Sample Category Title

US CPI Inflation Expected to Cool Further, But Will It Hurt Dollar?

The US CPI report for June will be keenly awaited on Wednesday (12:30 GMT) as investors remain undecided about the timing of the Fed’s next rate hike. The producer price index will follow on Thursday. Inflation according to the consumer price index is on its way down and that trend is expected to be maintained in the upcoming release. However, underlying measures of inflation have been a lot stickier so core CPI will be the main focus as far as Fed policymakers are concerned and potentially a bigger catalyst for US dollar volatility.

The sticky problem that just won’t go away

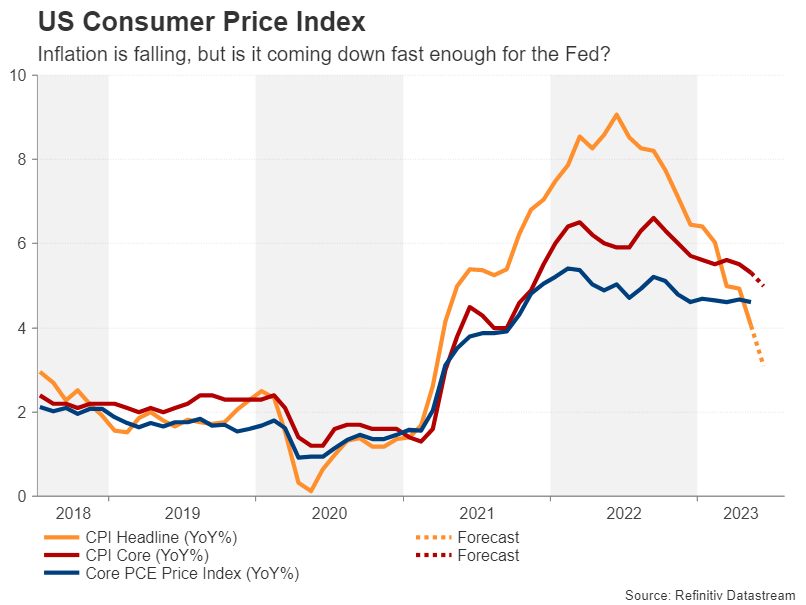

Central banks appear to have won the initial fight against skyrocketing prices but the war on inflation isn’t quite over as there is now a new battle – sticky inflation. This couldn’t be more evident in the United States where inflation rose quickly to peak just above 9.0% exactly a year ago and appears to be falling just as fast. However, core inflation, which is a more reliable indicator of what’s happening to price pressures underneath the surface, has remained stubbornly high, declining only marginally this year.

Core CPI stood at 5.3% y/y in May, fractionally lower from 5.7% in December but significantly above the headline rate of 4.0%. The picture is even worse when looking at the alternative core PCE price index, which has been stuck between 4.6% and 4.7% since December.

(Slowly) Going in the right direction

When viewed against an ongoing tight labour market, a flatlining trend in core inflation well above the 2% target is hardly what the Fed was hoping it would have achieved by mid-year, having raised rates by 500 basis points in the course of just 15 months. The June figures are not anticipated to provide much relief either.

Whilst the headline CPI rate is forecast to have plunged to a more than two-year low of 3.1%, the core rate is expected to have made more gradual progress, slowing to 5.0% in June. On the face of it, there is nothing too alarming about either figure as both are headed in the right direction. However, with the core measures still printing so high above the target, the Fed cannot afford to take its eye off the ball.

It explains why FOMC members have maintained such a strong bias for more tightening even though they decided to keep rates on hold in June. Chair Powell has been defending the move as simply a further downshift in the pace of tightening rather than a pause and although markets are not entirely convinced, they are growing increasingly doubtful about the likelihood of a rate cut in the first half of 2024.

