Sample Category Title

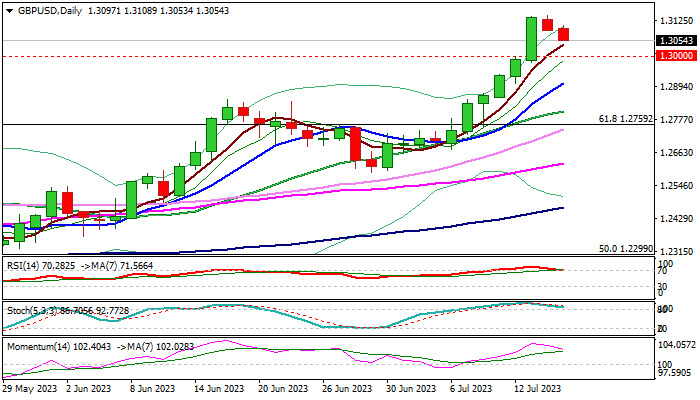

GBP/USD: Cable Eases from New 2023 Top, UK CPI Data Eyed for Fresh Signals

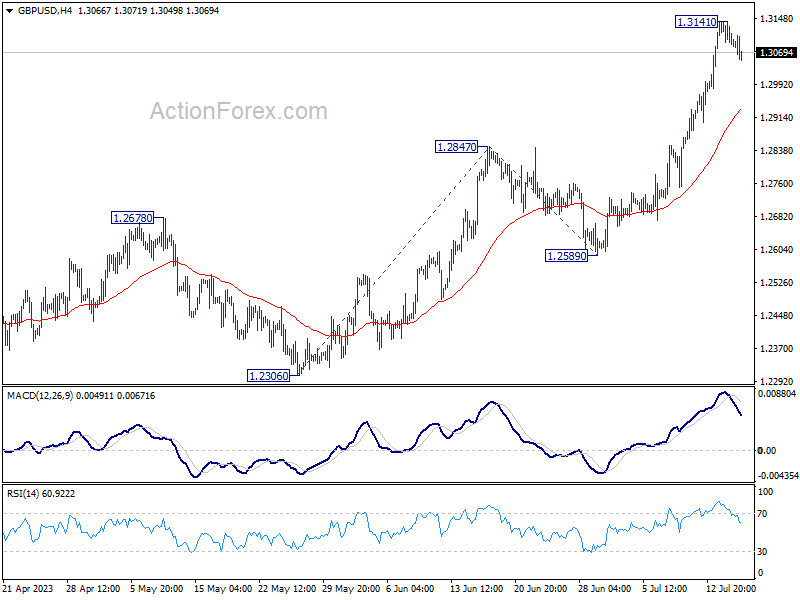

Pullback from new 2023 high (1.3141), where last week’s strong bullish acceleration was repeatedly rejected, extends into the second straight day.

Strongly overbought RSI /stochastic and fading bullish momentum on daily chart, contributed to decision to collect some profits.

Fresh bears face initial support at 1.30 (psychological), ahead of rising 10DMA (1.2906) and former top at 1.2848 (June 16), which should contain extended dips and keep larger bulls in play.

Markets shift focus on UK inflation report (due on Wednesday’s morning) which may provide more clues about BoE’s decision in Aug policy meeting.

British inflation is expected to ease in June (y/y 8.2% f/c vs 8.7% in May) with softer results to ease pressure on central bank, while above-forecast figures would add to expectations for 50 basis points hike.

Res: 1.3108; 1.3141; 1.3200; 1.3298.

Sup: 1.3041; 1.3000; 1.2906; 1.2848.

Sunset Market Commentary

Markets

The new trading week started with some risk-off. Growth concerns took the upper hand following Chinese Q2 GDP numbers published in early Asian dealings this morning. There were some green shoots, including the better-than-expected June industrial production figures, but markets dismissed them. European equities slip more than one percent. Technical charts supported the downleg. The EuroStoxx50 tested the strong 4400 resistance area end last week. Failing to push through instead triggered a countermove lower for a fifth time since April. Core bonds advanced, pushing yields in the euro area and US several bps lower before paring declines after a stronger-than-expected NY Fed Empire index. The headline figure eased from 6.6 to 1.1, pointing at marginally increasing factory activity. This compares to the -3.5 consensus was expecting. Both prices paid and received eased further to the lowest level in two years but the gauges for six months ahead picked up. New orders stabilized at a low level while the employment subindex for the first time since January hit positive territory again. The business outlook six months ahead deteriorated a few points to 14.3 to remain around the highest levels since mid-2022. US yields erased all previous losses of as much as 6 bps to trade flat for the day. German rates join the US trading pattern and drop 0.8-2 bps with the wings underperforming the belly.

