Sample Category Title

Fed Powell keeps Sep hike open, S&P 500 continues to lose upside momentum

US equities ended mixed in Wednesday's session, following Fed's expected rate increase by 25 bps to 5.25-5.50%. Despite the major policy decision, market volatility was surprisingly restrained throughout the trading session. Fed Chair Jerome Powell indicated that another rate hike could be on the table for September, while steering clear of predicting when a rate cut might transpire, pointing to the prevailing high economic uncertainty.

Current market expectations for additional rate hikes this year stand at 22% for September, 33% for November, and 30% for December. The likelihood of a rate cut commencing as early as March next year is considered to be 55.8%.

Powell, in the post-meeting press conference, stated, "It is certainly possible we would raise the funds rate at the September meeting if the data warranted, and I would also say it's possible that we would choose to hold steady at that meeting". He emphasized that Fed's monetary policy decisions will continue to be formulated on a meeting-by-meeting basis, largely dependent on economic data and indicators.

When discussing potential rate cuts, Powell asserted, "We'd be comfortable cutting rates when we're comfortable cutting rates," suggesting that a cut could take place next year if inflation hovers consistently near the Fed's target. However, he stressed that this scenario remains a considerable 'if,' given the considerable uncertainty surrounding future economic developments and subsequent policy meetings.

More on FOMC

- FOMC to Assess Policy One Meeting at a Time

- Fed Review: Balancing Act With Focus on Data

- FOMC Goes for a Summer Hike

- FOMC Hikes Again, Signals More May Be Needed

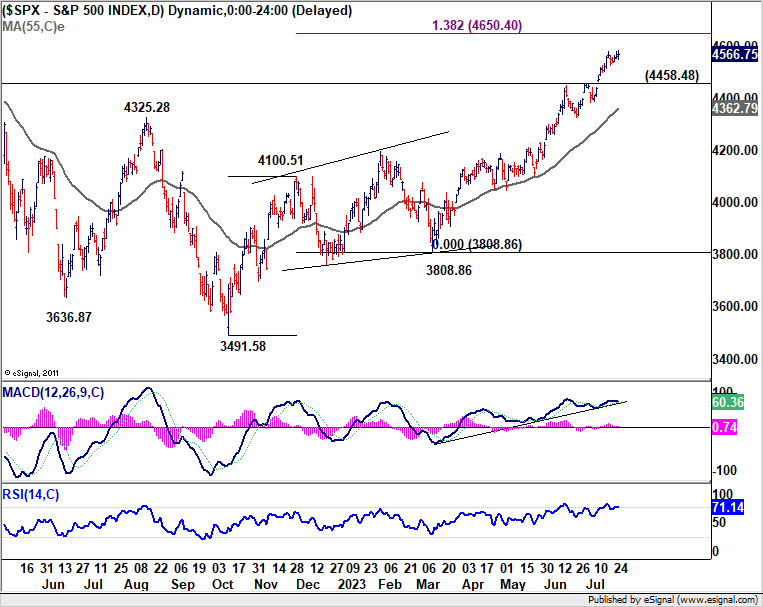

S&P 500 closed down slightly by -0.02% overnight. The index continued to lose upside momentum as seen in D MACD. While further rise cannot be ruled out, upside would likely be limited by 138.2% projection of 3491.58 to 4100.51 from 3808.86 at 4650.40. Meanwhile, break of 4458.48 resistance turned support will confirm that a correction is at least underway, and target 55 D EMA (now at 4362.79) and below.

