Sample Category Title

A Slow Start to the Week, Central Bank Speak and Key Data Eyed

It's been a relatively slow start to the week so far but things are likely to pick up with more appearances from prominent central bankers and key data due for release in the coming days.

Equity markets are a little higher early in the European session after what has been a tough couple of weeks. Stubborn inflation has investors concerned that there may be a much heavier economic price to pay for restoring price stability which appears to have shaken confidence a little.

Not only are more rate hikes being priced in but the prospect of rate cuts this year has become more fantasy than reality. Obviously, some are faring much worse than others, the UK being a prime example, but progress has also been much slower than hoped elsewhere and the likelihood is that getting from 4% to 2%, for example, may prove more challenging again. We need to see some concrete signs of progress or sentiment could suffer much further.

Oil remains volatile but range-bound amid an uncertain outlook

Oil is trading a little higher on Tuesday after rebounding off the lows in very choppy conditions in recent days. While there will of course be various contributing factors behind these moves, the fact remains that oil is trading within the same range it has for almost two months and what we're continuing to see is it fluctuate roughly between the upper and lower boundaries.

Brent has fallen just short of the previous lows now on four occasions in the last couple of months which may suggest we're seeing some consolidation but if we are, it's extremely gradual and could last many more months yet. I would say recent trading is merely a reflection of the immensely uncertain environment caused by extremely stubborn inflation pressures and the ever-changing expectations for interest rates.

Gold weighed down by stubborn inflation and higher rate expectations

Stubborn inflation is proving to be challenging for gold which has continued to pare its 2023 gains over the last couple of weeks. There has clearly been a view until recently that inflation will start to fall considerably which will enable central banks to stop hiking, maybe even consider easing, boosting gold's prospects. But as yet, we're seeing quite the opposite.

Traders still appear somewhat reluctant to accept that it won't happen, which has helped bring some resilience to the yellow metal during declines. That belief hasn't yet been rewarded, with gold now more than 7% off its highs and the recent break below $1,940 could be another sign of vulnerability.

Can Bitcoin be propelled higher on ETF excitement?

We've seen some consolidation in bitcoin in recent days after it hit fresh highs for the year late last week. There's been no shortage of crypto newsflow but the excitement around an ETF may well be what's pulled traders back in. Either way, it promises to be an intriguing and potentially volatile second half to the year as we await the outcome of that and the action brought against various exchanges from the SEC.

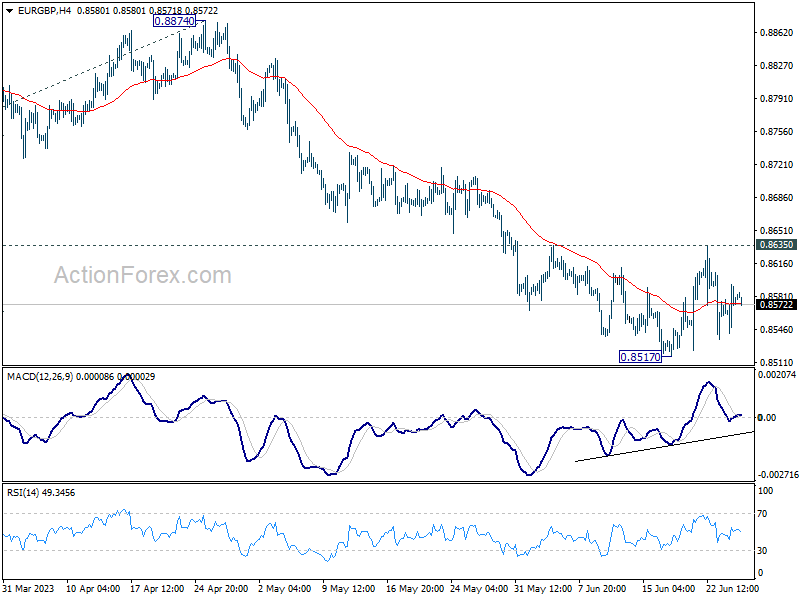

EUR/GBP Tests Resistance

USD/CHF forms triple bottom

The US dollar bounces as risk aversion compounds the Fed’s hawkish stance. The bull’s second attempt came to a halt at 0.9010 which is a support-turned-resistance after a mid month sell-off. A failure to break higher would indicate that the path of least resistance will be down, putting the recent double bottom of 0.8910 at risk, and where a breakout would force early bulls’ to bail out and trigger a new round of selling to the daily support and May’s lows of 0.8820, potentially causing a bear continuation in the medium-term.

