Sample Category Title

ECB Lagarde: Economic outlook deteriorated, inflation drivers changing

ECB President Christine Lagarde, struck a somber tone during the post-meeting press conference. She acknowledged that the economic outlook for Eurozone has "deteriorated" in the near term, citing persistent high inflation and tighter financial conditions as key factors pressuring the manufacturing output.

Lagarde stated, "High inflation and tighter financing... is weighing especially on manufacturing output, which is also being held down by weak external demand." Though she noted the resilience in the services sector, she cautioned that its "momentum is slowing". The economy is expected to "remain weak in the short run."

She then noted a shift in the drivers of inflation. External sources are easing, she noted, but domestic price pressures, including from rising wages and robust profit margins, are gaining prominence. "While some measures are moving lower, underlying inflation remains high overall," Lagarde pointed out.

ECB press conference live stream

https://www.youtube.com/watch?v=-HMXeiixuKM

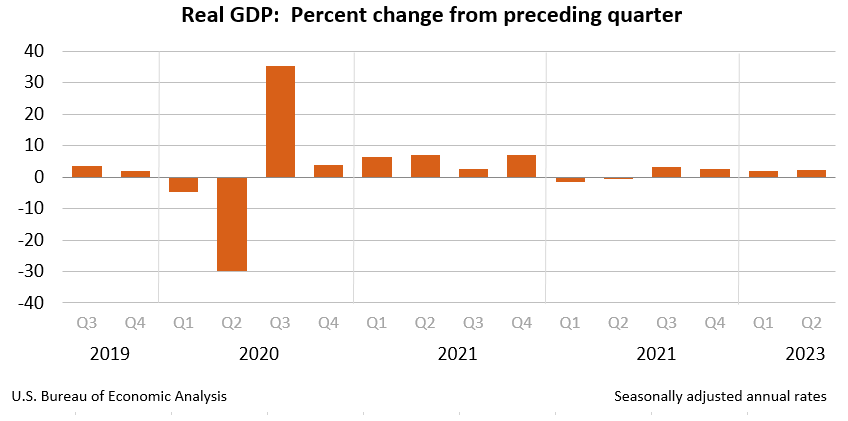

US GDP grew 2.4% in Q2, faster than Q1 and above expectations

US GDP grew 2.4% annualized in Q2, according to the "advance" estimate, well above expectation of 1.6%. That's also a faster growth than Q1's 2.0% annualized. PCE price index slowed from 4.1% to 2.6% while PCE core price index also fell form 4.9% to 3.8%.

BEA said: "Compared to the first quarter, the acceleration in GDP in the second quarter primarily reflected an upturn in private inventory investment and an acceleration in nonresidential fixed investment. These movements were partly offset by a downturn in exports, and decelerations in consumer spending, federal government spending, and state and local government spending. Imports turned down."

Also released, in June, durable goods orders rose 4.7% versus expectation of 1.0%. Ex-transport orders rose 0.6%, versus expectation of 0.1%. Goods trade deficit narrowed to USD -87.8B, versus expectation of USD -91.8B.

Initial jobless claims dropped slightly to 221k in the week ending July 21, below expectation of 233k.

ECB hikes 25 bps, maintains data-dependent approach

ECB sticks to the script and delivers another 25bps hike on its three key interest rates today, meeting market expectations. The main refinancing, marginal lending, and deposit rates now stand at 4.25%, 4.50%, and 3.75% respectively, effective August 2.

In its statement, the ECB highlighted the ongoing concerns around inflation, indicating it was poised to remain "above the target for an extended period", despite expectations of a decrease over the remainder of the year. It also noted that while some measures showed signs of easing, "underlying inflation remains high overall."

ECB reiterated that it is committed to setting interest rates at "sufficiently restrictive" levels "for as long as necessary". Stressing the bank's ongoing commitment to a data-dependent strategy, it added, "The Governing Council will continue to follow a data-dependent approach to determining the appropriate level and duration of restriction."

(ECB) Monetary policy decisions

Inflation continues to decline but is still expected to remain too high for too long. The Governing Council is determined to ensure that inflation returns to its 2% medium-term target in a timely manner. It therefore today decided to raise the three key ECB interest rates by 25 basis points.

