge the RBNZ Monetary Policy Committee in August – so we must play the man (the MPC) as opposed to the ball on this one.

Our forthcoming August Economic Overview will describe our new forecasts in greater detail. However, the bottom line is that the interest rate reductions we had previously expected to occur in the second half of 2024 will likely now occur more slowly, consistent with the RBNZ only easing cautiously as inflation moderates slowly. We suspect many other central banks will be taking a similar, cautious approach.

The Next Key Data Releases that Could Allow ECB to Hike in September

The July central banks meetings lived up to expectations as both the Fed and the ECB announced their respective rate hikes but essentially removed their forward guidance. Data dependency is the new name of the game as the market is now counting down to the mid-September meetings. Which are the next key dates until the September 14 ECB gathering? What data figures would the ECB hawks like to see to push for another rate hike? Could the euro manage to defy expectations for a tough August against the US dollar?

ECB’s change of strategy

ECB's President Lagarde, representing the entire governing council, announced a strategy change, following nine consecutive rate hikes over the past 12 months, by moving to a data dependency stance. Using Lagarde’s own words, “data and our assessment of data will actually tell us whether and how much ground we have to cover”. The market obviously interpreted her message as dovish with the euro underperforming the dollar.

It has always been difficult for central banks to signal the likely end in their hiking (or easing) cycles as they have to maintain the fragile balance in their boards and avoid market disappointment. A big plus for Lagarde, compared to the Fed's Chairman Powell, is that she appears to have developed a decent relationship with the market in the current hiking cycle. This could prove crucial if the ECB decides to announce another rate hike at the September 14 gathering.

Key dates until the next ECB meeting

With data releases being the new compass for the ECB going forward, Table 1 below shows the key data releases and their respective dates up to the September ECB meeting.

What would the ECB hawks need to see to support a rate hike?

The ECB’s mandate remains price stability. Naturally, they are closely following all the inflation-linked data releases, indicators and projections. This framework includes market-based indicators like the 5year-5year inflation swaps, which remains elevated at 2.48%, the various business surveys and the famous ECB staff projections. Understandably, the market would be on its toes on the relevant dates as seen in Table 1 above. However, the key ones for the next 45 days are the August 23 release of the preliminary August PMIs (specifically, the prices paid subcomponent), and the German and euro area aggregate preliminary CPI prints for August on August 30/31.

A plethora of upside surprises could prove decisive for the September discussion. Especially if the headline euro area CPI stabilizes above 5% following an aggressive downward move since November 2022 and the core CPI indicator continues to confirm its stubborn nature. In addition, the ECB staff forecasts, to be released after the September 14 ECB meeting, play a key role in setting monetary policy. Therefore, the combination of strong inflation prints for August and the 2025 CPI rate staff projection remaining comfortably above the 2% threshold (it was seen at 2.2% at the June 2023 staff projections), could tip the balance in favour of another 25bps rate move.

Certain ECB members seem to care more about growth

Certain ECB members seem to be really concerned by the recent bad run of growth-related data releases, and particularly by the fact that Germany has been the growth laggard in 2023. It is worth noting that we are experiencing a rather rare occasion of France outgrowing Germany for three consecutive quarters. Therefore, ECB members will likely be all over the growth data as the final 2nd quarter GDP prints from Germany and the euro area aggregate are coming on August 25 and September 7 respectively. Stronger growth figures, especially in Germany, would really be welcomed by the ECB hawks.

Furthermore, the German IFO surveys, German factory orders and the various PMI surveys (especially the orders subcomponents) would undoubtedly be dissected by both sides at the ECB as they try to prop up their arguments for the September meeting. Especially in the case of the PMIs, the ECB hawks would really love the headline German manufacturing PMI to reverse its recent tanking and plot a course towards the 50-midpoint. Such a move would probably need further positive news from China, on top of the recent announcements that have not really caused much enthusiasm in the market.

