Sample Category Title

(FED) Federal Reserve Issues FOMC Statement

Recent indicators suggest that economic activity has been expanding at a moderate pace. Job gains have been robust in recent months, and the unemployment rate has remained low. Inflation remains elevated.

The U.S. banking system is sound and resilient. Tighter credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. The extent of these effects remains uncertain. The Committee remains highly attentive to inflation risks.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to raise the target range for the federal funds rate to 5-1/4 to 5-1/2 percent. The Committee will continue to assess additional information and its implications for monetary policy. In determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Lisa D. Cook; Austan D. Goolsbee; Patrick Harker; Philip N. Jefferson; Neel Kashkari; Lorie K. Logan; and Christopher J. Waller.

Too Dovish Market Expectations from FOMC?

After pausing at the last meeting, the Fed will announce its rate decision today with a widely expected 25-point hike to a range of 5.25%-5.50%. This event is 97% priced into interest rate futures, according to the FedWatch tool, and the main intrigue lies in the clues as to the Fed’s next moves. And there is plenty of room for speculation.

In their speeches, FOMC officials keep reminding us that the fight against inflation is not over and will be a long one. Translated into the language of interest rates, this means the prospect of (at least) one more hike and a long (up to a year) plateau period.

Markets see the situation differently, assuming there will be no further hikes and that the first cut will come before a year.

Managing these expectations is a major challenge for the Fed. But does the US central bank have to? If so, it could disappoint markets and give the dollar a boost.

In addition to core and headline inflation, the Fed also looks at the labour market. The near multi-year low in the unemployment rate promises to keep upward pressure on prices, suggesting room for further tightening. Separately, house prices are rising for the third month in a row, despite multi-year highs in mortgage rates. Rental prices are rising even faster, reducing the backlog from previous years but acting as a critical pro-inflationary factor.

The Fed’s hawkish tone later on Wednesday could trigger a broad correction in equities and provide a longer-term boost to the dollar, taking the DXY index into the 103.0-103.7 range. This could lead to widespread profit-taking in equities, taking the Nasdaq100 below 15000 and the S&P500 to 4400.

A softening of the Fed’s stance would pave the way for a quick return of the DXY below 100 and set the stage for further gains in equities, with the potential to update multi-month highs in the coming weeks.

Bank of Japan Meeting: A Policy Tweak Cannot Be Ruled Out

The Bank of Japan will announce its latest policy decision on Friday after concluding its two-day meeting. Speculation has been intensifying in the run up to the meeting about what the central bank will decide, as higher inflation has raised the possibility of another tweak to its yield curve control policy. Officials have tried to play down the prospect of a policy shift, but the Bank of Japan has a long track record of shocking the markets and so traders have good cause to be wary. This has provided some respite for the yen, even if it turns out to be temporary.

Inflation finally rears its ugly head

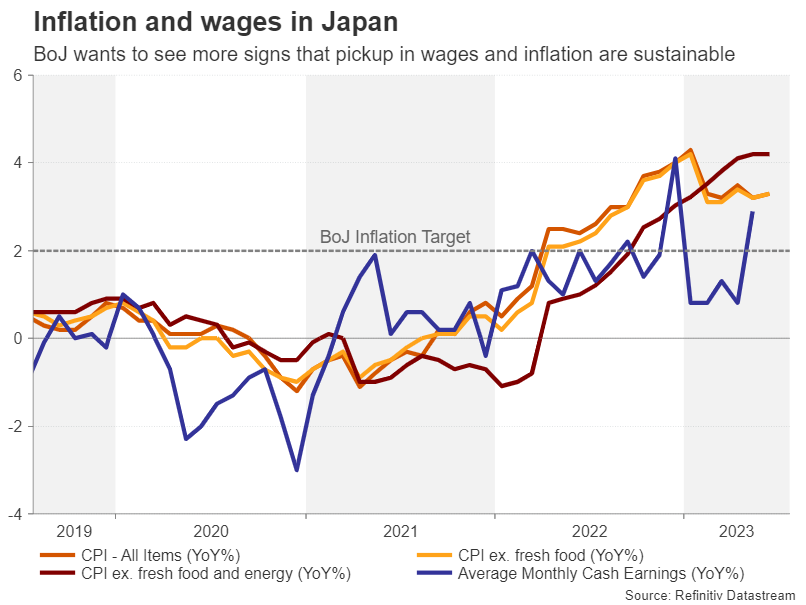

After decades of non-existent price pressures, inflation in Japan is finally headed in the right direction. The consumer price index rose at the fastest pace since the early 1990s back in January, hitting 4.3%. That is quite significant when considering that all the previous spikes in inflation over the last 30 years have been entirely down to increases in the sales tax. But the Bank of Japan isn’t celebrating quite yet. As other central banks fret about sticky inflation, the BoJ isn’t convinced that high inflation is here to stay in Japan. This need for caution is somewhat supported by the data.