Gold Price Aims Higher, US GDP Report Next

Key Highlights

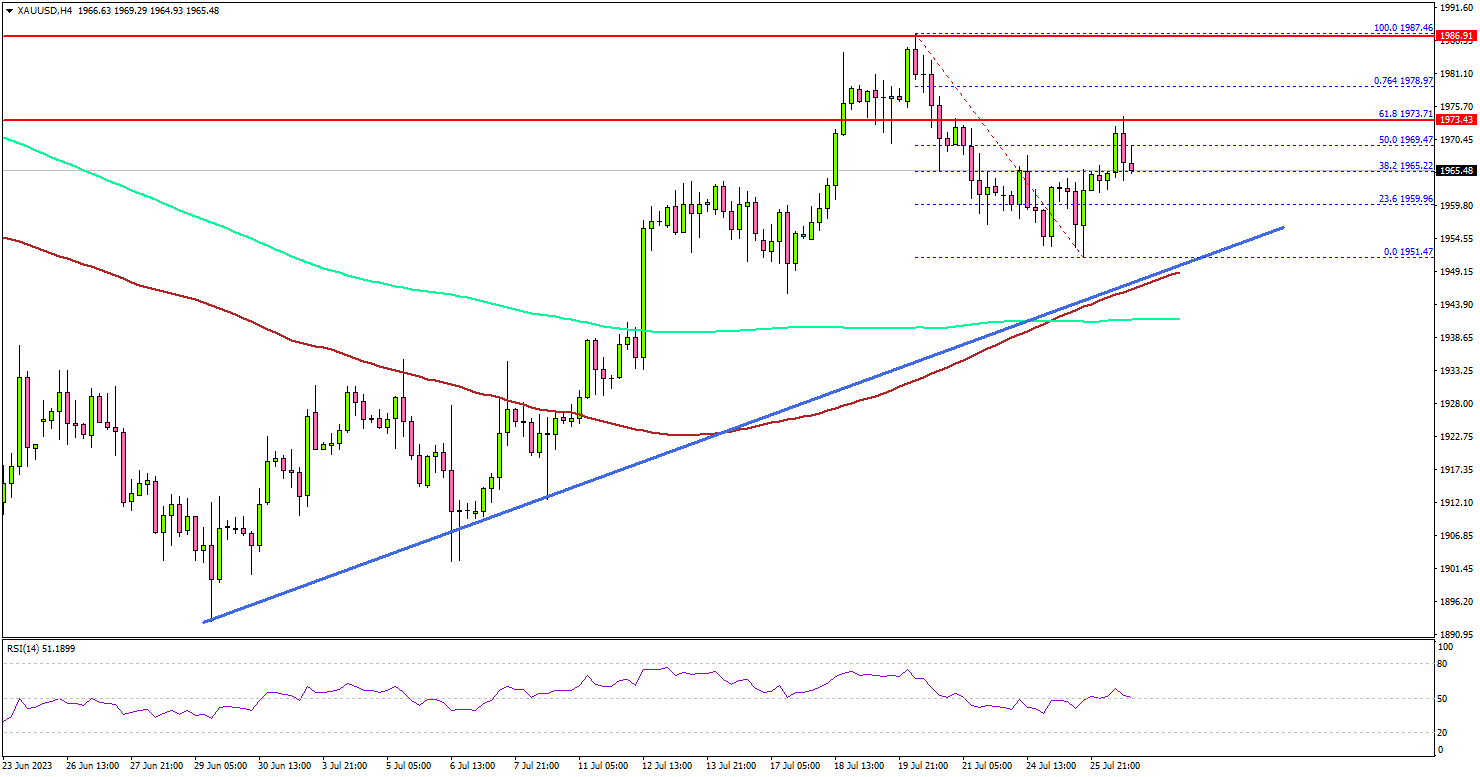

- Gold price is eyeing an upside break above the $1,975 resistance.

- A major bullish trend line is forming with support near $1,955 on the 4-hour chart.

- Crude oil prices might climb further above $80.

- The US GDP could grow 1.8% in Q2 2023 (Preliminary), down from 2.0%.

Gold Price Technical Analysis

Gold price found support near $1,950 against the US Dollar. The price seems to be forming a base above $1,950 and slowly moving higher.

The 4-hour chart of XAU/USD indicates that the price was able to settle above $1,950 and the 100 Simple Moving Average (red, 4 hours), and the 200 Simple Moving Average (green, 4 hours).

Recently, there was a break above the 50% Fib retracement level of the downward move from the $1,987 swing high to the $1,951 low. However, it is now facing a key barrier at $1,975.

The next major resistance is near the $1,978 level or the 76.4% Fib retracement level of the downward move from the $1,987 swing high to the $1,951 low, above which the price could rise toward $1,985.

Any more gains might send the price toward the $1,992 resistance level or even $2,000. Conversely, the price might correct lower. Initial support is near the $1,958 level. The next major support is near $1,955. There is also a major bullish trend line forming with support near $1,955 on the same chart.

If the bulls fail to protect the $1,955 support, there is a risk of a major decline. In the stated case, the price could decline toward the $1,925 level.

Looking at crude oil prices, there was a steady increase and it seems like the bulls might aim for a move toward the $82 level.

Economic Releases to Watch Today

- US Gross Domestic Product for Q2 2023 (Preliminary) – Forecast 1.8% versus previous 2.0%.

- US Initial Jobless Claims - Forecast 235K, versus 228K previous.

FOMC to Assess Policy One Meeting at a Time

With the downside risks to growth now believed to be as significant as inflation’s potential upside, the FOMC are beginning to look beyond the tightening cycle.

At their July meeting, the FOMC decided to raise the fed funds rate by 25bps as expected to a mid-point of 5.375%. Also in line with prior communications and the market’s expectations was the detail and tone of the statement and press conference. The focus throughout was the robust health of the economy today, but also the scale of the tightening delivered and the lags with which policy impacts.

