Sample Category Title

Fed Mester signals need for further rate hike, foresees no impending recession

In a speech delivered today, Cleveland Fed President Loretta Mester expressed surprise at the resilience shown by the economy which, in her words, "has shown more underlying strength than anticipated earlier this year." However, Mester also raised concerns regarding the stubbornly high inflation rates, noting that "progress on core inflation [has been] stalling."

"In order to ensure that inflation is on a sustainable and timely path back to 2%," she said, "my view is that the funds rate will need to move up somewhat further from its current level and then hold there for a while as we accumulate more information on how the economy is evolving."

Mester also touched on labor market's imbalance during reopening, where she noted that "labor demand well outpaced labor supply, putting upward pressure on wages and price inflation." Although she sees progress in achieving a more balanced situation, she cautioned that "it is slow progress and demand is still outpacing supply."

Despite these challenges, Mester revealed a streak of optimism in the business community. She said that most business leaders "think there won't be a recession this year, and many think that, even if demand slows down some more, a recession will be avoided or will be very mild."

Wall Street Awaits Wednesday’s CPI Data and Start of Earnings Season

- Wednesday’s inflation report expected to show CPI m/m: 0.3%e v 0.1% prior; y/y: 3.1%e v 4.0% prior; Core CPI m/m: 0.3%e v 0.4% prior; Core CPI y/y: :5.0%e v 5.3% prior

- Fed’s Barr on banks: These changes would increase capital requirements overall

- Fed Mester noted that the funds rate will need to move up somewhat further from its current level and then hold there for a while

US stocks are wavering ahead of both a key inflation report that should core CPI remain sticky and what should be a rough earnings season. Friday’s employment report showed a hiring slowdown but also strong wage gains. What will make this inflation report exciting is that we could see annual headline inflation fall to 2.8%, while core inflation remains hot, bolstered by housing inflation. The steep decline in annual CPI won’t remain a recurring theme and pricing pressures might remain throughout the summer.

The big banks will kickoff earnings season and expectations are for the largest loan losses since the pandemic. Considering how high stocks have rushed higher, it will be difficult for this earnings season to deliver strong enough results for fresh highs.

China’s growth story remains a drag on the global economy. Perhaps more important for markets was last night’s Chinese prices data. China saw CPI post the lowest reading in 2 years, with a 0% year-over-year reading, while producer prices plunged 5.4% from a year earlier, the worst decline since December 2015. It is getting uglier in China and that is why officials are scrambling to deliver more support to real estate developers. The real estate crisis has been lingering for a couple of years and it is messing up their COVID reopening. The PBOC is going to do more, but this piecemeal policy support strategy is not working.

Treasury Secretary Yellen’s trip to Beijing was positive but nothing meaningful was expected to be achieved. Yellen assuaged concerns that harsh restrictions might not get imposed by both countries. The US needs China’s rare minerals and China needs foreign chips.

Will BoC Hit the Hike Button Again?

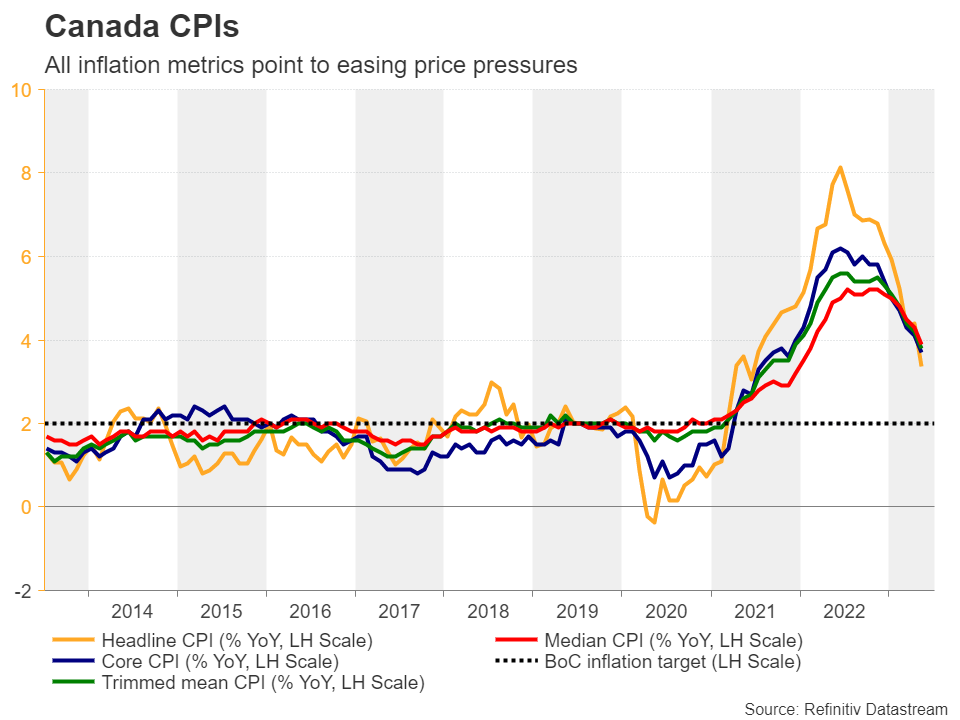

Following the larger-than-expected slowdown in Canada’s inflation data for May, inventors were confused as to whether a hike is warranted at the Bank of Canada’s upcoming meeting, scheduled for Wednesday (14:00 GMT). That said, Friday’s strong jobs report tilted the scale towards the rate-hike scenario. With that in mind, how will the outcome affect the Canadian dollar?

Inflation slows by a full percentage point

At its June meeting, the BoC decided to raise its target for the overnight rate to 4.75%, ending a pause period that began in January. In the accompanying statement, officials noted that although headline inflation is globally coming down due to lower energy prices, underlying inflation remains stubbornly high, adding that they will continue to evaluate whether the inflation dynamics are consistent with achieving their objective.