The rate increase today reflects the Governing Council's assessment of the inflation outlook, the dynamics of underlying inflation, and the strength of monetary policy transmission. The developments since the last meeting support the expectation that inflation will drop further over the remainder of the year but will stay above target for an extended period. While some measures show signs of easing, underlying inflation remains high overall. The past rate increases continue to be transmitted forcefully: financing conditions have tightened again and are increasingly dampening demand, which is an important factor in bringing inflation back to target.

The Governing Council's future decisions will ensure that the key ECB interest rates will be set at sufficiently restrictive levels for as long as necessary to achieve a timely return of inflation to the 2% medium-term target. The Governing Council will continue to follow a data-dependent approach to determining the appropriate level and duration of restriction. In particular, its interest rate decisions will continue to be based on its assessment of the inflation outlook in light of the incoming economic and financial data, the dynamics of underlying inflation, and the strength of monetary policy transmission.

The Governing Council also decided to set the remuneration of minimum reserves at 0%. This decision will preserve the effectiveness of monetary policy by maintaining the current degree of control over the monetary policy stance and ensuring the full pass-through of the interest rate decisions to money markets. At the same time, it will improve the efficiency of monetary policy by reducing the overall amount of interest that needs to be paid on reserves in order to implement the appropriate stance.

The details of the change to the remuneration of minimum reserves are provided in a separate press release to be published at 15:45 CET.

Key ECB interest rates

The Governing Council decided to raise the three key ECB interest rates by 25 basis points. Accordingly, the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will be increased to 4.25%, 4.50% and 3.75% respectively, with effect from 2 August 2023.

Asset purchase programme (APP) and pandemic emergency purchase programme (PEPP)

The APP portfolio is declining at a measured and predictable pace, as the Eurosystem no longer reinvests the principal payments from maturing securities.

As concerns the PEPP, the Governing Council intends to reinvest the principal payments from maturing securities purchased under the programme until at least the end of 2024. In any case, the future roll-off of the PEPP portfolio will be managed to avoid interference with the appropriate monetary policy stance.

The Governing Council will continue applying flexibility in reinvesting redemptions coming due in the PEPP portfolio, with a view to countering risks to the monetary policy transmission mechanism related to the pandemic.

Refinancing operations

As banks are repaying the amounts borrowed under the targeted longer-term refinancing operations, the Governing Council will regularly assess how targeted lending operations and their ongoing repayment are contributing to its monetary policy stance.

***

The Governing Council stands ready to adjust all of its instruments within its mandate to ensure that inflation returns to its 2% target over the medium term and to preserve the smooth functioning of monetary policy transmission. Moreover, the Transmission Protection Instrument is available to counter unwarranted, disorderly market dynamics that pose a serious threat to the transmission of monetary policy across all euro area countries, thus allowing the Governing Council to more effectively deliver on its price stability mandate.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:45 CET today.

USD/JPY Technical: Bulls Rejected at 20-Day Moving Average

- The 20-day moving average has capped further upside in the USD/JPY so far since last Friday, 21 July.

- BoJ will release its monetary policy decision and latest quarterly outlook report tomorrow, 28 July. The consensus is an upgrade for its FY2023 consumer inflation forecast to be above 2% while maintaining the upper limit of the YCC at 0.50%.

- Recent minor downtrend phase from 21 July 2023 high of 141.95 to today, current intraday low of 139.38 may see a retracement.

- Key resistance zone at 140.70/142.50.

The recent rebound of 456 pips seen in the USD/JPY from the 14 July 2023 minor swing low of 137.24 retested the downward-sloping 20-day moving average last Friday, 21 July that is acting as resistance around 142.10/142.50.

Thereafter, the price actions of USD/JPY retreated twice so far this week at/near the 20-day moving average, declined by 254 pips to print a 5-day intraday low of 139.38 as of today, 27 July Asian session at this time of the writing.

The current short-term weakness of the USD/JPY has materialized ahead of the Bank of Japan (BoJ)’s monetary policy decision tomorrow where the consensus is an upgrade of its consumer inflation forecast to be above 2% (above BoJ’s target) for FY 2023 for its latest economic quarter outlook, and no change on the upper limit of the Yield Curve Control (YCC) programme on the yield of the 10-year Japanese Government Bond (JGB) to capped at 0.50%.