The currencies Down Under are today’s laggards. That should come as no surprise since the risk-off can be traced back to slowing growth in one of Australia’s and New Zealand’s most important trading partner. AUD/USD goes into it’s second day of declines to test the 0.68 big figure. NZD/USD in a parallel move goes from 0.636 to 0.633. Commodities feel the pressure as well with oil losing 1.4% to further slip sub $80 again. Soft commodities, and especially wheat, are doing much better. It follows Russia’s decision to terminate and not to extend the UN-Turkey brokered grain deal, potentially limiting world supply ahead of the harvest season (see headline below). Other currency pairs trade extremely tight ranges today. EUR/USD moves sideways around 1.123. The trade-weighted dollar stages an unconvincing attempt to recoup the 100 barrier. EUR/GPB bounces towards the 0.86 area in technical trading with sterling on edge for Wednesday’s CPI numbers.

News & Views

Russia today formally withdrew from the Black Sea grain deal brokered last year to export Ukrainian grain across the Black Sea. Since the deal, around 33 million of commodities have exported from Ukraine. Russian president Putin’s spokesman Peskov said that western sanctions should be removed to bolster trade (eg reconnecting an agricultural bank to the SWIFT international payments system) in a parallel agreement under which the UN vowed to improve access to Russian food and fertilizer exports. In November of last year, Russia already ditched the Black Sea grain deal for one day, before Turkish President Erdogan helped agreeing an extension. Putin and Erdogan meet again in August with exit deal becoming one of the key talking points. Wheat prices spike around 2% higher on the news today.

Polish monetary council member Duda said in a Business Insider Polska interview that the MPC will have arguments to carefully discuss interest rate cuts as soon as after summer holidays. Of course given that they see a fast decrease in inflation, putting it on permanent downward trend in the long term. She thinks that inflation could fall into single digit territory faster than the current NBP forecast of Q4 2023. Polish prices have not increased M/M in the last two months, providing evidence for the ongoing disinflation process. Falling energy and food prices are slowing down global price growth. Supply chains have improved. These are other elements limiting price pressure. Polish swap rate today drop up to 15 bps in the 5-10yr bucket of the curve. The Polish zloty holds firm though, changing hands near recent tops around 4.45.

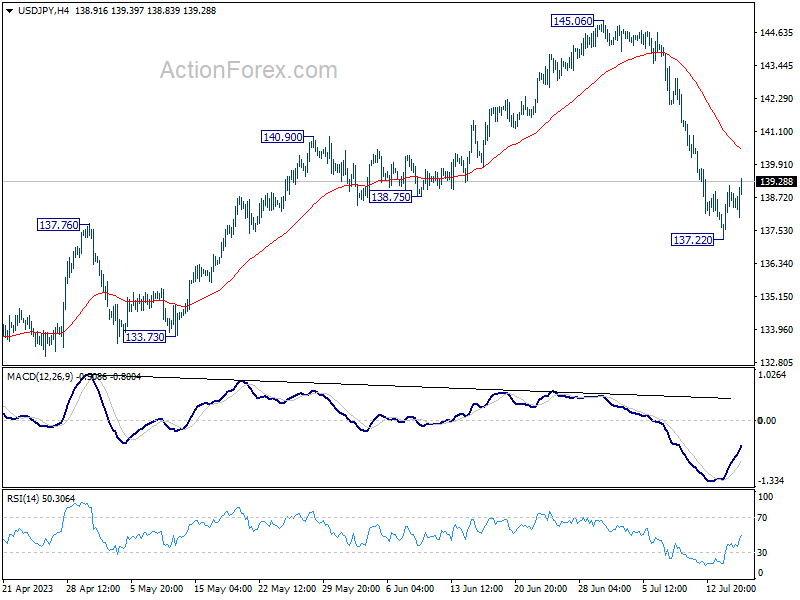

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 137.63; (P) 138.40; (R1) 139.55; More...

