Sample Category Title

European Central Bank: Dovish and Data Dependent

Summary

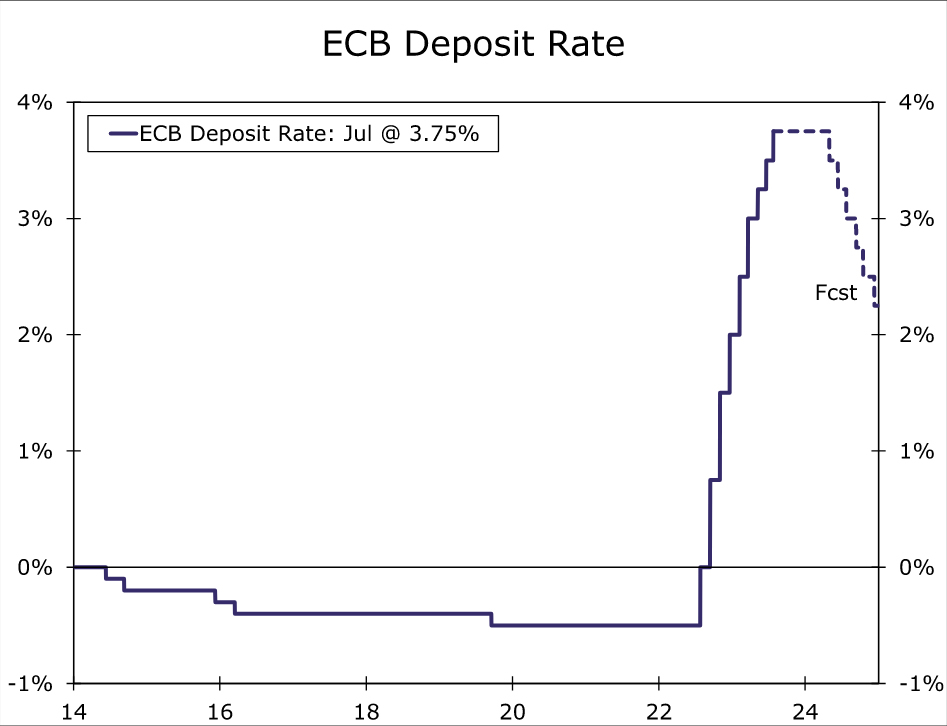

- The European Central Bank (ECB) raised its Deposit Rate 25 bps to 3.75% at today's monetary policy announcement, matching widespread expectations. More significantly, the ECB sounded more downbeat on the economy and, in contrast to recent meetings, was cautious in offering any guidance about policy beyond this July meeting.

- Ahead of today's announcement, we believed that a policy rate of 3.75% could mark the peak for this cycle. That view is unchanged, with sentiment and survey data likely to remain subdued for the time being, and so long as inflation continues to trend in a more favorable direction in the months ahead. We do not expect the ECB to begin cutting interest rates until well into 2024, once more convincing progress in reducing underlying inflation closer to the central bank's target is evident.

European Central Bank Hikes Rates, But Cautious in Offering Policy Guidance

The European Central Bank (ECB) raised its Deposit Rate 25 bps to 3.75% at today's monetary policy announcement, matching widespread expectations. More significantly, the ECB sounded more downbeat on the economy and, in contrast to recent meetings, was cautious in offering guidance about policy beyond this July meeting. Ahead of today's announcement, we believed that a policy rate of 3.75% could mark the peak for this cycle. That view is unchanged, with sentiment and survey data likely to remain subdued for the time being, and so long as inflation continues to trend in a more favorable direction in the months ahead.

Overall, there were several comments in the ECB's accompanying statement, and from ECB President Lagarde's press conference, that pointed to a shift toward a less hawkish (or more dovish) approach than previously:

- The ECB said future decisions will ensure that key interest rates will be set at sufficiently restrictive levels. That is a change from previous terminology that interest rates would be brought to sufficiently restrictive levels.

- The ECB said past rate increases continue to be transmitted forcefully, and that financing conditions have tightened again and are increasingly dampening demand. ECB President Lagarde reinforced this, saying the central bank is definitely seeing policy being transmitted “strongly.”

- The ECB also decided to set the remuneration of minimum reserves at 0%.

- ECB President Lagarde said the near-term outlook has deteriorated, with manufacturing output held down by weak external demand while services activity was more resilient. The economy is expected to remain weak in the short run.

- Importantly, ECB President Lagarde said policymakers have an open mind on decisions in September and beyond, and that the ECB may vary from one meeting to another. Specifically with respect to September, Lagarde said “we are not going to cut”, and that September could be a hike or could be a pause. This is a significant contrast to recent meetings, where the ECB has explicitly signaled or promised a rate hike at the following meeting.

While outweighed by dovish comments, there were still one or two hawkish elements, most notably the ECB repeating that while inflation continues to decline, it “is still expected to remain too high for too long.”