Headline CPI appears to have peaked as it’s eased a little since January to just above 3.0%. Core CPI, which excludes fresh food prices and is the measure targeted by the BoJ to achieve 2% inflation, has also settled slightly above 3.0%.

However, when stripping out both food and energy prices from the CPI index, the annual rate of inflation stood at 4.2% in June and has yet to peak. When adding to the equation the effects of a weaker currency – the Japanese yen has depreciated by about 7% versus the US dollar this year – there is a reasonable argument to assume that inflation is set to stay above the BoJ’s 2% target for some time to come.

It’s all about sustained wage growth

Yet, like his predecessor, new governor, Kazuo Ueda, wants to see more evidence that inflationary pressures won’t dissipate once the pandemic and energy shocks have faded, and for that to happen, there has to be a domestically driven demand backdrop. Hence, all the focus on wage growth.

Some progress has been made; wage increases accelerated at the end of 2022 before falling back earlier this year. But there are positive signs that average cash earnings are starting to pick up again as they rose by 2.9% year-on-year in May.

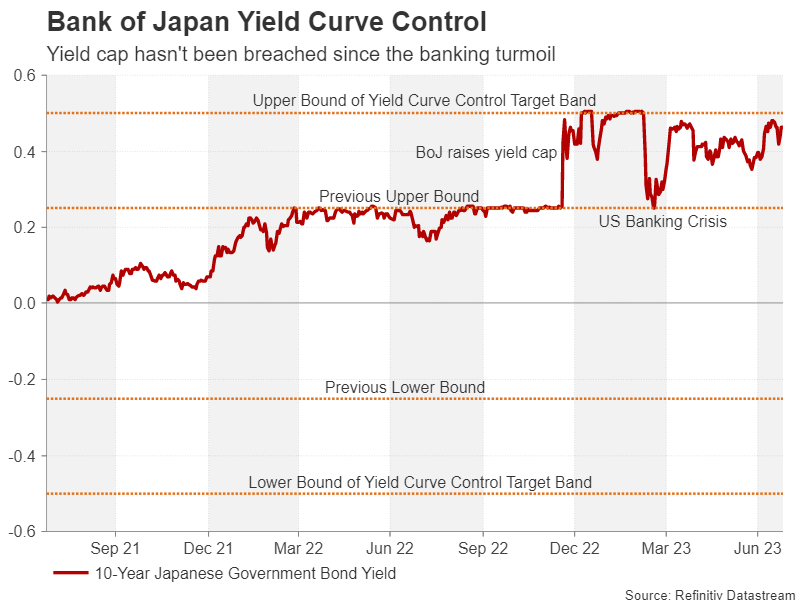

The big question now is whether or not these tentative signals that high inflation is becoming more embedded in the Japanese economy, and more importantly, in the Japanese people’s mindset, warrant another recalibration of the Bank’s yield curve control (YCC) policy. YCC was last adjusted in December when the target band on the 10-year JGB yield was widened by 25 basis points to 0.50% above and below zero percent.

The case for a BoJ shock

If the BoJ were to opt for another tweak, an increase in the band from ±0.50% to ±1.00% would be the likely scenario. The main case for the BoJ to act pre-emptively and catch markets by surprise is to avoid a situation where speculators push up the 10-year yield to the upper limit of the target band, forcing the Bank to make emergency bond purchases. The risk of a prolonged or intense pressure on the yield cap is that it could lead to a disorderly exit from yield curve control policy – something that would be hugely embarrassing for the BoJ as well as potentially costly.

A tweak now would keep speculators at bay well into 2024, buying policymakers some valuable time to properly assess the country’s changing inflation landscape. But most importantly, the Bank would in fact be prolonging the lifespan of YCC, enabling it to maintain an ultra-accommodative policy stance even as it allows the 10-year yield to climb to multi-year highs.

A boost for the yen? Maybe.

