Sample Category Title

Week Ahead – NFP Report to Probably Steal the Limelight from BoE and RBA

The Bank of England and Reserve Bank of Australia will wrap up the summer central bank decisions in the coming week, although the US jobs report may attract the most attention. The ISM PMIs will be the other highlights in the United States, while employment numbers are due in Canada and New Zealand too. Over in Europe, the agenda will be dominated by flash inflation and GDP data. Oil will also be in the spotlight as the OPEC+ alliance holds its monthly meeting.

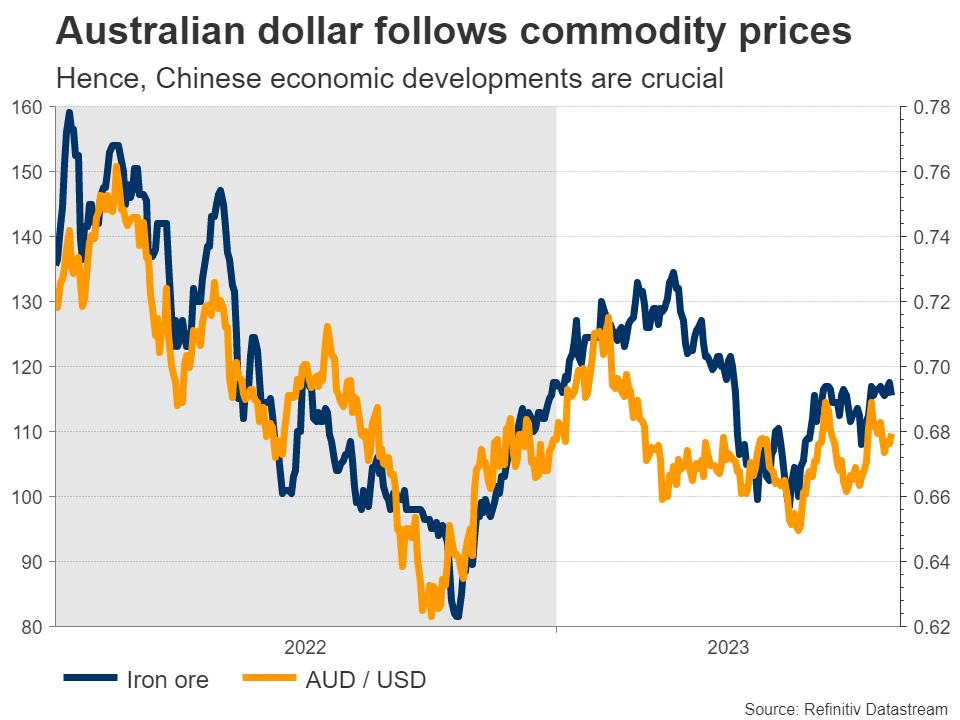

Another close call for the RBA?

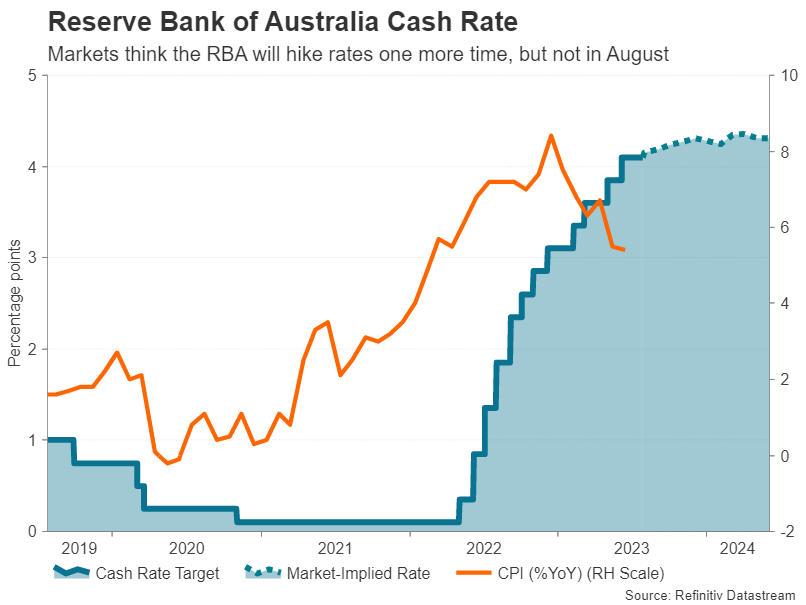

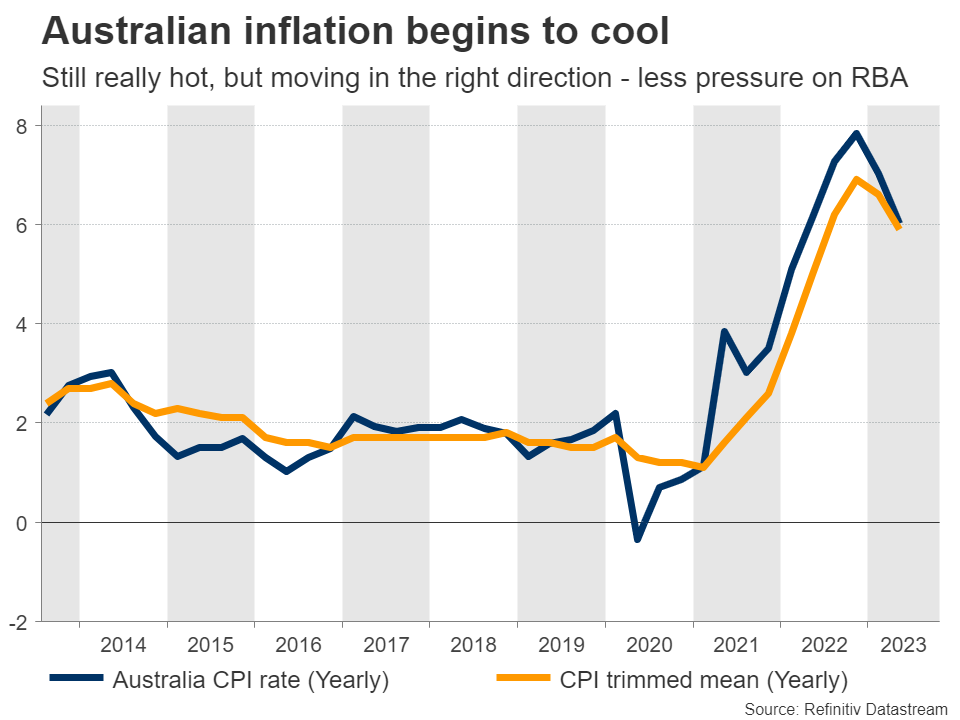

The Reserve Bank of Australia meets on Tuesday for its August policy decision and markets and economists are split as to what the outcome will be. Analysts are predicting a 25-basis-point increase in the cash rate to 4.35% following a pause in July. However, the minutes of the July meeting revealed the decision was a close call and that the Board would “reassess the situation” in August.

