Sample Category Title

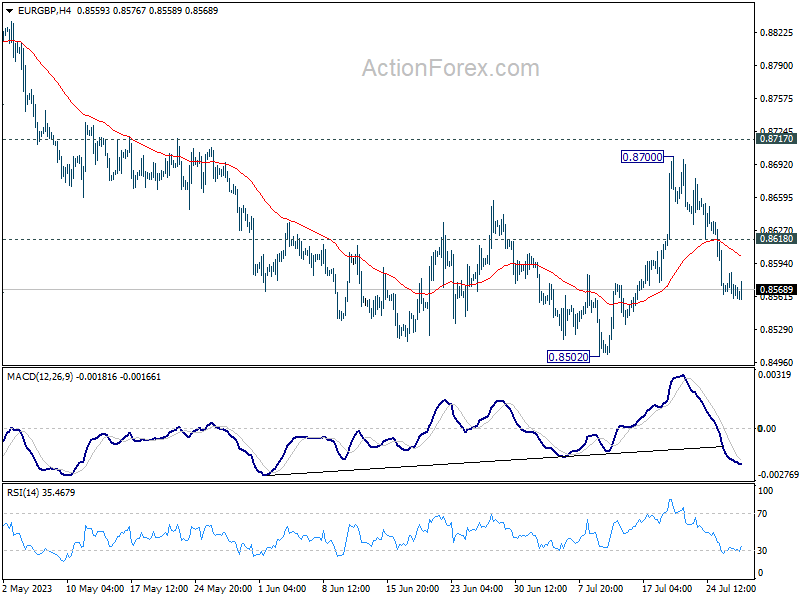

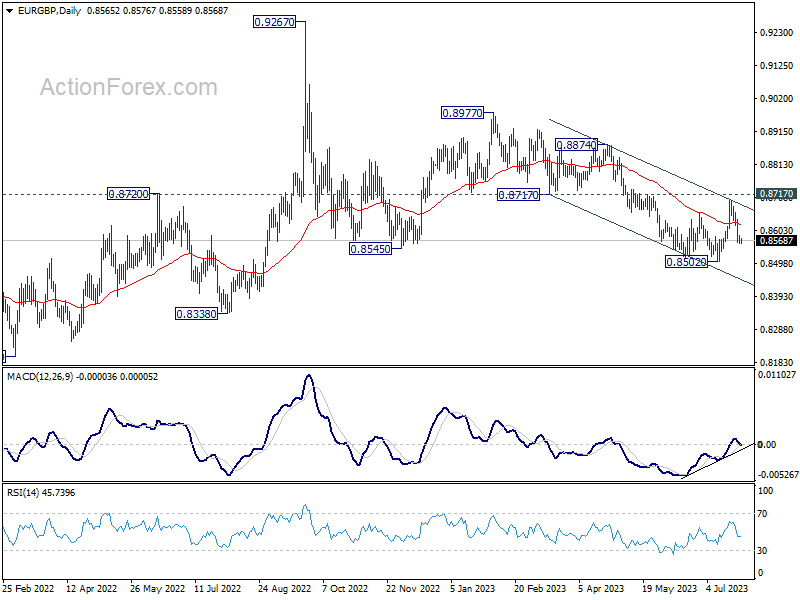

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8556; (P) 0.8571; (R1) 0.8582; More...

EUR/GBP's fall from 0.8700 is still in progress and intraday bias stays on the downside for retesting 0.8502 low. Decisive break there will resume larger decline form 0.8977. On the upside, above 0.8618 minor resistance will turn intraday bias neutral first.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Firm break of 0.8717 support turned resistance will argue that it has completed with three waves down to 0.8502. Further break of 0.8977 will bring retest of 0.9267 high. Nevertheless, rejection by 0.8717, followed by break of 0.8502 will resume the decline towards 0.8201 (2022 low).

