Sample Category Title

Bundesbank Nagel: We have to be a little bit more patient

Bundesbank President and ECB Governing Council member, Joachim Nagel expects a 25 bps increase for the upcoming July meeting of ECB. As for the meeting in September, Nagel stated on Monday, "we will see what the data will tell us."

Unlike previous financial cycles, core inflation rates in developed nations are not declining as swiftly, implying a more drawn-out recovery process. Despite this, Nagel dismissed the notion of an over-tightened policy risking a hard landing for Europe as interest rates rise. "It's too early to really declare a certain kind of victory when it comes to our inflation fight," Nagel remarked.

Notably, the Bundesbank chief advised patience in the face of these challenges, acknowledging a potentially slower pace in transmission of monetary policy. "This time maybe we have to be a little bit more patient. The pace of the transmission channel is maybe not as fast as it was in the past," he added.

GBP/USD Turns Attractive On Dips, Gold Price Climbs Higher

Key Highlights

- GBP/USD is showing positive signs above the 1.3000 resistance.

- A major bullish trend line is forming with support near 1.2940 on the 4-hour chart.

- EUR/USD is extending gains above the 1.1240 level.

- Gold price was able to climb above the $1,950 resistance.

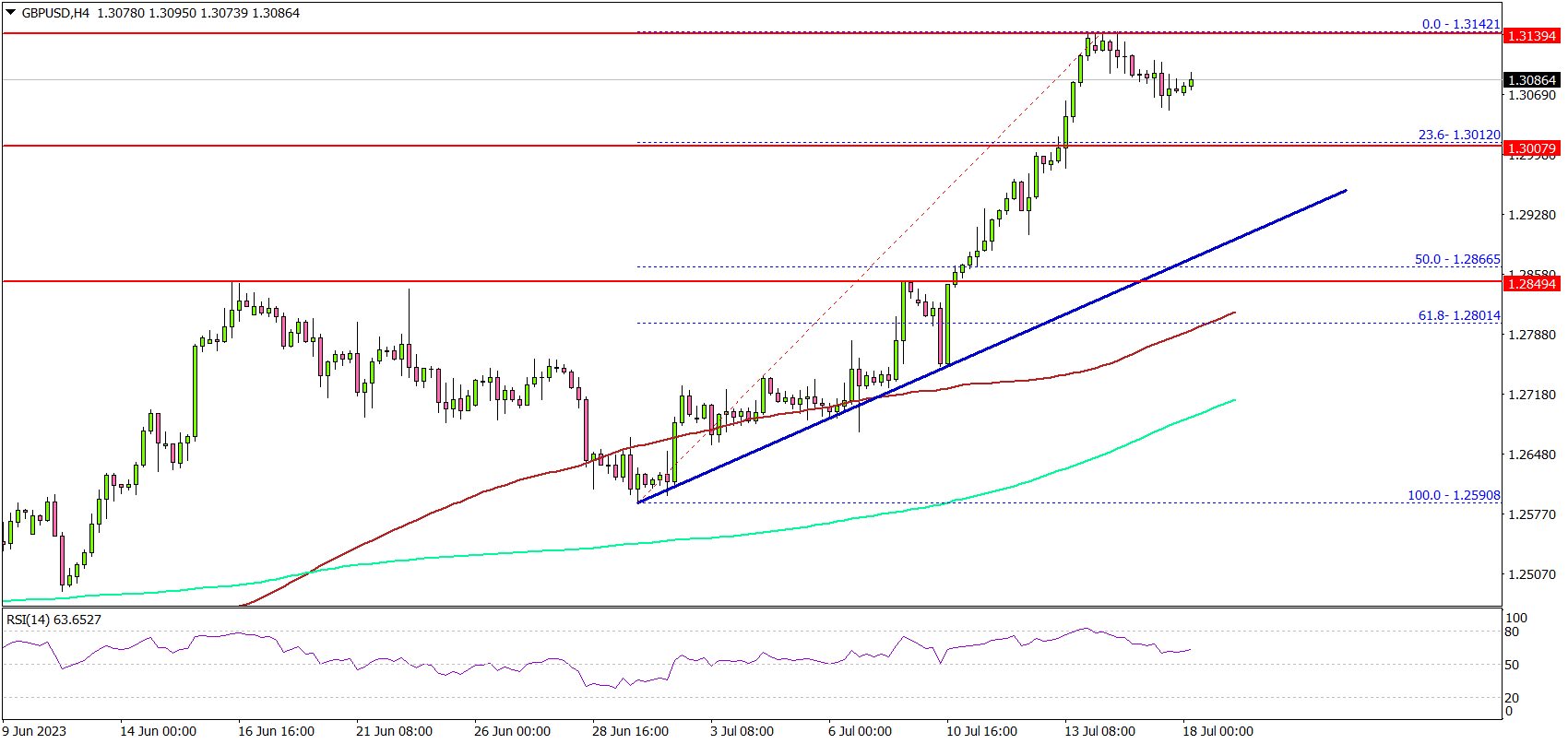

GBP/USD Technical Analysis

The British Pound started a major increase above the 1.2850 resistance against the US Dollar. GBP/USD even broke 1.3000 to move further into a bullish zone.

Looking at the 4-hour chart, the pair settled above the 1.3000 level, the 200 simple moving average (green, 4 hours), and the 100 simple moving average (red, 4 hours).

