Sample Category Title

(RBNZ) Official Cash Rate remains on hold

The Monetary Policy Committee today agreed to leave the Official Cash Rate (OCR) at 5.50%.

The level of interest rates are constraining spending and inflation pressure as anticipated and required. The Committee agreed that the OCR will need to remain at a restrictive level for the foreseeable future, to ensure that consumer price inflation returns to the 1 to 3% annual target range, while supporting maximum sustainable employment.

Global economic growth remains weak and inflation pressures are easing. This follows a period of significant monetary policy tightening by central banks internationally. Global inflation rates continue to decline, assisted by the normalisation of international supply chains, and the decline in shipping costs and energy prices. The weaker global growth has led to lower export prices for New Zealand's goods.

In New Zealand, inflation is expected to continue to decline from its peak, and with it measures of inflation expectations. Core inflation is expected to decline as capacity constraints ease. While employment is above its maximum sustainable level, there are signs of labour market pressures dissipating and vacancies declining.

Consumer spending growth has eased and residential construction activity has declined, while house prices have returned to more sustainable levels. More generally, businesses are reporting slower demand for their goods and services, and weak investment intentions.

The return of net inward migration continues broadly as anticipated, and is assisting to ease labour shortages. The net impact of immigration on overall capacity pressures remains uncertain. The ongoing recovery in tourism spending is supporting demand.

The repair and rebuild underway in regions of the North Island due to severe weather events will support economic activity in the near term. Broader government spending is anticipated to decline in inflation-adjusted terms and in proportion to GDP.

The Committee is confident that with interest rates remaining at a restrictive level for some time, consumer price inflation will return to within its target range of 1 to 3% per annum, while supporting maximum sustainable employment.

Record of meeting July 2023

The Monetary Policy Committee discussed recent developments in the New Zealand economy. The Committee agreed that monetary conditions are restricting spending and reducing inflationary pressure as anticipated. However, inflation remains too high. Spending needs to remain subdued to better match the economy's ability to supply goods and services, so that consumer price inflation returns to its target range of 1 to 3%. Supply capacity constraints in the economy continue to ease.

Global economic growth remains below trend for most of our trading partners, partly as a result of significant monetary policy tightening by central banks internationally. Global growth is expected to weaken further. Economic growth is moderating more rapidly in China, with recent data suggesting a slowing in economic momentum.

Headline inflation has continued to fall in most countries, assisted by lower energy prices and a normalisation of international supply chains and shipping costs. However globally, core inflation remains high. This has prompted some central banks to further increase interest rates recently. In discussing recent central bank policy moves, the Committee noted that monetary policy in New Zealand reached a more restrictive level earlier than in many other economies.

The Committee discussed domestic economic developments. Recent data suggest that tight monetary conditions are constraining domestic spending as expected. Residential building activity has started to ease and falling consent numbers suggest it will continue to slow. Economic activity contracted slightly in the March 2023 quarter. Recent indicators suggest that growth is likely to remain weak in the near term, despite some support from repair and rebuild work underway in regions of the North Island due to severe weather events. Broader government spending is anticipated to decline in inflation-adjusted terms and in proportion to GDP.

Labour shortages have started to ease, partly in response to the recent arrival of more migrants. Firms report that it is becoming easier to find labour and economy-wide vacancy rates have fallen.

The Committee judged that after recent falls, house prices are now around sustainable levels. House prices have stabilised in recent months and the Committee noted that the outlook for the housing market has become more balanced. Higher net migration is supporting demand for housing but higher interest rates continue to exert downward pressure on housing demand.

The Committee agreed that there is no trade-off between meeting the Committee's inflation and employment objectives and maintaining the stability of the financial system. Debt levels are high in some parts of the economy, and pockets of stress are emerging. However, early indicators point to only a moderate increase in stressed lending over the coming months and non-performing loans remain at very low levels.

In discussing their Remit objectives, the Committee noted inflation is still expected to decline within the target band by the second half of 2024. The Committee discussed risks to the persistence of domestic inflation pressures and imported inflation and judged that the risks around the inflation projection were broadly balanced. Employment remains above its maximum sustainable level, however recent indicators suggest that labour market conditions are easing.