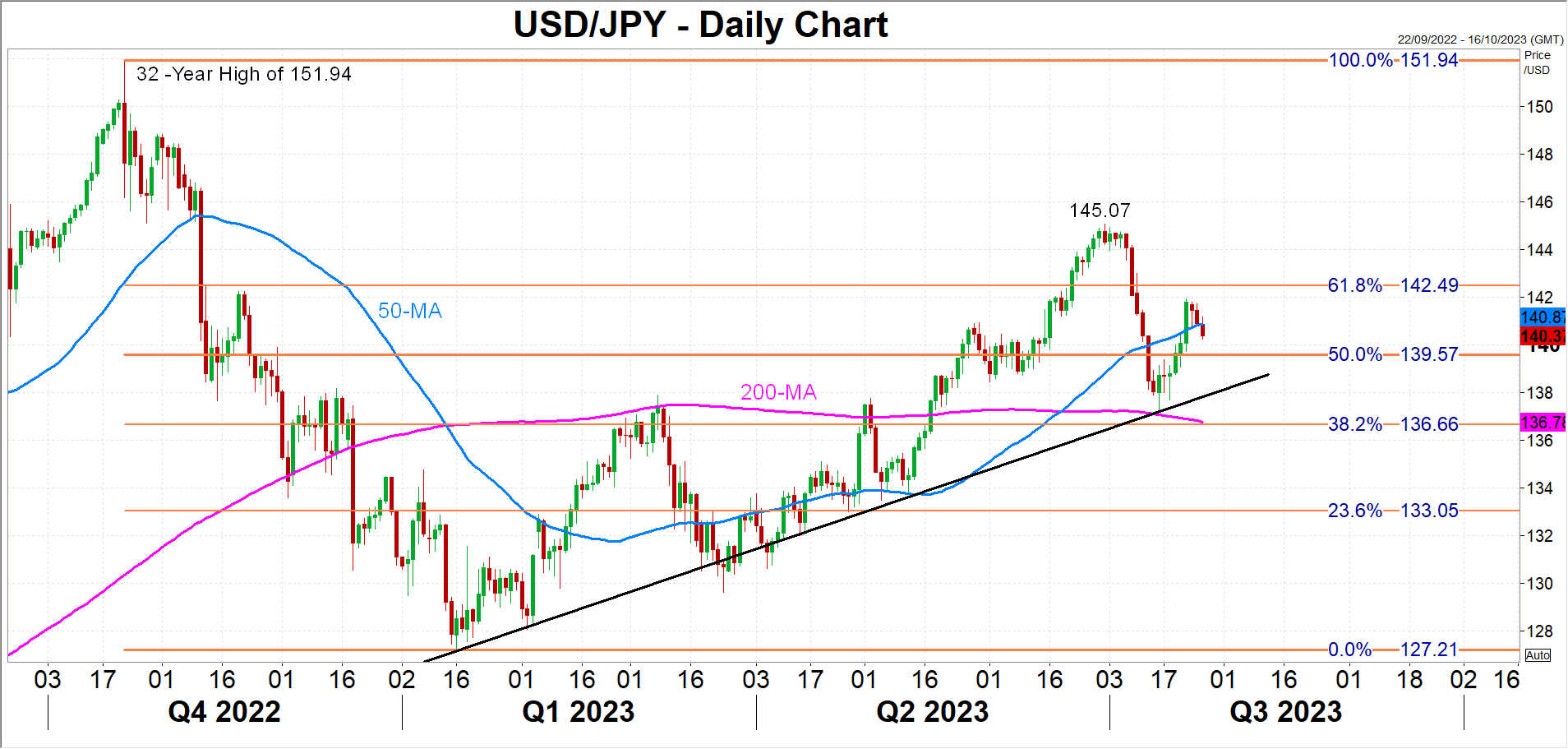

For the yen, a widening of the target band would come as welcome relief and the immediate reaction would be a spike higher. Dollar/yen could dip towards its ascending trendline before sellers target the 200-day moving average at 136.78 and the 133.00 congested region.

However, further gains would likely depend more on what the US Federal Reserve signals about its tightening plans and how the dollar responds to that. In the months ahead, if expectations about Fed rate cuts, or even a long pause, don’t materialize, a tweak in YCC policy might not be enough to prevent the yen from revisiting its 2023 and 2022 lows of 145.07 and 151.94 per dollar, respectively.

USD/JPY Softens as Yen Hedges Surge Ahead of BOJ

- Rate cut odds for the December FOMC meeting now stands at 15.1% vs 16% yesterday

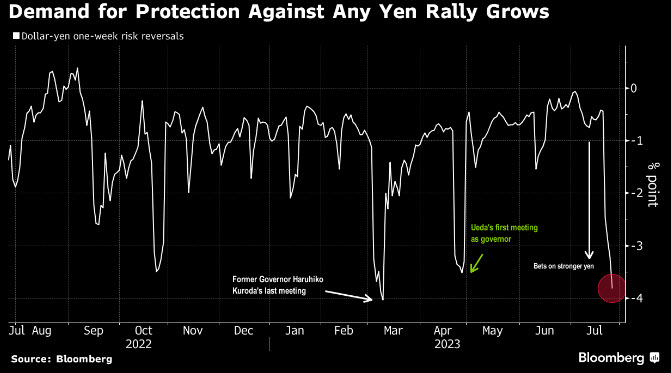

- Protection against yen strength rises to a four-month high

- Bearish tones emerging for USD/JPY as top Ichimoku cloud tested

The Japanese yen is catching modest bids here as stocks soften on Microsoft’s disappointing AI outlook and as pressure builds for the BOJ to tighten.

Microsoft’s results were adequate, but that won’t be enough to keep the mega-cap tech/AI trade going. Profit taking will likely remain the dominant theme for tech, especially if Meta disappoints after the close. Microsoft’s slowdown with their cloud business and lowering the bar for their AI growth should only trigger a modest pullback. Microsoft is still winning the AI race and still seems to have a robust long-term outlook.

The BOJ got some solid advice about their yield curve control program from the IMF Chief Economist Gourinchas. He said, “Our advice for the Japanese authorities is that right now monetary policy can remain accommodating, but it needs to prepare itself for the need to maybe start tightening.”

