Sample Category Title

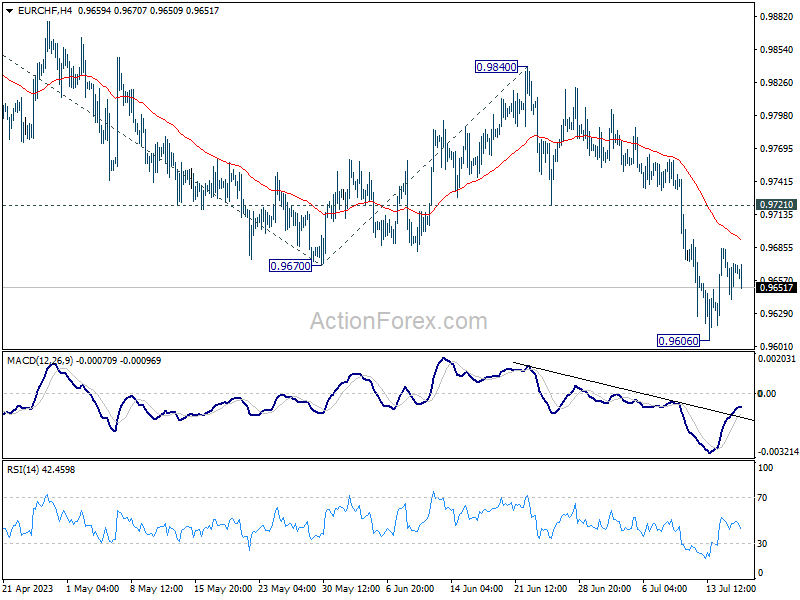

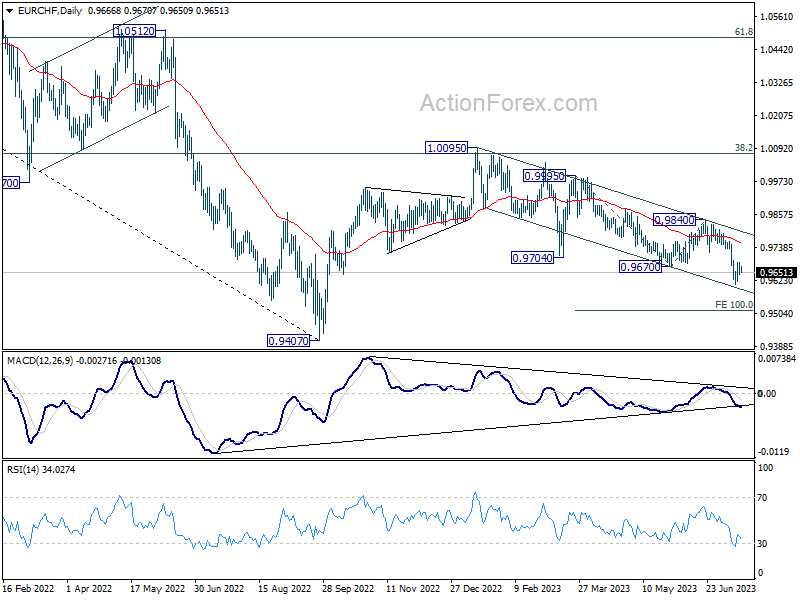

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9644; (P) 0.9667; (R1) 0.9690; More...

EUR/CHF is staying in consolidation above 0.9606 and intraday bias remains neutral. Also, outlook remains bearish with 0.9721 support turned resistance intact. On the downside, break of 0.9606 will resume larger decline from 1.0095 to 100% projection of 0.9995 to 0.9670 from 0.9840 at 0.9515.

In the bigger picture, medium term outlook is staying bearish as the pair is capped below falling 55 W EMA (now at 0.9913). Down trend form 1.2004 (2018 high) is in favor to extend through 0.9407 at a later stage. Nevertheless, decisive break of 38.2% retracement of 1.1149 to 0.9407 will raise the chance of bullish trend reversal.

