Sample Category Title

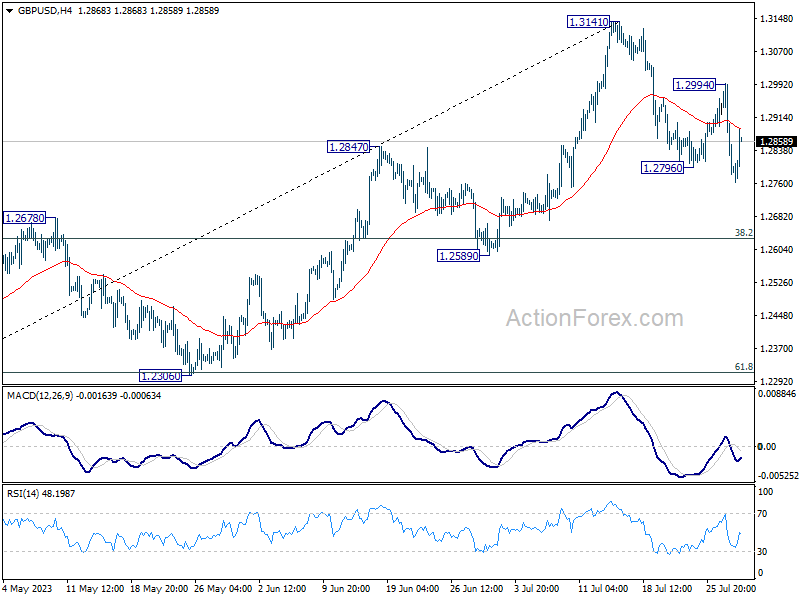

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2720; (P) 1.2858; (R1) 1.2934; More...

GBP/USD recovers notably after dipping to 1.2761 earlier today. But for now, further decline is in favor as long as 1.2994 resistance holds. Fall from 1.3141 would target 55 D EMA (now at 1.2718) and possibly below. On the upside, break of 1.2994 resistance will argue that the pull back has completed, and bring retest of 1.3141 high.

In the bigger picture, as long as 1.2678 resistance turned support holds, rise from 1.0351 (2022 low) is expected to continue. Next target is 100% projection of 1.0351 to 1.2445 from 1.1801 at 1.3895. However, sustained break of 1.2678 will argue that it's at least correcting this rally, with risk of bearish reversal.

Dollar Down Again on PCE Inflation, Yen Reverses Too

Dollar is reversing much of yesterday's gain as both headline and core PCE price indexes showed more than expected moderation. Meanwhile, Yen is also reversing earlier gains around BoJ policy decisions. On the other hand, European majors are making a notable comeback, with Sterling outperforming Euro and Swiss Franc. Commodity currencies however, are staying as the worst performers, except that Loonie is just mixed.

In Europe, at the time of writing, FTSE is up 0.14%. DAX is up 0.22%. CAC is up 0.01%. Germany 10-year yield is flat at 2.473. Earlier in Asia, Nikkei dropped -0.40%. Hong Kong HSI rose 1.41%. China Shanghai SSE rose 1.84%. Singapore Strait Times rose 1.01%. Japan 10-year JGB yield rose 0.1094 to 0.550.

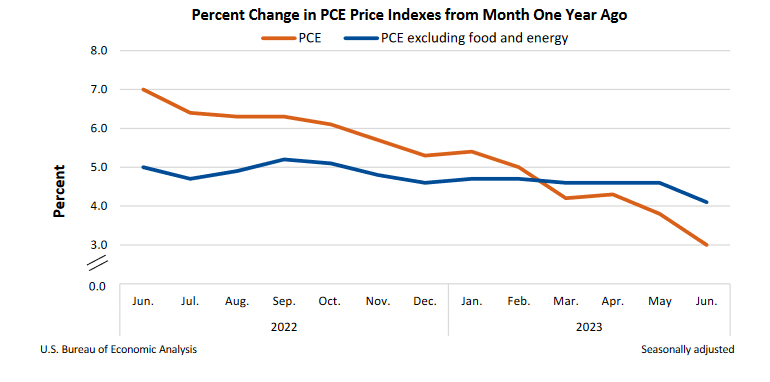

US PCE slows to 3.0% yoy, core PCE down to 4.1% yoy, below expectations

US personal income rose 0.3% mom or USD 69.5B in June, below expectation of 0.5% mom. Spending rose 0.5% mom or USD 100.4B, above expectation of 0.4% mom.