Downside risks for euro/dollar

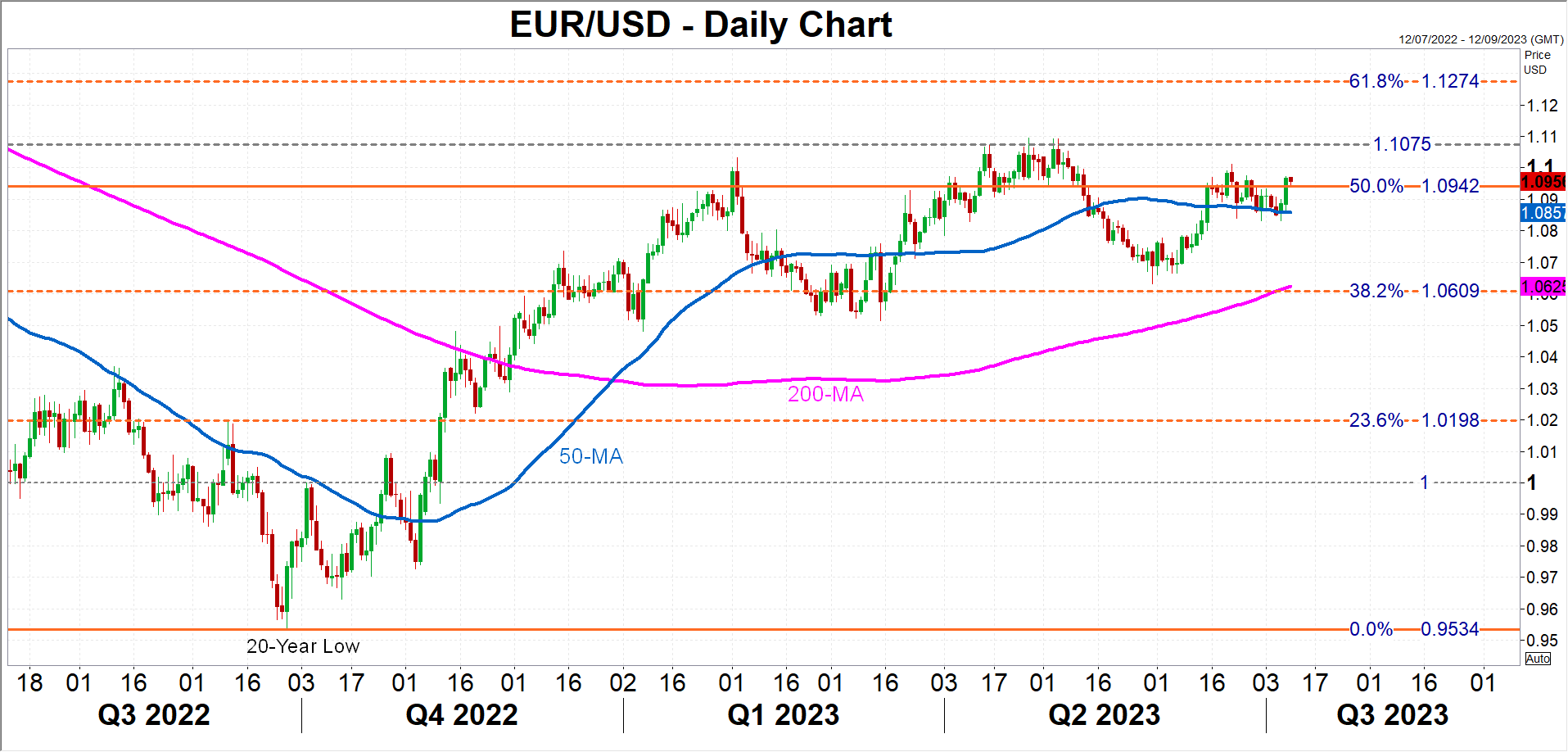

Moreover, with the US economy still in a somewhat better shape than the Eurozone, which is losing momentum faster, a further steepening of the market-implied rate path for the Fed poses a significant risk for euro/dollar given that more rate increases are currently priced in for the ECB.

A stronger-than-expected CPI report would push up the odds for a 25-bps rate rise in July as well as for an additional hike later in the year. The euro could potentially tumble towards its 38.2% Fibonacci retracement of the January 2021-September 2022 downtrend in the $1.06 region, which lies between the March and May lows.

However, if the inflation data is on the soft side, particularly if core CPI falls more than expected, the euro could have another attempt at overcoming the $1.1075 resistance before eyeing the 61.8% Fibonacci of $1.1274.

Diverging paths

More broadly though, the dollar’s outlook has become somewhat complicated, not just because of the Fed’s foggy policy outlook, but also because of the varying degrees of divergence with other central banks.

The pound for example is the least likely to suffer should the Fed not disappoint in hiking again as the Bank of England is almost guaranteed to do the same to tackle the UK’s persistent inflation problem. The yen on the other hand is in danger of revisiting the more than three-decade lows from October 2022 as the Bank of Japan has yet to signal its willingness to begin the process of unwinding its massive stimulus.

Is It Really the End of Rate-Hiking Road for RBNZ?