The Committee noted that monetary conditions have continued to tighten with mortgage rates increasing further in recent months in response to higher wholesale rates. The Committee noted that bank term deposit rates had increased recently, broadening the transmission of tighter monetary policy. The lagged effects of previous monetary tightening is still passing through to households as more households move off lower fixed rates. Average mortgage rates on outstanding loans have increased from about 3% in early 2022 to about 5% currently. Based on current commercial bank pricing, average mortgage rates are expected to reach around 6% in early 2024.

The Monetary Policy Committee discussed the appropriate stance of monetary policy. The Committee agreed that interest rates will need to remain at a restrictive level for the foreseeable future, to ensure consumer price inflation returns to the 1 to 3% target range while supporting maximum sustainable employment.

On Wednesday 12 July the Committee reached consensus to leave the Official Cash Rate unchanged at 5.5%.

Technicals and Triggers – USD/JPY, GBP/USD, GBP/JPY, USD/MXN

FX volatility might be returning given Wall Street is seeing some exhaustion with several key currency trades. The end of tightening for the advance economies keeps getting delayed and sooner than later it will deliver a major blow to growth. FX volatility should pick up as diverging policies from the Fed, BOE, and PBOC could trigger some significant moves in H2.

USD/JPY

A lot of macro traders were expecting dollar strength to intensify against the Japanese yen as interest rate differentials appear likely to widen further over the next few months. The carry trade isn’t making a comeback given the rising prospects of a recession coming to the US. Everyone also remains on intervention watch from Japan’s Ministry of Finance, but expectations are for action if dollar-yen tests the 150 region. The consensus on Wall Street is that Japan will probably act, but it might not happen until after the summer. A tweak to yield curve control could trigger yen strength but that won’t happen until the BOJ’s price goal is achieved. BOJ Governor Ueda has been clear that no tweaks will occur until the prospects heighten for inflation to sustainably reach its 2% target.

USD/JPY weakness towards 140 has triggered some buyers and that might gain momentum if risk appetite can remain throughout tomorrow’s US inflation report (Wednesday 830am est). Further upside could eye a return to the 145 zone if risk aversion does not run wild post both Wednesday’s CPI reading and Friday’s bank earnings.

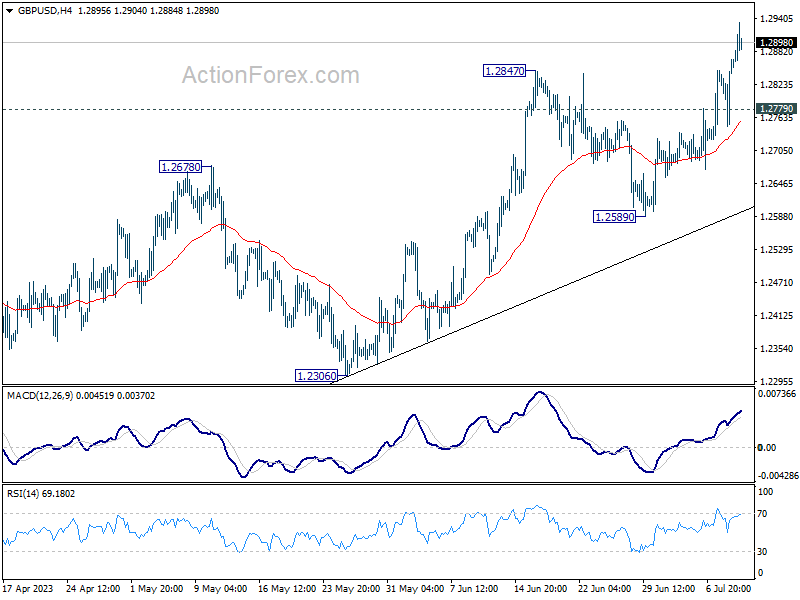

GBP/USD

GBP/USD (4-hour chat) has been in a general rally for the past two days, but that could be coming to an end if a bearish butterfly pattern forms. The headlines have been mostly bullish for the pound, but that could be reaching an inflection point. Inflation is forcing the BOE to be extremely hawkish and that could soon lead to a significant economic downturn. Many traders are focusing on today’s UK wage growth, as it posted the biggest rise outside the pandemic period, but jumps in jobless claims suggest the labor market is cooling.