Overall, while today's announcement leaves the door slightly ajar for a September rate hike, we think that door may be closed by the time of that meeting. So long as activity data and confidence surveys remain soft (which we think is likely) and inflation trends, both headline and underlying, continue to improve (which we think is more likely than not), we believe the European Central Bank will hold its policy rate steady at 3.75%. Indeed, at this time we believe that 3.75% will be the peak policy rate for the current cycle, and that rates will be held at that level for an extended period. We do not expect the ECB to begin cutting interest rates until Q2-2024, once more convincing progress in reducing underlying inflation closer to the central bank's target is evident.

Sunset Market Commentary

Markets

Powell’s ‘Big Mute’ on the future trajectory of tightening yesterday but at the same time expressing hope the Fed might be able to engineer a soft landing this morning supported a outright risk-on sentiment. The EuroStoxx 50 easily gained 1%+. The dollar was on the backfoot with EUR/USD extending gains beyond 1.11. For afternoon trading, key question was which out of two would have most market impact: A series of US data including US Q1 GDP growth (annex PCE deflator), durable goods orders and jobless claims, concretizing the Fed’s data dependent approach, or the ECB decision annex guidance (if any) at the post-meeting press conference.

As was the case for the Fed yesterday, the ECB as expected raised its policy rate by 25 bps, bringing the depo rate to 3.75%. The decision was unanimous, Lagarde said at the press conference. Contrary to the Fed, the ECB slightly amended/softened its inflation assessment in the policy statement. ‘Inflation continues to decline but is still expected to remain too high for too long. The Governing Council is determined to ensure that inflation returns to its 2% medium-term target in a timely manner’. At the same time communiqué reads that ‘The developments since the last meeting support the expectation that inflation will drop further over the remainder of the year but will stay above target for an extended period. While some measures show signs of easing, underlying inflation remains high overall’. In this respect, interest rates will be set at a sufficiently restrictive level for as long as necessary. The appropriate level and the duration of restriction also will be determined by a data-depended approach. At the press conference, as did the Fed yesterday, Lagarde clarified that the ECB turned to a completely open and data dependent approach with respect to the future decisions (September and beyond). European yields already declined immediately after the press release of the decision and this trend was accelerated after Lagarde during the press conferences stressed the ‘complete open bias’. The ECB still repeated that the focus gradually turns to domestic drivers of inflation including wages and profit margins, but that didn’t change investors’ view. At the time of writing, the German yield curve shows a bullish steepening with yields declining between 11 bps (2-y) and 5.0 bps (30-y).

Global bond markets initially softened after the publication of the ECB decision, but US data were strong/stronger than expected across the board. US Q2 growth accelerated from 2.0% Q/Qa to 2.4% (1.8% expected) mainly due to resilient consumption (1.6% Q/Qa) and a rebound in investment (5.9%). The core PCE deflator softened slightly more than expected (3.8% from 4.9%). Headline durable goods orders also beat expectations (4.7% M/M). Shipments were more moderate. US jobless claims declined further from 228k tot 221k. All combined, today’s releases in a data-depended approach support the case for further tightening. After some softening before the data releases, US yields current trade about 3.0 bps higher across the US Treasury curve.

On other markets, equities remain well bid, with Europe this time outperforming (EuroStoxx 50 +2.25%). The US S&P 500 opens about 0.8% higher. On FX markets, interest rate divergence post the US data and the ECB decision caused a sharp reversal of initial USD softness. EUR/USD dropped from intraday top near 1.1150 to currently test the 1.10 area. USD/JPY also jumped from an intraday low of 139.38 this morning to currently trade near 140.75.News & Views

Today was another important day for the Turkish central bank to reestablish credibility among investors. Governor Hafize Gaye Erkan for the first time since her appointment last month published Turkish inflation forecasts. These projections in the past often raised eyebrows, appearing to be very unrealistic. This time around, the central bank estimates year-end price pressures to be a whopping 58%, more than double the 22.3% under her predecessor. By end 2024, inflation would still amount to 33% vs a previous estimate of 8.8%. It’s not expected to hit the 5% target over a three-year horizon either. The governor said the groundwork for the start of a sustainable disinflation in 2024 is being laid. Even if the recent policy tightening under Erkan was less than markets hoped for (900 bps to 17.5%), the new forecasts in any case suggest the central bank is far from done. For the Turkish lira, the proof of the pudding is in the eating. USD/TRY stabilizes around record highs just south of the 27 big figure.

