Sample Category Title

GBP/JPY Weekly Outlook

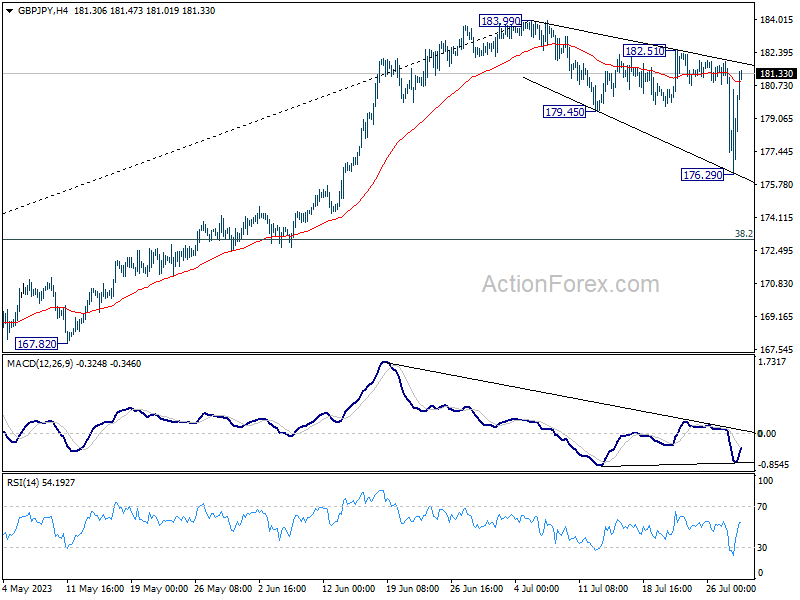

GBP/JPY dropped sharply to as low as 176.29 but rebounded strong well ahead of 38.2% retracement of 155.33 to 183.99 at 173.04. The development argues that price actions from 183.99 high are merely correcting the rise from 155.33. Initial bias stays neutral this week first. Break of 182.51 resistance should bring further rise through 183.99 to resume larger up trend. Meanwhile, outlook will now stay bullish as long as 173.04 holds, in case of another dip.

In the bigger picture, as long as 172.11 resistance turned support holds, up trend from 123.94 (2020 low) is expected to continue through 183.99 at a later stage, towards 195.86 (2015 high). Nevertheless, firm break of 172.11 will argue that larger correction is already underway.

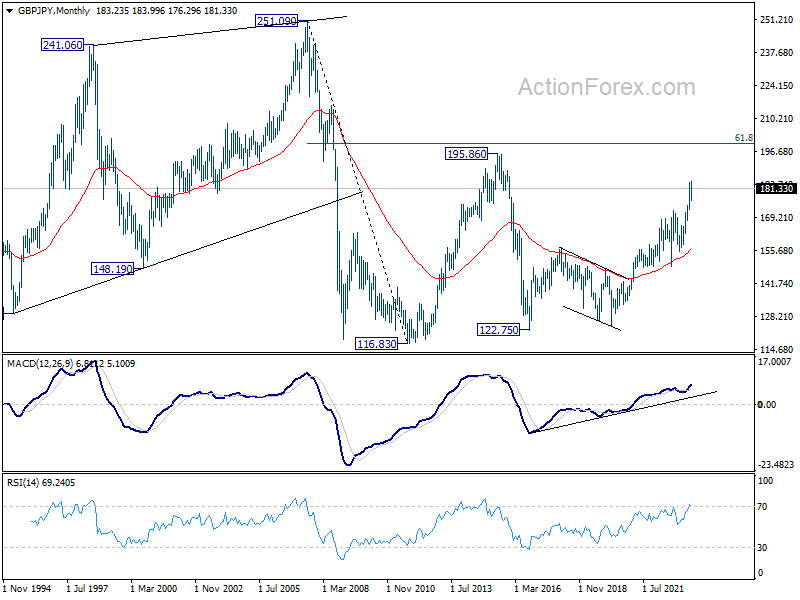

In the longer term picture, rise from 122.75 (2016 low) in still in progress to retest 195.86 (2015 high). Based on current momentum, break of 195.86 is in favor. But strong resistance could still be seen from 61.8% retracement of 251.09 (2007 high) to 116.83 (2011 low) at 199.80 to limit upside on first attempt.

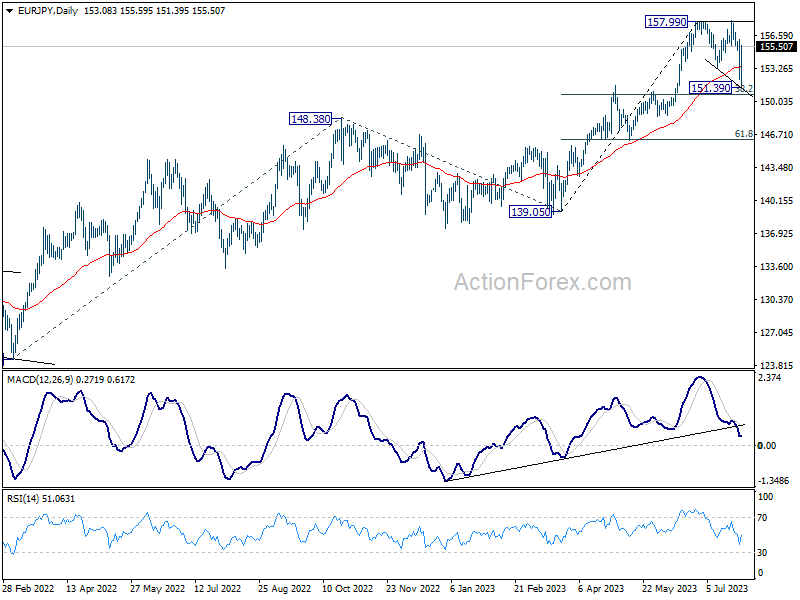

EUR/JPY Weekly Outlook

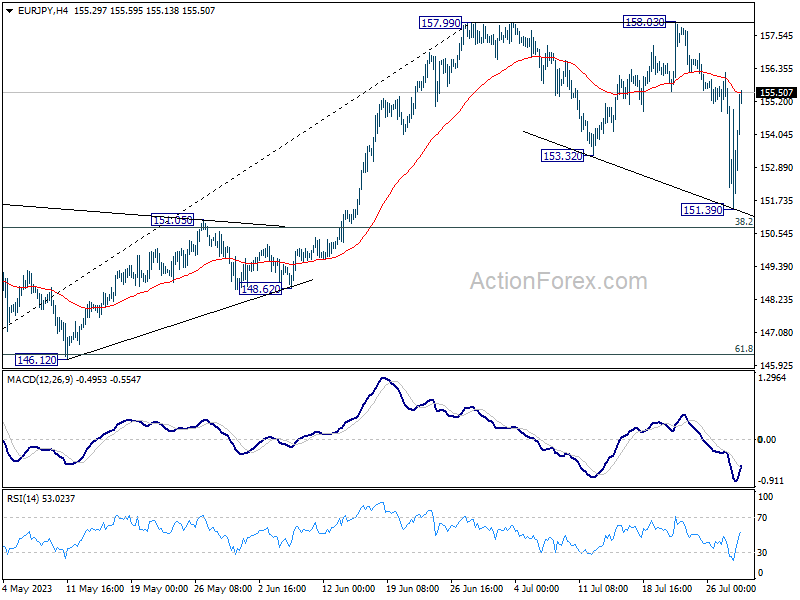

EUR/JPY dropped sharply to as low as 151.39 last week, but recovered strongly ahead of 38.2% retracement of 139.05 to 157.99 at 150.77. The development argues that price actions from 157.99 are merely a correction to the rise from 139.05 only. Initial bias stays neutral this week first. Break of 157.99 will resume larger up trend to 162.82 projection level next. For now, outlook will remain bullish as long as 150.77 holds, in case of another dip.

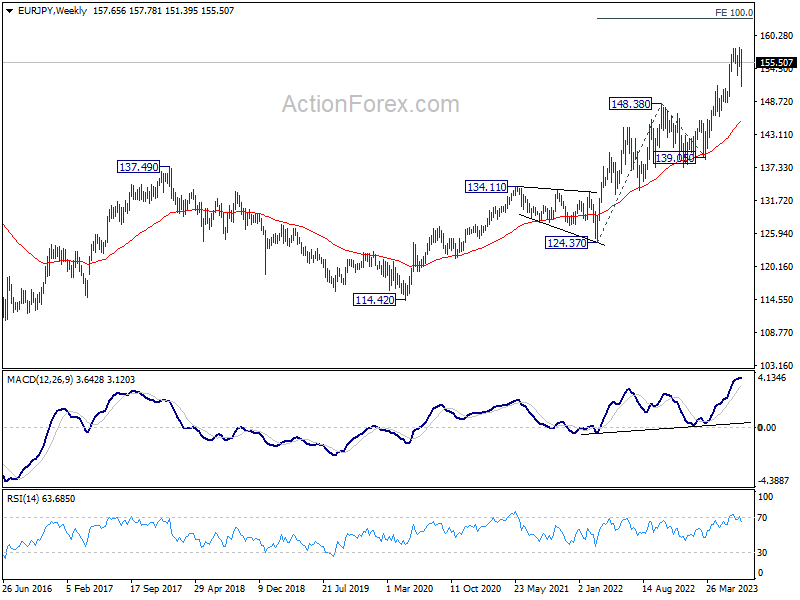

In the bigger picture, as long as 151.60 resistance turned support holds, rise from 114.42 (2020 low) is in progress. On resumption, next target is 100% projection of 124.37 to 148.38 from 138.81 at 162.82. Nevertheless, sustained break of 151.60 will argue that larger correction is already underway. Deeper decline would be seen to 55 W EMA (now at 145.56).