Looking first at the guidance for activity, the assessment of GDP growth in the decision statement was strengthened (“modest” replaced by “moderate”). Job gains also continued to be characterised as robust; and, in the press conference, Chair Powell made clear the FOMC still view labour demand as greater than available supply, albeit less so than earlier in the cycle. In terms of the risks, there was no evidence of concern over the outlook for activity or the labour market; however, it is clear that the full weight of policy is yet to impact, and Chair Powell also emphasised that the latest evidence on credit conditions (from the upcoming Senior Loan Officer Survey) point to already tight conditions tightening further.

On prices, Chair Powell sought to carefully balance the still “elevated” level of inflation with the material progress seen of late. Clearly one better-than-expected print on inflation should not be taken as an ‘all clear’ signal and momentum in the highly-weighted shelter component is still extraordinary and set to slow only at a moderate pace; but we have now seen annual core goods inflation abate below the 2.0%yr headline target, from a peak above 12%yr, and core services ex-shelter or ‘supercore’ inflation retreat 2.5ppts from a peak of 6.5%yr to 4.0%yr, having averaged 1.4% annualised through Q2. As we continue to highlight, US inflation ex-shelter is now benign and the full effect of rate hikes yet to be felt.

For policy, broadly speaking, the downside risks to activity are now believed to be as significant as upside uncertainty for inflation. Decisions in coming months are therefore set to be determined by incoming data, specifically how it confirms/ conflicts with that already received. Less clear, but also highly significant, is the state of financial conditions which need to remain restrictive at least through the end of 2023. Note, this does not mean the FOMC want to keep term interest rates at their current absolute level; instead, they desire for the decline in term interest rates to lag the deceleration in inflation, keeping real interest rates materially above zero.

Worth reflecting on for early-2024 are Chair Powell’s comments late in the press conference regarding the timing of fed fund rate decisions vis a vis the 2.0%yr target. In short, he made clear that policy lags have to factored in, and hence that the Committee must stop hiking and start cutting before inflation reaches 2.0%yr. This perspective is entirely consistent with our expectation of a first cut in March 2024, with the annualised pace of inflation by that time likely 2.0%, but the annual rate still somewhat above (on our forecasts).

Also of note from the press conference is that Chair Powell believes a return to neutral, or potentially an expansionary policy setting, will be appropriate once inflation risks have abated. This points towards a large reduction in the fed funds rate to around 2.50% (the FOMC’s ‘longer run’ expectation) in contrast to the current 3.4% end-2025 median expectation of the Committee. Having peaked at its current level of 5.375%, Westpac sees the fed funds rate down at 2.625% mid-2025 and the US 10 year yield stabilising around 2.70%.

On the information to hand, the risk that the fed funds rate is increased further in the near term and/or the forecast decline in rates to mid-2025 proves much shallower than we currently forecast is set to be determined by capacity constraints across the US economy, particularly housing. Also critical will be how inflation expectations are affected. On the latter, the degree to which nominal wage growth exceeds inflation over the period will define the risk to broader inflation and its persistence.

Fed Review: Balancing Act With Focus on Data

- The Fed hiked rates by 25bp to 5.25 - 5.50% as widely anticipated. We make no changes to our Fed call, and still think this was the final hike of the cycle.

- Powell's tone was balanced, as he gave few new signals on the future rate outlook. Markets interpreted this slightly dovishly, as the latest 'dots' from June were still clearly in favour of one more hike beyond July.

- The decision provided moderate support to US Treasuries, and lifted EUR/USD close to 1.11. We still see the cross at 1.06/1.03 on the 6M/12M horizon.

The Fed delivered the widely anticipated 25bp hike in the July meeting while keeping the door open for further hikes. That said, Powell carefully refrained from pre-committing to any future policy actions.

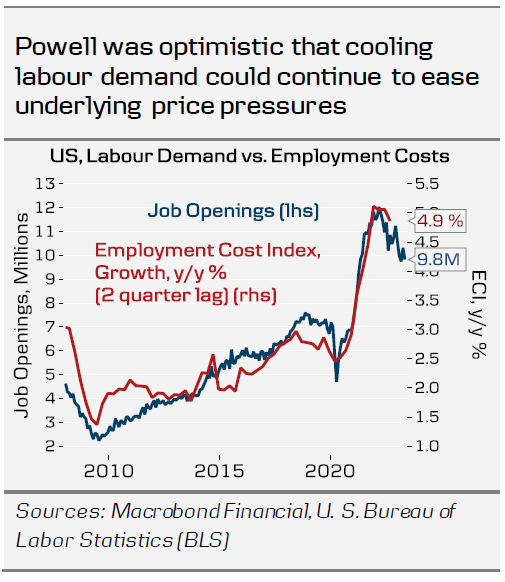

The focus remains on incoming data, with two more CPI prints and Jobs Reports still to go before the September meeting. Powell highlighted that the June CPI had been a modest positive surprise, and underscored that the combination of easing labour demand and recovering labour force participation has loosened labour market conditions as well.