The clock is ticking on the BOJ and they may want to move away from YCC sooner than later as an abrupt change could cause unwanted market chaos.

Fed

Ahead of the Fed, it seems Wall Street is extremely confident the Fed will be one-and-done. Fed Chair Powell will argue that one cool inflation report doesn’t mean their inflation fight is almost over and that another rate hike will depend on the data. The Fed will skip tightening in September and the economic slowdown should allow them to refrain from raising rates in November. The market is starting to price in rate cuts in December and that will probably be met with a strong rebuttal from Powell. Powell will say they are not cutting this year and that higher for longer should be the outlook for rates.

Yen

The big trade in FX this week might be the Japanese yen. Leading up to the BOJ decision, traders are putting on hedges in case Governor Ueda surprises us with a tweak to YCC. The one-week risk reversals for USD/JPY are now at the lowest levels in four months. If more hedges keep piling in, that could provide some more short-term strength for dollar-yen.

It might be hard to see significant positioning before the FOMC decision, but if yen strength remains the dominant theme post-Powell, this trade could continue to Friday’s BOJ event. On a break of the 140.00 level, momentum traders could see prices target 139.14, which is the 38.2% Fibonacci retracement level of the March low to July high move.

Crypto Market Poised to Move

Market picture

The crypto market is maintaining a wait-and-see approach, moving in a narrow range after the sell-off on Monday. The markets appear to be waiting for the directions after Fed’s decision.

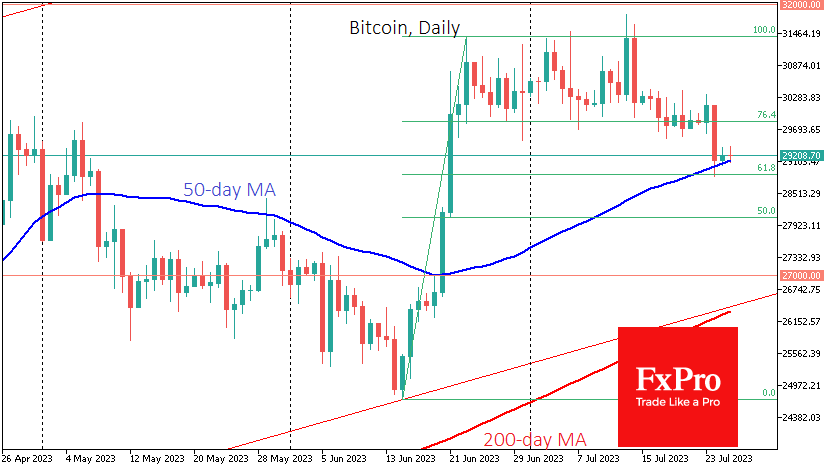

Bitcoin stuck to its 50-day moving average, trading just above $29.1K. One of the following sharp moves could stop the recent mini-lull, determining the future trend.

A drop under $28.8K would mark the transition to a deeper correction scenario down to $27K, where the 200-week average and the lower boundary of the ascending corridor lie.

However, Bitcoin has about the same chance of returning to growth. We will get more confidence when the price strengthens to $29.7K.

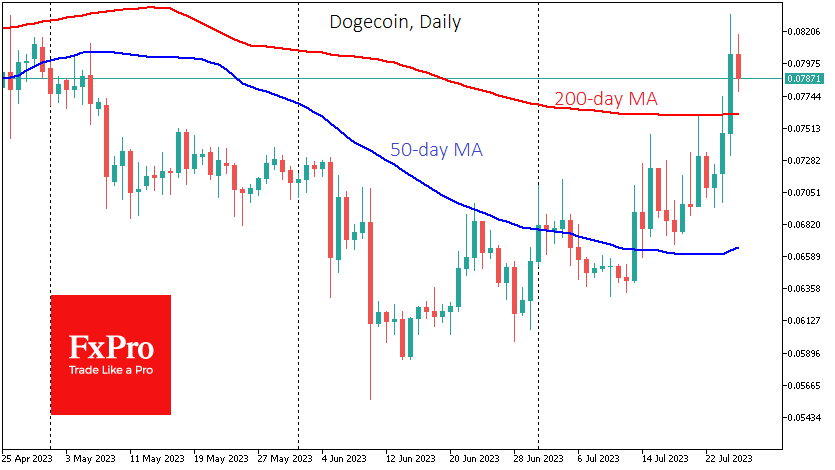

Dogecoin has added over 14% since the beginning of the week on the back of Twitter’s logo change. The rebranding to “X” has increased networking activity and altcoin’s value. Elon Musk promised to make Twitter a financial hub.

News background

Glassnode recorded “unloading” among Bitcoin whales (from 1000 BTC). Since 30 May, the aggregate balance of bitcoins owned by whales, excluding exchange wallets, has decreased by 255k BTC. The monthly rate of decline in the metric (148k BTC) was the fastest in history.