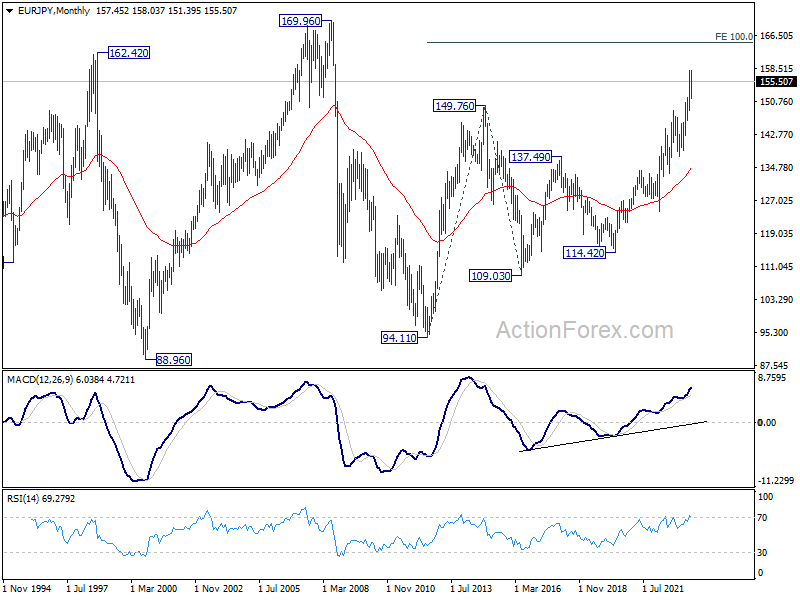

In the long term picture, rise from 109.03 (2016 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 109.03 at 164.68, and possibly further to 169.96 (2008 high).

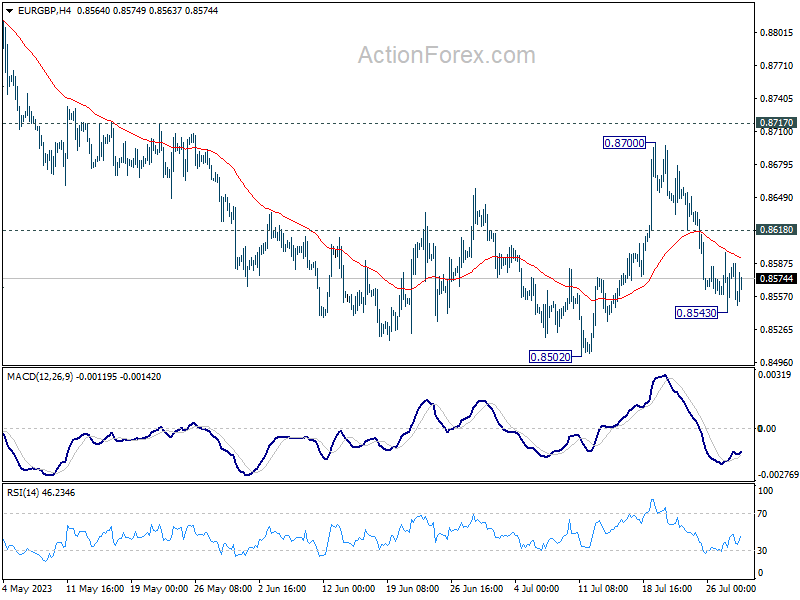

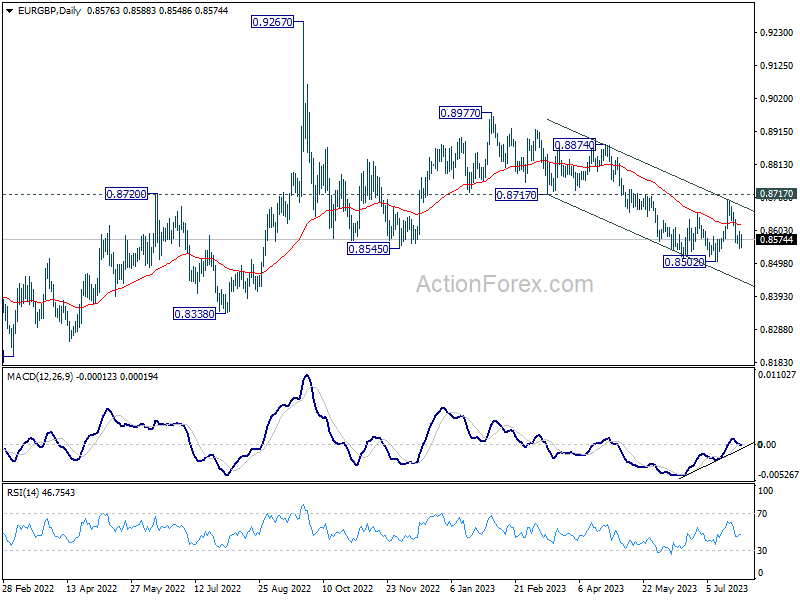

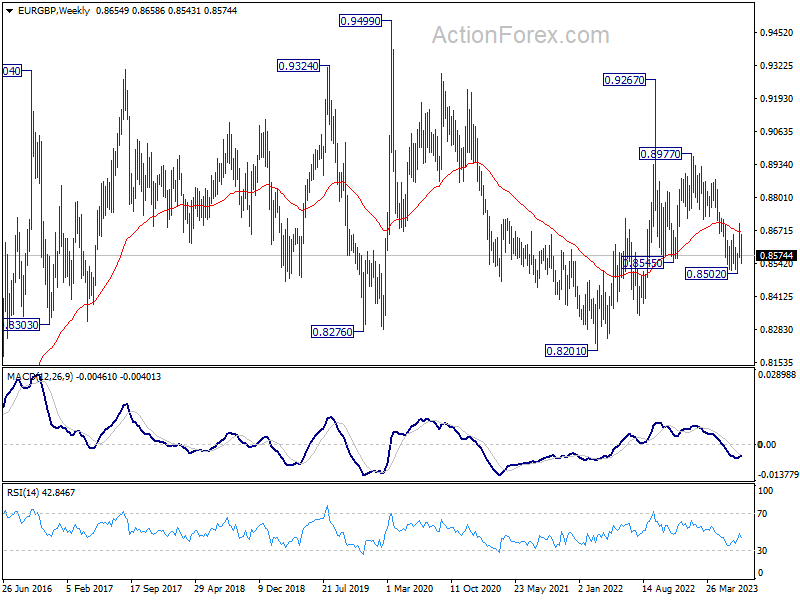

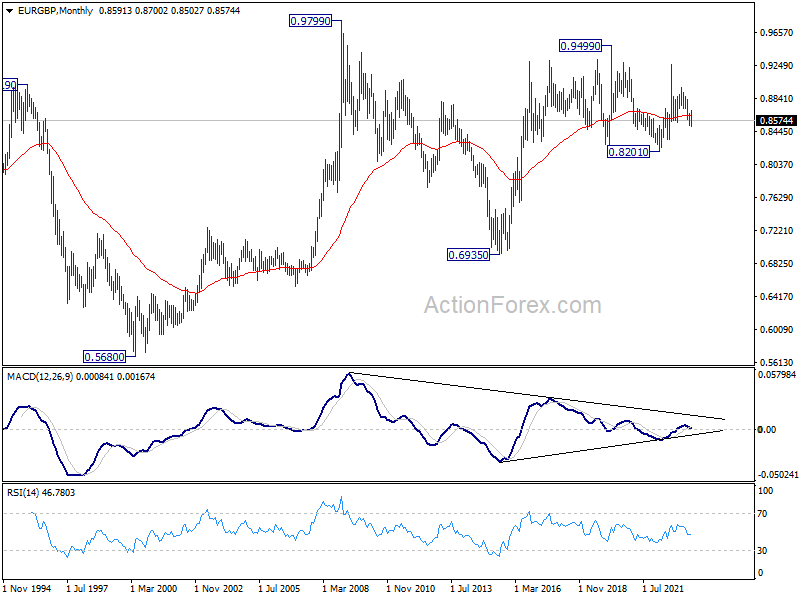

EUR/GBP Weekly Outlook

EUR/GBP's steep pull back last week mixed up the near term outlook. Initial bias stays neutral this week first. On the downside, below 0.8543 will target a test on 0.8502 low. Decisive break there will resume larger decline from 0.8977. On the upside, above 0.8618 minor resistance will turn bias back to the upside for 0.8700, and possibly further to 0.8717 key support turned resistance.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Firm break of 0.8717 support turned resistance will argue that it has completed with three waves down to 0.8502. Further break of 0.8977 will bring retest of 0.9267 high. Nevertheless, rejection by 0.8717, followed by break of 0.8502 will resume the decline towards 0.8201 (2022 low).