If the pound-dollar bullish trend respects the psychological 1.3000 resistance, some bullish bets might get taken down. The four-hour GBP/USD is displaying a potential bearish butterfly pattern. If this technical reversal pattern holds, a moderate decline could see downward momentum target the 1.2800 region. If a dramatic move triggers a rally above the 1.3000 level, the bearish reversal pattern could be invalidated. Further upside targets include the 1.3250 region.

GBP/JPY

The British pound has appreciated over 18% to the Japanese yen this year as stubborn inflation has bolstered the odds of aggressive central bank tightening by the BOE. Pound-yen has steadily gathered strength in the first half of the year but exhaustion could be settling in. The pound initially rallied earlier in London after weekly hourly earnings came in scorching hot, which should raise the prospects of a half-point rate hike at the August 3rd BOE meeting. The pound may get a major boost against the dollar if it can extend above the 1.30 level, but for some traders it is looking toppish against the yen.

GBP/JPY may have a decent pullback if continued bearishness takes price below the bullish trendline that has been in place since March. Pound downside momentum could target 176.50 against the yen if the bullish trend line (around the 179.75 ) is invalidated.

Key resistance currently resides around the 184.20 level.

USD/MXN

The Mexican peso is one of top-performing currencies of the year and that trade is starting to lose momentum. The interest rate differential (Banxico overnight rate stands at 11.25%) and robust economic growth prospects have made the peso a very attractive trade this year. A weakening global growth outlook however will start to dampen prospects for EM currencies. Emerging markets need their key trading partners to thrive and China’s disappointing economic recovery is triggering some profit-taking.

USD/MXN has major support at the 17.00 level and if a rebound emerges, upside could target the 50-day SMA around the 17.45 level. Given the softening outlook for the next year, peso weakness to the dollar could eventually target the 20.00 level.

Gold – Edging Higher Ahead of US Inflation Report

Gold appears to have found some support again in recent days after rebounding twice around $1,900.

The US jobs report was one possible risk event that could have triggered a big move in gold, one way or another, and the other is due tomorrow in the shape of the US inflation report.

It seems gold bulls are feeling a little more confident, although $1,940 still poses a test having been a notable area of support in late May and the first half of June.

Gold

Source – OANDA on Trading View

We could just be seeing a corrective move after such a strong pullback from the highs in May, although a strong inflation number again tomorrow could send it lower once more.

If we do see a move above $1,940, the next levels that stand out are $1,960 and $1,980 which coincide with the 38.2% and 50% Fibonacci retracement levels, respectively.

If this is just a corrective move as part of a deeper decline, these may be viewed as possible rotation zones, especially falling around the 55/89-day simple moving average band.

Further above, the 61.8 fib level falls at $2,000 which is a major psychological barrier and as we’ve seen previously, a notable level of support and resistance.

Of course, gold hasn’t traded around here too much in its history but we can see that between March and May, the price was responsive to the level.

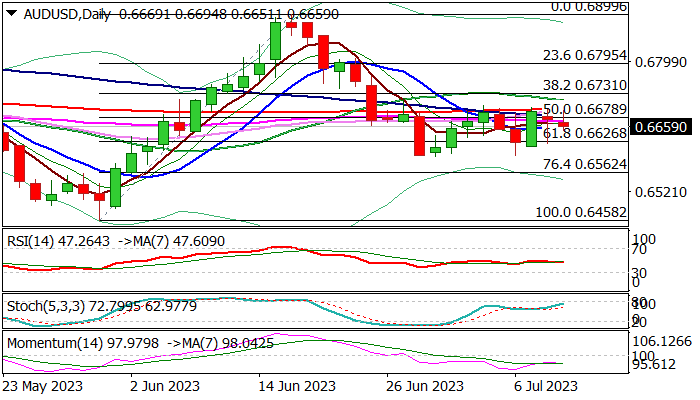

AUD/USD: Multiple Upside Rejections at 200DMA Keep the Downside at Risk

Australian dollar edged lower on Tuesday, pushing towards the mid-point of near-term range (0.6595/0.6705) after 200DMA (0.6697) again capped upside attempts, fueled by improved Australian Jun consumer sentiment and business confidence data.