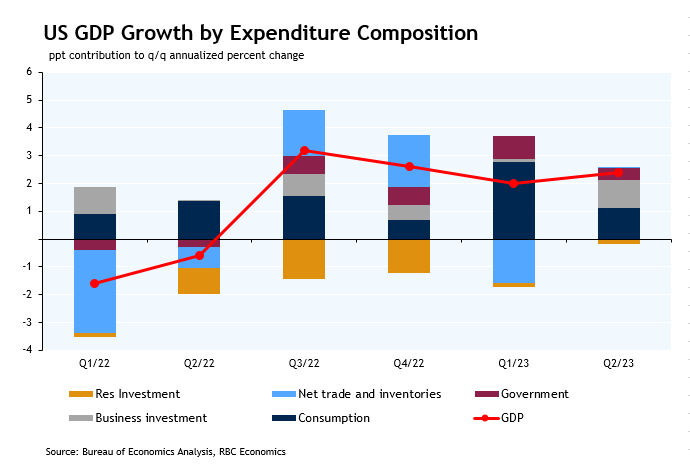

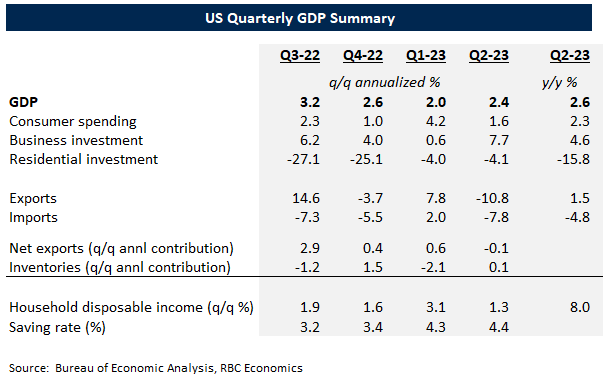

US: Real GDP Expanded Solidly in Q2, Beating Expectations

Real GDP expanded by a solid 2.4% quarter-over-quarter (q/q, annualized) in the second quarter of 2023. The reading came in notably above the consensus forecast, which called for a modest gain of 1.8% q/q.

Consumer spending grew by 1.6% – decelerating from 4.2% recorded in Q1. Spending on services (+2.1%) accounted for most of the gains, while durable (+0.4%) and non-durable (+0.9%) expenditures also ticked up.

Business investment jumped 7.7% q/q, as capital outlays on equipment (+10.8%) and intellectual property products (+3.9%) both rebounded. In addition, investments in structures continued to see robust strength (+9.7%).

Residential investment (-4.1%) continued to decline in Q2, despite a modest turnaround in residential construction, as sales of new and existing homes continued to struggle under higher mortgage rates.

Government spending increased 2.6% q/q, as spending at both the federal (+0.9%) and state & local (+3.6%) level moved higher. Federal expenditure growth moderated as nondefense spending declined, while defense spending continued to grow.

Exports fell by 10.8% in the second quarter, while imports recorded a more modest decline of 7.8%. This left the trade deficit roughly unchanged from Q1.

Inventory investment ticked up slightly in the second quarter – adding 0.1 percentage points to headline growth.

The core PCE deflator rose 3.8% on a q/q (annualized) basis – decelerating from 4.9% in Q1.

Key Implications

The U.S. economy expanded for a fourth consecutive quarter in 2023Q2, marking a full year of growth since the brief slowdown at the start of 2022. The resilience in consumer spending – which makes up roughly two thirds of GDP – has kept the economy growing solidly during the first half of the year. With the labor market remaining strong, consumers have been able to weather the headwinds of higher prices and higher interest rates so far.

This was shown in domestic demand in the second quarter, with steady consumer spending on services being joined by modest growth in durable and non-durable expenditures. Business investment also jumped up in the second quarter as equipment purchases rose notably and investment in structures remained elevated. Measures of consumer and business sentiment have stabilized in recent months as near-term growth prospects have improved, although future expectations remain relatively pessimistic.

With the Federal Reserve's most recent hike yesterday, the policy rate now sits at its highest level in 22 years. Progress has been made on the inflation front, however the Federal Reserve will need more time to decide whether the trajectory is pointing to a sustainable return to its 2% target. The cumulative effects of the 525bps in rate hikes have not yet fully filtered through the economy and are expected to continue to weigh on economic growth through the second half of this year.

Euro Sinks as ECB Signals a September Pause is Possible

The ECB raised rates for potentially the final time in the tightening cycle on Thursday, although it refused to give any indication of what will happen going forward.

Instead, the central bank is insisting that decisions will be guided by the economic data and that interest rates will need to remain sufficiently restrictive for some time. This is consistent with what we heard from the Fed a day earlier and what most major central banks will be communicating soon enough if they aren't already.

We remain in a period of uncertainty on the economic data, despite the progress that has already been achieved and the further moves that are expected over the rest of the year. If the inflation data continues to improve as many expect, there's every chance the ECB pauses in September and doesn't then feel it necessary to hike further by October.

There are, of course, an abundance of upside risks to the inflation data from the economy continuing to display significant resilience, as we've already seen this year, or fresh energy or food price shocks. These things and more could tempt the ECB to hike further later in the year.

The lack of commitment to further rate hikes from the ECB today weighed on the euro and saw eurozone yields decline. The single currency plunged against the dollar, slipping back below 1.10 after coming close to 1.1150 earlier in the day.

It would appear the ECB has failed to open the door to a pause without triggering too much excitement, as it would have preferred. President Lagarde was desperately trying to avoid doing so in the press conference, repeatedly referring back to previous comments rather than directly answering questions, and it seems in doing so, traders have instead opted to read between the lines. We may see efforts to correct this in the weeks ahead.