It tested the 1.3140 zone and recently started a minor downside correction. Immediate support is near the 1.3020 level. The next major support is seen near the 1.2950 and 1.2940 levels.

Besides, there is also a major bullish trend line forming with support near 1.1165 on the same chart. The next major support is at 1.2880, below which there could be a drop to 1.2800 or the 100 simple moving average (red, 4 hours).

Any more losses might send the pair toward the 1.2720 support zone. On the upside, immediate resistance is near the 1.3120 level.

The next major resistance is near 1.3140. If there is a move above the 1.31400 resistance, the pair could rise toward 1.3250. Any more gains might send the pair toward the 1.3400 resistance zone in the near term.

Looking at EUR/USD, the pair is moving higher and might soon attempt a clear move above the 1.1250 resistance zone.

Economic Releases

- US Retail Sales for June 2023 (MoM) – Forecast +0.5%, versus +0.3% previous.

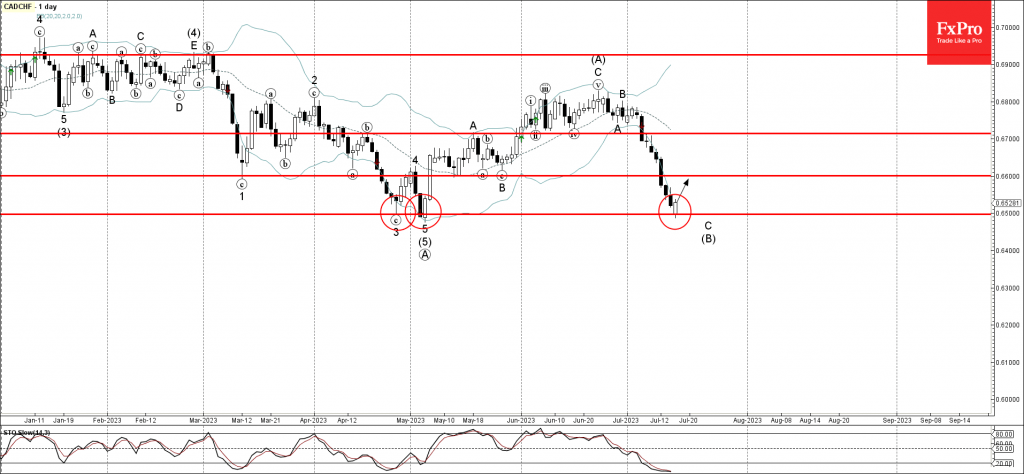

CADCHF Wave Analysis

- CADCHF reversed from resistance level 0.6400

- Likely to fall to support level 0.6255

CADCHF currency pair recently reversed up from the powerful support level 0.6495 (previous monthly low from April and May) intersecting with the lower daily Bollinger Band.

The upward reversal from the support level 0.6495 stopped the previous impulse wave C of the intermediate ABC correction (B) from last month.

Given the strength of the support level 0.6495, CADCHF can be expected to rise further toward the next resistance level 0.6600.

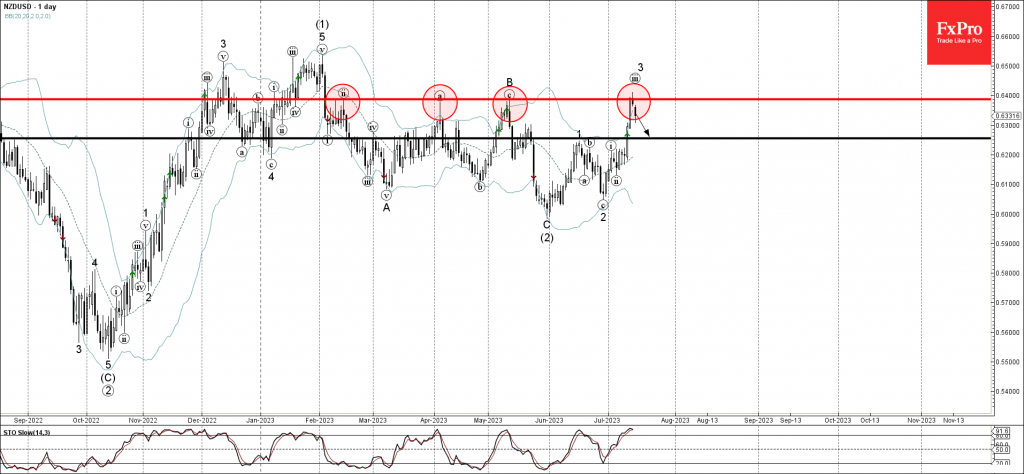

NZDUSD Wave Analysis

- NZDUSD reversed from resistance level 0.6400

- Likely to fall to support level 0.6255

NZDUSD recently reversed down from the major resistance level 0.6400 (which has been reversing the price from last February).

The downward reversal from the resistance level 0.6400 stopped the previous impulse waves (iii) and 3.

Given the strength of the resistance level 0.6400 and the overbought daily Stochastic, NZDUSD can be expected to fall further toward the next support level 0.6255, previous monthly high from June.

Gold – Edges Lower after Failing at $1,960 But Recovery Over?