Changpeng Zhao is going to get the Commodity Futures Trading Commission (CFTC) lawsuit against Binance cancelled. The exchange is preparing two motions to quash the CFTC lawsuit filed in federal court in Chicago.

Stablecoin issuers whose reserves consist of derivatives or covered bonds will receive additional regulation, according to a draft of new European Banking Authority (EBA) rules. The document suggests increased capital requirements for such firms if the tokens they issue are deemed “significant”.

YouTube blogger Bitboy Crypto said he remains optimistic about XRP as the coin returns to cryptocurrency exchanges.

Sunset Market Commentary

Markets

The countdown to a Fed decision most often is a long-drawn yawn with eco data often ignored. Today, even these ’to be ignored‘ data were almost completely absent. US new home sales, to be published after finishing this report for sure won’t break the stalemate. Uncertainty on growth and how much further tightening still to expect from the Fed and the ECB combined with mixed results caused equity investors to stay at bay. European stocks underperform with the EuroSroxx 50 losing 1.5%+. US indices opened about 0.5% lower. The risk-off hardly any impact on US Treasuries. Except for a benchmark change in the 5-y (-2.5 bps), US yields are changing less than 1 bp in a daily perspective. Despite the broader risk-off and recent unconvincing EMU data, German yields ‘rebound’ between 3 bps (30-y) and 5.3 bps (5-y). The German 2-yield (3.10%) is supported by the 3.0% big figure. The 10-y (2.46%) is locked in a tight range near the 2.5% pivot. 10-y Intra-EMU spreads also show only small moves going into tomorrow’s ECB meeting. Greece continues to outperform (-4 bps). In FX markets, the dollar is losing modestly after a solid data driven comeback over the previous 10 days. DXY trades near 101.2. EUR/USD hovers close to 1.1070 from an open near 1.105. The yen outperforms (USD/JPY 140. from an open at 140.9). The risk-off helps, but investors maybe also stay cautious on yen shorts going into Friday’s BoJ meeting. Is there a (small?) chance for the BoJ tweaking its yield curve control. Even if it’s only a tail-risk, the impact if it happens could be big, including for the yen. Quite a divergent performance of CE currencies. The Czech koruna (EUR/CZK 24.05) and the especially Polish zloty (EUR/PLN 4.42) are well bid. The zloty even nears the YTD strongest against the euro. The forint is fighting an uphill battle (EUR/HUF 383.5 from an open below 380). MNB yesterday for the third consecutive month cut the O/N ‘emergency’ depo tender rate by 100 bps to 15.0%. Some forint investors apparently see a declining premium as changing the risk-reward balance.

The main dish for markets of course is the Fed decision and Powell’s press conference. As the MPC in June raised the dots signalling a peak in the target range to 5.50/5.75% and considering Fed comments since then, anything different from a 25 bps hike would be a big surprise. Even with latest payrolls and CPI slightly softer than expected, other data suggest that the US economy is holding resilient and that no recession in imminent. Demand probably stays too strong for the Fed to already feel comfortable that (core) inflation will sustainably return to 2%. In this context, we expect Powell to keep the door open for a further 25 bps step in September (or later) depending on the data. For markets, such a scenario shouldn’t be a big surprise. Even if Powell holds a hawkish tone, it won’t be easy for the 2-y and 10-y to surpass big figures yields at 5.0% and 4.0% respectively. Such a test probably needs solid payrolls (next week) and/or higher than expected inflation (August 10). Given recent good US data (especially compared to EMU), the dollar might stay well bid post-Fed, with EUR/USD 1.1012 (22 June top)/1.10 first next reference.

News & Views

Credit rating agency Fitch raised Brazil’s long-term foreign currency debt rating to BB from BB-, two levels below investment grade. It retains a stable outlook. Fitch is referring to a better-than-expected macroeconomic and fiscal performance amid successive shocks in recent years, proactive policies and reforms for the upgrade. It acknowledges lingering political tensions and said the new leftist Lula government advocates a shift away from the liberal economic agenda of the past governments. But Fitch expects pragmatism and the country’s broader institutional checks-and-balances should prevent radical policy changes. New fiscal rules, even as some have yet to be approved, and major tax reforms should result in an improvement in the in 2023 worsened fiscal position, Fitch said. Underpinning Brazil’s rating today are its large and diverse economy, deep domestic markets and high per-capita income. A flexible exchange rate creates shock-absorption capacity and the country disposes of robust international reserves and a sovereign net external creditor position. Risks mainly arise from high government debt, fiscal rigidities, weak economic growth potential and relatively low governance scores. The Brazilian real reacts stoic to Fitch’s decision. From a broader perspective though, the currency is trading at its strongest level since June 2022. USD/BRL is changing hands around 4.74.

