Sample Category Title

Yen Hopes for FX Intervention

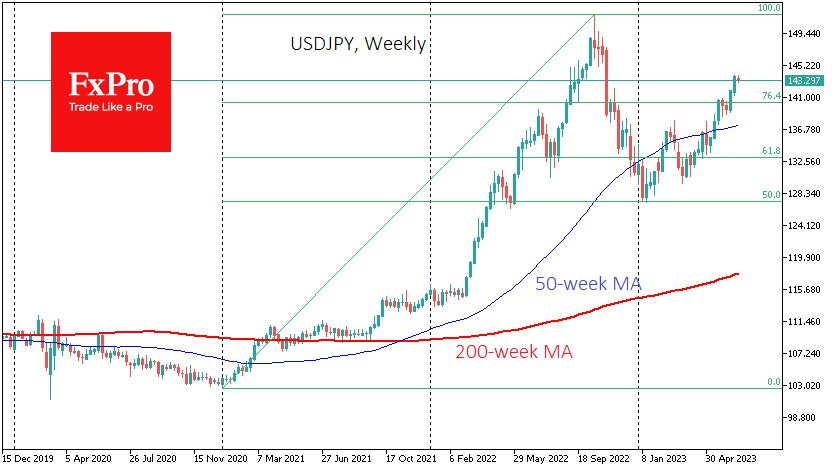

The Yen has been under pressure, losing 3.5% against the Dollar and over 5.6% against the Euro since the beginning of the month. The EURJPY has risen to its highest level since September 2008. The USDJPY is trading above 143.50, where the intervention took it in October and November last year, and close to the 1998 turning point.

The yen’s sharp weakness and proximity to historical highs have traders pricing in the likelihood that the central bank will intervene at the behest of the Ministry of Finance to strengthen the exchange rate. However, the nominal exchange rate means little to the government and the central bank, so the focus is on economic indicators.

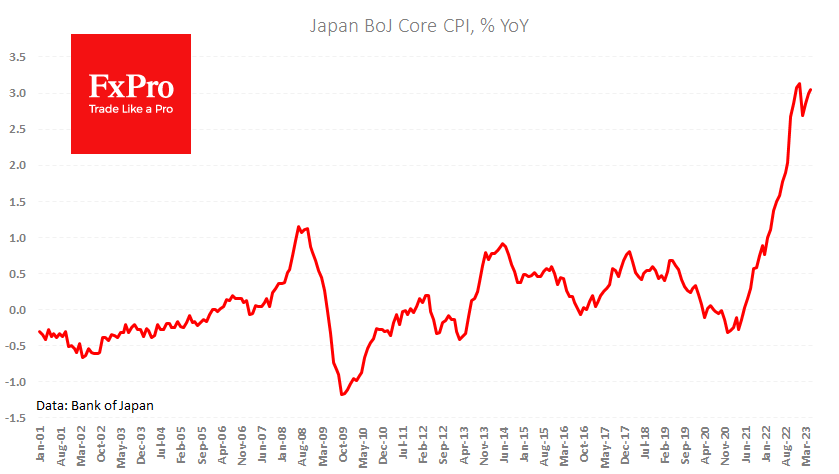

The most important of these is the Bank of Japan’s core CPI. Here we see an acceleration to 3.1% y/y from 3.0% the previous month and a low of 2.7% in February. Although the rate of price increases in Japan is significantly lower than in the US and Europe, there are no signs of a peak.

For the economy, this means that inflation expectations are becoming more firmly anchored. On the one hand, higher inflation is in line with central bank targets of previous decades. Hence the relative apathy of the BoJ, which has yet to take the slightest step to tighten policy in the fight against rising prices.

There is a belief that exchange rate depreciation improves export competitiveness. However, this rule only really applies when it is certain that the exchange rate will stay the same.

Therefore, the case for intervention to support the yen is growing, but it isn’t easy to foresee when it will occur. It could be the current USDJPY level of 143, where the pair has been stuck for a third day, or the 150 area, where the USD climbed in October 2022.

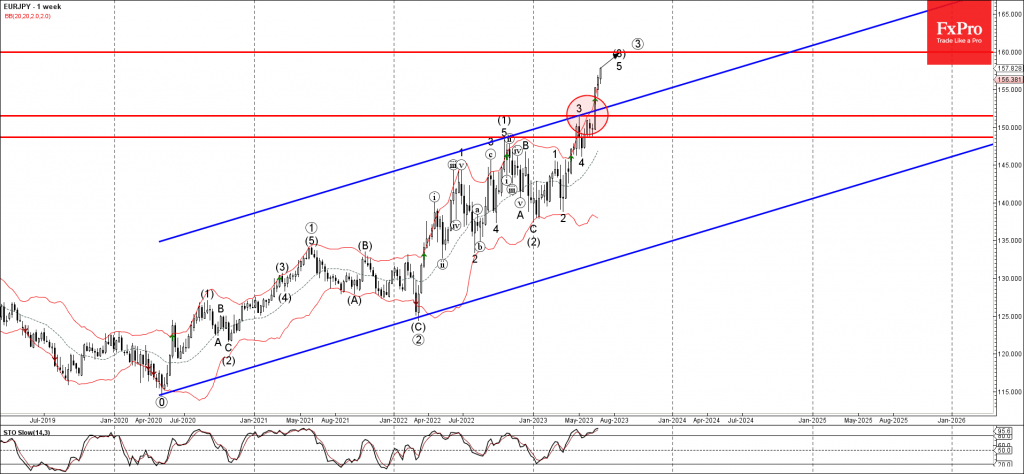

EURJPY Wave Analysis

- EURJPY under bullish pressure

- Likely to rise to resistance level 160.00

EURJPY under the bullish pressure after the price broke the resistance level 151.50 (which stopped the previous weekly impulse wave 3 in April).