The Bank will publish updated economic projections on Friday but it’s doubtful how much clarity they will provide. Economic data has been somewhat mixed lately – the jobless rate dipped to 3.5% in June, but inflation also fell more than expected, with CPI cooling to 6.0% year-on-year in Q2.

However, other indicators have been gloomier as the manufacturing and services PMIs both contracted in July. That’s why the markets aren’t convinced that policymakers will press the hike button, although they do foresee one final 25-bps increase over the next nine months. But there is reason to be optimistic as Australian exporters stand to benefit from China’s renewed efforts to stimulate its economy.

Therefore, if policymakers choose to stay on the sidelines for another meeting, the decision might not be very negative for the Australian dollar as a hawkish hold is the most dovish scenario. But neither are they likely to close the door to additional hikes if they decide not to wait and raise rates next week, boosting the local dollar.

The aussie could also gain if the PMIs out of China show some improvement in July. The official manufacturing and non-manufacturing PMIs are out on Monday, while the Caixin manufacturing and services PMIs are due on Tuesday and Thursday, respectively.

BoE to downshift again

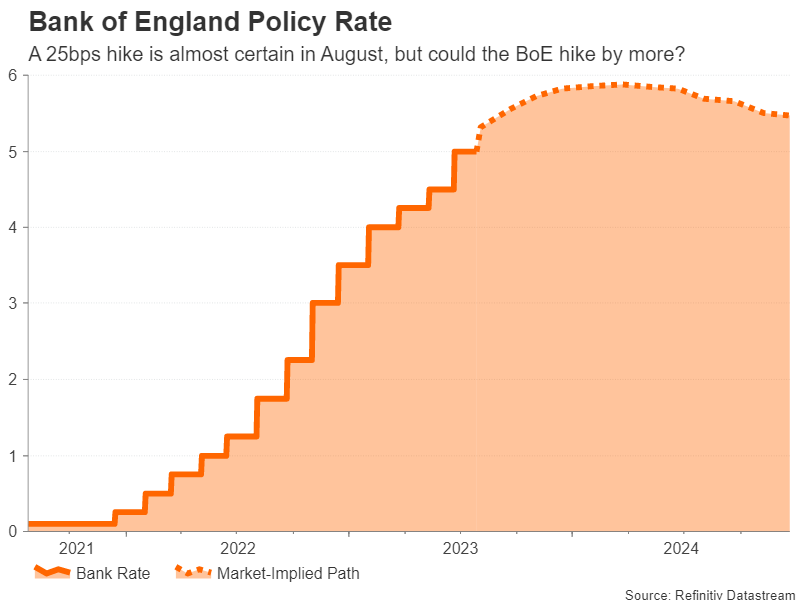

The Bank of England is certain to raise the Bank Rate again when it meets on Thursday but there is less confidence about the size of the hike. A 25-bps increase is fully baked in, but markets have assigned around a 30% probability of a larger 50-bps move. Following the June inflation figures when UK CPI finally tumbled below 8% and core CPI eased too, the arguments for a second consecutive double hike have weakened considerably, and even more so after the recent dismal PMIs for July.

Very poor flash PMI estimates tend to get revised up and that could happen when the final readings are released on Tuesday (manufacturing) and Thursday (services). However, the UK economy is clearly struggling amid a slowdown in its biggest trading partners and households being squeezed from soaring mortgage costs. Hence, the Bank of England is unlikely to go big even as it stresses the need for further tightening.

In the event that the BoE doesn’t surprise, what might be more relevant for the pound is the BoE’s latest set of inflation forecasts, in particular, how fast it sees CPI falling to the 2% target.

Is the US labour market coming off the boil?

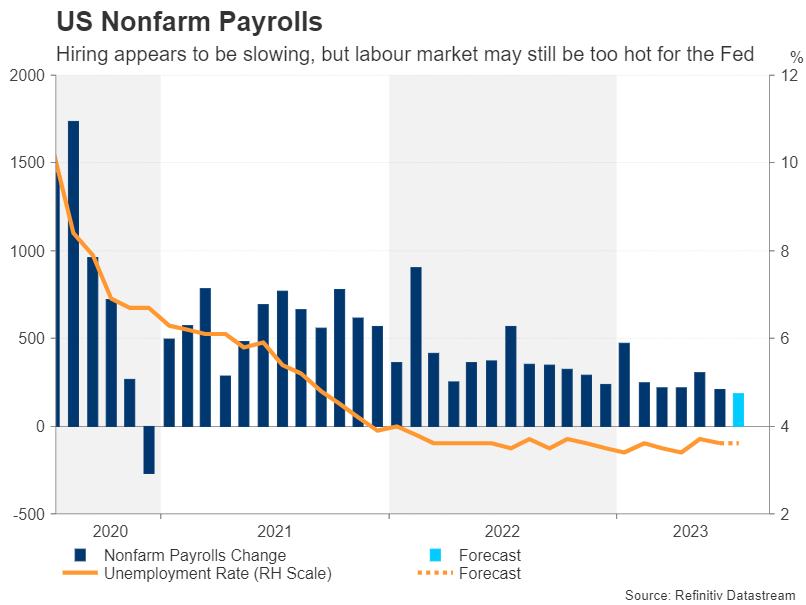

The Fed decision may be out of the way but the upcoming jobs report could prove more vital for the markets as Powell kept his options open for the September meeting. The jobs market in America has been steadily losing steam this year but not nearly fast enough to ease concerns about a wage-price spiral. However, the Fed may finally be getting what it wants as employment grew at the slowest pace in two-and-a-half years in June and that trend likely continued in July.

Nonfarm payrolls are expected to have risen by 184k in July, down from 209k previously. The unemployment rate is forecast to have held steady at 3.6%, while average earnings probably kept growing by slightly more than 4% y/y.

The weekly jobless claims have been edging lower for most of July so a positive NFP surprise is possible, though the markets might not necessarily welcome a strong print as it would bolster the case for a September rate hike.

Investors will be able to further scrutinize the US labour market with Tuesday’s JOLTS job openings and Wednesday’s ADP employment report. Other data will include the Chicago PMI on Monday and factory orders on Thursday.

But aside from the payrolls numbers, what could move the US dollar the most are the ISM PMIs on Tuesday (manufacturing) and Thursday (non-manufacturing). Like in Europe, the US manufacturing sector has been in recession this year but in stark contrast, the services economy has continued to expand, and the non-manufacturing PMI unexpectedly bounced higher in June.

With the Fed undecided about whether to raise rates again, the incoming data could swing the odds in the dollar’s favour if they are stronger-than-expected.