In the long term picture, long term range pattern is extending. But rise from 0.6935 (2015 low) is expected to resume at a later stage, to 0.9799 (2009 high).

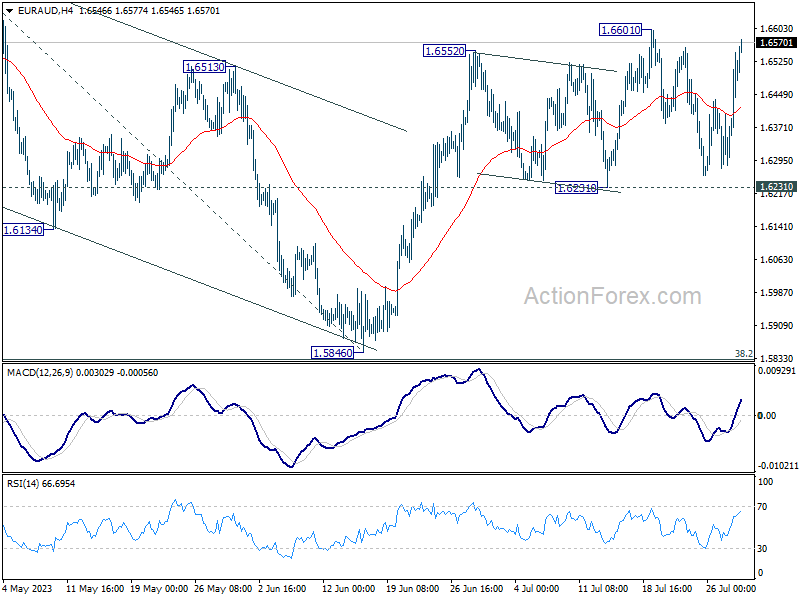

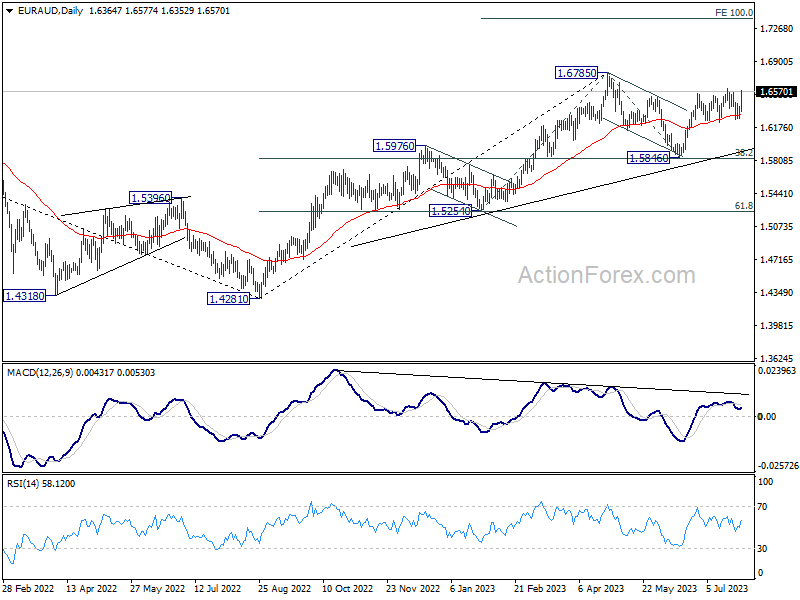

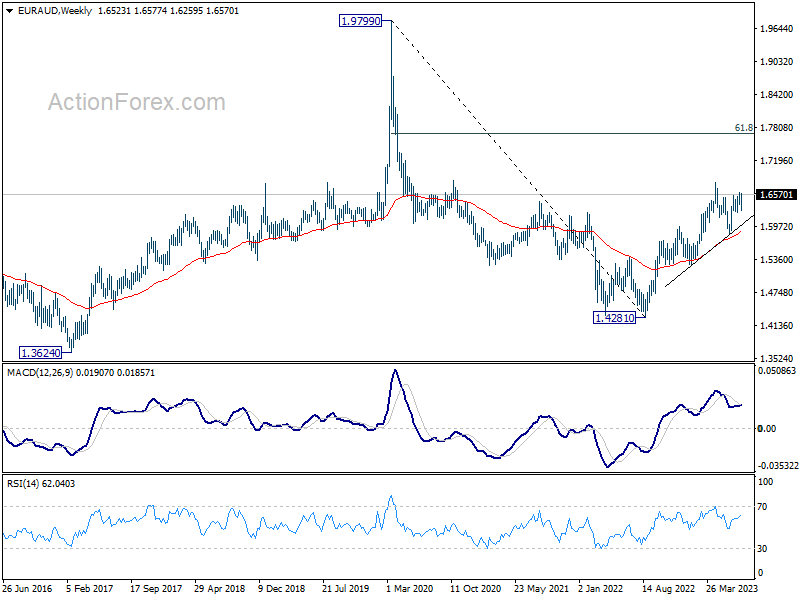

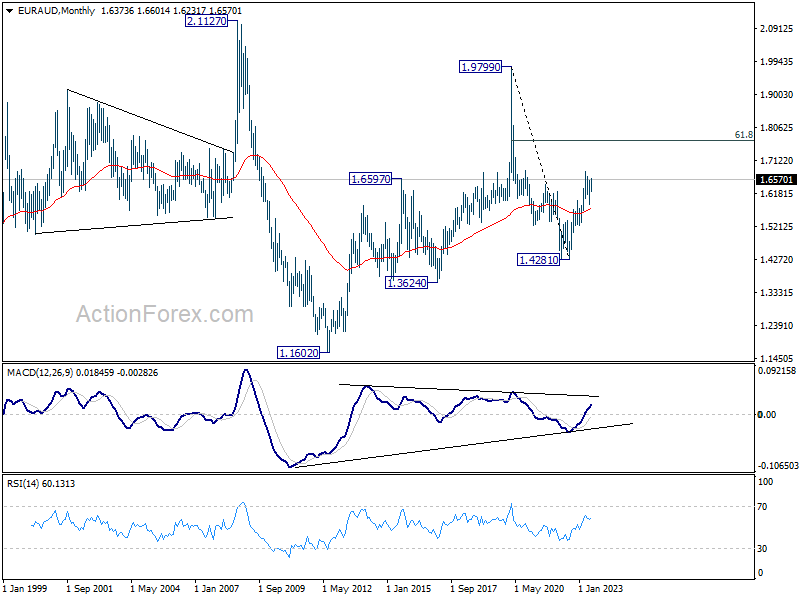

EUR/AUD Weekly Outlook

EUR/AUD stayed in range of 1.6231/6601 last week and outlook is unchanged. Initial bias remains neutral this week first. Further rally is expected with 1.6231 support intact. Firm break of 1.6601 will solidify the case that corrective fall from 1.6785 has completed, and target a retest on this high next.

In the bigger picture, with 38.2% retracement of 1.4281 to 1.6785 at 1.5828 intact, rally from 1.4281 is still in progress. Firm break of 1.6785 will confirm rise resumption. Next target is 100% projection of 1.5254 to 1.6785 from 1.5846 at 1.7377. On the other hand, rejection by 1.6785 will extend the corrective pattern with another fall leg. But outlook will stay bullish as long as 1.5828 holds.

In the longer term picture, it's still early to decide if rise from 1.4281 is resuming whole up trend from 1.1602 (2012 low). But in either case, further rally is in favor as long as 1.5254 support holds. Next target is 61.8% retracement of 1.9799 to 1.4281 at 1.7691.