PCE price index rose 0.2% mom, above expectation of -0.1% mom. Core PCE price index (excluding food and energy) also rose 0.2% mom, matched expectations. Prices for goods decreased -0.1% mom and prices for services increased 0.3% mom. Food prices decreased -0.1% mom and energy prices increased 0.6% mom.

From the same month one year ago, PCE price index slowed from 3.8% yoy to 3.0% yoy, below expectation of 3.1% yoy. Core PCE price index slowed from 4.6% yoy to 4.1% yoy, below expectation of 4.2% yoy. Goods prices were down -0.6% yoy while services prices were up 4.9% yoy. Food prices increased 4.6% yoy and energy prices decreased -18.9% yoy.

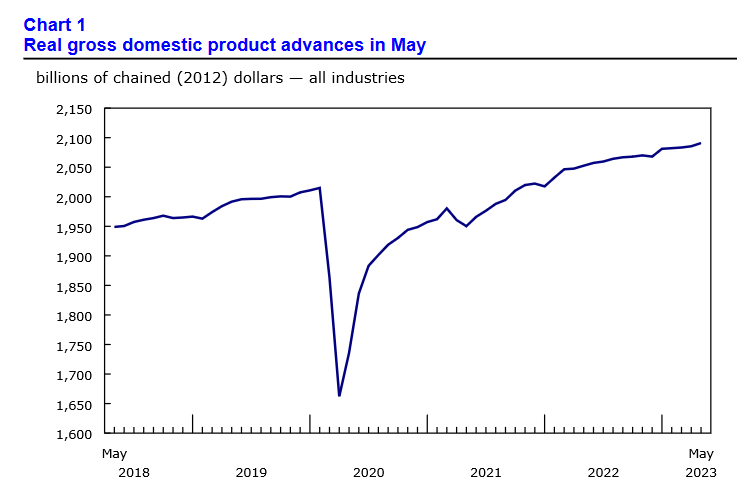

Canada GDP grew 0.3% mom in May, but down -0.2% mom in Jun

Canada GDP grew 0.3% mom in May, matched expectations. Services-producing industries were up 0.5%, while goods-producing industries partially offset the increase with -0.3% decline. Overall, 12 of 20 industrial sectors posted increases.

Advance information indicates that GDP decreased -0.2% mom in June. The decrease was driven by the wholesale trade and manufacturing sectors. These decreases were partially offset by increases in oil and gas extraction as well as in the real estate and rental and leasing sector.

ECB policymakers weigh in on rates

Several top ECB policymakers have today voiced their thoughts on the future of the bank's interest rate hikes, highlighting a variety of perspectives.

Yannis Stournaras, Chief of Greek Central Bank, hinted towards the nearing end of interest rate increases, stating, "It looks like we are very close to the end of interest rate rises." While he doesn't completely rule out another possible hike in September, he noted, "if there is one further - I see it difficult - in September, I believe we will stop there."

However, Slovakia's Central Bank Head Peter Kazimir suggested a less definitive stance, indicating a pause rather than an outright end to the cycle of rate increases. "Even if we were to take a break in September, it would be premature to consider it automatically...the end of the cycle," Kazimir opined, further adding, "We are looking for the right place to stay for a large part of next year...And you will recognize that it has to be a place where we all must like it a little."

Adding a nuanced perspective to the discourse, Francois Villeroy de Galhau, head of French Central Bank, expressed the ECB's growing confidence that it will achieve its 2% inflation target by 2025, attributing this confidence to the effective transmission of rate hikes to the broader economy.

Villeroy emphasized the need for continued perseverance and pragmatism, stating, "Given the time needed for this full transmission, perseverance is now the prime key virtue. Pragmatism is second - decisions at our next meetings will be open and entirely data driven."

French GDP grew strongly by 0.5% qoq, bolstered by foreign trade

France's GDP surpassed expectations in Q2, growing by 0.5% qoq, significantly better than anticipated 0.1% qoq growth. French economy managed to outperform due to robust rebound in foreign trade activities.

According to the data, the main driver of this better-than-expected performance was the positive contribution from foreign trade, which added 0.7 points to GDP growth. Exports in particular saw a rebound this quarter, rising 2.6% after -0.8% contraction in the previous period. Meanwhile, imports also saw an increase, though less pronounced, rising by 0.4% after falling -2.0% in the prior period.