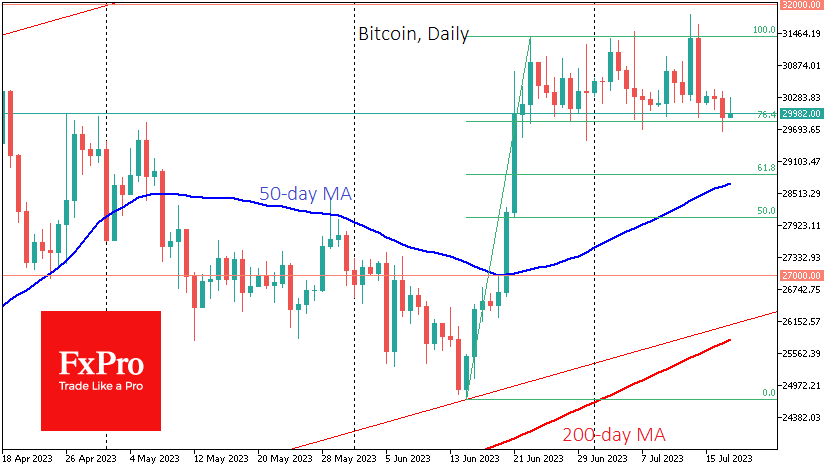

Bitcoin Risks Falling Out of Range

Market picture

Crypto market capitalisation fell 0.8% overnight to $1.20 trillion. Bitcoin loses 0.9%, Ethereum – 1.7%, while top altcoins performance varies from -5.8% (Solana) to -0.3% (BNB).

In contrast to the positive performance of stock indices, which updated multi-month highs, the first cryptocurrency rolled back below 30k on Monday. Early attempts to raise the price have been unsuccessful, leaving Bitcoin near the lower end of its four-week trading range. A failure of current support at $29.8K opens the door to a deeper correction at $28.6-28.8K, the 50-day moving average and 61.8% of the rally from the late June lows.

CoinShares said crypto fund investments rose by $137 million last week, the fourth consecutive week of inflows. Bitcoin investments increased by $140 million, while Ethereum investments fell by $2 million. Investments in funds that allow shorting of bitcoin decreased by $3 million.

Fund inflows over the past four weeks totalled $742 million, the largest inflow since the last quarter of 2021. Trading volume rose to $2.3 billion for the week, well above the annual average of $1.4 billion, CoinShares noted.

News background

Former Securities and Exchange Commission (SEC) official John Reed Stark said it was too early to celebrate Ripple’s victory in its legal battle with the US regulator.

He said the court’s decision was based on “shaky ground” and that SEC officials would successfully appeal.

Australian banking group National Australia Bank (NAB) has banned customers from making payments to cryptocurrency exchanges and platforms, describing the transactions as high-risk.

Binance, the largest exchange, has integrated Lightning Network’s Layer 2 Bitcoin network solution to reduce fees and increase the speed of initial cryptocurrency transactions. The Lightning Network integration could be an important step towards mass adoption of BTC.

The G20 Financial Stability Board (FSB) has recommended a global cryptocurrency regulatory framework. The FSB called for stricter rules to protect the assets of cryptocurrency customers. Large firms will be required to separate some of their activities and functions.

Gold May Break Higher

USD/CHF struggles for bids

The US dollar tries to stabilise after the market saw a low probability of further interest rate increases after July. The sell-off seems to be slowing down after the RSI repeatedly showed a deeply oversold greenback. An oversold RSI on the daily chart is another sign of exhaustion and could cause a snapback if sellers start to take some chips off the table. Trend followers are likely to be waiting to sell into strength and 0.8700 would be the first area to probe for resistance. 0.8550 is the closest level to see if the bleeding would stop.

EUR/GBP tests key resistance

The pound pulls lower as traders reposition ahead of the UK’s CPI on Wednesday. After a bit of hesitation below the previous swing high of 0.8580, a convincing bullish breakout indicates a strong enough pressure as the euro strives to cement its base above 0.8500 and to bottom out. The support-turned-resistance of 0.8600 is a key hurdle and its breach would help the bulls take over the short-term direction, exposing the recent top of 0.8655. 0.8570 at the start of the latest breakout is the first support in case of a retracement.

XAU/USD finds support

Gold consolidates gains as a lack of catalyst helps the post-CPI rally catch its breath. A bounce above the supply zone of 1937 and the 30-day SMA has prompted sellers to cover, easing the downward pressure. The direction is still skewed to the upside from the daily chart’s perspective and the current rebound could attract the bulls’ attention. 1966 is the next obstacle to clear, then June’s high of 1982 would be the bears’ last stronghold. On the downside, 1933 is a fresh support to maintain the current momentum.

