Sample Category Title

EUR/AUD Weekly Outlook

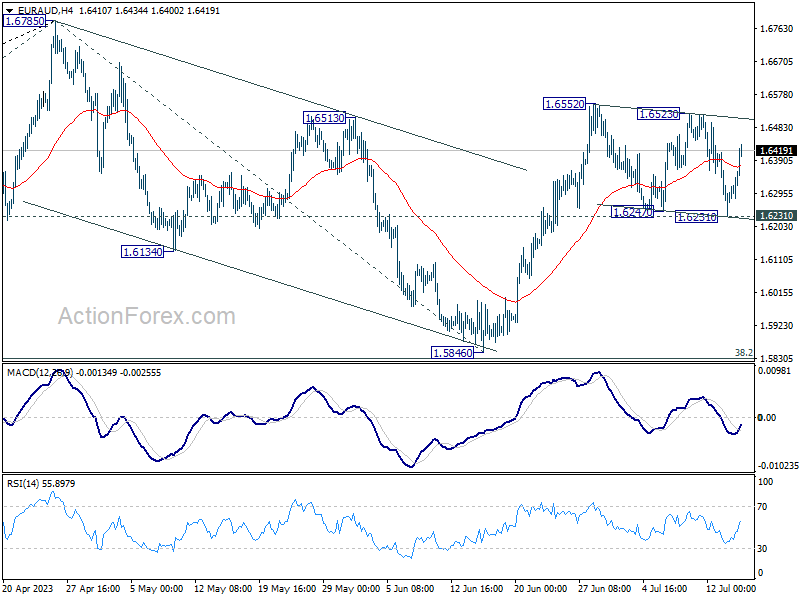

EUR/AUD dipped to 1.6231 last week but quickly rebounded after drawing support from 1.6247. Initial bias stays neutral first and outlook remains mildly bullish. Correction from 1.6785 should have completed with three waves down to 1.5846. Above 1.6552 will target a retest on 1.6785 high next. Nevertheless, on the downside, firm break of 1.6231 will dampen this view and turn bias to the downside for 1.5846 support.

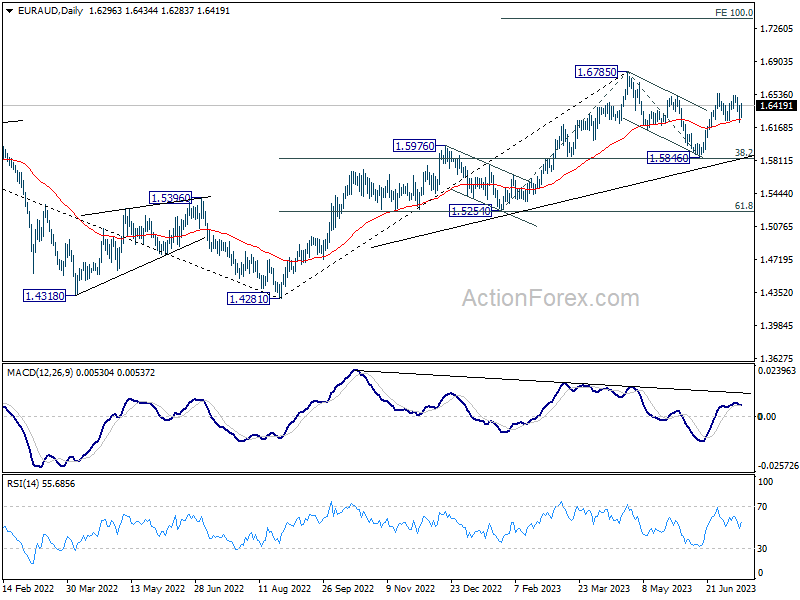

In the bigger picture, with 38.2% retracement of 1.4281 to 1.6785 at 1.5828 intact, rally from 1.4281 is still in progress. Firm break of 1.6785 will confirm rise resumption. Next target is 100% projection of 1.5254 to 1.6785 from 1.5846 at 1.7377. On the other hand, rejection by 1.6785 will extend the corrective pattern with another fall leg. But outlook will stay bullish as long as 1.5828 holds.

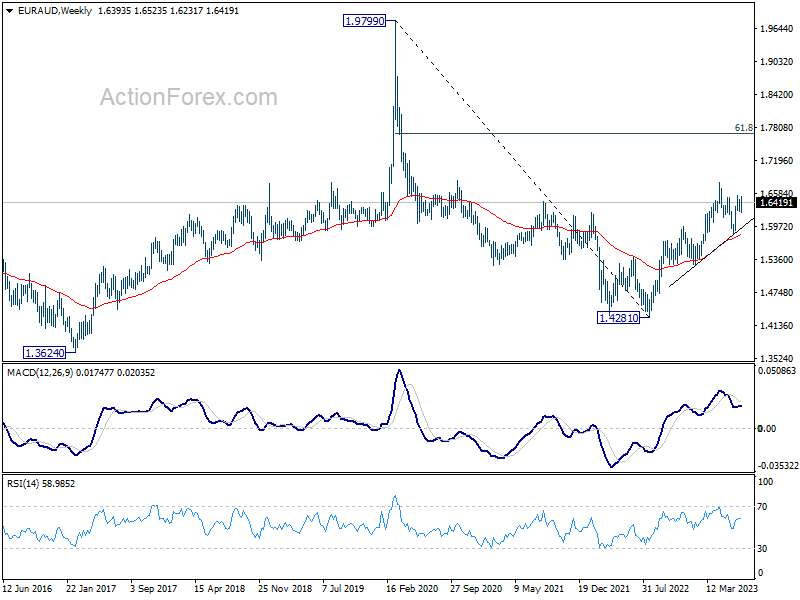

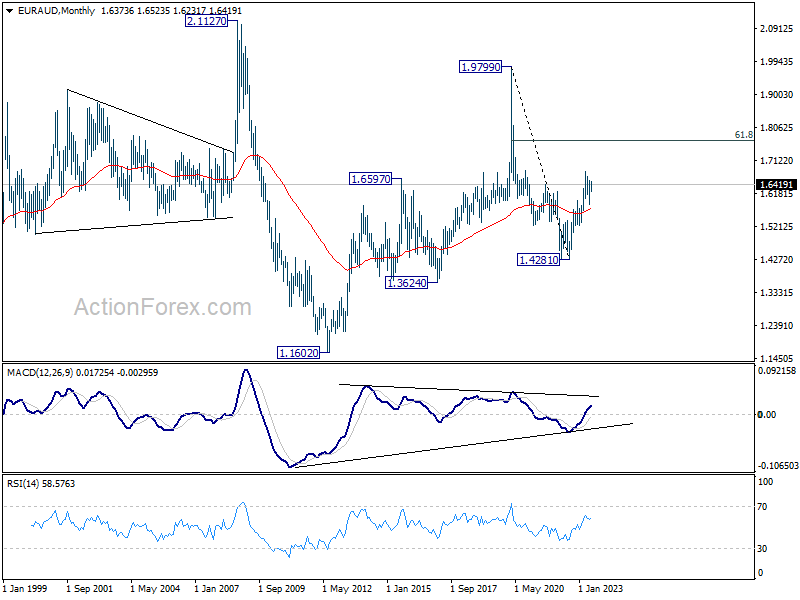

In the longer term picture, it's still early to decide if rise from 1.4281 is resuming whole up trend from 1.1602 (2012 low). But in either case, further rally is in favor as long as 1.5254 support holds. Next target is 61.8% retracement of 1.9799 to 1.4281 at 1.7691.