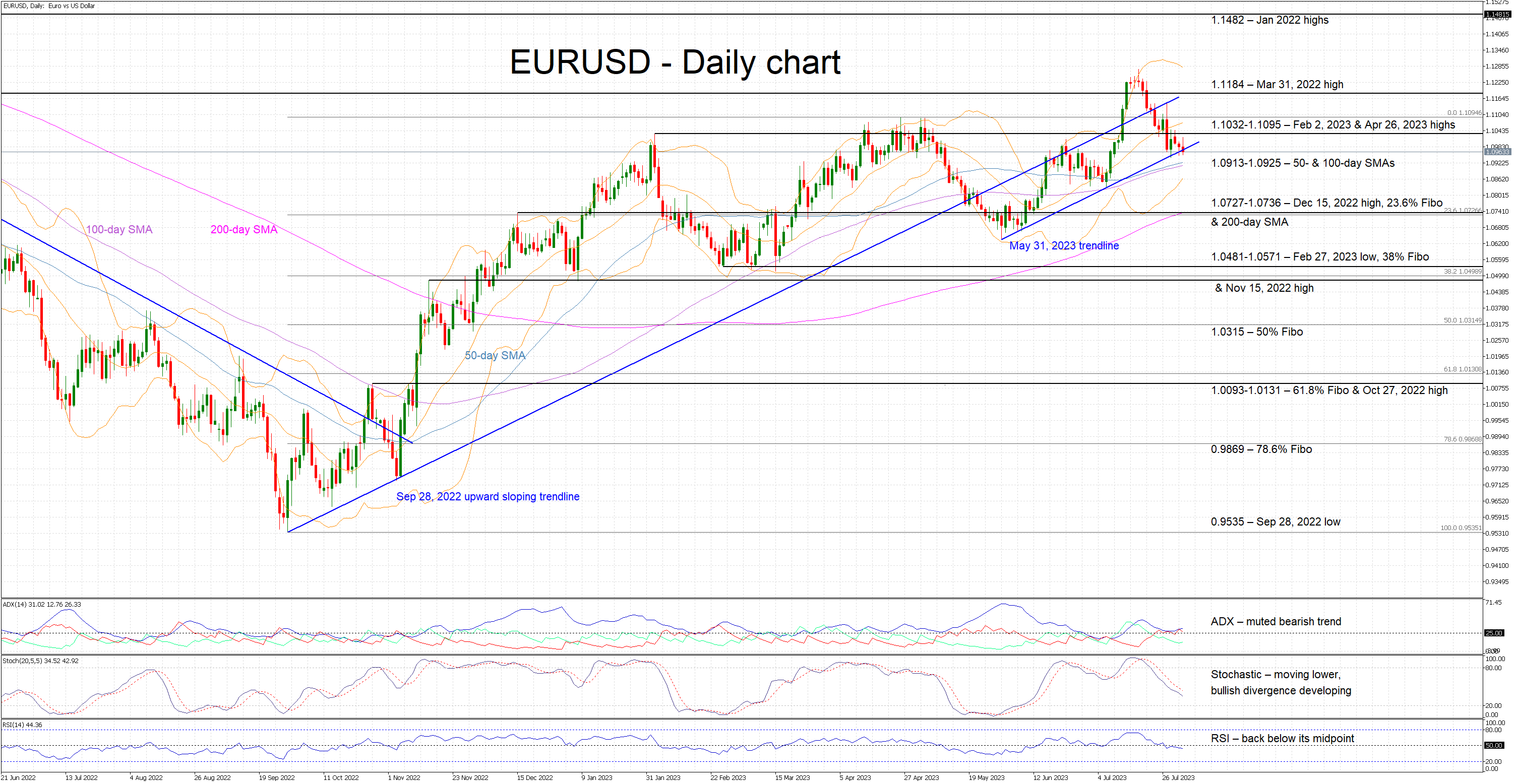

Euro would benefit from stronger data releases

The euro remains on the backfoot as the main driver of its recent performance was the market's confidence that the ECB will maintain its hawkish strategy. Removing this factor, the euro looks very vulnerable and thus raising questions for the viability of the long-term rally recorded against the US dollar since the September 28, 2022 low. A plethora of upside data surprises, particularly on the inflation front, could reenergize the euro bulls in recording a new 2023 high above the current one at $1.1275. On the flip side, the $1.0913-$1.0925 area is important from a short-term perspective as a break of this range would open the door to a more aggressive move towards $1.0727.

