Sample Category Title

Cliff Notes: Disinflation Begins to Ease Global Policy Makers’ Concerns

Key insights from the week that was.

The Australian Q2 CPI report provided a constructive update on inflation, highlighting a broad-based moderation in the pace of price increases across the consumption basket. The main results were a 0.8% (6.0%yr) lift in headline inflation and a 0.9% (5.9%yr) rise in trimmed mean inflation, both of which were below the market’s expectation and our own. Highlighting the extent of the underlying moderation, the six-month annualised pace of core inflation has fallen from 6.0%yr to 4.3%yr, driven not only by a slowing in goods inflation but also services, including household services such as childcare as well as medical and hospital services. This is a welcome development for the RBA, with the easing in both headline and underlying inflation now running ahead of their forecasts from May.

In light of this update, as discussed by Chief Economist Bill Evan, we have lowered our forecast for the peak in the cash rate from 4.60% to 4.35%. That said, the persistence of services inflation and historically-tight labour market still present clear upside risks to the inflation outlook, concerns which Governor Lowe has consistently emphasised in recent months. In our view, this warrants additional insurance to be taken in the form of one further 25bp rate hike next week. A tightening bias is also likely to remain in place in coming months as the Board continue to assess the pace and breadth of disinflation across the services sector as well as the labour market’s strength.

Offshore, the US FOMC and European Central Bank (ECB) both raised their policy rates by 25bps at their July meeting as expected. In the press conference, FOMC Chair Powell made clear that the Committee will be closely scrutinising the strength and capacity of the economy in the months ahead, with subsequent decisions 'data dependent'. Notably, between the July and September meetings, two CPI reports and two employment reports are due, giving the Committee clarity on whether June’s below-expectations CPI is a sign of the emergence of broad-based and sustainable disinflation or just a one-off reading. The former requires a further deceleration in employment and spending into 2024, and for inflation expectations to remain well anchored.

While the Q2 advanced GDP estimate came in at an above-trend 0.6%qtr, 2.6%yr annualised, the component detail was consistent with a disinflationary outlook. Services consumption slowed to a near-trend pace and growth in goods consumption was negligible in the quarter. Business investment meanwhile surprised to the upside as equipment spending surged following a protracted period of weakness and non-residential construction continued to grow strongly. Note the investment outcomes are not a concern for inflation on their own; to the contrary, greater capacity and efficiency will aid the fight against inflation. Housing investment remains a source of concern though, with activity continuing to contract at a time when additional supply is necessary. Also worthy of note is that both the consumer and aggregate GDP deflator came in below expectations, the GDP deflator noticeably so. This result may be the result of dissipating supply frictions, but it could also be statistical – a point to watch as revisions are received.

Looking ahead, the latter part of Q2 experienced a loss of momentum and further tightening in credit conditions, pointing to a materially weaker pace of growth through the second half and into 2024. Constructively though, Chair Powell's forward guidance on 2024 and beyond went as far as to envision a need to 'stop raising long before you got to 2% inflation and… start cutting before you got to 2% inflation too'. He also went on to signal an eventual return to neutral or expansionary monetary policy. We view these comments as broadly in line with our current forecasts for a first rate cut in March 2024 and significant easing thereafter through 2024 and 2025 to a fed funds rate of 2.625%. You can read our full analysis on the FOMC’s decision and US outlook here.

Mirroring the US FOMC’s decision, the ECB also raised their three policy rates by 25bps as widely expected, though the statement carried a more doveish tone. President Christine Lagarde signalled that little forward guidance would be given from here, with future rate hikes data-dependent. Lagarde expanded upon the change of verb describing the path of interest rates from ‘the key ECB interest rates will be brought to levels sufficiently restrictive to achieve a timely return of inflation’ to ‘set to’. She explained this change of verb was deliberate and the two inflation readings alongside indicators of policy transmission would guide the decision in September. Additionally, the ECB announced it would cease remuneration for minimum reserves to make monetary policy transmission more 'efficient'.

The ECB’s projections suggest inflation is expected to average 5.4% in 2023, while growth thus far would put inflation at 4.9%yr in 2023. In addition to a weaker inflation print, the second quarter Bank Lending Survey released this week, showed that credit standards had tightened for enterprises and house purchases. Demand for credit has also fallen further for enterprises, though the net percentage of banks reporting an increase in home loan demand had become less negative. The latter was a result of less pessimistic housing market prospects.