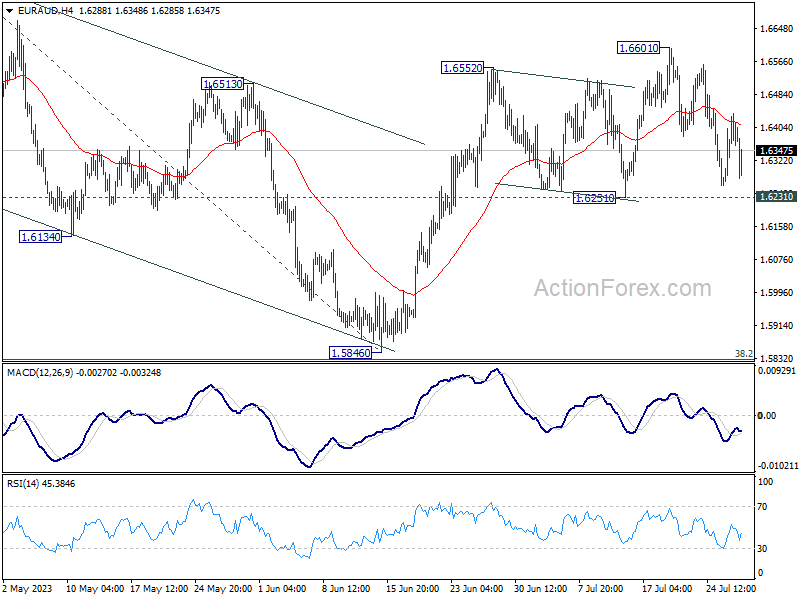

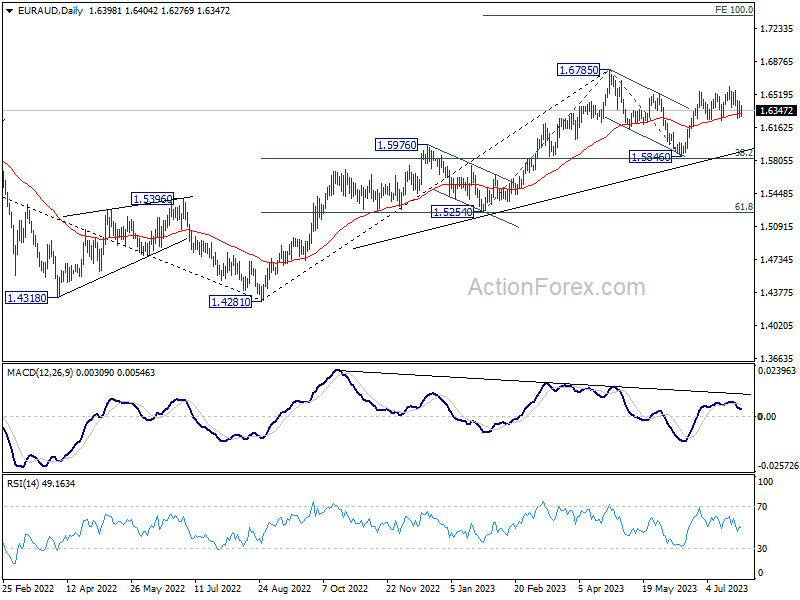

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6305; (P) 1.6372; (R1) 1.6471; More...

EUR/AUD is staying in range below 1.6601 and intraday bias remains neutral. Further rally is in favor with 1.6231 support intact. On the upside, break of 1.6601 will resume the rebound from 1.5846 and target 1.6785 high next. However, firm break of 1.6231 will bring deeper fall to extend the corrective pattern from 1.6785.

In the bigger picture, with 38.2% retracement of 1.4281 to 1.6785 at 1.5828 intact, rally from 1.4281 is still in progress. Firm break of 1.6785 will confirm rise resumption. Next target is 100% projection of 1.5254 to 1.6785 from 1.5846 at 1.7377. On the other hand, rejection by 1.6785 will extend the corrective pattern with another fall leg. But outlook will stay bullish as long as 1.5828 holds.

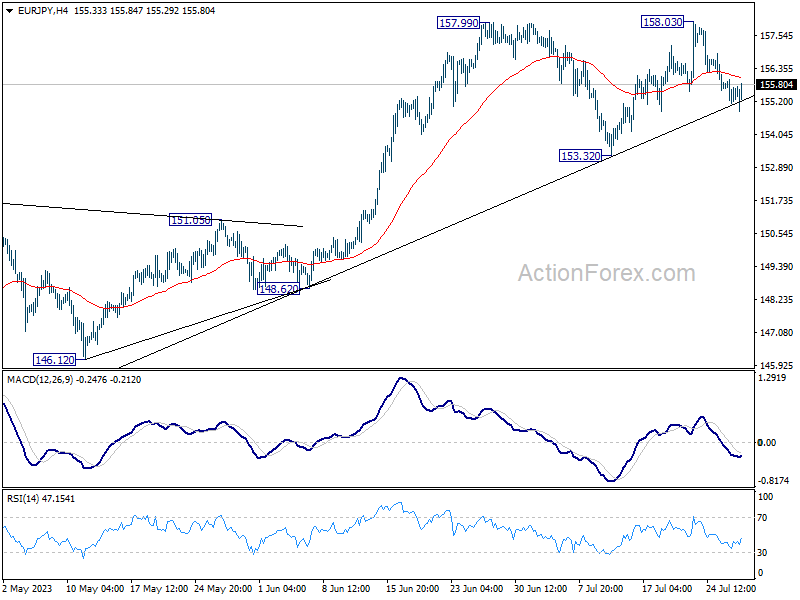

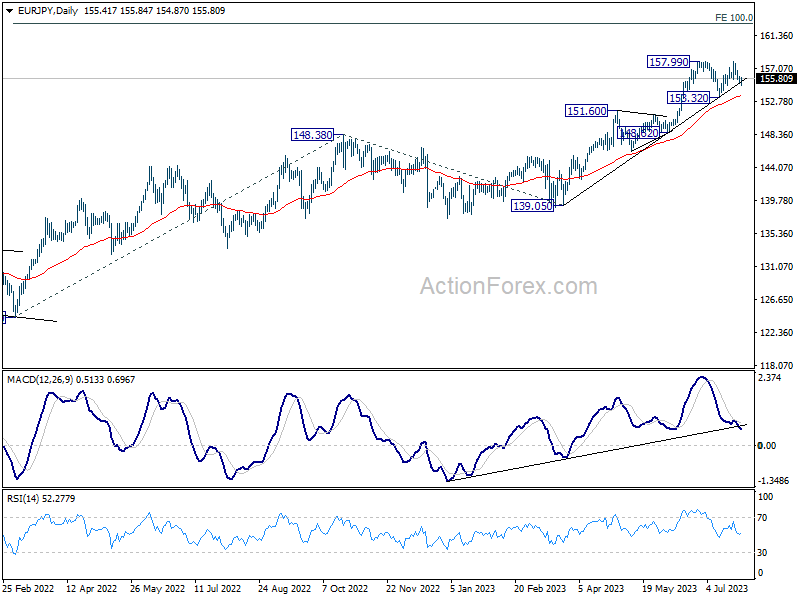

EUR/JPY Daily Outlook

Daily Pivots: (S1) 155.09; (P) 155.54; (R1) 155.93; More....