What To Trade In August?

As is the custom, every new month in the financial market often presents long-term, swing trading opportunities for traders like you and me. Even better, FBS is usually there to provide insights into the expected trading opportunities through such analytical pieces as this. So, keep reading, and let’s review a few of these trade ideas together.

GBPJPY - D1 Timeframe

As I mentioned in a recent article, GBPJPY, after having broken out of a consolidation channel, returned for a retest of the turncoat trendline, which it had initially broken below. As a result, I expect a reaction from the supply zone to confirm my bearish sentiment and present me with reliable entry criteria. The rejection from that supply zone is the final piece of the puzzle I would be waiting for.

Analyst’s Expectations:

- Direction: Bearish

- Target: 174.671

- Invalidation: 184.168

GBPAUD - D1 Timeframe

GBPAUD is retesting a major supply zone extending to the monthly timeframe. The initial movement had been rejected from the supply zone and trendline resistance earlier, so I expect to see a further drop from the same zone. Although the market is yet to present a proper break of structure, the price would nonetheless reach for the trendline support and the demand zone below it.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.87287

- Invalidation: 1.94012

GBPUSD - D1 Timeframe

GBPUSD recently broke out of a consolidation channel and has completed a retest of the said trendline. Looking at the current price action, the break of structure, and the trendline retest, I expect to see a continuation of the downward movement. The rejection from the trendline is expected to push prices further down toward the demand zone between the 50 and 100 period moving averages.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.27000

- Invalidation: 1.28760

CONCLUSION

The trading of CFDs comes at a risk. Thus, to succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.

Sunset Market Commentary

Markets

Fitch’s US rating downgrade from the top AAA to AA+ (stable outlook) didn’t go uncommented. Fitch cited a worsening budget situation, a high and growing debt burden and an erosion of governance (ie. narrowly avoiding a default as debt ceiling discussions get resolved at the eleventh hour) as reasons for the move. US Treasury Secretary Yellen already yesterday evening lashed out at the rating agency, calling its decision arbitrary and based on outdated data. Prominent economists including former Treasury Secretary Summers said that there are indeed reasons to be concerned about the long-run trajectory of the US deficit but added that the country’s ability to service debt wasn’t in doubt. Others were “puzzled” about the “strange move”, and shouldn’t impact markets much. Evidence from the past (eg. with S&P 2011 US rating cut) indeed shows effects, if any, are limited and temporary. The largest moves were visible on equity markets. In Asian dealings, stock indices lost up to 3% and more. European markets opened lower and then extended losses up to 1.75% (EuroStoxx 50) before paring them to about 1% currently. We nevertheless feel that the Fitch decision was seen as an excuse for some profit-taking after a strong July month rather than anything else. US equity futures also pared their losses, resulting in a lower opening of 0.4-1.3%. US government bonds at the center of all the fuzz at first … strengthened. Marginally, but still. That too is a copy paste of the 2011 script, when rating agency S&P also lowered the US’s AAA rating a notch over the debt ceiling. Back then, US bonds outright surged although circumstances were not all the same (European debt crisis, ultra-low policy rates, Fed shortly after announced a second round of “Operation Twist”). The minor UST advance was later undone by a strong ADP job report though. Some 324k jobs were created in July, crushing consensus for 190k. The figure for June saw a downward 42k revision but does little to counterbalance the big beat. Leisure and hospitality (+201k) are again driving growth, ADP said. It added that manufacturing remains a point of weakness, with the interest-rate sensitive industry shedding jobs for the fifth month straight (-36k). “The economy is doing better than expected and a healthy labor market continues to support household spending. We continue to see a slowdown in pay growth without broad-based job loss.”, the ADP chief economist summarizes. US yields currently add 2.1-7.8 bps across the curve with the 10-y moving further north of the 4% barrier. German Bunds hugely outperform by shedding 2.4-7 bps. The dollar rose against most peers, including the euro – even as the common currency was doing pretty well itself. EUR/USD loses further territory towards 1.095. DXY extends a winning streak to 102.5. Cyclicals and other more risky currencies including AUD, NZD and SEK all feel selling pressure as does sterling. EUR/GBP rises well above 0.86(2). News & Views