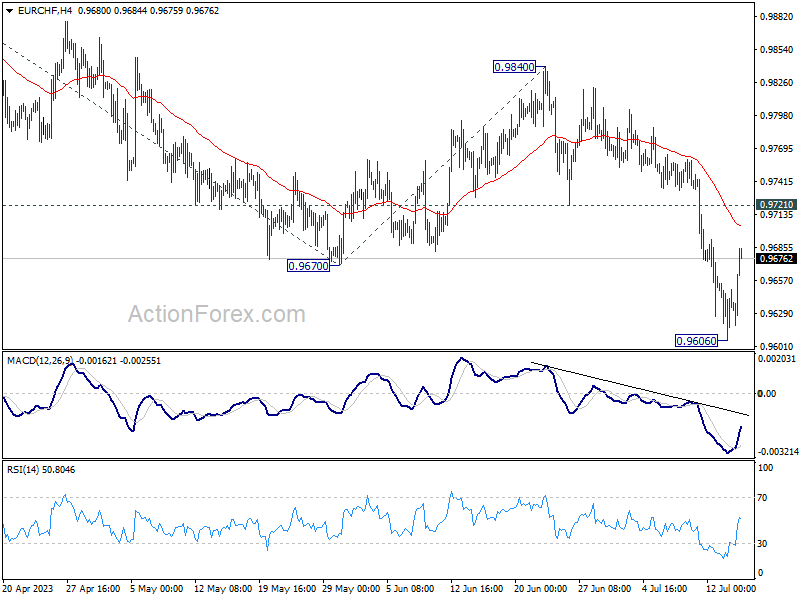

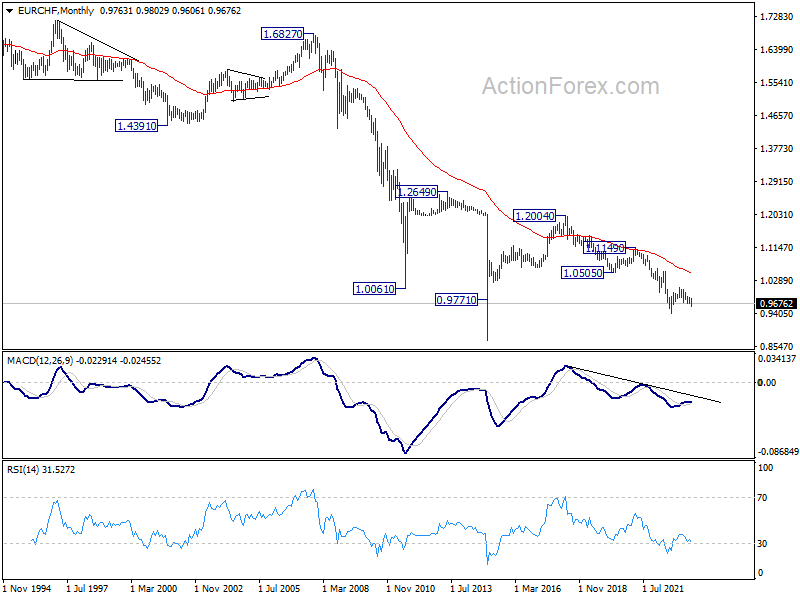

EUR/CHF Weekly Outlook

EUR/CHF broke through 0.9670 last week to resume the whole decline from 1.0095. But a temporary low was formed at 0.9606 with subsequent recovery. Initial bias is turned neutral this week first. Some consolidations could be seen, but outlook will stay bearish as long as 0.9721 support turned resistance holds. Below 0.9606 will target 100% projection of 0.9995 to 0.9670 from 0.9840 at 0.9515.

In the bigger picture, medium term outlook is staying bearish as the pair is capped below falling 55 W EMA (now at 0.9913). Down trend form 1.2004 (2018 high) is in favor to extend through 0.9407 at a later stage. Nevertheless, decisive break of 38.2% retracement of 1.1149 to 0.9407 will raise the chance of bullish trend reversal.

In the long term picture, it's still way too early too call for bullish trend reversal with upside capped well below 55 M EMA (now at 1.0459) and 1.0505 support turned resistance (2020 low). The multi-decade down trend could still continue.

Summary 7/17 – 7/21

Monday, Jul 17, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 02:00 | CNY | GDP Y/Y Q2 | 7.10% | 4.50% |

| 02:00 | CNY | Industrial Production Y/Y Jun | 2.60% | 3.50% |

| 02:00 | CNY | Retail Sales Y/Y Jun | 3.40% | 12.70% |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Jun | 3.40% | 4.00% |

| 12:30 | USD | Empire State Manufacturing Index Jul | 0.0 | 6.6 |

| 12:30 | CAD | Wholesale Sales M/M May | 2.20% | -1.40% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 02:00 | CNY | GDP Y/Y Q2 | |

| Forecast: 7.10% | Previous: 4.50% | ||

| 02:00 | CNY | Industrial Production Y/Y Jun | |

| Forecast: 2.60% | Previous: 3.50% | ||

| 02:00 | CNY | Retail Sales Y/Y Jun | |

| Forecast: 3.40% | Previous: 12.70% | ||

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Jun | |

| Forecast: 3.40% | Previous: 4.00% | ||

| 12:30 | USD | Empire State Manufacturing Index Jul | |

| Forecast: 0.0 | Previous: 6.6 | ||

| 12:30 | CAD | Wholesale Sales M/M May | |

| Forecast: 2.20% | Previous: -1.40% | ||

Tuesday, Jul 18, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | RBA Meeting Minutes | ||

| 04:30 | JPY | Tertiary Industry Index M/M May | 0.40% | 1.20% |

| 12:15 | CAD | Housing Starts Jun | 215K | 202K |

| 12:30 | CAD | CPI M/M Jun | 0.40% | |

| 12:30 | CAD | CPI Y/Y Jun | 3.40% | |

| 12:30 | CAD | CPI Core M/M Jun | 0.20% | |

| 12:30 | CAD | CPI Median Y/Y Jun | 3.90% | |

| 12:30 | CAD | CPI Trimmed Y/Y Jun | 3.80% | |

| 12:30 | CAD | CPI Common Y/Y Jun | 5.20% | |

| 12:30 | CAD | Raw Material Price Index Jun | -4.90% | |

| 12:30 | CAD | Industrial Product Price M/M Jun | -1% | |

| 12:30 | USD | Retail Sales M/M Jun | 0.50% | 0.30% |

| 12:30 | USD | Retail Sales ex Autos M/M Jun | 0.30% | 0.10% |

| 13:15 | USD | Industrial Production M/M Jun | 0.00% | -0.20% |

| 13:15 | USD | Capacity Utilization Jun | 79.50% | 79.60% |

| 14:00 | USD | Business Inventories May | 0.20% | 0.20% |

| 14:00 | USD | NAHB Housing Market Index Jul | 55 | 55 |

| 22:45 | NZD | CPI Q/Q Q2 | 0.90% | 1.20% |

| 22:45 | NZD | CPI Y/Y Q2 | 6.70% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | RBA Meeting Minutes | |

| Forecast: | Previous: | ||

| 04:30 | JPY | Tertiary Industry Index M/M May | |

| Forecast: 0.40% | Previous: 1.20% | ||

| 12:15 | CAD | Housing Starts Jun | |

| Forecast: 215K | Previous: 202K | ||

| 12:30 | CAD | CPI M/M Jun | |

| Forecast: | Previous: 0.40% | ||

| 12:30 | CAD | CPI Y/Y Jun | |

| Forecast: | Previous: 3.40% | ||

| 12:30 | CAD | CPI Core M/M Jun | |

| Forecast: | Previous: 0.20% | ||

| 12:30 | CAD | CPI Median Y/Y Jun | |

| Forecast: | Previous: 3.90% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Jun | |

| Forecast: | Previous: 3.80% | ||

| 12:30 | CAD | CPI Common Y/Y Jun | |

| Forecast: | Previous: 5.20% | ||

| 12:30 | CAD | Raw Material Price Index Jun | |

| Forecast: | Previous: -4.90% | ||

| 12:30 | CAD | Industrial Product Price M/M Jun | |

| Forecast: | Previous: -1% | ||

| 12:30 | USD | Retail Sales M/M Jun | |

| Forecast: 0.50% | Previous: 0.30% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Jun | |

| Forecast: 0.30% | Previous: 0.10% | ||

| 13:15 | USD | Industrial Production M/M Jun | |

| Forecast: 0.00% | Previous: -0.20% | ||

| 13:15 | USD | Capacity Utilization Jun | |

| Forecast: 79.50% | Previous: 79.60% | ||

| 14:00 | USD | Business Inventories May | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 14:00 | USD | NAHB Housing Market Index Jul | |

| Forecast: 55 | Previous: 55 | ||

| 22:45 | NZD | CPI Q/Q Q2 | |

| Forecast: 0.90% | Previous: 1.20% | ||

| 22:45 | NZD | CPI Y/Y Q2 | |

| Forecast: | Previous: 6.70% | ||

Wednesday, Jul 19, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Westpac Leading Index M/M Jun | -0.30% | |

| 06:00 | GBP | CPI M/M Jun | 0.70% | |

| 06:00 | GBP | CPI Y/Y Jun | 8.20% | 8.70% |

| 06:00 | GBP | Core CPI Y/Y Jun | 7.10% | 7.10% |

| 06:00 | GBP | RPI M/M Jun | 0.70% | |

| 06:00 | GBP | RPI Y/Y Jun | 10.90% | 11.30% |

| 06:00 | GBP | PPI Input M/M Jun | -0.20% | -1.50% |

| 06:00 | GBP | PPI Input Y/Y Jun | 0.50% | |

| 06:00 | GBP | PPI Output M/M Jun | -0.30% | -0.50% |

| 06:00 | GBP | PPI Output Y/Y Jun | 2.90% | |

| 06:00 | GBP | PPI Core Output M/M Jun | -0.30% | |

| 06:00 | GBP | PPI Core Output Y/Y Jun | 4.10% | |

| 09:00 | EUR | Eurozone CPI Y/Y Jun F | 5.50% | 5.50% |

| 09:00 | EUR | Eurozone CPI Core Y/Y Jun F | 5.40% | 5.40% |

| 12:30 | USD | Building Permits Jun | 1.48M | 1.49M |

| 12:30 | USD | Housing Starts Jun | 1.47M | 1.63M |

| 14:30 | USD | Crude Oil Inventories | 5.9M | |

| 23:50 | JPY | Trade Balance (JPY) Jun | -0.66T | -0.78T |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Westpac Leading Index M/M Jun | |

| Forecast: | Previous: -0.30% | ||

| 06:00 | GBP | CPI M/M Jun | |

| Forecast: | Previous: 0.70% | ||

| 06:00 | GBP | CPI Y/Y Jun | |

| Forecast: 8.20% | Previous: 8.70% | ||

| 06:00 | GBP | Core CPI Y/Y Jun | |

| Forecast: 7.10% | Previous: 7.10% | ||

| 06:00 | GBP | RPI M/M Jun | |

| Forecast: | Previous: 0.70% | ||

| 06:00 | GBP | RPI Y/Y Jun | |

| Forecast: 10.90% | Previous: 11.30% | ||

| 06:00 | GBP | PPI Input M/M Jun | |

| Forecast: -0.20% | Previous: -1.50% | ||

| 06:00 | GBP | PPI Input Y/Y Jun | |

| Forecast: | Previous: 0.50% | ||

| 06:00 | GBP | PPI Output M/M Jun | |

| Forecast: -0.30% | Previous: -0.50% | ||

| 06:00 | GBP | PPI Output Y/Y Jun | |

| Forecast: | Previous: 2.90% | ||

| 06:00 | GBP | PPI Core Output M/M Jun | |

| Forecast: | Previous: -0.30% | ||

| 06:00 | GBP | PPI Core Output Y/Y Jun | |

| Forecast: | Previous: 4.10% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Jun F | |