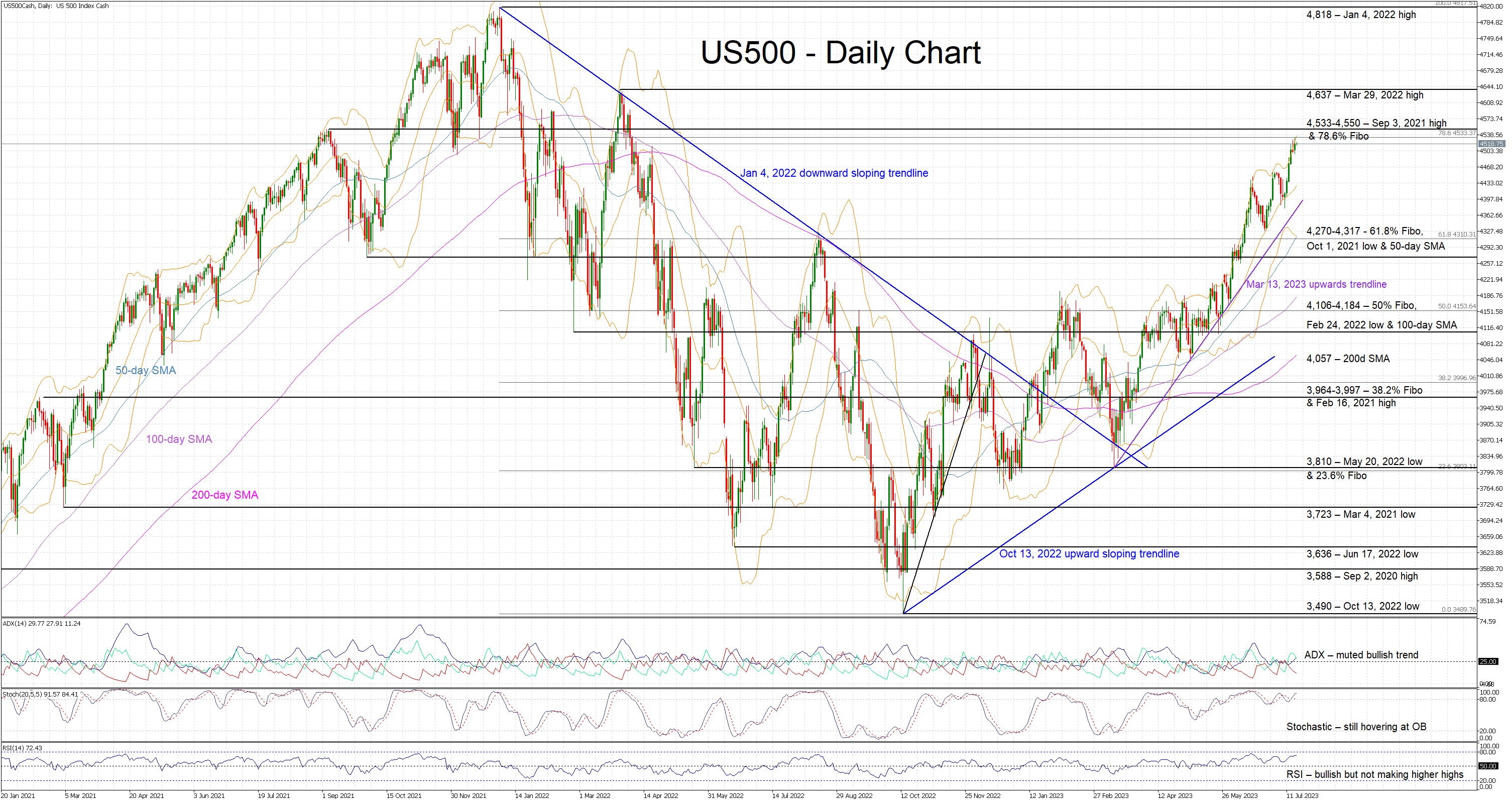

US 500 Cash Index Rally Continues; Correction Long Overdue

The US 500 cash index continues its advance, and it is currently trading at the highest level since April 6, 2022. The move since the March 13, 2023 low has been exponential with the lack of significant corrections being very visible at this stage. The index is currently hovering below the busy 4,533-4,550 area, as the bulls appear keen to record another 2023 high.

In the meantime, while the momentum indicators are clearly on the bulls’ camp, there are some early signs of rally exhaustion manifesting. More specifically, both the RSI and the stochastic oscillator continue to support the current upleg. However, both these indicators are unable to register higher highs and thus opening the door to the much-expected correction. Crucially, the Average Directional Movement Index (ADX) seems unimpressed by the current US 500 index upleg as it trades just a tad above the 25-level threshold.

Should the move higher have legs, the initial target would probably be the 4,533-4,550 area that is defined by the 78.6% Fibonacci retracement level of the January 4, 2022 – October 12, 2022 downtrend and the September 3, 2021 high. Higher, the March 29, 2022 high is unlikely to trouble the bulls’ much as they set their eyes at the all-time high of 4,818.