Intraday bias in EUR/JPY is mildly on the downside as fall from 158.03 is trying to extend lower. But downside should be contained by 153.32 support to complete the corrective pattern from 157.99. On the upside, decisive break of 157.99/158.03 will confirm resumption of larger up trend, and target 162.82 projection level next.

In the bigger picture, as long as 151.60 resistance turned support holds, rise from 114.42 (2020 low) is in progress. On resumption, next target is 100% projection of 124.37 to 148.38 from 138.81 at 162.82. Nevertheless, sustained break of 151.60 will argue that larger correction is already underway.

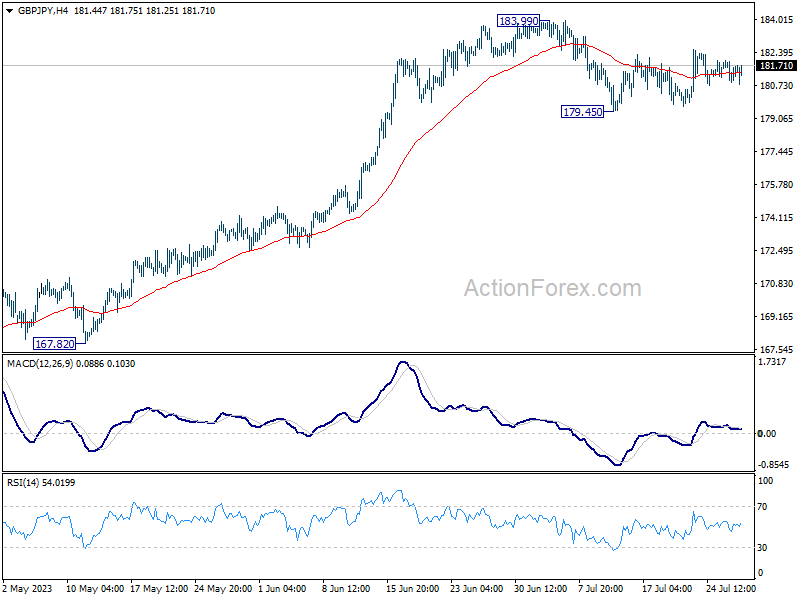

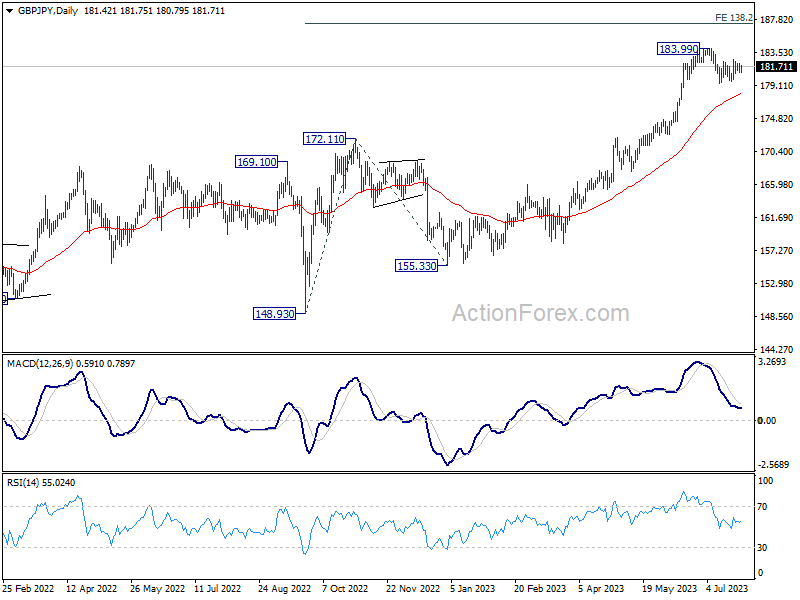

GBP/JPY Daily Outlook

Daily Pivots: (S1) 180.94; (P) 181.49; (R1) 182.07; More...

GBP/JPY is still extending sideway trading and intraday bias remains neutral. On the downside, break of 179.45 will resume the correction from 183.90 to 55 D EMA (now at 178.11) and possibly below. On the upside, firm break of 183.99 high will resume larger up trend to 187.36 projection level.

In the bigger picture, as long as 172.11 resistance turned support holds, up trend from 123.94 (2020 low) is expected to continue. On resumption, next target is 138.2% projection of 148.93 to 172.11 from 155.33 at 187.36, and then 195.86 (2015 high). Nevertheless, firm break of 172.11 will argue that larger correction is already underway.