Should data continue to come in mild, further rate hikes may not be needed. However, much like the RBA, a tight labour market and momentum in services inflation could justify the ECB take additional precautions in coming months.

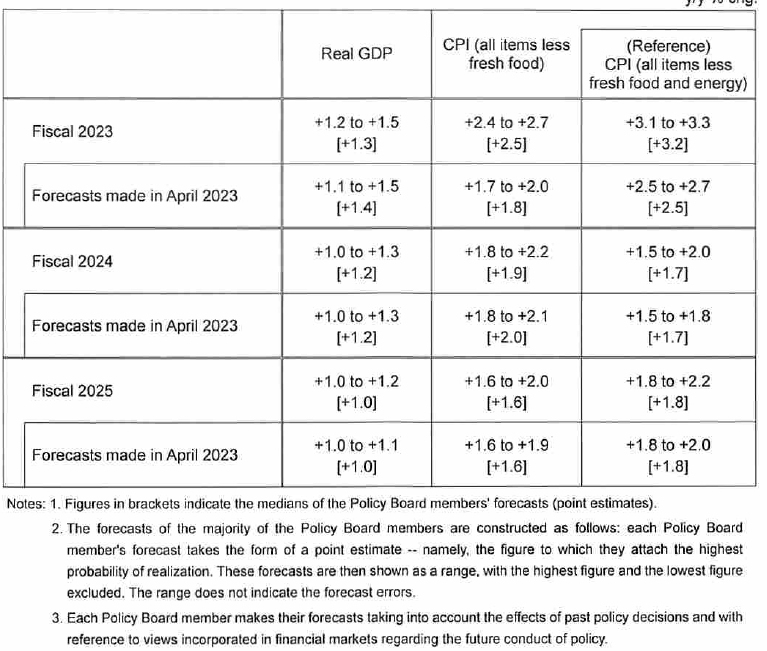

BoJ keeps policy unchanged, one member wants YCC tweak

BoJ keeps monetary policy unchanged today, despite some speculation of at least a minor tweak to the yield curve control. Short term policy rate is held at -0.10% and 10-year JGB yield target is kept at around 0%, by unanimous vote.

The band for 10-year JGB yield fluctuation is also kept at plus and minus 0.50% from the target level, by 8-1 majority vote. Nakamura Toyoaki dissented with preference for allowing greater flexibility in conducting YCC.

In the new economic forecasts, BoJ upgraded CPI core and CPI core-core forecasts for fiscal 2023, but other projections are kept largely unchanged.

- Real GDP growth at 1.3% in fiscal 2023, downgraded from 1.4% as made in April.

- Real GDP growth at 1.2% in fiscal 2024, unchanged.

- Real GDP growth at 1.0% in fiscal 2025, unchanged.

- CPI core at 2.5% in fiscal 2023, upgraded from 1.8%.

- CPI core at 1.9% in fiscal 2024, downgraded from 2.0%.

- CPI core at 1.6% in fiscal 2025, unchanged.

- CPI core-core at 3.2% in fiscal 2023, upgrade from 2.5%.

- CPI core-core at 1.7% in fiscal 2024, unchanged.

- CPI core-core at 1.8% in fiscal 2025, unchanged.

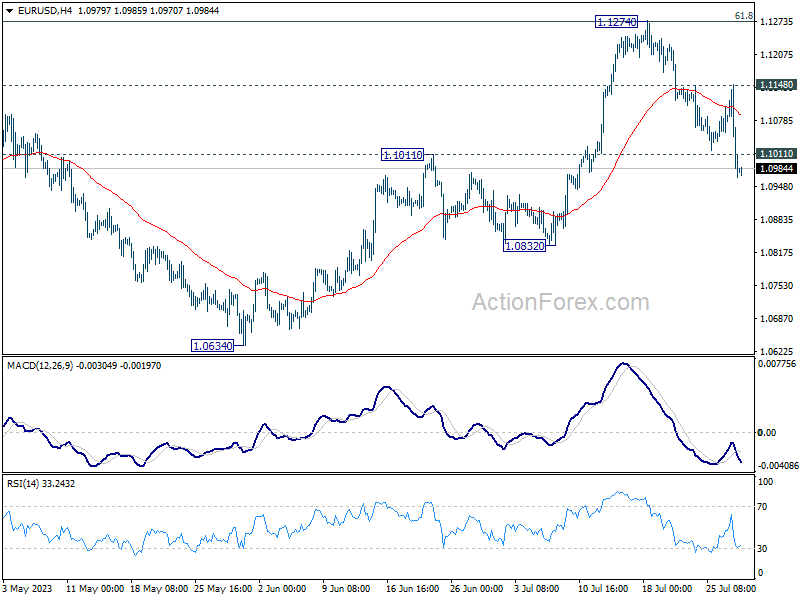

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0912; (P) 1.1031; (R1) 1.1096; More...