EUR/GBP tests resistance

The pound pared gains as traders worried about the impact of the BoE’s large-sized hike on the economy. The latest spike prompted sellers to cover and eased the pressure. But a doji at 0.8635 at the confluence of a previous swing high and the 30-day SMA is a show of rejection in this important supply zone. A pullback to the base of the bullish momentum at 0.8530 is a test of buyers’ resolve as its breach would invalidate the rebound and cause an extension to 0.8400. 0.8600 is the resistance as the RSI recovers to the neutral area.

US 30 struggles for support

The Dow Jones 30 slips as investors assess the political turmoil in Russia. The index is still striving to hold onto its gains after lifting the key daily resistance of 34300. A fall below 33900 has put the short-term bulls on the defensive, leading to more profit-taking as they stepped to the side. 33600 over the 30-day SMA is another level to see whether buyers would stake in again and keep the bullish MA cross intact on the daily chart. Failing that, 33100 would be the next stop. 34000 is the closest hurdle in case of a bounce.

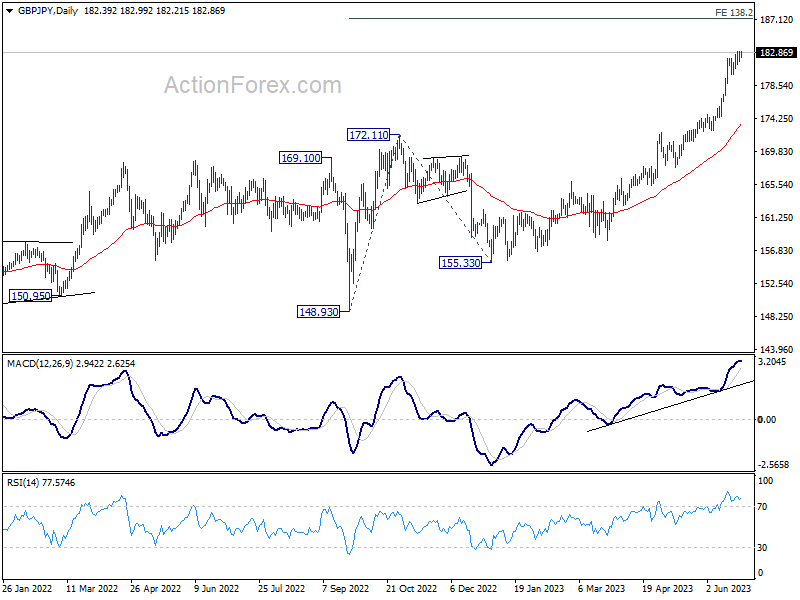

GBP/JPY Daily Outlook

Daily Pivots: (S1) 181.75; (P) 182.37; (R1) 183.06; More...

Further rise is expected in GBP/JPY despite loss of upside momentum. Current up trend should target 138.2% projection of 148.93 to 172.11 from 155.33 at 187.36 next. On the downside, however, break of 179.90 support will confirm short term topping, and turn bias back to the downside for deeper pull back.

In the bigger picture, up trend from 123.94 (2020 low) is extending. Next target is 195.86 (2015 high). For now, medium term outlook will remain bullish as long as 172.11 resistance turned support holds, even in case of deep pull back.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 155.92; (P) 156.33; (R1) 156.90; More....

Intraday bias in EUR/JPY stays neutral at this point, and further rally is expected with 154.30 support intact. Above 156.92 will resume larger up trend to 100% projection of 139.05 to 151.60 from 146.12 at 158.67. On the downside, break of 154.03 will turn bias back to the downside for deeper pull back.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 100% projection of 124.37 to 148.38 from 138.81 at 162.82. For now, medium term outlook will remain bullish as long as 148.38 resistance turned support holds, even in case of deep pull back.