| Forecast: 5.50% | Previous: 5.50% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Jun F | |

| Forecast: 5.40% | Previous: 5.40% | ||

| 12:30 | USD | Building Permits Jun | |

| Forecast: 1.48M | Previous: 1.49M | ||

| 12:30 | USD | Housing Starts Jun | |

| Forecast: 1.47M | Previous: 1.63M | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 5.9M | ||

| 23:50 | JPY | Trade Balance (JPY) Jun | |

| Forecast: -0.66T | Previous: -0.78T | ||

Thursday, Jul 20, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | NAB Business Confidence Q2 | -4 | |

| 01:30 | AUD | Employment Change Jun | 15.0K | 75.9K |

| 01:30 | AUD | Unemployment Rate Jun | 3.60% | 3.60% |

| 06:00 | CHF | Trade Balance (CHF) Jun | 4.23B | 5.48B |

| 06:00 | EUR | Germany PPI M/M Jun | -0.40% | -1.40% |

| 06:00 | EUR | Germany PPI Y/Y Jun | 1.00% | |

| 08:00 | EUR | Eurozone Current Account (EUR) May | 2.5B | 3.6B |

| 12:30 | USD | Initial Jobless Claims (Jul 14) | 245K | 237K |

| 12:30 | USD | Philadelphia Fed Manufacturing Jul | -15.5 | -13.7 |

| 14:00 | USD | Existing Home Sales Jun | 4.27M | 4.30M |

| 14:00 | EUR | Eurozone Consumer Confidence Jul P | -16 | -16 |

| 14:30 | USD | Natural Gas Storage | 49B | |

| 23:01 | GBP | GfK Consumer Confidence Jul | -24 | |

| 23:30 | JPY | National CPI Y/Y Jun | 3.20% | |

| 23:30 | JPY | National CPI Core Y/Y Jun | 3.20% | |

| 23:30 | JPY | National CPI Core-Core Y/Y Jun | 4.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | NAB Business Confidence Q2 | |

| Forecast: | Previous: -4 | ||

| 01:30 | AUD | Employment Change Jun | |

| Forecast: 15.0K | Previous: 75.9K | ||

| 01:30 | AUD | Unemployment Rate Jun | |

| Forecast: 3.60% | Previous: 3.60% | ||

| 06:00 | CHF | Trade Balance (CHF) Jun | |

| Forecast: 4.23B | Previous: 5.48B | ||

| 06:00 | EUR | Germany PPI M/M Jun | |

| Forecast: -0.40% | Previous: -1.40% | ||

| 06:00 | EUR | Germany PPI Y/Y Jun | |

| Forecast: | Previous: 1.00% | ||

| 08:00 | EUR | Eurozone Current Account (EUR) May | |

| Forecast: 2.5B | Previous: 3.6B | ||

| 12:30 | USD | Initial Jobless Claims (Jul 14) | |

| Forecast: 245K | Previous: 237K | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Jul | |

| Forecast: -15.5 | Previous: -13.7 | ||

| 14:00 | USD | Existing Home Sales Jun | |

| Forecast: 4.27M | Previous: 4.30M | ||

| 14:00 | EUR | Eurozone Consumer Confidence Jul P | |

| Forecast: -16 | Previous: -16 | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 49B | ||

| 23:01 | GBP | GfK Consumer Confidence Jul | |

| Forecast: | Previous: -24 | ||

| 23:30 | JPY | National CPI Y/Y Jun | |

| Forecast: | Previous: 3.20% | ||

| 23:30 | JPY | National CPI Core Y/Y Jun | |

| Forecast: | Previous: 3.20% | ||

| 23:30 | JPY | National CPI Core-Core Y/Y Jun | |

| Forecast: | Previous: 4.30% | ||

Friday, Jul 21, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:00 | GBP | Retail Sales M/M Jun | 0.30% | |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Jun | 19.2B | |

| 12:30 | CAD | Retail Sales M/M May | 1.10% | |

| 12:30 | CAD | Retail Sales ex Autos M/M May | 1.30% | |

| 12:30 | CAD | New Housing Price Index M/M Jun | 0.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:00 | GBP | Retail Sales M/M Jun | |

| Forecast: | Previous: 0.30% | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Jun | |

| Forecast: | Previous: 19.2B | ||

| 12:30 | CAD | Retail Sales M/M May | |

| Forecast: | Previous: 1.10% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M May | |

| Forecast: | Previous: 1.30% | ||

| 12:30 | CAD | New Housing Price Index M/M Jun | |

| Forecast: | Previous: 0.10% | ||

Weekly Economic & Financial Commentary: Downside Inflation Surprise Probably Not Enough to Stop the Fed

Summary

United States: Downside Inflation Surprise Probably Not Enough to Stop the Fed

- This week provided additional evidence that economy-wide price pressures are gradually easing. Both the headline and core CPI ticked up 0.2% each in June, the lowest monthly advances since early 2021. Core producer prices similarly posted their softest annual increase since February 2021. Although labor demand remains healthy, other indicators suggested that employers may be pulling back on hiring.

- Next week: Retail Sales (Tue), Industrial Production (Tue), Housing Starts (Wed)

International: Bank of Canada Open to More Rate Hikes; EM Central Banks Approaching Rate Cuts

- While the Bank of Canada lifted policy rates this week, policymakers seemed open to additional rate hikes as inflation persists more than expected. We continue to believe the BoC has achieved its peak policy rate; however, risks are tilted toward at least one more 25 bps hike. On the other hand, central banks in the emerging markets are ready to begin easing monetary policy. Institutions in Latin America are likely to act in the coming weeks and months, while our framework suggests policymakers across regions have space to cut interest rates before the end of this year.

- Next week: Canada Inflation (Tue), United Kingdom Inflation (Wed), Central Bank of Turkey (Thu)

Interest Rate Watch: Falling Inflation Brings Treasury Yields Down with It

- This week's cooling inflation data helped generate falling Treasury yields as investors bet that the FOMC would hike the fed funds rate one final time in July but start cutting rates in 2024. As we go to print, the 10-year Treasury is yielding 3.82%, down 24 bps from one week ago. The two-year Treasury yield, which is more sensitive to near-term moves in the federal funds rate, is down 20 bps on the week.

Credit Market Insights: Rate Hikes Continue to Catch Up to Lending Markets

- U.S. consumer borrowing data were surprisingly soft in May. Total consumer credit rose by "just" $7.24 billion, which not only undercut the Bloomberg consensus forecast by a wide margin, but marked the slowest pace of credit growth since November 2020. The slowdown in credit could indicate that high interest rates are catching up to the economy.

The Weekly Bottom Line: Inflation Data Brings A Healthy Dose of Optimism

U.S. Highlights

- Financial markets rallied this week following a string of promising data pointing to easing U.S. inflationary pressures.

- Inflation as measured by the Consumer Price Index fell to the slowest pace of growth since March 2021 in June. Core inflation also only increased modestly on the month. Input costs also trended lower last month, with the Producing Purchase Index falling to the lowest reading since August 2020.

- Though the data overwhelmingly point to easing inflationary pressures, the Federal Reserve is still expected to deliver another 25 basis-point hike later this month.

Canadian Highlights

- The Bank of Canada hiked the policy rate by another 25 basis points to 5.00%. The decision doubles down on the Bank’s commitment to wrestle inflation back to target.

- Future meetings are live for an interest rate hike, but we believe the Bank of Canada is likely done. Our forecasts point to further moderation in inflation, slowing growth, and a cooler labour market ahead.

- All eyes are on next week’s inflation data for June. We expect headline CPI to continue cooling, but stickiness to persist in core measures.

U.S. – Inflation Data Brings A Healthy Dose of Optimism

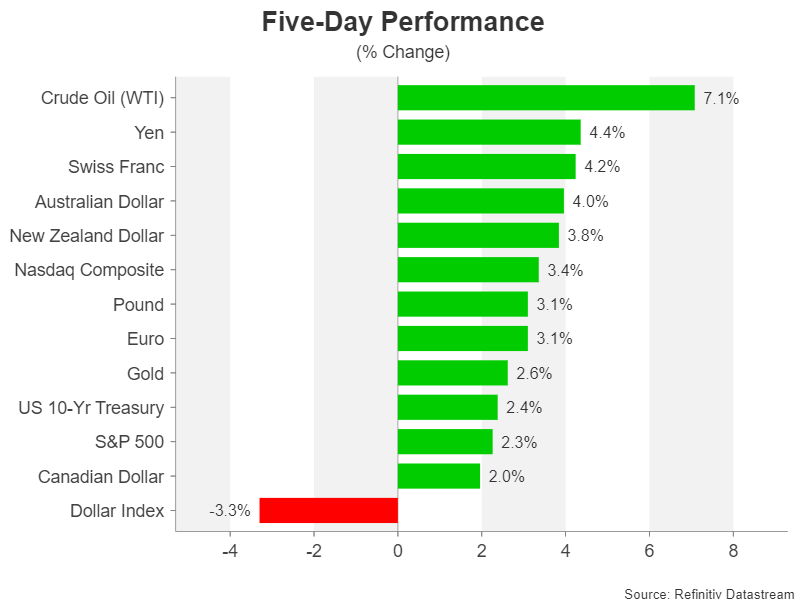

Sentiment across global financial markets firmed this week following a lower-than-expected reading on U.S. inflation. Recession fears have been top of mind for investors over the past year amidst the Federal Reserve’s most aggressive tightening cycle in several decades. But signs of cooling inflation provided a dose of optimism that policymakers might achieve a goldilocks scenario of returning price stability without tipping the economy into recession. At the time of writing, the S&P 500 is up 2.5% on the week, WTI has rallied by just over 4% to $76 per-barrel, while yields across the board traded lower by approximately 20bps. The 10-Year Treasury yield currently sits at 3.8%.