On the flip side, the bears are anxiously trying to stage a small pullback. They would be keen on a move towards the March 13, 2023 upward sloping trendline and the 4,270-4,317 range respectively. The latter is populated by the 61.8% Fibonacci retracement, the October 1, 2021 low and the 50-day simple moving average (SMA). If successful, the bears could have a go at the 4,106-4,184 range, a key level from a sentiment-perspective.

To conclude, with the US 500 cash index rally continuing unabated, the bears are trying to muster up the courage and sufficient evidence from the momentum indicators to finally stage a decent correction.

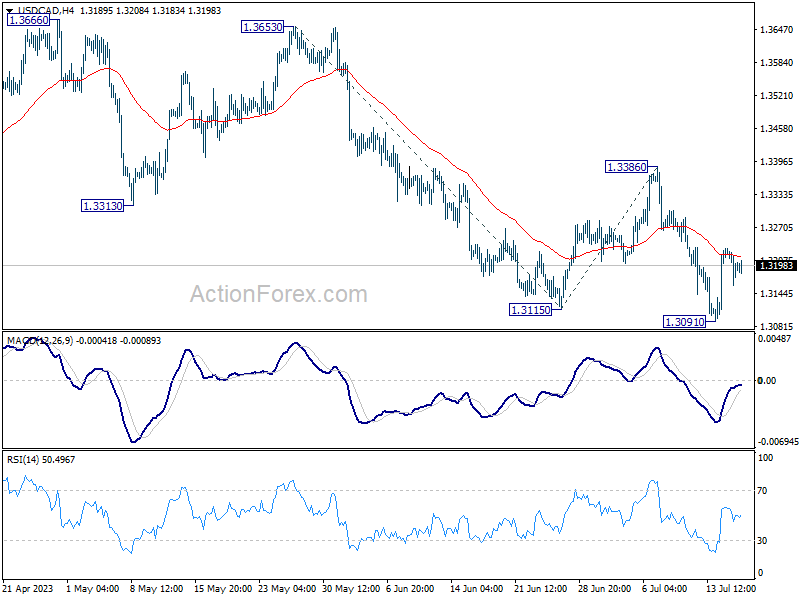

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3163; (P) 1.3198; (R1) 1.3234; More....

No change in USD/CAD's outlook as intraday bias remains neutral. Outlook will remain bearish as long as 1.3386 resistance holds. Break of 1.3091 will resume larger decline to 61.8% projection of 1.3653 to 1.3115 from 1.3386 at 1.3054. However, firm break of 1.3386 will indicate near term reversal and turn outlook bullish.

In the bigger picture, price actions from 1.3976 are viewed as a correction to up trend from 1.2005 (2021 low) only. But even so, deeper decline is expected as long as 1.3386 resistance holds. Further fall could be seen to 61.8% retracement of 1.2005 to 1.3976 at 1.2758. Meanwhile, break of 1.3386 will be a sign that the correction has completed and bring stronger rally back to retest 1.3976.