The breakout of the resistance level 151.50 coincided with the breakout of the weekly up channel from 2020, which accelerated the active intermediate impulse wave (3).

Given the clear weekly uptrend, EURJPY can be expected to rise further toward the next resistance level 160.00, forecast price for the completion of the active impulse wave (3).

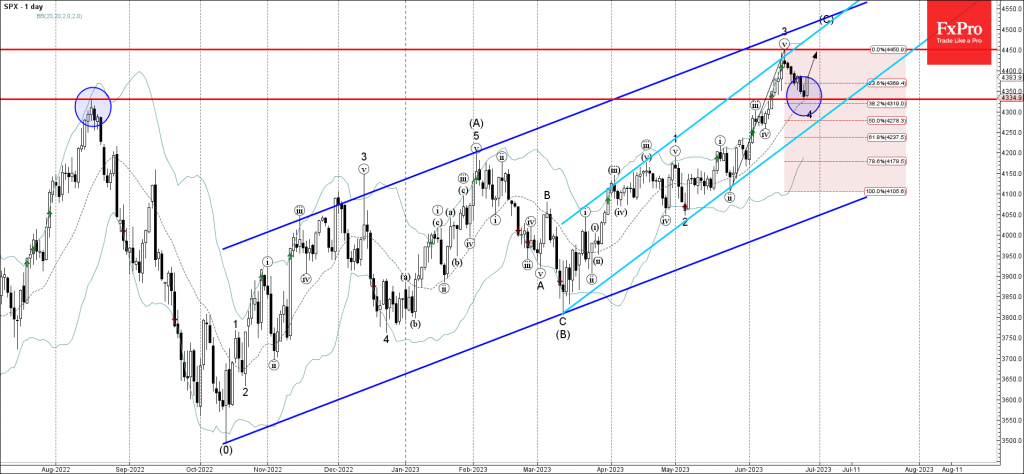

S&P 500 index Wave Analysis

- S&P 500 reversed from support level 4330.0

- Likely to rise to resistance level 4450.00

S&P 500 index recently reversed up from the key support level 4330.0 (former multi-month high from August of 2022, acting as the support after it was broken at the start of June) standing near the 38.2% Fibonacci correction of the upward impose from May.

The upward reversal from the support level 4330.00 stopped the previous short-term corrective wave 4.

Given the prevailing uptrend, S&P 500 index can be expected to rise further toward the next resistance level 4450.00 (top of the previous impulse wave 3).

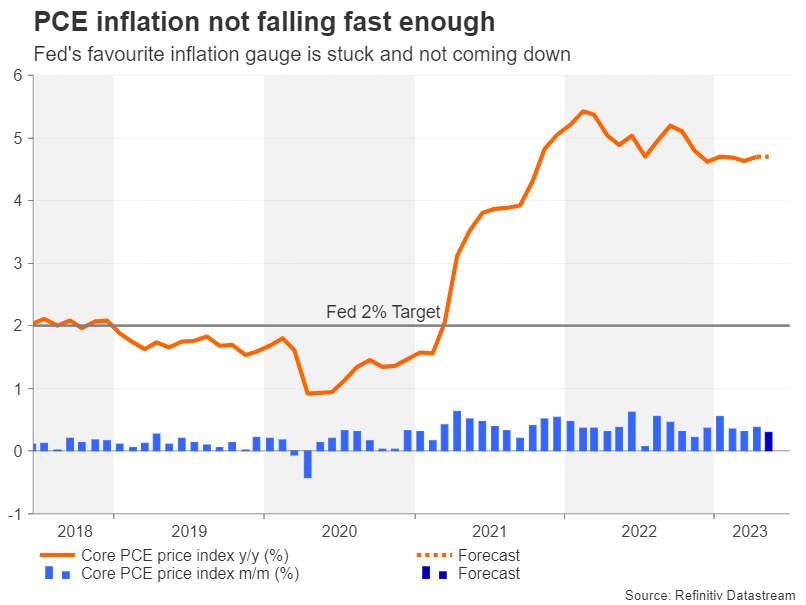

US Core PCE Data Might Fuel Sticky Inflation Fears as Dollar Stays Supported

A flurry of second-tier data releases in the United States this week will culminate on Friday with the all-important PCE inflation figures (12:30 GMT). Amid a very mixed picture on economic growth lately, the incoming gauges will be scrutinized closely. But ultimately, without any definitive red flags of an imminent recession, the best policy guide for Federal Reserve officials will be the core PCE price index. The US dollar stands ready to gain from any upbeat data following renewed jitters about Europe’s growth prospects.

A clouded outlook

Economic growth appears to be losing momentum on both sides of the Atlantic, although it is more pronounced in the euro area. Recession warnings have been sounding for some time now, but it’s hard to get an accurate read on the US economy. The downturn in the manufacturing sector appears to be deepening according to the latest PMIs by S&P Global but the slump in the housing market may be bottoming out. There is still no indication of a substantial cooling off in the red-hot labour market, which is encouraging consumers to keep on spending.