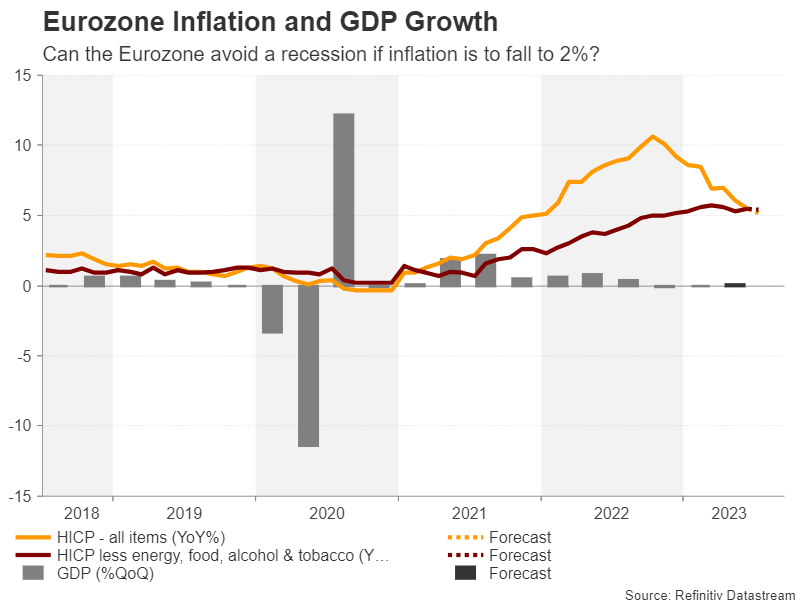

Euro eyes flash CPI as ECB ponders pausing

The European Central Bank made a dovish turn this week by not committing to further rate hikes. The change in stance came on the back of softer inflation readings as well as growing signs that the Eurozone economy could be headed for a recession.

Monday’s flash CPI numbers for July will therefore be crucial in shaping expectations about additional rate hikes in the euro area this year. The headline rate of inflation slipped to 5.5% y/y in June and is projected to fall again to 5.3% in July to a one-and-a-half year low.

However, underlying inflation is proving to be a lot stickier as core CPI that excludes all volatile items such as food and energy edged up in June to 5.5%. It is forecast to inch lower to 5.4% in July, but any upside surprises could lead to some scaling back of bets that the ECB is done raising rates.

Preliminary GDP estimates for the second quarter are also released on Monday. Economic growth was flat in the first quarter, but GDP likely managed a modest expansion of 0.1% in the three months to June.

With future rate hikes hanging in the balance, the euro will be very sensitive to price and growth indicators in the run up to the September meeting.

More data and an OPEC meeting

Elsewhere, CPI numbers will be watched in Switzerland on Thursday and New Zealand’s quarterly jobs data will be important for the kiwi early on Wednesday. Meanwhile, Canada will get employment figures too for July on Friday.

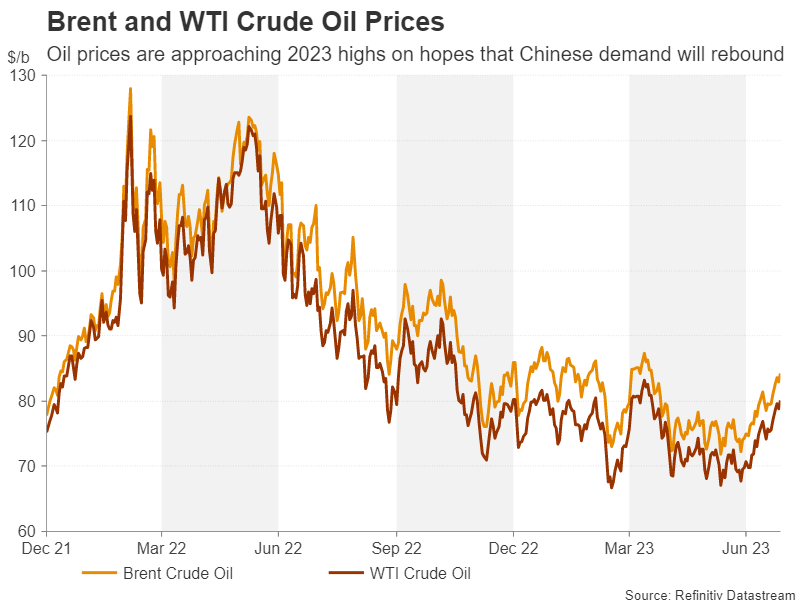

Another solid labour market report could boost the odds of one more rate increase by the Bank of Canada this year, lifting the loonie. On the other hand, the Canadian currency will likely shrug off a meeting of OPEC and non-OPEC countries on Thursday as the major oil producers are not expected to announce any significant changes to their output quotas. Oil futures have been rallying lately following the previously announced cuts by Saudi Arabia and Russia, but also on the hopes that more pro-growth policies in China will buoy demand.

RBA Unlikely to Raise Rates, But Might Sound Hawkish

The Reserve Bank of Australia (RBA) will conclude its latest meeting at 04:30 GMT Tuesday. Economic developments have been mixed lately, so markets are only pricing in a 20% probability for a rate increase. As for the Australian dollar, the most crucial variable might be the power and scope of China’s stimulus measures, instead of any domestic developments.

Mixed news

The Australian economy has displayed some mixed signs lately. On the bright side, the labor market is exceptionally tight, with the unemployment rate hovering near its lowest levels in five decades.

In addition, the prices of commodities that Australia exports have started to recover, encouraged by the promise of new stimulus measures in China, who is the world’s largest consumer of commodities and also Australia’s biggest trading partner.

Meanwhile, inflation seems to be cooling down. The CPI rate for the second quarter clocked in at 6%, which is still very elevated but a clear improvement from the 7% in the previous quarter. While services inflation and rents remain extremely hot, those pressures have been partially negated by a sharp cooldown in the prices of goods.

The problem is that business surveys point to a slowdown in economic growth moving forward. In July, the composite PMI fell into contractionary territory - a warning sign that economic activity is losing steam as higher borrowing costs begin to bite consumers.

RBA decision

Turning to the upcoming meeting, market participants think the most likely outcome is that the RBA does not raise interest rates, with the implied probability for no action standing at around 80% and the chance of a rate hike near 20%.

This pricing seems fair. Inflation is cooling off and business sentiment is worsening, so there doesn’t seem to be any real urgency for the RBA to push the rate-hike button again.

Yet, the central bank might strike a relatively hawkish tone, keeping the prospect of future action alive. With the labor market so tight, there’s a concern that wage pressures could intensify, keeping the inflationary fire burning for some time. Similarly, there’s a risk inflation could receive a second wind if China rolls out a strong stimulus package.

Bearing everything in mind, the most sensible strategy might be for the RBA to keep rates unchanged but signal that the tightening cycle is not over yet. Such a combination could inject volatility into the markets.