Interestingly, this upper limit of the YCC is a wild card for tomorrow as several ex-BoJ officials have advocated an upward revision to the 0.50% limit as the current economic conditions warrant it such as elevated sticky inflation conditions in Japan where the national-wide core (excluding fresh food), and core-core (excluding fresh food & energy) stood at 3.3% y/y, and 4.2% y/y for June; at a 31-year and 41-year high respectively.

Before BoJ releases its monetary policy decision and updated quarterly projections, BoJ officials will have a chance to access the leading Tokyo area’s consumer inflation data for July which is being released three hours earlier tomorrow as a key input to debate and assess the suitability of a change to the limits of the YCC programme.

Price actions have traced out a potential medium-term bearish reversal “Head & Shoulders”

Fig 1: USD/JPY medium-term trend as of 27 Jul 2023 (Source: TradingView, click to enlarge chart)

The price actions of USD/JPY have evolved into a potential bearish reversal “Head & Shoulders” configuration since the high of 29 May 2023.

The appearance of this potential “Head & Shoulders” suggests that the medium-term uptrend phase from the 16 January 2023 low of 127.22 to the 21 July 2023 high of 141.95 may have reached its terminal condition where a potential medium-term downtrend phase may materialize next, and a break below the 136.90 neckline support of the “Head & Shoulders” increases the odds.

Minor short-term downtrend from 21 July high reached an oversold condition

Fig 2: USD/JPY minor short-term trend as of 27 Jul 2023 (Source: TradingView, click to enlarge chart)

The recent minor downtrend phase from the 21 July 2023 high of 141.95 to today, 27 July’s current intraday low of 139.38 has reached an oversold condition as indicated by the hourly RSI oscillator.

This observation suggests the risk of a minor bounce to retrace a portion of the minor downtrend with the key resistance zone coming in at 140.70/142.50.

Watch the 142.50 key medium-term pivotal resistance to maintain the short-term bearish bias and a break below the 139.15 near-term support exposes the next support at 137.65/136.90 (also the neckline of the “Head & Shoulders” & 200-day moving average).

On the other hand, a clearance above 142.50 invalidates the bearish bias to see the next resistance coming in at 143.60.