Since then, the employment report for May revealed that the economy lost jobs, driving the unemployment rate up to 5.2% from 5.0%, while the CPIs for the same period revealed a larger-than-expected slowdown in both headline and core terms. Specifically, the headline CPI rate fell a full percentage point, to 3.4% year-on-year from 4.4%, and the core one dropped to 3.7% y/y from 4.1%. On the other hand, though, retail sales for April grew much more than expected, pointing towards upside risks to consumer prices in the months ahead.

These releases led to confusion among investors, who ahead of Friday’s employment report for June, were split on whether Canadian policymakers should hit the hike button for a second time in a row this week.

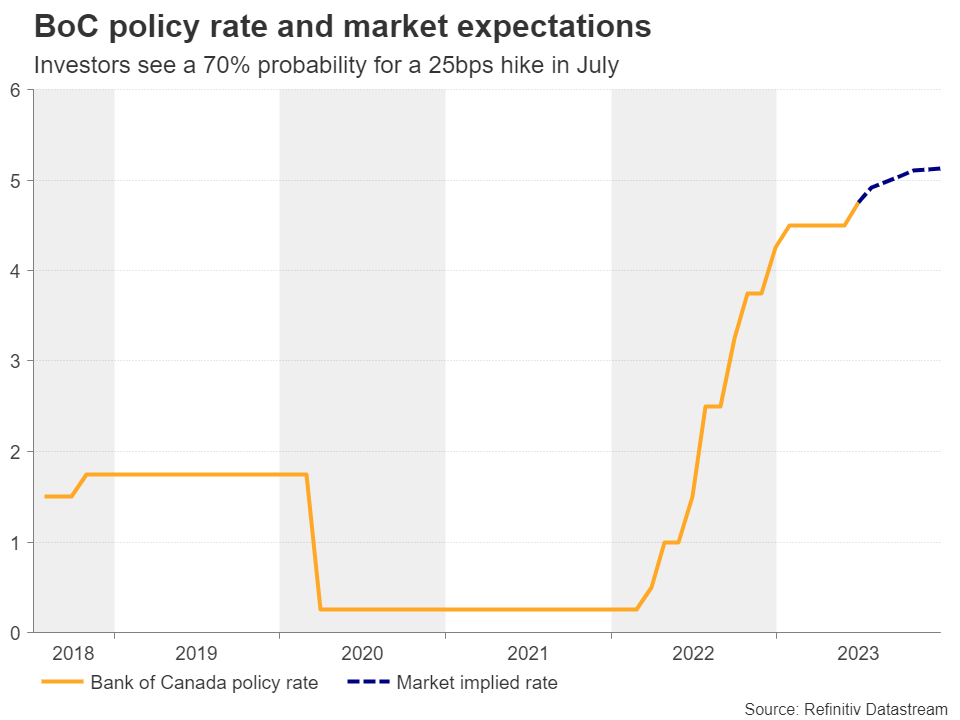

Friday’s jobs data tilt the scale towards a hike

That said, Friday’s jobs data revealed that the economy gained triple the expected jobs in June and that although the unemployment rate rose further to 5.4%, the participation rate increased as well. In other words, the rise in the unemployment rate may have been because more economically inactive people were willing to register and start actively looking for a job.

This shifted the scale towards another hike on Wednesday, with the market now assigning a 70% probability for a rate increase and 30% for no action at all. As for the rest of the year, investors are nearly split on whether another quarter-point hike is needed by December.

Statement and new projections to enter the spotlight

Having all that in mind, a 25bps hike on Wednesday could help the loonie gain initially but not much as this is a largely expected decision. If policymakers do push the hike button, the attention is likely to quickly turn to the accompanying statement and the quarterly monetary policy report, which includes updated macroeconomic projections.

The April report revealed that inflation is likely to return to the Bank’s 2% objective at the end of 2024, but that was before the larger-than-expected slowdown in May. Therefore, if there are downside revisions to the inflation outlook and the Bank does not clearly signal the need for additional hikes, investors are likely to scale back their bets about another hike by year end.

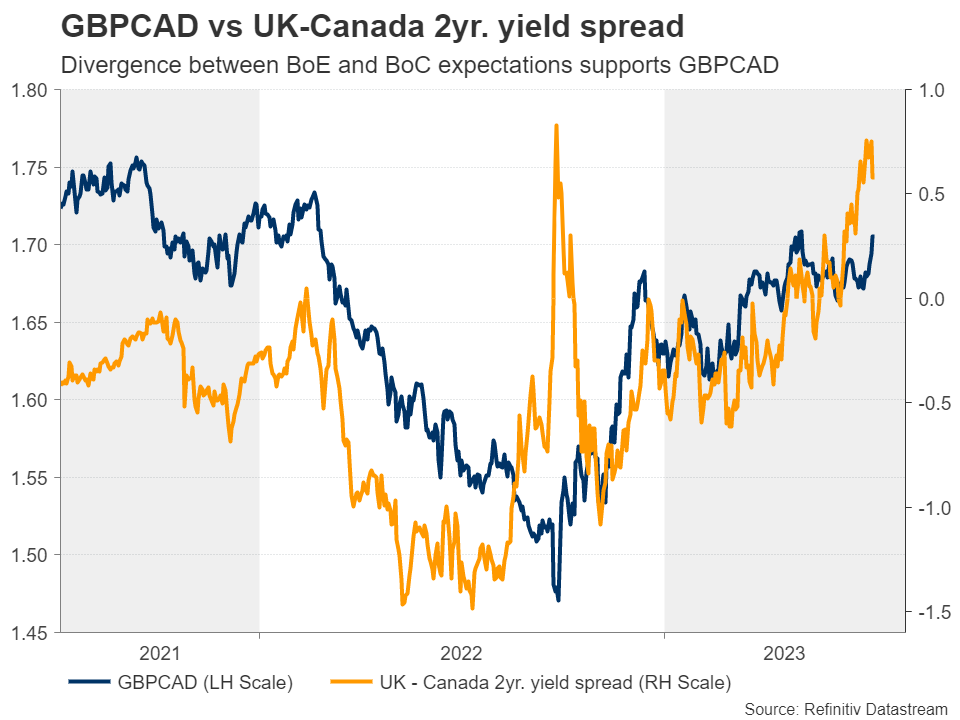

A dovish hike could hurt the loonie

This would add a dovish flavor to a potential hike and may work against the Canadian dollar. Specifically, the loonie may weaken the most against the pound, which has been benefiting from expectations that the BoE will deliver another 140bps worth of hikes before it signals the end of its own tightening crusade. For the loonie to enjoy sustained gains, the BoC may need to raise rates now and clearly telegraph that more hikes are looming.