The Bank of Japan’s deputy governor and one of the key policy architects said Friday’s tweak to the yield curve control programme should not be seen as moving towards an exit from its ultra-easy stance. It is aimed at “patiently continuing with monetary easing”. He also pushed back against any expectations for a rate hike soon, saying that would mean the BoJ is in a state where it needs to cool the economy to address high inflation. The latter is still well above the 2% target but the central bank holds on to the view that it is the result of cost-push factors. Since Friday’s tweak, the Japanese 10y yield surged beyond 0.60%. The move was so abrupt the BoJ intervened on Monday with unscheduled bond buying. Uchida said there is no specific level at which the BoJ would step in again. He did say that they will, depending on the speed at which it is reaching 1% (the de facto new 10-y rate cap). The 10-y yield today adds another 2 bps to 0.638%, the highest in nine years.

The US Treasury boosted the auction size for the upcoming August-October quarter compared to the May-July quarter as it seeks to restore its depleted cash balance and to fund a bigger than in May expected deficit. It is the first time it did so in over two years. For maturities from 2y up to 7y, the size will increase between $1 bn to $3 bn in every month from August on. Maturities from the 10y over 20y to 30y will get a significant one-time boost this month before scaling down by $3 bn again for the final two months of the quarter. The US next week kicks off its mid-month refinancing operation through a 3-y, 10-y and 30-y auction. The combined surplus compared to the first month of the previous quarter amounts to $7bn (or $103 bn in total).

Swiss Franc Eases Ahead of Swiss Inflation Report

- Swiss inflation projected to fall to 1.6%

- ADP Employment blows past estimate

The Swiss franc has extended its losses on Wednesday. In the North American session, USD/CHF is trading at 0.8795, up 0.50%.

Swiss inflation expected to fall to 1.6%

Swiss National Bank President Jordan has often complained that inflation remains too high, although other central bankers, who are grappling with much higher inflation, would be happy to change places. I suppose that Jordan would grudgingly admit that the inflation picture has brightened. Inflation fell to 1.7% in June, as both the headline and core rates dropped into the Bank’s target range of 0%-2% for the first time since January 2022. The good news is expected to continue on Thursday, with Swiss inflation projected to tick lower to 1.6% in July.

Although Switzerland’s inflation picture is looking bright, the SNB is still expected to go ahead with a rate hike at the meeting on September 21st. The SNB is concerned that inflation could reverse directions and rise to 2% by the end of the year, due to rising services inflation and higher mortgage costs. Inflation may continue to decelerate in July, but the SNB could dismiss the downswing as temporary and decide to keep raising rates.

Investors will be keeping a close eye on US employment releases over the next few days. The ADP Employment report kicked off a host of job releases, highlighted by nonfarm payrolls on Friday. ADP looked sharp with a gain of 327,000 for July, below the June reading of a revised 455,000 but easily beating the consensus estimate of 189,000. A month ago, the sizzling ADP reading made headlines and raised speculation that nonfarm payrolls might follow suit with a strong release. In the end, nonfarm payrolls fell significantly, as expected. It remains to be seen whether NFP will deliver another soft reading or will it follow ADP and surprise with a banner reading.

USD/CHF Technical

- USD/CHF is testing resistance at 0.8776. The next resistance is at 0.8848

- 0.8665 and 0.8593 are providing support