On the other hand, final domestic demand, excluding inventories, weighed on GDP growth once again, contributing a negative -0.1%, consistent with the previous quarter. This is largely attributed to a decrease in household consumption, which dropped by -0.4%. However, Gross Fixed Capital Formation (GFCF) noted a slight increase of 0.1%.

Contribution of inventory changes to GDP growth was minimally negative in Q2, at -0.1%.

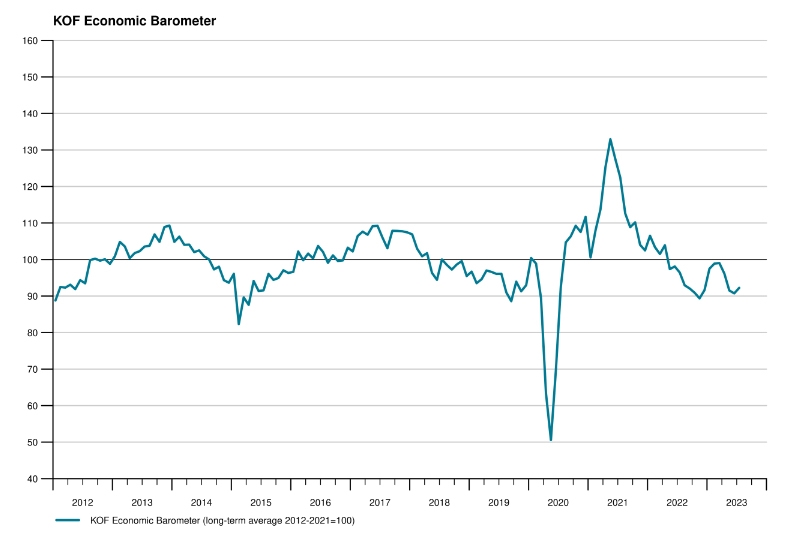

Swiss KOF rose slightly to 92.2, economic environment remains difficult

Swiss KOF Economic Barometer rose from 90.7 to 92.2 in July, above expectation of 90.0. KOF said: "The economic environment remains difficult for the Swiss economy."

It added: "All indicator bundles except those for consumption continue to point to a rather below-average development, but they moved in different directions in July.

"The outlook for services, financial and insurance services as well as for foreign demand and domestic consumption has brightened somewhat. On the other hand, the outlook for construction activity and for manufacturing, whose outlook is particularly gloomy, have clouded over."

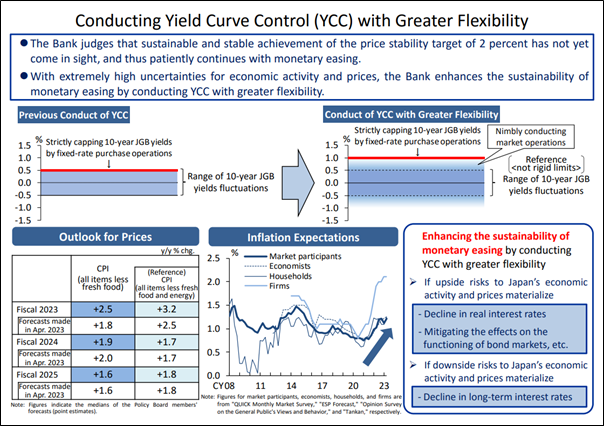

BoJ imposes minor tweak in YCC

On the surface, BoJ kept monetary policy unchanged today. Short term policy rate is held at -0.10% and 10-year JGB yield target is kept at around 0%, by unanimous vote. The band for 10-year JGB yield fluctuation is also kept at plus and minus 0.50% from the target level, by 8-1 majority vote.

However, there were key alterations including decision to buy 10-year JGB yields at 1% in fixed-rate operations, up from previous rate of 0.5%, caught investors' attention. Additionally, BoJ's pledge to conduct yield curve control with "greater flexibility" and to "nimbly respond" to both upside and downside risks was noted.

At the post-meeting press conference, BoJ Governor Kazuo Ueda explained the details of the changes. "We will not tolerate an increase in the 10-year bond yield above 1% and will step in if it does," Ueda emphasized.

While yield moves between 0.5% and 1%, BoJ will monitor the yield level, pace of change, and speed, and conduct various market operations to counter any excessive upward pressure on long-term interest rates. He added, "We don't expect the yield to move up to 1%, but have set this cap as a pre-emptive measure."

In the new economic forecasts, BoJ upgraded CPI core and CPI core-core forecasts for fiscal 2023, but other projections are kept largely unchanged.