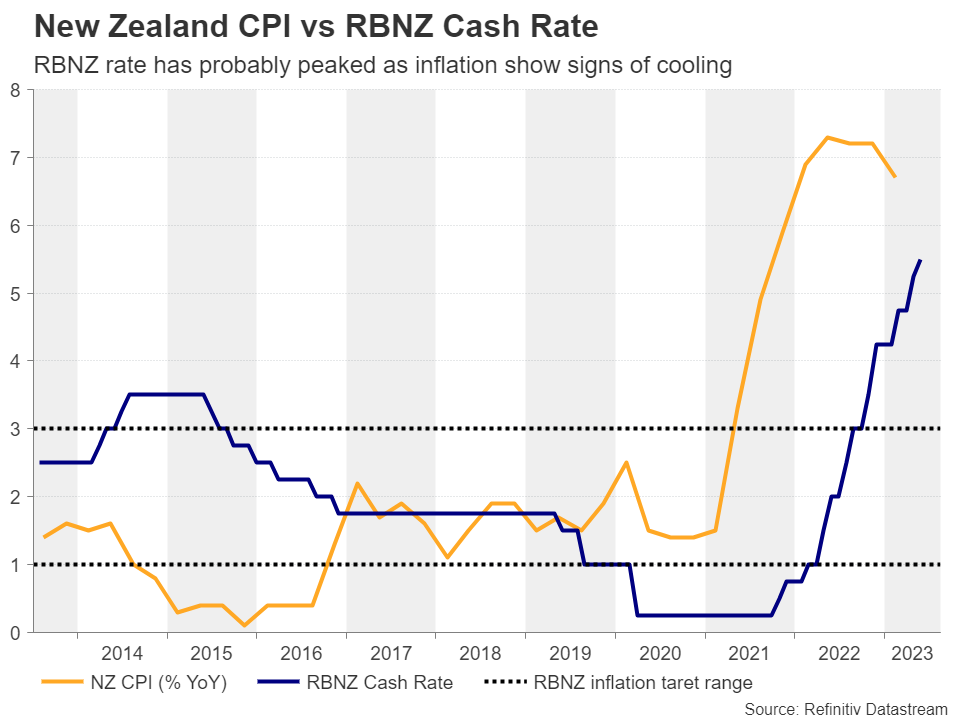

Despite its tendency to produce surprises at its rate-setting meetings, it feels like the Reserve Bank of New Zealand has completed its hiking cycle. With the market endorsing a pause at this week’s gathering, the kiwi has to look elsewhere for a potential boost against the US dollar.

Events since the last RBNZ meeting

A total of six central banks will update the market on their rate decisions during July. With the next-door Reserve Bank of Australia announcing a pause last week, the focus has shifted to the RBNZ. The market is overwhelmingly expecting no change at the current official cash rate. There is an 8% probability of a surprise 25 bps rate move on Wednesday, as some market participants still have the April events fresh in their minds.

However, the wider environment is slightly different now. With China’s growth failing to pick up pace and the euro area slowing aggressively, the global growth outlook is becoming more complicated. In addition, the inflation-related monthly domestic indicators like the ANZ commodity price index are pointing to a gradual deceleration of price pressures, matching similar indicators across the globe.

However, this perceived inflation slowdown has to be confirmed by the CPI figures for the second quarter of 2023, released on July 19. It is fair to assume that the Monetary Policy Committee will probably have an early preview of these numbers at Wednesday’s meeting. The RBNZ’s own inflation projections had the headline figure dropping to 2% by September 2025, in line with its recently updated remit.

Looks tough for the RBNZ to deliver a hike

There are a few reasons for Orr et al to consider another 25bps rate hike. Chief amongst them is the continued improvement in domestic sentiment. Various confidence surveys show a pickup in consumer sentiment and business activity despite the 525 bps of cumulative rate hikes over the two years. In the meantime, the RBNZ could be feeling some political pressure as the next General Election will be held in October 2023. The incumbent government is neck-and-neck with the main opposition group.

Having said that, it seems appropriate for the RBNZ to pause at this meeting and prepare for the August 16 gathering. This way RBNZ members will have enough time to evaluate the announcements and the impact of the end-of-July meetings by both the Fed and the ECB, and also examine their own freshly prepared economic projections. Compared to Western central banks, August is a “live” meeting for the RBNZ as it has announced rate movements in its recent history despite the understandably lower liquidity conditions.

Kiwi would enjoy some boost

The kiwi has been gradually weakening against the US dollar during 2023. Disappointment following the May 24 RBNZ meeting produced a sizeable sell-off that led to the lowest 2023 print of 0.5984 on May 31. The kiwi has been recovering somewhat since, as the market has turned its focus at the end-of-July Fed meeting.

Confirmation of expectations for a pause on Wednesday would cause a small disappointment and thus prompt a sell-off in the kiwi/dollar pair. In this case, a move towards the 0.6060-0.6092 area looks plausible. In the likely event of a rate hike, kiwi bulls will probably react with enthusiasm. The 0.6171-0.6187 area is unlikely to stand in the bulls’ way, as the main target would probably be closer to the 0.6272 area, a tad above the midpoint on the recent rectangle.