Pound/loonie trades in uptrend mode

The pound/loonie pair moved higher last week, overcoming the 1.6970 barrier, but staying below the peak of May 4 at 1.7150, which is also the highest point since February 25. Overall, the price structure suggests that the pair has been trading in an uptrend since September, but one that has been losing momentum recently.

A trend continuation could be signaled upon a break above 1.7150, a move that would confirm a higher high on the daily chart and perhaps pave the way towards the high of February 21, 2022, at around 1.7370, the break of which could extend the pair’s gains towards the 1.7600 territory, which acted as a ceiling between April 20 and September 20, 2021.

For the outlook to turn bearish, pound/loonie may need to fall below the 1.6525 zone, which currently coincides with the 200-day exponential moving average. Such a dip may allow declines towards the 1.6230 zone, marked by the low of March 2, or the 1.6075 territory, which offered support between February 7 and 16.

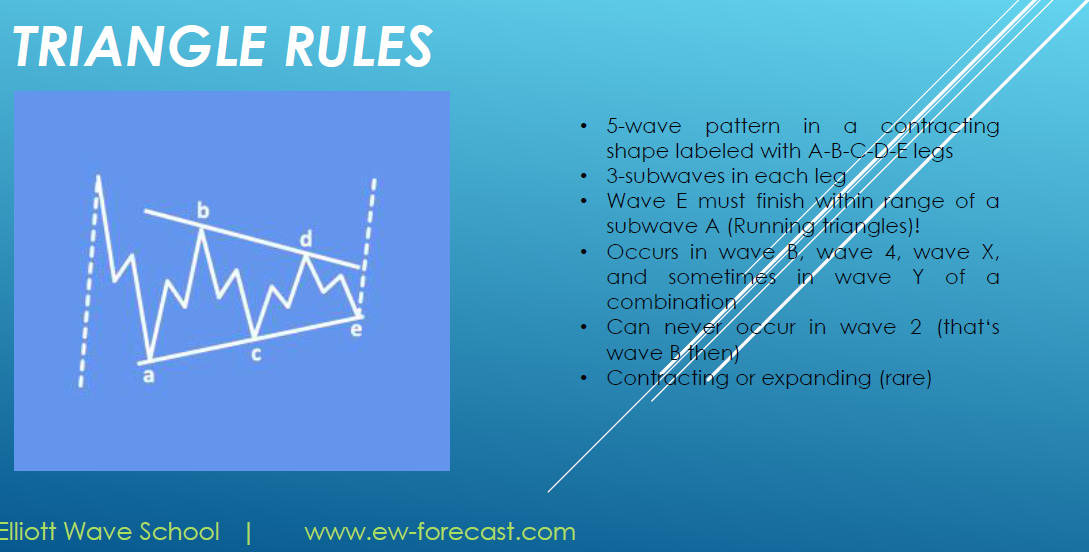

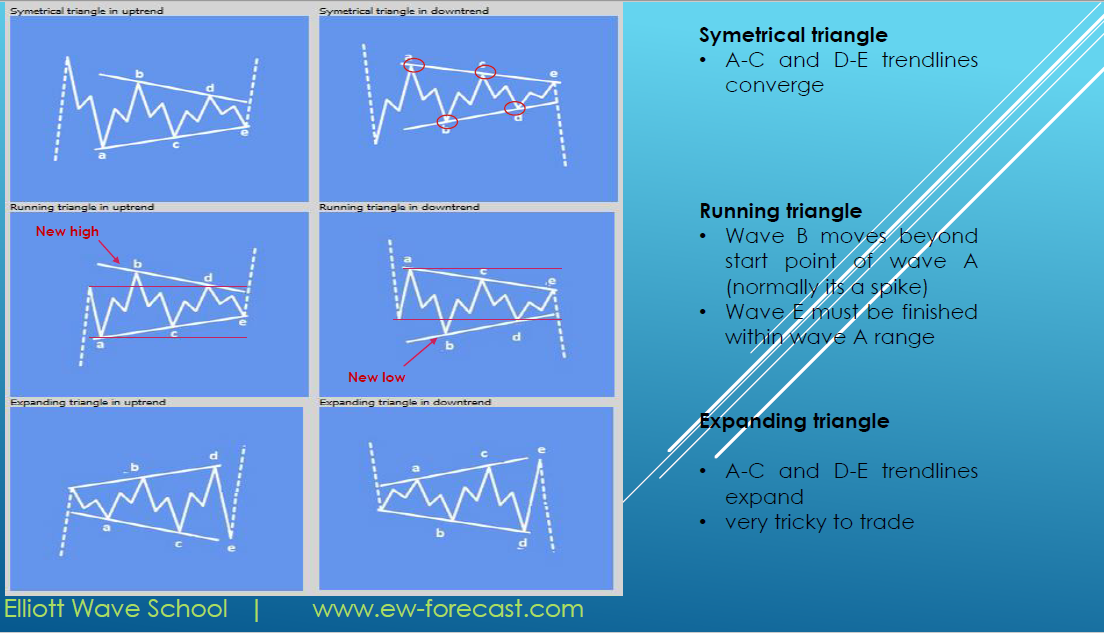

AUD/NZD: Price Approaching Triangle Support (Elliott Wave forecast)

NZD is doing much better compared to AUD for the last few weeks, but with RBNZ on Wednesday the flows may change. From an Elliott wave perspective, we see pair coming down into big and important Fib support at 1.0650-1.07 where we expect temporary support for wave D that belongs to a higher degree triangle. Triangle it's an A-B-C-D-E pattern, so we may have to wait and be aware of more sideways price action through the summer, before the market may finally break lower; ideally later this year.