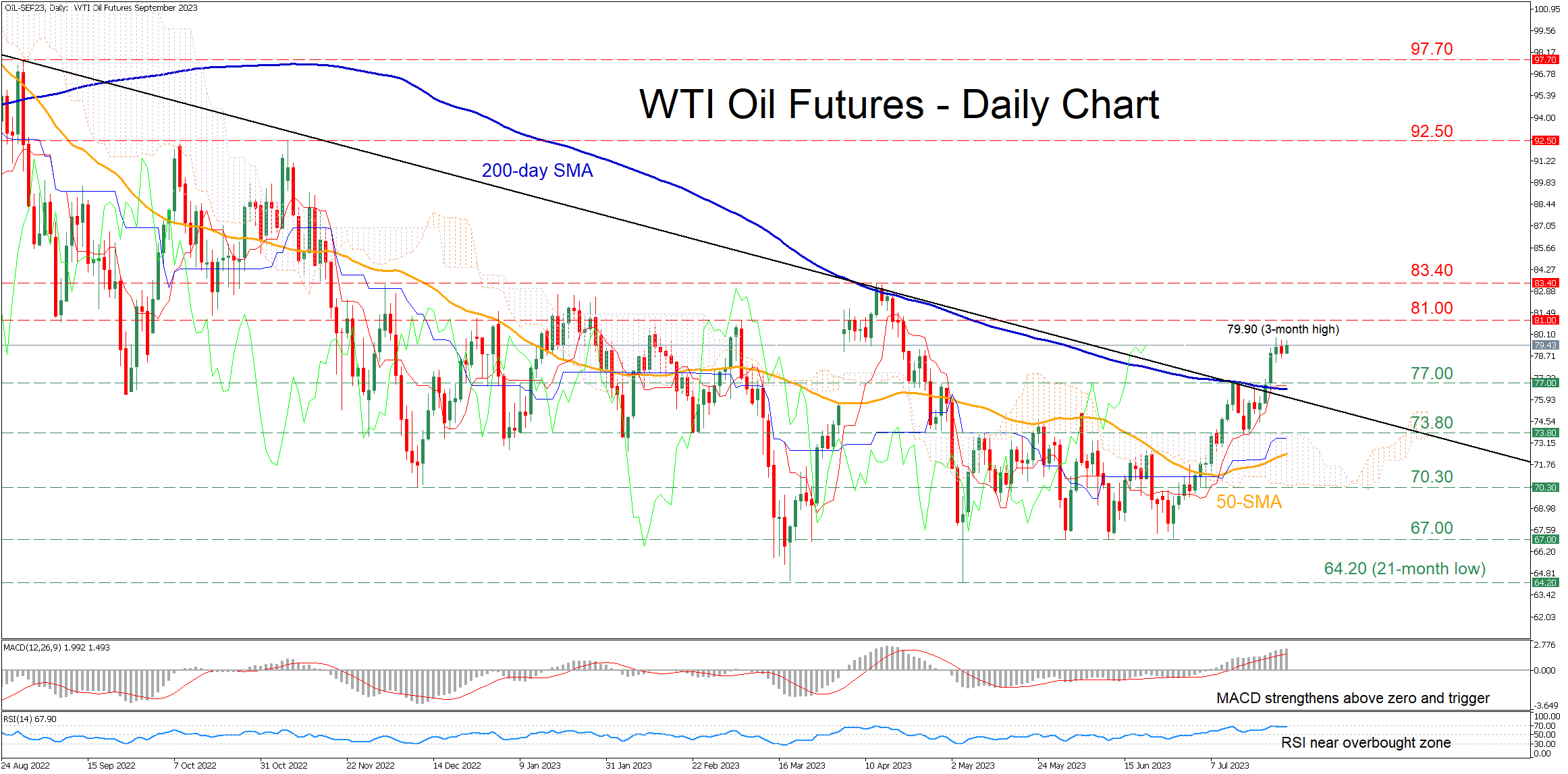

WTI Oil Futures Consolidate Near 3-Month Peak

WTI oil futures (September delivery) have been in a steady uptrend since late June, crossing above both the 50- and 200-day simple moving averages (SMAs) as well as the descending trendline that connects their lower highs since September 2022. However, in the last couple of daily sessions, oil has shown signs of consolidation near its three-month peak of 79.90.

The momentum indicators currently suggest that bullish forces are holding the upper hand. Specifically, the RSI has flatlined slightly below its 70-overbought threshold, while the MACD is strengthening above both zero and its red signal line at its highest level since April.

Should the recent advance extend, the bulls could target the March peak of 81.00. Piercing through that zone, the price might challenge the 2023 high of 83.40 registered in April. Further advances could then cease at the November 2022 high of 92.50.

Alternatively, if the rebound falters and the price reverses downwards, the previous resistance of 77.00 could serve as initial support. Sliding beneath that floor, oil may descend towards 73.80 before the December 2022 bottom of 70.30 gets tested. Even lower, the 67.00 hurdle, which held strong three times during May and June, could provide downside protection.

In brief, WTI oil futures have been trading sideways for the past few sessions after failing to post a fresh three-month high. Nevertheless, it is likely that the price is building a base ahead of an upcoming bullish breakout as near-term risks remain tilted to the upside.