On the other hand, he acknowledged that stronger-than-expected economic activity as well as the recent easing in financial conditions (weaker USD, stronger equities) could contribute to prolonging inflation pressures.

Responding to a question on the lags of policy transmission, Powell hinted that the upcoming Q2 Senior Loan Officer Opinion Survey (due for release 31st July) will signal further tightening in credit conditions. The Fed staff is no longer forecasting a recession for the US economy, but a clear slowdown remains the most likely scenario.

Powell emphasized that the Fed's policy stance is now clearly restrictive, as real yields have risen sharply over the past year. We discussed this in our Fed preview, 20 July, and this week, the Conference Board's consumer survey showed further signs of declining inflation expectations, despite overall positive development in the sentiment.

Powell also noted that the Fed could continue QT even when cutting rates in the future. We agree, as over the summer, even the increased T-bill issuance following the debt ceiling raise has had little impact on USD liquidity conditions. So far, money market funds have absorbed the issuance by reallocating funds from the Fed's ON RRP facility, while bank reserves remain steady at a healthy level. This means the Fed can continue QT well into 2024, while as our base case, we forecast the first rate cuts in Q1 next year.

Overall, with few new policy signals, we make no changes to our Fed call, and still think today marked the end of the rate hiking cycle. We expect the upcoming inflation releases to continue signalling cooling underlying inflation, and track the July Core CPI close to the June print around 0.2% m/m. With excess savings soon depleted and credit conditions still tightening, the balance of risks for the economic outlook remains tilted to the downside despite the most recent encouraging data.

Markets: Slightly dovish, no changes to longer-term views

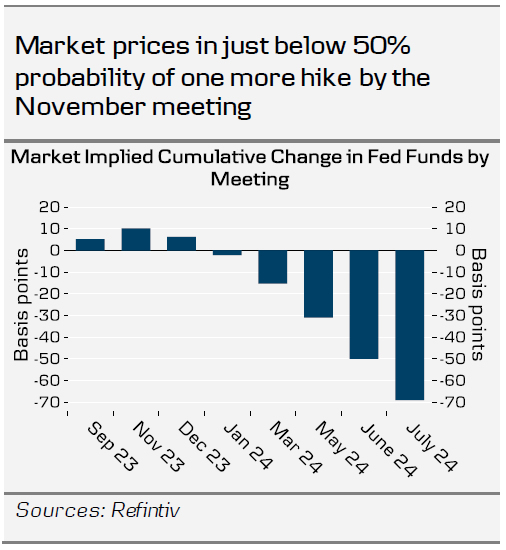

Today's message from the FOMC provided moderate support to treasuries, with the 10Y UST yield down by about 4bp since the rate announcement. Money markets are still pricing in a decent probability (just below 50%) for a final 25bp hike by the November meeting. Nonetheless, we expect the market pricing to align with our view of no further hikes as signs of softening labour market conditions and inflation show up in the data. This should make better room for duration plays, as the end of the hiking cycle will draw market focus towards the timing and pace of future rate cuts. Weakening US macro data should have a stronger impact on FOMC pricing in that environment. With the 2s10s UST curve rather extremely inverted at currently -98bp, the conclusion of the hiking cycle should also pave the way for a more resilient bull steepening of the curve going forward.

EUR/USD moved slightly higher just below 1.11, as the market interpretation was a bit to the dovish side. Overall, however, there were no surprises from the Fed, and hence it does not give us reason to change our FX view. We maintain our strategic case for a lower EUR/USD. We expect the relative strength of the US economy to weigh on the EUR/USD in the coming months, and we continue to forecast the cross at 1.06/1.03 in 6/12M. Tomorrow, we expect a relatively muted market reaction on the back of the ECB meeting. If anything, EUR/USD could move lower if the ECB does not deliver any firm signs of a September hike.

FOMC Goes for a Summer Hike

Summary

- The FOMC raised its target range for the fed funds rate by 25 bps today. The move was widely expected by financial markets and economists. The Committee has hiked its policy rate by 525 bps since March 2022.

- The post-meeting statement was little changed from the previous statement released in June. The Committee characterized the ongoing expansion in economic activity as "moderate," a small upgrade from "modest" in the June statement. The Committee continued to describe unemployment as low and inflation as elevated.