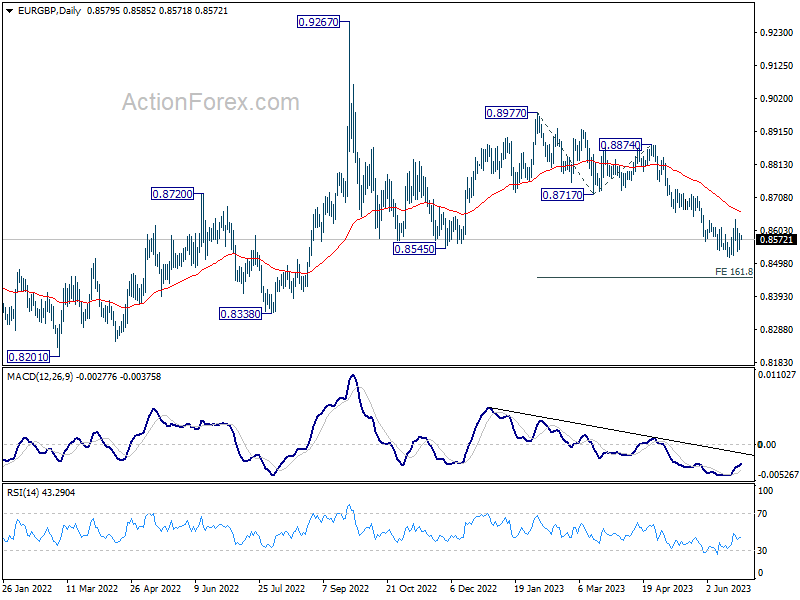

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8550; (P) 0.8572; (R1) 0.8602; More...

Range trading continues in EUR/GBP and intraday bias stays neutral. On the downside, break of 0.8517 will resume the fall from 0.8977 to 161.8% projection of 0.8977 to 0.8717 from 0.8874 at 0.8453. Nevertheless, decisive break of 0.8635 will confirm short term bottoming, and bring stronger rebound to 55 D EMA (now at 0.8661) and above.

In the bigger picture, the down trend from 0.9267 (2022 high) is still in progress. It's seen as part of the long term range pattern from 0.9499 (2020 high). Deeper fall would be seen towards 0.8201 (2022 low). But strong support should be seen from there to bring reversal. This will now remain the favored case as long as 0.8717 support turned resistance holds.