USD/JPY's consolidation from 137.22 is extending and intraday bias remains neutral. Upside of recovery should be limited by 55 4H EMA (now at 140.45) and bring another decline. Break of 137.22 and sustained trading below 137.90 resistance turned support will confirm the larger bearish case, and target 127.20 and below.

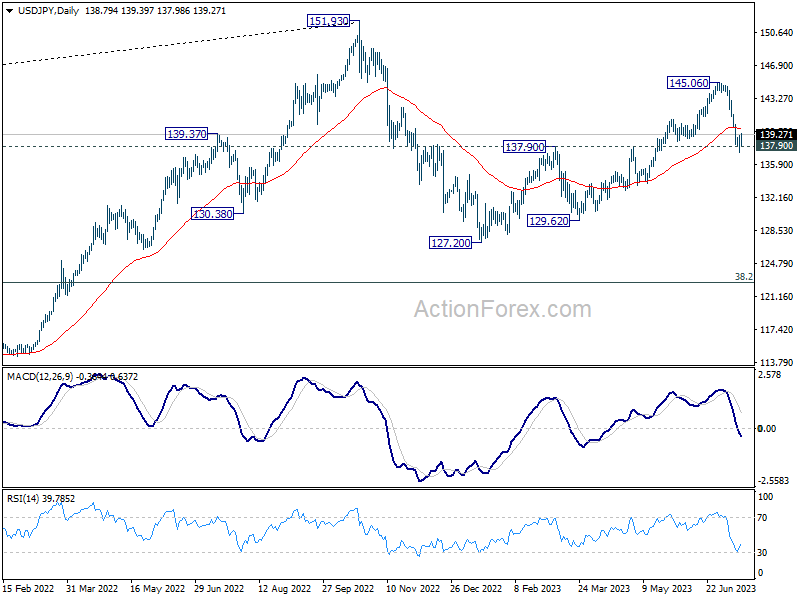

In the bigger picture, fall from 145.06 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Sustained break of 137.90 resistance turned support should confirm this case and target 127.20 (2023 low) and below. For now, this will remain the favored case as long as 145.06 resistance holds, even in case of strong rebound.