Strong offers at 0.6700 zone keep the Aussie dollar pressured and define near-term consolidation range, with bearish technical picture on daily chart keeping the downside at risk for now.

Decline of 14-d momentum deeper into negative territory, adds to bearish near-term outlook, though scenario still looks for confirmation on penetration of daily cloud (cloud top lays at 0.6638) to open way for attack at range base (0.6595) and signal continuation of larger downtrend from 0.6899 (June 16 peak) on firm break lower.

Only sustained break above 200DMA would sideline larger bears and possibly allow for stronger recovery.

Res: 0.6678; 0.6697; 0.6711; 0.6747.

Sup: 0.6650; 0.6626; 0.6595; 0.6562.

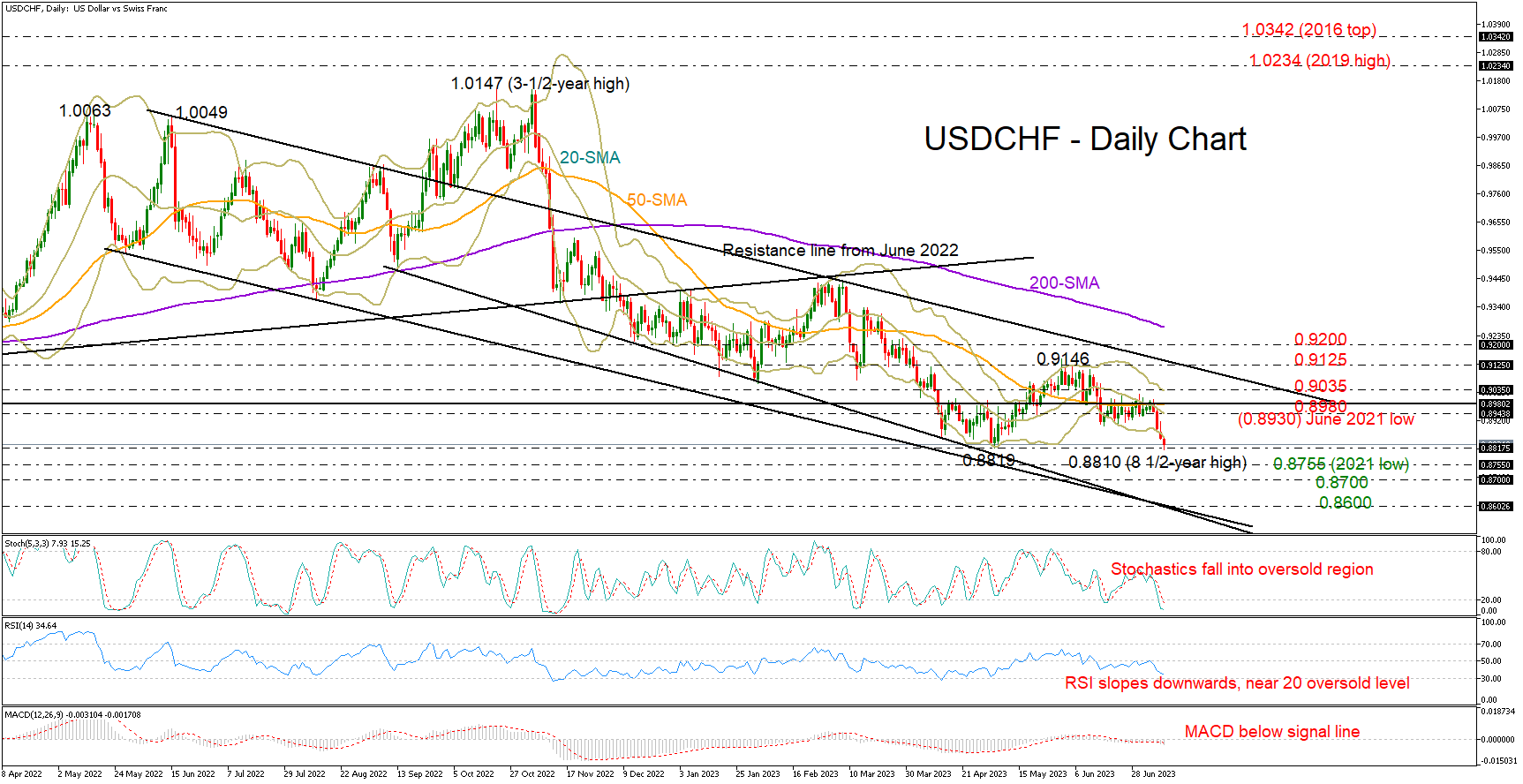

Will USDCHF Get Back on a Downtrend?