- Real GDP growth at 1.3% in fiscal 2023, downgraded from 1.4% as made in April.

- Real GDP growth at 1.2% in fiscal 2024, unchanged.

- Real GDP growth at 1.0% in fiscal 2025, unchanged.

- CPI core at 2.5% in fiscal 2023, upgraded from 1.8%.

- CPI core at 1.9% in fiscal 2024, downgraded from 2.0%.

- CPI core at 1.6% in fiscal 2025, unchanged.

- CPI core-core at 3.2% in fiscal 2023, upgrade from 2.5%.

- CPI core-core at 1.7% in fiscal 2024, unchanged.

- CPI core-core at 1.8% in fiscal 2025, unchanged.

Australia retail sales down -0.8% mom in Jun, cost-of-living pressures weigh

Australia retail sales turnover fell -0.8% mom in June, much worse than expectation of 0% mom. Sales turnover rose 2.3% yoy compared with June 2022.

Ben Dorber, ABS head of retail statistics, said: "Retail turnover fell sharply in June due to weaker than usual spending on end of financial year sales. This comes as cost-of-living pressures continued to weigh on consumer spending.

"There was extra discounting and promotional activity in May, leading up to mid-year sales events. This delivered a boost in turnover for retailers, but that proved to be temporary as consumers pulled back on spending in June."

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2720; (P) 1.2858; (R1) 1.2934; More...

GBP/USD recovers notably after dipping to 1.2761 earlier today. But for now, further decline is in favor as long as 1.2994 resistance holds. Fall from 1.3141 would target 55 D EMA (now at 1.2718) and possibly below. On the upside, break of 1.2994 resistance will argue that the pull back has completed, and bring retest of 1.3141 high.

In the bigger picture, as long as 1.2678 resistance turned support holds, rise from 1.0351 (2022 low) is expected to continue. Next target is 100% projection of 1.0351 to 1.2445 from 1.1801 at 1.3895. However, sustained break of 1.2678 will argue that it's at least correcting this rally, with risk of bearish reversal.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Y/Y Jul | 3.20% | 2.80% | 3.10% | |

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Jul | 3.00% | 2.90% | 3.20% | |

| 23:30 | JPY | Tokyo CPI ex Food Energy Y/Y Jul | 4.00% | 3.80% | ||

| 01:30 | AUD | Retail Sales M/M Jun | -0.80% | 0.00% | 0.70% | 0.80% |

| 01:30 | AUD | PPI Q/Q Q1 | 0.50% | 0.90% | 1.00% | |

| 01:30 | AUD | PPI Y/Y Q1 | 3.90% | 3.90% | 5.20% | |

| 03:28 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 05:30 | EUR | France GDP Q/Q Q2 | 0.50% | 0.10% | 0.20% | 0.10% |

| 07:00 | CHF | KOF Economic Barometer Jul | 92.2 | 90 | 90.8 | 90.7 |

| 09:00 | EUR | Germany GDP Q/Q Q2 | 0.00% | 0.10% | -0.30% | |

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Jul | 94.5 | 95 | 95.3 | |

| 09:00 | EUR | Eurozone Industrial Confidence Jul | -9.4 | -7.5 | -7.2 | -7.3 |

| 09:00 | EUR | Eurozone Services Sentiment Jul | 5.7 | 5.3 | 5.7 | 5.9 |

| 09:00 | EUR | Eurozone Consumer Confidence Jul F | -15.1 | -15.1 | -15.1 | |

| 12:00 | EUR | Germany CPI M/M Jul P | 0.30% | 0.30% | 0.30% | |

| 12:00 | EUR | Germany CPI Y/Y Jul P | 6.20% | 6.20% | 6.40% | |

| 12:30 | CAD | GDP M/M May | 0.30% | 0.30% | 0.00% | 0.10% |

| 12:30 | USD | Personal Income M/M Jun | 0.30% | 0.50% | 0.40% | 0.50% |

| 12:30 | USD | Personal Spending M/M Jun | 0.50% | 0.40% | 0.10% | 0.20% |

| 12:30 | USD | PCE Price Index M/M Jun | 0.20% | -0.10% | 0.10% | |

| 12:30 | USD | PCE Price Index Y/Y Jun | 3.00% | 3.10% | 3.80% | |

| 12:30 | USD | Core PCE Price Index M/M Jun | 0.20% | 0.20% | 0.30% | |

| 12:30 | USD | Core PCE Price Index Y/Y Jun | 4.10% | 4.20% | 4.60% | |

| 12:30 | USD | Employment Cost Index Q1 | 1.00% | 1.10% | 1.20% | |

| 13:45 | USD | Chicago PMI Jul | 72.6 | 41.5 | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Jul F | 72.6 | 72.6 |

US PCE slows to 3.0% yoy, core PCE down to 4.1% yoy, below expectations

US personal income rose 0.3% mom or USD 69.5B in June, below expectation of 0.5% mom. Spending rose 0.5% mom or USD 100.4B, above expectation of 0.4% mom.