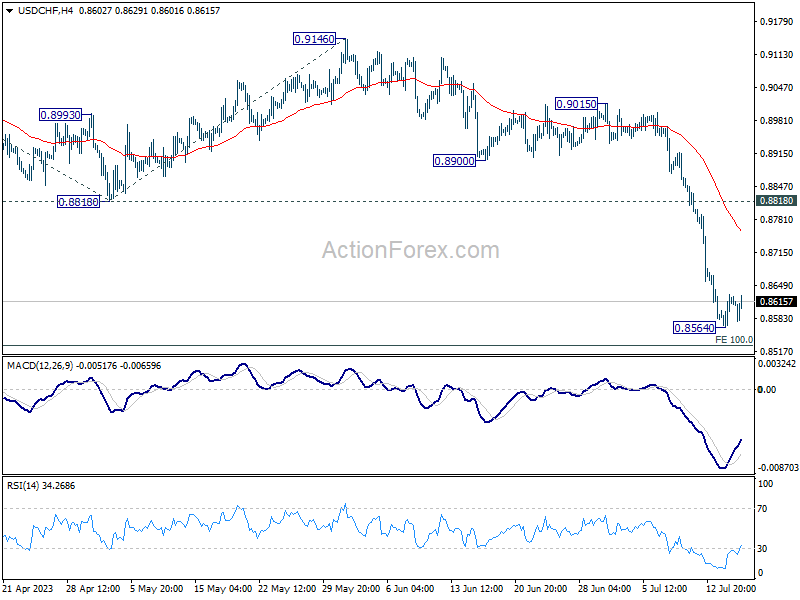

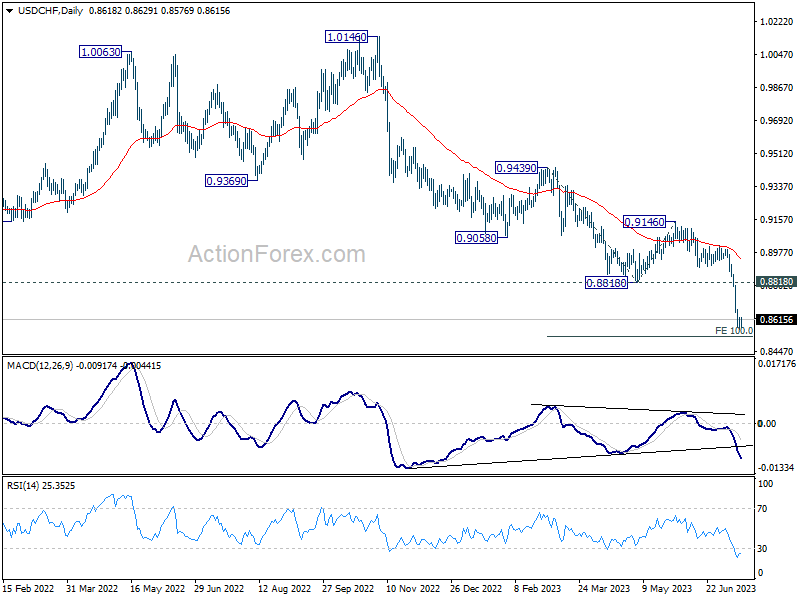

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8580; (P) 0.8606; (R1) 0.8646; More...

USD/CHF is extending the consolidation form 0.8564 and intraday bias stays neutral. Upside of recovery should be limited below 0.8818 support turned resistance to bring another fall. Break of 0.8564 will resume larger down trend and target 100% projection of 0.9439 to 0.8818 from 0.9146 at 0.8525 next.

In the bigger picture, the break of 0.8756 (2021 low) indicates break out from the long term range pattern. For now, medium term outlook will stay bearish as long as 0.9146 resistance holds. Further fall would be seen to 61.8% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.8317 next.

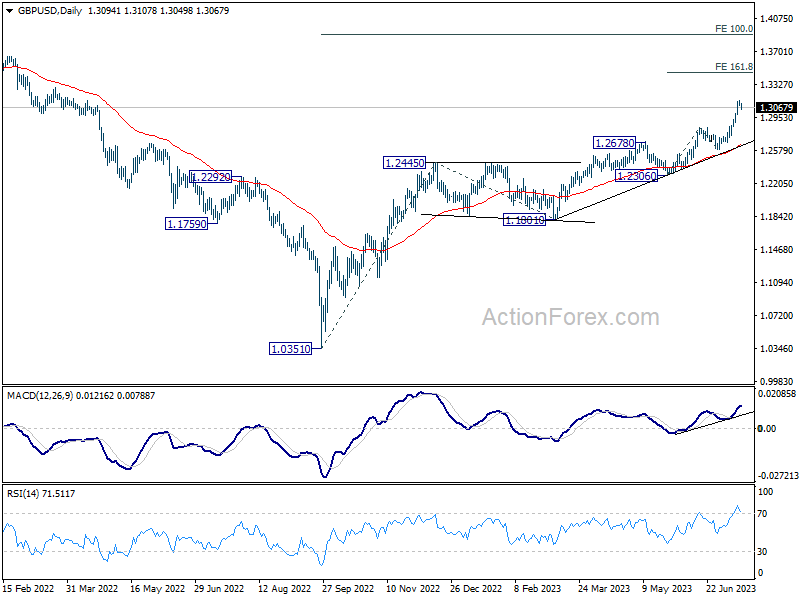

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3075; (P) 1.3108; (R1) 1.3127; More...

GBP/USD's consolidation from 1.3141 is extending and intraday bias remains neutral. Downside of retreat should be contained above 1.2847 resistance turned support to bring rise resumption. On the upside, break of 1.3141 will resume larger up trend and target 161.8% projection of 1.2306 to 1.2847 from 1.2589 at 1.3464 next.

In the bigger picture, rise from 1.0351 medium term bottom (2022 low) is in progress. Next target is 100% projection of 1.0351 to 1.2445 from 1.1801 at 1.3895. Break there will target 1.4248 key long term resistance (2021 high) next. This will now remain the favored case as long as 1.2678 resistance turned support holds.