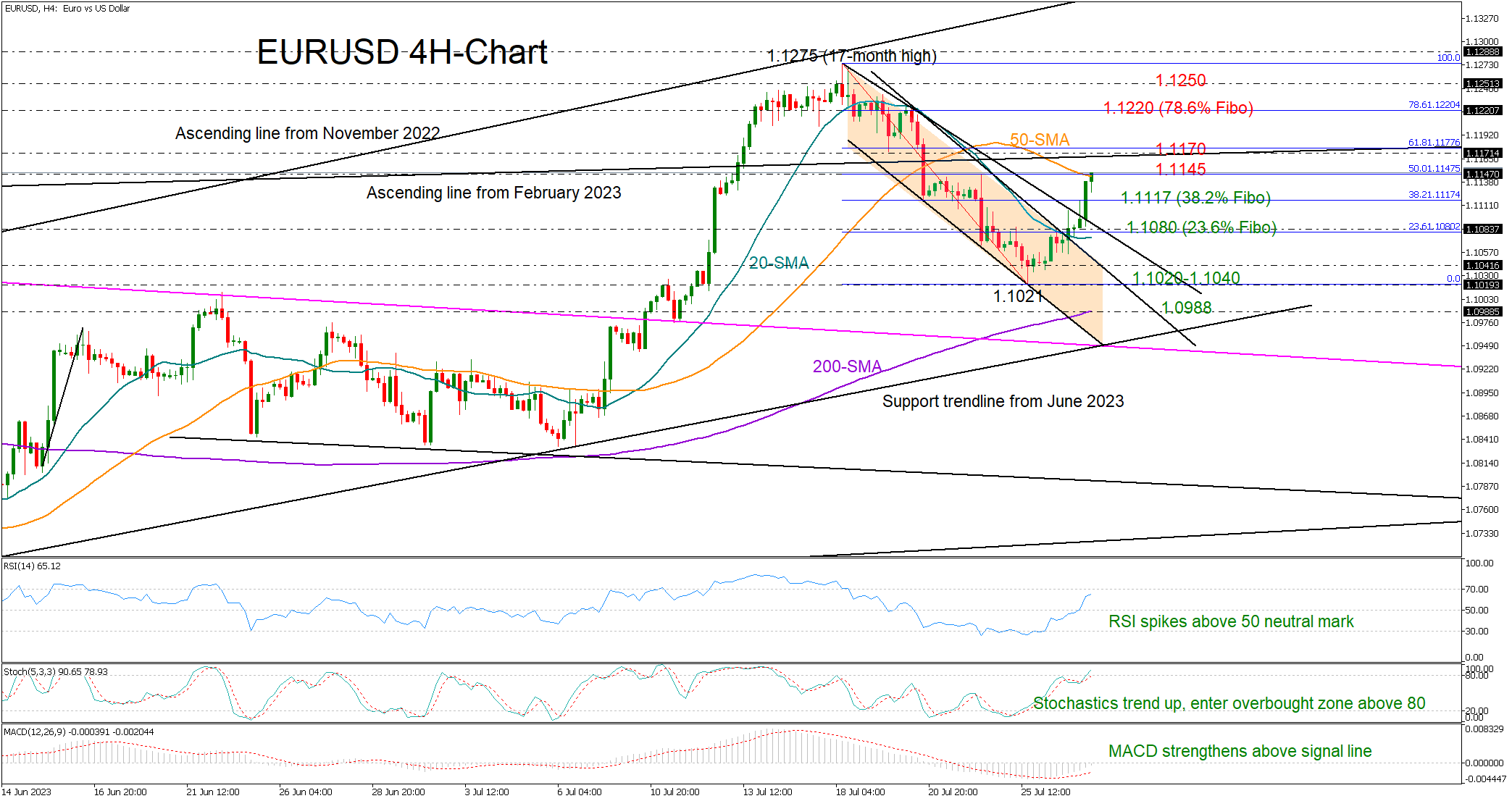

EURUSD Cheers Up Before ECB Rate Decision

EURUSD jumped into the 1.1100 area ahead of the ECB policy announcement early on Thursday, exiting its bearish channel on the four-hour chart.

The 50-period simple moving average (SMA) is currently keeping the bulls busy around 1.1145 and if it proves tough to surpass, the pair could switch into corrective mode. The 61.8% Fibonacci retracement of the latest downfall is adding extra importance to that region, while slightly higher at 1.1170, the resistance line, which links the highs from February and April 2022, could also force a pullback.

Encouragingly, the clear positive trajectory in the momentum indicators suggests there might be more upside pressure. A decisive close above 1.1170 could be a prerequisite for a rally towards the 1.1220 level, where the 78.6% Fibonacci mark is located. Even higher, the bulls will attempt to strengthen the long-term uptrend above the 1.1250-1.1275 resistance and towards the 1.1345-1.1365 territory. Note that the long-term ascending line from the November 2022 low is in the neighborhood.

If the bears retake control below the 38.2% Fibonacci of 1.1117, the price may seek a shelter near the 23.6% Fibonacci of 1.1080 and the 20-period SMA. A step lower could halt within the 1.1040-1.1020 support area. If this collapses, the spotlight will fall on the 200-period SMA currently at 1.0990.

Summing up, EURUSD could preserve positive momentum in the coming sessions, though only a successful penetration of the 1.1170 mark would reverse the previous bearish wave from 1.1275.

ECB Interest Rate Decision Could Spark a Reversal

On Thursday, the European Central Bank is expected to hike interest rates by a quarter percentage point to 3.75%. After July, the certainty of further rate hikes is unclear, leading to a craving for guidance in financial markets. The ECB may turn more cautious in signaling future policy while confirming a data-dependent approach. Core inflation remains stubbornly high, and the impact of a weakening economy on policy is uncertain. Bank lending data suggests tightening financing conditions may lead to speculation that rates are close to peaking.