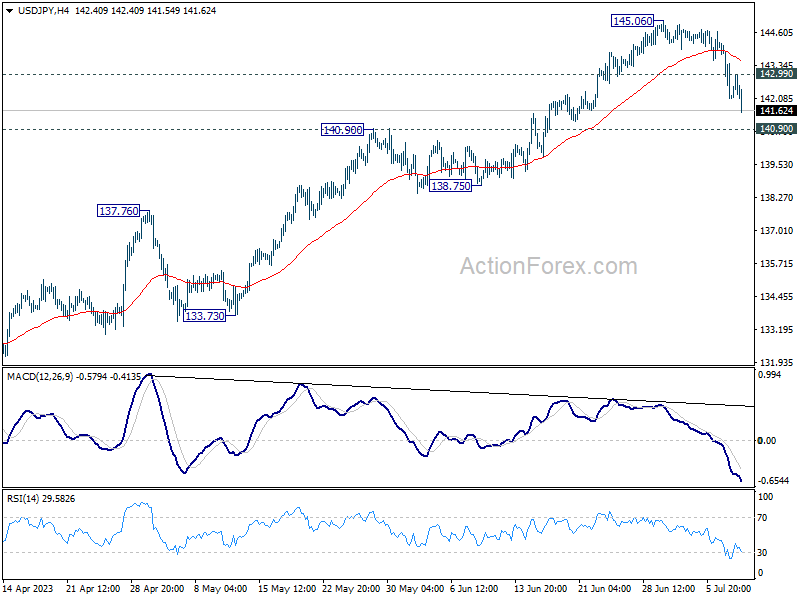

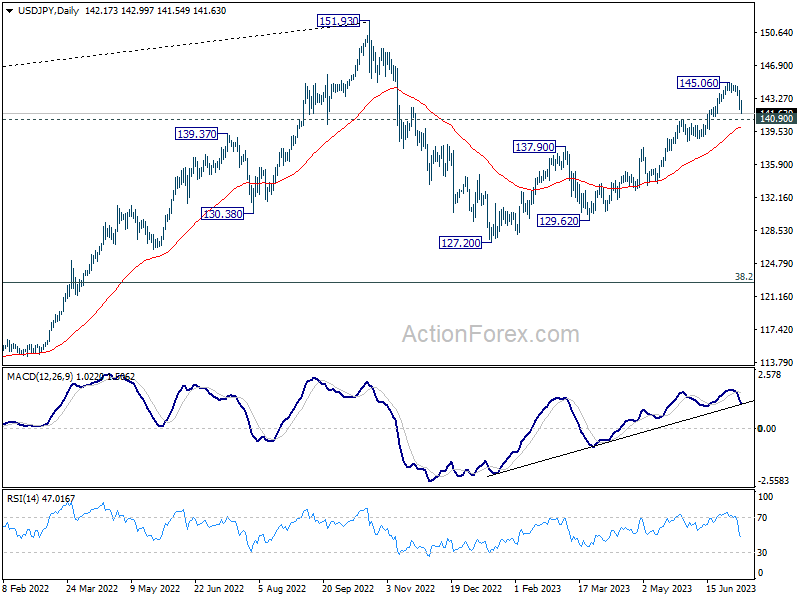

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 141.42; (P) 142.81; (R1) 143.54; More...

USD/JPY's decline from 145.06 temporary top continues today and intraday bias stays on the downside for 140.90 resistance turned support. Firm break there will raise the chance that whole rebound from 127.20 has completed. Deeper decline should then be seen to 137.90 resistance turned support for confirmation. On the upside, above 142.99 minor resistance will turn intraday bias neutral first.

In the bigger picture, rise from 127.20 is seen as the second leg of the corrective pattern from 151.93 high. Further rally could still be seen as long as 137.90 resistance turned support holds, to retest 151.93. But strong resistance should be seen there to limit upside. However, Break of 137.90 will indicate that the third leg has started back towards 127.20.

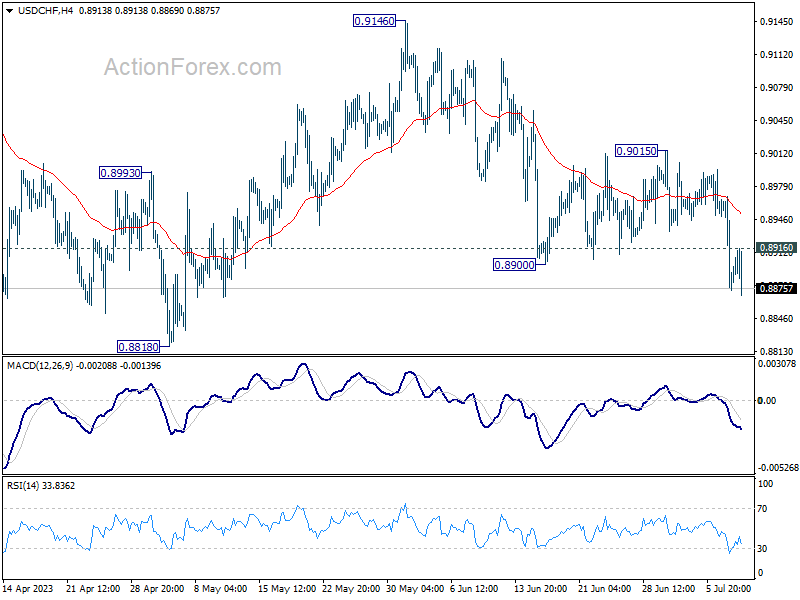

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8855; (P) 0.8913; (R1) 0.8949; More...

USD/CHF's fall continues today and intraday bias stays on the downside. Current decline from 0.9146 should target 0.8818 and below, to resume whole down trend from 1.0146. Strong support is expected from 0.8756 to contain downside and bring rebound. On the upside, above 0.8916 minor resistance will turn intraday bias neutral first. Yet, break of 0.9015 resistance is needed to confirm short term bottoming. Otherwise, outlook will stay bearish.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high). While further decline cannot be ruled out, strong support is expected from 0.8756 long term support to bring reversal. Firm break of 0.9146 resistance should confirm medium term bottoming.