USDCHF went downhill to print an eight-and-a-half year low of 0.8810 slightly below May’s trough on Tuesday after getting rejected near its 20-day simple moving average (SMA).

Another leg down is possible as the RSI and the stochastic oscillator have yet to bottom out in the oversold area. Yet, with the price set to close below the lower Bollinger band for the second consecutive day, a turning point could be near.

If the price sinks below May’s trough of 0.8819, the next stop could be somewhere between the 2021 low of 0.8755 and the 0.8700 psychological mark. Running lower, the bears might face a tougher battle near 0.8600, where two support lines interest each other.

Alternatively, an upside reversal will aim for a close above the 20-day SMA at 0.8940 and the key bar of 0.8980. If the latter gives way, the upper Bollinger band at 0.9035 might immediately cap the price, delaying an extension towards the one-year-old resistance trendline at 0.9125. A faster rally could bring the 0.9200 level under the spotlight.

In a nutshell, USDCHF sellers could stay active in the short-term. A sustainable move below 0.8819 could mark a new lower low within the 0.8755-0.8700 area.

BoE’s Challenge: Simultaneous Growth of Wages and Unemployment

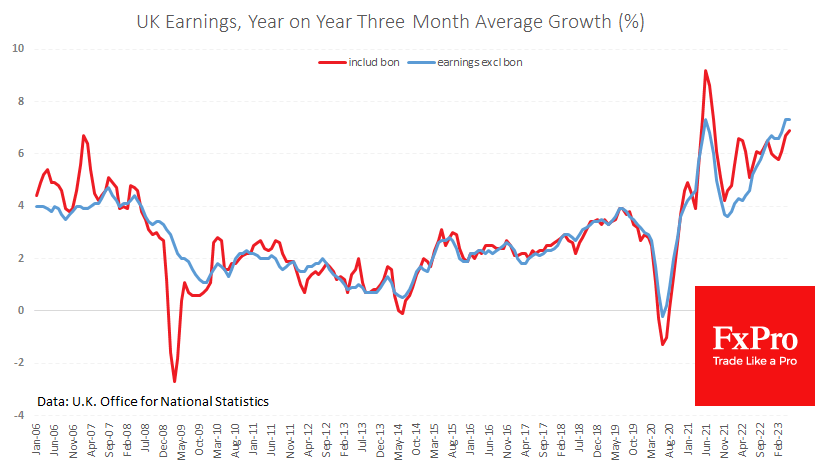

UK labour market data is making the Bank of England’s task of fighting inflation complex, with markets increasing expectations of a 50bp rate hike in early August. But we focus on falling employment, which could be the first sign of a recession.

A recent labour market report noted increased wage growth to 6.9% y/y, including bonuses. Excluding the turbulence during COVID-19, this is a record pace in the history of this indicator since 2001. But the most important signal is that wages are accelerating, in contrast to interest rate hikes. This will push up domestic inflation, including the most worrying sector, services.

Theoretically, the central bank should be stepping up its fight against inflation and pushing the monetary tightening pedal further down. This argument is supported by consumer inflation figures, which stood at 8.7% in the UK in May, much higher than in Japan (3.2%), the US (4%), France (4.5%) or Germany (6.1% in May and 6.4% in June).