EUR/USD's fall from 1.1274 continues today and intraday bias remains on the downside. Sustained trading below 1.1011 resistance turned support will argue that larger correction is underway. Deeper fall would then be seen to 1.0832 support and below. For now, risk will stay mildly on the downside as long as 1.1148 resistance holds, in case of recovery.

In the bigger picture, a medium term top could be formed at 1.1274, after failing to break through 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 decisively, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.0962) will bring deeper correction to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to set the range for consolidation.

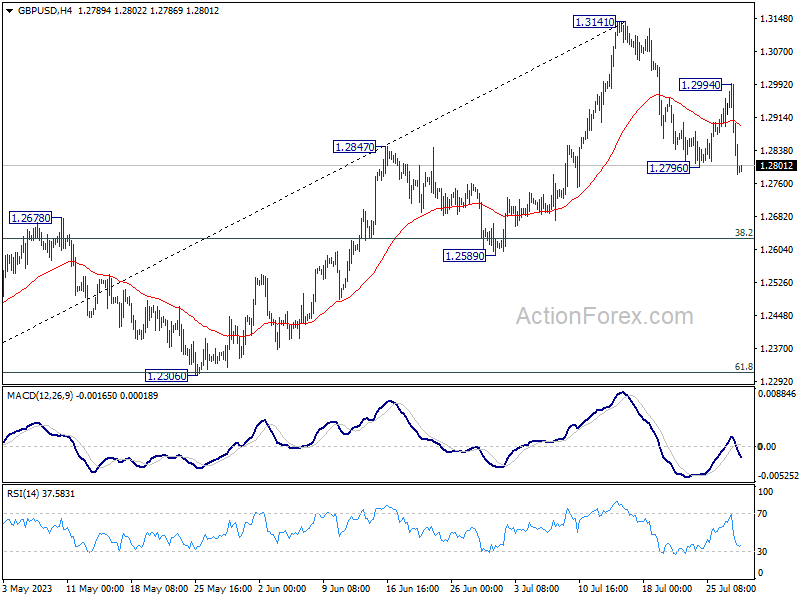

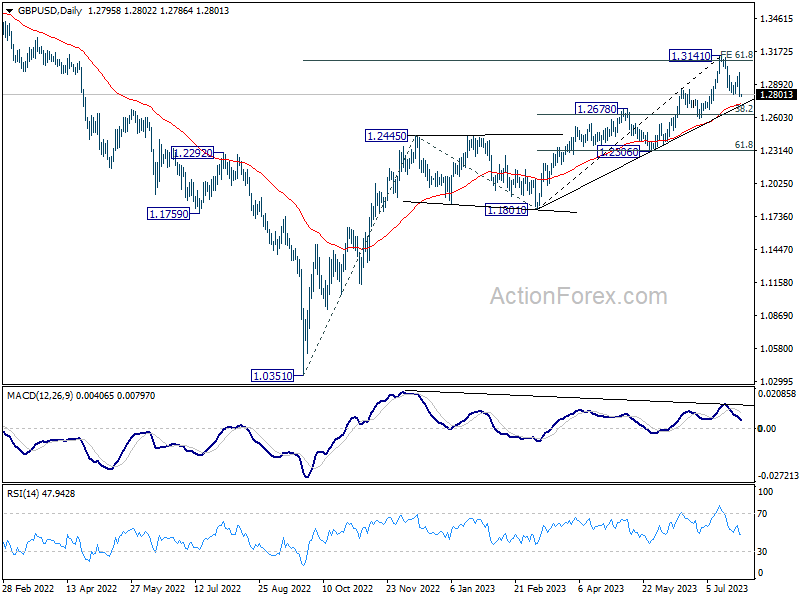

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2720; (P) 1.2858; (R1) 1.2934; More...

GBP/USD's fall from 1.3141 resumed by breaking 1.2796 support. Intraday bias is back on the downside for 55 D EMA (now at 1.2718) and possibly below. On the upside, break of 1.2994 resistance will argue that the pull back has completed, and bring retest of 1.3141 high.