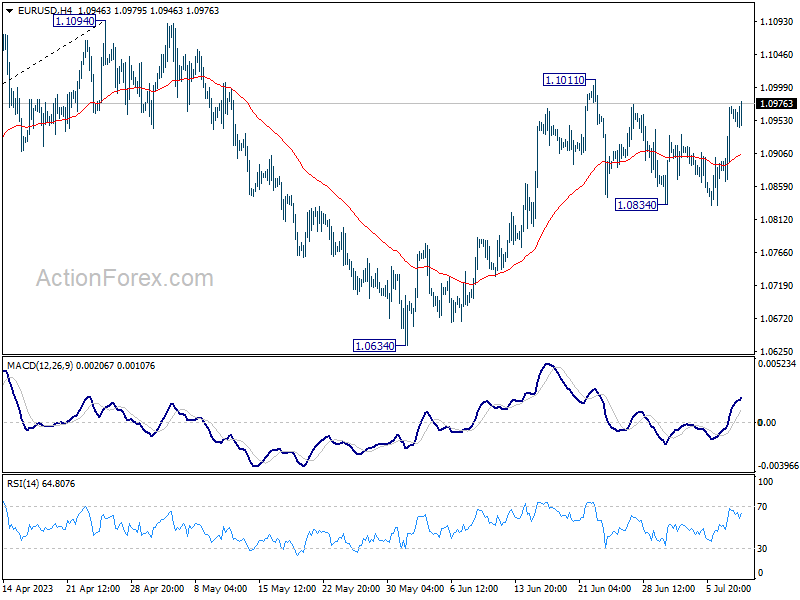

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0900; (P) 1.0936; (R1) 1.1006; More...

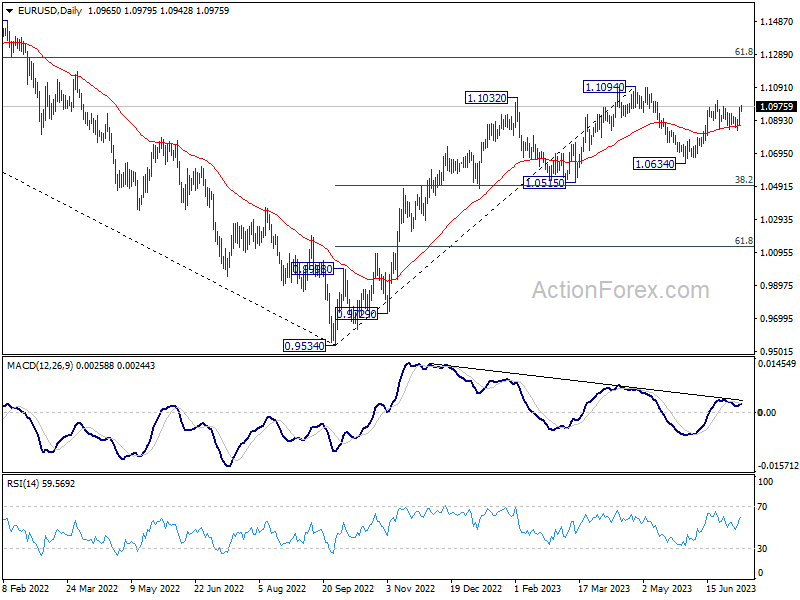

EUR/USD is still capped below 1.1011 resistance and intraday bias neutral. Further rally remains in favor. On the upside, break of 1.1011 will resume the rise from 1.0634 and target 1.1094 resistance. Decisive break there will resume larger up trend from 0.9534 to 1.1273 fibonacci level. However, firm break of 1.0834 will turn bias to the downside for 1.0634 support instead.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

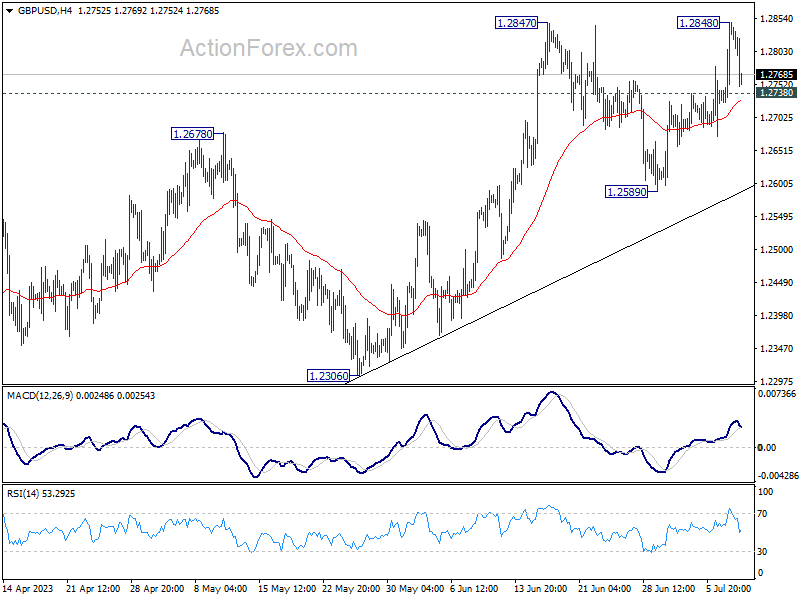

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2760; (P) 1.2805; (R1) 1.2883; More...