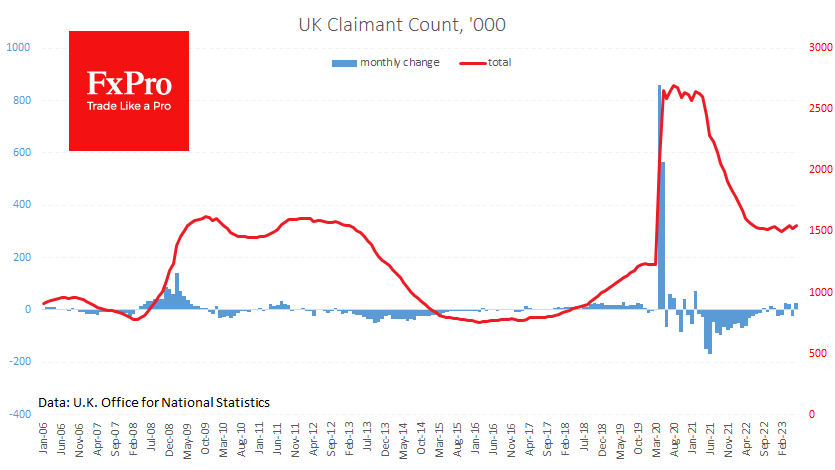

The unemployment rate rose to 4.0%. This is still historically low, but the rise from 3.5% in August makes it impossible to doubt the trend. The number of people claiming unemployment benefits rose by 25.7k in June and by 53.1k over three months.

So, wage growth in May came simultaneously as employment fell. We often see such cuts in times of crisis, when layoffs of the lowest paid initially push up the average wage level in the economy. But then, by hurting consumption, these cuts trigger a cycle of ever more widespread layoffs. Given the UK’s high and still rising interest rates, we may see this spiral in the coming quarters.

Interestingly, the GBPUSD exchange rate has not contributed significantly to the acceleration in inflation and remains close to its level of a year ago. However, the Pound is now rallying on speculation that the Bank of England will not only continue to hike interest rates but will do so more aggressively at its next meeting in early August.

Tactically, GBPUSD has a good chance of rising to just above 1.30 now that it has fully climbed out of the hole it fell into last April. However, given the dark clouds on the macroeconomic horizon, we are less optimistic that the Pound’s rally can continue.

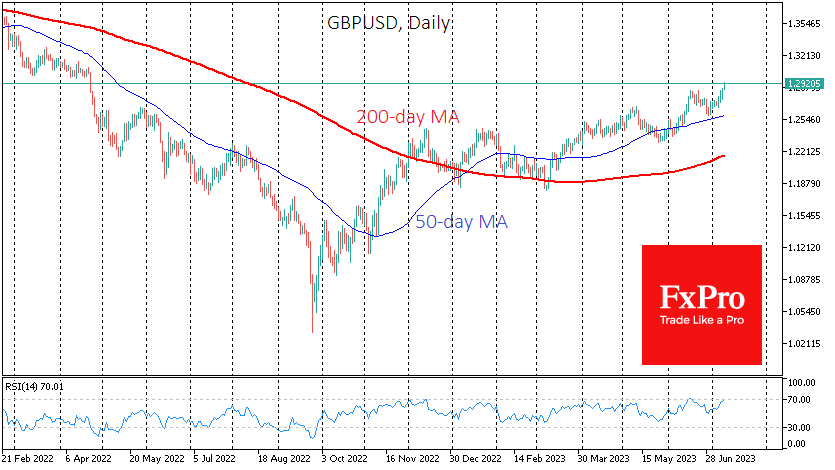

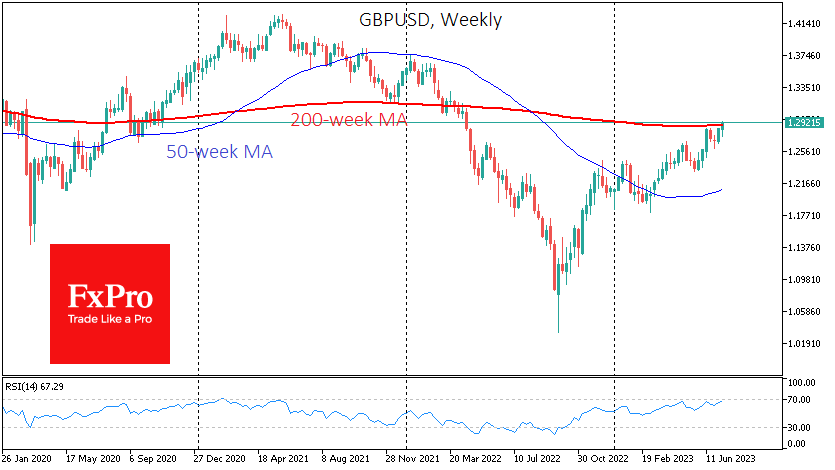

GBPUSD has spent much time near its 200-week average in recent years, reversing or gaining strength before continuing the move. A rise above 1.2890 has brought the pair back above this curve. At the same time, the RSI on the weekly and daily charts are approaching the overbought territory. This is not a signal for an immediate stop but an indication that the upward potential is nearly exhausted, at least for the next few weeks.