As things stand, it may take several more months for the fog to clear, hence why policymakers continue to fixate on sticky inflation as their primary concern, and on that front, Friday’s numbers are more likely to make the case for further rate increases this year than not.

Will core PCE become unstuck?

The core PCE price index, which the Fed prefers to use for achieving its 2% inflation target, has been stuck between 4.6% and 4.7% all year and the flat trend isn’t about to change if the forecasts are to be believed. Expectations are that the core PCE price index was unchanged at 4.7% on a yearly basis in May, although the month-on-month rate is projected to have slowed slightly to 0.3%, which may please the Fed.

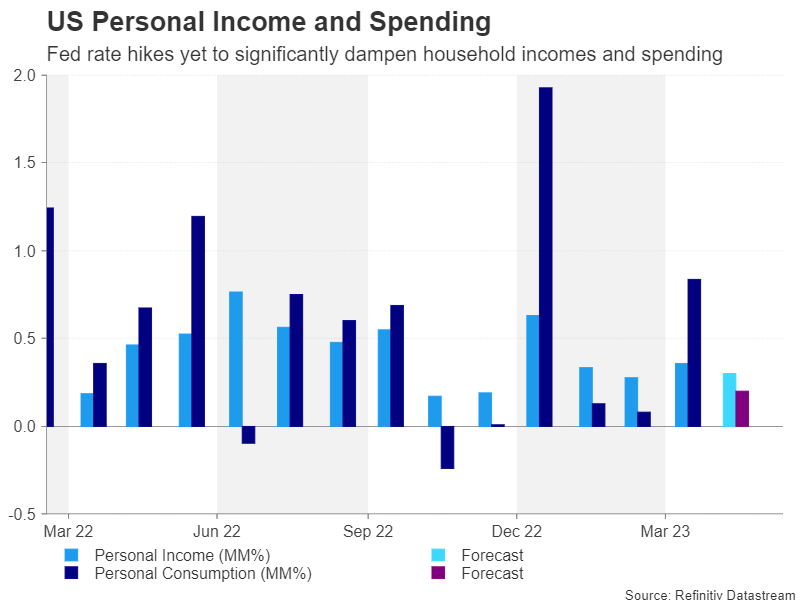

Personal consumption is also expected to have slowed, from 0.8% to 0.2% m/m in May, while personal income is forecast to have moderated marginally to 0.3% m/m.

Rate cuts bets are pared back

A day earlier, the final estimate of GDP growth in Q1 will likely get revised up slightly to 1.4%. The weekly jobless claims will also be important on Thursday amid somewhat higher numbers in recent weeks. The jobless claims provide a first look at how many people are applying for unemployment benefits. But even after the latest spikes, they remain at very healthy levels.

Thus, on the face of it, there are very few signs that the American economy is about to tip into recession, even after a cumulative 500 basis points of rate increases since 2022. This robustness is prompting many investors to think twice about betting on early rate cuts. However, market expectations remain hugely diverged from the Fed’s dot plot even after the latest repricing, and so, in the absence of a sharp drop in inflation or a surprise jump in unemployment, there are significant upside risks for the dollar in the medium term.