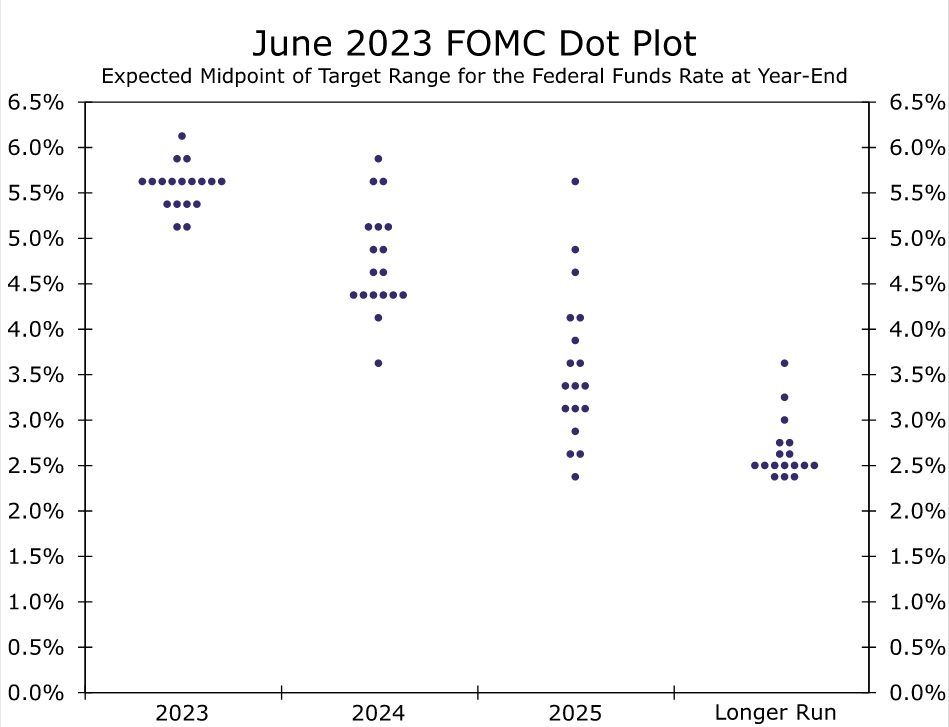

- This meeting did not include an update to the Committee's Summary of Economic Projections, which includes the dot plot. The median dot in the June projections was for a federal funds rate of 5.625% at year-end, which implies one more rate hike between now and the end of 2023.

- In his press conference, Chair Powell stated that it was "possible" the Committee could hike again at its September meeting, but he quickly followed that statement by noting that it was also "possible" the FOMC would be on hold come the next meeting. Data dependency was a key theme that emerged during his post-meeting presser.

- Our base case remains that today's rate hike will be the FOMC's last of this tightening cycle. That said, we would not be shocked if the FOMC squeezed in one more rate hike between now and the end of the year. Regardless, quantitative tightening should continue for the foreseeable future.

FOMC Hikes Rates by 25 bps. Will It Be the Last?

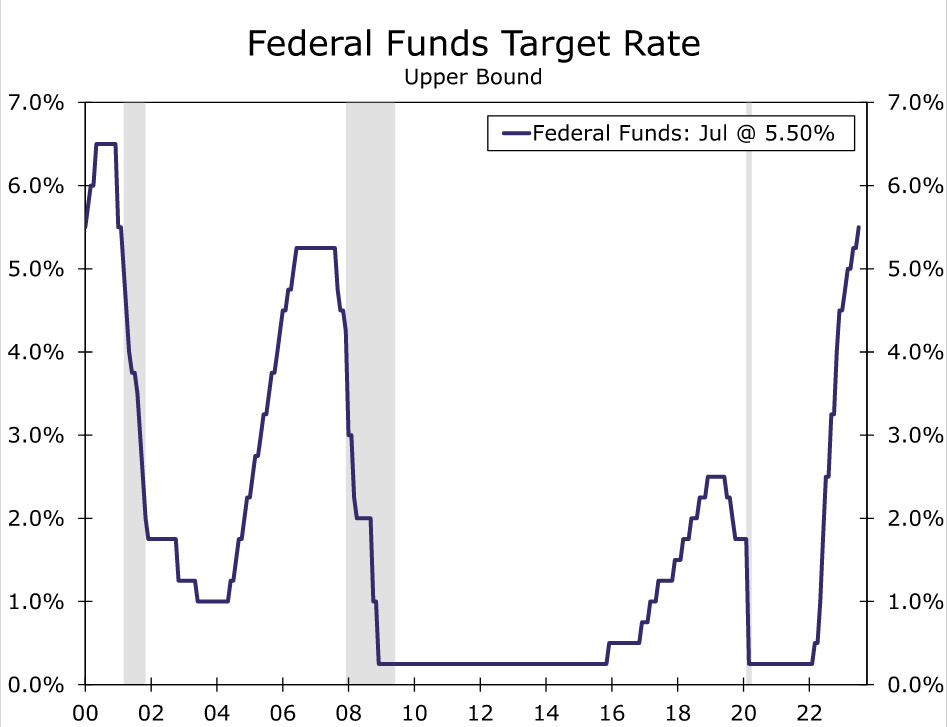

After pausing in June, the FOMC resumed its rate hike campaign at its July meeting, increasing the target range for the federal funds rate by 25 bps. The range now stands at 5.25%-5.50% and has increased by 525 bps since March 2022 (Figure 1). The decision to raise rates was supported by all 11 members who were eligible to vote at this meeting. The FOMC also reaffirmed the current pace of quantitative tightening. That is, the Federal Reserve will allow up to $60 billion of Treasury securities and up to $35 billion of mortgage-backed securities to roll off its balance sheet every month.