- Gold pares gains after post-inflation bounce

- US yields remain lower, pulling the dollar down with them

- Resistance levels remain above at key Fibonacci levels

Gold has rotated lower over the last couple of days after previously recovering on the back of encouraging US inflation data.

The decline in US yields that we’ve seen since the release has weighed heavily on the US dollar and given the yellow metal a real boost after having endured a pretty torrid May and June.

Is the recovery sustainable?

The rotation occurred around $1,960 which was the first notable test of resistance after breaking above $1,940 earlier in the week.

XAUUSD Daily

Source – OANDA on Trading View

It falls around the 38.2% Fibonacci retracement level – May highs to June lows – and now the focus will be on whether that prior resistance level – $1,940 – turns into support.

Confirmation of the breakout – which may come from the price now finding support at $1,940 as it was previously resistance – could be bullish although there remains plenty of resistance ahead.

If the price does trend higher from here, the next tests of resistance could come around $1,980 and $2,000 which are the 50% and 61.8% Fibonacci retracement levels of the above move, respectively. The latter is also a major psychological level.

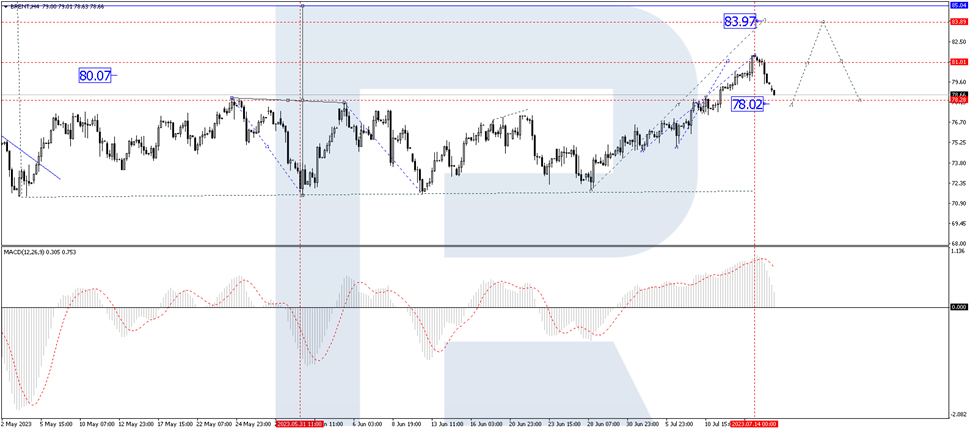

Brent Failed to Rise Despite Improved Sentiment

Crude oil prices have paused in their rally. Brent quotes on Monday dropped to 79.20 USD per barrel.

One of the reasons for this local decline might be the market decision to lock in a part of the profit after the steady growth earlier. This version is also supported by the fact that today is the first work day after the weekend.

At the same time, the commodity market sentiment improved noticeably over the last week. Large investment houses still expect a shortage in crude oil supply in the second half of this year, which looks like a favourable factor, keeping in mind the current demand parameters.

The buyers are equally supported by the fundamental background. The geopolitical situation in Libya is unstable, which might lead to problems with the supply of energy carriers.

Technical analysis of Brent:

On the H4 Brent chart, the structure of the third wave of growth is developing. At a certain point, the quotes rose to 78.00. A consolidation range formed around this level, the price broke it upwards and extended to 81.45. Today the market is correcting this growth. A technical return to 78.00 is expected with a test of this level from above. Next, a rise to 84.00 is to follow. This is a local target. After the quotes reach this level, a new correction to 78.00 could develop, followed by an increase to 85.00. This is the first target. Technically, this scenario is confirmed by the MACD: its signal line is at the highs, moving out of the histogram area, which is a signal in favour of a decline to zero.

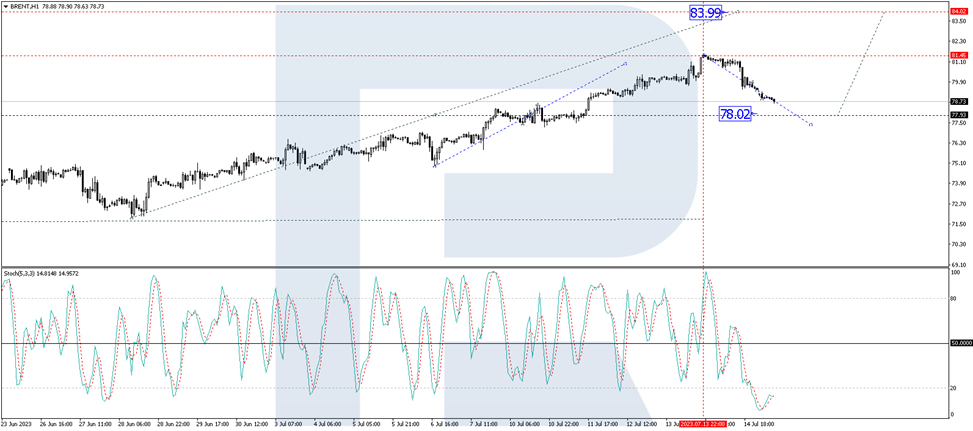

On the H1 Brent chart, a corrective wave to 78.00 is developing. After it is over, a wave of growth to 84.00 is expected to start. This is a local target. Technically, this scenario is confirmed by the Stochastic oscillator: its signal line is under 20, ready to go on growing to 50. And if this level also breaks, the potential for a rise to 80 could open.