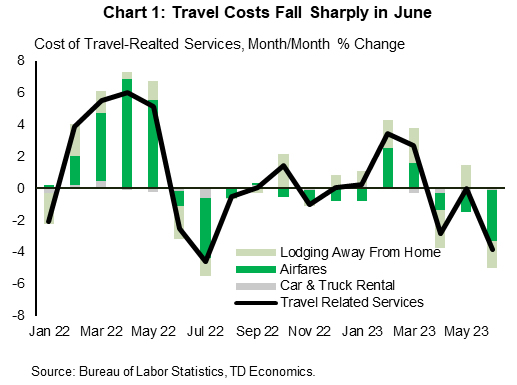

The Consumer Price Index (CPI) eased to a 3.0% pace y/y in June – the lowest reading since March 2021. But, perhaps more notable, core inflation rose by just 0.16% m/m – the slowest pace of growth in 28 months – and dipped to 4.8% y/y. A hefty decline in travel related services underpinned last month’s deceleration, as well as a continued deceleration in shelter costs (Chart 1). Used vehicle prices also fell by a modest 0.5% m/m, which came after outsized gains in each of the two-months prior.

Looking to the months ahead, there’s good reason to remain optimistic that further progress will be made on the inflation front. For starters, the much anticipated slowing in shelter costs now appears to be firmly intact, with both owners’ equivalent rent (OER) and rent of primary residence (RPR) having decelerated in recent months. More importantly, current market-based measures of rent continue to show rental costs slowing, which means further disinflationary pressure on OER and RPR as more leases roll over.

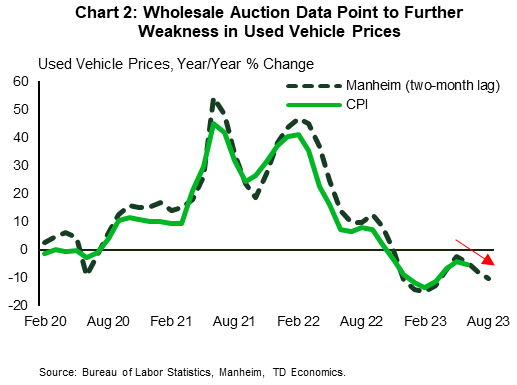

On the goods side, used vehicle prices are expected to be a source of downward pressure on inflation in the coming months. Wholesale auction data for used vehicle prices have tumbled in recent months, with the pass-through to the consumer measure typically taking 2-3 months. (Chart 2). Outside of this category, prices across all other goods have already been flat for three consecutive months and are likely to trend lower through the second half of this year alongside weaker consumer spending. Input costs are also trending favorably. The June reading on the Producer Price Index (PPI) showed that the 12-month change slowed to just 0.1% for final demand products – the lowest reading since August 2020.

Though the recent string of data overwhelming point to a continued easing in inflationary pressures, it is widely expected that Fed will deliver on another 25bps rate hike later this month. No matter which way you slice it, core inflation on a 12, 6, and 3-month annualized basis is still running at a multiple of the Fed’s 2% inflation target. And, with the labor market continuing to exude considerable resilience, policymakers will need to see more convincing evidence that the disinflationary process is firmly intact before calling it quits. Fed Chair Powell has repeatedly emphasized the risk of ‘stopping short’, so the FOMC is likely to maintain a tightening bias over the near-term as they continue to monitor incoming data and fine-tune the end point of its tightening cycle.

Canada – These Boots Were Made For Hiking

Canadian markets were centered on the Bank of Canada (BoC) interest rate decision this week, where the BoC opted to raise the overnight rate by 25 basis points (bps) to 5.00%, the highest level since April 2001. The move aligned with market expectations and matched our own forecast. Canadian yield moves were muted post-announcement. A soft CPI report stateside likely influenced the Canadian rates curve, with yields finishing down on the week. However, the Canadian dollar jumped to 76 cents U.S. and is holding this level into week-end.

As recently as six months ago, markets were pessimistic about the Canadian economy, and expected rate cuts this year. However, that line of thinking has all but evaporated as economic data continues to roll in stronger than expected. Not only have there been 50 bps of hikes since the BoC hopped off the sidelines, but this week's policy decision certainly had a hawkish tilt as officials have kept the door open to further moves. Macklem & Co. are trying to restore public confidence in their commitment to achieving their two percent inflation target.

Inflation is decelerating, but at a pace slower than the BoC would like to see. According to the MPR, headline annual inflation is now forecast to linger around 3.0% for another year and overall price stickiness has forced the BoC to adjust their path back to 2.0%. Policy makers had previously thought this could be achieved by the end of 2024, but this has now been pushed until mid-2025. Core inflation is also running at a still-uncomfortable pace.

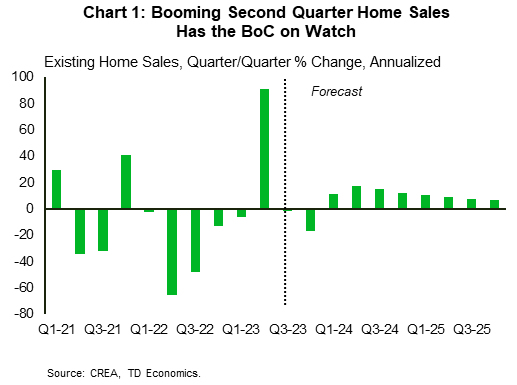

The BoC revised up its outlook for Canada's GDP growth this year, citing more persistent excess demand, a tight labour market, strong population growth, and a surprise upturn in housing. On housing, recently released data saw Q2 sales surge on a quarter-on-quarter (q/q) basis (Chart 1). That said, we still think that home sales will decline, on average, in the second half of this year, with this week's interest rate hike likely to have a near-term negative impact.

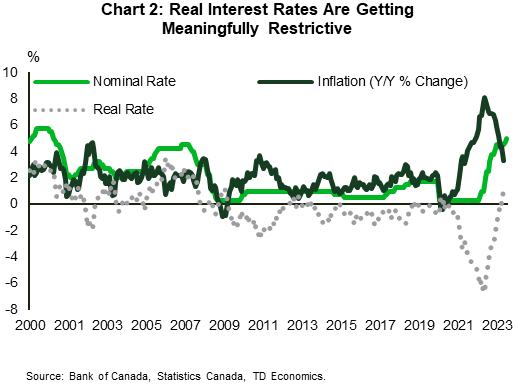

Markets are now pricing in a 50% chance of another rate hike by the end of the year, but we believe the Bank of Canada has reached the peak. Our base case is that key metrics tracked by the BoC will continue to moderate, especially as real rates become increasingly restrictive (Chart 2). Compared to the BoC, our own forecast sees consumption slowing down materially in coming quarters, with this softness more apparent in 2024 as mortgage renewals increasingly strain household budgets.

The BoC will need to digest a deluge of upcoming data before they meet again on September 6th. Front and center is next week's inflation report for June where we expect further moderation of headline measures. We don't expect much short-term respite in core measures as progress has effectively stalled over the past several months. Retail trade for May will further inform the state of the consumer.

Week Ahead – UK Inflation, Earnings, Interest Rate Decisions Galore

US

The week before the July 26th FOMC meeting will contain a handful of key economic reports and several key earnings results. The initial assessment of the economy is somewhat upbeat as CEO Jamie Dimon noted that the US economy continues to be ‘resilient’. Next week’s big earnings include Goldman Sachs, Tesla, Netflix, Morgan Stanley, and American Express.

On Monday, the ISM manufacturing report will show activity is slowing down, with the headline reading expected to fall back into contraction territory. On Tuesday, the June retail sales report is expected to show strength, as major car discounts encouraged buying. Demand for services might still remain strong but is expected to weaken once we get into the fall. Industrial production probably won’t impress given the weakness we saw with the PMI readings. On Wednesday, both building permits and housing starts should show some weakness. Thursday’s releases include jobless claims which might only show modest labor market sluggishness and some weaker existing home sales.

Eurozone

President Christine Lagarde’s comments at the ECB conference in Frankfurt on Monday may be the highlight next week as traders try to better understand whether the central bank is as close to the end of its tightening cycle as they think. The ECB has pushed back before but the data is looking on a much better trajectory. Final HICP inflation figures will also be released on Wednesday.