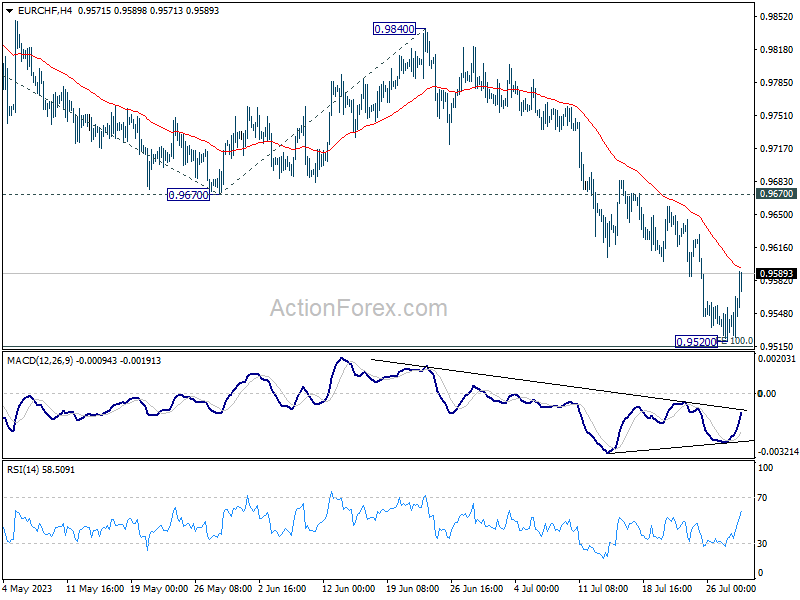

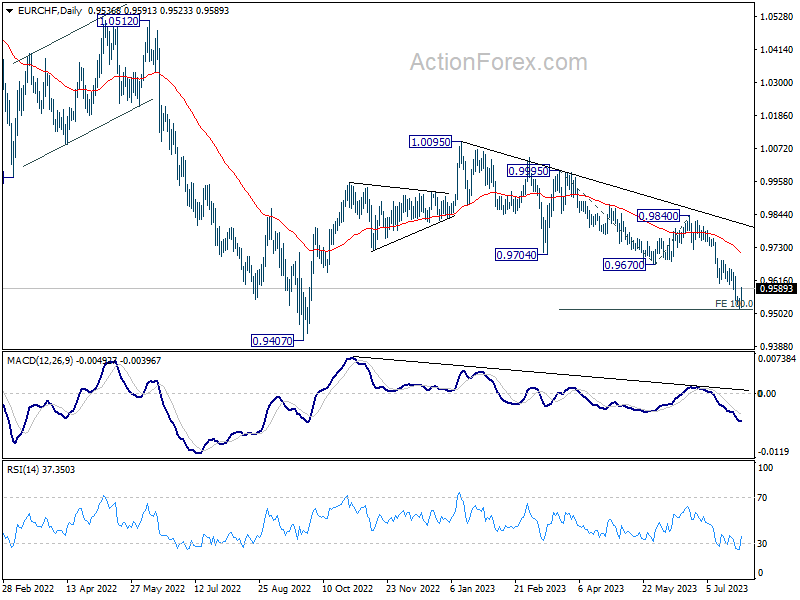

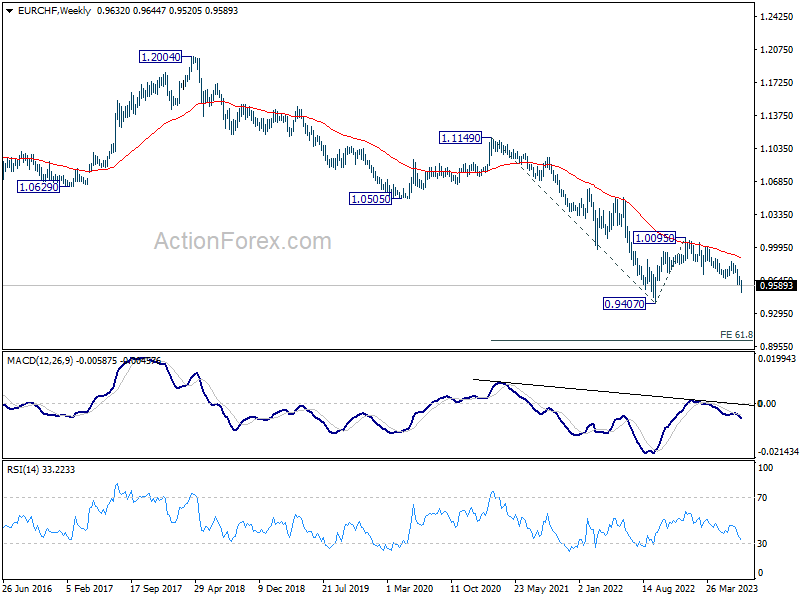

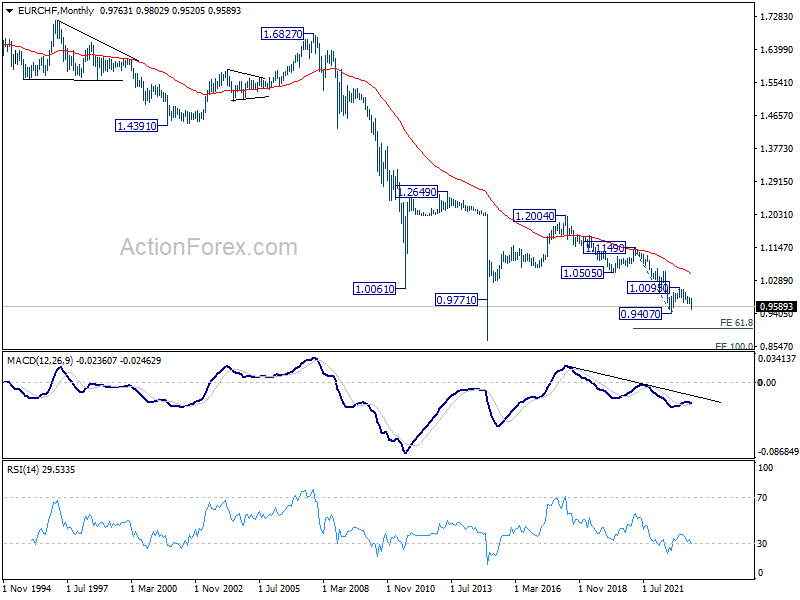

EUR/CHF Weekly Outlook

EUR/CHF's down trend resumed last week and fell to as low as 0.9520, just ahead of 100% projection of 0.9995 to 0.9670 from 0.9840 at 0.9515. A temporary low should be in place with subsequent recovery. Initial bias is turned neutral this week for consolidations. Outlook will remain bearish as long as 0.9670 support turned resistance holds. Break of 0.9520 will resume the fall from 1.0095 to 0.9407 low.

In the bigger picture, medium term outlook is staying bearish as the pair is capped well below falling 55 W EMA (now at 0.9876). Down trend from 1.2004 (2018 high) is in favor to continue. Sustained break of 0.9407 will target 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. For now, this will remain the favored case as long as 0.9840 resistance holds, in case of strong rebound.

In the long term picture, outlook remains bearish as it's staying well below 55 M EMA (now at 1.0459). Break of 1.00095 resistance is needed to be the first sign of bottoming, or the multi-decade down trend is expected to continue.

Weekly Economic & Financial Commentary: Fed Hikes and Keeps Its Options Open

Summary

United States: Ground Control to Major Powell: Odds of Soft Landing Rising

- Economic data continued to beat expectations this week. Real GDP came in at a stronger-than-expected 2.4% annualized rate in Q2. Inflation and compensation costs have decelerated; yet, we suspect the FOMC would like to see continued moderation before it concludes that inflation is sufficiently low and stable.

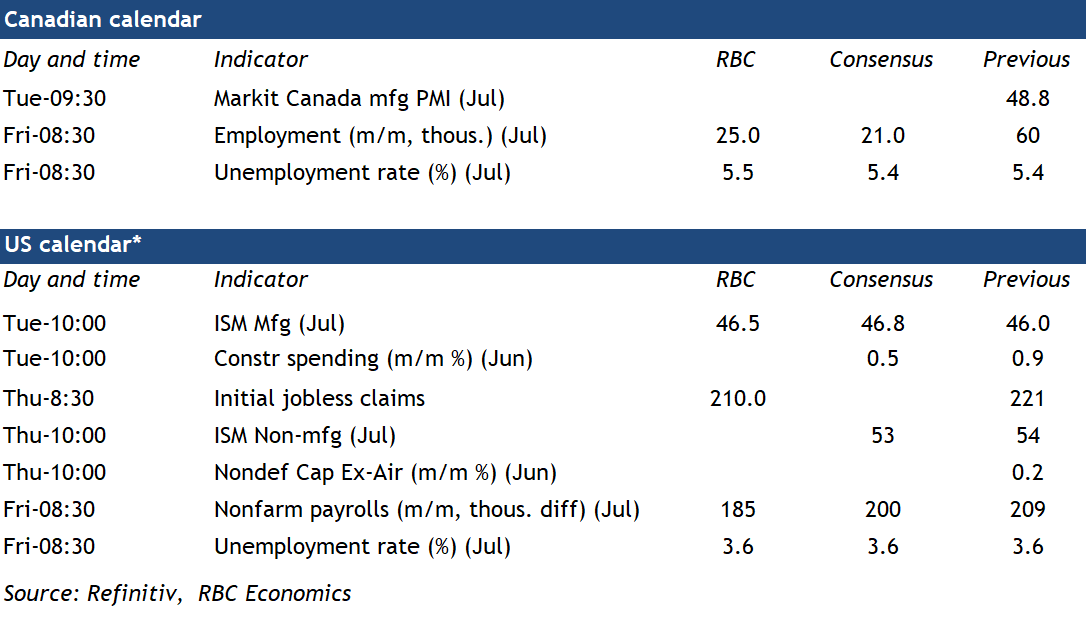

- Next week: Construction Spending (Tue.), ISM Indices (Tue. & Thu.), Employment (Fri.)

International: European Central Bank Raises Interest Rates; Bank of Japan Tweaks Monetary Policy

- The European Central Bank (ECB) raised its Deposit Rate 25 bps to 3.75% at this week's policy announcement, but was cautious in offering any guidance about policy beyond this July meeting. We expect the ECB to hold rates steady for an extended period in September and beyond, and do not see the ECB easing monetary policy until Q2-2024. The Bank of Japan tweaked its monetary policy stance in a hawkish direction, saying it would allow 10-year Japanese Government Bond Yields to rise flexibly to somewhere between 0.50% and 1.00%.

- Next week: China PMIs (Mon.), Reserve Bank of Australia Policy Rate (Tue.), Bank of England Policy Rate (Thu.)

Interest Rate Watch: Fed Hikes and Keeps Its Options Open

- The Federal Open Market Committee hiked the federal funds rate by 25 bps at its July monetary policy meeting. The post-meeting communication was little changed from June as the committee keeps its options open regarding additional tightening.