AUD/USD Edges Lower ahead of RBA Minutes, Lowe is Out

- Australian dollar soared over 2% last week

- RBA minutes to be released on Tuesday

- RBA Governor Lowe will be replaced by Michelle Bullock

The Australian dollar has started the week in negative territory. In the European session, AUD/USD is trading at 0.6816, down 0.32%. The Aussie is coming off a banner week, with gains of 2.18% against the US dollar.

Has RBA hit the terminal rate?

The Reserve Bank of Australia releases the minutes of the July 4th meeting on Tuesday. At that meeting, the RBA took a pause and maintained the cash rate at 4.10%. The burning question is whether interest rate levels have peaked. The markets are more confident that the RBA is leaning towards another pause in August, with a 75% probability of a 25-bp hike in August, compared to 48% just a week ago.

The RBA has based its rate decisions on key economic data, in particular, inflation and employment reports. Thursday’s employment report will be a key factor in the RBA rate decision. If the employment numbers are stronger than expected, we’ll likely see the markets revise higher the probability of a rate hike in August.

There was a feeling in the air that RBA Governor Lowe would be shown the front door, and the axe came down on Friday. Lowe has been heavily criticised for assurances he made as late as November 2021 that he would not raise rates until 2024, only to embark on an aggressive rate-hike campaign soon after.

The RBA’s zig-zagging of rate hikes and pauses hurt the central bank’s credibility, and a recent review of the RBA found that major structural changes were needed. Add a 7% inflation level to the mix, and it’s not difficult to see why the government decided that a change was needed at the helm of the RBA.

AUD/USD Technical

- There is resistance at 0.6855 and 0.6947

- 0.6786 and 0.6676 are providing support

July Flashlight for the FOMC Blackout Period

Summary

- The FOMC kept the fed funds rate unchanged in June, but the post-meeting statement said that the Committee would take into account "economic and financial developments" when "determining the extent to which additional policy firming may be appropriate."

- In our view, recent "economic and financial developments" will lead the FOMC to raise its target range for the federal funds rate by 25 bps on July 26.

- For starters, the employment reports for May and June, which were released since the FOMC last raised rates on May 3, showed that while job growth is slowing, the labor market remains tight and is helping to keep inflation above the Committee's 2% target.

- Inflation slowed in June, including the smallest monthly gain in the core CPI since 2021. However, with price growth running well-above target for about two years now, we believe participants will want to be more confident that inflation is on a sustainable downward path before ending the FOMC's tightening cycle.

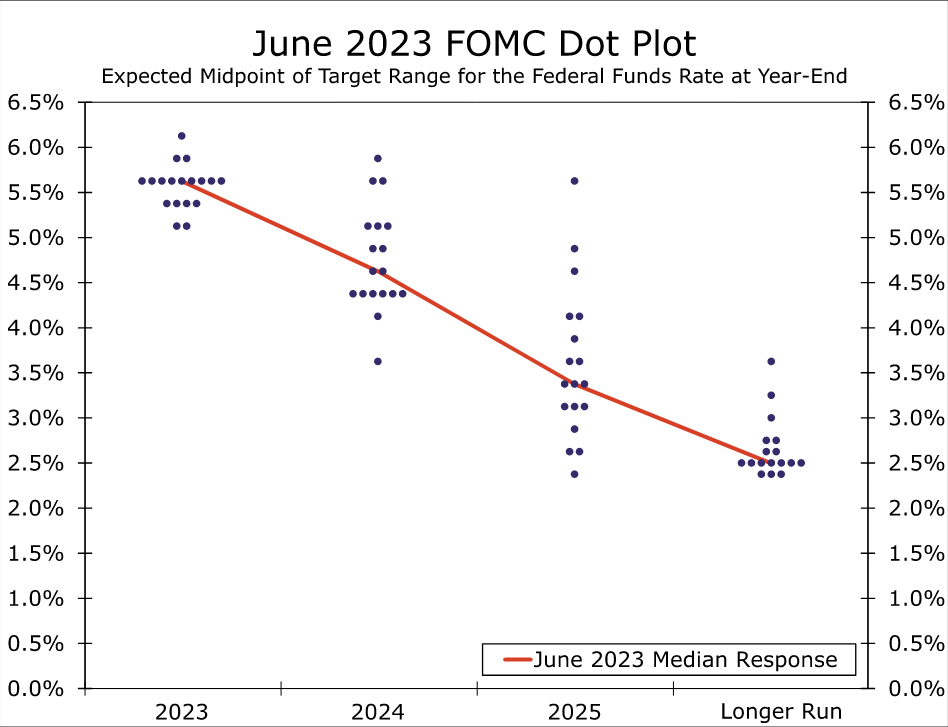

- Furthermore, written and verbal communication by Fed officials since the last FOMC meeting suggest that further tightening likely lies in store. The "dot plot" that was released after the June 14 meeting showed that most members believed that further tightening would be appropriate by the end of this year, and Fed officials have generally sounded hawkish in recent public comments.

- The FOMC could conceivably refrain from hiking its target range by 25 bps on July 26, but we do not believe a consensus currently exists among Committee members for another hold next week. A far more likely way to reach consensus, in our view, would be via a 25 bps rate hike with indications in the post-meeting statement that the FOMC is prepared to hike further, if "economic and financial developments" warrant.