PCE price index rose 0.2% mom, above expectation of -0.1% mom. Core PCE price index (excluding food and energy) also rose 0.2% mom, matched expectations. Prices for goods decreased -0.1% mom and prices for services increased 0.3% mom. Food prices decreased -0.1% mom and energy prices increased 0.6% mom.

From the same month one year ago, PCE price index slowed from 3.8% yoy to 3.0% yoy, below expectation of 3.1% yoy. Core PCE price index slowed from 4.6% yoy to 4.1% yoy, below expectation of 4.2% yoy. Goods prices were down -0.6% yoy while services prices were up 4.9% yoy. Food prices increased 4.6% yoy and energy prices decreased -18.9% yoy.

Canada GDP grew 0.3% mom in May, but down -0.2% mom in Jun

Canada GDP grew 0.3% mom in May, matched expectations. Services-producing industries were up 0.5%, while goods-producing industries partially offset the increase with -0.3% decline. Overall, 12 of 20 industrial sectors posted increases.

Advance information indicates that GDP decreased -0.2% mom in June. The decrease was driven by the wholesale trade and manufacturing sectors. These decreases were partially offset by increases in oil and gas extraction as well as in the real estate and rental and leasing sector.

ECB policymakers weigh in on rates

Several top ECB policymakers have today voiced their thoughts on the future of the bank's interest rate hikes, highlighting a variety of perspectives.

Yannis Stournaras, Chief of Greek Central Bank, hinted towards the nearing end of interest rate increases, stating, "It looks like we are very close to the end of interest rate rises." While he doesn't completely rule out another possible hike in September, he noted, "if there is one further - I see it difficult - in September, I believe we will stop there."

However, Slovakia's Central Bank Head Peter Kazimir suggested a less definitive stance, indicating a pause rather than an outright end to the cycle of rate increases. "Even if we were to take a break in September, it would be premature to consider it automatically...the end of the cycle," Kazimir opined, further adding, "We are looking for the right place to stay for a large part of next year...And you will recognize that it has to be a place where we all must like it a little."

Adding a nuanced perspective to the discourse, Francois Villeroy de Galhau, head of French Central Bank, expressed the ECB's growing confidence that it will achieve its 2% inflation target by 2025, attributing this confidence to the effective transmission of rate hikes to the broader economy.

Villeroy emphasized the need for continued perseverance and pragmatism, stating, "Given the time needed for this full transmission, perseverance is now the prime key virtue. Pragmatism is second - decisions at our next meetings will be open and entirely data driven."

Canadian Dollar Flat Ahead of Canadian GDP

- Canada’s GDP expected to rebound in May

- US releases PCE index

The Canadian dollar is almost unchanged on Friday, trading at 1.3223 in the European session. Things could get busier for the Canadian dollar in the North American session, as Canada releases GDP and the US publishes its preferred inflation indicator, the PCE index.

Canada’s GDP expected to improve in May

Canada’s economy stalled in April, as GDP came in at 0.0% m/m. The driver behind the weak reading was a strike by Canada’s largest government worker union in April, causing a drop in economic activity in the public sector. There are expectations for an improvement in May, with a consensus estimate of 0.3% m/m.

Despite the downswing in April, Canada’s economy has been in good shape, with a 3.2% gain in the first quarter. As is the case with the United States, Canada’s labour market has defied expectations and remained robust despite aggressive tightening by the central bank. This has complicated the Bank of Canada’s tough battle to push inflation back to the 2% target and means that additional rate hikes remain on the table.

The BoC released its Summary of Deliberations from the July meeting on Wednesday. At the meeting, the BoC raised rates by 0.25%, bringing the cash rate to 5.0%. The Bank’s Governing Council noted that inflation remained persistent due to the tight labour market and higher-than-expected consumption.