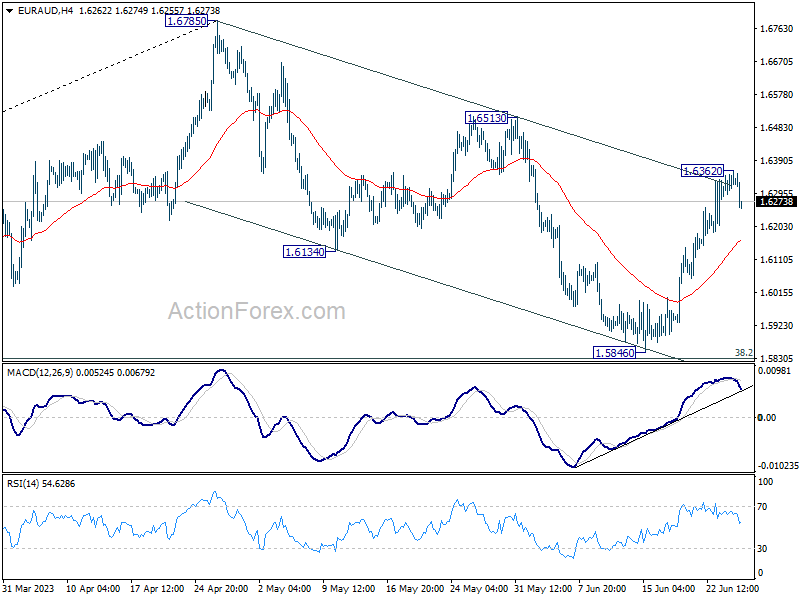

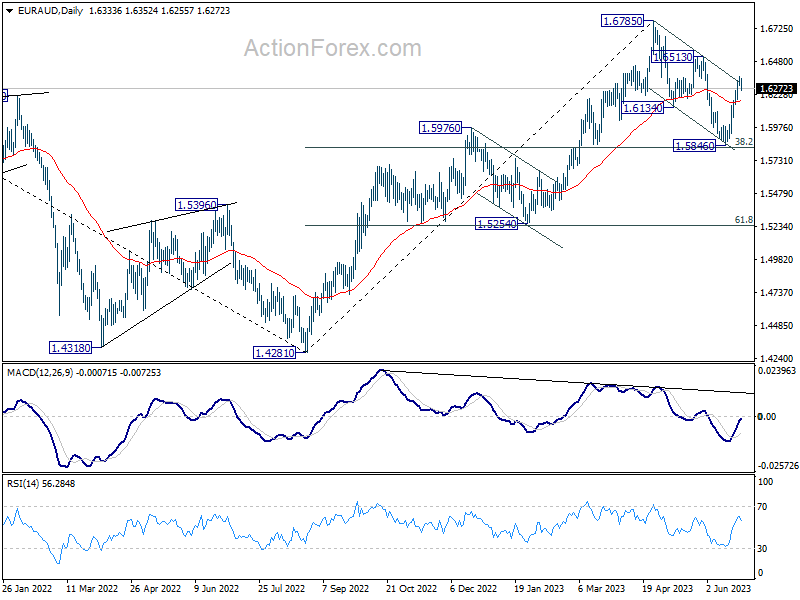

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6301; (P) 1.6333; (R1) 1.6369; More...

Intraday bias in EUR/AUD is turned neutral with current retreat. But outlook is unchanged that corrective fall from 1.6785 should have completed with three waves down to 1.5846. On the upside, above 1.6362 will target 1.6513 resistance first. Firm break there will confirm this case and target 1.6785 high next. Nevertheless sustained trading below 55 4H EMA (now at 1.6160) will bring retest of 1.5846 support instead.

In the bigger picture, with 38.2% retracement of 1.4281 to 1.6785 at 1.5828 intact, rally from 1.4281 is still in progress. Firm break of 1.6785 will confirm rally resumption. Rejection by 1.6785 will extend the corrective pattern with another fall leg. But outlook will stay bullish as long as 1.5828 holds.

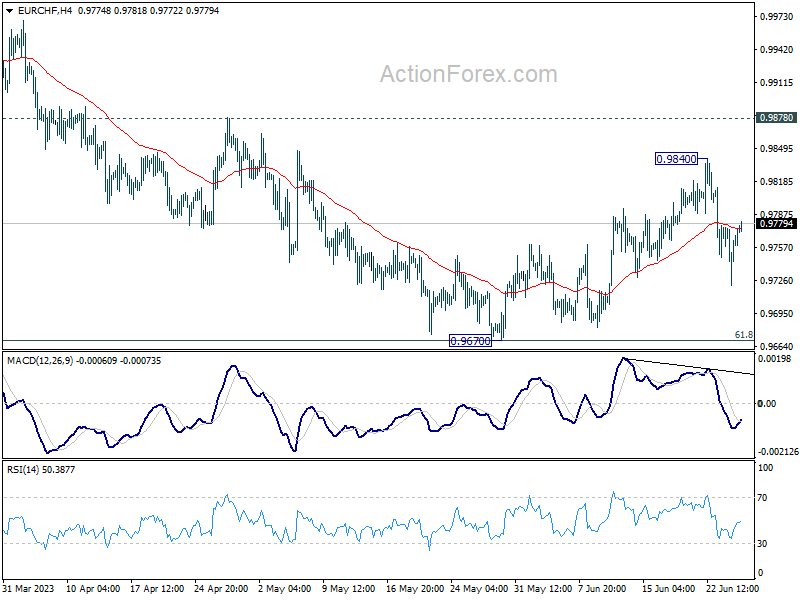

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9736; (P) 0.9756; (R1) 0.9789; More...

Intraday bias in EUR/CHF is turned neutral with current development. But another fall cannot be ruled out, to retest 0.9670 low. Sustained break there will resume the whole fall from 1.0095. Nevertheless, break of 0.9840 will resume the rebound from 0.9670 to 0.9878 resistance.

In the bigger picture, medium term outlook is staying bearish as the pair is capped below falling 55 W EMA (now at 0.9918). Down trend form 1.2004 (2018 high) is in favor to extend through 0.9407 at a later stage. Nevertheless, decisive break of 38.2% retracement of 1.1149 to 0.9407 will raise the chance of bullish trend reversal.