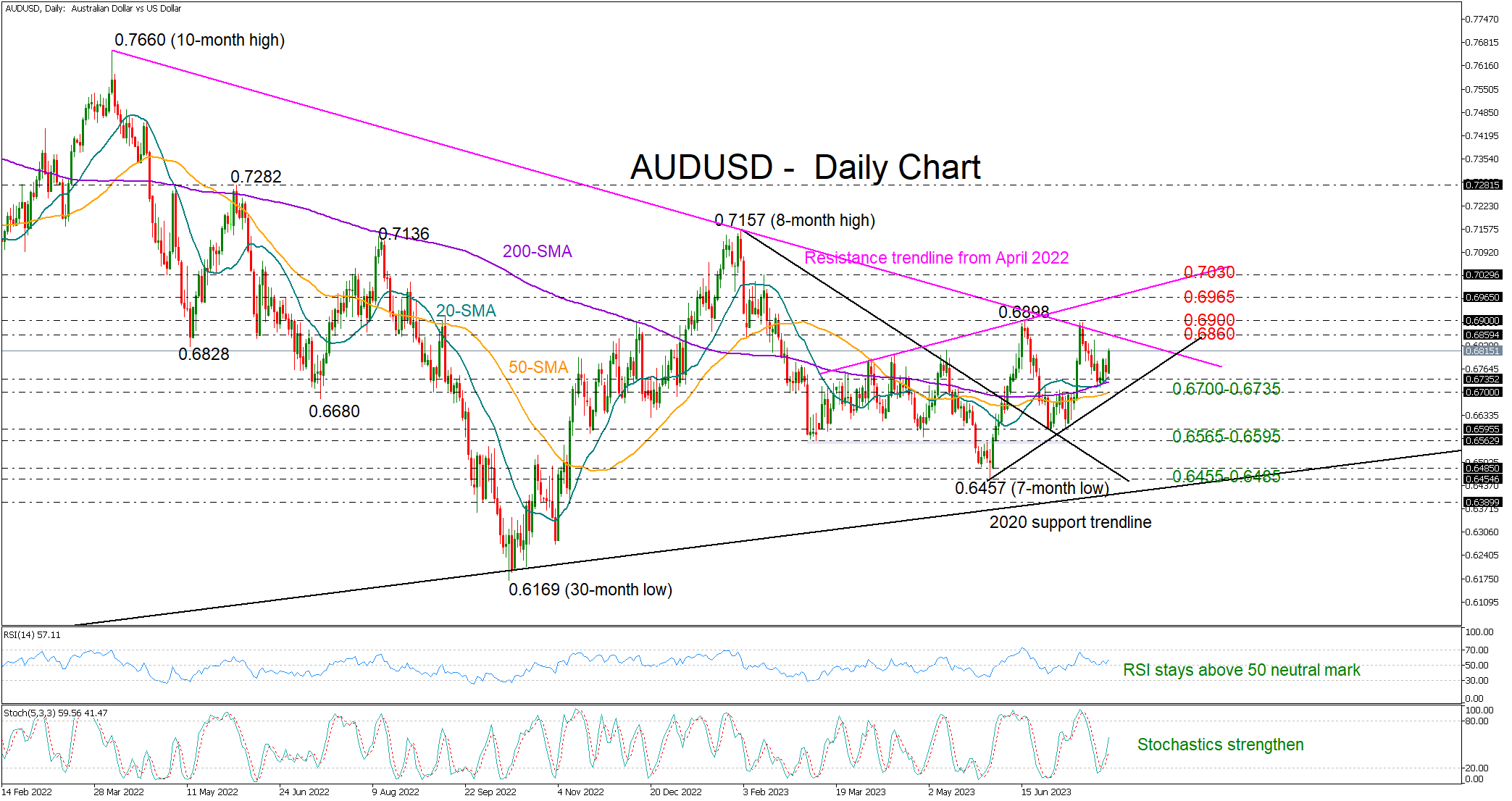

AUDUSD Poised for An Upturn

AUDUSD seems to have secured a strong foothold near 0.6735 and around its 20- and 200-day simple moving averages (SMAs), increasing optimism that the next bull run to 0.6900 could happen soon.

From a technical perspective, the pair could recoup some extra ground in the short term as the RSI has avoided a drop below its 50 neutral mark, turning softly higher in the aftermath. Likewise, the stochastic oscillator has changed direction to the upside.

Still, traders could maintain some caution as the tough descending line from April 2022 at 0.6860 could postpone the battle with the 0.6900 mark. If buying appetite boosts the price above the latter, the spotlight will shift to the resistance line, which connects the highs from April and June, at 0.6965. Snapping that barrier, the bulls may next take a breather around 0.7030 and then push towards the 2023 peak of 0.7157.

Alternatively, the pair could drift lower to re-examine its SMAs within the 0.6700-0.6735 territory. Failure to pivot there could activate strong selling pressures towards the former support zone of 0.6565-0.6595. If this cracks too, the pair may revisit June’s floor of 0.6455-0.6485.

In brief, AUDUSD could experience a positive session in the short term, though whether it will sustainably pierce through the 0.6900 resistance remains to be seen.

US Dollar Weakens After the Fed’s Decision to Raise Rates

After the 11th increase, the interest rate reached 5.5%.

At the same time, the US dollar weakened because:

- market participants may consider this to be the last hike in the cycle (although Powell admitted the possibility of a rate hike in September);

- the Fed is no longer considering a recession scenario, which has reduced the relevance of cash as a defensive asset. Reuters reports analysts saying Powell's tone has become more dovish.

The weakening of the US dollar led to an increase in the prices of currencies traded in tandem with the USD. Thus, the EUR/USD rate rose by 0.75% from the low of the week, where the support block is located:

- level 50% of growth A→B;

- median line of the ascending channel (shown in blue);

- level 1.02, which worked as a resistance in June.

At the same time, the nearest resistance is at the level of 1.111, which was support last week. Pay attention to the rate of decline in the price on the EUR/USD chart on the 20th and 24th — a sign of the initiative of the bears. Will they be able to break through the support block, or will the bulls intend to use it as a support for a new swing within the channel shown in blue? There should be more arguments for reasoning after the news from the ECB is released today at 15:15 GMT+3.

Trade global forex with the Innovative Broker of 2022*. Choose from 50+ forex markets 24/5. Open your FXOpen account now or learn more about trading forex with FXOpen.

* FXOpen International, Innovative Broker of 2022, according to the IAFT

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

China Equities Maintain Short-term Bullish Momentum Ex-post Politburo and FOMC

- The press release of the recently concluded China’s Politburo meeting consisted of a more expansionary tone such as the implementation of “counter-cyclical” measures.