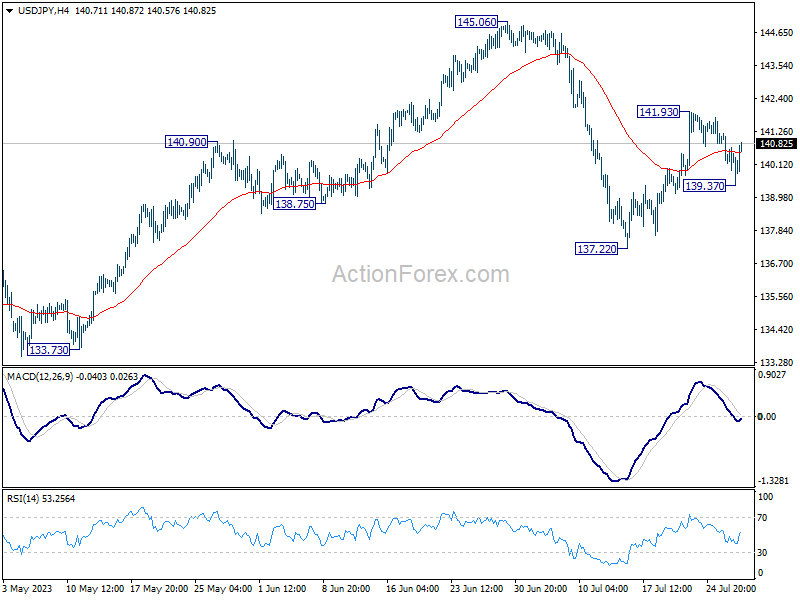

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 139.73; (P) 140.46; (R1) 140.98; More...

Intraday bias in USD/JPY is turned neutral again as it recovered after dipping to 139.37. On the upside, break of 141.93 will resume the rebound from 137.22 and target a test on 145.06 high. On the downside, below 139.37 will bring deeper fall to retest 137.22 support instead.

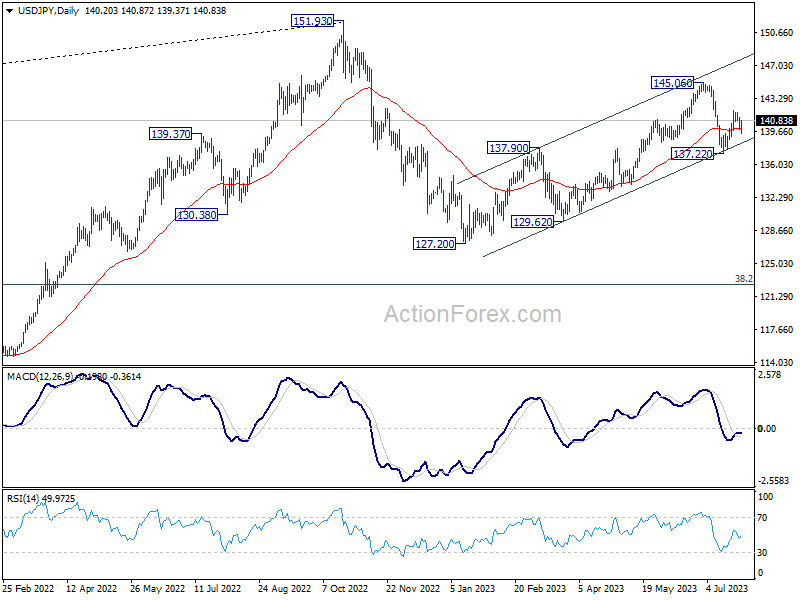

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Current development suggests that the second leg (the rise from 127.20) might not be over yet. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