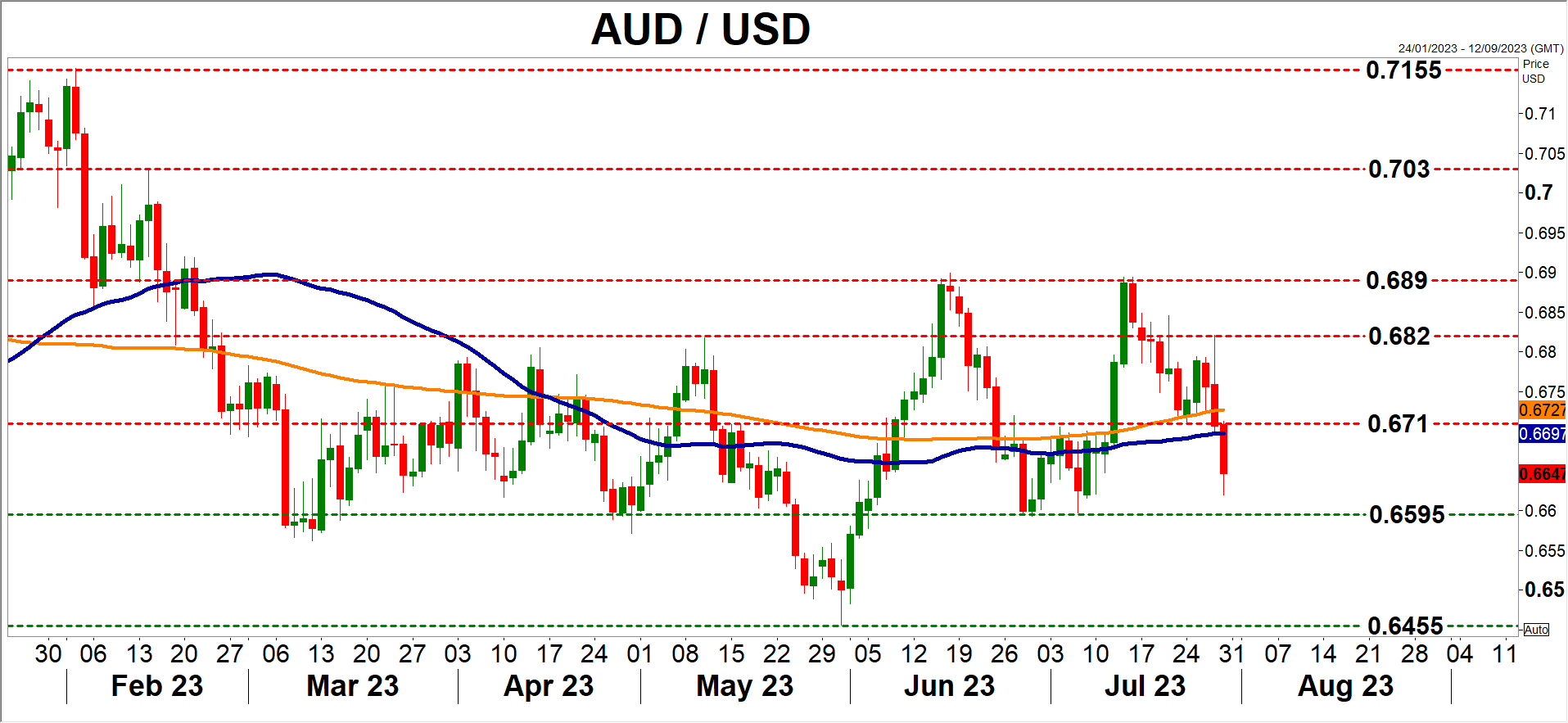

The initial reaction in the aussie might be negative in case rates are kept unchanged, although any weakness could be short-lived and even reverse if the RBA strikes a hawkish tone.

Looking at the charts, the levels in aussie/dollar that could come into play in this scenario are 0.6710 on the upside and 0.6595 on the downside. Overall, the pair has been in a downtrend since early 2021 and it would take a clean break above 0.7160 to change that.

China matters most

In the big picture, the main driver for the aussie might be how the Chinese economy evolves, not what the RBA does. Markets know that the central bank is close to the end of its tightening campaign, even if it raises rates one final time.

On the other hand, there’s a lot of uncertainty surrounding China. Beijing has promised stimulus measures to boost domestic consumption, as the economy struggles with a slowdown in the manufacturing and real estate sectors, but hasn’t announced anything specific yet.

The details and scope of these measures will be extremely important for commodity prices, and by extension, for the commodity-sensitive Australian dollar. A round of powerful stimulus would likely propel the currency higher, but if Chinese authorities underwhelm, the aussie could suffer collateral damage.

Until there is some clarity on this subject, it’s difficult to get too excited about the aussie.

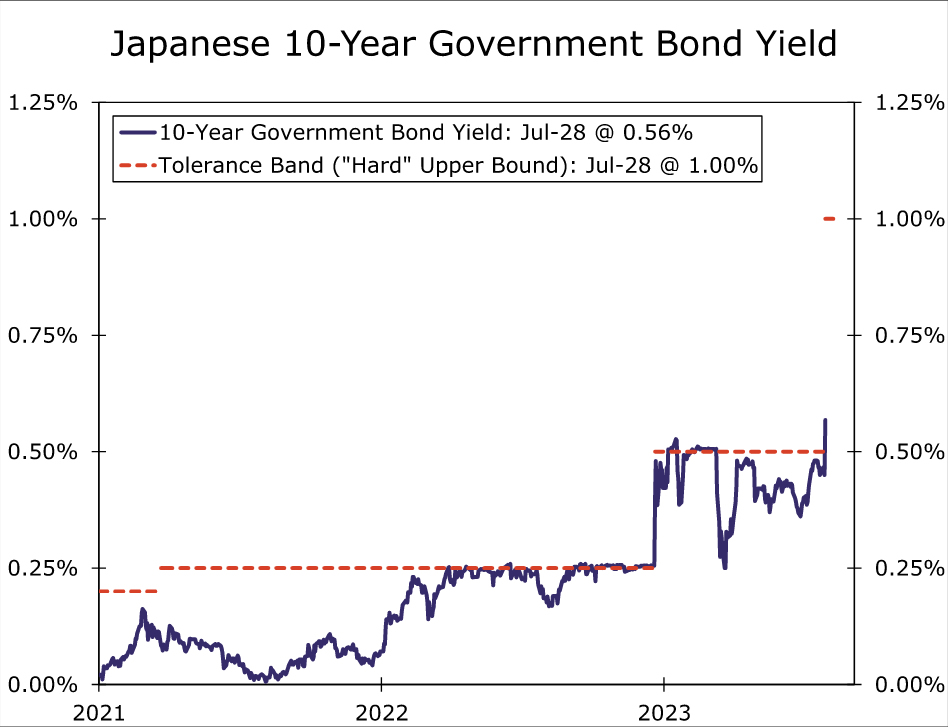

Bank of Japan Delivers Another Hawkish Policy Tweak

Summary

- The Bank of Japan (BoJ) sprung a surprise at today's monetary policy announcement, delivering another hawkish tweak to its Yield Curve Control policy. While the BoJ did not change its main policy parameters, it said it would conduct yield curve control with greater flexibility, regarding the upper and lower bounds of the range as references, not as rigid limits, in its market operations.