- A dovish tilt is now being priced in by interest rates futures after yesterday’s FOMC meeting. Based on the CME FedWatch tool, the odds have increased to bring forward the expected first Fed Funds rate cut to March 2024 from May/June 2024.

- This latest set of dovish expectations on the future path of the Fed’s monetary policy has negated the prior steep depreciation of the yuan against the US dollar.

- Short-term positive animal spirits have been revived in China equities, and its proxies (the Hang Seng Indices) ex-post Politburo & FOMC.

The market’s reaction so far has been positive in terms of risk-on behaviour toward China equities and their proxies (Hang Seng Index, Hang Seng TECH Index & Hang Seng China Enterprises Index) ex-post press release on the outcome of the July’s Politburo meeting that concluded on Monday, 24 July after the close of the Asian session as well as yesterday’s ex-post US central bank, Federal Reserve’s FOMC meeting on its interest rate policy.

The Politburo is a top decision-making body led by President Xi that set key economic policy agenda for China, and Monday’s meeting set the agenda for the coming months to implement expansionary policies to address the current weak internal demand environment. It vowed to implement a counter-cyclical policy to boost consumption, more support for the property market, and ease local government debt.

The share prices of China ADR listed in the US stock exchanges have a remarkable intraday performance on Monday, 24 July US session. China’s Big Tech such as Alibaba (BABA), and Baidu (BIDU) ended the US session with gains of around 5%. A basket of China stocks listed as exchange-traded funds in the US soared as well, the KranShares CSI China Internet ETF (KWEB), and Invesco Golden Dragon China ETF (PGJ) rallied by +4.5% and +4% respectively, notched their best single day return since May 2023.

Even though the press release lacks the details of the implementation of upcoming fiscal stimulus measures (again), and refrains from enacting major stimulus measures that increase the risk of debt overhang in the property sector, it is the choice of words, and tonality used that sparked the risk-on behaviour. Firstly, President Xi’s key phrase on China’s housing market, houses are for living, not for speculation” has been omitted for the first since mid-2019” which suggests that more leeway to negate the ongoing weakness in houses prices such as easing home buying restrictions in major cities such as Shanghai and Beijing.

Secondly, the term “counter-cyclical” measures are being emphasized which suggests that boosting domestic demand takes priority over infrastructure spending. Given the heightened risk of a deflationary spiral taking shape in China and a “liquidity trap” situation where more accommodative monetary policy may lead to lesser marginal economic growth, the key solution to break the adverse deflationary spiral and its liquidity trap aftereffects is to shore up consumer confidence via expanding domestic demand actively.