- We do not expect the FOMC to make any technical tweaks to the interest rate it pays on reserve balances that banks hold at the central bank, nor to its repo and reverse repo rates.

Recent Data Support the Case for Another Rate Hike

The Federal Open Market Committee (FOMC) has raised its target range for the federal funds rate by 500 bps since March 2022. The rapid pace of tightening last year, which transpired as inflation was shooting higher, was meant to quickly turn the stance of monetary policy from accommodative to restrictive. The Committee has slowed the pace of tightening this year as economic activity has decelerated and inflation has receded. In the statement that was released following the policy meeting on May 3, at which the FOMC hiked rates by 25 bps, and again on June 14, when it kept rates unchanged, the Committee said it would take into account "economic and financial developments" when "determining the extent to which additional policy firming may be appropriate."

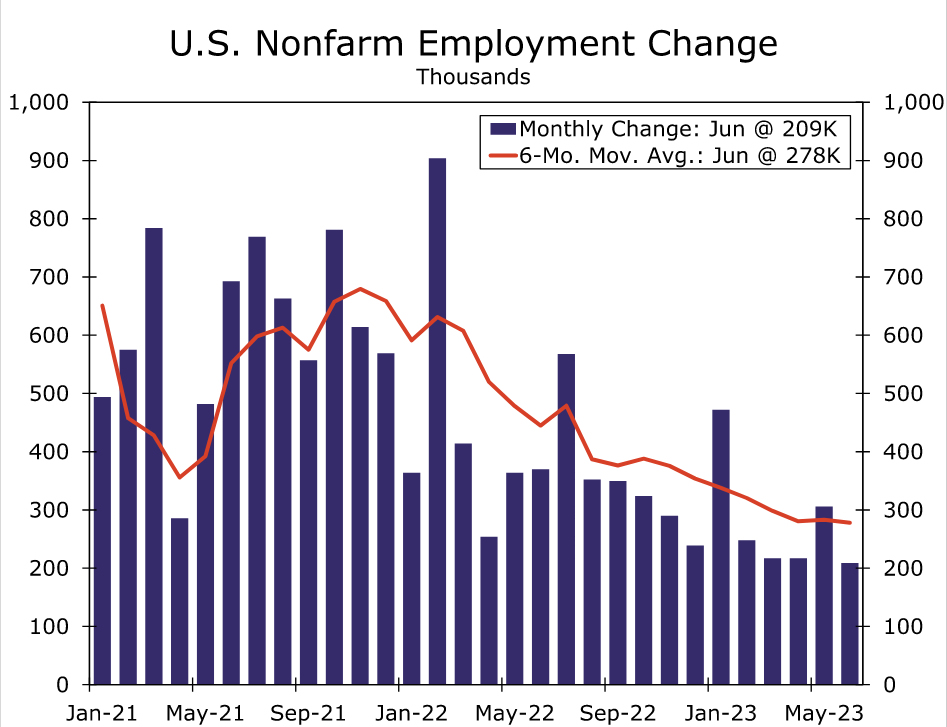

In that regard, recent data suggest that more "policy firming" may indeed "be appropriate." For starters, the U.S. economy added 209K jobs in June (Figure 1). Although the monthly addition to payrolls in June was the smallest since December 2020, the increase still exceeded the average rise of roughly 185K per month during the 2010-2019 expansion. Only 3.6% of the labor force was unemployed in June, little changed from the cyclical low of 3.4% hit in January and April, and the year-over-year rise in average hourly earnings stayed constant at 4.4% last month. In short, the labor market remains tight, which is helping to keep inflation elevated.