Topic of the Week: Summer Strife

- A string of labor disputes have put union activity and workers' bargaining power front and center. The willingness to strike reflects the tight state of the labor market as well as decades-high inflation. With union compensation growth lagging behind inflation and non-union pay over the past few years, the push appears to be more catch-up than a canary of future wage trends.

The Weekly Bottom Line: Preparing for Landing

U.S. Highlights

- Fed Chair Powell signaled a meeting-by-meeting approach on changes to the fed funds rate, opting to evaluate incoming data and fine-tune interest rates to help temper inflation.

- The second quarter’s GDP release showed an economy that continues to chug along at a solid pace – exceeding expectations for a steeper slowdown.

- The Fed will keep rates in restrictive territory into next year so, even if a recession is avoided, tepid economic growth is to be expected.

Canadian Highlights

- Canadian GDP growth has pointed to a new cruising speed, as the country worked through several shocks, including the public sector strike and wildfire shutdowns.

- The BoC’s summary of deliberations signaled the central bank is trying to strike the right balance between bringing inflation back to target without putting too much pressure on the economy.

- With underlying data pointing to inflation being stuck around 3%, the BoC appears to be leaning hawkishly, which has kept yields elevated and supported the loonie.

U.S. – Preparing for Landing

Readers would be right to ask, what’s “moderate” about another upside surprise to economic growth in the second quarter? Fed Chair Powell signaled a meeting-by-meeting approach on changes to the fed funds rate, opting to evaluate incoming data and fine-tune interest rates to help temper inflation. Incoming data have shown that the economy remains resilient – buoyed by healthy consumer spending growth and business investment – as fears of a recession gradually fade. What remains to be seen is whether inflation will continue to moderate in the coming months or whether the Fed will have to push interest rates higher still – thereby raising the odds the economy contracts.

The second quarter’s GDP release showed an economy that continues to chug along at a solid pace – exceeding expectations for a steeper slowdown. However, the composition of growth was interesting. In line with our forecasts, consumer spending growth advanced 1.6% quarter-on-quarter (q/q) annualized – slowing from 4.2% in Q1. The Fed will be reassured that its rate hiking cycle is filtering through to consumer behavior as spending growth slows despite a drum-tight labor market. Moreover, with rates at multidecade highs, the housing market is feeling the force of tight financing conditions, with residential investment continuing to pull back in the second quarter – now contracting for the ninth quarter in a row. With demand growth slowing, imports pulled back again – now having contracted for the third time in the past year. The gradual slowdown is also not unique to the U.S., as plummeting export growth indicates the global economy is slowing under the weight of inflation and higher interest rates.

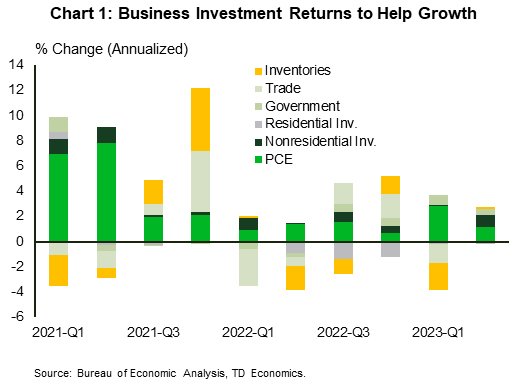

A pleasant surprise in the data was the healthy activity in the business sector that provided a meaningful lift to the economy (Chart 1). Nonresidential investment advanced 7.7% q/q – good for the strongest showing since the first quarter of 2022. The flow of federal funds to support climate friendly investments is helping fuel the ongoing strength in structures and equipment investment – the latter registering its best quarterly growth rate since 2011, outside of the post-2020 lockdown bounce.

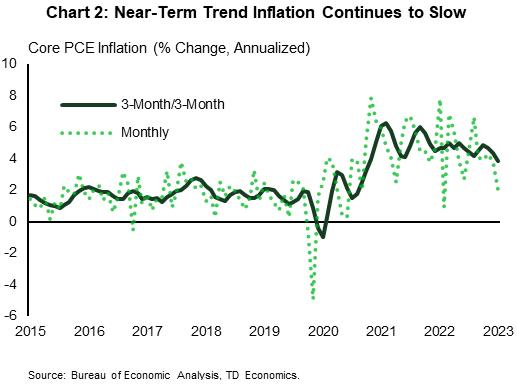

With full second quarter data showing a healthy consumer, all eyes were on June’s personal income and outlay report for signals of spending and price momentum heading into the summer months. Healthy spending held up in June and outstripped income growth, denting the personal savings rate. Between higher interest rates, strong inflation and depleting savings the pandemic era spending binge is slowing down. This is music to the Fed’s ears as it means softening inflationary pressures. Needless to say, the downside surprise on core PCE inflation (4.1% year-on-year vs. 4.2% expected) was a particularly welcome development. Even more encouraging, the near-term trend (Chart 2) has eased to its slowest pace since March 2021.

With inflation slowing and consumer spending remaining resilient the odds of a soft landing are ticking higher. However, the Fed will keep rates in restrictive territory into next year so, even if a recession is avoided, tepid economic growth is to be expected.

Canada – Canadian Economy Searching for Balance

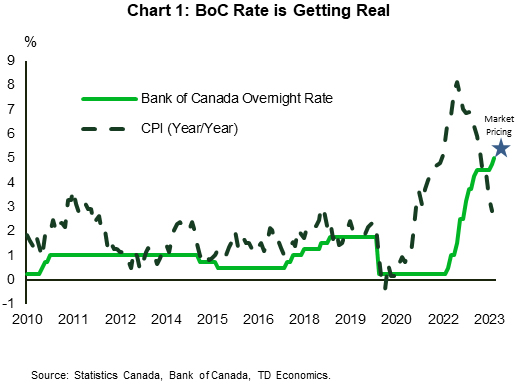

Economic momentum in Canada looks to be finding its cruising speed in spite of a number of shocks that hit the country over the last few months. With GDP accelerating in May, and payroll data bouncing back strongly, expectations for another Bank of Canada (BoC) hike have nudged higher this week (Chart 1). This has the Canada two-year yield reaching a 22 year high of 4.8%, pushing the Canadian dollar to the upper end of the 72 to 76 U.S. cent range that has prevailed over the last ten months.

After leading the G7 in GDP growth in the first quarter of 2023, tracking for the Q2 has come in right around our estimate of 1% quarter-on-quarter annualized. Not bad considering the negative impulse coming from the public sector strike and wildfires that caused many firms in the oil & gas sector to shut production. Indeed, growth remained quite broad, with 12 of 20 industry sectors in expansion. Within this, the service sector continued to drive growth, a sign that cyclical strength may persist through the remainder of the summer.

As has been the case over 2023, strong consumer demand has been the impetus for Canadian economic resilience. And it hasn't just been people spending on 'need to have' items. Canadians have been spending on luxury items, such as new cars and dining out at restaurants. Such behaviour is not what occurs when people are preparing for recession. The robustness of the labour market has raised confidence. People have been seeing plenty of jobs on offer and wages rising faster than inflation. This improves purchasing power, notwithstanding the high interest rate environment. Just look at this week's payroll data, which showed a 130k gain in May and more than offset the impact of April's public sector strike decline.

The BoC has highlighted the resurgence in economic momentum for why it decided to execute on back-to-back rate hikes in June and July. While the BoC still thinks that consumer spending will cool on the back of past rate hikes, in its summary of deliberations, it stated that the "moderation will take longer than previously anticipated given the stronger-than-expected momentum in consumption in the second quarter and the combination of a still-tight labour market with accumulated savings by households”. In the BoC's mind, longer lags and less sensitivity to interest rates were convincing enough to keep increasing interest rates.

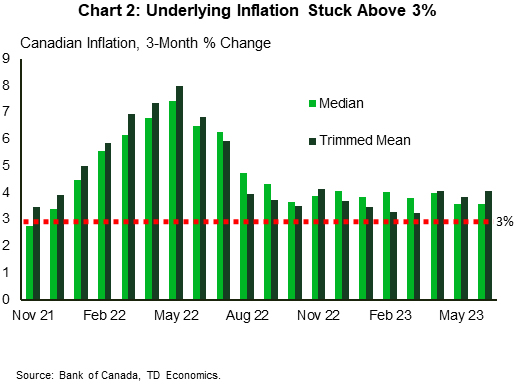

This speaks to the internal debate going on at the BoC. On one hand, the 475 basis point increase in the policy rate since early last year should eventually slow economic growth. But with the economy having surprised to the upside for most of this year, the Bank has had to question whether it has done enough. As we have written about a lot, the strength in consumer demand has caused expectations for core inflation to be stuck above 3% (Chart 2). So, although total CPI has moved to 2.8% year-on-year in June, forward-looking inflation indicators are signaling that the BoC will be hard-pressed to get inflation to settle at its 2% target.

All Eyes on Jobs Report Amid Booming Canadian Population Growth

Fresh labour market data for Canada and the U.S. lands next week. And both Bank of Canada Governor Tiff Macklem and U.S. Fed Chair Jerome Powell will be on the lookout for signs that higher interest rates are cooling things down.