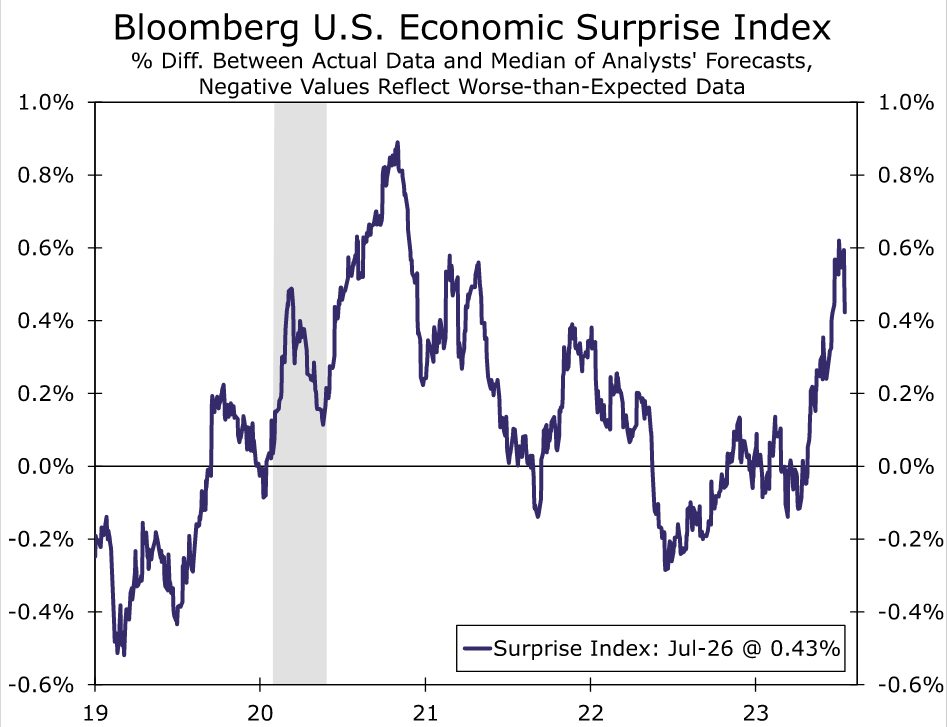

Since the FOMC last met on June 13-14, the economy has continued to weather the headwinds stemming from tighter monetary policy better than expected. In recent weeks, the Bloomberg Economic Surprise Index, which measures the degree to which economic data come in stronger or weaker than consensus expectations, has come off its recent peak but remains near a two-and-a-half year high (Figure 2). The post-meeting statement changed slightly to reflect this reality. The Committee upgraded its assessment of economic activity by characterizing the pace of expansion as "moderate" instead of "modest". The statement still characterized recent job gains as "robust" and the unemployment rate as "low."

Otherwise, there were essentially no other changes to the post-meeting statement. This meeting did not include an update to the Committee's Summary of Economic Projections, which includes the dot plot. The median dot in the June projections was for a federal funds rate of 5.625% at year-end, which implies one more rate hike between now and the end of 2023 (Figure 3). The statement language reaffirmed that the FOMC wants to keep its options open in regard to future tightening: "In determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments."

In his press conference, Chair Powell highlighted the progress that has been made in bringing down inflation thus far, but he cautioned that the "process of getting inflation back down to 2% has a long way to go." The Chair stated that it was "possible" the Committee could hike at the September meeting, but that it was also "possible" the FOMC could be on hold. The importance of future economic data and its role in future monetary policy decisions came up numerous times during the presser, and Chair Powell explicitly stated that this is "not an environment where we want to provide a lot of forward guidance." Generally speaking, the Chair's comments seemed to reiterate that the FOMC wants to preserve maximum flexibility as it awaits future data that will help determine whether monetary policy is sufficiently restrictive to bring inflation down to a more tolerable level.