- The BoJ also said it would offer to buy 10-year JGB's at 1.00% every day through fixed-rate purchase operations if needed. In effect, the change means the Bank of Japan will cap 10-year JGB yields at 1.00% or, perhaps more accurately and in reality, somewhere between 0.50% and 1.00%.

- Overall, we view today's policy adjustment as primarily driven by operational and tactical considerations. From a purely economic perspective, we think the case for a further shift to less accommodative monetary policy is growing but not yet overwhelming. From an operational perspective we also see limited likelihood of a further policy adjustment for now if, as we expect, global tightening is near an end, meaning global bond yields could stabilize and eventually move lower. Against this backdrop, we see Bank of Japan monetary policy as on hold for the foreseeable future, and certainly at least for the rest of 2023.

Bank of Japan Loosens Grip on Long Term Bond Yield

The Bank of Japan (BoJ) sprung a surprise at today's monetary policy announcement, delivering another hawkish tweak to its Yield Curve Control policy, a move that occurred a little sooner than the October adjustment we had forecast. With respect to its main policy parameters, the BoJ held its Policy Balance Rate at -0.10%, and said it would continue to target a 10-year Japanese Government Bond (JGB) yield of 0% with a fluctuation range of +/- 50 bps. Importantly however, the BoJ said it will “conduct yield curve control with greater flexibility, regarding the upper and lower bounds of the range as references, not as rigid limits, in its market operations.” The Bank of Japan also said it would offer to buy 10-year JGB's at 1.00% every day through fixed-rate purchase operations if needed. In effect, this change means the Bank of Japan will cap 10-year JGB yields at 1.00% or, perhaps more accurately and in reality, somewhere between 0.50% and 1.00%.

In our view, a cap of “somewhere between 0.50% and 1.00%” reflects comments from BoJ Governor Ueda, who said that depending on the situation yields could go beyond 0.50%, but that he didn't expect long-term yields to get to 1.00%, nor did he think it was appropriate for yields to get to 1.00%. Ueda added that he did not view the move as a step towards normalization. The BoJ's modestly upgraded economic projections also suggest only a moderate increase in the 10-year JGB cap to “somewhere between 0.50% and 1.00%”, with inflation not yet seen rising sustainably above 2%. The BoJ raised its core CPI forecast for FY2023 to 2.5%, but lowered in core CPI forecast for FY2024 slightly to 1.9%, while keeping at 1.6% for 2025. The central bank did however acknowledge that the risk to its inflation forecasts were to the upside. Separately, the BOJ lowered its GDP growth forecast for FY2023 slightly to 1.3%.

Overall, we view today's policy adjustment as primarily driven by operational and tactical considerations, and against that backdrop, do not expect the BoJ to follow up with another policy adjustment in the near-term. From a purely economic perspective, the case for less accommodative monetary policy is growing but not yet overwhelming, in our view. With respect to economic growth prospects, it is true that Japan started 2023 on a firm footing, with Q1 GDP growing at 2.8% quarter-over-quarter annualized and the Q2 Tankan survey hinting at ongoing growth through the first half of the year. However, while wage growth has quickened it has not kept pace with the increase in prices, meaning that in real or inflation-adjusted terms, trends in employee compensation and household income have turned negative. The negative income trends could eventually restrain the consumer, and see Japan's economy lose momentum over time. We also expect inflation to recede, and indeed the Bank of Japan's own forecasts see inflation slowing back below 2% over the medium-term. Thus, from an economic perspective we do not see a strong rationale to tighten policy in the period ahead. From an operational perspective, we also see limited likelihood of a further policy adjustment for now. If, as we expect, global monetary policy tightening comes to an end in the immediate months ahead, upward pressure on global bond yields should ebb and, global bond yields could start moving lower. In this environment we would not expect 10-year Japanese government yields to rise close to the “hard” yield cap of 1.00% for the time being, and therefore do not envisage any significant new operational challenges for the Bank of Japan in terms of implementing monetary policy. Against this backdrop, we see Bank of Japan monetary policy as on hold for the foreseeable future, and certainly at least for the rest of 2023.

US: Consumer Spending Grows, Even as Prices Remain Elevated in June

Personal income grew 0.3% month-on-month (m/m) in June, which was below market expectations for 0.5% growth. This marked a deceleration from the prior month's gain of 0.5%. Gains were led by compensation to employees, which also rose by 0.5% for the third consecutive month.

Accounting for inflation and taxes, real personal disposable income rose 0.2% m/m, slightly slower than the 0.4% growth posted the previous month.

Personal consumption expenditures rose 0.5% m/m, a marked acceleration from the 0.2% gain in May (revised higher from 0.1%). June's reading came in just above market expectations for 0.4% growth.

- Expenditures on services grew 0.4% m/m for the second consecutive month. Spending on financial services and insurance, housing and utilities, and recreation were the primary contributors to movements in the services category.

- There was also an increase in goods spending. Goods spending rose by 0.8% m/m, a rebound from the 0.3% decline posted in May. There was an improvement in spending on both durables (1.4%) and non-durables (0.5%)..

Adjusting for inflation, real spending grew 0.4% for the month, coming in just above the consensus estimate for a 0.3% gain. In real terms, goods spending was up 0.9% m/m, while services were up a more muted 0.1%.

The personal consumption expenditure (PCE) price deflator rose 0.2% m/m, and 3.0% on a year-on-year (y/y) basis – right in line with market consensus forecast and below May's reading (3.8% y/y).

The core PCE price deflator (which excludes food and energy and is the Fed's preferred measure of inflation) rose 0.2% m/m, again in line with the consensus forecast and below May's reading (0.3%). On an annual basis, core PCE inflation decelerated to 4.1% y/y from 4.6% y/y the month prior (consensus forecast was 4.2% y/y). This is the first time in the last seven months that the measure has gone below 4.6%.

The personal saving rate was 4.3% in June, which was 0.3%-pts below the 4.6% reading in May.

Key Implications

U.S. households were feeling optimistic in June, and it showed in their spending. Despite high prices and tightening credit conditions, consumers did their part to keep economic growth in positive territory. As such, growth in real consumption expenditure for 2023 Q2 was 1.6% annualized (down from 4.2% in 2023 Q1), and was the primary contributor to the above-expectations 2.4% (q/q annualized) growth in real GDP. Services spending did most of the heavy lifting, but goods spending also lent a helping hand.