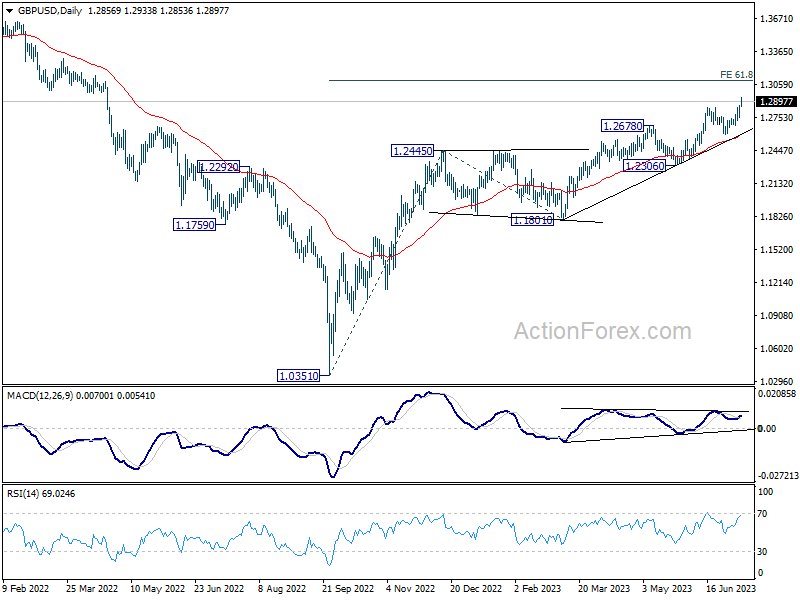

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2785; (P) 1.2826; (R1) 1.2903; More...

Intraday bias in GBP/USD remains on the upside at this point. Current rally should target 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095. On the downside, break of 1.2779 minor support will turn intraday bias neutral again. But outlook will stay bullish as long as 1.2589 support holds, in case of retreat.

In the bigger picture, the strong support from 55 W EMA (now at 1.2341) is a medium term bullish sign. Outlook will stay bullish as long as 1.2306 support holds. Rise from 1.0351 medium term bottom (2022 low) is expected to extend further to retest 1.4248 key resistance (2021 high).