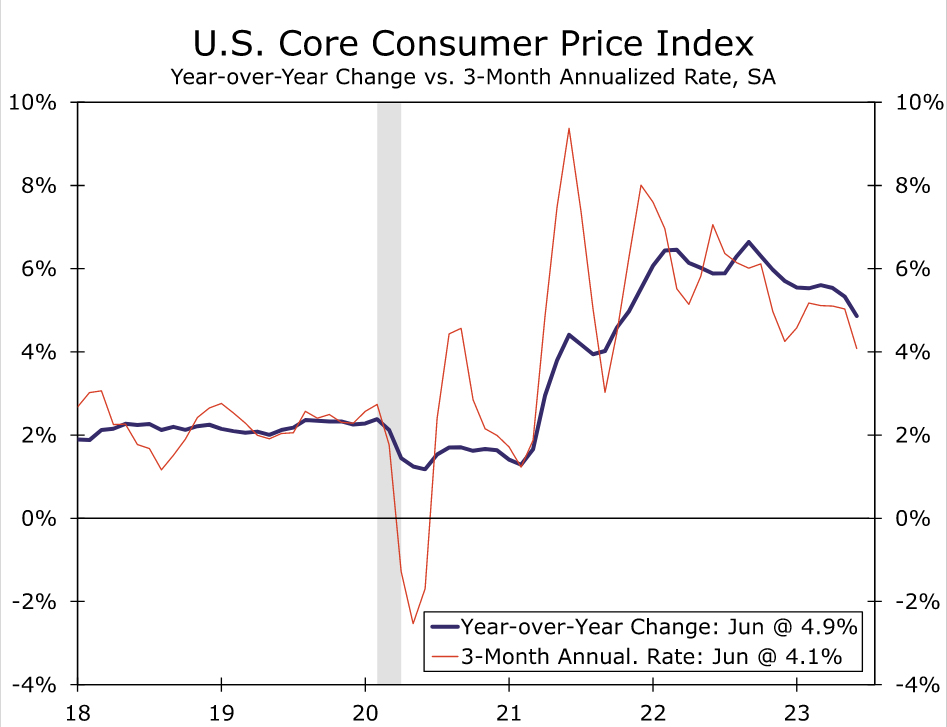

Our base case remains that today's rate hike will be the FOMC's last of this tightening cycle. For much of this tightening cycle, the FOMC has been playing catch up amid sky-high inflation and a federal funds rate that was at the zero lower bound just 16 months ago. Today, with the fed funds rate comfortably north of 5%, the Fed's balance sheet steadily shrinking and core inflation trending down (Figure 4), the case for additional tightening is more tenuous. That said, we would not be shocked if the FOMC squeezed in one more rate hike between now and the end of the year. Regardless, quantitative tightening should continue for the foreseeable future. The FOMC will get two more employment reports and two additional CPI readings between now and its next meeting on September 19-20. The annual Jackson Hole Economic Symposium, to be held August 24-26, affords Chair Powell another opportunity to offer his assessment of the U.S. economic outlook.

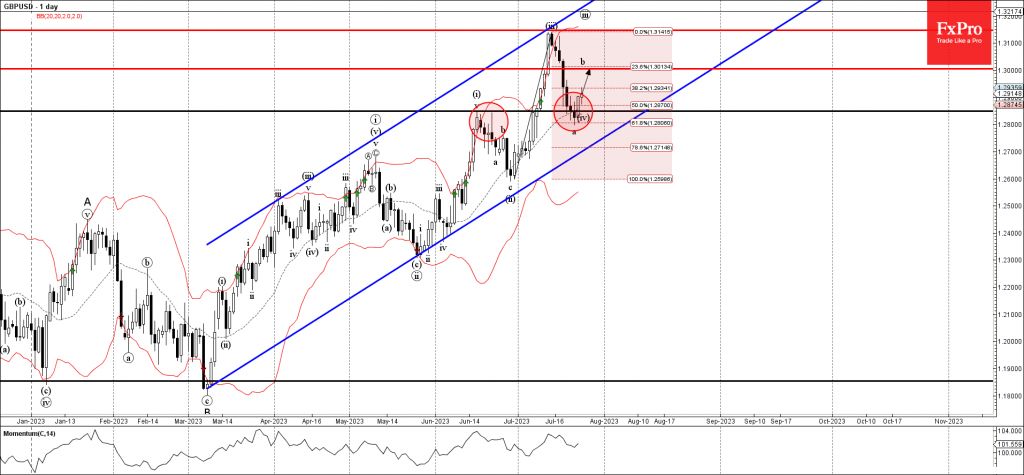

GBPUSD Wave Analysis

- GBPUSD reversed from support zone

- Likely to rise to resistance level 1.3000

GBPUSD recently reversed up from the support area set between the key support level 1.2850 (former monthly high from June), lower daily Bollinger Band and the 50% Fibonacci correction of the upward impulse from June.

The upward reversal from this support area started the active short-term correction b.