In the bigger picture, as long as 1.2678 resistance turned support holds, rise from 1.0351 (2022 low) is expected to continue. Next target is 100% projection of 1.0351 to 1.2445 from 1.1801 at 1.3895. However, sustained break of 1.2678 will argue that it's at least correcting this rally, with risk of bearish reversal.

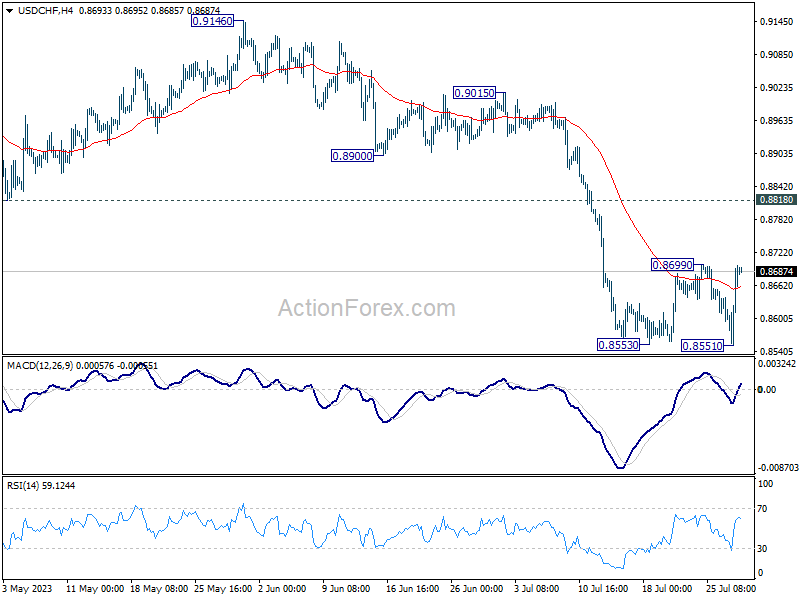

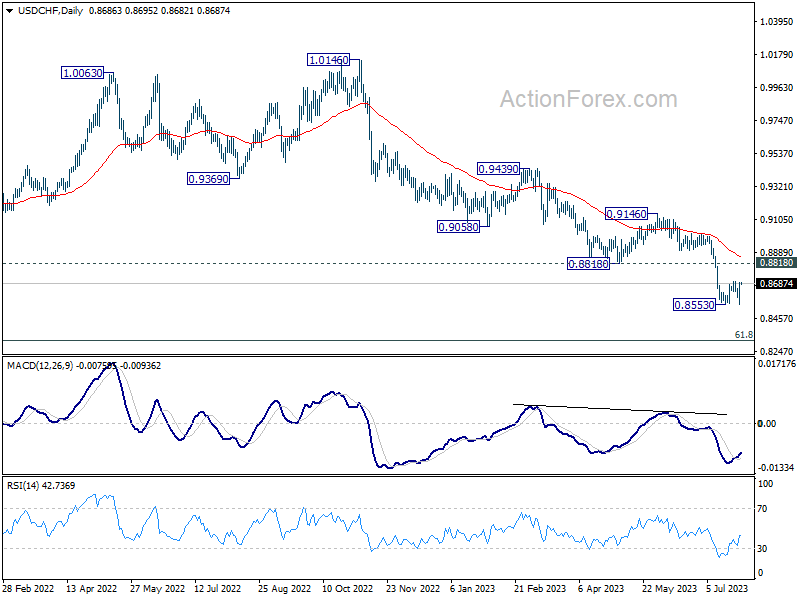

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8598; (P) 0.8648; (R1) 0.8744; More....

Intraday bias in USD/CHF remains neutral for the moment. On the upside, break of 0.8699 will bring stronger rebound towards 0.8818 support turned resistance. On the downside, firm break of 0.8551 will resume larger down trend from 1.0146, targeting 0.8317 fibonacci level.

In the bigger picture, the break of 0.8756 (2021 low) indicates break out from the long term range pattern. For now, medium term outlook will stay bearish as long as 0.9146 resistance holds. Further fall would be seen to 61.8% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.8317 next.