Dollar bulls refuse to go quietly

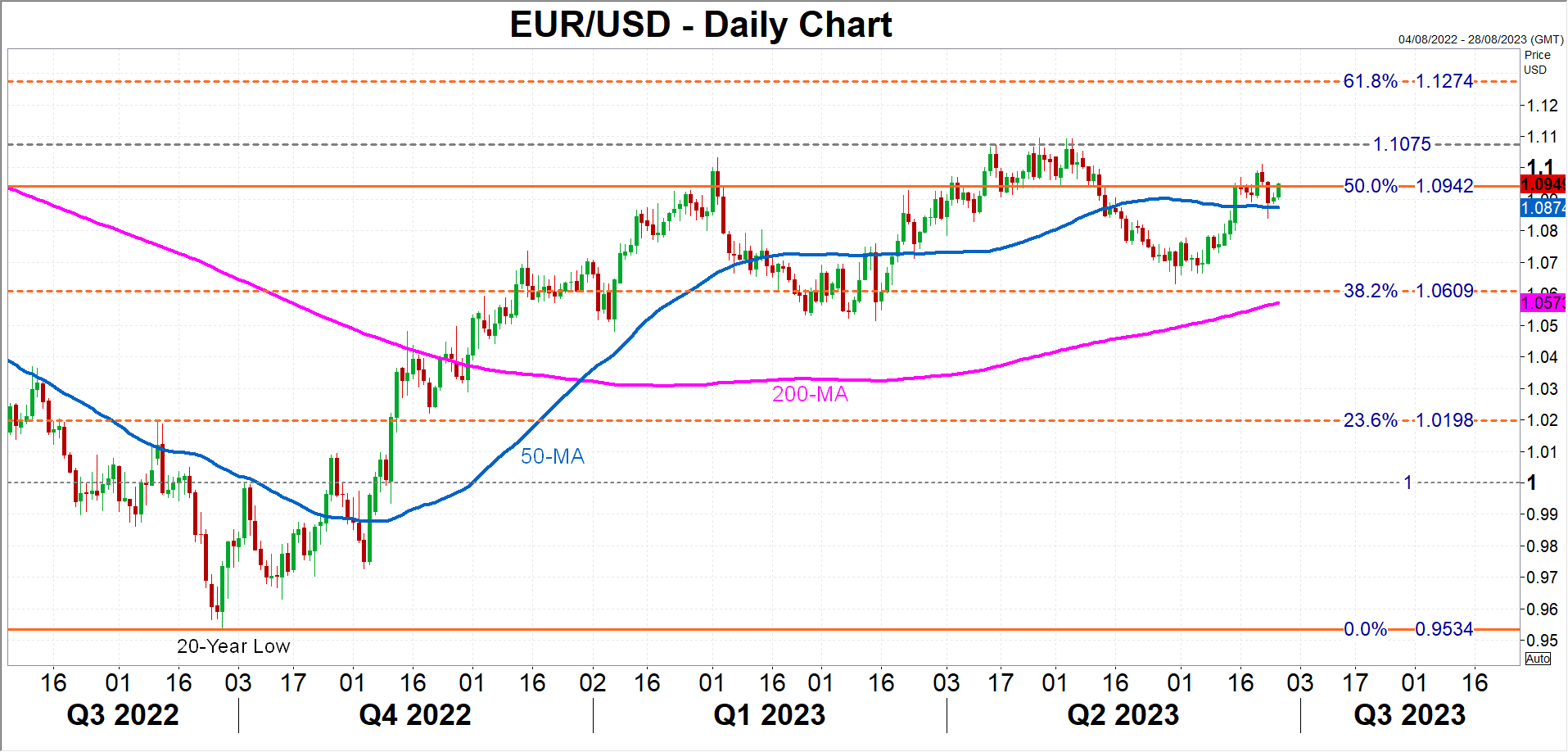

The euro’s advance against the greenback has stalled around the 50% Fibonacci retracement level of the 2021-2022 downtrend as the Eurozone recovery has stumbled and inflationary pressures in the region have started to dissipate, questioning the ECB’s resolve to hike rates a few more times this year. In the US, although inflation has come down considerably, it’s looking increasingly likely that it will need an extra nudge from the Fed to fall further, and the core PCE data may validate that view.

If the euro comes under fresh pressure on the back of a strong report on Friday, the 50-day moving average is the nearest support at $1.0873 that could defend against any declines. Should it be breached, the next critical region is likely to be between the 38.2% Fibonacci of $1.0609 and the 200-day moving average at $1.0572.

However, if the core PCE price index drops unexpectedly, the euro might manage to clear the 50% Fibonacci of $1.0942, after which, the $1.1075 area will attract interest again after the pair repeatedly failed to conquer it in April and May. A break higher would turn the spotlight on the 61.8% Fibonacci of $1.1274.

Banks in focus this week

In the bigger picture, the dollar has been consolidating against a basket of currencies for much of the year, mainly due to expectations of monetary policy divergence between the Fed and other central banks constantly swinging back and forth. The highly uncertain economic outlook is mostly to blame for this, but the banking turmoil also played a role.

The Fed will publish the results of its annual stress test on Wednesday, which are said to have been tougher this year, although the changes are unrelated to the strains in the banking sector and many smaller regional banks are not included. With the Fed’s post-banking crisis regulatory overhaul not due to be unveiled until later this summer, markets may cheer the stress test results as most banks are expected to pass with flying colours.