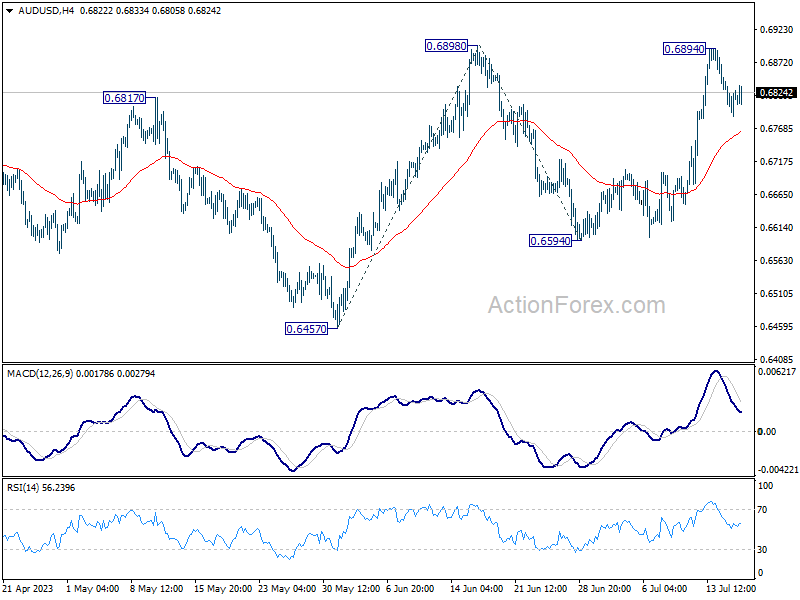

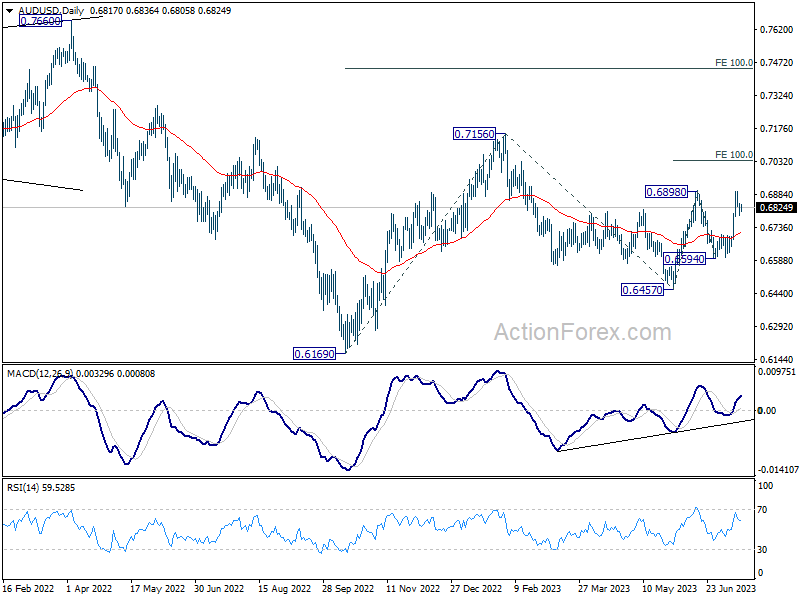

AUD/USD Daily Report

Daily Pivots: (S1) 0.6787; (P) 0.6817; (R1) 0.6846; More...

Intraday bias in AUD/USD stays neutral at this point. On the upside, decisive break of 0.6898 resistance will firstly confirm resumption of rise from 0.6457. Secondly, that should also confirm completion of the fall from 0.7156 at 0.6457. Next target will be 100% projection of 0.6457 to 0.6898 from 0.6594 at 0.7035, and then 0.7156 resistance.

In the bigger picture, price actions from 0.7156 are seen as a correction to the rebound from 0.6169 (2022 low). Break of 0.6898 resistance will argue that rise from 0.6169 is ready to resume through 0.7156. Next target will be 100% projection of 0.6169 to 0.7156 from 0.6457 at 0.7444. For now, this will be the favored case as long as 55 D EMA (now at 0.6703) holds.