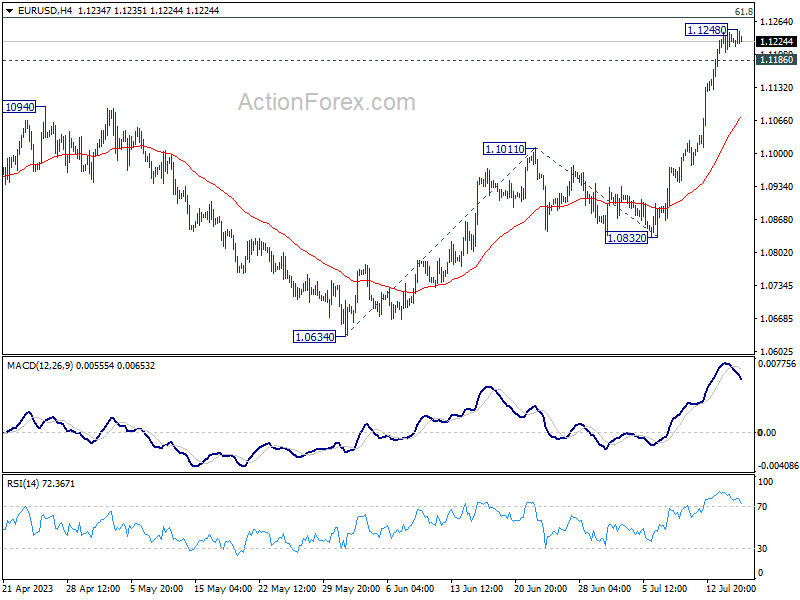

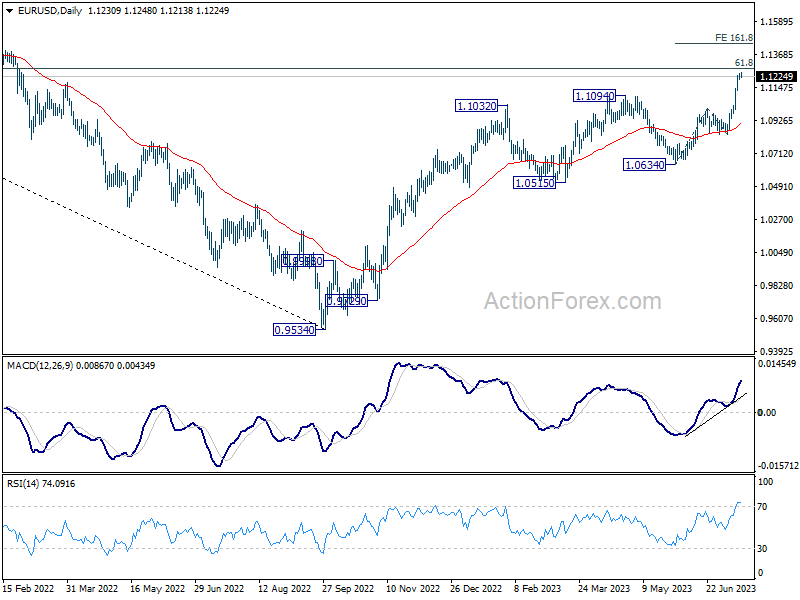

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1207; (P) 1.1226; (R1) 1.1248; More...

Intraday bias in EUR/USD is turned neutral with extended loss of upside momentum as seen in 4 H MACD. While further rise cannot be ruled out, upside should be limited by 1.1273 fibonacci level on first attempt. Break of 1.1186 minor support will bring deeper pull back first. Nevertheless, sustained break of 1.1273 will extend larger up trend to 161.8% projection of 1.0634 to 1.1011 from 1.0832 at 1.1442 next.

In the bigger picture, as rise from 0.9534 extends, focus is now on 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next. Meanwhile, outlook will continue to stay bullish as long as 1.0832 support holds, even in case of deep pull back.