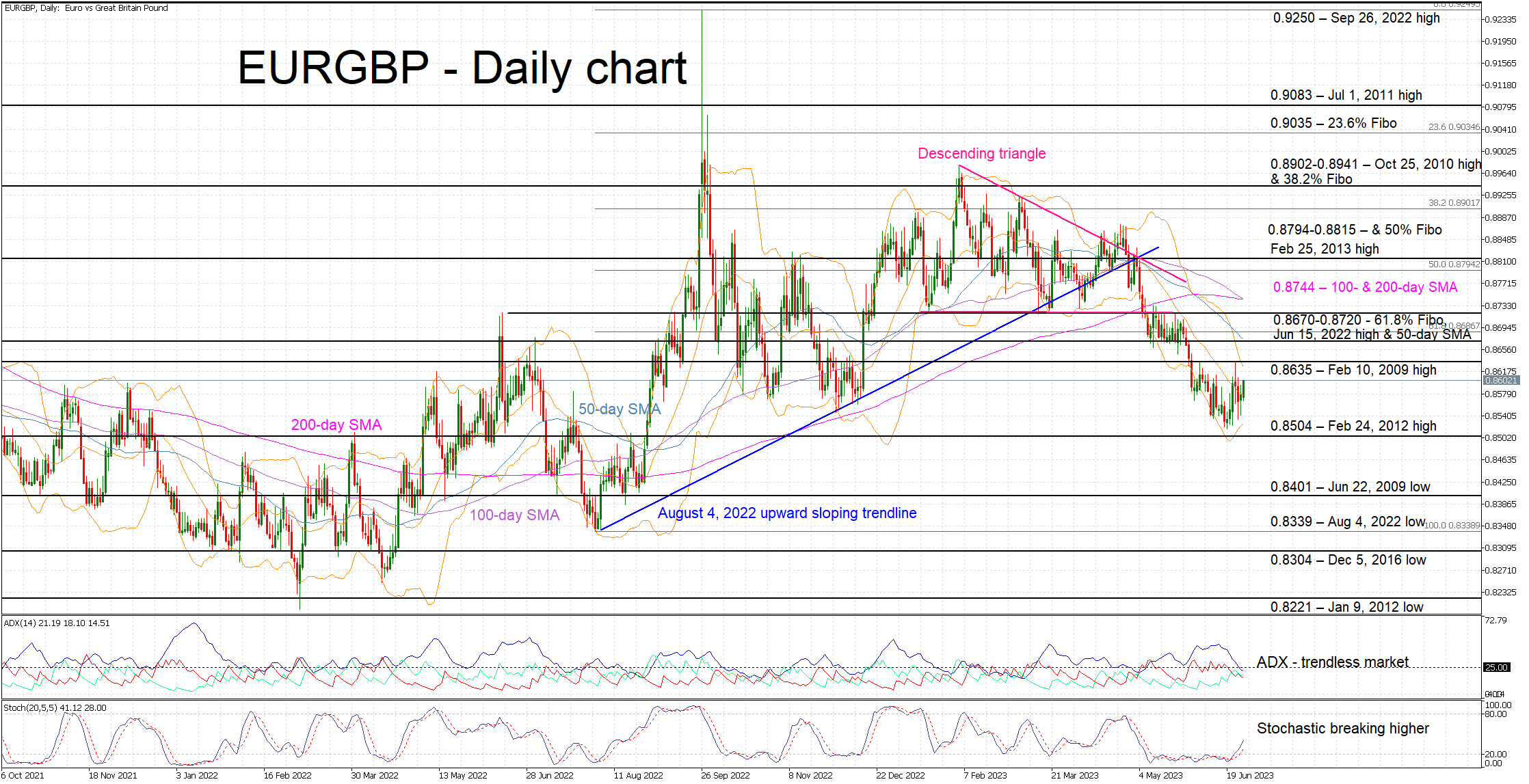

Can This Week’s Inflation Report Steer the ECB Away from Another Rate Hike?

We are getting closer to the end of June, and it is time for another euro area inflation report (Friday, 09:00 GMT). Despite the recent moderation in inflationary pressures, CPI releases continue to gravely affect market movements. The euro has been having a mixed month but a strong dataset this week could potentially help it recover some of its recent losses against the pound.

Where are we now?

The European Central Bank has been on a monetary policy restrictive path for the past 11 months, raising rates at every single meeting with the last rate move announced at the June 15 gathering. Lagarde was quite clear at the last press conference that the ECB is determined to continue hiking, unabated by the recent inflation figures and the weaker survey data.

The overwhelming majority of ECB members is treating the July rate hike as a given. Particularly as core inflation remains elevated, employment continues to tighten to record levels and the neighboring central bank, the Bank of England, has decided to ramp up its tightening strategy. The focus has turned to September, a slightly premature reaction considering there are three months left to that meeting.

However, the market is extremely interested in comments regarding the inflation outlook in the second half of 2023. The annual ECB forum on Central Banking is currently taking place at Sintra, Portugal, with the entire ECB executive council, including President Lagarde, expected to make an appearance, and most likely offer their insight on the inflation outlook.

More immediately, the repeated weak prints of the various business surveys, especially the recent German PMI figures and the German IFO survey, ought to have raised some eyebrows at the Bundesbank corridors and energized the ECB doves. Consequently, we expect these doves to highlight the need for restraint. Their attempt to affect the July meeting outcome appears to be doomed unless inflation this week produces a major downside surprise.