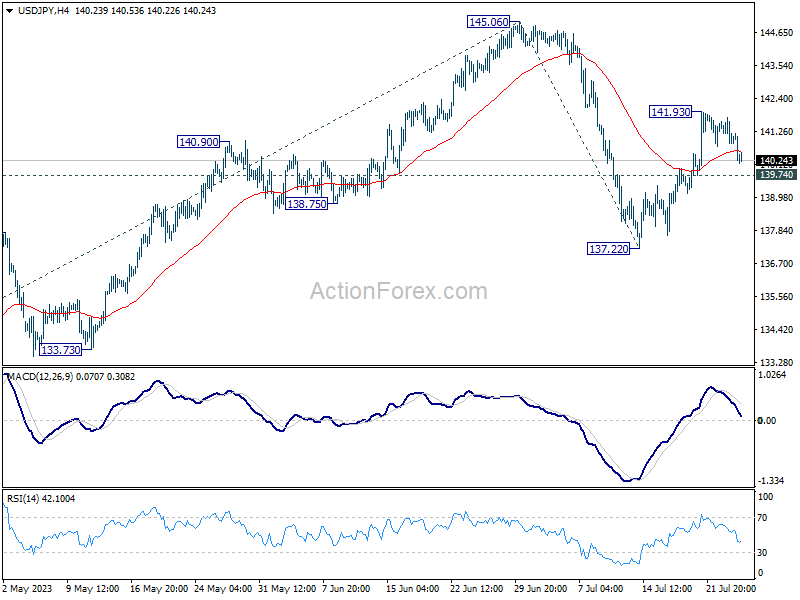

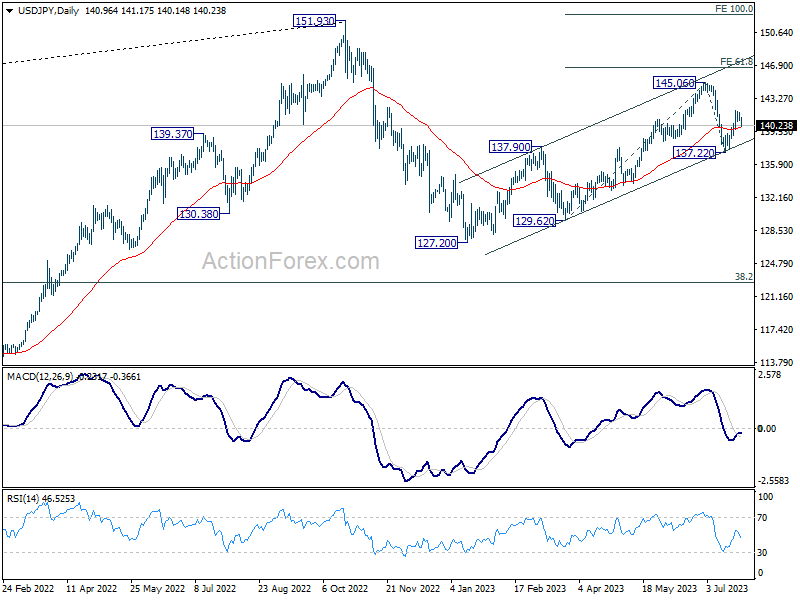

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 140.60; (P) 141.17; (R1) 141.47; More...

Intraday bias in USD/JPY remains neutral for the moment. Further rise is mildly in favor with 139.74 minor support intact. On the upside, above 141.93 will resume the rebound from 137.22 to 145.06 first. Firm break there will target 61.8% projection of 129.62 to 127.22 from 145.06 at 146.76 next. On the downside, below 139.74 minor support will bring retest of 137.22 instead.

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Current development suggests that the second leg (the rise from 127.20) might not be over yet. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