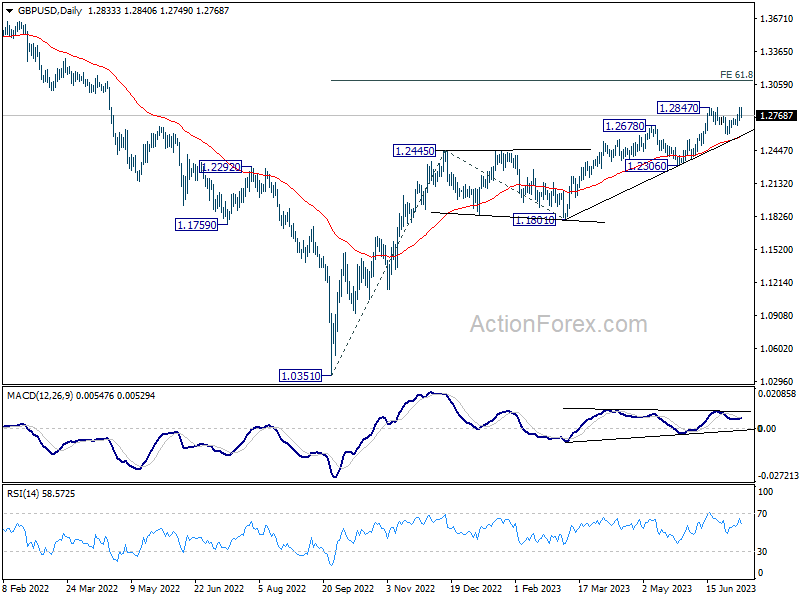

Intraday bias in GBP/USD is turned neutral with current retreat. On the downside, break of 1.2738 minor support will indicate that consolidation from 1.2847 is extending with another falling leg, back to 1.2589 support. On the upside, decisive break of 1.2847/8 will confirm resumption of larger up trend from 1.0351. Next target is 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095.

In the bigger picture, the strong support from 55 W EMA (now at 1.2341) is a medium term bullish sign. Outlook will stay bullish as long as 1.2306 support holds. Rise from 1.0351 medium term bottom (2022 low) is expected to extend further to retest 1.4248 key resistance (2021 high).

Antipodean Currencies Under Pressure With Sterling, Euro Shrugs Weak Investor Confidence

Australian and New Zealand Dollar are under some selling pressure today, with the Sterling following suit. These currency fluctuations do not appear to be tied to any specific market developments, but their concurrent weakness may suggest a cautious undertone prevalent among risk-averse traders. Notably, market participants might be realigning their positions in anticipation of this week's UK employment and GDP data, and RBNZ hold.

Simultaneously, capital appears to be flowing towards Dollar, Canadian and Euro. Despite rather poor Eurozone investor sentiment data, Euro remains robust. The immediate outlook for Dollar hinges largely on the upcoming CPI and PPI data. Canadian Dollar is buoyed by firm oil prices and expectations of an imminent rate hike from BoC. Meanwhile, Yen is extending recent rally against the weaker currencies today while staying firm in tight range against Dollar and Euro.

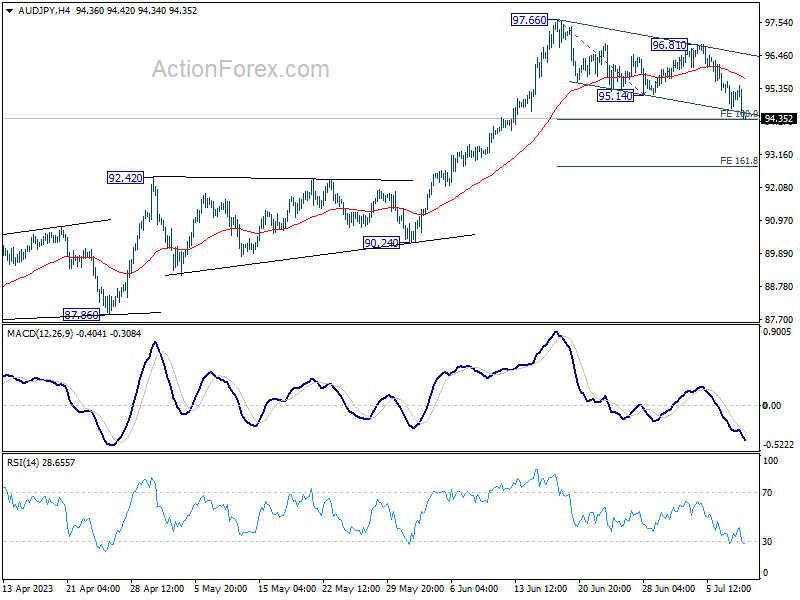

Technically, AUD/JPY in proximity to 100% projection of 97.66 to 95.14 from 96.81 at 94.29. Strong support could be seen around current level to bring rebound. Break of 95.14 support turned resistance be a signal of short term bottoming. However, sustained trading below 94.29, and further downside acceleration, will argue that AUD/JPY is probably reversing the whole rise from 86.04 (March low).

In Europe, at the time of writing, FTSE is up 0.46%. DAX is up 0.54%. CAC is up 0.70%. Germany 10-year yield is up 0.0251 at 2.660. Earlier in Asia, Nikkei dropped -0.61%. Hong Kong HSI rose 0.62%. China Shanghai SSE rose 0.22%. Singapore Strait Times rose 0.31%. Japan 10-year JGB yield rose 0.0363 at 0.473.

Eurozone Sentix fell to -22.5, more serious than usual summer lull

The economic outlook for Eurozone dimmed as Sentix Investor Confidence Index suffered its third consecutive monthly fall, reaching an eight-month low in July. The index tumbled from -17 to -22.5, significantly underperforming market expectations of -18.9. Both Current Situation Index and Expectations Index followed suit, dropping from -15.8 to -20.5 and from -18.3 to -24.5 respectively.

Sentix offered a stark assessment of the situation: "As of early July 2023, the Eurozone economy remains in recession mode." The investment group expressed skepticism about the potential sources of an economic boost, observing the U.S. economy's struggle to generate positive momentum, while downplaying any hope of central banks stepping in to counteract the economic downturn.

The investor sentiment towards the central banks' policies was especially pessimistic, with the topic index "central bank policy" plummeting from -13 to -24, indicating that investors foresee an intensification of restrictive monetary measures.

Compounding this gloomy outlook, the corresponding Inflation Barometer slid from -6 to -14.5 points, with Sentix cautioning that the current situation is "clearly more serious than the usual summer lull".

BoJ upgrades assessment on three regions, all picking or recovering moderately

In the Regional Economic Report released today, BoJ painted an encouraging picture of economic recovery. Despite challenges like past spike in commodity prices. All nine regions "had been either picking up or recovering moderately".

Moreover, three regions - Tokai, Chugoku, and Kyushu-Okinawa - have received upgrades in their economic outlooks, while the views on Hokkaido, Tohok, Hokuriku, Kanto-Koshinetsu, Kinki, and Shikoku remain unchanged.