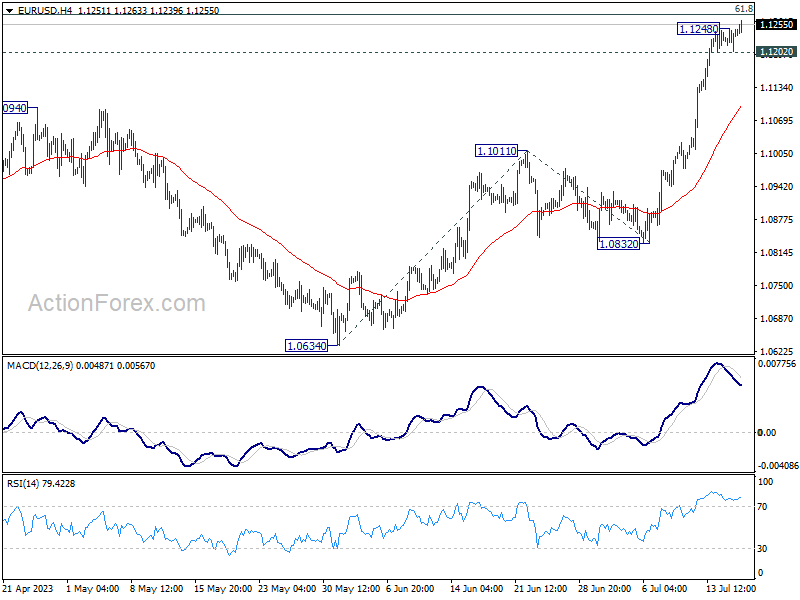

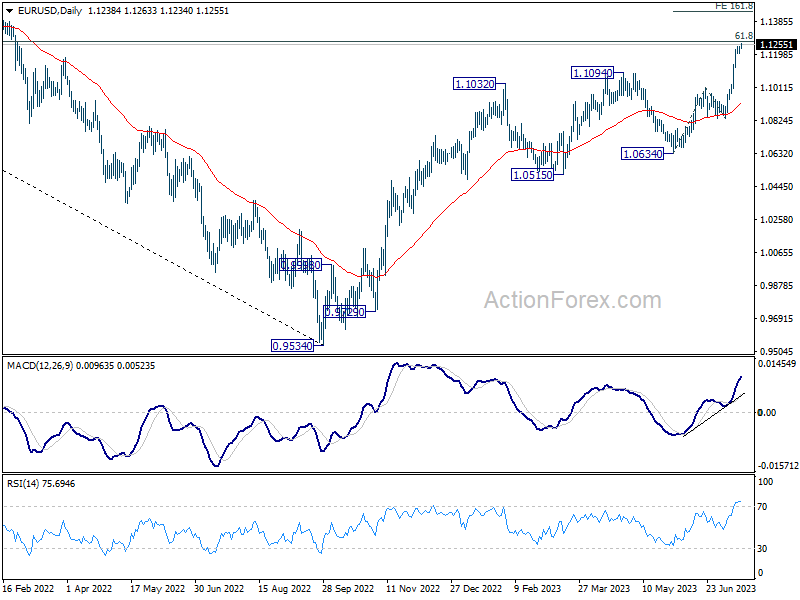

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1211; (P) 1.1230; (R1) 1.1257; More...

EUR/USD's rally is resuming by breaking 1.1248 minor resistance. However, upside could be limited by 1.1273 fibonacci level on first attempt, on loss of momentum. On the downside, break of 1.1202 minor support will turn bias back to the downside for deeper pull back. Nevertheless, sustained break of 1.1273 will extend larger up trend to 161.8% projection of 1.0634 to 1.1011 from 1.0832 at 1.1442 next.

In the bigger picture, as rise from 0.9534 extends, focus is now on 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next. Meanwhile, outlook will continue to stay bullish as long as 1.0832 support holds, even in case of deep pull back.