June’s CPI will be the key release of the week

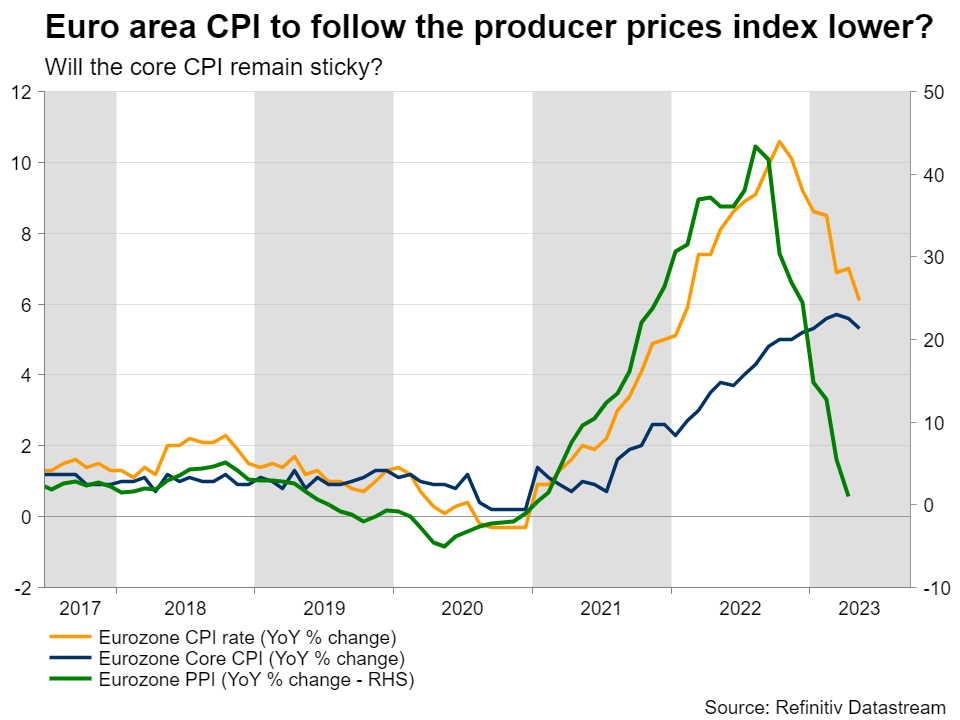

The preliminary numbers from Germany are expected on Thursday with the euro area aggregate scheduled to be released a day later. The market is looking for a small uptick in year-on-year German headline inflation, but the euro area headline figure is seen dropping to 5.6% YoY, the lowest print since March 2022. More interestingly, the euro area core subindex is forecast to accelerate to 5.5% YoY. Economists have long argued against the core CPI’s perceived ability to predict the future headline figures, but nevertheless it remains at high levels, raising the risk of inflation becoming entrenched in wage agreements and more generally in the public’s perception.

Should these forecasts be confirmed, the market reaction will probably be modest. More interestingly, a weaker set of results will probably not unsettle the market much, but it will definitely raise questions regarding the September meeting’s outcome. If there is an acute market reaction, it will probably be met with skepticism as the ECB will get another two CPI reports until September, and hence could check if inflation is indeed in a downward spiral. On the flip side, a strong set of data is unlikely to dramatically change ECB expectations, but it is bound to affect the euro, especially against the pound.

Euro suffering against the pound

This pair has been drawing much attention as the pound has recently shown unexpected strength even though the BoE is severely behind the curve in terms of rate hikes. Their recent 50 bps rate move decision could further support the pound, provided they stay on course and avoid a return to the mentality that led to inflation remaining north of 8% for 14 consecutive months.

Technically, the picture is not overly supportive of the pound. The recent sell-off failed to test the key 0.8504 level and the pair is now hovering around the December 2022 lows. Pound bulls could be taking a breather after a good run, but they need to be on their toes as the momentum indicators are flashing red. The stochastic oscillator has broken above its oversold area, sending a strong bullish message. Should the inflation data support the more hawkish outlook for the ECB, we could see the euro/pound pair going higher towards the key 0.8670-08720 area.

On the flip side, weak inflation figures coupled with lingering growth outlook concerns could provide a much-needed boost to the new euro/pound in recording a new 2023 low. If the February 24, 2012 high at 0.8504 is successfully broken, euro bears could then set their eyes lower and towards the 0.8400 area.

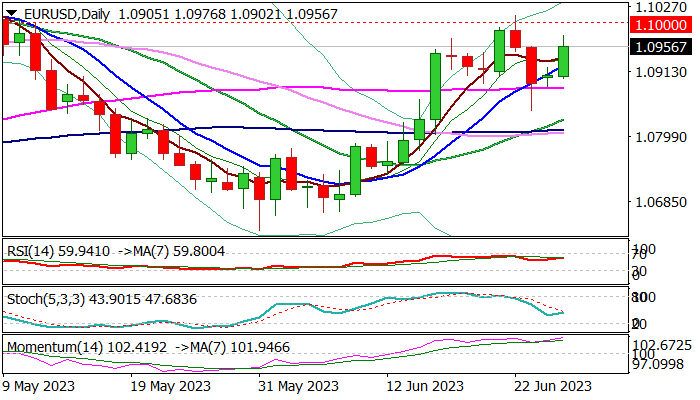

EUR/USD: Euro Rallies on ECB’s Fresh Hawkish Rhetoric

EURUSD was sharply up in European / early US session on Tuesday, reversing the large part of last Thu/Fri pullback and shifting near-term focus to the upside on signals that correction from new multi-week high (1.1012) is likely over.

The single currency received strong boost from ECB President’s hawkish comments today, as Mrs. Lagarde and majority of policymakers promoted higher interest rates for longer period, signaling new era of tight policy.

Lagarde said that inflation, initially thought to be transitory, became entrenched into the broader economy and will likely remain elevated for a longer period, with story of inflation peak being abandoned for now.

Although we did not hear something substantially new from the ECB, the news impacted market strongly, making the Euro more attractive to investors.

Improved picture on daily chart, as positive momentum continues to strengthen and MA’s returned to full bullish configuration, contribute to bullish outlook.

Fresh bears eye key barriers at 1.10 (psychological) and 1.1012 (June 22 peak) with firm break here to generate signal of bullish continuation and expose 2023 peak at 1.1095 (Apr 26).

Rising 10DMA (1.0925) offers solid support, followed by pivotal supports at 1.0900 zone (daily cloud top / Tenkan-sen).

Res: 1.0976; 1.1000; 1.1012; 1.1053.

Sup: 1.0940; 1.0925; 1.0905; 1.0883.