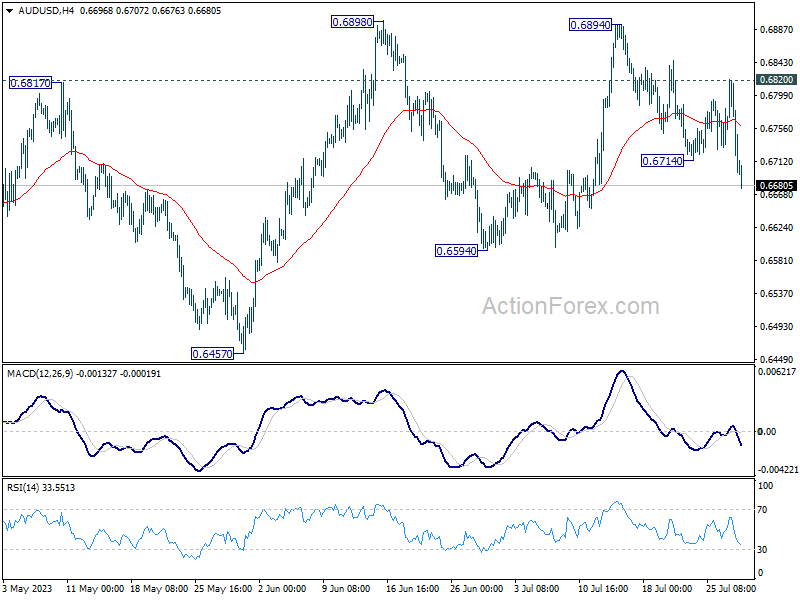

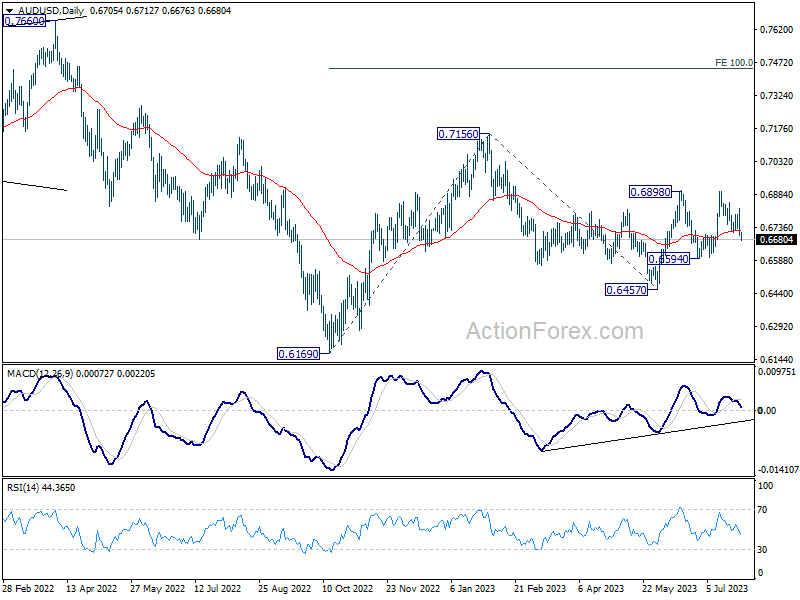

AUD/USD Daily Report

Daily Pivots: (S1) 0.6664; (P) 0.6742; (R1) 0.6787; More...

AUD/USD's fall from 0.6894 resumed by breaking through 0.6714 and intraday bias is back on the downside. As this decline is seen as the third leg of the corrective pattern from 0.6898, downside should be contained by 0.6594 support. On the upside, break of 0.6820 resistance will turn bias back to the upside for 0.6894/8 resistance zone.

In the bigger picture, price actions from 0.7156 are seen as a correction to the rebound from 0.6169 (2022 low). Break of 0.6898 resistance will argue that rise from 0.6169 is ready to resume through 0.7156. Next target will be 100% projection of 0.6169 to 0.7156 from 0.6457 at 0.7444. For now, this will be the favored case as long as 55 D EMA (now at 0.6720) holds.