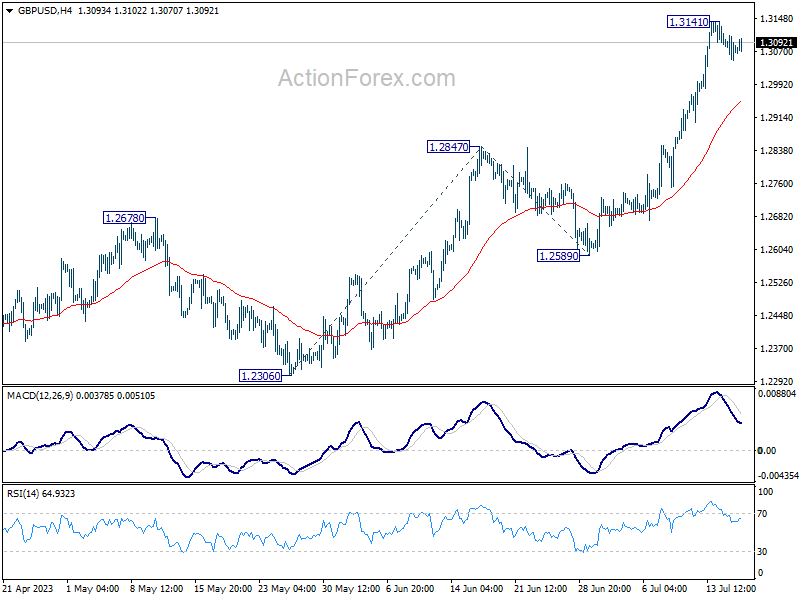

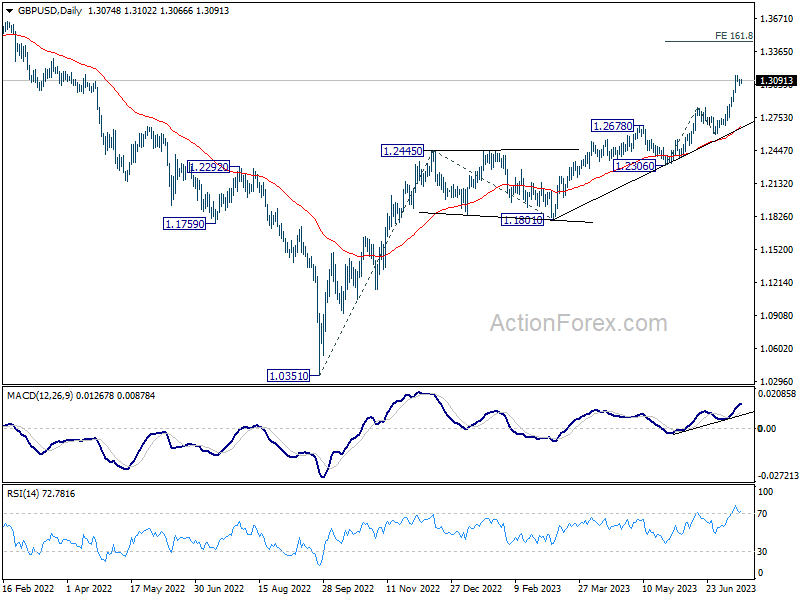

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3075; (P) 1.3108; (R1) 1.3127; More...

Intraday bias in GBP/USD remains neutral as consolidation from 1.3141 is extending. Downside of retreat should be contained above 1.2847 resistance turned support to bring rise resumption. On the upside, break of 1.3141 will resume larger up trend and target 161.8% projection of 1.2306 to 1.2847 from 1.2589 at 1.3464 next.

In the bigger picture, rise from 1.0351 medium term bottom (2022 low) is in progress. Next target is 100% projection of 1.0351 to 1.2445 from 1.1801 at 1.3895. Break there will target 1.4248 key long term resistance (2021 high) next. This will now remain the favored case as long as 1.2678 resistance turned support holds.

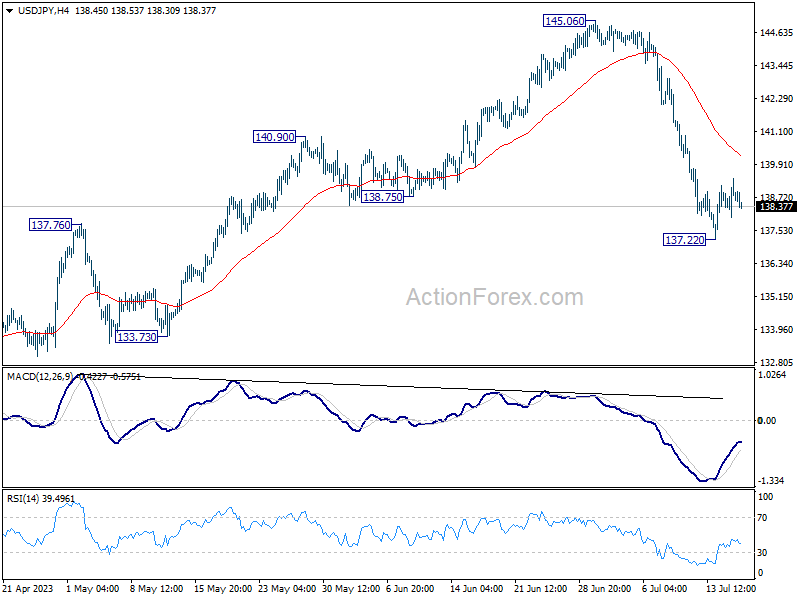

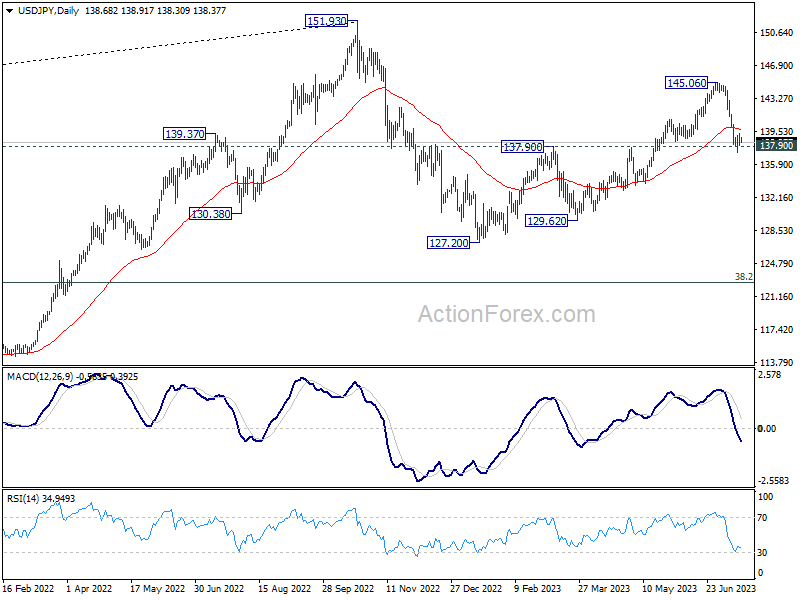

USD/JPY Daily Outlook

Daily Pivots: (S1) 138.01; (P) 138.71; (R1) 139.41; More...