On the prices side, inflation has been trending in the right direction, but the Fed is yet to be convinced of its staying power. With its preferred measure still hovering above 4%, the Central Bank delivered on its promise, raising its policy rate this week to a 22-year high. The Fed's task is complicated by the fact that real incomes are rising, which keeps the spending power of consumers intact. While good for consumers, it continues to complicate the Fed's task of bringing inflation in line with target. Still, a resilient consumer and strong labor market increase the odds that the Fed will eventually get to target without tipping the economy into a recession. The Central Bank may just have to exercise a bit of patience in the interim.

Sunset Market Commentary

Markets

The first ECB governors came to speech in the wake of yesterday’s policy meeting. Muller kicked off by saying that previous rate increases are having an impact and that next decisions are no longer obvious. Vasle and Simkus joined by adding that September could either be a hike or a pause, depending on the data. Kazimir struck the most hawkish cord. Core inflation remains too high and risks are still clearly tilted to the upside, he said. He does acknowledge that the latest hike to 3.75% brought the ECB close to the peak. Germany’s Nagel also referred to stubborn core inflation but kept an open mind on whether to hike or pause in September. France’s Villeroy repeated the “data dependence” code the ECB now lives by. Both him and Nagel stressed the need for keeping rates high for long enough. Acting on the quotes proved tricky with a slew of European data scheduled for release though. Several euro area member states published July inflation numbers, including Spain (2.1%, up from 1.6% with core rising too), Germany (6.5% from 6.8%), France (5% from 5.3%) and Belgium (4.14% from 4.15%). Data from the first printed higher than expected while our neighbours in the south and east missed the bar by the tiniest margin. The latter two also published a first Q2 growth estimate. France crushed the bar by growing a nice 0.5% q/q (0.9% y/y). Germany stagnated but saw its Q1 figure revised upwards from -0.3% to -0.1%. Belgium’s economy grew a meagre 0.2%. Services single-handedly support growth with the industry still teetering. As if a clean markets response wasn’t already difficult enough, US data came interfering too. The all-important Employment Cost Index (+1% q/q in Q2) rose less than the 1.1% consensus. June income and spending data were about in line with expectations, considering the upward revisions to the previous month. PCE deflators were spot on (0.2% m/m, 3% y/y) with the core gauge slightly less than anticipated in the yearly print (0.2% m/m, 4.1% y/y).

The data in general confirm markets’ current belief that tightening is close to an end and a soft landing is actually on the table. Core bonds in general gain with USTs outperforming Bunds. The latter gapped significantly lower at the open, catching up with a BoJ-inspired move in the US late-yesterday. From there on, however, yield gains quickly evaporated. Changes vary between -6 bps at the front and +2.7 bps at the longest tenor. US yields move from -3.9 bps to +0.8 bps in similar steepening/less inversion of the curve. EUR/USD is struggling for the 1.10 big figure going into the weekend. Sterling is well bid. EUR/GBP is easing towards 0.855. Unlike the euro and USD, the pound is the only one having clear(est) sight on further tightening, even if already accounting for next week’s BoE (25 or 50 bps?) rate hike. European equities wiped out earlier minor losses to trade flat and WS opens >1% higher (Nasdaq).

News & Views

Swedish growth contracted by 1.5% in Q2 putting the level of activity 2.4% lower y/y. It follows a 0.6 % Q/Q rise in Q1. Monthly retail sales in June also declined 0.3% M/M to be 4.4% y/y. June labour market data showed a sizeable increase in the labour force participation. The number of people in the labour force rose 103k compared to the same month last year to 5.940 mln. The relative labour force participation rate amounted to 78.5%, an increase by 1.1 ppts. The unemployment rate rose to 7.9% from 7.2%. However, due the rise in the labour force the higher unemployment rate mirrored both a higher number of unemployed and employed people. Soft activity data won’t make it easier for the Riksbank to convincingly execute further tightening as it still has to cope with high inflation (CPIF 6.4% Y/Y in June). The Riksbank end June raised its policy rate by 25 bps points to 3.75%. The krone early this month rebounded from an all-time low against the euro at EUR/SEK 11.95. The pair currently hovers near 11.55.

The Swiss KOF Economic Barometer improved slightly in July from 90.7 to 92.2 after three consecutive monthly declines. However the economic environment in the Swiss economy is still labeled as difficult. All indicator bundles except those for consumption continue to point to a rather below-average development, but they moved in different directions in July. The outlook for services, financial and insurance services as well as for foreign demand and domestic consumption has brightened somewhat. On the other hand, the outlook for construction activity and for manufacturing, whose outlook is particularly gloomy, have clouded over. The Swiss franc was well bid in July, but today some modest correction kicked in. At EUR/CHF 0.956, the franc still trades strong compared to levels near 0.98 a month ago.

Canada’s Economy Grew in May, with Slowdown Projected in June

The Canadian economy advanced 0.3% month-on-month (m/m) in May, coming in a tick below Statistics Canada's advanced estimate of 0.4% m/m. However, April's flat reading was revised upward by one-tenth providing an offset to this month's figure. The flash estimate for June growth points toward a -0.2% m/m contraction.

April's reading was balanced, with output expanding in 12 of 20 industries. Services-producing industries led the gain, rising by 0.5% m/m. Goods-producing industries contracted by 0.3% m/m, after expanding in the four months prior.

As expected, goods-producing sectors were dragged down by the adverse effects of the wildfires in May. Oil and gas extraction fell 3.6% m/m, and excluding oil sands, dropped 6.6% m/m. All said, mining, quarrying, and natural gas shaved two-tenths off of the headline reading. Manufacturing (+1.6% m/m) partially offset the decline in goods, as supply chains issues continued to ease. The construction sector contracted 0.8% m/m in May, led by residential building construction (-1.8% m/m).

Also as anticipated, the public administration sector rebounded as workers came back to the job after striking until the end of April. The sector rebounded 1.3% m/m and contributed one-tenth to headline GDP. Wholesale trade also provided a lift to services, rebounding by a healthy 2.9% m/m after contracting for three straight months. The real estate sector provided an assist with a gain of 0.5% m/m.

This month's 0.3% m/m for May mark's the largest gain since January 2023. If advanced estimates are correct, June's decrease will mark the first contraction since December 2022.

Key Implications

Canadian GDP came in roughly in line with expectations. With today's print, last month's upward revision and the flash estimate for June, second quarter GDP growth is tracking around 1.0%. This would undershoot the Bank of Canada's (BoC) most recent 1.5% annualized estimate for Q2 growth and put it in line with our current forecast. Still, the BoC reiterated in their July policy statement that they are still concerned with excess demand.