Australian Dollar Slips After Soft Chinese Inflation Data

- AUD/USD slides 1%

- China’s CPI and PPI slow in June

The Australian dollar continues to show sharp volatility. AUD/USD is down 0.80% on Monday, trading at 0.6637. The decline has erased most of the 1% gains we saw on Friday.

China’s inflation stalls

China’s consumer price inflation slowed to 0.0% y/y in June, below the 0.2% gain in May, which was also the consensus estimate. On a monthly basis, CPI declined by 0.2% for a second month, shy of the consensus estimate of 0.0%. China’s producer price index fell in June by 5.4% y/y, worse than the -4.6% reading in May and below the -5.0% consensus estimate.

The soft numbers indicate that China may have entered a phase of deflation and are further evidence that China’s recovery from Covid has been sluggish and uneven. The Chinese central bank cut lending rates in June and Goldman Sachs lowered its estimate for China’s GDP for 2023 from 6% to 5.4%.

China is Australia’s number one trading partner and the Australian dollar is sensitive to Chinese economic releases. The soft inflation data mean less economic activity and less demand for Australian exports to the Asian giant. In response, the Australian dollar has dropped sharply on Monday.

US nonfarm payrolls slip in June

Is the US labour market finally cooling down? Friday’s nonfarm payroll report was soft, falling from a downwardly revised 306,000 in May to 209,000 in June, missing the consensus estimate of 225,000. The drop in nonfarm payrolls was dramatic, especially with all the hype ahead of the release after the ADP Employment report posted a massive gain of 497,000, up from 267,000 and crushing the consensus estimate of 228,000. There were expectations that nonfarm payrolls would follow suit and force the Fed to keep raising rates.

In the end, nonfarm payrolls wasn’t much lower than the estimate, but the US dollar still took it on the chin against the major currencies on Friday, and the Aussie jumped by 1%. The markets have almost fully priced in a rate hike on July 26th but then expect a pause in September. If Wednesday’s inflation report misses expectations, there will be more talk of the Fed winding up its tightening cycle before the end of the year.

AUD/USD Technical

- AUD/USD is putting pressure on support at 0.6626. This is followed by support at 0.6560

- 0.6682 and 0.6732 are the next resistance lines

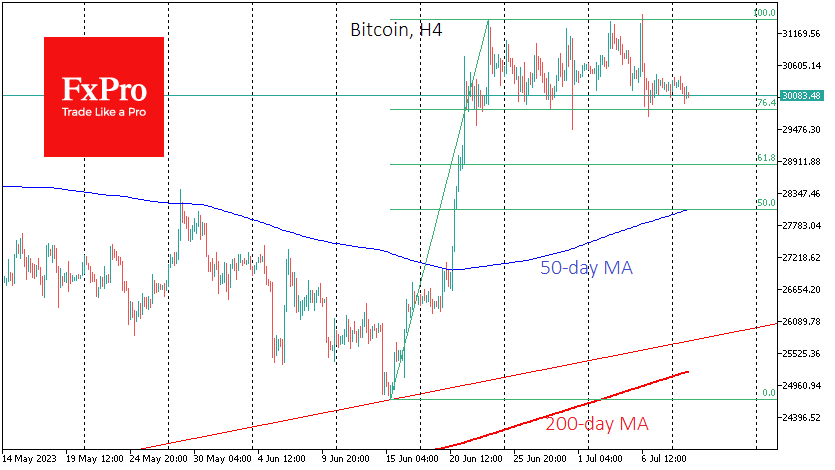

Bitcoin Holds Its Range, But Pressure Mounts

Market picture

Crypto market capitalisation has fallen 3% over the past seven days to $1.17 trillion. The Fear and Greed Index is at 56 (greed), having corrected from 62 a week earlier. Capitalisation has stabilised at $1.20 trillion in the first half of the week and at 1.18 in the second half. Capitalisation falls early on Monday, following the downtrend in global equity indices.

Bitcoin starts the week near $30.20K, having fended off attempts to break below a meaningful round level since the second half of last week. However, Bitcoin failed to break out of its range at the beginning of last week, where it has been consolidating for the past three weeks. We should be prepared for BTCUSD to go deeper into a correction just below $29.0K.

Ethereum lost 5.7% to $1860. Other leading altcoins in the top 10 fell between 0.2% (Tron) and 17% (Litecoin). The exception was Solana (+6.7%).

News background

According to JPMorgan, the approval of a spot bitcoin ETF will not significantly impact the crypto market. Such funds exist in Canada and Europe but have yet to attract significant investor interest. In addition, last year, the outflow of funds from gold ETFs did not benefit bitcoin funds, including futures ETFs.