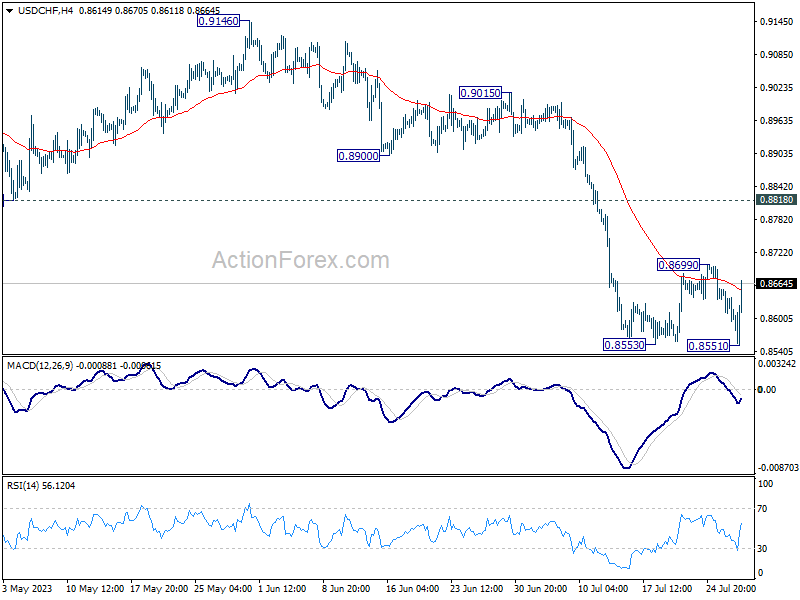

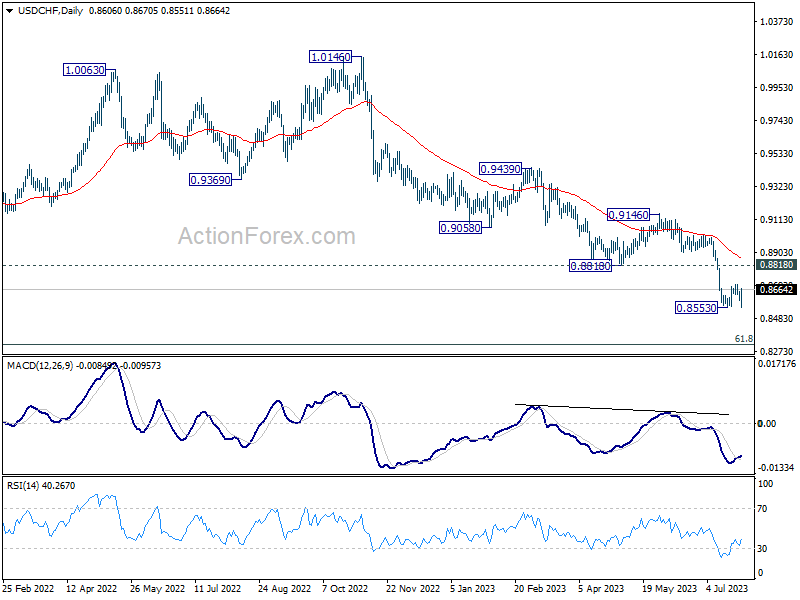

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8585; (P) 0.8621; (R1) 0.8643; More...

USD/CHF rebounded after dipping to 0.8551 but stays below 0.8699 resistance. Intraday bias remains neutral first. On the upside, above 0.8699 will bring stronger rise towards 0.8818 support turned resistance. on the downside, firm break of 0.8551 will resume larger down trend from 1.0146, targeting 0.8317 fibonacci level.

In the bigger picture, the break of 0.8756 (2021 low) indicates break out from the long term range pattern. For now, medium term outlook will stay bearish as long as 0.9146 resistance holds. Further fall would be seen to 61.8% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.8317 next.

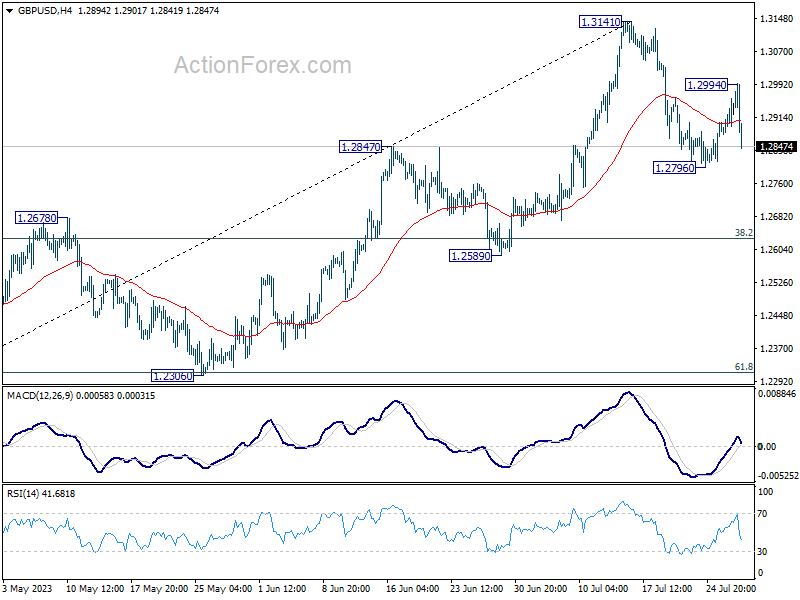

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2840; (P) 1.2872; (R1) 1.2935; More...

GBP/USD falls sharply after hitting 1.2994 and intraday bias is turned neutral again. On the downside, break of 1.2796 will resume the fall from 1.3141 to 55 D EMA (now at 1.2721) and possibly below. On the upside, above 1.2994 will resume the rebound from 1.2796 and target a test on 1.3141 high instead.

In the bigger picture, as long as 1.2678 resistance turned support holds, rise from 1.0351 (2022 low) is expected to continue. Next target is 100% projection of 1.0351 to 1.2445 from 1.1801 at 1.3895. However, sustained break of 1.2678 will argue that it's at least correcting this rally, with risk of bearish reversal..