The Federal Reserve didn’t surprise anyone when it raised rates by 0.25% on Wednesday, bringing the benchmark rate to a range of 5.25%-5.50%. Fed Chair Powell reiterated that “policy has not been restrictive enough for long enough”, adding that the Fed could continue tightening. Still, the money markets are betting that the Fed is done with hiking, and have priced in an 80% likelihood of a pause in September.

USD/CAD Technical

- There is resistance at 1.3272 and 1.3319

- 1.3195 and 1.3148 are providing support

Yen Goes on a Wild Ride after BoJ Shocker

The Japanese yen took investors on a wild ride on Friday but has settled down. In the European session, USD/JPY is trading at 139.54, up 0.05%.

Yen swings wildly after BoJ tweaks yield curve control

The Bank of Japan appears to relish catching the markets with its pants down, and I’ll be the first to admit that I was shocked to read that the BoJ had made a shift in policy at today’s policy meeting. Clearly, I wasn’t alone, as the yen has fluctuated almost 400 points since the BoJ shocked the markets and announced it would loosen its yield curve control. The policy statement noted that the BoJ will “conduct yield curve control with greater flexibility, regarding the upper and lower bounds of the range as references, not as rigid limits, in its market operations”.

BoJ Governor Ueda had signalled that he would maintain policy settings, and he reiterated this stance just a few days ago. Instead, Ueda went ahead with his first major policy shift since taking over as head of the BoJ in April, which triggered sharp volatility from the yen.

In September, the BoJ widened the target band on 10-year Japanese government bonds (JGBs) from 0.25% to 0.50%, sending the yen sharply higher. The BoJ said in today’s policy statement that the target band will remain in the range of -0.50% to +0.50%, but it will offer to purchase JGBs at 1%. Effectively, this widens the band by a further 50 basis points.

The BoJ maintained interest rates at -0.1% and raised its inflation forecast for fiscal 2023 from 1.8% to 2.5%. Inflation has persistently hovered above the 2% target and has put pressure on the BoJ to normalize its monetary policy. Interestingly, Governor Ueda insisted at a follow-up press conference that today’s tweak was not intended as a step towards policy normalization, dampening any expectations that the BoJ will abandon its yield curve control.

USD/JPY Technical

- USD/JPY has pushed above resistance at 1.4049. Above, there is resistance at 142.62