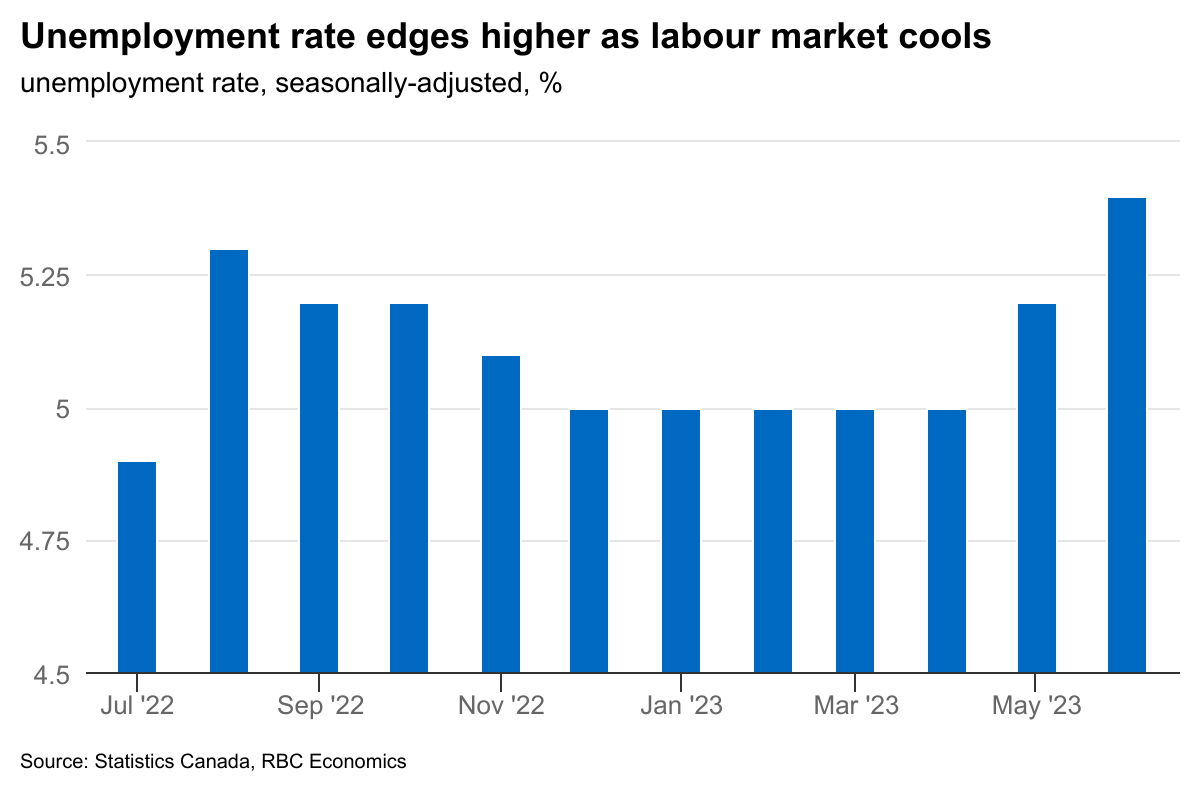

In Canada, we expect a 25,000 uptick in new jobs in July following a stronger increase of 60,000 jobs last month. Still, surging population growth means that won’t be enough to absorb all new labour market entrants. The unemployment rate edged up 0.2 percentage points in each of May and June and we look for another tick higher in July. Total job postings have also been trending lower. And slower wage growth in recent months has been consistent with signs that the surge of excess demand for workers in the economy has weakened.

The jobs report is among a slew of indicators to come in advance of the BoC’s next interest rate decision on September 6th (including one more monthly inflation reading.) The key question is whether interest rates (overnight rate now at 5% after another hike this month) are sufficiently restrictive to tame inflation. GDP has remained firmer than expected but has also been boosted by strong population growth. Per-capita GDP growth rates have been substantially softer. And higher unemployment rates would help to reassure the BoC that the balance of labour demand and supply is returning. We see softening job markets keeping the BoC on the sidelines with no additional interest rate increases this year. Still, central banks in Canada and abroad won’t hesitate to hike interest rates further if needed to put inflation back in target range.

Week ahead data watch

The next U.S. jobs report will come out on Friday. We expect the unemployment rate to hold steady at 3.6%, and non-farm payroll employment to rise (+185,000) in July, slightly lower than the +228,000 in the prior month. Labour markets remain firm, but we look for unemployment to drift higher during the second half of the year.

Week Ahead – BoE to Keep Hiking, US Jobs and Eurozone Inflation Eyed

US

With inflation steadily cooling, the Fed’s historic tightening campaign appears to be ending. The focus on Wall Street won’t just be inflation but now also economic activity.

The upcoming week will be filled with several economic readings. On Monday, we will see two Fed regional surveys. The MNI Chicago PMI is expected to slightly improve while the Dallas Fed manufacturing activity report remains deeply in negative territory. Tuesday will be busy with the final manufacturing PMI reading, the ISM manufacturing report, and JOLTS job openings. Wednesday contains the ADP employment change which is expected to show hiring cooled from the 497,000 pace to 185,000. Thursday has initial jobless claims and the ISM services report. Friday is all about the July nonfarm payroll report, which should show hiring eased from 209,000 to 185,000. The unemployment rate is expected to remain steady at 3.6%, while average hourly earnings on a monthly basis tick lower to a 0.3% pace.

Earnings will be massive this week as we get updates from Caterpillar, Pfizer, Uber, JetBlue, Humana, Yum Brands, Apple, and Amazon.

Eurozone

Next week gets off to a fast start, with eurozone flash HICP data released shortly after the European open. Further progress is expected in the report, albeit the more substantial moves aren’t expected until September. Still, favourable base effects and lower energy prices should ensure inflation continues to fall in the months ahead, alleviating pressure on the ECB to hike again in September.

UK

Many of the major central banks are now pondering whether further rate hikes are necessary, meaning meetings without them are going to become increasingly common. Unfortunately for the Bank of England, it can’t include itself in that list with at least a couple more hikes likely needed before it can even consider pausing. The inflation data last month was a big step in the right direction and if repeated over the next couple of months could leave the MPC in a much better position in November. For now, 25 basis points is the least we can expect and new forecasts will tell us how close they now feel they are to achieving their mandate.

Russia

The CBR is expected to release its monetary policy report on Monday which will be keenly eyed as the central bank has started raising interest rates again. There’s also a wide array of data being released next week including GDP, retail sales, unemployment, and PMIs.

South Africa

Next week mainly offers tier two and three economic data with the whole economy PMI on Thursday probably the pick of the bunch.

Turkey

Inflation is expected to spike again in July, rising 9.1% on the month and 47.3% on an annualized basis. The central bank has started raising rates again after the predictable failure of its pre-election easing program. But it has faced criticism for raising too slowly, something this report may highlight. Whether it will change anything is another thing as the central bank knows the views of President Erdogan and what has happened to previous policymakers that have raised rates faster.

Switzerland

CPI data on Thursday is expected to provide some comfort for the SNB, with prices seen falling slightly month on month in July. That is expected to take the annualized figure to 1.6% and well within the central bank’s target range, removing the pressure to raise rates again in September.

China

On Monday, we will have July’s NBS manufacturing & non-manufacturing PMIs. The consensus is for another month of contraction for the manufacturing sector at 49.2, slightly above June’s reading of 49. In the service sector, growth is forecast to decline further to 52.9 from 53.2 in June. If these data turn out as expected, it will be a fourth consecutive month of contraction for the manufacturing PMI and a fourth consecutive month of growth slowdown for the non-manufacturing PMI.

On Tuesday, the Caixin manufacturing PMI that includes small and medium-sized enterprises for July will be out. A slight dip in growth to 50.3 is expected, from 50.5. In addition, the Caixin services PMI will be released on Thursday; the consensus is eyeing a dip to 52 from 53.9 in June. If it comes in as expected, it will be the slowest growth in services since January 2023.

If these key PMIs continue to show softness in both external and internal demand, China policymakers are likely to see an increased need to introduce more targeted stimulus to shore up consumer demand and confidence after the recently concluded Politburo meeting that has vowed to introduce “counter-cyclical” measures to negate the current weakness seen.

India

Two key data will be released; the manufacturing PMI on Tuesday and the Services PMI on Thursday. A slight dip in growth in July’s manufacturing to 57 from 57.8 is expected in July. If it turns out as expected, it will be a second consecutive month of growth slowdown in the manufacturing PMI.

The services PMI for July is expected to dip slightly as well to 58 from 58.5 in June. If it turns out as expected, it will be a third consecutive month of growth slowdown in the services sector.

Australia

The key highlight for this week will be the RBA interest rate decision on Tuesday; a 25 basis points hike on the policy cash rate is expected to 4.35% after the RBA left it unchanged during the previous meeting.

Interestingly, data from the ASX 30-day interbank cash rate futures as of 28 July has only priced in an 8% chance of a rate hike of 25 bps on Tuesday which is down significantly from 48% last Friday, 21 July. This reduction in odds is likely due to the recent slowdown in Q2 inflationary growth.

Next up, we will have the balance of trade for June on Thursday.

New Zealand

Two key data points to watch in the coming week. Firstly, ANZ business confidence for July with the forecast calling for another dip to -22 from -18 in June.