Sunset Market Commentary

Markets

The ECB-forum in Sintra shifted in higher gear with more speakers hitting the wires today. Kazaks from Latvia kicked off in early European dealings saying the risks of doing too little are still bigger than doing too much. More hikes are necessary and he added that should the central bank pause at some meeting, it doesn’t mean a stop to the tightening cycle altogether. He also called markets plain wrong in predicting rate cuts in 2024H1. His Baltic colleague Simkus struck a similar tone while ECB President Lagarde reaffirmed the central bank’s base case for another hike in July. She also noted it is unlikely that the ECB can soon say the rate peak has been reached and that the ECB must avoid expectations of a too-rapid policy reversal. Next we have Belgium’s Wunsch offering concrete guidance whether or not to expect a pause in September. For that to happen, core CPI must fall in all three occasions between now and that meeting. If analysts are right on this Friday’s June outcome (expectations for core CPI to rise to 5.5% from 5.3%), we’re looking at an ECB depo rate of 4.25% minimum. German Bunds trade rather stoic today. We do note a slight underperformance of the front, adding 1.4 bps vs longer maturities down 1.5-3.3 bps. In other ECB news, the central bank has allotted more than €18.5bn in its weekly MRO. Not a huge amount compared to the excess liquidity still sloshing around in markets but still the biggest uptake since 2017. The surge precedes a big TLTRO repayment (>€500bn) by financial institutions later this week. US Treasuries also trade without a clear direction. They temporarily neared the intraday lows again after stronger-than-expected durable goods orders, including the core shipment gauges. Two separate indicators tracking US housing prices also came in higher than anticipated, underscoring the ongoing bottoming out in the market. US yields (ex 2-y, benchmark change) currently shed 1.4-2.1 bps across the curve. The EuroStoxx50 on equity markets pared opening gains to trade flat. Wall Street opens in the green with the Nasdaq outperforming. The euro is having the upper hand on currency markets today. EUR/USD rebounds from 1.0906 to 1.0969 currently. It is being helped by an overall lackluster USD performance. The Japanese yen hits a new 15-y low against the euro at EUR/JPY 157.38 with hawkish ECB talk marking an ever bigger contrast with BoJ policy. EUR/GBP extends its recent bottoming out process. The pair is trying to recoup the 0.86 big figure.

News & Views

After an unexpected and broad-based decline in the June overall business Climate index yesterday, the German IFO institute today also reported a drop its exports expectations measure. Sentiment in the German export industry deteriorated notably this month expectations index falling from +1.0 in May to minus 5.6 points in June, marking the lowest level since November 2022. “In addition to weak demand on the German domestic market, we’re now also seeing fewer orders from abroad,” Klaus Wohlrabe, Head of Surveys at Ifo was quoted in the press release. The majority of industries expect exports to decline in coming months with only clothing manufacturers and the beverage industry expecting significant growth. Following months of growth, food companies now expect a drop in international sales. The outlook for the metal industry also worsened considerably as is the case for the furniture industry, which is suffering in part from the weak construction sector.

Canadian May inflation figures printed at consensus. Headline inflation rose by 0.4% M/M (from 0.7% in April) with the Y/Y figure slowing from 4.4% to 3.4%, the smallest increase since June 2021. The slowdown was largely driven by lower year-over-year prices for gasoline (-18.3%) resulting from a base effect. Excluding gasoline, prices rose 4.4% in May following a 4.9% increase in April. Service inflation slowed to 4.6% from 4.8%. The largest contributors to the month-over-month increase were mortgage interest costs and travel services, which includes traveler accommodation and travel tours. A 3-month moving average of some key inflation metrics flagged by the BoC slowed from around 3.8% to 3.7%. Canadian money markets are split 50/50 over whether the central bank will conduct a second-consecutive rate hike at its July 12 policy meeting after a two meeting-pause earlier this year. The loonie showed some volatility on the releases but holds near pre-CPI levels of 1.3155.