Today's reading points to some slowing momentum heading into the summer months. Since April, GDP data has been impacted by a series of transitory shock whose net effects make the data more difficult to interpret. Looking ahead, headline GDP figures may continue to be skewed by the government's grocery rebate and the effects of the B.C. port strike in July. All said, slowing growth appears to be in the cards for the Canadian economy, and we believe this will be enough for the BoC to remain on hold at its next meeting.

EUR/USD Rebounds after Sharp Losses

- EUR/USD rebounds after 1% fall on Thursday

- US GDP for Q1 beats expectations

The euro has bounced back on Friday after sliding 0.99% a day earlier. In the European session, EUR/USD is trading at 1.1018, up 0.38%. On the economic calendar, the US PCE Price Index, the Fed’s preferred inflation gauge, fell to 3.0% in June, down from 3.8% in May.

ECB, US GDP send euro sharply lower

The European Central Bank raised interest rates by 0.25% on Thursday, bringing the main rate to 3.75%. The ECB statement warned that inflation, although on the decline, “is expected to remain too high for too long”. The ECB did not provide any forward guidance, as the statement said the Governing Council would base its decisions on the data. ECB President Lagarde didn’t add much to this stance, saying that ECB members were “open-minded” about rate decisions at upcoming meetings and wouldn’t commit to whether the ECB would raise or pause in September.

The rate increase can be described as a ‘hawkish hike’, as the statement kept the door open for further hikes. Nevertheless, the euro lost ground following the decision, which could reflect expectations that the ECB is close to its peak rate, despite the hawkish rhetoric.

The eurozone economy is struggling, and this week’s Services PMIs pointed to weakness in Germany and France, the biggest economies in the bloc. The eurozone could slip into recession this year, which means that the ECB will have to think carefully before its raises rates. On the other side of the coin, inflation, which is the ECB’s number one priority, is at 5.5%, well above the target of 2%. The eurozone releases the July inflation report on Monday and the reading could be a key factor in the ECB’s rate decision at the September meeting.

The euro lost further ground on Thursday after better-than-expected US data. In the second quarter, GDP rose 2.4% q/q, above the Q1 reading of 2.0% and the consensus estimate of 1.8%. US Durable Goods Orders and unemployment claims were better than expected, a further indication that the Fed may be able to guide the economy to a soft landing even with interest rates at their highest levels in 22 years.

EUR/USD Technical

- EUR/USD is testing resistance at 1.1002. The next resistance line is 1.1063

- There is support at 1.0895 and close by at 1.0861

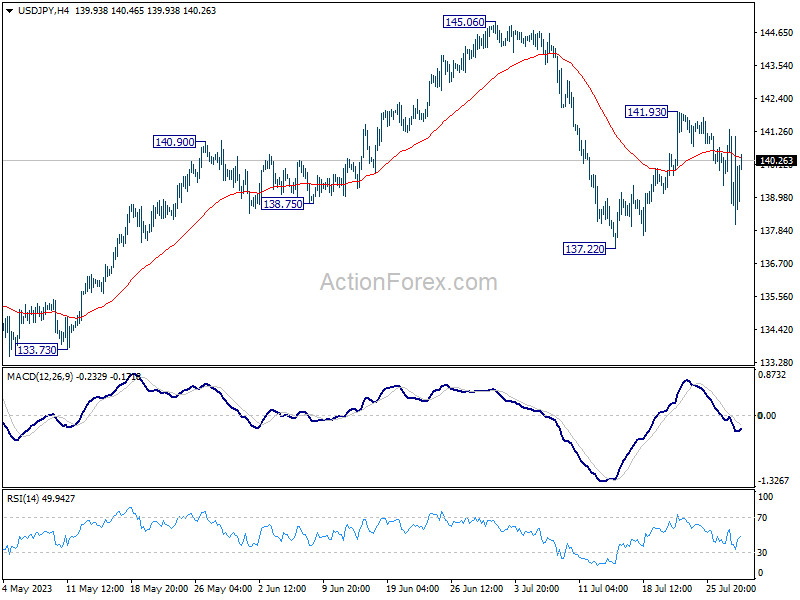

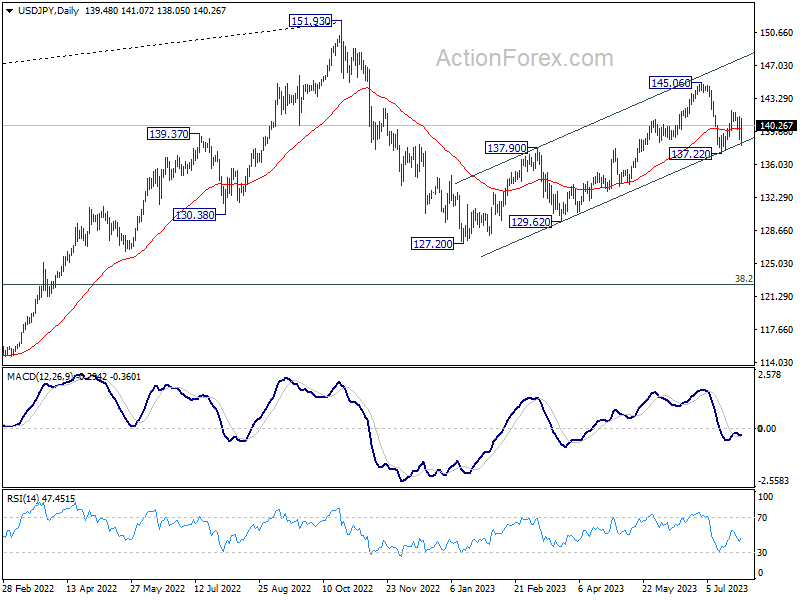

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 138.40; (P) 139.86; (R1) 140.95; More...

Intraday bias in USD/JPY is turned neutral again as it recovery after failing to break through 137.22 support. On the downside, break of 137.22 will resume the whole decline from 145.06, and carries larger bearish implications. On the upside, though, break of 141.93 will resume the rebound from 137.22 and target a test on 145.06 high.