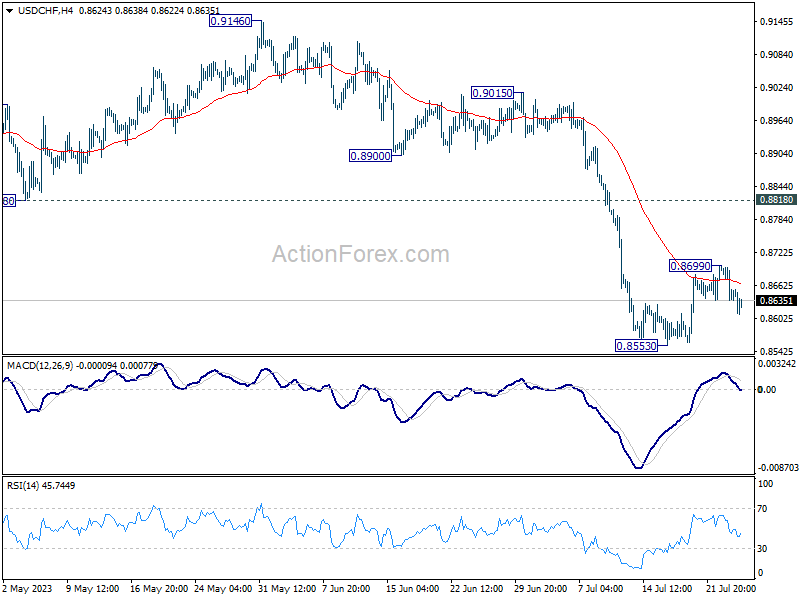

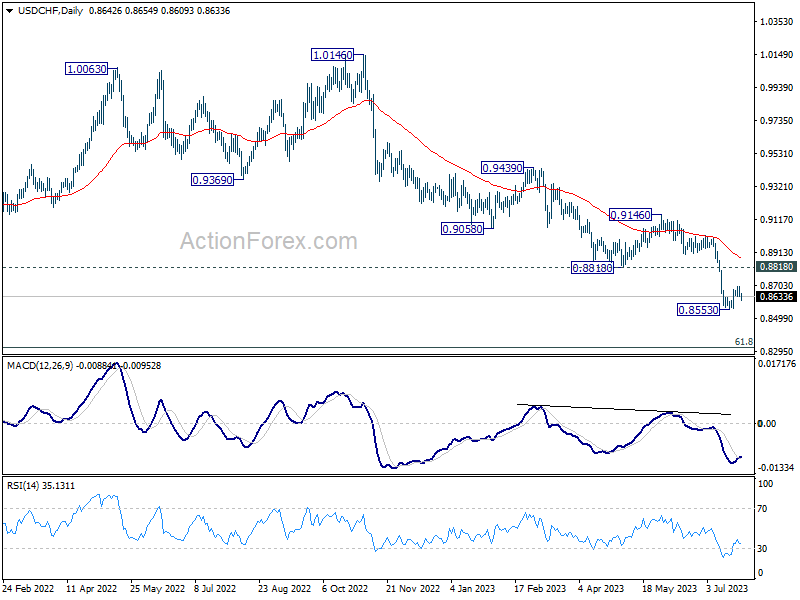

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8616; (P) 0.8659; (R1) 0.8681; More...

Intraday bias in USD/CHF remains neutral for the moment. Outlook stays bearish with 0.8818 support turned resistance intact. Break of 0.8553 will resume larger down trend from 1.0146. On the upside, above 0.8599 will resume the rebound towards 0.8818 instead.

In the bigger picture, the break of 0.8756 (2021 low) indicates break out from the long term range pattern. For now, medium term outlook will stay bearish as long as 0.9146 resistance holds. Further fall would be seen to 61.8% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.8317 next.

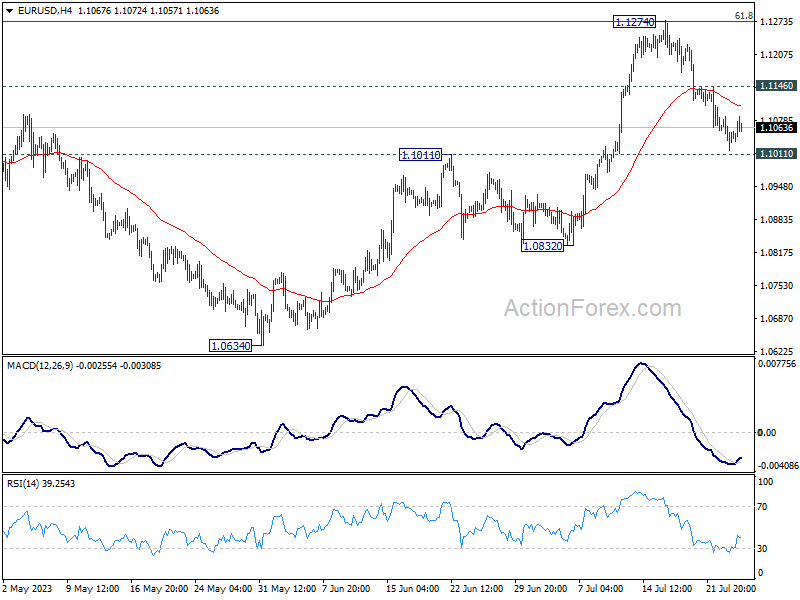

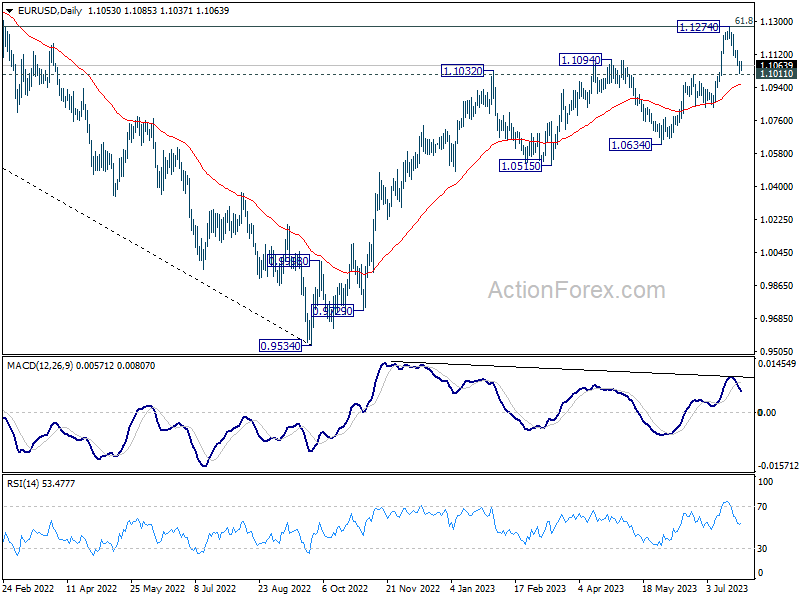

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1022; (P) 1.1054; (R1) 1.1088; More...