Employment data will be out on Wednesday. The consensus for Q2 employment change is for a dip to 0.6% from 0.8% in Q1 while the Q2 unemployment rate is expected to tick up slightly to 3.5% from 3.4%, and the participation rate to hold steady at 72%.

Japan

Several key data releases in the coming week. On Monday, we will have industrial production, retail sales, and housing starts for June as well as consumer confidence data.

Industrial production is forecast to improve to 5.3% y/y in June from 4.2% y/y in May, the consensus for retail sales is expecting a slight increase to 5.9% y/y in June from 5.7% y/y in May while consumer confidence for July is forecasted to improve further to 36.8 in July from 36.2 in June.

The unemployment rate for June will be released on Tuesday with the consensus eyeing a slight dip to 2.5% from the 2.6% recorded in May.

Lastly, market participants will scan for more clues on further monetary policy normalization in the Bank of Japan’s monetary policy meeting minutes on Wednesday as it just implemented a creative flexible tweak on the upper and lower limits of the Yield Curve Control program for the 10-year JGB yield.

Singapore

The manufacturing PMI for July will be out on Wednesday, a slight improvement to 49.9 from 49.7 in June is being forecasted. Retail sales for June will be released on Friday where a dip is being forecast to 1% y/y from 1.8% y/y in May.

Lastly, the two major Singapore banks; DBS Group, and Oversea-Chinese Banking Corp will release their Q2 earnings on Thursday and Friday, respectively, before the market opens.

Summary 7/31 – 8/4

Monday, Jul 31, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | Industrial Production M/M Jun P | 2.40% | -2.20% |

| 23:50 | JPY | Retail Trade Y/Y Jun | 5.40% | 5.70% |

| 01:00 | CNY | NBS Manufacturing PMI Jul | 49.2 | 49 |

| 01:00 | CNY | Non-Manufacturing PMI Jul | 53.1 | 53.2 |

| 01:00 | NZD | ANZ Business Confidence Jul | -18 | |

| 01:00 | AUD | TD Securities Inflation M/M Jul | 0.10% | |

| 01:30 | AUD | Private Sector Credit M/M Jun | 0.40% | 0.40% |

| 05:00 | JPY | Housing Starts Y/Y Jun | -0.20% | 3.50% |

| 05:00 | JPY | Consumer Confidence Index Jul | 37 | 36.2 |

| 06:00 | EUR | Germany Import Price Index M/M Jun | -0.80% | -1.40% |

| 06:00 | EUR | Germany Retail Sales M/M Jun | -0.20% | 0.40% |

| 08:00 | EUR | Italy GDP Q/Q Q2 P | 0.00% | 0.60% |

| 08:30 | GBP | Mortgage Approvals Jun | 49K | 51K |

| 08:30 | GBP | M4 Money Supply M/M Jun | 0.50% | 0.20% |

| 09:00 | EUR | Eurozone GDP Q/Q Q2 P | 0.20% | -0.10% |

| 09:00 | EUR | Eurozone CPI Y/Y Jul P | 5.30% | 5.50% |

| 09:00 | EUR | Eurozone CPI Core Y/Y Jul P | 5.40% | 5.50% |

| 13:45 | USD | Chicago PMI Jul | 43.5 | 41.5 |

| 22:45 | NZD | Building Permits M/M Jun | -2.20% | |

| 23:01 | GBP | BRC Shop Price Index Y/Y Jun | 8.40% | |

| 23:30 | JPY | Unemployment Rate Jun | 2.60% | 2.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | Industrial Production M/M Jun P | |

| Forecast: 2.40% | Previous: -2.20% | ||

| 23:50 | JPY | Retail Trade Y/Y Jun | |

| Forecast: 5.40% | Previous: 5.70% | ||

| 01:00 | CNY | NBS Manufacturing PMI Jul | |

| Forecast: 49.2 | Previous: 49 | ||

| 01:00 | CNY | Non-Manufacturing PMI Jul | |

| Forecast: 53.1 | Previous: 53.2 | ||

| 01:00 | NZD | ANZ Business Confidence Jul | |

| Forecast: | Previous: -18 | ||

| 01:00 | AUD | TD Securities Inflation M/M Jul | |

| Forecast: | Previous: 0.10% | ||

| 01:30 | AUD | Private Sector Credit M/M Jun | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 05:00 | JPY | Housing Starts Y/Y Jun | |

| Forecast: -0.20% | Previous: 3.50% | ||

| 05:00 | JPY | Consumer Confidence Index Jul | |

| Forecast: 37 | Previous: 36.2 | ||

| 06:00 | EUR | Germany Import Price Index M/M Jun | |

| Forecast: -0.80% | Previous: -1.40% | ||

| 06:00 | EUR | Germany Retail Sales M/M Jun | |

| Forecast: -0.20% | Previous: 0.40% | ||

| 08:00 | EUR | Italy GDP Q/Q Q2 P | |

| Forecast: 0.00% | Previous: 0.60% | ||

| 08:30 | GBP | Mortgage Approvals Jun | |

| Forecast: 49K | Previous: 51K | ||

| 08:30 | GBP | M4 Money Supply M/M Jun | |

| Forecast: 0.50% | Previous: 0.20% | ||

| 09:00 | EUR | Eurozone GDP Q/Q Q2 P | |

| Forecast: 0.20% | Previous: -0.10% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Jul P | |

| Forecast: 5.30% | Previous: 5.50% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Jul P | |

| Forecast: 5.40% | Previous: 5.50% | ||

| 13:45 | USD | Chicago PMI Jul | |

| Forecast: 43.5 | Previous: 41.5 | ||

| 22:45 | NZD | Building Permits M/M Jun | |

| Forecast: | Previous: -2.20% | ||

| 23:01 | GBP | BRC Shop Price Index Y/Y Jun | |

| Forecast: | Previous: 8.40% | ||

| 23:30 | JPY | Unemployment Rate Jun | |

| Forecast: 2.60% | Previous: 2.60% | ||

Tuesday, Aug 1, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Jul F | 49.4 | 49.4 |

| 01:30 | AUD | Building Permits M/M Jun | -7.90% | 20.60% |

| 01:45 | CNY | Caixin Manufacturing PMI Jul | 50.3 | 50.5 |

| 04:30 | AUD | RBA Interest Rate Decision | 4.35% | 4.10% |

| 07:45 | EUR | Italy Manufacturing PMI Jul | 43.9 | 43.8 |

| 07:50 | EUR | France Manufacturing PMI Jul F | 44.5 | 44.5 |

| 07:55 | EUR | Germany Unemployment Change Jun | 15K | 28K |

| 07:55 | EUR | Germany Unemployment Rate Jun | 5.70% | 5.70% |

| 07:55 | EUR | Germany Manufacturing PMI Jul F | 38.8 | 38.8 |

| 08:00 | EUR | Italy Unemployment Rate Jun | 7.70% | 7.60% |

| 08:00 | EUR | Eurozone Manufacturing PMI Jul F | 42.7 | 42.7 |

| 08:30 | GBP | Manufacturing PMI Jul F | 45 | 45 |

| 09:00 | EUR | Eurozone Unemployment Rate Jun | 6.50% | 6.50% |

| 13:30 | CAD | Manufacturing PMI Jul | 48.9 | 48.8 |

| 13:45 | USD | Manufacturing PMI Jul F | 49.0 | 49.0 |

| 14:00 | USD | ISM Manufacturing PMI Jul | 46.5 | 46 |

| 14:00 | USD | ISM Manufacturing Employment Index Jul | 42.3 | 48.1 |

| 14:00 | USD | ISM Manufacturing Prices Paid Jul | 41.8 | |

| 14:00 | USD | Construction Spending M/M Jun | 0.60% | 0.90% |

| 22:45 | NZD | Employment Change Q2 | 0.60% | 0.80% |

| 22:45 | NZD | Unemployment Rate Q2 | 3.50% | 3.40% |

| 23:50 | JPY | Monetary Base Y/Y Jul | -0.70% | -1.00% |

| 23:50 | JPY | BoJ Minutes |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Jul F | |

| Forecast: 49.4 | Previous: 49.4 | ||

| 01:30 | AUD | Building Permits M/M Jun | |

| Forecast: -7.90% | Previous: 20.60% | ||

| 01:45 | CNY | Caixin Manufacturing PMI Jul | |

| Forecast: 50.3 | Previous: 50.5 | ||

| 04:30 | AUD | RBA Interest Rate Decision | |

| Forecast: 4.35% | Previous: 4.10% | ||

| 07:45 | EUR | Italy Manufacturing PMI Jul | |

| Forecast: 43.9 | Previous: 43.8 | ||

| 07:50 | EUR | France Manufacturing PMI Jul F | |

| Forecast: 44.5 | Previous: 44.5 | ||

| 07:55 | EUR | Germany Unemployment Change Jun | |

| Forecast: 15K | Previous: 28K | ||

| 07:55 | EUR | Germany Unemployment Rate Jun | |

| Forecast: 5.70% | Previous: 5.70% | ||

| 07:55 | EUR | Germany Manufacturing PMI Jul F | |

| Forecast: 38.8 | Previous: 38.8 | ||

| 08:00 | EUR | Italy Unemployment Rate Jun | |

| Forecast: 7.70% | Previous: 7.60% | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Jul F | |