GBPUSD Bullish Sequence Suggests Pullback to Find Support

GBPUSD shows an incomplete bullish sequence from 9.26.2022 low and 3.8.2023 low favoring further upside. Near term, rally from 5.26.2023 low ended wave 1 at 1.2848 as a 5 waves impulse Elliott Wave structure. Up from 5.26.2023 low, wave ((i)) ended at 1.2545 and pullback in wave ((ii)) ended at 1.2367. Pair then rallied again in wave ((iii)) towards 1.2699, and dips in wave ((iv)) ended at 1.2626. Final leg higher wave ((v)) ended at 1.2848 which completed wave 1.

Pullback in wave 2 is now in progress to correct cycle from 5.26.2023 low. Internal subdivision of the pullback is unfolding as a double three Elliott Wave structure. Down from 6.16.2023 high, wave (a) ended at 1.269 and wave (b) ended at 1.2842. Wave (c) lower ended at 1.2682 which completed wave ((w)). Rally in wave ((x)) is in progress as a zigzag where wave (a) ended at 1.2749 and wave (b) ended at 1.2687. Expect wave (c) to end below wave 1 at 1.2848 and pair to turn lower in wave ((y)) as a zigzag structure to complete wave 2. Then as far as pivot at 1.236 low stays intact, expect pair to find support in 7 swing for further upside.

GBPUSD 1 Hour Elliott Wave Chart

GBPUSD Elliott Wave Video

https://www.youtube.com/watch?v=I9X09PZXhmA

EUR/USD Went Nowhere

Markets

Friday’s risk-off market setting persisted at the European start to the trading week. The Russian uprising offered at least part of the explanation from a short term dynamic point of view. German Ifo business sentiment fell back in June (especially expectations) but that didn’t came as a surprise after last week’s dismal German PMI. Risk sentiment turned more neutral from the start of US dealings with US Treasuries for example paring all gains into the close. The US eco calendar was empty apart from a $42bn 2-yr Note auction. Investors other than primary dealers took around 87% of the amount on offer (68.5% for indirect bid), which is one of the highest shares ever. The auction stopped slightly through the 1 PM bid side with the auction yield (4.67%) just below the 16-yr high from February (4.673%). The bid cover was 2.86. The US Treasury continues its end-of-month refinancing with a $43bn 5-yr Note auction tonight. Daily changes on the US yield curve ranged between flat and -2.3 bps (5-yr) with the belly of the curve outperforming the wings. German Bunds outperformed with yields losing 2.2 bps (2-yr) to 4.7 bps (5-yr). From a technical point of view, the German 10-yr yield tests support coming from an incoming upward trend line with the 200d mavg being the high profile mark at 2.26%. European stock markets ended mixed as did the US (ranging from flat for Dow to -1.16% for Nasdaq). EUR/USD went nowhere, starting and ending the day just above 1.09.

ECB Lagarde today gives the formal start to the ECB’s annual forum in Sintra. Tomorrow’s line-up is the interesting one with a panel discussion featuring ECB Lagarde, Fed Powell, BoE Bailey and BoJ Ueda. At yesterday’s opening reception and dinner, IMF first deputy managing director Gopinath (former chief economist) presented those attending with three uncomfortable truths for monetary policy. The first is that inflation is taking too long to get back to target. The second is that financial stresses could generate tensions between central banks’ price and financial stability objectives. The final one is that going forward, central banks are likely to experience more upside inflation risks than before the pandemic. Eco data today include US durable goods orders, house prices, Richmond Fed manufacturing index and consumer confidence. We fear that their market-moving potential will be rather low given this week’s back-loaded events (apart from Sintra EMU CPI and US PCE deflators). The market path of least resistance remains the risk-off dynamic.

News and views

The British Retail Consortium (BRC) reported that the rise in UK shop prices slowed in June to 8.4% from 9% In May. Monthly price growth decelerated from 0.5% M/M to 0.2% M/M. Food price inflation remained at 0.5% M/M but eased from 15.4% Y/Y to 14.6%. Non-food prices were unchanged for the month and decelerated from 5.8% to 5.4% Y/Y. The CEO of the BRC said that “if the current situation continues, food inflation should drop to single digits later this year.” The BRC press release also indicates that if global supply chain costs continue to fall, we may now be past the peak of price increases. However with most households needing to save money, purchasing behavior for the rest of this year is still likely to shift towards essential needs with discretionary consumption being deprioritized or delayed.