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Current development suggests that the second leg (the rise from 127.20) might not be over yet. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

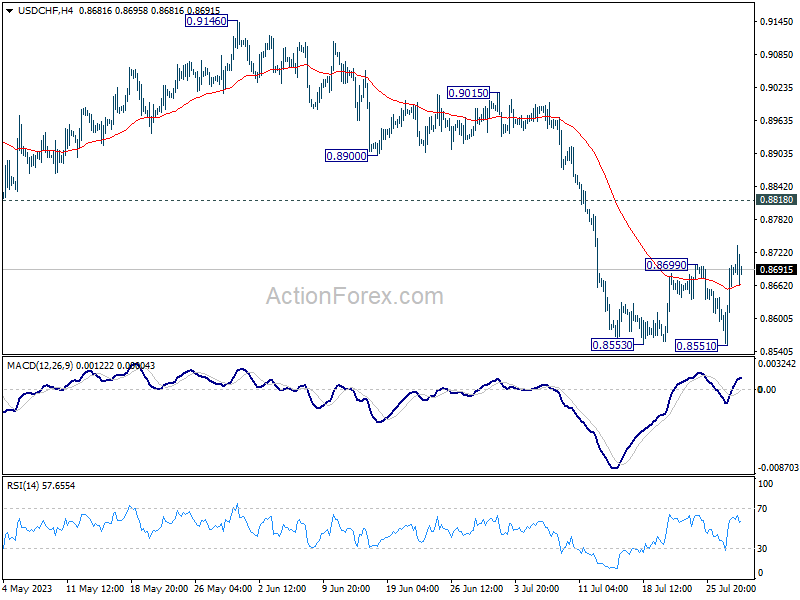

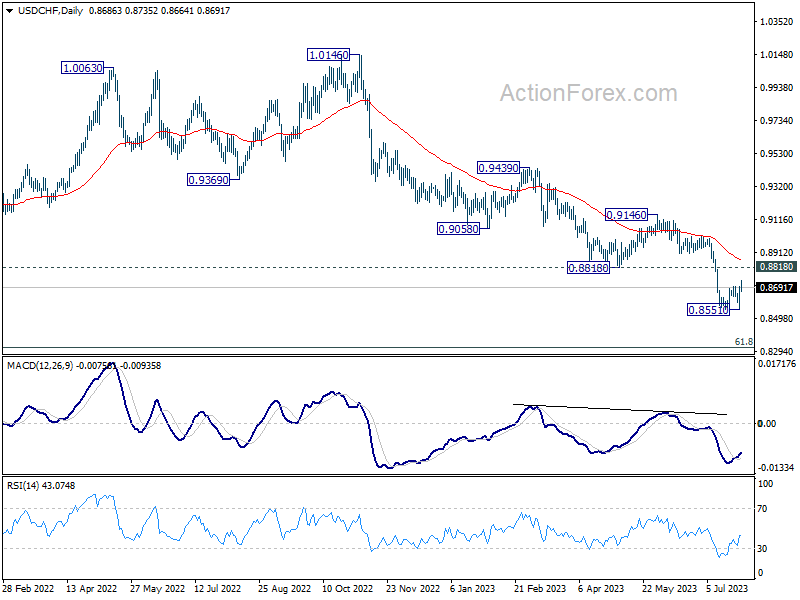

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8598; (P) 0.8648; (R1) 0.8744; More....

Intraday bias in USD/CHF is back on the upside with break of 0.8699 resistance. Further rise would be seen towards 0.8818 support turned resistance. On the downside, firm break of 0.8551 will resume larger down trend from 1.0146, targeting 0.8317 fibonacci level.

In the bigger picture, the break of 0.8756 (2021 low) indicates break out from the long term range pattern. For now, medium term outlook will stay bearish as long as 0.9146 resistance holds. Further fall would be seen to 61.8% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.8317 next.

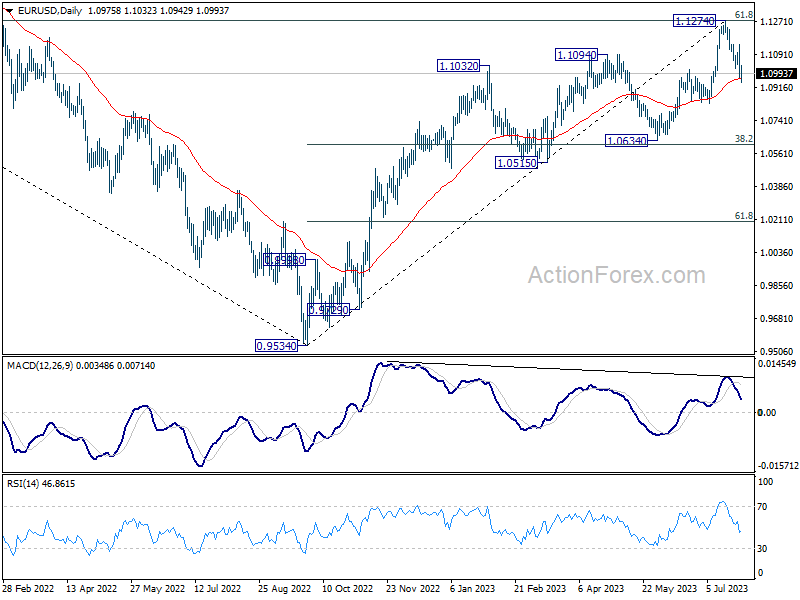

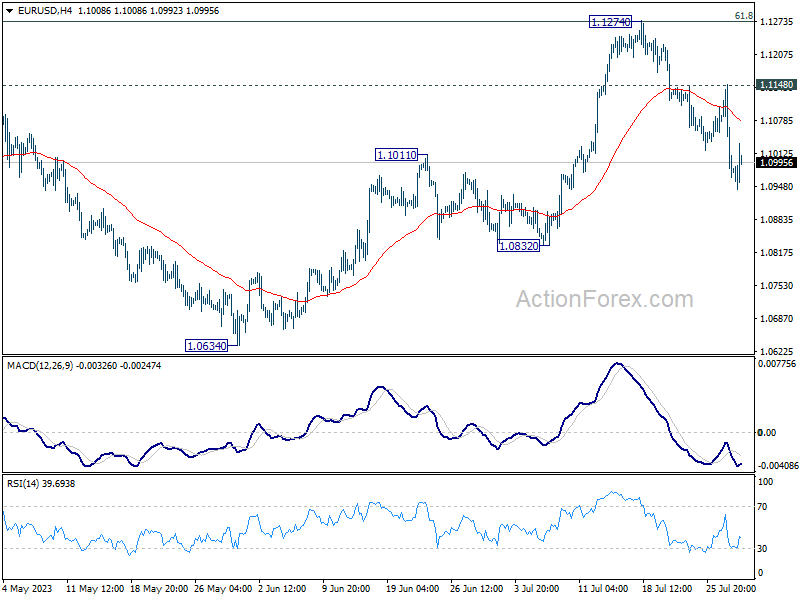

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0912; (P) 1.1031; (R1) 1.1096; More...

EUR/USD recovered after dipping to 1.0942 but further decline is still in favor as long as 1.1148 resistance holds. Sustained trading below 1.1011 resistance turned support will argue that larger correction is underway. Deeper fall would then be seen to 1.0832 support and below. For now, risk will stay mildly on the downside as long as 1.1148 resistance holds, in case of recovery.

In the bigger picture, a medium term top could be formed at 1.1274, after failing to break through 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 decisively, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.0962) will bring deeper correction to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to set the range for consolidation.