U.S. GDP Growth Accelerated in Q2

Q2 U.S. GDP came in at 2.4% (annualized rate), up from a 2% growth in the prior quarter. Much of that growth was driven by consumer spending, and non-residential investment.

Consumer spending growth slowed, but was still firm at 1.6% with spending on goods little changed but spending on services rising solidly (2.1%).

Non-residential investment surged 7.7% in Q2, with investment on equipment being the largest contributor, which grew 10.8% after two consecutive declines.

Residential investment fell by -4.1%, consistent with another tick lower in existing home sales in Q2. Residential investment likely will rise for the first time in ten quarters in Q3 with signs that housing markets may be past their bottom.

Household disposable incomes jumped another 5.2% in Q2 reflecting still-resilient labour markets and firm wage growth. The household savings rate also edged higher (+0.1%), suggesting that household purchasing power is still strong.

Bottom line: GDP growth continued to climb in Q2, and the economy has been persistently more resilient than expected despite surging interest rates. Labour markets are still very strong, but Fed Chair Powell highlighted lower job vacancies and slower wage growth as signs of slowing under the surface. And inflation pressures have eased substantially in recent months. We expect labour markets to soften over the second half of the year and for slower inflation to be sustained – there are two more employment reports and two CPI reports before the Fed’s next policy decision. Contingent on that, we do not expect additional interest rate hikes from the Fed, although policymakers also won't hesitate to hike interest rates further if inflation were to reaccelerate.

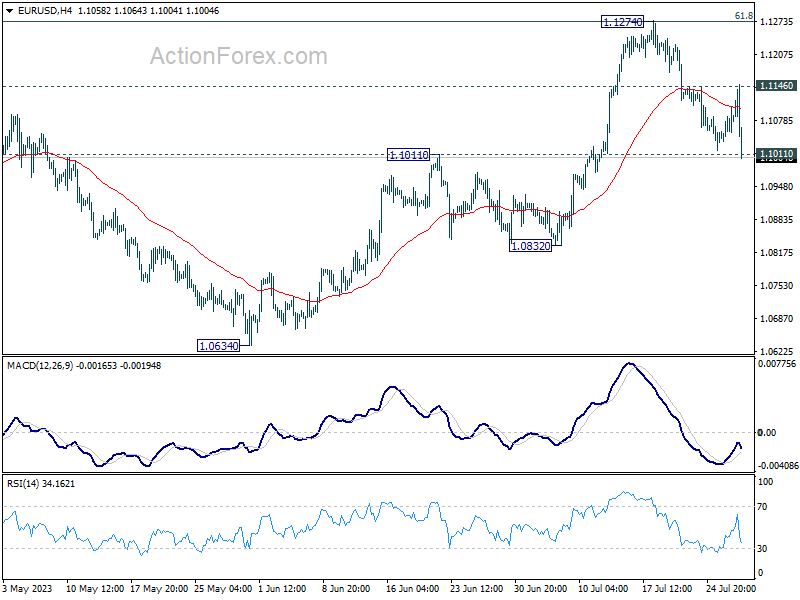

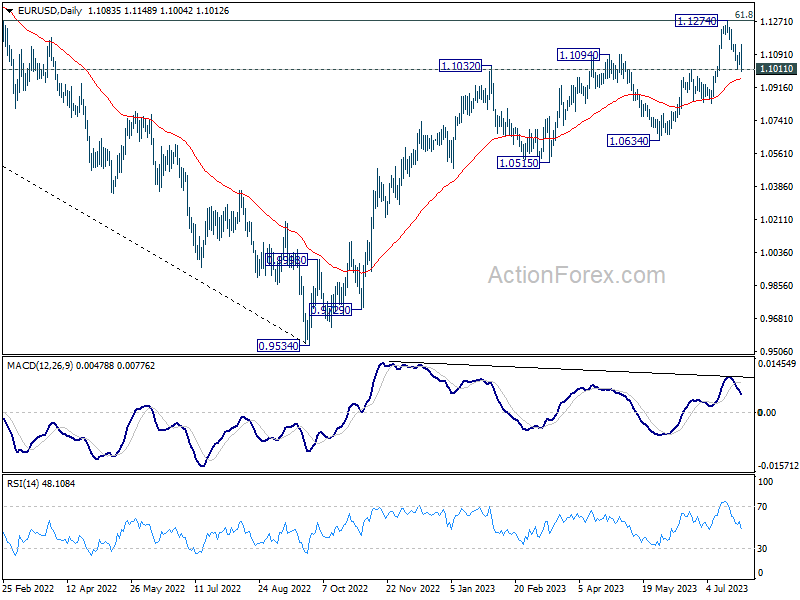

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1047; (P) 1.1077; (R1) 1.1115; More...

EUR/USD falls sharply after rejection by 1.1146 resistance and immediate focus is now on 1.1011 resistance turned support. Decisive break there will argue that larger correction is underway. Deeper fall would then be seen to 1.0832 support next. Nevertheless, rebound from current level, followed by firm break of 1.1146, will bring retest of 1.1274 high instead.