UK

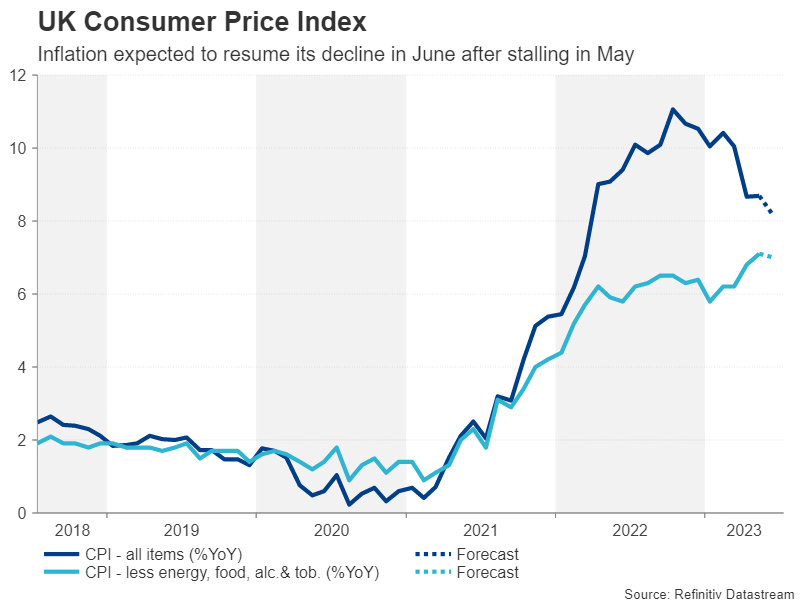

UK inflation data on Wednesday is undoubtedly the one to watch next week. It seems we’re seeing progress on inflation everywhere except the UK at the moment. The headline is expected to fall back to 8.2% for June, with core staying at 7.1%. But both have surpassed expectations on numerous occasions recently as inflation has remained stubbornly high. Are better readings from the US and eurozone a sign of things to come for the UK, finally? Retail sales will also be released on Friday.

Russia

The Russian central bank is expected to hike the key rate by 50 basis points on Friday, taking it back to 8%. This comes as inflationary pressures are building and the rouble has been falling against the dollar. It hit its lowest level since March last year, recently, which is also more than 10% below its pre-invasion levels.

South Africa

The SARB is expected to leave its repo rate unchanged next week at 8.25% after what has been a very aggressive tightening cycle. It’s risen 4.75% since September 2021 but with inflation now close to target – fresh data for June will be released a day earlier on Wednesday – the time to pause may have arrived. Of course, a nasty shock from the CPI could change that.

Turkey

The CBRT will announce its latest interest rate decision on Thursday and another wide range of forecasts are likely ahead of the event. The central bank broke away from the unconventional policy approach adopted prior to the election and almost immediately abandoned after, so a large hike is likely on the cards. But the new CBRT Governor was more conservative than many expected at the last meeting and could be again this time. The lira remains near record lows though so the pressure is on.

Switzerland

No major releases or events next week.

China

The housing price index (new home prices) for June will be released this Saturday, and it will be closely watched to monitor the financial health of Chinese property developers that are still suffering from a bout of debt overhang due to overleveraging in the past 5 years. In the prior month of May, average new home prices have managed to inch up 0.1% year-on-year after consecutive months of contractions since April 2022.

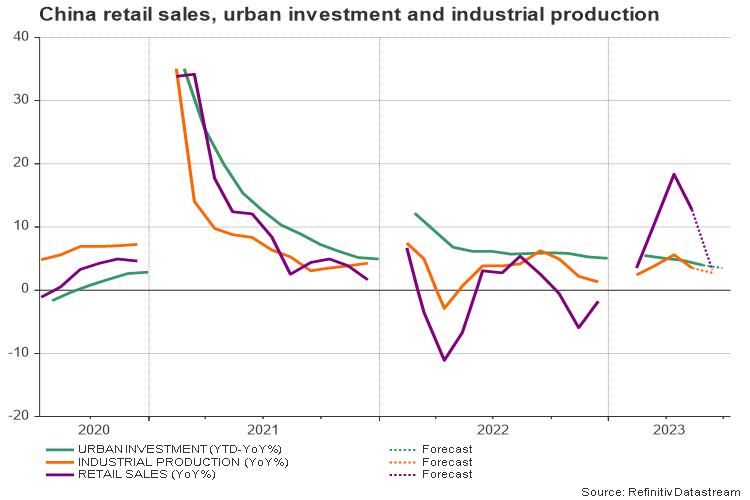

On Monday, we will have the release of Q2 GDP, industrial production, retail sales, and unemployment data. Retail sales and the youth unemployment figures will be pivotal for gauging the current state of internal demand which has been lackluster since March. Growth in retail sales for June is expected to plummet to 3.2% year-on-year from 12.7% recorded in May. On the labor market front, the youth unemployment rate surged to a record high of 20.8% in May, that’s about four times above the nationwide unemployment rate.

On Monday, China’s central bank, the PBoC will decide on its one-year Medium-Term Lending Facility Rate (currently at 2.65%) followed by Thursday’s decision on the one-year and five-year Loan Prime Rates (currently at 3.55% and 4.20%, respectively).

Given the latest policy pledge by PBoC to stabilize growth via utilizing its arsenal of monetary policy tools, there is a possibility that another round of interest rate cuts may be implemented in the coming week.

India

No major key data releases.

Australia

The RBA minutes of the last monetary policy meeting held on 4th July will be released on Tuesday. Market participants will be scrutinizing the details of the minutes for hints on whether the current official cash rate of 4.1% is the terminal rate for the current tightening cycle after the RBA chose to stand pat on 4th July. Based on the RBA Rate Indicator as of 14th July, the ASX 30-day interbank cash rate futures for the August 2023 contract has priced in a 29% probability of a 25-bps hike to bring the cash rate to 4.35% at the next monetary policy decision on 1st August; that’s a decrease in odds from 52% seen in a week ago.

Labor market conditions for June will be out on Tuesday; employment change is expected to be lower at 17,000 versus 75,900 in May while the unemployment rate is expected to hold steady at 3.6%.

New Zealand

Q2 inflation data is due out on Wednesday. Expectations are for a cooler print of 5.9% year-on-year from 6.7% printed in Q1. On a quarter-on-quarter basis, it is expected to slide to 0.9% from 1.2% in Q1. If this cooler consensus turns out as expected, it will be the second (y/y) and third (q/q) consecutive quarters of an inflationary growth slowdown.

Japan

Balance of trade data for June is due out on Thursday; growth in exports is expected to improve to 2.2% year-on-year from 0.6% in May while imports are expected to deteriorate further to -11.3% year-on-year from -9.9% in June.

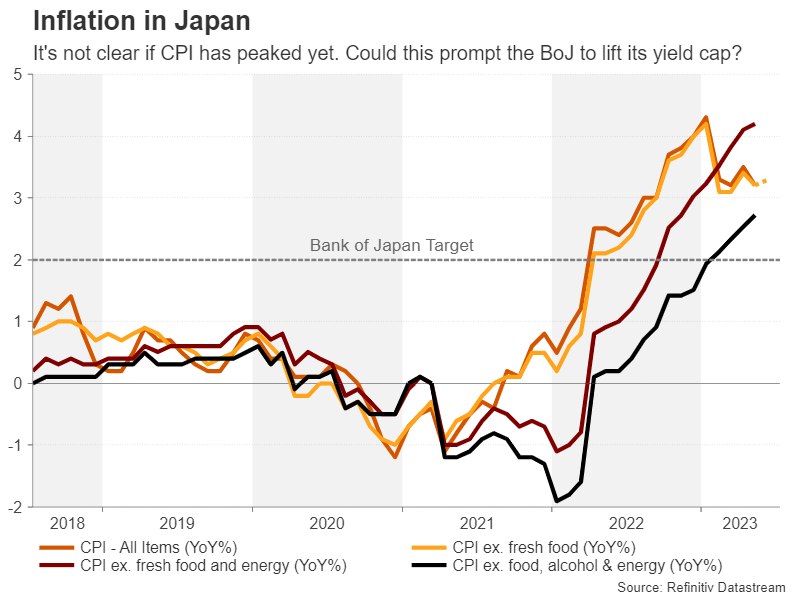

Inflation data will then be released on Friday. The core inflation rate for June is expected to tick slightly higher to 3.3% year-on-year from 3.2% in May while June’s core-core inflation rate (excluding fresh food & energy) is expected to remain at an elevated sticky level of 4.3% year-on-year in May. If these inflationary prints come in as expected, it is likely to put more pressure on the Bank of Japan to bring forward monetary policy normalization, a tilt away from the current ultra-dovish stance.

Singapore

The key data to note will be the balance of trade for June to be released on Monday; non-oil exports growth declined to -14.7% year-on-year in May, its 8th consecutive month of contraction. Another weak reading is expected for June due to a weak external environment, especially from China, one of its major trading partners.