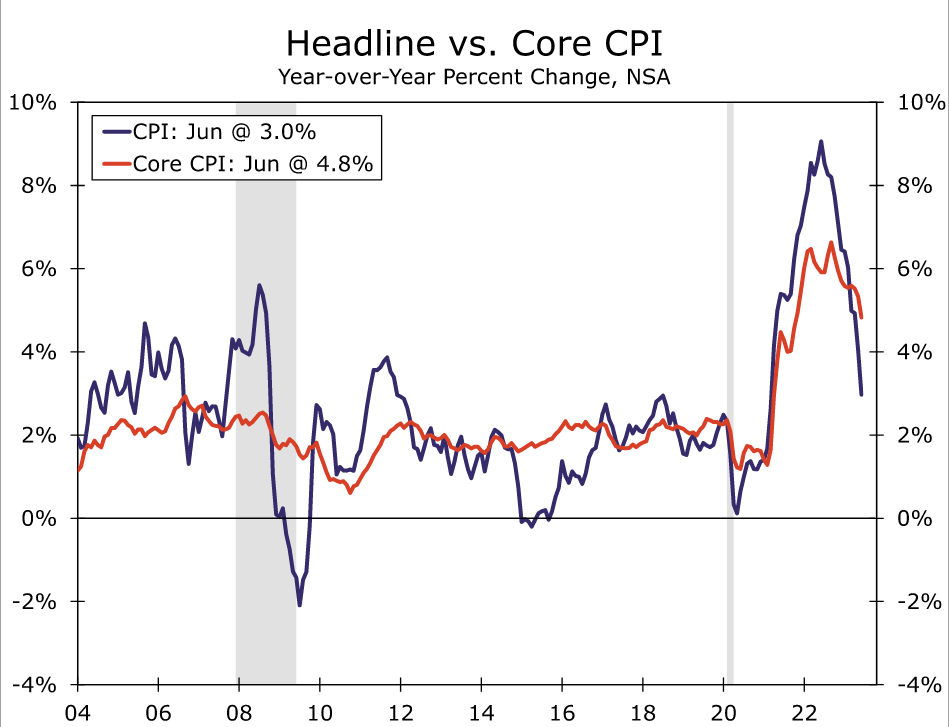

Data released on July 12 showed that consumer prices edged up 0.2% in June relative to the previous month, which caused the year-over-year rate of CPI inflation to drop from 4.0% in May to 3.0% in June (Figure 2). Since peaking at 9.1% in June 2022, the overall rate of CPI inflation has receded by more than six percentage points. While there has been broad-based deceleration in consumer prices over the past year, the 27% drop in the gasoline component of the CPI since June 2022, which has little to do with Fed policy tightening per se, has helped to pull the overall rate of CPI inflation lower over the past year. When looking at the "core" rate of CPI inflation, which excludes prices of food and energy but accounts for 80% of the consumer price index, the FOMC has had less success in bringing inflation lower. The year-over-year rate of core CPI inflation, which rose to a 40-year high of 6.6% last September, has receded to only 4.8%. Moreover, the core CPI in June rose at an annualized rate of 4.1% relative to three months prior (i.e., March). Although down from the comparable three-month rate of change of 5.0% in May, inflation is still running well above the FOMC's 2% target.

Core inflation was initially pushed higher by rapid acceleration in prices of core goods (i.e., prices of goods excluding food and energy). But a rotation of consumer spending away from goods and toward services in conjunction with the healing of supply chains have led to considerable moderation in core goods inflation since early 2022. In June, prices of core goods were up only 1.4% on a year-ago basis. Although the acceleration in prices of core services, which account for nearly 60% of the overall CPI, lagged the moonshot in core goods prices, service sector inflation has been slower to recede. In June, prices of core services were up 6.2% on a year-ago basis.

Because wages and salaries are the largest cost component for most service-providing businesses, a return to an overall inflation rate of 2% will be difficult for the Federal Reserve to achieve as long as the labor market remains excessively tight. At 3.6% currently, the jobless rate is below what most FOMC members estimate it should be in the "longer run" (i.e., after 2025). This long-run estimate of the unemployment rate can be interpreted as a proxy for the "equilibrium" jobless rate, or the so-called non-accelerating inflation rate of unemployment (NAIRU). In order to generate some "slack" in the labor market, the Fed must slow growth in the economy enough to bring labor demand into better balance with labor supply. Interest rate increases affect the economy with long and variable lags, and individual policymakers can disagree about whether more monetary tightening is currently needed to bring the demand for labor in line with the supply of labor. But written and verbal communication by many Fed officials since the last FOMC meeting suggest that further tightening likely lies in store.

Most FOMC Members Seem to Support Further Tightening

For starters, the "dot" plot that was released at the conclusion of the June 14 FOMC meeting showed that 16 of the 18 Committee members deemed that at least 25 bps of further tightening would be appropriate by the end of this year (Figure 3). More recently, Fed officials have sounded hawkish in public commentary. Last week, a number of FOMC members, including Governors Christopher Waller and Michael Barr, Cleveland Fed President Loretta Mester and San Francisco Fed President Mary Daly all indicated their support for further monetary tightening this year. In sum, we think that a 25 bps rate hike on July 26 is highly likely.

Although the FOMC could conceivably refrain from tightening further on July 26, we think that probability is rather low. As discussed previously, the economy remains resilient and inflation continues to run well above the FOMC's target of 2%. Financial markets are more or less fully priced for a 25 bps rate hike on July 26, and the FOMC has tried to refrain from surprising markets in recent years. Although Fed speakers did not discuss the specific timing of further rate hikes in recent comments, pausing again at this meeting after the Committee decided to keep rates on hold on June 14 does not seem probable to us. The June dot plot indicated that 12 of the 18 FOMC members thought that at least 50 bps of further tightening would be appropriate by the end of the year. This suggests to us that holding policy rates steady for the second consecutive meeting is not the consensus view on the FOMC. Furthermore, a second consecutive "skip" would likely lead markets to discount the possibility of further tightening, leading to an easing in financial conditions.

Likewise, we think the probability of a 50 bps rate hike next week is even less likely than another pause. Payrolls and core consumer prices have decelerated since the FOMC last met in June. Financial markets are not currently priced for a 50 bps rate hike on July 26 and, as noted above, the FOMC tries to refrain from surprising market participants. Furthermore, the FOMC is a consensus-driven body, and we do not believe a consensus currently exists among Committee members for a 50 bps rate hike next week. A far more likely way to reach consensus, in our view, would be via a 25 bps rate hike with indications in the post-meeting statement, supported by comments by Chair Powell in his press conference, that the FOMC is prepared to hike further, if "economic and financial developments" warrant.