Lightning Labs, the company behind the second-tier Lightning Network solution, has unveiled a set of tools that will make it easier for AI systems to work with the Bitcoin blockchain and the Lightning Network itself.

According to The Block Data, Binance’s market share decline has accelerated following the departure of several top executives. Only 58% of the total cryptocurrency trading volume is now on the platform.

Binance CEO Changpeng Zhao has denied media claims that the company has been struggling with senior staff for months.

The company’s lawyer said the BarnBridge DAO protocol faces a non-public investigation by the US Securities and Exchange Commission (SEC). The filing of claims against BarnBridge could indicate that the SEC is looking beyond targeting large cryptocurrency companies and has turned its attention to smaller players in the crypto market.

USD Breaks Lower

EUR/USD tests recent peak

The US dollar plunged after job growth slowed in June. The pair previously found support over 1.0840 at the base of a bullish momentum back in mid-June, which coincided with the 30-day SMA. The directional bias has remained upward from the daily chart’s perspective with a bullish MA cross as a sign of stabilisation in the two-week long consolidation. A pop above 1.0930 has put the single currency back on track and led to a test of the recent peak of 1.1010. 1.0890 is a fresh support in case the bulls need to catch their breath.

GBP/CAD aims at year’s peak

The Canadian dollar slumped as a rising jobless rate may ease the hike pressure on the BoC. A close above the June high of 1.6970 has attracted momentum buyers, sending the pair towards this year’s peak of 1.7140. 1.7070 is the intermediate hurdle in its way and the RSI’s overbought condition could prompt the bulls to take some profit. The support-turned-resistance of 1.6940 is the first level to expect renewed buying interest and 1.6850 on the 20-day SMA would be the bulls’ second line of defence.

GER 40 sees liquidation

The Dax 40 tumbled as central banks’ recent hawkish messages drove bond yields higher. A sharp fall below the demand zone 15650-15700 from a previous lengthy consolidation is a sign of capitulation by short-term bulls. The RSI has recovered into neutral territory as sellers took profit, but the index is yet to stabilise as traders might be wary of catching a falling knife. The start of a breakout rally (15400) at the end of March is the level to see if buyers are making their way back, and 15800 is the first hurdle to clear.

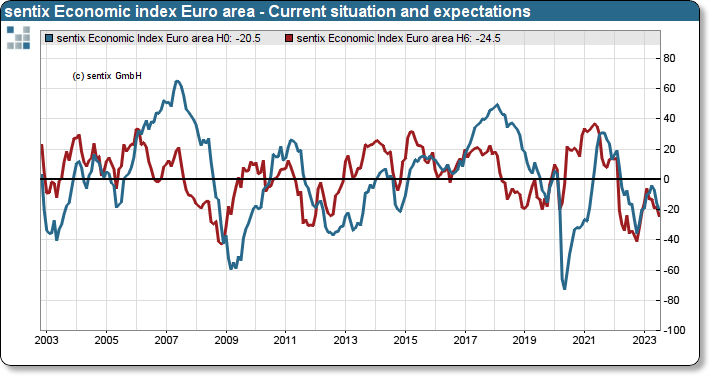

Eurozone Sentix fell to -22.5, more serious than usual summer lull

The economic outlook for Eurozone dimmed as Sentix Investor Confidence Index suffered its third consecutive monthly fall, reaching an eight-month low in July. The index tumbled from -17 to -22.5, significantly underperforming market expectations of -18.9. Both Current Situation Index and Expectations Index followed suit, dropping from -15.8 to -20.5 and from -18.3 to -24.5 respectively.

Sentix offered a stark assessment of the situation: "As of early July 2023, the Eurozone economy remains in recession mode." The investment group expressed skepticism about the potential sources of an economic boost, observing the U.S. economy's struggle to generate positive momentum, while downplaying any hope of central banks stepping in to counteract the economic downturn.

The investor sentiment towards the central banks' policies was especially pessimistic, with the topic index "central bank policy" plummeting from -13 to -24, indicating that investors foresee an intensification of restrictive monetary measures.

Compounding this gloomy outlook, the corresponding Inflation Barometer slid from -6 to -14.5 points, with Sentix cautioning that the current situation is "clearly more serious than the usual summer lull".