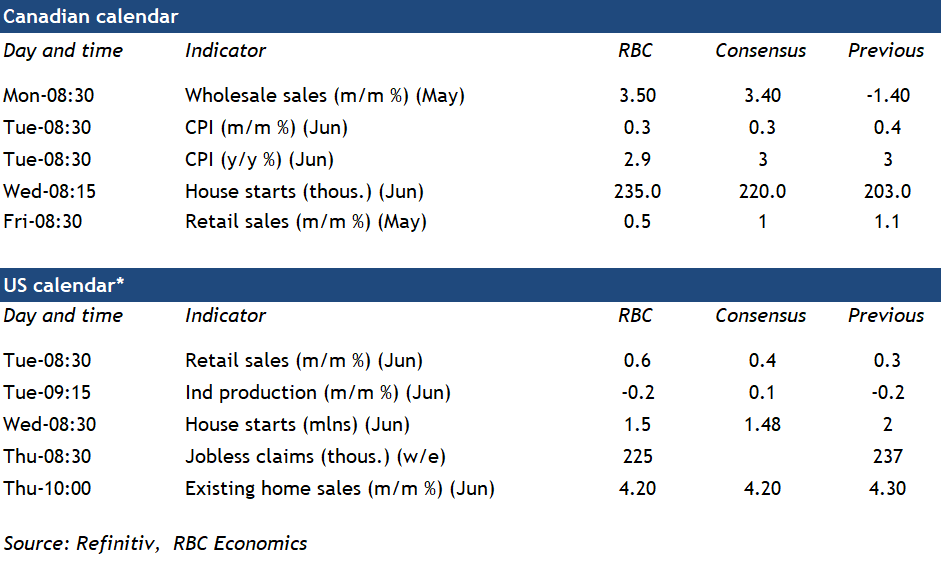

Canadian CPI Growth to Fall to Top End of BoC Target Range in June

Canada’s June CPI release will come on the heels of a downside surprise in the U.S. inflation data that lowered the odds of additional Federal Reserve interest rate hikes beyond a widely expected July increase. Year-over-year growth in Canadian CPI also looks set to decelerate substantially – we expect to see a 2.9% rate in June, down from 3.4% in May and just below the top end of the Bank of Canada’s 1% to 3% target. That marks a dramatic slowdown from a peak rate of 8% a year ago. Much of that slowing has come from lower energy prices. Gasoline prices were running 20% below year ago levels in June after surging last year on higher oil prices. Mortgage interest costs have continued to surge (a record +30% year-over-year as of May.) Food prices will not outright decline but the rate of growth in grocery prices has been decelerating in recent months.

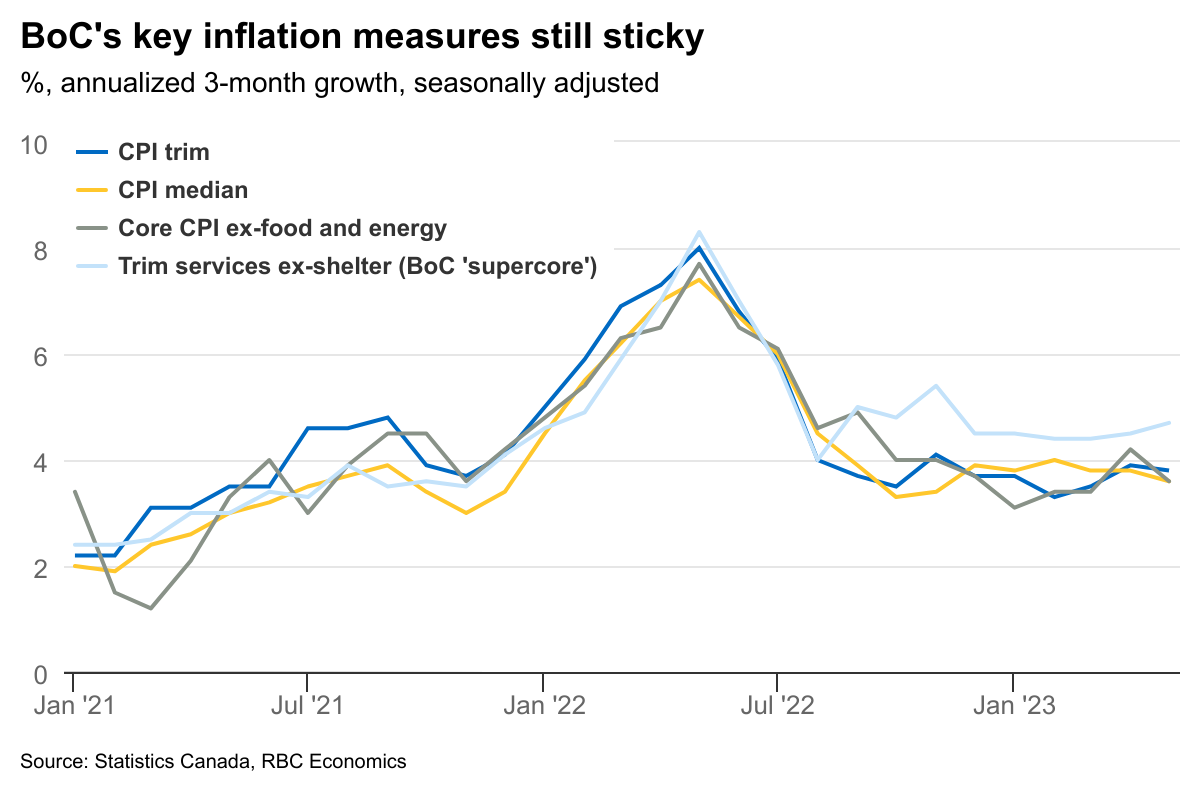

But the BoC will be focused on more recent month-over-month growth in the range of ‘core’ measures designed to provide a better gauge of underlying broader inflation pressures. And growth in those has been stickier at rates still above the BoC target. The BoC’s preferred median and trim CPI measures have been tracking in the range of 3 ½% to 4% at an annual rate and core services excluding shelter (BoC ‘super-core’) has been running closer to 5%.

Consumer demand is still firm – particularly for discretionary services heading into the busy summer travel season. And home resale markets are once again adding to price growth as existing home prices start to edge higher after declining last year. The BoC won’t hesitate to hike interest rates again if that momentum in spending persists. However, interest rate headwinds continue to build. The household debt service ratio very likely hit a new record high in Q2, leaving households vulnerable to any deterioration in labour markets. And the unemployment rate edged higher in May and June. We continue to expect broader inflation pressures will slow enough to prevent additional interest rate hikes from the central bank.

Week ahead data watch

StatCan’s early indicator showed the “core” wholesale sales (excluding petroleum products) increased by 3.5%, sales in the miscellaneous sector added to most of the growth in May, offsetting the decrease in farm product sales.

Canadian housing starts likely bumped up from 203K in May to 235 in June. Permits issuance has been slowing, but the 3-month rolling average of permits issuance was still running at 250k – above the level of May starts and implying more building activity in the pipeline.

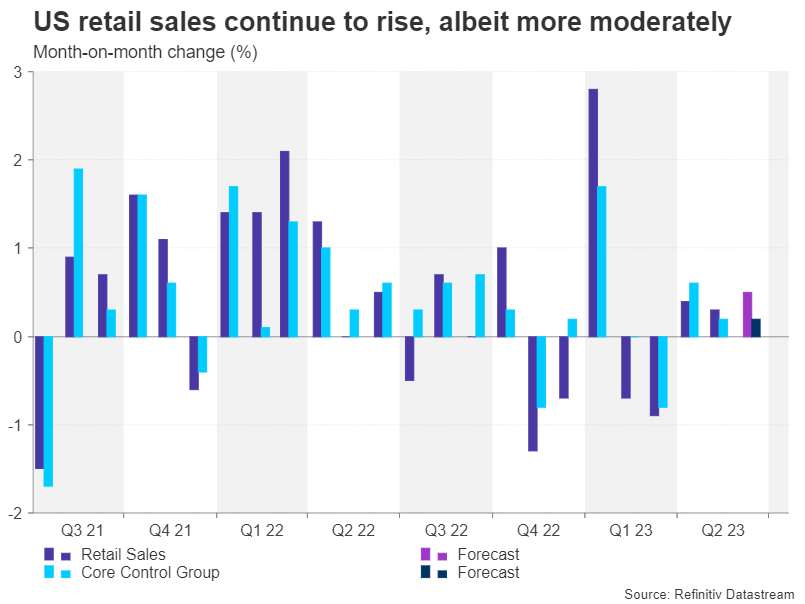

U.S. retail sales likely ticked up 0.6% in June, thanks to a boost in auto sales during that month. We expect ex-auto sales were little changed at +0.1% on a month-over-month basis, supported by a price-related increase in gasoline station sales.

We expect a dip (-0.2%) in June’s industrial production in the U.S., due to declines in utility sector output (fewer cooling days than normal).

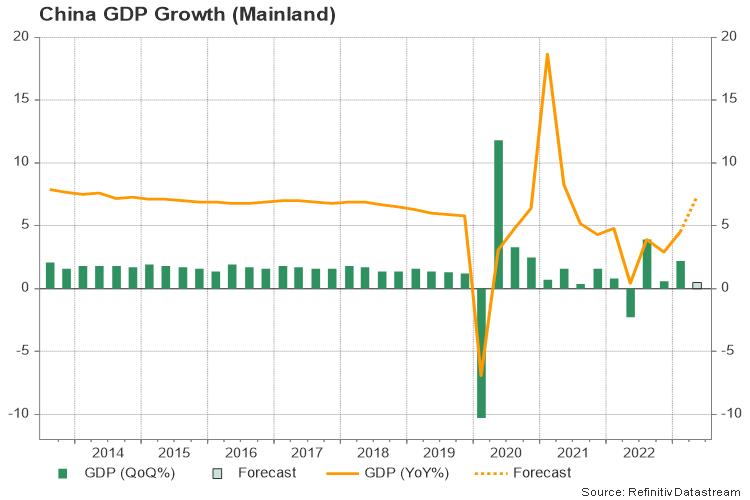

Will China’s Q2 GDP Data be the Next Bull Catalyst in Markets?