The report also revealed that numerous regions have seen wage increases across small and mid-sized firms broadening to an extent not witnessed in recent years. However, the future of these wage hikes remains uncertain.

Takeshi Nakajima, BoJ's branch manager overseeing Kansai western Japan region, underscored this ambiguity, stating that it's premature to predict if companies will continue raising wages next year. "A lot of companies in the region say that will depend on this year's earnings and what their rivals could do," Nakajima said during a news conference.

He added, "If companies can earn enough revenues to pay for higher wages, there's hope wage rises will continue. Given uncertainty over the outlook, however, it's premature to say decisively that this will happen."

China's PPI down -5.4% yoy, CPI flat in Jun

China's factory-gate inflation, as measured by PPI, marked its ninth consecutive decline in June, slumping by -5.4% yoy. This drop is the steepest since December 2015 and outstripped -4.6% yoy in May, a well as expectation of -5.0 yoy. PPI fell -0.8% on a month-on-month basis in June, slightly less than the -0.9% mom fall registered in May.

National Bureau of Statistics statistician Dong Lijuan pointed to tumbling commodity prices, particularly oil and coal, as the driving force behind the slump in factory-gate prices. The comparison to high base figures from the previous year also played a role in the significant drop.

Additionally, China's CPI continued to lose momentum, sliding from 0.2% yoy in May to 0.0% yoy in June, its lowest reading since February 2021. This downturn defied expectations of a 0.2% yoy. On a month-on-month basis, June's CPI mirrored the previous month, dipping by -0.2%.

Analysing the CPI's components, core CPI, which excludes volatile food and energy prices, showed a tempered 0.4% yoy rise, compared to 0.6% yoy in May. Food prices accelerated by 2.3% yoya leap from May's 1.0% yoy increase, while non-food prices moved in the opposite direction, falling by -0.6% yoy in contrast to a flat performance in May.

The sustained descent in PPI, coupled with lackluster CPI, underlines the ongoing deflationary pressures in China's economy.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2760; (P) 1.2805; (R1) 1.2883; More...

Intraday bias in GBP/USD is turned neutral with current retreat. On the downside, break of 1.2738 minor support will indicate that consolidation from 1.2847 is extending with another falling leg, back to 1.2589 support. On the upside, decisive break of 1.2847/8 will confirm resumption of larger up trend from 1.0351. Next target is 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095.

In the bigger picture, the strong support from 55 W EMA (now at 1.2341) is a medium term bullish sign. Outlook will stay bullish as long as 1.2306 support holds. Rise from 1.0351 medium term bottom (2022 low) is expected to extend further to retest 1.4248 key resistance (2021 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Jun | 3.20% | 3.50% | 3.40% | |

| 23:50 | JPY | Current Account (JPY) May | 1.70T | 1.87T | 1.90T | |

| 01:30 | CNY | CPI Y/Y Jun | 0.00% | 0.20% | 0.20% | |

| 01:30 | CNY | PPI Y/Y Jun | -5.40% | -5.00% | -4.60% | |

| 05:00 | JPY | Eco Watchers Survey: Outlook Jun | 53.6 | 54.8 | 55 | |

| 08:30 | EUR | Eurozone Sentix Investor Confidence Jul | -22.5 | -18.9 | -17 | |

| 12:30 | CAD | Building Permits M/M May | 10.50% | 7.30% | -18.80% | |

| 14:00 | USD | Wholesale Inventories May F | -0.10% | -0.10% |

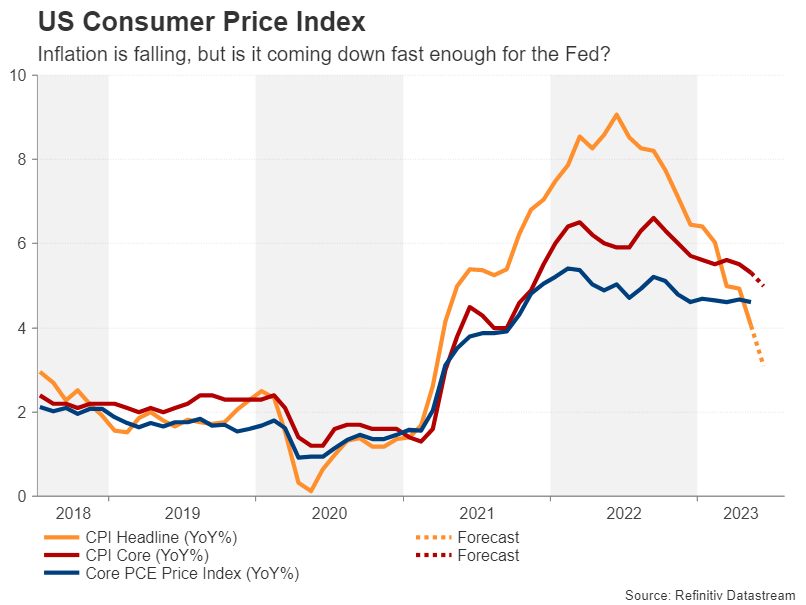

US CPI Inflation Expected to Cool Further, But Will It Hurt Dollar?

The US CPI report for June will be keenly awaited on Wednesday (12:30 GMT) as investors remain undecided about the timing of the Fed’s next rate hike. The producer price index will follow on Thursday. Inflation according to the consumer price index is on its way down and that trend is expected to be maintained in the upcoming release. However, underlying measures of inflation have been a lot stickier so core CPI will be the main focus as far as Fed policymakers are concerned and potentially a bigger catalyst for US dollar volatility.

The sticky problem that just won’t go away

Central banks appear to have won the initial fight against skyrocketing prices but the war on inflation isn’t quite over as there is now a new battle – sticky inflation. This couldn’t be more evident in the United States where inflation rose quickly to peak just above 9.0% exactly a year ago and appears to be falling just as fast. However, core inflation, which is a more reliable indicator of what’s happening to price pressures underneath the surface, has remained stubbornly high, declining only marginally this year.