Intraday bias in EUR/USD stays neutral at this point. Near term outlook will stay bullish as long as 1.1011 resistance turned support holds. Above 1.1146 minor resistance will turn bias back to the upside for retesting 1.1274 high first. However, firm break of 1.1011 will argue that larger correction is underway. Deeper fall would then be seen to 1.0832 support next.

In the bigger picture, rise from 0.9534 is still expected to continue as long as 1.1011 resistance turned support holds. Decisive break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next. However, firm break of 1.1011 will indicate rejection by 1.1273 and raise the chance of reversal.

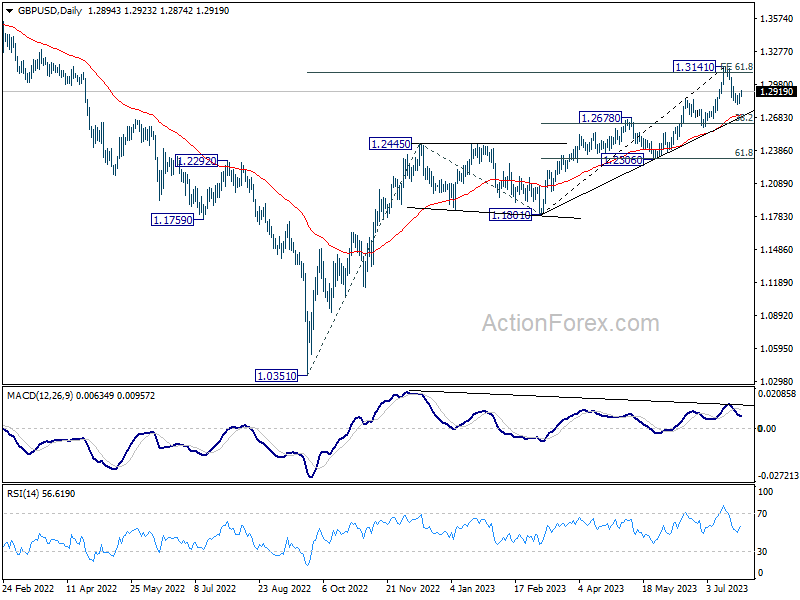

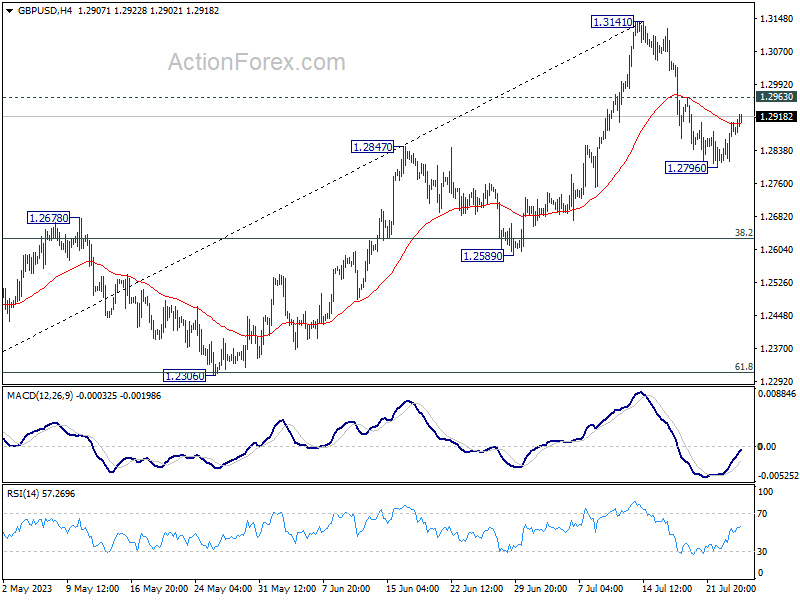

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2840; (P) 1.2872; (R1) 1.2935; More...

GBP/USD's recovery from 1.2796 continues today but stays below 1.2963 minor resistance. Intraday bias remains neutral at this point. On the downside, below 1.2796 will resume the fall from 1.3141 to 55 D EMA (now at 1.2703) and possibly below. On the upside, break of 1.2963 minor resistance will turn bias back to the upside retest 1.3141 high instead.

In the bigger picture, as long as 1.2678 resistance turned support holds, rise from 1.0351 (2022 low) is expected to continue. Next target is 100% projection of 1.0351 to 1.2445 from 1.1801 at 1.3895. However, sustained break of 1.2678 will argue that it's at least correcting this rally, with risk of bearish reversal.