EURUSD - H4 Timeframe

EURUSD, as seen from the chart, is trading within a drop-base-drop supply zone, with the intersection of the 50-period moving average. Though these aren’t exactly my premium kind of trade ideas, I believe the ‘rates’ decision from the ECB later today will go a long way to influence whether or not this ends up playing out according to the trade idea.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.10867

- Invalidation: 1.11528

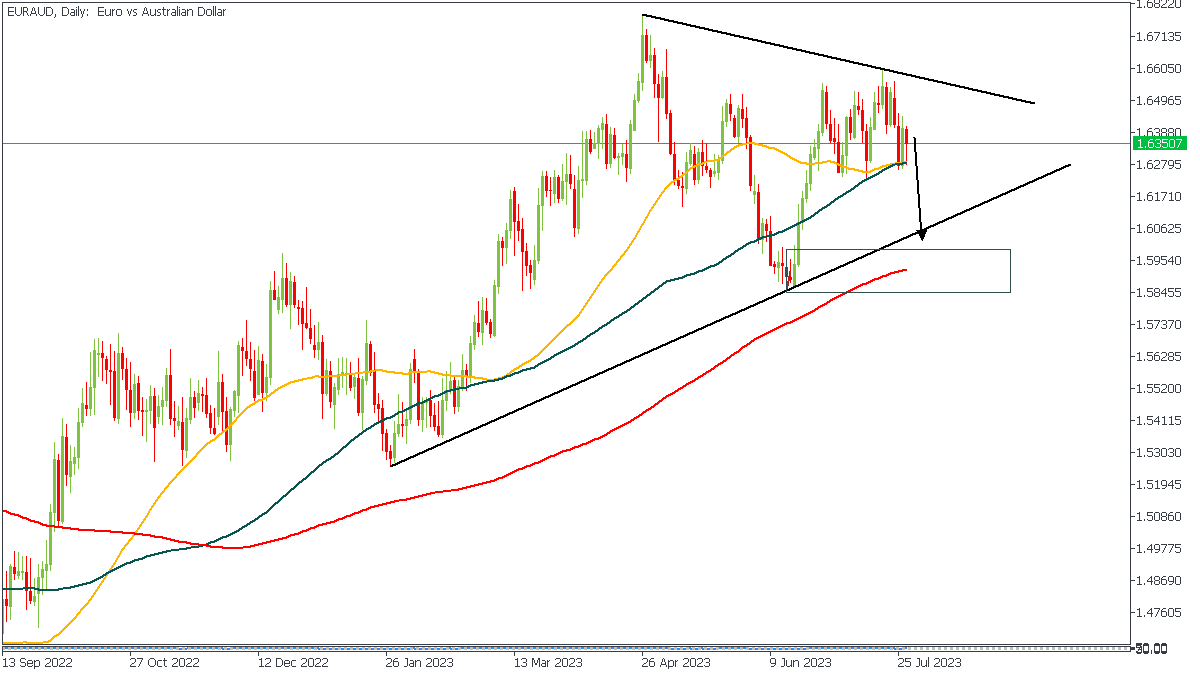

EURAUD - D1 Timeframe

EURAUD is clearly trading inside a wedge pattern, with the most recent price action coming from the rejection at the trendline resistance. From here, this means that we can expect to see a continued drop in prices until it reaches the trendline support - my thoughts. I understand that the moving average threatens the further decline of price. Hence the need to watch out for the outcome of the ECB release patiently.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.60888

- Invalidation: 1.64472

EURCAD - D1 Timeframe

EURCAD is on its way downwards, having gotten rejected from the resistance trendline. Currently, the price action doesn’t appear to be clear yet since there hasn’t really been a clear break of structure. My plan here, however, is to watch for a break and retest either of the trendlines, then position to trade in the direction of the breakout. In the meantime, I expect that we will see a continuation of the bearish movement soon.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.44686

- Invalidation: 1.48876

CONCLUSION

The trading of CFDs comes at a risk. Thus, to succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.