We Do Not Expect Any Change in the Pace of QT

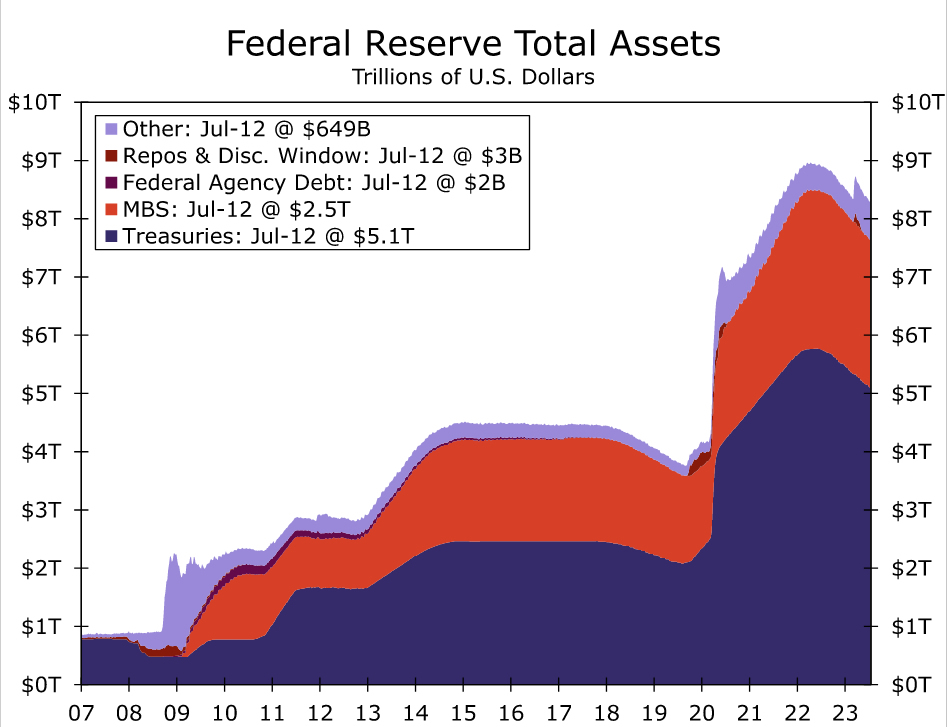

Not only has the FOMC been tightening monetary policy via rate hikes since March 2022, but it has also undertaken "quantitative tightening" (QT) since last June. That is, the FOMC is currently allowing up to $60 billion worth of Treasury securities and up to $35 billion worth of mortgage-backed securities (MBS) to roll off the central bank's balance sheet every month. As shown in Figure 4, the size of the Fed's balance sheet peaked at roughly $9 trillion in April 2022 before shrinking to $8.3 trillion in early March of this year. The failures of some regional banks in mid-March caused the balance sheet to spike by approximately $400 billion over the following two weeks as some liquidity-strapped banks tapped the Fed's emergency lending facilities. But as tensions in financial markets have subsided since March, the outstanding stock of emergency loans has trended lower and the size of the Fed's balance sheet has declined to $8.3 trillion.

The FOMC held a previously scheduled policy meeting on March 22, less than two weeks after the failures of Silicon Valley Bank and Signature Bank. Despite lingering tensions in financial markets at that time, the FOMC decided on March 22 to maintain the monthly pace of QT at $60 billion of Treasury securities and $35 billion of MBS. With many measures of financial market volatility at low levels and with few signs that banks are experiencing liquidity issues, we look for the FOMC to maintain its current pace of QT at the July 26 meeting. Our expectation regarding the pace of QT was reinforced last week by Minneapolis Fed President Kashkari who said "I think the bar would be quite high in tweaking our path for the balance sheet runoff." Accordingly, we look for the Fed's balance sheet to decline further in the month's ahead and reach roughly $7.7 trillion by year-end.

Additionally, we do not expect the FOMC will make any technical tweaks to the interest rate it pays on reserve balances that banks hold at the central bank, nor to its repo and reverse repo rates. That is, we expect the Committee will lift all three of these rates by 25 bps, in line with the increase in the target range for the federal funds rate.

Inflation to Determine the Size of the Next BoE Rate Hike

The focus this week is on Wednesday’s UK CPI release (06.00 GMT). With the next Bank of England meeting scheduled in two weeks, this report will probably determine the size of the expected rate hike. In the meantime, the pound continues to outperform the euro but a potential downside surprise on Wednesday could really clip its wings.