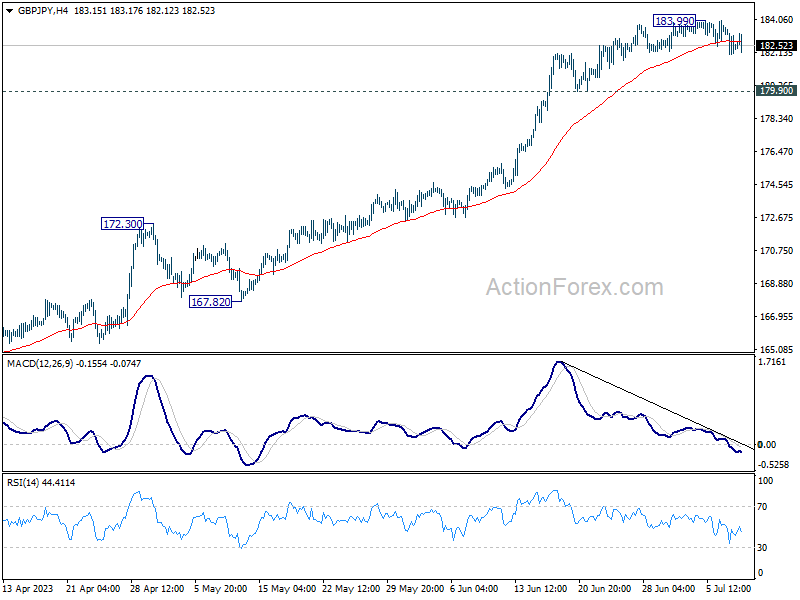

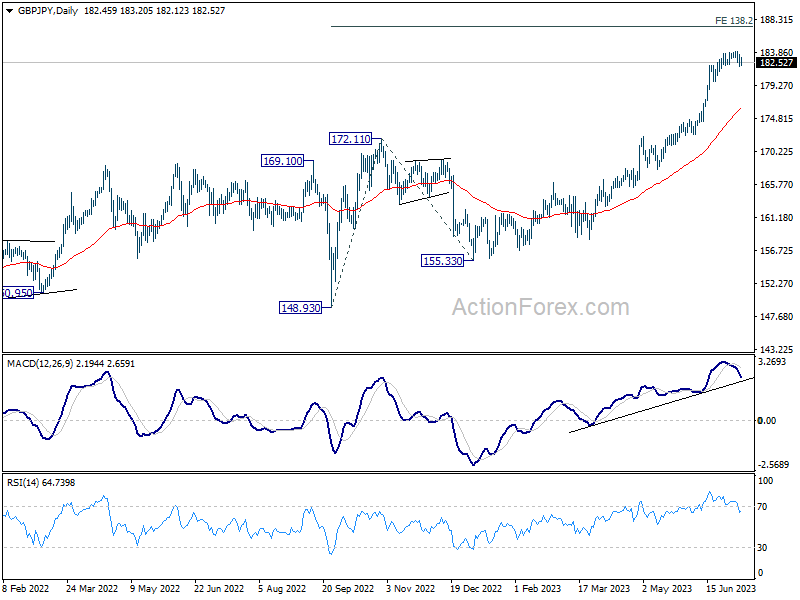

GBP/JPY Daily Outlook

Daily Pivots: (S1) 181.81; (P) 182.72; (R1) 183.41; More...

Intraday bias in GBP/JPY stays mildly on the downside at this point. Fall from 183.99 short term top would target 179.90 support. Firm break there will target 55 D EMA (now at 176.22). On the upside, break of 183.99 will resume larger up trend.

In the bigger picture, as long as 172.11 resistance turned support holds, uptrend from 123.94 (2020 low) is expected to continue. On resumption, next target is 195.86 (2015 high). Nevertheless, firm break of 172.11 will argue that larger correction is already underway.

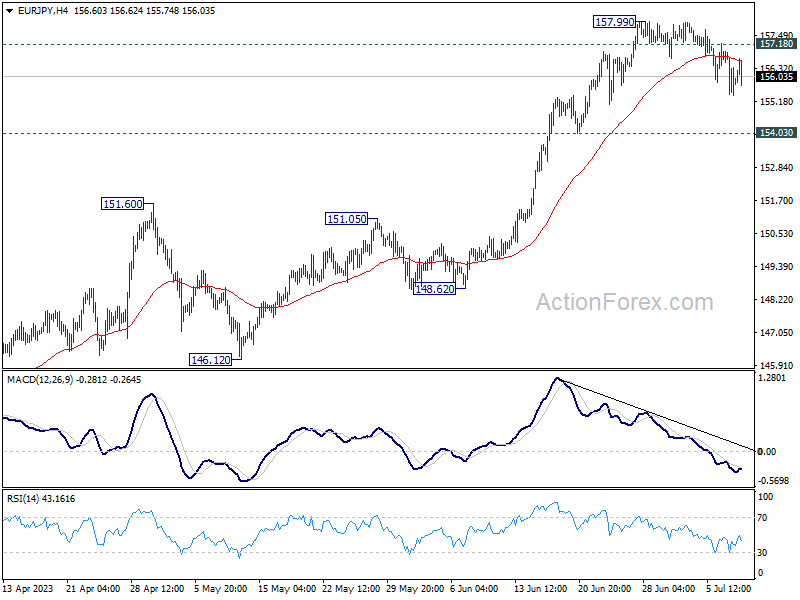

EUR/JPY Daily Outlook

Daily Pivots: (S1) 155.24; (P) 156.08; (R1) 156.78; More....