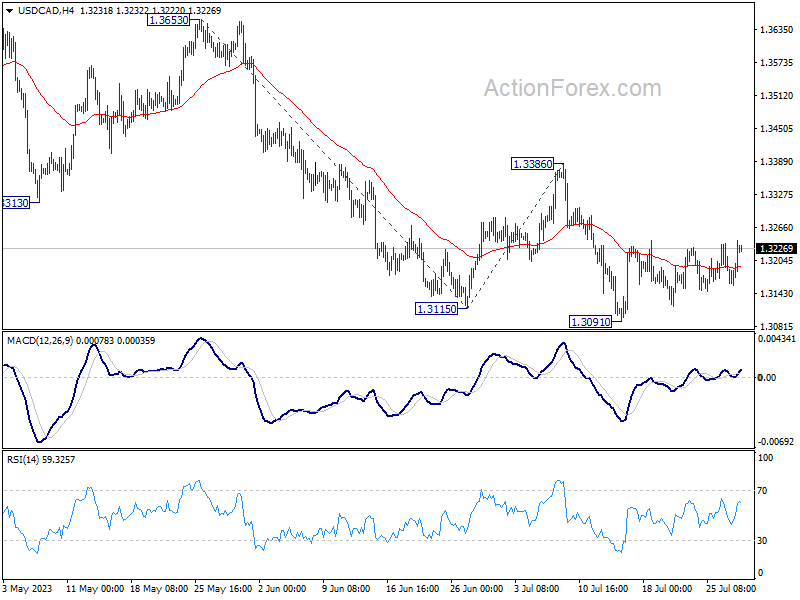

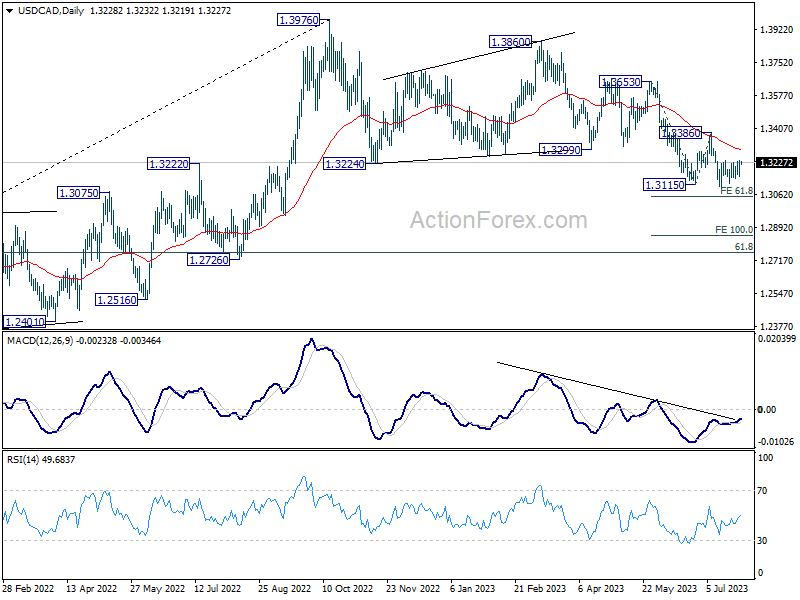

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3174; (P) 1.3208; (R1) 1.3259; More....

No change in USD/CAD's outlook as range trading continues. Intraday bias stays neutral at this point. Further decline is expected as long as 1.3386 resistance holds. Break of 1.3091 will resume larger fall and target 61.8% projection of 1.3653 to 1.3115 from 1.3386 at 1.3054. However, firm break of 1.3386 will indicate near term reversal and turn outlook bullish.

In the bigger picture, price actions from 1.3976 are viewed as a correction to up trend from 1.2005 (2021 low) only. But even so, deeper decline is expected as long as 1.3386 resistance holds. Further fall could be seen to 61.8% retracement of 1.2005 to 1.3976 at 1.2758. Meanwhile, break of 1.3386 will be a sign that the correction has completed and bring stronger rally back to retest 1.3976.