Intraday bias in USD/JPY remains neutral as consolidation from 137.22 is extending. Upside of recovery should be limited by 55 4H EMA (now at 140.18) and bring another decline. Break of 137.22 and sustained trading below 137.90 resistance turned support will confirm the larger bearish case, and target 127.20 and below.

In the bigger picture, fall from 145.06 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Sustained break of 137.90 resistance turned support should confirm this case and target 127.20 (2023 low) and below. For now, this will remain the favored case as long as 145.06 resistance holds, even in case of strong rebound.

Better to Wait the Outcome of Next Week’s ECB/Fed Policy Meetings

Markets

Yesterday had little to offer from an economic point of view and that showed in daily trading. Main FI and FX markets traded sideways from the start. US stock markets (up to +0.93% for Nasdaq) parted ways with key European indices (up to -1% lower). Technical elements played in Europe after failure last week to pierce key resistance (4400) in the EuroStoxx 50. ECB members are about to join their US colleagues in the pre-meeting blackout period, but that didn’t hold some back for some last-minute comments. ECB Nagel – German, hawk by nature - stated the obvious by calling the July hike and stuck with the main message that data will decide on the outcome of the September meeting. His personal connotations – “core inflation is very sticky”, “don’t currently see a risk of overtightening” and “too early to declare victory over inflation” – barely conceal his preference though. Bank of Italy governor Visco – Italian, dove by nature - is more hopeful and believes that inflation may drop more quickly than forecast. He assumes that the drop in energy prices will more quickly show in core prices as well. Therefore, he’s wary about doing too much from a monetary policy point of view. ECB Villeroy is still scheduled to speak today and later this week, but on both occasions the topic is non-monetary policy related. The ECB’s Q2 Bank Lending Survey (July 25) is the final piece of key input ahead of the July 27 policy meeting.

Today’s eco calendar contains US retail sales. Consensus expects a 0.5% M/M headline gain and a 0.3% M/M increase for the retail control group (used as proxy for consumption calculations in GDP). We don’t expect retail sales to have a big market impact following final pre-Summer lull 2-way positioning at the start of the month. Traded volumes are shrinking fast and risk-reward it’s better to wait the outcome of next week’s ECB/Fed policy meetings. In this scenario, EUR/USD 1.1274 resistance (62% retracement on 2021-2022 USD rise) should theoretically hold, but risks if any are clearly for a sooner break higher. EUR/GBP moves further away from the low 0.85 support area (currently 0.86) awaiting tomorrow’s inflation numbers which should seal the (discounted) 50 bps BoE rate hike in August. On a very first small positive note, a Lloyds survey showed that UK food and drink manufacturers cut prices in June for the first time in more than 3 years.

News and views

The NY Fed’s SCE credit access survey showed that the overall rejection rate for credit applicants increased to 21.8% the highest level since June 2018. The increase was broad-based across all age groups. The rejection rate for auto loans increased to 14.2% from 9.1% in February, a new series high. It also increased for credit cards, credit card limit increase requests, mortgages, and mortgage refinance applications. The average reported expectation of applicants that a loan application will be rejected increased sharply for all loan types. It rose to 30.7% for auto loans (series high), 32.8% for credit cards, 42.4% for credit limit increase requests (series high), 46.1% for mortgages (series high), and 29.6% for mortgage refinance applications.

Minutes of the Reserve Bank of Australia’s (RBA) July policy meeting indicated that the MPC discussed both the option to raise the policy rate further by 25 bps or holding the cash rate unchanged at 4.10%. The case to increase the cash rate further was centered on observations that inflation was forecast to remain above target for an extended period and the risk that this timeframe would be extended without further monetary policy tightening. The labour market remains very tight, notwithstanding some easing in conditions recently. Supporting the case for leaving the policy rate unchanged, members noted that monetary policy had been tightened considerably and rapidly over the prior year and that the stance of monetary policy was clearly restrictive. Mortgage interest payments (as a share of household disposable income) were around a record high and will rise further. The MPC saw considerable uncertainty about the resilience of household consumption. The MPC also pondered the risk that the unemployment rate would rise beyond the rate required to ensure inflation returns to target in a reasonable timeframe. The MPC concluded to leave the policy rate unchanged an reassess the situation at the August meeting. Some further tightening may be required but this depends on how the economy and inflation evolve.