While China is having another power battle in the artificial intelligence field against the US, economists are still hoping for the second biggest economy to bolster global growth as recession fears in the rest of the world persist. Monday’s Q2 GDP growth figures could bring some cheer to investors, likely showing the fastest expansion in two years.

Q2 GDP growth expected to pick up pace

China's post-lockdown growth was not satisfactory to investors, despite a 4.5% y/y expansion. Traders saw the glass half empty after Chinese officials admitted that “foundation for economic recovery is not solid yet”, while pointing to low base effects for another rosy quarter ahead.

Indeed, given the bleak economic picture in Q2 2022 in the face of pandemic constraints, base effects have probably produced a whopping 7.3% GDP growth in the April-June 2023 period according to forecasts. This is far above the government’s 5.0% expansion target for 2023 and could be good news to investors, who have been long waiting for China’s reopening to bolster global economic activity.

Challenges remain

However, quarter-on-quarter expansion is expected to slow down significantly to 0.5% from 2.2% previously, suggesting that the second quarter did not add much value to the domestic output.

June’s trade report was the latest evidence to cast a shadow on China’s economic strength earlier this week. Exports surprised to the downside, marking their largest decline of 12.4% y/y. Imports stayed negative for the seventh consecutive month, indicating a broken relation with external markets as geopolitical conflicts persist and top trade partners suffer from inflation and recession risks. In detail, Chinese demand for raw materials and semiconductors, which are a key component for the booming AI technology, plummeted in double digits.

Consumer-driven recovery is not sufficient either, making retail sales data important to watch on Monday too. Estimates point to a sharp pullback from 12.6% y/y to 3.2% y/y, with analysts in JPMorgan, Goldman Sachs and S&P projecting a fading pent-up demand to further weigh on consumption during the upcoming quarters.

Deflation is another reflection of dampened demand. While central banks in developed economies are battling stubbornly high inflation through higher interest rates, China is on the opposite side of the river, with the People’s Bank of China cutting several lending rates in June, albeit marginally, to bolster consumer confidence and therefore boost price pressures. The headline CPI inflation has been falling at a steady pace over the past five months, suggesting that more forceful stimulus measures are needed.

The government has been refraining from providing direct cash to consumers, implementing tax policies and fee cuts instead to support the economy throughout the pandemic. As pledged in January, the ministry of finance will expand its expansionary fiscal policy this year, especially in the property market, where investment is still diminishing. Yet, the government's bond issuance has been lower than last year expected to bring the total quota to 3.85 trillion yuan compared to 4 trillion yuan in 2022.

Market reaction

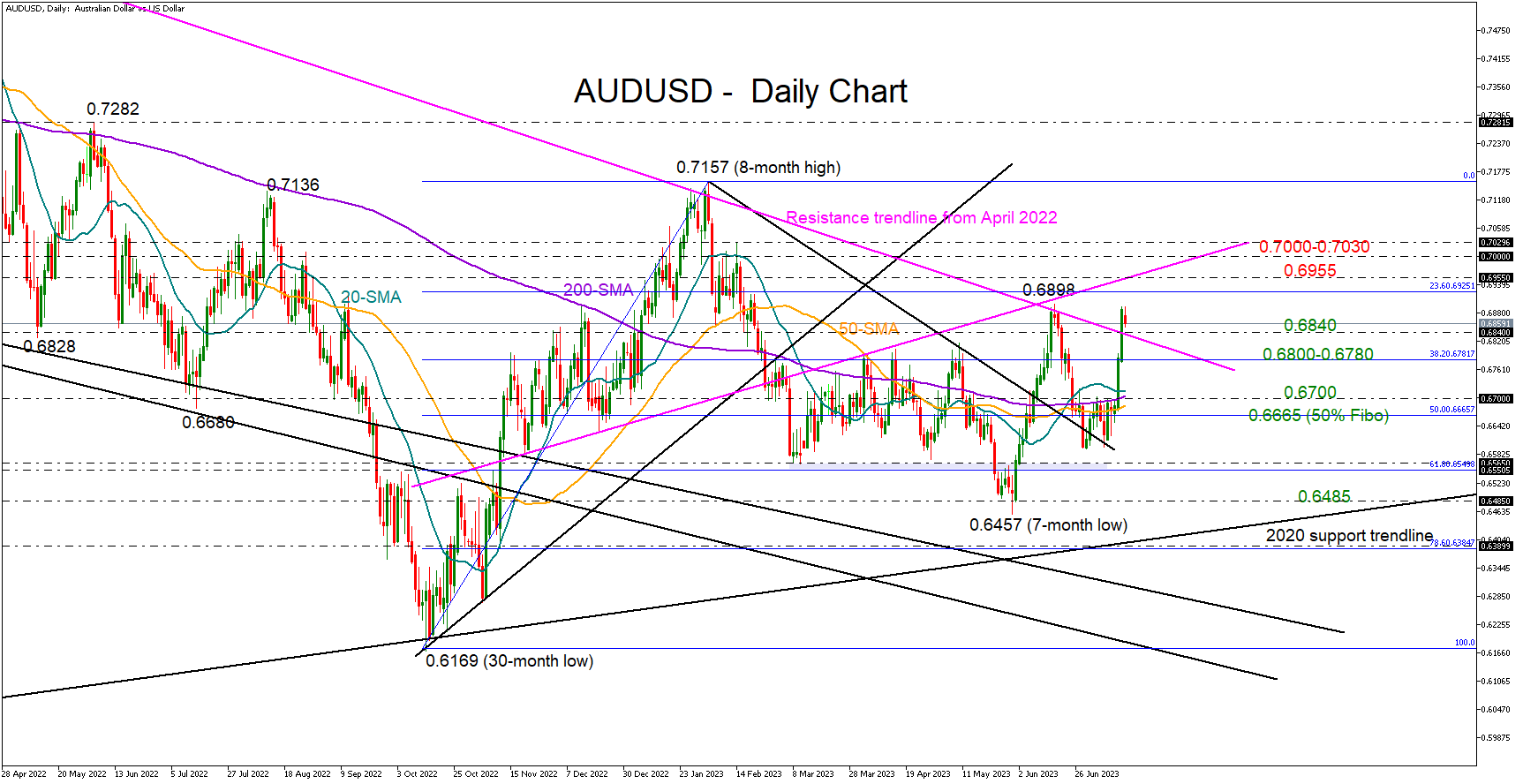

Perhaps delayed effects ahead and heightened fiscal debt levels are holding back dynamic support measures for now. Nevertheless, although the months ahead could be challenging given the rising unemployment rate and an uncertain geopolitical environment, potential headlines of new stimulus in China could bode well for risk-sensitive and commodity currencies such as the Aussie given that 32% of Australia’s exports are delivered in China.

Stronger-than-expected GDP data could boost global sentiment and specifically commodity currencies, including the yuan sooner next week, but the reaction could be measured as the second half of 2023 could provide a better picture of China's economic outlook. In FX markets, AUDUSD could extend its bullish wave towards the 0.6955 resistance area. The 0.7000 psychological mark and the February 14 peak of 0.7028 could next attract attention.

Alternatively, given the optimistic GDP forecasts, a downside surprise cannot be ruled out. A reading below the government’s 5% growth target could weigh significantly on AUDUSD, pressing the pair back to the 0.6800-0.6780 zone, if the broken resistance line gives way at 0.6840. Even lower, the simple moving averages (SMAs) will next attempt to pause the sell-off around 0.6700.

Week Ahead – Focus on China GDP and US Retail Sales, More CPI Data on Tap

Inflation data will continue to dominate the economic agenda in the coming week, although the spotlight will probably fall on Chinese GDP figures as well as US retail sales. The countries reporting CPI numbers include Canada, New Zealand, Japan and the United Kingdom. With inflation seemingly coming under control in America, investors will be on the lookout for any divergence in other countries’ progress. However, sentiment will likely be shaped by growth indicators from the world’s two largest economies as both desperately try to avoid a recession.

Chinese GDP rebound could mask cracks below the surface

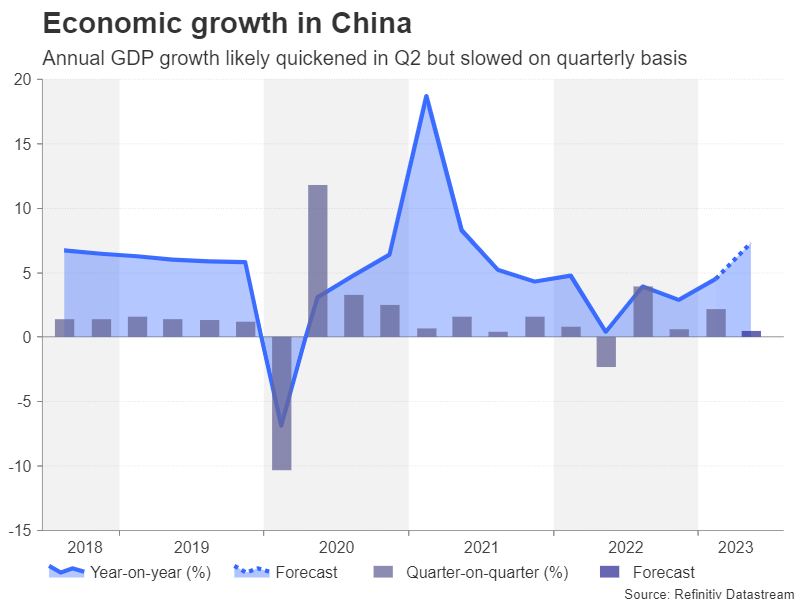

China is rarely out of the headlines these days amid persisting fears that the economic recovery is faltering and doubts about how far the government is willing to go to pump more stimulus. On Monday, when the second quarter GDP estimate is reported, investors will likely breathe a sigh of relief, at least initially.