| Forecast: 42.7 | Previous: 42.7 | ||

| 08:30 | GBP | Manufacturing PMI Jul F | |

| Forecast: 45 | Previous: 45 | ||

| 09:00 | EUR | Eurozone Unemployment Rate Jun | |

| Forecast: 6.50% | Previous: 6.50% | ||

| 13:30 | CAD | Manufacturing PMI Jul | |

| Forecast: 48.9 | Previous: 48.8 | ||

| 13:45 | USD | Manufacturing PMI Jul F | |

| Forecast: 49.0 | Previous: 49.0 | ||

| 14:00 | USD | ISM Manufacturing PMI Jul | |

| Forecast: 46.5 | Previous: 46 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Jul | |

| Forecast: 42.3 | Previous: 48.1 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Jul | |

| Forecast: | Previous: 41.8 | ||

| 14:00 | USD | Construction Spending M/M Jun | |

| Forecast: 0.60% | Previous: 0.90% | ||

| 22:45 | NZD | Employment Change Q2 | |

| Forecast: 0.60% | Previous: 0.80% | ||

| 22:45 | NZD | Unemployment Rate Q2 | |

| Forecast: 3.50% | Previous: 3.40% | ||

| 23:50 | JPY | Monetary Base Y/Y Jul | |

| Forecast: -0.70% | Previous: -1.00% | ||

| 23:50 | JPY | BoJ Minutes | |

| Forecast: | Previous: | ||

Wednesday, Aug 2, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 07:00 | CHF | SECO Consumer Climate Q3 | -25 | -30 |

| 07:30 | CHF | Manufacturing PMI Jul | 44.2 | 44.9 |

| 12:15 | USD | ADP Employment Change Jul | 195K | 497K |

| 14:30 | USD | Crude Oil Inventories | -0.6M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 07:00 | CHF | SECO Consumer Climate Q3 | |

| Forecast: -25 | Previous: -30 | ||

| 07:30 | CHF | Manufacturing PMI Jul | |

| Forecast: 44.2 | Previous: 44.9 | ||

| 12:15 | USD | ADP Employment Change Jul | |

| Forecast: 195K | Previous: 497K | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -0.6M | ||

Thursday, Aug 3, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) Jun | 10.50B | 11.79B |

| 01:45 | CNY | Caixin Services PMI Jul | 52.5 | 53.9 |

| 06:00 | EUR | Germany Trade Balance (EUR) Jun | 15.5B | 14.4B |

| 06:30 | CHF | CPI M/M Jul | -0.10% | 0.10% |

| 06:30 | CHF | CPI Y/Y Jul | 1.50% | 1.70% |

| 07:45 | EUR | Italy Services PMI Jul | 52.3 | 52.2 |

| 07:50 | EUR | France Services PMI Jul F | 47.4 | 47.4 |

| 07:55 | EUR | Germany Services PMI Jul F | 52 | 52 |

| 08:00 | EUR | Italy Retail Sales M/M Jun | 0.00% | 0.70% |

| 08:00 | EUR | Eurozone Services PMI Jul F | 51.1 | 51.1 |

| 08:30 | GBP | Services PMI Jul F | 51.5 | 51.5 |

| 09:00 | EUR | Eurozone PPI M/M Jun | -0.20% | -1.90% |

| 09:00 | EUR | Eurozone PPI Y/Y Jun | -1.50% | |

| 11:00 | GBP | BoE Interest Rate Decision | 5.25% | 5.00% |

| 11:00 | GBP | MPC Official Bank Rate Votes | 7--0--2 | 7--0--2 |

| 11:30 | USD | Challenger Job Cuts Y/Y Jul | 25.20% | |

| 12:30 | USD | Initial Jobless Claims (Jul 28) | 223K | 221K |

| 12:30 | USD | Nonfarm Productivity Q2 P | 1.10% | -2.10% |

| 12:30 | USD | Unit Labor Costs Q2 P | 2.70% | 4.20% |

| 13:45 | USD | Services PMI Jul F | 52.4 | 52.4 |

| 14:00 | USD | ISM Services PMI Jul | 53 | 53.9 |

| 14:00 | USD | Factory Orders M/M Jun | 0.20% | 0.30% |

| 14:30 | USD | Natural Gas Storage | 16B |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) Jun | |

| Forecast: 10.50B | Previous: 11.79B | ||

| 01:45 | CNY | Caixin Services PMI Jul | |

| Forecast: 52.5 | Previous: 53.9 | ||

| 06:00 | EUR | Germany Trade Balance (EUR) Jun | |

| Forecast: 15.5B | Previous: 14.4B | ||

| 06:30 | CHF | CPI M/M Jul | |

| Forecast: -0.10% | Previous: 0.10% | ||

| 06:30 | CHF | CPI Y/Y Jul | |

| Forecast: 1.50% | Previous: 1.70% | ||

| 07:45 | EUR | Italy Services PMI Jul | |

| Forecast: 52.3 | Previous: 52.2 | ||

| 07:50 | EUR | France Services PMI Jul F | |

| Forecast: 47.4 | Previous: 47.4 | ||

| 07:55 | EUR | Germany Services PMI Jul F | |

| Forecast: 52 | Previous: 52 | ||

| 08:00 | EUR | Italy Retail Sales M/M Jun | |

| Forecast: 0.00% | Previous: 0.70% | ||

| 08:00 | EUR | Eurozone Services PMI Jul F | |

| Forecast: 51.1 | Previous: 51.1 | ||

| 08:30 | GBP | Services PMI Jul F | |

| Forecast: 51.5 | Previous: 51.5 | ||

| 09:00 | EUR | Eurozone PPI M/M Jun | |

| Forecast: -0.20% | Previous: -1.90% | ||

| 09:00 | EUR | Eurozone PPI Y/Y Jun | |

| Forecast: | Previous: -1.50% | ||

| 11:00 | GBP | BoE Interest Rate Decision | |

| Forecast: 5.25% | Previous: 5.00% | ||

| 11:00 | GBP | MPC Official Bank Rate Votes | |

| Forecast: 7--0--2 | Previous: 7--0--2 | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Jul | |

| Forecast: | Previous: 25.20% | ||

| 12:30 | USD | Initial Jobless Claims (Jul 28) | |

| Forecast: 223K | Previous: 221K | ||

| 12:30 | USD | Nonfarm Productivity Q2 P | |

| Forecast: 1.10% | Previous: -2.10% | ||

| 12:30 | USD | Unit Labor Costs Q2 P | |

| Forecast: 2.70% | Previous: 4.20% | ||

| 13:45 | USD | Services PMI Jul F | |

| Forecast: 52.4 | Previous: 52.4 | ||

| 14:00 | USD | ISM Services PMI Jul | |

| Forecast: 53 | Previous: 53.9 | ||

| 14:00 | USD | Factory Orders M/M Jun | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 16B | ||

Friday, Aug 4, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | RBA Monetary Policy Statement | ||

| 06:00 | EUR | Germany Factory Orders M/M Jun | -2.00% | 6.40% |

| 06:45 | EUR | France Industrial Output M/M Jun | -0.30% | 1.20% |

| 08:00 | EUR | Italy Industrial Output M/M Jun | 0.00% | 1.60% |

| 08:30 | GBP | Construction PMI Jul | 48.2 | 48.9 |

| 09:00 | EUR | Eurozone Retail Sales M/M Jun | 0.30% | 0.00% |

| 12:30 | USD | Nonfarm Payrolls Jul | 200K | 209K |

| 12:30 | USD | Unemployment Rate Jul | 3.60% | 3.60% |

| 12:30 | USD | Average Hourly Earnings M/M Jul | 0.30% | 0.40% |

| 12:30 | CAD | Net Change in Employment Jul | 15.5K | 59.9K |

| 12:30 | CAD | Unemployment Rate Jul | 5.50% | 5.40% |

| 14:00 | CAD | Ivey PMI Jul | 50.2 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | RBA Monetary Policy Statement | |

| Forecast: | Previous: | ||

| 06:00 | EUR | Germany Factory Orders M/M Jun | |

| Forecast: -2.00% | Previous: 6.40% | ||

| 06:45 | EUR | France Industrial Output M/M Jun | |

| Forecast: -0.30% | Previous: 1.20% | ||

| 08:00 | EUR | Italy Industrial Output M/M Jun | |

| Forecast: 0.00% | Previous: 1.60% | ||

| 08:30 | GBP | Construction PMI Jul | |

| Forecast: 48.2 | Previous: 48.9 | ||

| 09:00 | EUR | Eurozone Retail Sales M/M Jun | |

| Forecast: 0.30% | Previous: 0.00% | ||

| 12:30 | USD | Nonfarm Payrolls Jul | |

| Forecast: 200K | Previous: 209K | ||

| 12:30 | USD | Unemployment Rate Jul | |

| Forecast: 3.60% | Previous: 3.60% | ||

| 12:30 | USD | Average Hourly Earnings M/M Jul | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 12:30 | CAD | Net Change in Employment Jul | |

| Forecast: 15.5K | Previous: 59.9K | ||

| 12:30 | CAD | Unemployment Rate Jul | |

| Forecast: 5.50% | Previous: 5.40% | ||

| 14:00 | CAD | Ivey PMI Jul | |

| Forecast: | Previous: 50.2 | ||