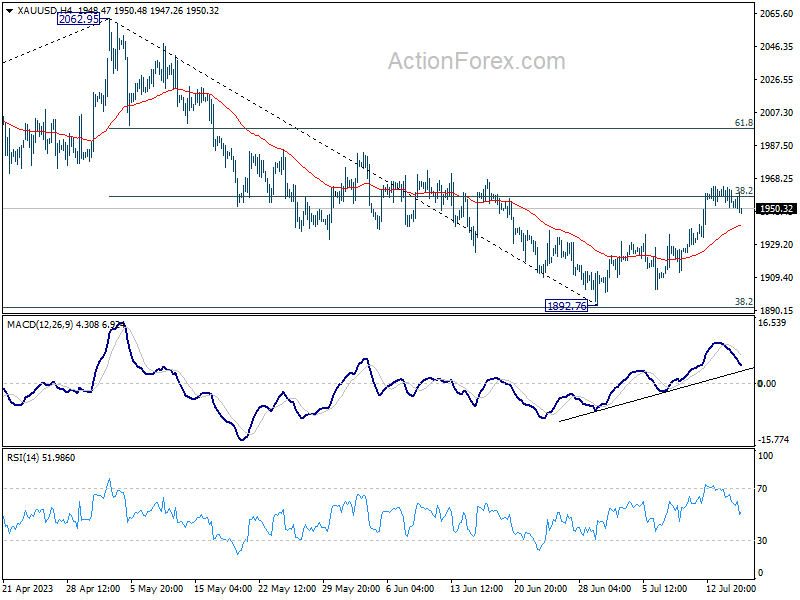

Commodities Down in Mild Risk-off Markets, Swiss Franc Firm With Dollar and Euro

With mild risk aversion permeating the markets, Gold and some other commodities are weakening notably today. China's latest economic indicators paint a dreary picture – a sluggish recovery, dampened consumer demand, record youth unemployment, and escalating deflation risk. With a key meeting of the Chinese Communist Party's Politburo around the corner, all eyes are on the potential roll-out of substantial economic stimulus. Yet, market expectations remain modest for now.

The Swiss Franc is currently outperforming in the markets, followed closely by the Dollar and Euro. Conversely, Japanese Yen is showing signs of weakness as it continues to digest recent gains. Australian and New Zealand Dollars are languishing at the bottom of the performance list, with the British Pound hot on their heels.

Technically, Gold is trying to fall away from 38.2% retracement of 2062.95 to 1892.76 at 1957.77. Next focus is 55 4H EMA (now at 1940.07). Strong support from there will keep the rebound from 1892.76 alive. Sustained break of 1957.77 will pave the way to 61.8% retracement at 1997.93. Nevertheless, firm break of the EMA will argue that the rebound has completed and bring retest of 1892.76 low.

In Europe, at the time of writing, FTSE is down -0.26%. DAX is down -0.56%. CAC is down -1.22%. Germany 10-year yield is down -0.034 at 0.480. Earlier in Asia, Japan and Hong Kong markets were closed. China Shanghai SSE dropped -0.87%. Singapore Strait Times rose 0.18%.

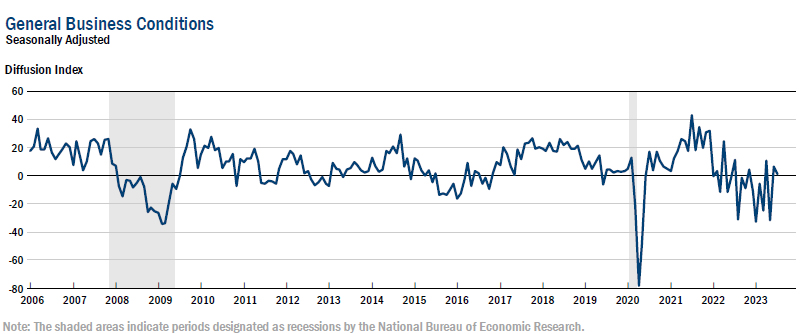

US Empire State Manufacturing fell to 1.1, waning optimism and moderating price increases

US Empire State Manufacturing Survey showed a decline in the headline general business conditions index, falling from 6.6 to a modest 1.1 in July, slightly above expectation of 0.0. While 29% of respondents reported improved conditions over the month, 27% reported a deterioration.

Price increases showed a moderating trend. Prices paid index fell -5 pts to 16.7, and prices received index also declined by -5 pts to 3.9. Over the past year, the prices paid index has seen a near-50 point drop, while the prices received index has cumulatively fallen by -27 points.

On the other hand, index for future business conditions declined from 18.9 to 14.3, signaling that although businesses are anticipating better conditions ahead, overall optimism remains relatively subdued.

Bundesbank: German inflation to cool post Sep, but core to stay high

Bundesbank, in its monthly report, anticipates a dip in Germany's inflation rate starting from September. One-off effects, such as the temporary introduction of the "tank discount" and nine-euro ticket, are expected to fade, easing the inflationary pressure.

The Bundesbank also envisions that the recent decrease in prices for primary products will progressively reflect in consumer costs, adding to the deflationary forces.

Contrarily, core inflation rat is projected to remain substantially high over the summer months. The summer season typically witnesses elevated prices for holidays packages, and this year is expected to be no different.