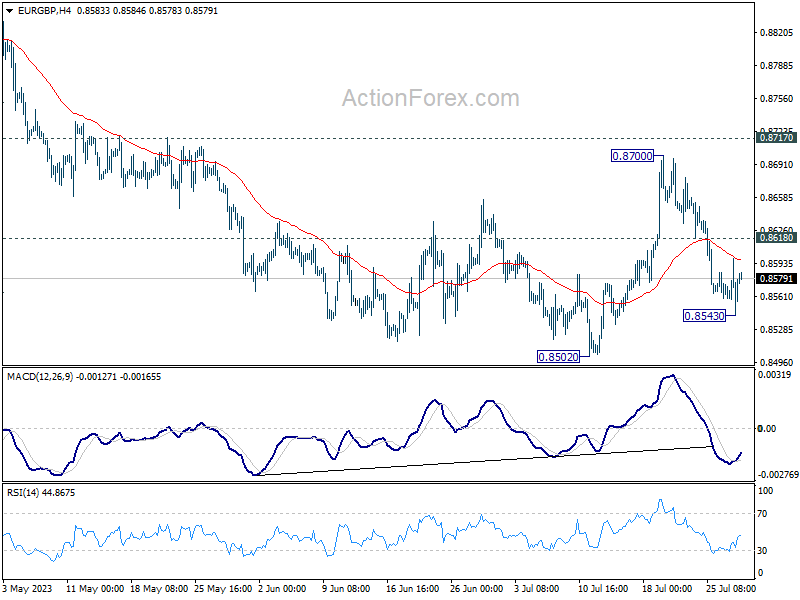

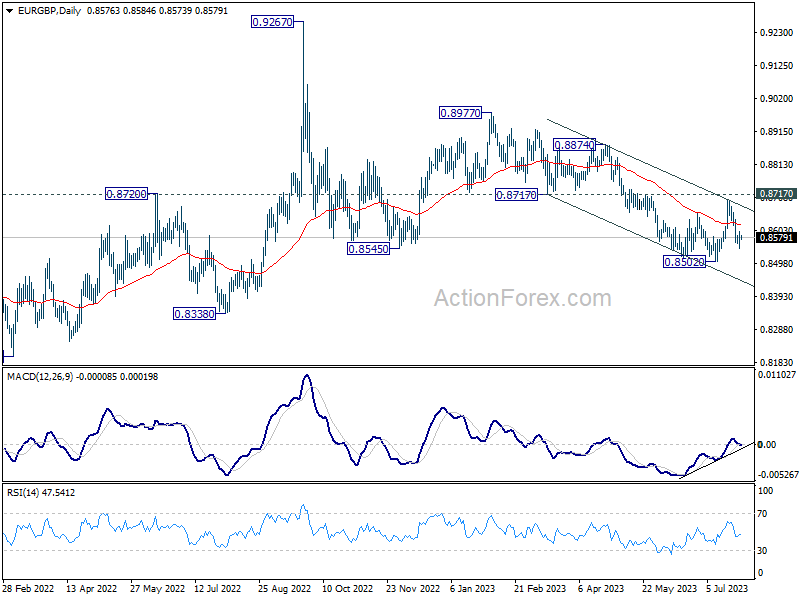

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8549; (P) 0.8574; (R1) 0.8605; More...

Intraday bias in EUR/GBP is turned neutral with current recovery. On the downside, below 0.8543 will target a test on 0.8502 low. Decisive break there will resume larger decline from 0.8977. On the upside, above 0.8618 minor resistance will turn bias back to the upside for 0.8700, and possibly further to 0.8717 key support turned resistance.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Firm break of 0.8717 support turned resistance will argue that it has completed with three waves down to 0.8502. Further break of 0.8977 will bring retest of 0.9267 high. Nevertheless, rejection by 0.8717, followed by break of 0.8502 will resume the decline towards 0.8201 (2022 low).