Intraday bias in EUR/JPY remains mildly on the downside at this point. Correction from 157.99 short term top should extend to 154.03 support or below. But overall outlook will stay bullish as long as 151.60 resistance turned support holds. Larger rally is still expected to resume through 157.99 after the correction completes. On the upside, above 157.18 minor resistance will bring retest of 157.99 high first.

In the bigger picture, as long as 151.60 resistance turned support holds, rise from 114.42 (2020 low) is in progress. On resumption, next target is 100% projection of 124.37 to 148.38 from 138.81 at 162.82. Nevertheless, sustained break of 151.60 will argue that larger correction is already underway.

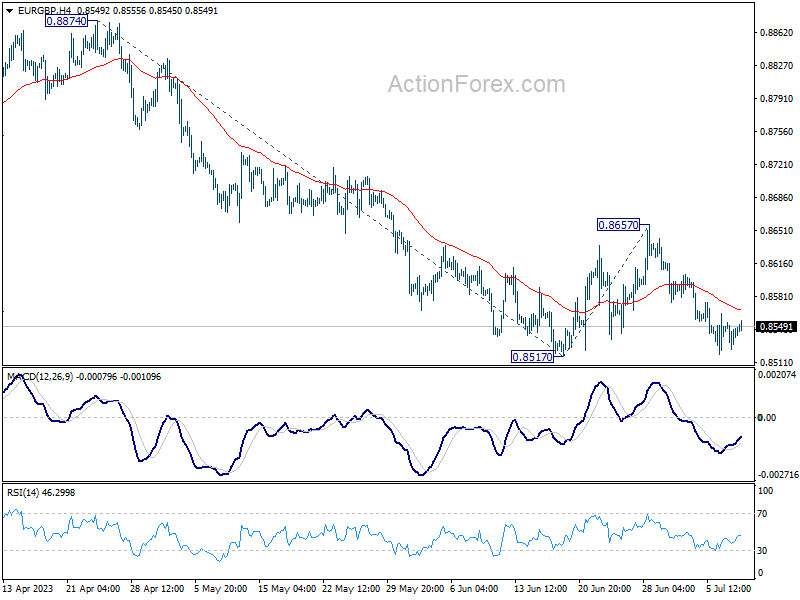

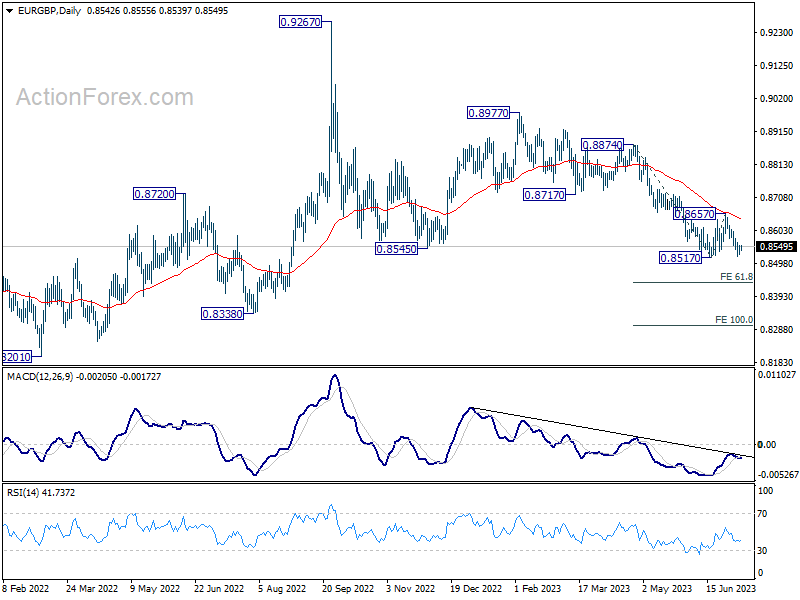

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8528; (P) 0.8541; (R1) 0.8557; More...