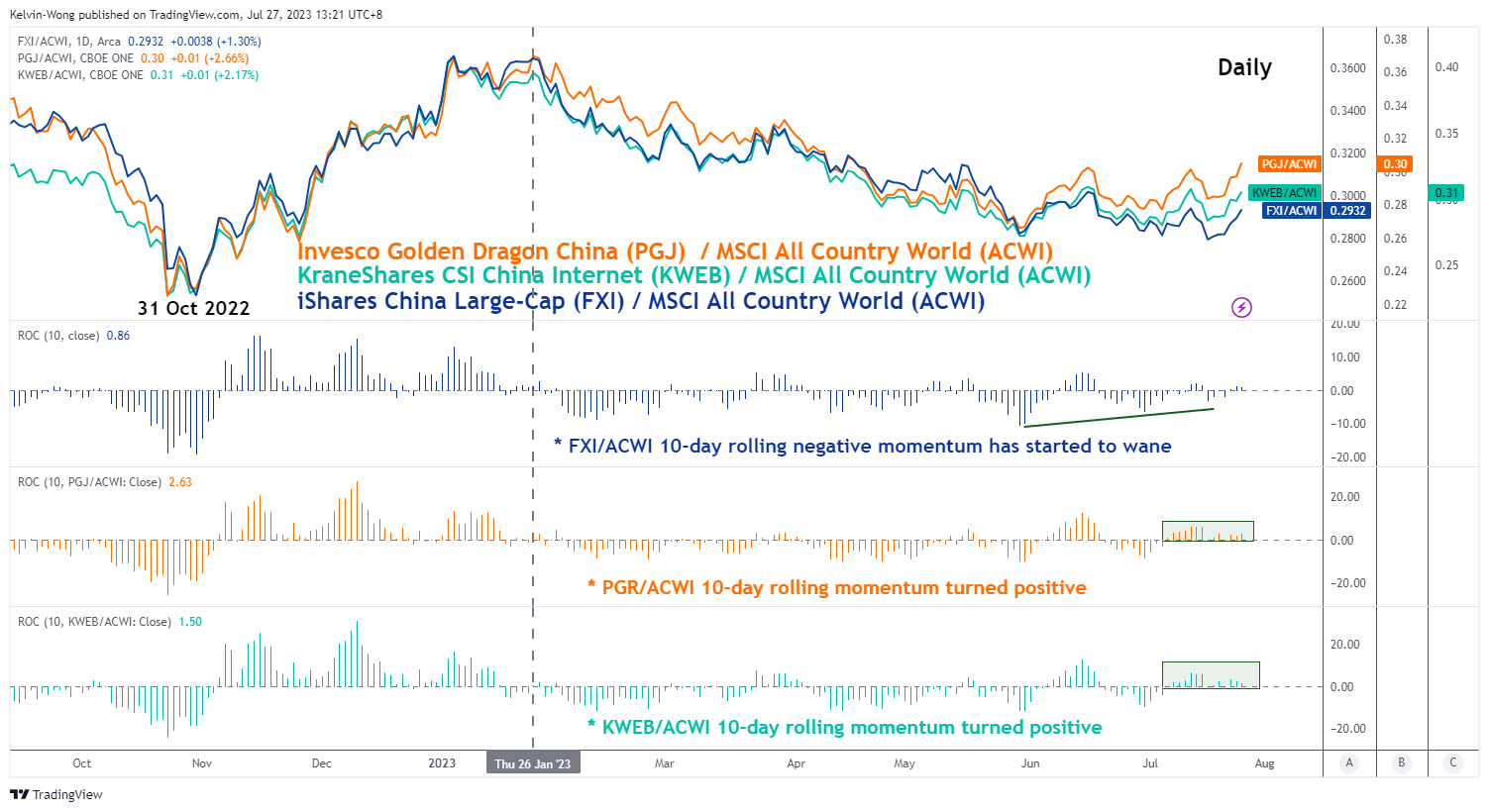

Outperformance of China ADR exchange-traded funds supported by a stronger yuan

Fig 1: Relative momentum of China ADRs ETFs vs. MSCI All Country World ETF of 26 Jul 2023 (Source: TradingView, click to enlarge chart)

Overall, short-term sentiment seems to have turned bullish for China equities where China ADR ETFs have outperformed major US benchmark US stock indices on a month-to-date horizon as of yesterday, 26 July 2023; the KranShares CSI China Internet ETF (KWEB), and Invesco Golden Dragon China ETF (PGJ) gained by +12% and +13.14% respectively over S&P 500 (+2.61%), and MSCI All Country World Index ETF (+2.97%).

Also, yesterday’s Fed Chair Powell ex-post FOMC press conference indicated that the Fed will be data-dependent in deciding whether to pause or hike the Fed Funds rate at its next FOMC meeting on 20 September. This implies that the Fed is likely not in a mode of raising interest rates at every other meeting after yesterday’s expected 25 basis points hike to bring the Fed Funds rate to a 22-year high at 5.25% to 5.50%.

Markets seem to be pricing in a more dovish tilt on the expected start of the first Fed Funds rate cut. Based on the CME FedWatch tool derived from the 30-day Fed Funds futures pricing data, the odds have increased for the first expected cut to occur on the 20 March 2024 FOMC meeting with a combined probability of 56.07%. Previously, before yesterday’s FOMC, higher odds for the expected first-rate cut were clustered between the 1 May and 19 June 2024 FOMC meetings.

The current dovish tilt on the expected future trajectory of the Fed Funds rate has negated further upside yield premium of the US’s 2-year Treasury note over China’s 2-year sovereign bond. Since Monday, 24 Jul, the yield premium has narrowed by 11 bps to 2.75% from 2.86% as of today at this time of the writing which in turn supported the yuan from a further deprecation against the US dollar.

USD/CNH (offshore yuan) remained below its 20-day moving average

Fig 2: USD/CNH medium-term trend as of 27 Jul 2023 (Source: TradingView, click to enlarge chart)

The yuan has started to strengthen against the US dollar in the short-term horizon since last Thursday, 20 July which in turn created a positive feedback loop back that reinforces the bullish sentiment towards China equities. The USD/CNH (offshore yuan) has failed to break above its 20-day moving average, acting as a key intermediate resistance at 7.2160 with a bearish momentum reading seen on its daily RSI oscillator.

Hence, further potential weakness in the USD/CNH is likely to be able to kickstart short-term uptrend phases for China equities and its proxies.

ECB Policy Meeting to Large Extent Might Follow Scrip of Fed Meeting

Markets

Seldom the day of a Fed decision yielded as little news for markets and analysts as was the case yesterday. The Fed policy decision annex press conference hardly caused any ripples. As expected, Powell and Co in an unanimous vote raised the target range for the Fed Fund rate by 25 bps to 5.25%/5.50%. The Fed policy statement was an almost exact copy from the June text. At the press conference, Chair Powell had only one message: the Fed entered a completely data dependent mode. There is still a way to go for to reach its 2.0% goal in a sustainable way, but a decision on additional tightening will be made on the basis of upcoming data, with the Fed chair especially mentioning two CPI releases and payrolls reports and the Employment Cost index as key pointers in the Fed’s decision making process at the September meeting. The Fed still ‘excludes’ rate cuts this year. The reaction, especially in interest rate markets, was close to non-existent. Except for the 5-y (benchmark change -5.15 bps) daily changes in the US yield curve were less than 2.5 bps. In this respect, there was more movement in German/EMU yields after recent data-driven bond rally. Investors took some chips off the table going into today’s ECB policy decision with German yields rising between 7.3 bps (5-y) and 5.5 bps (30-y). US equities showed some swings around the Fed press conference, but at the end of the day closed little changed (S&P 500 -0.02%). Powell seeing a growing chance of a soft landing of the US economy after all was a fairly constructive message for equities/risk assets. This constructive assessment maybe also slowed recent bid for the dollar. DXY eased to close below the 101 level. EUR/USD also rebounded to close at 1.1086, just below the 1.1095 technical reference. The yen still slightly outperformed the dollar and the euro (close at 140.25 and 155.48 respectively).