China's annual GDP growth missed expectations, youth unemployment hit new record

China's Q2 GDP growth rose by 6.3% yoy, an improvement from Q1's 4.5% but fell short of expectation 7.1% yoy. On a quarter-to-quarter basis, GDP grew by 0.8%, deceleration from the previous quarter's 2.2% but still outpacing projected 0.5%.

Despite being the fastest annual pace since Q2 2021, this performance appears skewed due to low base effect from last year's lockdown. For H1 as a whole, GDP expanded by 5.5% when compared to the same period last. This growth outperformed the government's modest target of approximately 5% for the year.

Other figures published by the National Bureau of Statistics on Monday painted a mixed picture. In June, retail sales increased by 3.1% yoy, falling short of the expected 3.5% and down significantly from May's 12.7% growth. On a brighter note, industrial production, reflecting activity in manufacturing, mining, and utilities sectors, surged by 4.4% yoy last month, a jump from May's 3.5% and surpassing expectations of 2.6%.

Fixed-asset investment, traditionally used to bolster growth, rose by 3.8% yoy in the first half of 2023, a slowdown from the 4% increase witnessed in the first five months. However, this growth exceeded the expected 3.4%.

In terms of employment, the picture appears bleak for the younger generation. Unemployment rate for those aged 16-24 reached a record 21.3% in June, up from 20.8% in May. Conversely, overall urban surveyed jobless rate remained static at 5.2% last month.

In a separate announcement, PBoC maintained the rate on CNY 103B worth of one-year medium-term lending facility loans to some financial institutions at 2.65%.

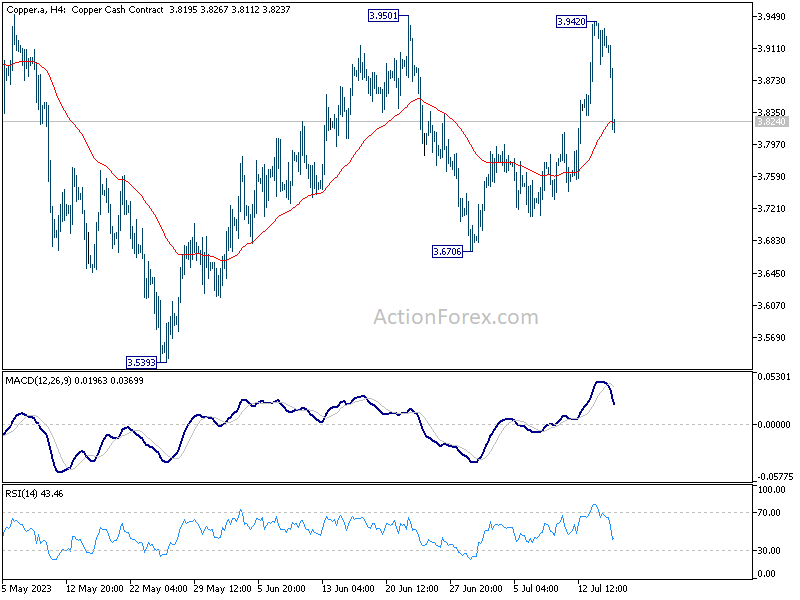

Oil and Copper slide after China concerns

The release of disappointing Chinese economic data earlier today has cast a shadow on global sentiment, instigating downturns in oil and copper prices, as well as European indices and US futures.

WTI crude oil experienced a fleeting rebound following a Reuters news alert suggesting that Saudi Arabia was extending voluntary output cut. However, the news alert was withdrawn shortly after, as it merely echoed an earlier report from June 4. Now, WTI prices are being pressured lower amid concerns over domestic demand in China and the partial restart of Libyan production that had been previously halted.

Technically, near term bias is neutral in WTI after a top was formed at 77.22, ahead of 100% projection of 63.37 to 74.74 from 66.94 at 78.1. While the stay above 55 D EMA is a near term bullish sign, i cannot be ruled out that rebound from 63.37 is merely a corrective bounce. Break of 72.57 support will argue that the rebound have completed and target 63.67 and possibly below. Nevertheless, firm break of 78.01 will add another evidence for trend reversal and target 83.46.