Yesterday, economic sentiment indicators published in Hungary and the Czech Republic continued to indicate ongoing soft economic conditions. Hungarian GKI economic sentiment dropped from -16.1 to -20.4. Business confidence dropped from -4.7 to -118, the lowest level since November 2020. Confidence in the future dropped in all four sectors surveyed (industry, construction, trade and services). According to GKI, consumer confidence ‘improved’ slightly from -48.5 to -44.8, but remains at historically low levels. In the Czech republic, the composite confidence indicator also declined from 1.4 to -2.6. Business confidence slowed from 6.9 to 2.2. Indices declined in the four subcategories as well. Consumer confidence declined slightly further from -20.3 to -21.8. Despite soft eco data published yesterday, local currencies continued to perform well with the forint strengthening close to the cycle peak (EUR/HUF 369). Also the Czech korona s strengthened from 23,73 to close near 23.635.

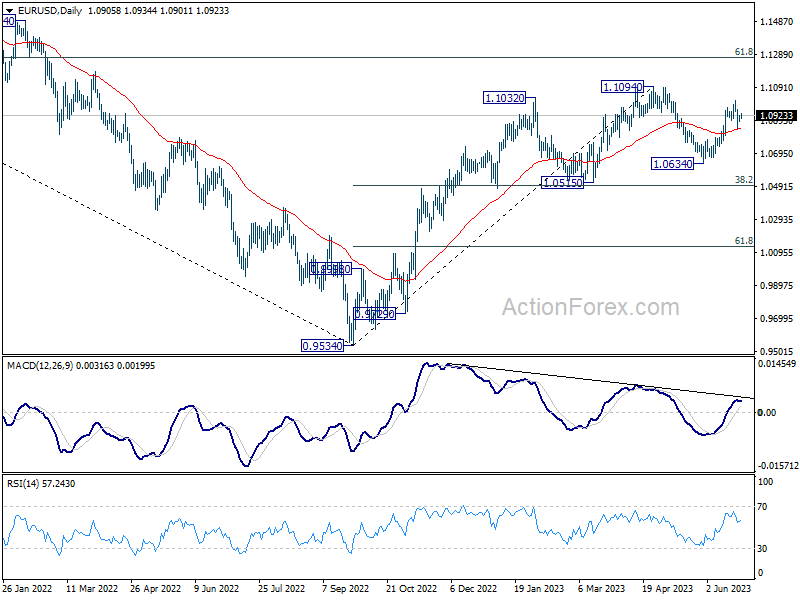

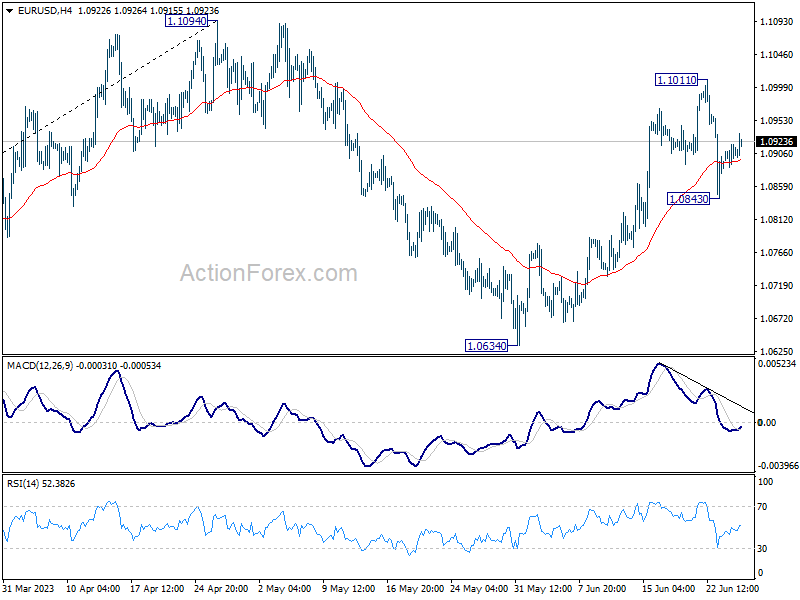

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0889; (P) 1.0904; (R1) 1.0921; More...

Intraday bias in EUR/USD is turned neutral with current recovery. But risk stays mildly on the downside for now. Fall from 1.1101 is seen as the third leg of the corrective pattern from 1.1094. Sustained break of 55 D EMA (now at 1.0838) will target 1.0634 support and below. however, break of 1.1011 will target a test on 1.1094 high instead.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).