Asian equity markets this morning apparently feel comfortable with yesterday’s Fed-message with most indices in green. US Treasuries are gaining marginally. De dollar is little changed. Later today, the ECB policy meeting to a large extent might follow the scrip of yesterday’s Fed meeting. Anything different from a 25 bps hike would be a huge surprise. At the ECB press conference, chair Lagarde probably will get many questions on recent poor activity data. However, with (core) inflation still at 5.5% we expect the ECB chair to reiterate its commitment to get inflation back under control. As did Powell yesterday, Lagarde will keep all options open for the September meeting (and beyond), probably with some warnings against too soft market positioning/expectations. Given the Fed’s data-depended approach, markets also will keep a close look at the US eco data, including the first estimate of the US Q1 GDP (expected at 1.8% Q/Qa). The core PCE deflator is expected to ease from 4.9% to 4.0%. US durable goods orders are a volatile series, but weekly jobless claims (expected at 235k) recently often also had an impact on the intraday price dynamics. Given current market pricing only discounting a probability of less than 50% for an additional Fed rate hike, upward surprises might support US yields. In FX markets, the dollar rebound lost some momentum. In EUR/USD the 1.1021/1.10 area remains first ST support.

News and views

Advisors to the UK chancellor Hunt become increasingly concerned that the Bank of England is overdoing it in the fight against inflation. A majority worries that rapidly rising rates will topple the economy in a recession just as the country is headed towards elections next year. Their view is being taken seriously by top Treasury officials, especially after June UK (core) CPI showed a bigger-than-expected decline. It was the first such positive surprise after four consecutive negative ones though. Some members in the advising panel think the BoE feels public pressure to tighten further because of criticism that it was too slow to move at the start and some, including former BoE governor Haldane have publicly called on the central bank to pause. The UK Treasury in a statement yesterday highlighted that the advising committee’s view does not necessarily reflects the views of government. It stressed that monetary policy is the responsibility of the Bank of England’s MPC and that it is committed to that. The discussion comes ahead of the central bank’s August 3 meeting. Markets expect a 25 bps rate hike (to 5.25%) at a minimum, with a 50% chance discounted for another 50 bps move.

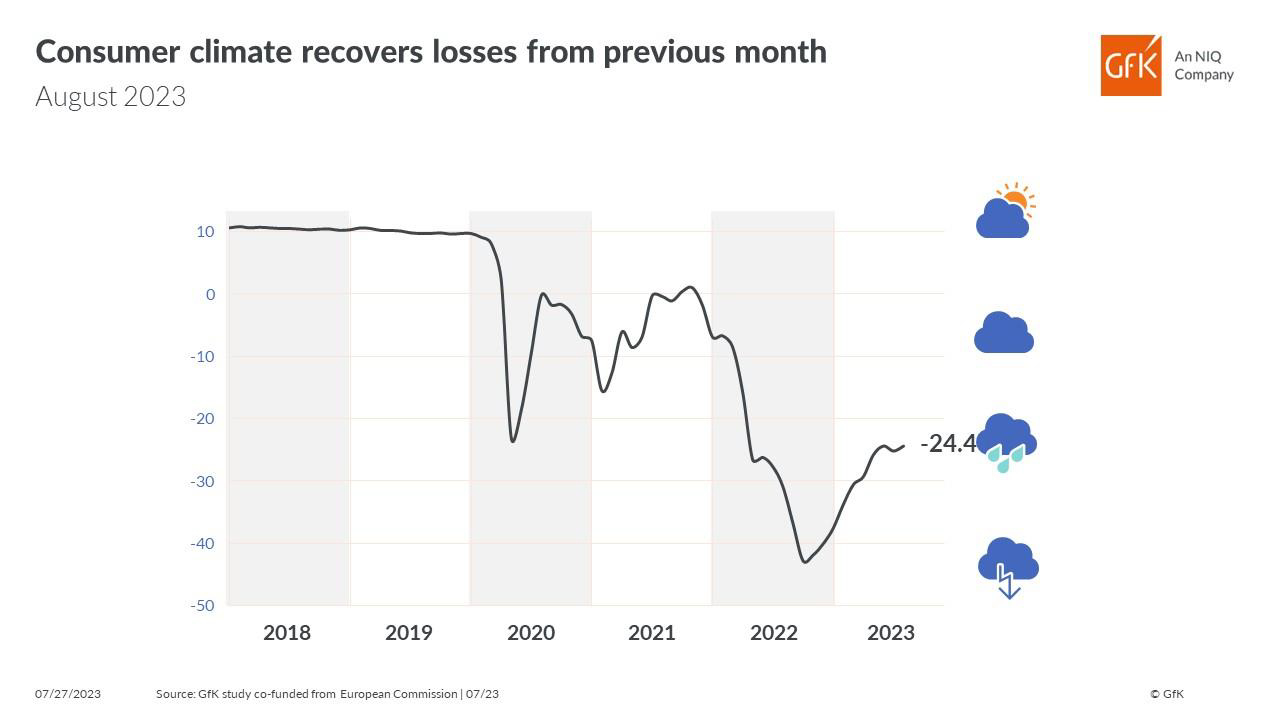

Germany Gfk consumer sentiment edged up to -24.4 on declining inflation

Germany Gfk Consumer Sentiment for August improved from -25.2 to -24.4, slightly above expectation of -24.7. In July, Economic Expectations was unchanged at 3.7. Income Expectations rose from -10.6 to -5.1. Propensity to buy ticked up from -14.6 to -14.3.

"Currently, only income expectations are contributing to the improvement in consumer sentiment. The main reason for the decrease in pessimism is the hope of declining inflation rates," explains GfK consumer expert Rolf Bürkl.

"This has somewhat improved the chances of consumer sentiment resuming its recovery course. However, the level will still remain low in the coming months, and private consumption will therefore not be able to make a positive contribution to overall economic development."