Copper, a commodity particularly sensitive to Chinese data, also felt the pinch. Rejection by 3.9501 resistance keep near term outlook neutral for now. While prior break of 55 D EMA is a bullish sign, upside is capped below falling trend line resistance (from 4.3556). On the upside, break of 3.9501 will resume the rebound from 3.5393 and argues that whole fall form 4.3556 has finished. However, break of 3.6706 would indicate that fall from 4.3556 is ready to resume through 3.5395.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1207; (P) 1.1226; (R1) 1.1248; More...

Intraday bias in EUR/USD is turned neutral with extended loss of upside momentum as seen in 4 H MACD. While further rise cannot be ruled out, upside should be limited by 1.1273 fibonacci level on first attempt. Break of 1.1186 minor support will bring deeper pull back first. Nevertheless, sustained break of 1.1273 will extend larger up trend to 161.8% projection of 1.0634 to 1.1011 from 1.0832 at 1.1442 next.

In the bigger picture, as rise from 0.9534 extends, focus is now on 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next. Meanwhile, outlook will continue to stay bullish as long as 1.0832 support holds, even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 02:00 | CNY | GDP Y/Y Q2 | 6.30% | 7.10% | 4.50% | |

| 02:00 | CNY | Industrial Production Y/Y Jun | 4.40% | 2.60% | 3.50% | |

| 02:00 | CNY | Retail Sales Y/Y Jun | 3.10% | 3.40% | 12.70% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Jun | 3.80% | 3.40% | 4.00% | |

| 12:30 | USD | Empire State Manufacturing Index Jul | 1.1 | 0 | 6.6 | |

| 12:30 | CAD | Wholesale Sales M/M May | 3.50% | 2.20% | -1.40% |

US Empire State Manufacturing fell to 1.1, waning optimism and moderating price increases

US Empire State Manufacturing Survey showed a decline in the headline general business conditions index, falling from 6.6 to a modest 1.1 in July, slightly above expectation of 0.0. While 29% of respondents reported improved conditions over the month, 27% reported a deterioration.

Price increases showed a moderating trend. Prices paid index fell -5 pts to 16.7, and prices received index also declined by -5 pts to 3.9. Over the past year, the prices paid index has seen a near-50 point drop, while the prices received index has cumulatively fallen by -27 points.

On the other hand, index for future business conditions declined from 18.9 to 14.3, signaling that although businesses are anticipating better conditions ahead, overall optimism remains relatively subdued.

Bundesbank: German inflation to cool post Sep, but core to stay high

Bundesbank, in its monthly report, anticipates a dip in Germany's inflation rate starting from September. One-off effects, such as the temporary introduction of the "tank discount" and nine-euro ticket, are expected to fade, easing the inflationary pressure.

The Bundesbank also envisions that the recent decrease in prices for primary products will progressively reflect in consumer costs, adding to the deflationary forces.

Contrarily, core inflation rat is projected to remain substantially high over the summer months. The summer season typically witnesses elevated prices for holidays packages, and this year is expected to be no different.

Oil and Copper slide after China concerns

The release of disappointing Chinese economic data earlier today has cast a shadow on global sentiment, instigating downturns in oil and copper prices, as well as European indices and US futures.

WTI crude oil experienced a fleeting rebound following a Reuters news alert suggesting that Saudi Arabia was extending voluntary output cut. However, the news alert was withdrawn shortly after, as it merely echoed an earlier report from June 4. Now, WTI prices are being pressured lower amid concerns over domestic demand in China and the partial restart of Libyan production that had been previously halted.

Technically, near term bias is neutral in WTI after a top was formed at 77.22, ahead of 100% projection of 63.37 to 74.74 from 66.94 at 78.1. While the stay above 55 D EMA is a near term bullish sign, i cannot be ruled out that rebound from 63.37 is merely a corrective bounce. Break of 72.57 support will argue that the rebound have completed and target 63.67 and possibly below. Nevertheless, firm break of 78.01 will add another evidence for trend reversal and target 83.46.

Copper, a commodity particularly sensitive to Chinese data, also felt the pinch. Rejection by 3.9501 resistance keep near term outlook neutral for now. While prior break of 55 D EMA is a bullish sign, upside is capped below falling trend line resistance (from 4.3556). On the upside, break of 3.9501 will resume the rebound from 3.5393 and argues that whole fall form 4.3556 has finished. However, break of 3.6706 would indicate that fall from 4.3556 is ready to resume through 3.5395.