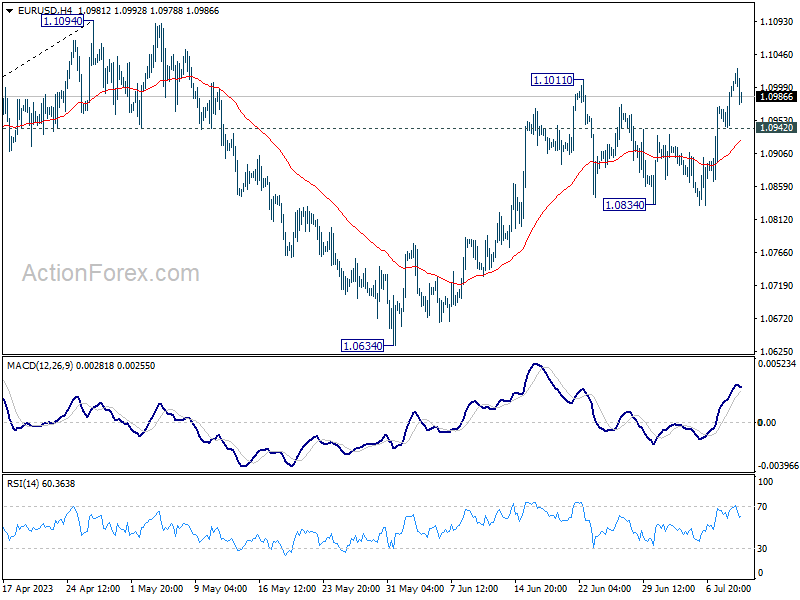

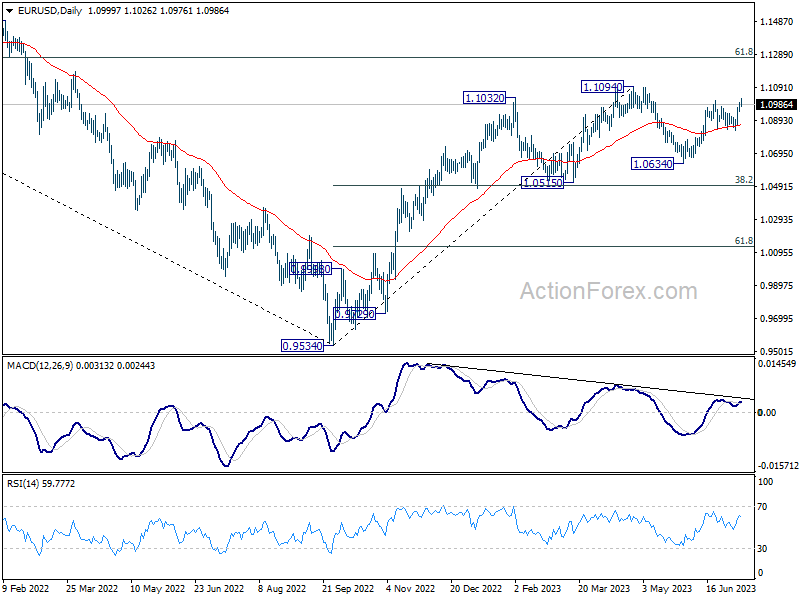

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0963; (P) 1.0982; (R1) 1.1021; More...

Intraday bias in EUR/USD stays mildly on the upside despite current retreat. Rise from 1.0634 should be extending for retesting 1.1094 high. Decisive break there will resume larger up trend from 0.9534 to 1.1273 fibonacci level. On the downside, below 1.0942 minor support will turn intraday bias neutral first. But further rally will remain in favor as long as 1.0834 support holds.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

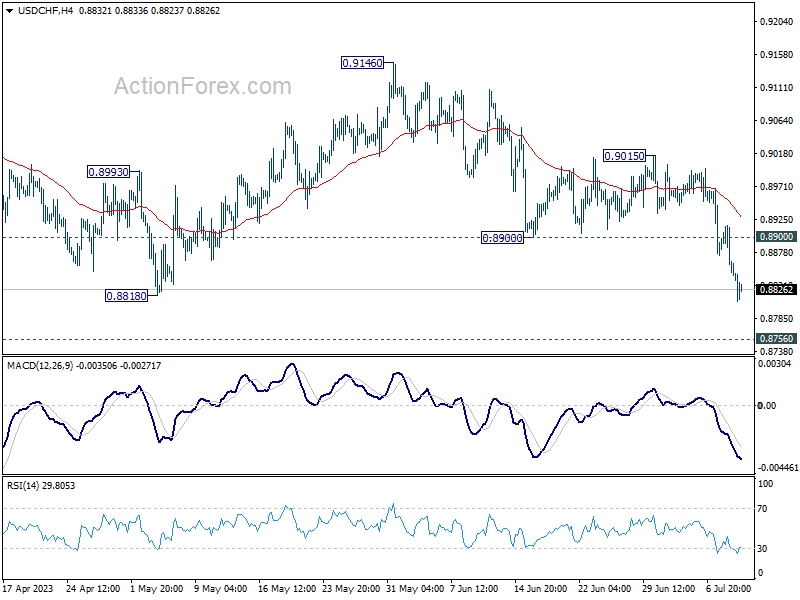

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8830; (P) 0.8874; (R1) 0.8897; More...

USD/CHF's decline continues today and breaks 0.8818 and intraday bias stays on the downside. But while further decline could be seen, strong support is expected from 0.8756 to contain downside. On the upside, above 0.8900 support turned resistance will turn intraday bias back to the upside for rebound. first. However, decisive break of 0.8756 will carry larger bearish implication.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high). While further decline cannot be ruled out, strong support is expected from 0.8756 long term support to bring reversal. Firm break of 0.9146 resistance should confirm medium term bottoming.