- There is support at 139.03 and 1.3840

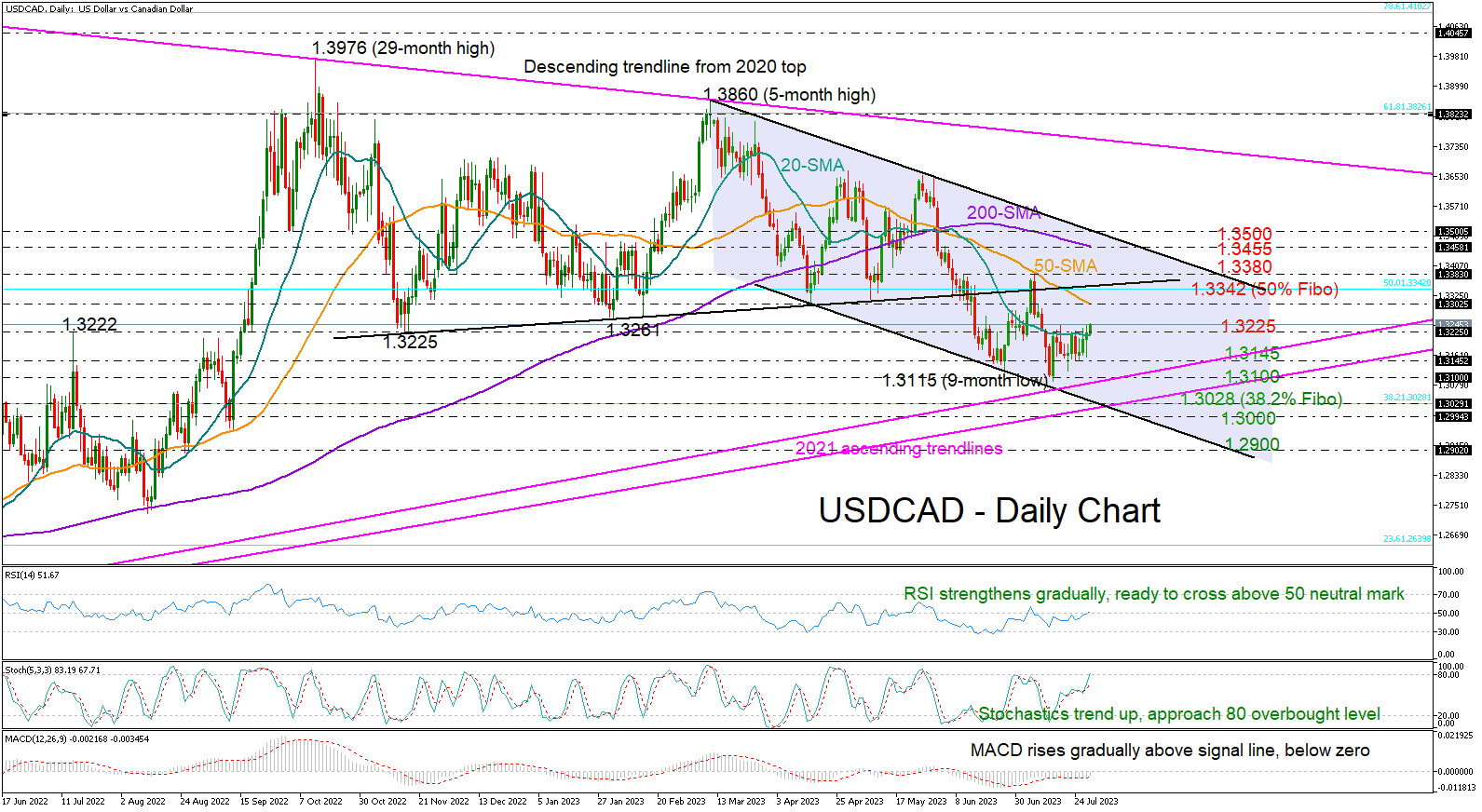

USDCAD Hopes for a New Bullish Correction

USDCAD has been in a range for the second consecutive week, unable to extend its rebound off a nine-month low of 1.3115 above the nearby resistance of 1.3225.

The odds for a bullish extension are increasing, given the positive slope in the momentum indicators. But with the RSI fluctuating below 50 and the MACD remaining within the negative zone, any improvement may be brief.

If the price sustains today’s bullish move above the 20-day SMA and 1.3225, the falling 50-day simple moving average (SMA) could first halt upside pressures at around 1.3300. Then, the 1.3040-1.3080 constraining zone, which encapsulates the former support trendline, the 50% Fibonacci retracement level of the 2020-2021 downtrend, and July’s high, could delay an extension towards the 200-day SMA at 1.3455. Yet only a sustainable close above the broad bearish channel and beyond 1.3500 would brighten the short-term outlook.

Alternatively, a pullback could re-examine the strong 1.3100-1.3145 support area, where the ascending trendline from May 2021 is positioned. If they break that base, the bears could immediately target the channel’s lower boundary, which coincides with the 38.2% Fibonacci mark and the flatter tentative ascending trendline from May 2021 at 1.3028. Should downside forces strengthen below the 1.3000 psychological level, the price might seek shelter at around 1.2900.

To sum up, USDCAD has been stubbornly pushing for a close above 1.3225 despite its unsuccessful attempts. If it breaches that bar this time, the pair could enjoy some recovery, though it will need stronger buying confidence to cross above the tough 1.3300-1.3380 resistance area.

No Major Risk-off after BoJ’s Creative YCC Flexibility Tweak

- Bank of Japan maintained its ultra-loose monetary policy but issued a lukewarm hawkish statement to introduce a “flexible” Yield Curve Control programme on the 10-year JGB yield.

- JPY strengthen but did not lead to a sell-off in other Asian benchmark stock indices.

- Nikkei 225 has managed to trim its intraday loss of -2.60% and ended with a smaller magnitude of -0.4%.

- Japanese banks outperformed; the TOPIX-17 Banks ETF rallied by +4.70%.

- The new YCC with “greater flexibility” may reduce speculative activities in the JGB futures market.

Bank of Japan (BoJ) has once again maintained its ultra-loose monetary policy outright in today’s conclusion of its July MPM; kept the short-term interest rate target unchanged at -0.1% and maintained the 10-year Japanese Bond Government Bond yield at around 0% with upper and lower limits cap at 0.5% on each side.

Also, BoJ has upgraded its median consumer inflation (CPI) forecast for FY 2023 on its latest quarterly outlook report; core CPI is expected to increase to 2.5% year-on-year (y/y) from the prior forecast of 1.8% y/y, and core-core CPI (excluding fresh food & energy) has also been raised to 3.2% y/y from prior forecast of 2.5% y/y.