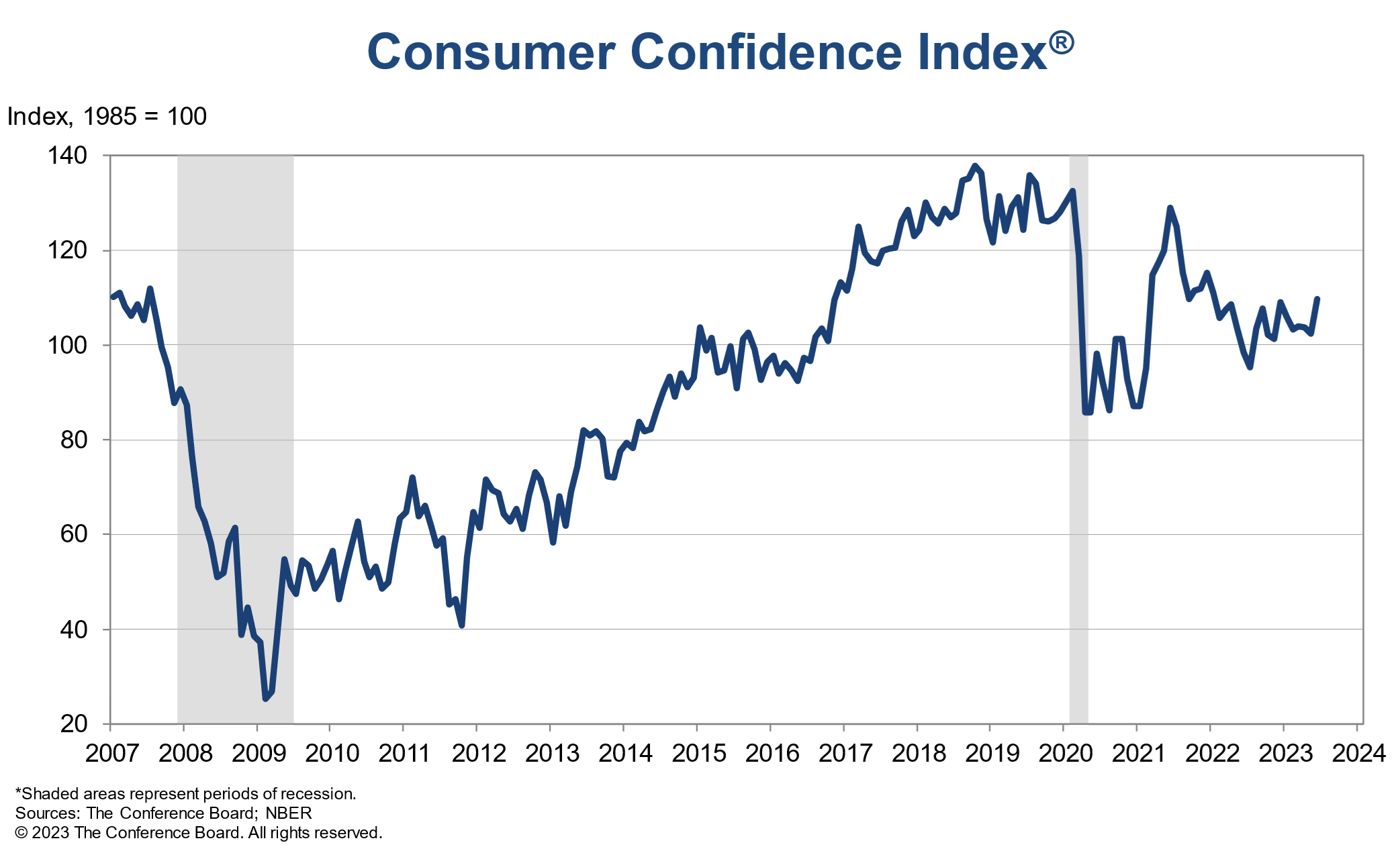

US consumer confidence rose to 109.7, highest since Jan 2022

US Conference Board Consumer Confidence rose from 102.5 to 109.7 in June, well above expectation of 103.6. Present Situation Index rose from 148.9 to 155.3. Expectations Index jumped from 71.5 to 79.3, but remained below 80 which was associated with a recession within the next year.

"Consumer confidence improved in June to its highest level since January 2022, reflecting improved current conditions and a pop in expectations," said Dana Peterson, Chief Economist at The Conference Board.

"Assessments of the present situation rose in June on sunnier views of both business and employment conditions."

"Although the Expectations Index remained a hair below the threshold signaling recession ahead, a new measure found considerably fewer consumers now expect a recession in the next 12 months compared to May."

Canada: Inflation Cools in May

Consumer price inflation cooled to 3.4% year-on-year (y/y) in May, down from 4.4% in April – right in line with market expectations. That marks the slowest pace of inflation in nearly two years.

Prices at the pump were the main story. Favourable base year effects leave gasoline prices down 18.3% lower than a year ago, an even sharper decline than -7.7% in April. Excluding gasoline, the CPI rose 4.4% in May, following a 4.9% increase in April.

Inflation at the grocery store remained firm, with prices up 9% y/y in May.

Shelter inflation eased slightly to 4.7%, down from 4.9% in April. Mortgage interest cost inflation keeps rising, up 29.9% versus a year ago in May. Statistics Canada cited that it is the largest single contributor to the year-on-year pace of inflation. Excluding higher mortgage costs, inflation would have been 2.5% y/y in May.

There were signs of easing price pressures for consumer goods. Clothing and footwear inflation was 0.7% y/y in May, down from 2.5% y/y in April and furniture prices were down 2.9% y/y, the smallest increase in three years. Overall durable goods inflation cooled to 1.0% y/y in May from 2.2% in April.

Services inflation cooled from 4.8% y/y in April to 4.6% y/y. Our measures of "supercore" inflation – a measure of core services inflation – remained elevated at 5.5% y/y, from 5.7% in April thanks to a sizeable increase in travel services prices.

The Bank of Canada's underlying inflation pressures cooled below the 4% mark in May. CPI-trim eased to 3.8% y/y versus 4.2% in April and CPI-median at 3.9% versus 4.3% y/y in April. Looking at the recent monthly trends, CPI- trim on a three-month annualized basis was at 3.8%, down from 3.9% and median at 3.6%, down from 3.8% in April.

Key Implications

Canadian inflation continued to cool in May, but progress is unlikely to be enough to prevent the Bank of Canada from raising rates in July. Improvements in core inflation are slow, particularly on the services side, with inflation picking up in discretionary areas like travel services and restaurant meals (6.8% y/y in May). Cooler goods inflation is welcome, but the BoC has likely been counting on that already as supply chain snarls improve.

Looking at the Bank's core measures, Governor Macklem may have a Bon Jovi earworm, humming, "whoa, we're half way there…". But, there is still a ways to go to get inflation all the way back to 2%. And the bank would rather not be "livin' on a prayer", and is likely to take rates another quarter point higher in July to ensure demand, and hence price pressures cool further.