In the bigger picture, rise from 0.9534 is still expected to continue as long as 1.1011 resistance turned support holds. Decisive break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next. However, firm break of 1.1011 will indicate rejection by 1.1273 and raise the chance of reversal. Deeper fall would be seen back to 1.0634 support first.

Dollar Resurges after Strong GDP Data, Euro Weakens Post ECB Rate Hike

Euro turns weaker after ECB's expected rate hike. Downside momentum is also picking up when ECB President Christine Lagarde indicated that even minor alterations in the statement's phrasing were intentional. ECB has shifted its wording from interest rates "will be brought to" to will be "set" at a sufficiently restrictive level, providing a basis to that it's now restrictive enough for a pause.

Meanwhile, Dollar is making a robust comeback, triggered by stronger than expected GDP data, among other positive economic indicators. Despite being the second weakest currency for the week so far, sharing the spot with Euro, the greenback now appears to have a chance to alter its positive given the current momentum. However, the eventual picture for the week remains uncertain given that Yen might have some moves, as BoJ gears up for its policy announcement tomorrow. Meanwhile, it's starting to look hard for commodity currencies to maintain earlier gains.

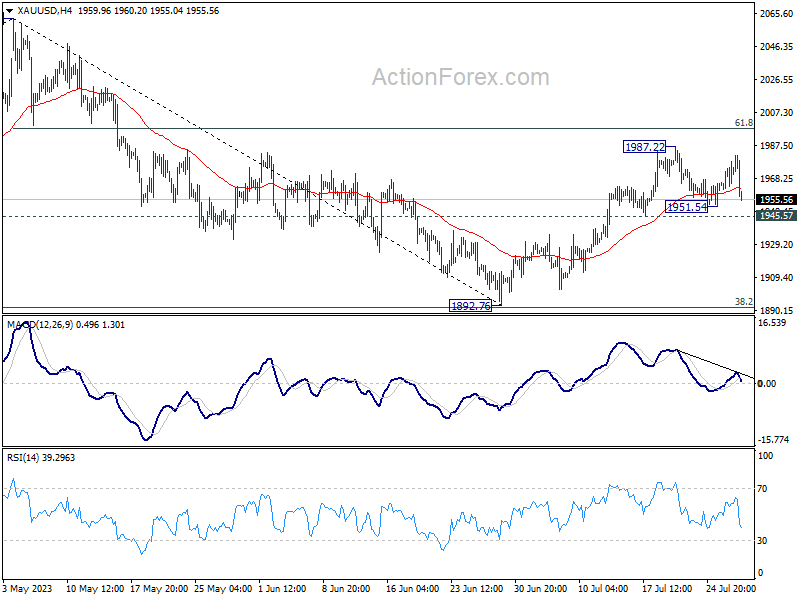

On the technical front, Gold experienced a downturn with the Dollar's resurgence, having failed to surpass the 1987.22 resistance mark. The consolidation from 1987.22 is extending with another drop. However, prospects for a further rise are still viable as long as the 1945.57 support level holds. Nevertheless, a firm break below 1945.57 could indicate the completion of the overall rebound from 1892.76 and may serve as a confirmation signal for an extended rally in the greenback.

In Europe, at the time of writing, FTSE is up 0.36%. DAX is up 1.36%. CAC is up 1.89%. Germany 10-year yield is down -0.047 at 2.439. Earlier in Asia, Nikkei rose 0.68%. Hong Kong HSI rose 1.41%. China Shanghai SSE dropped -0.20%. Singapore Strait Times rose 0.98%. Japan 10-year JGB yield dropped -0.0071 to 0.441.

US GDP grew 2.4% in Q2, faster than Q1 and above expectations

US GDP grew 2.4% annualized in Q2, according to the "advance" estimate, well above expectation of 1.6%. That's also a faster growth than Q1's 2.0% annualized. PCE price index slowed from 4.1% to 2.6% while PCE core price index also fell form 4.9% to 3.8%.

BEA said: "Compared to the first quarter, the acceleration in GDP in the second quarter primarily reflected an upturn in private inventory investment and an acceleration in nonresidential fixed investment. These movements were partly offset by a downturn in exports, and decelerations in consumer spending, federal government spending, and state and local government spending. Imports turned down."

Also released, in June, durable goods orders rose 4.7% versus expectation of 1.0%. Ex-transport orders rose 0.6%, versus expectation of 0.1%. Goods trade deficit narrowed to USD -87.8B, versus expectation of USD -91.8B.

Initial jobless claims dropped slightly to 221k in the week ending July 21, below expectation of 233k.

ECB hikes 25 bps, maintains data-dependent approach

ECB sticks to the script and delivers another 25bps hike on its three key interest rates today, meeting market expectations. The main refinancing, marginal lending, and deposit rates now stand at 4.25%, 4.50%, and 3.75% respectively, effective August 2.

In its statement, the ECB highlighted the ongoing concerns around inflation, indicating it was poised to remain "above the target for an extended period", despite expectations of a decrease over the remainder of the year. It also noted that while some measures showed signs of easing, "underlying inflation remains high overall."