No change in the median CPI forecasts for FY 2024 and FY 2025. For FY2024, forecasted core CPI (1.9% y/y), and core-core CPI (1.7% y/y), as for FY 2025, forecasted core CPI (1.6% y/y), and core-core CPI (1.8% y/y).

Meanwhile, the median forecast for FY 2023 real GDP is being downgraded slightly to 1.3% y/y from the previous forecast of 1.4% y/y. BoJ has maintained its real GDP median forecast for FY 2024 and FY 2025 at 1.2% y/y and 1% y/y respectively.

Based on its latest inflation and growth forecasts, BoJ seems to have a view that inflation growth is likely to slow down after FY 2023 in conjunction with a mild reduction in economic growth which suggests the 2% inflation target in terms of sustainability has not been obtained, and such forecasts support BoJ’s current modus operandi of maintain its ultra-easy monetary policy, in contrast with the rest of other developed nations.

Interestingly, BoJ is well-known for being a forerunner in enacting “creative monetary policies”, and issued a rather lukewarm hawkish monetary policy statement that starkly stated two key points.

Firstly, it will operate the Yield Curve Control (YCC) programme of the 10-year JGB yield with more flexibility to respond nimbly to upside and downside risks which implies that it is pointing to a potential abolishment of the current fixed upper and lower limits of 0.5% on either side (see chart below for more details on the new flexible YCC).

Fig 1: Bank of Japan’s new YCC with greater flexibility framework (Source: BoJ website, click to enlarge chart)

Secondly, BoJ will offer to purchase 10-year JGBs at 1% yield every business day through fixed-rate purchase operations which suggests subtly that the “new invisible” limit is now set at 1% on the YCC programme.

Overall, it seems that the new YCC with “greater flexibility” by not committing to any hard upper and lower limits is to reduce undesirable speculative activities in the financial markets, especially the JGB futures that are likely to trigger adverse reflexive loops into other asset classes and the real economy.

No major risk-off in the Asian session despite the continuation of JPY strength

Fig 2: USD/JPY minor short-term trend as of 28 Jul 2023 (Source: TradingView, click to enlarge chart)

Even though the USD/JPY has continued to weaken (JPY strengthening) ex-post BoJ meeting where it slipped below yesterday, 27 July US session low of 138.76 to print an intraday lower low of 138.06 after a retest of the 20-day moving average that is acting a key short-term resistance at around 141.30 during today, 28 July Asian session at this time of the writing.

In the past, a significant further JPY strengthening due to a slight hint of hawkish monetary policy from the BoJ tends to trigger a risk-off behaviour where Asian stock indices sold off. In today’s “subtle tweak” to the YCC, the worst performer in the Asian region today is the Nikkei 225 which ended with a daily loss of -0.40% (trimmed away a much larger intraday magnitude of -2.60%) while other Asian benchmark stock indices have traded mostly with gains throughout today’s session; Hang Seng Index (+1.45%), Hang Seng TECH Index (+3.00), China’s CSI 300 (+2.3%), and Singapore’s Straits Times Index, (+1%) at this time of the writing.

Japanese banks outperformed

Also, within the Nikkei 225, the share prices of Japanese banks stood out significantly today where the TOPIX-17 Banks exchange-traded fund was the top performer among the 17 TOPIX sectors with a daily gain of +4.70% which suggests that market participants are anticipating an improvement of net interest margins for Japanese banks in a new “flexible” YCC environment.

Fig 3: TOPIX-17 Banks ETF major term trend as of 28 Jul 2023 (Source: TradingView, click to enlarge chart)

From a technical analysis standpoint, the TOPIX-17 Banks’ ETF has traced a major bottoming formation in place since September 2011 which suggests that perhaps taking baby steps in normalization of Japan’s ultra-loose monetary policy may not lead to an adverse risk-off effect in the Japanese stock market and even globally by considering the current price actions movement seen in the major cross asset classes.

Swiss KOF rose slightly to 92.2, economic environment remains difficult

Swiss KOF Economic Barometer rose from 90.7 to 92.2 in July, above expectation of 90.0. KOF said: "The economic environment remains difficult for the Swiss economy."

It added: "All indicator bundles except those for consumption continue to point to a rather below-average development, but they moved in different directions in July.

"The outlook for services, financial and insurance services as well as for foreign demand and domestic consumption has brightened somewhat. On the other hand, the outlook for construction activity and for manufacturing, whose outlook is particularly gloomy, have clouded over."