Intraday bias in EUR/GBP remains neutral for the moment and outlook stays bearish. On the downside, firm break of 0.8517 will resume the whole decline from 0.8977. Next target will be 61.8% projection of 0.8874 to 0.8517 from 0.8650 at 0.8436. On the upside, above 0.8657 resistance will turn bias to the upside for stronger rebound instead.

In the bigger picture, the down trend from 0.9267 (2022 high) is still in progress. It's seen as part of the long term range pattern from 0.9499 (2020 high). Deeper fall could be seen towards 0.8201 (2022 low). But strong support should be seen from there to bring reversal. This will now remain the favored case as long as 0.8717 support turned resistance holds.

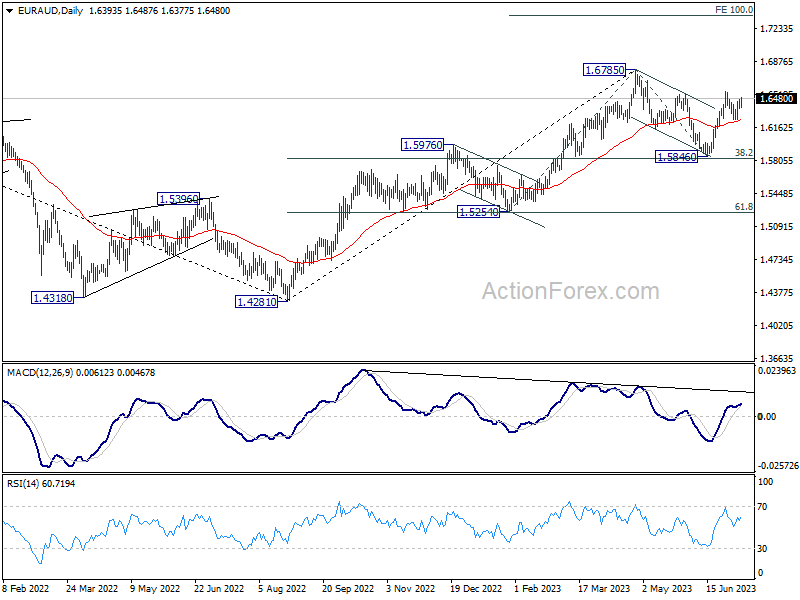

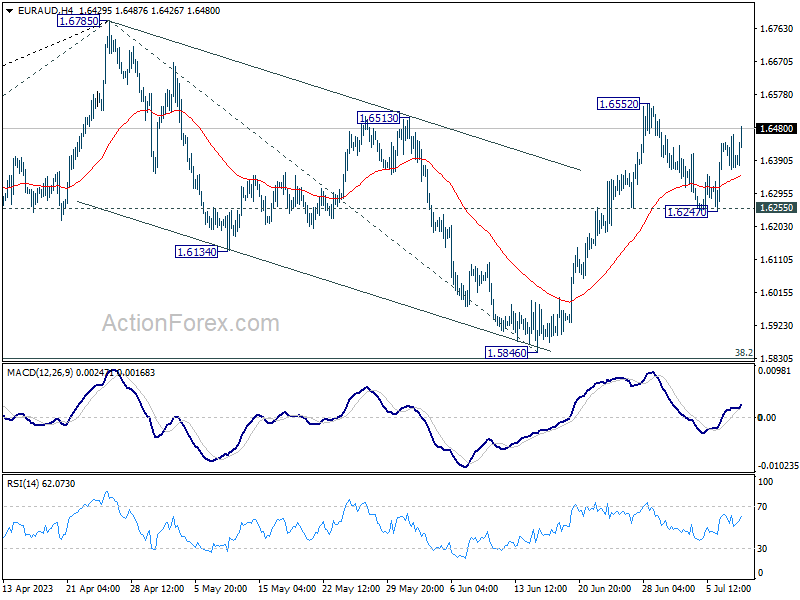

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6350; (P) 1.6407; (R1) 1.6447; More...

Intraday bias in EUR/AUD remains neutral for the moment. With 1.6255 support intact, further rally is expected. As noted before, correction from 1.6785 should have completed with three waves down to 1.5846. Above 1.6552 will target a retest on 1.6785 high next. Nevertheless, on the downside, firm break of 1.6255 will dampen this view and turn bias to the downside for 1.5846 support.

In the bigger picture, with 38.2% retracement of 1.4281 to 1.6785 at 1.5828 intact, rally from 1.4281 is still in progress. Firm break of 1.6785 will confirm rise resumption. Next target is 100% projection of 1.5254 to 1.6785 from 1.5846 at 1.7377. On the other hand, rejection by 1.6785 will extend the corrective pattern with another fall leg. But outlook will stay bullish as long as 1.5828 holds.