The economy is expected to have expanded by 7.3% year-on-year, which would make it the fastest growth since the second quarter of 2021. However, GDP shrank in the same quarter of 2022 so this would flatter the annual comparison. Moreover, on a quarterly basis, growth is projected at just 0.5%, which is below China’s average and well below the pace that is needed to achieve yearly growth of around 5% that the government is aiming for.

The underlying weakness will also likely be on full display in the monthly prints on industrial output and retail sales. Industrial production growth is forecast to have slowed from 3.5% to 2.7% y/y in June, and retail sales from 12.7% to 3.2% y/y.

The elusive stimulus

Investors have become somewhat frustrated lately from the lack of policy response from Chinese authorities to tackle the slowdown. The measures announced so far have been very targeted and a large-scale stimulus does not appear to be on the cards. The People’s Bank of China cut its loan prime lending rates last month for the first time since August 2022, and even though it was only by 10 basis points, a further cut is not very probable when it meets again on Thursday.

The incremental steps to boost growth have failed to set markets alight, but the soft CPI report out of the United States has given investors something to cheer about. In light of that, a stronger-than-expected GDP reading could add fuel to the risk rally, whereas if it disappoints, risk-sensitive currencies such as the Australian dollar as well as equities could come under selling pressure.

The aussie has already gained more than 4.0% in July so a lot is at stake if the US CPI-led euphoria evaporates. Aussie traders will also be watching domestic employment numbers on Thursday in addition to the minutes of the RBA’s July policy decision on Tuesday when the Bank went back into pause.

US data will have a hard time lifting the dollar

A central bank that will likely ‘unpause’ at its next meeting is the Federal Reserve. There seems to be a strong consensus among Fed officials that some further tightening is still required. But after the downside surprise in CPI, markets are more convinced than ever that a July hike would be the last. More crucially, investors have ramped up their bets of aggressive rate cuts in 2024, hammering the US dollar in the process.

It’s therefore going to be tough for next week’s US releases to switch those expectations around, meaning the dollar’s woes might not lessen anytime soon.

The data flurry will begin on Monday with the Empire State manufacturing index, followed by retail sales and industrial production on Tuesday. Growth in retail sales is expected to have quickened slightly to 0.5% month-on-month, suggesting consumer spending remains healthy while the summer season is in full swing.

Building permits and housing starts are due on Wednesday, with existing home sales coming up on Thursday, along with the Philly Fed manufacturing index. The US housing market is displaying some tentative signs of a recovery and a further indication of that next week might aid the greenback claw higher.

Will UK CPI resume its decline?

One of the currencies riding high on the back of the dollar’s drubbing is the pound. The British currency has stormed above the $1.30 level for the first time since April 2022. However, the rally will be put to the test on Wednesday when the latest UK inflation figures are published.

The consumer price index has repeatedly beaten expectations this year, causing a headache for the Bank of England. The most striking feature of the UK’s stubbornly high inflation problem is that core CPI has yet to peak after almost 500 basis points of rate increases.

There might be some reprieve for policymakers, though, if inflation drops to 8.2% y/y in June as expected from 8.7% in the prior month. Core CPI is projected to moderate too, but only negligibly to 7.0% y/y.

Retail sales data due Friday will also be watched.

Having already jumped by over 3.0% in July alone, the pound is at risk of a sharp correction should the CPI numbers miss the forecasts for once. However, even in this scenario, sterling’s prospects would remain significantly more bullish than its peers’ as the Bank of England would still have a longer tightening path ahead of it than other big central banks like the Fed and ECB.

Japan, New Zealand and Canada awaiting CPI reports too

The Reserve Bank of New Zealand kept its cash rate on hold at its July meeting, signalling that rates have likely peaked. The quarterly CPI readings out Wednesday are anticipated to support that decision as inflation is forecast to have fallen from 6.7% to 5.9% y/y in the three months to June.

But like the pound, the perked-up New Zealand dollar is in danger of a pullback should inflation decline more than expected.

The Bank of Canada on the other hand decided to raise interest rates this week and kept the door open to more. However, with inflation hitting a two-year low of 3.4% in May, investors are unsure if the BoC will hike again.

On Tuesday, the June CPI numbers are due and may stir things up for the Canadian dollar if BoC bets are blown in a particular direction.

The inflation releases will wrap up on Friday in Japan where speculation is growing about a possible tweak in policy by the Bank of Japan. Friday’s data could be important in helping policymakers make up their minds if they should lift or remove the upper limit on the 10-year JGB yield.

Headline and core CPI appear to have plateaued in Japan but the so-called ‘core core’ rate continues to climb. Thus, any upside surprises in the June figures could fuel speculation of a July move, boosting the Japanese yen, which is having its best week since November last year.

Sunset Market Commentary

Markets

Market activity shifted into a lower gear today after an impressive bond market rally since end last week fired impressive gains across multiple assets categories. Compared to the (intraday) peak levels end last week, the US 2-y and 10-y yield respectively dropped from 5.12% to 4.68% and from 4.09% to 3.78%. After a ‘hawkish tendency’ with investors selectively focusing on stronger than expected (even secondary) data, they all at once saw the glass again half empty. Mixed payrolls and slightly softer than expected US CPI rekindled hopes that the Fed would reconsider a pause or even an end to its hiking cycle after an ‘inevitable’ 25 bps step on July 26. Fed communication at least didn’t change and won’t change as Fed governors enter the ‘black-out’ period ahead of the upcoming policy meeting. German 2 & 10-y yields in the meantime declined from 3.35 % to 3.17% and from 2.68% to 2.48% as the ECB has more work to do in its anti-inflation campaign. US yields today regain between 5.5 bps (2-y) and 0.5 bps (30-y). The German 2-y yield adds 3 bps with the 30-y unchanged. Given the wild swings recorded earlier this week this basically no more than consolidation. Even so, equites still don’t budge. Equity investors see a decent chance for a soft landing with corporates maintaining a decent degree of price power. First US banking results released today were stronger than expected and didn’t provide much of a reason to reduce equity long exposure (EuroStoxx 50 +0.4% and testing the cycle top near 4420). The S&P 500 opens 0.25% higher, recording a gain of about 2.25% over the previous 5 days. The dollar got hammered across the board. DXY tumbled more than 3.5% from a peak near 103.5 on Thursday last week to currently changing hands just below the 100 barrier. EUR/USD (1.122) in the reference period jumped slightly less than 4 big figures, easily clearing the YTD top of 1.1095. It probably needs quite a set of stronger than expected US data to put a solid floor for the US currency. Today being the exception, the yen was one of the major beneficiaries of the USD sell-off. USD/JPY dropped from the high 144 area late last week to fill bids below 137.5 in Asia this morning (currently 138.75). Aside from the overall USD-correction markets ponder the chance for the BOJ tweaking its YCC, maybe already at the end of July meeting. In a broader perspective, the weaker dollar was a blessing for most smaller currencies (SEK, NOK, CHF, CAD, AUD, NZD). In central Europe, the forint profited most (EUR/HUF 374). The zloty (EUR/PLN 4.445) consolidates but is still within reach of the cycle top near EUR/PLN 4.41. It might sound a bit contradictory, but easing inflation fears at the same time triggered some kind of ‘reflationary’ rebound in cyclical commodities, including oil, but also the likes of copper.

News & Views

Swedish June inflation again surprised on the upside. Headline CPI (using a fixed mortgage rate) rose 0.9% m/m to be up 6.4% y/y. While easing from May, it was more than the 6% expected. A core gauge filtering for energy came in at 0.6% m/m and 8.1%, topping a 0.5% and 7.9% estimate. Both measures also surpassed the Riksbank’s June forecasts, keeping high pressure on the bank to tighten further, especially with the krone still at historically weak levels. At the June meeting it said it will increase rates “at least one more time this year” from 3.75% to 4%. The Riksbank at the same time is walking a tightrope with a higher rated impacting the country’s vulnerable property sector and potentially triggering knock-on effects to the broader economy. This helps explain the SEK’s dreadful performance over the past few months. Case in point: the SEK today loses out against the euro even as Swedish yields rise more than 4 bps vs minor losses in Germany/Europe. EUR/SEK trades 11.51, up from 11.44 at the open.

The Eurozone’s non-seasonally adjusted trade balance almost turned green in May, Eurostat data showed. The deficit narrowed to -0.3bn, significantly less than the €-11.7bn in April and vastly better than the €-30.3bn in May last year. The ongoing improvement came on the account of increased exports of chemicals and machinery while the value of imported energy products, especially from Russia, declined. Total exports in May stood at €241.9bn vs €242.2bn in imports. For the running year, euro area exports to the rest of the world rose to €1181.9bn in January-May (+3.7% compared to the same period in 2022), while imports fell to €1199.5bn (-5.1%). This led to a running deficit of €-17.6bn compared to the €-124.7bn in Jan-May 2022.