ECB reiterated that it is committed to setting interest rates at "sufficiently restrictive" levels "for as long as necessary". Stressing the bank's ongoing commitment to a data-dependent strategy, it added, "The Governing Council will continue to follow a data-dependent approach to determining the appropriate level and duration of restriction."

ECB President Christine Lagarde said in post meeting press conference:

ECB President Christine Lagarde, struck a somber tone during the post-meeting press conference. She acknowledged that the economic outlook for Eurozone has "deteriorated" in the near term, citing persistent high inflation and tighter financial conditions as key factors pressuring the manufacturing output.

Lagarde stated, "High inflation and tighter financing... is weighing especially on manufacturing output, which is also being held down by weak external demand." Though she noted the resilience in the services sector, she cautioned that its "momentum is slowing". The economy is expected to "remain weak in the short run."

She then noted a shift in the drivers of inflation. External sources are easing, she noted, but domestic price pressures, including from rising wages and robust profit margins, are gaining prominence. "While some measures are moving lower, underlying inflation remains high overall," Lagarde pointed out.

Germany Gfk consumer sentiment edged up to -24.4 on declining inflation

Germany Gfk Consumer Sentiment for August improved from -25.2 to -24.4, slightly above expectation of -24.7. In July, Economic Expectations was unchanged at 3.7. Income Expectations rose from -10.6 to -5.1. Propensity to buy ticked up from -14.6 to -14.3.

"Currently, only income expectations are contributing to the improvement in consumer sentiment. The main reason for the decrease in pessimism is the hope of declining inflation rates," explains GfK consumer expert Rolf Bürkl.

"This has somewhat improved the chances of consumer sentiment resuming its recovery course. However, the level will still remain low in the coming months, and private consumption will therefore not be able to make a positive contribution to overall economic development."

Australia export price down -8.5% qoq in Q2, largest fall since 2009

Australia's Q2 Export Price Index registered -8.5% qoq drop, the most substantial quarterly decline since Q3 2009. Concurrently, the index declined -11.2% yoy compared to the same quarter last year. On the flip side, Import Price Index dipped slightly by -0.8% qoq, - 0.3% yoy.

Michelle Marquardt, Head of Price Statistics at Australian Bureau of Statistics (ABS), attributed this steep fall in the Export Price Index to a substantial contraction in global energy demand. "Global economic slowdown and eased supply pressures are contributing to a retreat in energy prices from their 2022 peak," said Marquardt.

The dampening effect of weaker energy prices extended to the Import Price Index, which saw a decline of -0.8% in Q2 2023. More specifically, the prices of petroleum and petroleum products decreased by -7.0% in this quarter. Nevertheless, this decline in energy prices was somewhat counterbalanced by inflationary pressures on various imported consumption and capital goods.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1047; (P) 1.1077; (R1) 1.1115; More...

EUR/USD falls sharply after rejection by 1.1146 resistance and immediate focus is now on 1.1011 resistance turned support. Decisive break there will argue that larger correction is underway. Deeper fall would then be seen to 1.0832 support next. Nevertheless, rebound from current level, followed by firm break of 1.1146, will bring retest of 1.1274 high instead.

In the bigger picture, rise from 0.9534 is still expected to continue as long as 1.1011 resistance turned support holds. Decisive break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next. However, firm break of 1.1011 will indicate rejection by 1.1273 and raise the chance of reversal. Deeper fall would be seen back to 1.0634 support first.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Import Price Index Q/Q Q2 | -0.80% | -0.80% | -4.20% | |

| 06:00 | EUR | Germany Gfk Consumer Confidence Aug | -24.4 | -24.7 | -25.4 | -25.2 |

| 12:15 | EUR | ECB Main Refinancing Rate | 4.25% | 4.25% | 4.00% | |

| 12:15 | EUR | ECB Rate On Deposit Facility | 3.75% | 3.75% | 3.50% | |

| 12:30 | USD | Initial Jobless Claims (Jul 21) | 221K | 233K | 228K | |

| 12:30 | USD | GDP Annualized Q2 P | 2.40% | 1.60% | 2.00% | |

| 12:30 | USD | GDP Price Index Q2 P | 2.60% | 3.10% | 4.10% | |

| 12:30 | USD | Goods Trade Balance (USD) Jun P | -87.8B | -91.8B | -91.1B | -91.9B |

| 12:30 | USD | Wholesale Inventories Jun P | -0.30% | -0.10% | 0.00% | |

| 12:30 | USD | Durable Goods Orders Jun | 4.70% | 1.00% | 1.80% | |

| 12:30 | USD | Durable Goods Orders ex Transportation Jun | 0.60% | 0.10% | 0.70% | |

| 12:45 | EUR | ECB Press Conference | ||||

| 14:00 | USD | Pending Home Sales M/M Jun | -0.50% | -2.70% | ||

| 14:30 | USD | Natural Gas Storage | 12B | 41B |