Core CPI stood at 5.3% y/y in May, fractionally lower from 5.7% in December but significantly above the headline rate of 4.0%. The picture is even worse when looking at the alternative core PCE price index, which has been stuck between 4.6% and 4.7% since December.

(Slowly) Going in the right direction

When viewed against an ongoing tight labour market, a flatlining trend in core inflation well above the 2% target is hardly what the Fed was hoping it would have achieved by mid-year, having raised rates by 500 basis points in the course of just 15 months. The June figures are not anticipated to provide much relief either.

Whilst the headline CPI rate is forecast to have plunged to a more than two-year low of 3.1%, the core rate is expected to have made more gradual progress, slowing to 5.0% in June. On the face of it, there is nothing too alarming about either figure as both are headed in the right direction. However, with the core measures still printing so high above the target, the Fed cannot afford to take its eye off the ball.

It explains why FOMC members have maintained such a strong bias for more tightening even though they decided to keep rates on hold in June. Chair Powell has been defending the move as simply a further downshift in the pace of tightening rather than a pause and although markets are not entirely convinced, they are growing increasingly doubtful about the likelihood of a rate cut in the first half of 2024.

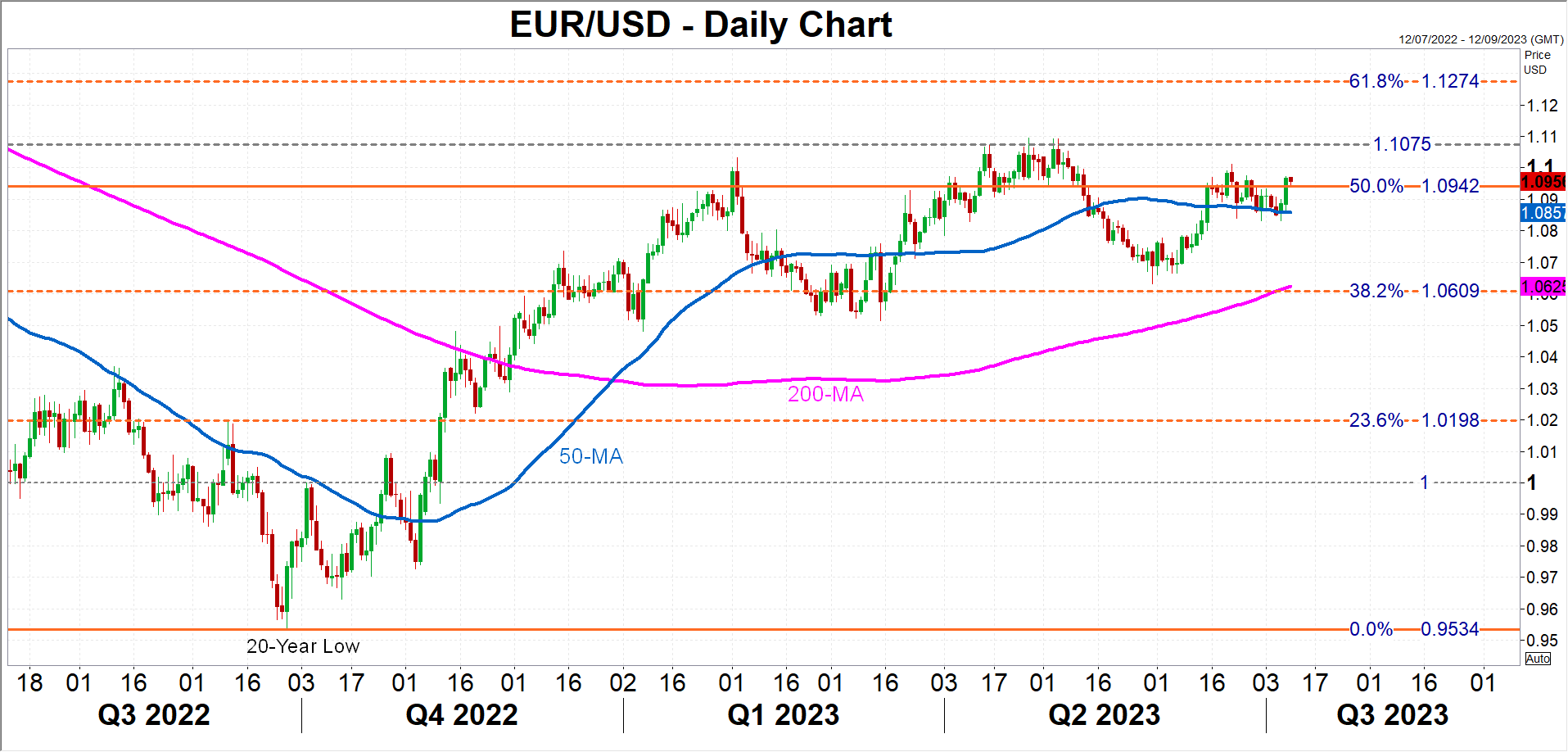

Downside risks for euro/dollar

Moreover, with the US economy still in a somewhat better shape than the Eurozone, which is losing momentum faster, a further steepening of the market-implied rate path for the Fed poses a significant risk for euro/dollar given that more rate increases are currently priced in for the ECB.

A stronger-than-expected CPI report would push up the odds for a 25-bps rate rise in July as well as for an additional hike later in the year. The euro could potentially tumble towards its 38.2% Fibonacci retracement of the January 2021-September 2022 downtrend in the $1.06 region, which lies between the March and May lows.

However, if the inflation data is on the soft side, particularly if core CPI falls more than expected, the euro could have another attempt at overcoming the $1.1075 resistance before eyeing the 61.8% Fibonacci of $1.1274.

Diverging paths

More broadly though, the dollar’s outlook has become somewhat complicated, not just because of the Fed’s foggy policy outlook, but also because of the varying degrees of divergence with other central banks.

The pound for example is the least likely to suffer should the Fed not disappoint in hiking again as the Bank of England is almost guaranteed to do the same to tackle the UK’s persistent inflation problem. The yen on the other hand is in danger of revisiting the more than three-decade lows from October 2022 as the Bank of Japan has yet to signal its willingness to begin the process of unwinding its massive stimulus.