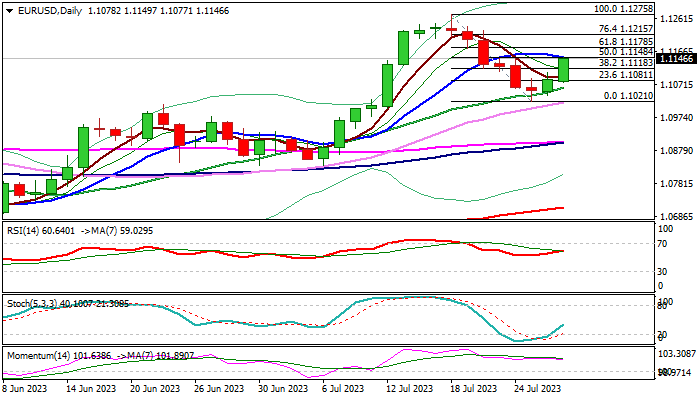

EUR/USD: Bulls Accelerate Ahead of Expected ECB Rate Hike

EURUSD accelerated higher on Thursday, gaining 0.6% in late Asian / European trading, lifted by expectations for 0.25% rate hike today and signals of possible another hike in September.

The ECB continues to face threats from high inflation, which eased significantly but is still 2.5 times above 2% target, while underlying inflation stands near record highs and may rise more.

On the other hand, sharp rise in borrowing cost, slowed economic growth and threatening of falling again into recession, which prompts policymakers to be very cautious in their near-future decision.

Technical picture on daily chart improved as fresh strength confirmed formation of Doji reversal pattern, signaling an end of 1.1275/1.1021 corrective phase.

North-heading RSI / stochastic and strong bullish momentum contribute to positive signals.

Bulls cracked pivotal barrier at 1.1148 (50% retracement / 10DMA) with break here to open way for extension towards 1.1178/1.1215 (Fibo 61.8% and 76.4% respectively) and possible stronger acceleration if ECB shows more hawkish stance.

Close above broken Fibo 38.2% (1.1118) is seen as minimum requirement to keep fresh bulls in play.

Res: 1.1178; 1.1215; 1.1229; 1.1275.

Sup: 1.1118; 1.1081; 1.1062; 1.1021.

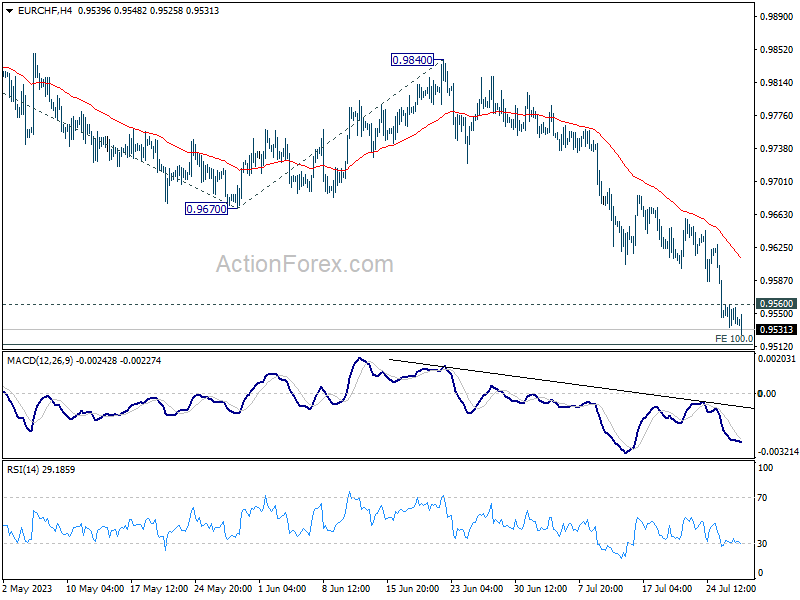

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9532; (P) 0.9547; (R1) 0.9559; More...

EUR/CHF's decline continues today and intraday bias stays on the downside for 100% projection of 0.9995 to 0.9670 from 0.9840 at 0.9515. Firm break there will pave the way to 0.9407 low. On the upside, above 0.9560 minor resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 0.9670 support turned resistance holds.

In the bigger picture, medium term outlook is staying bearish as the pair is capped well below falling 55 W EMA (now at 0.9876). Down trend from 1.2004 (2018 high) is in favor to continue. Sustained break of 0.9407 will target 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. For now, this will remain the favored case as long as 0.9840 resistance holds, in case of strong rebound.