BoE's inflation problem

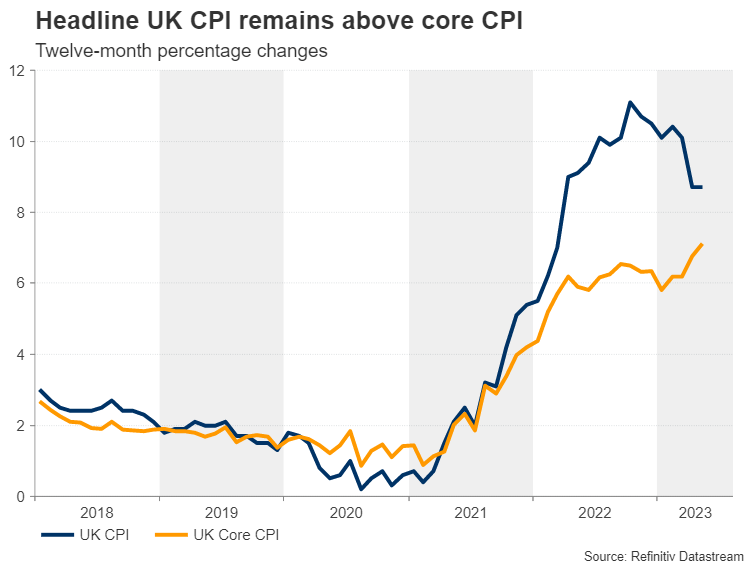

Compared to the rest of the central banks rushing to raise rates to squelch the acute inflationary pressure, the BoE opted for a more measured approach. As a result, headline inflation remains the highest in the developed world, failing to record the noteworthy drop seen in other regions over the past few months. Thus, the BoE has decided to act more forcefully as, following the surprise 50 bps rate hike at the June 22 gathering, there are growing expectations for a similarly sized move in two weeks’ time.

The main issue is that the BoE has lost valuable time and these rate hikes are probably coming too late. One of the reasonings behind the BoE's cautious approach may have been the expectation that the US economy would already have entered a recession by now, cooling US inflationary pressures, and also dragging UK inflation lower. This expectation was not confirmed and hence Bailey et al are now “forced” to adopt a more aggressive strategy that is bound to cause further significant damage to the real economy.

The housing sector is expected to really feel the higher interest rates. The BoE’s Credit Conditions Survey found that mortgage defaults in the March-May 2023 period increased to the highest level since 2009 when the subprime-induced recession was ravaging the global economy. This means the peak in defaults has yet to be seen in this cycle, potentially delivering a massive hit on total household wealth amidst the strongest inflation period since the 1970s.

June CPI on Wednesday morning

In this environment, Wednesday’s CPI prints for June are extremely important. The headline figure is expected to edge lower to an 8.2% year-on-year increase from 8.7% in May. If confirmed, this will be the lowest print since April 2022. However, it is still above its core component. This is forecast to remain at the record high of 7.1% YoY, confirming its stubborn nature. While we have seen numerous comments on the ability of core CPI to predict future inflation levels, it is an undeniable fact that the UK continues to experience significant inflationary pressure, well above the levels seen in both the US and the euro area.

In the meantime, there are increasing demands for strong salary rises to alleviate the inflationary problem. Last week’s offer by the government for 5-7% rises in public sector workers’ pay is sizeable but smaller than feared by the BoE. However, the risk of continued industrial action and an associated hit on the economy would have been devastating for the UK's growth outlook at this juncture. In this context, on Friday we get a double dose of data releases regarding the consumer sector that the BoE will be monitoring very closely.

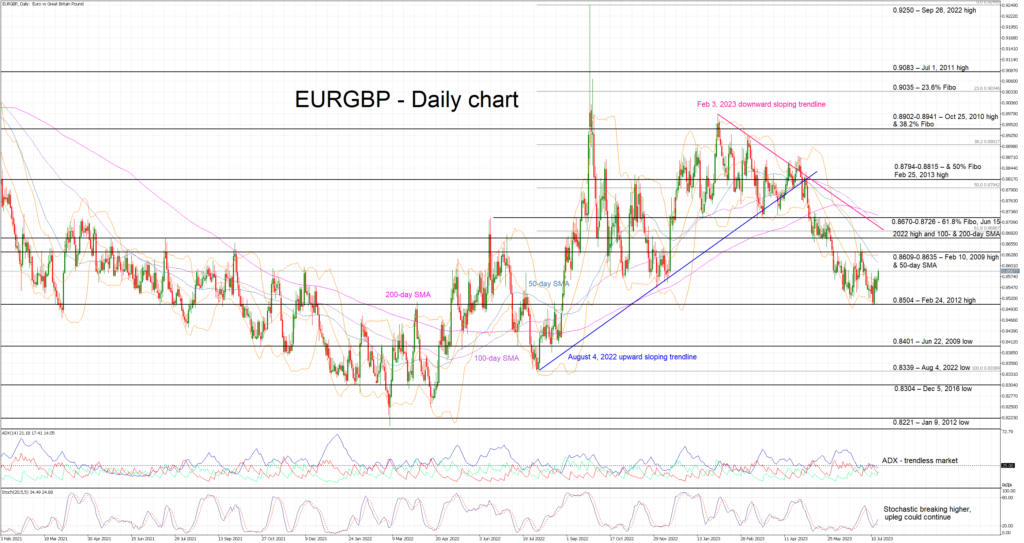

Euro/pound touched 0.85

The pound remains the star of 2023 and it is currently trading close to an 11-month high against the euro. The pound has shown extreme resilience throughout the year despite the different pace of monetary policy adjustment between the BoE and the ECB. This balance has tipped in favour of the pound lately, opening the door to more significant gains against the euro going forward.

The euro/pound pair almost broke 0.85 on July 11, prompting a small upleg towards the 0.8580 area. If the CPI report produces a significant downside surprise, especially if core inflation finally records a sizeable drop, the euro/pound pair could find strength to make a higher high and stage a move towards the 0.8670-0.8726 range. On the flip side, confirmation of current forecasts or a small pickup in inflation rates could probably cement the expectations for another 50bps move at the early-August BoE meeting, and hence allow the euro/pound pair to test the 0.8400 area.