Given the strong daily uptrend, GBPUSD can be expected to rise further toward the next round resistance level 1.3000 (target price for the completion of the active wave b).

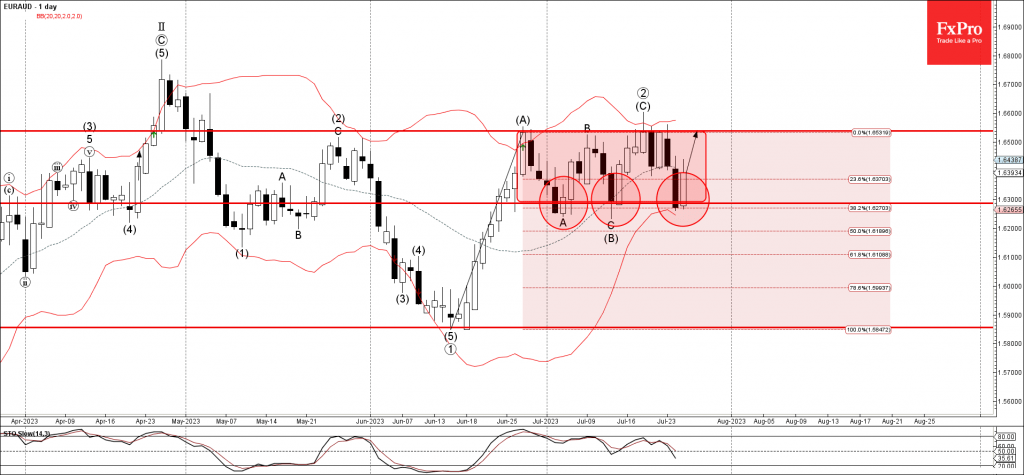

EURAUD Wave Analysis

- EURAUD reversed from support zone

- Likely to rise to resistance level 1.6540

EURAUD currency pair recently reversed up from the support zone lying between the key support level 1.6300 (which has been reversing the price from June), lower daily Bollinger Band and the 38.2% Fibonacci correction of the upward impulse from June.

The upward reversal from this support area is likely to form the daily candlesticks reversal pattern Bullish Engulfing.

EURAUD can be expected to rise further toward the next resistance level 1.6540 (which stopped the previous waves A, B and (C)).

FOMC Hikes Again, Signals More May Be Needed

The Federal Reserve Open Market Committee (FOMC) hiked the federal funds rate to the 5.25% to 5.50% range and announced a continuation of its balance sheet runoff.

The Fed updated its language to acknowledge the recent economic strength, stating "recent indicators suggest that economic activity has been expanding at a moderate pace. Job gains have been robust in recent months, and the unemployment rate has remained low. Inflation remains elevated."

It also maintained its view that "tighter credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. The extent of these effects remains uncertain. The Committee remains highly attentive to inflation risks."

All of the members of the FOMC voted in favor of the decision.

Key Implications

The Federal Reserve has hiked again after taking a brief pause in June. This move was widely expected with the Fed establishing a new cruising speed in its rate hiking cycle. Although the Fed gave itself extra time to assess whether the economy would turn under the weight of 500 basis points in rate hikes over the last 16 months, the economy has continued to exude surprising resilience.

What's next? The Fed has not seen enough evidence from the economy that it can declare an end to the hiking cycle. The Fed's own forecast shows that members think another hike is likely needed before year-end. Given the new slower pace of rate hikes, the Fed will likely hold rates steady at its next meeting in September. This will give the Fed a three-month window to monitor the economy before it decides whether it should hike again. If the labor market fails to weaken and/or core inflation fails to make the progress they expect, another 25 basis point hike would likely be on offer. As it stands, markets are giving this a 50/50 chance.

Fed hikes 25bps, issues near carbon copy statement as prior

FOMC raises federal funds rate by 25bps to 5.25-5.50% as widely expected, by unanimous vote. The accompanying statement is like a carbon copy for the June's one. The one exception is:

"The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to raise the target range for the federal funds rate to 5-1/4 to 5-1/2 percent."

Fed will continue to "continue to assess additional information and its implications for monetary policy."

Full statement below:

Recent indicators suggest that economic activity has been expanding at a moderate pace. Job gains have been robust in recent months, and the unemployment rate has remained low. Inflation remains elevated.

The U.S. banking system is sound and resilient. Tighter credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. The extent of these effects remains uncertain. The Committee remains highly attentive to inflation risks.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to raise the target range for the federal funds rate to 5-1/4 to 5-1/2 percent. The Committee will continue to assess additional information and its implications for monetary policy. In determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Lisa D. Cook; Austan D. Goolsbee; Patrick Harker; Philip N. Jefferson; Neel Kashkari; Lorie K. Logan; and Christopher J. Waller.