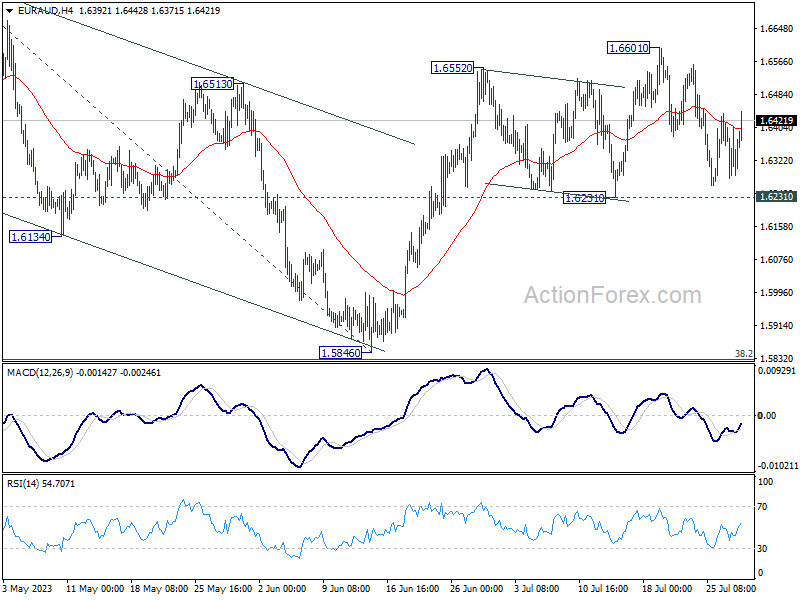

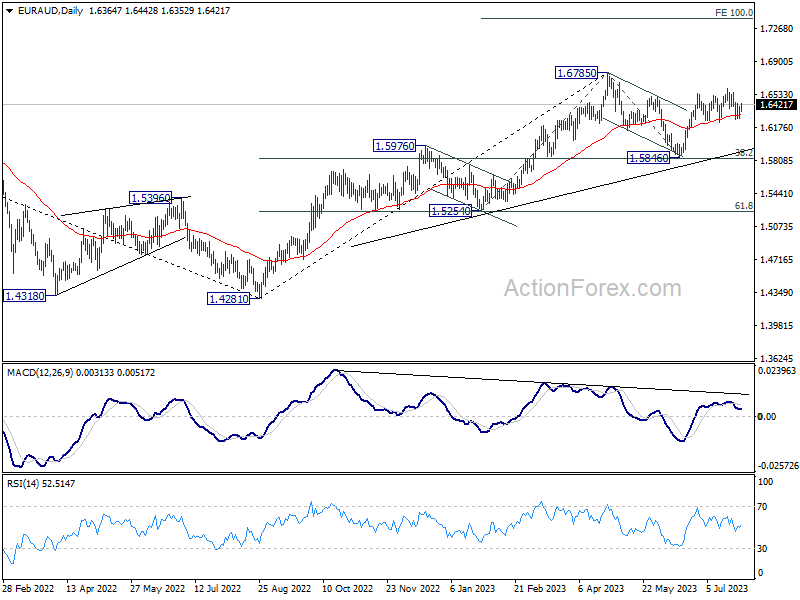

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6292; (P) 1.6351; (R1) 1.6422; More...

Sideway trading continues in EUR/AUD and intraday bias remains neutral at this point. With 1.6231 support intact, further rally is expected. On the upside, break of 1.6601 will resume the rebound from 1.5846 and target 1.6785 high next. However, firm break of 1.6231 will bring deeper fall to extend the corrective pattern from 1.6785.

In the bigger picture, with 38.2% retracement of 1.4281 to 1.6785 at 1.5828 intact, rally from 1.4281 is still in progress. Firm break of 1.6785 will confirm rise resumption. Next target is 100% projection of 1.5254 to 1.6785 from 1.5846 at 1.7377. On the other hand, rejection by 1.6785 will extend the corrective pattern with another fall leg. But outlook will stay bullish as long as 1.5828 holds.

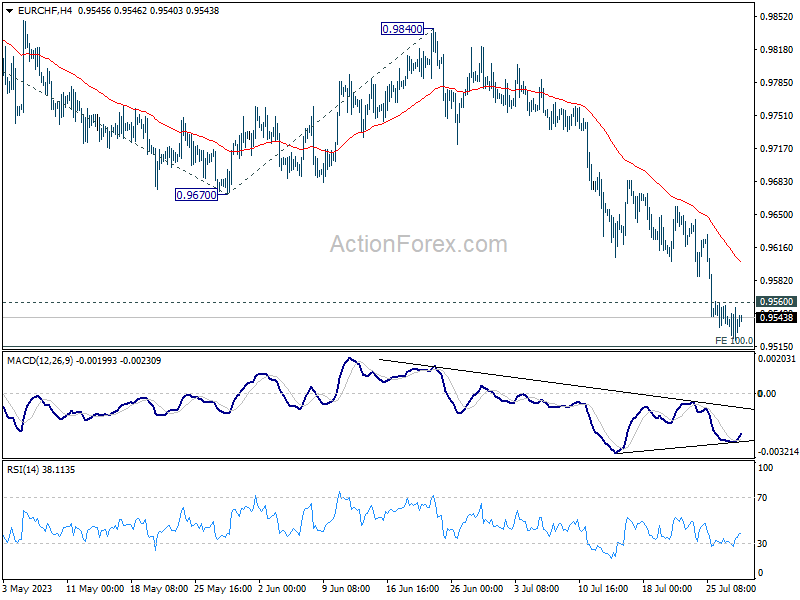

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9524; (P) 0.9540; (R1) 0.9559; More...

Intraday bias in EUR/CHF stays mildly on the downside despite loss of momentum. Sustained break of 100% projection of 0.9995 to 0.9670 from 0.9840 at 0.9515 will extend the fall from 1.0095 towards 0.9407 low. On the upside, above 0.9560 minor resistance will turn intraday bias neutral and bring consolidations. But outlook will stay bearish as long as 0.9670 support turned resistance holds.

In the bigger picture, medium term outlook is staying bearish as the pair is capped well below falling 55 W EMA (now at 0.9876). Down trend from 1.2004 (2018 high) is in favor to continue. Sustained break of 0.9407 will target 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. For now, this will remain the favored case as long as 0.9840 resistance holds, in case of strong rebound.