Sample Category Title

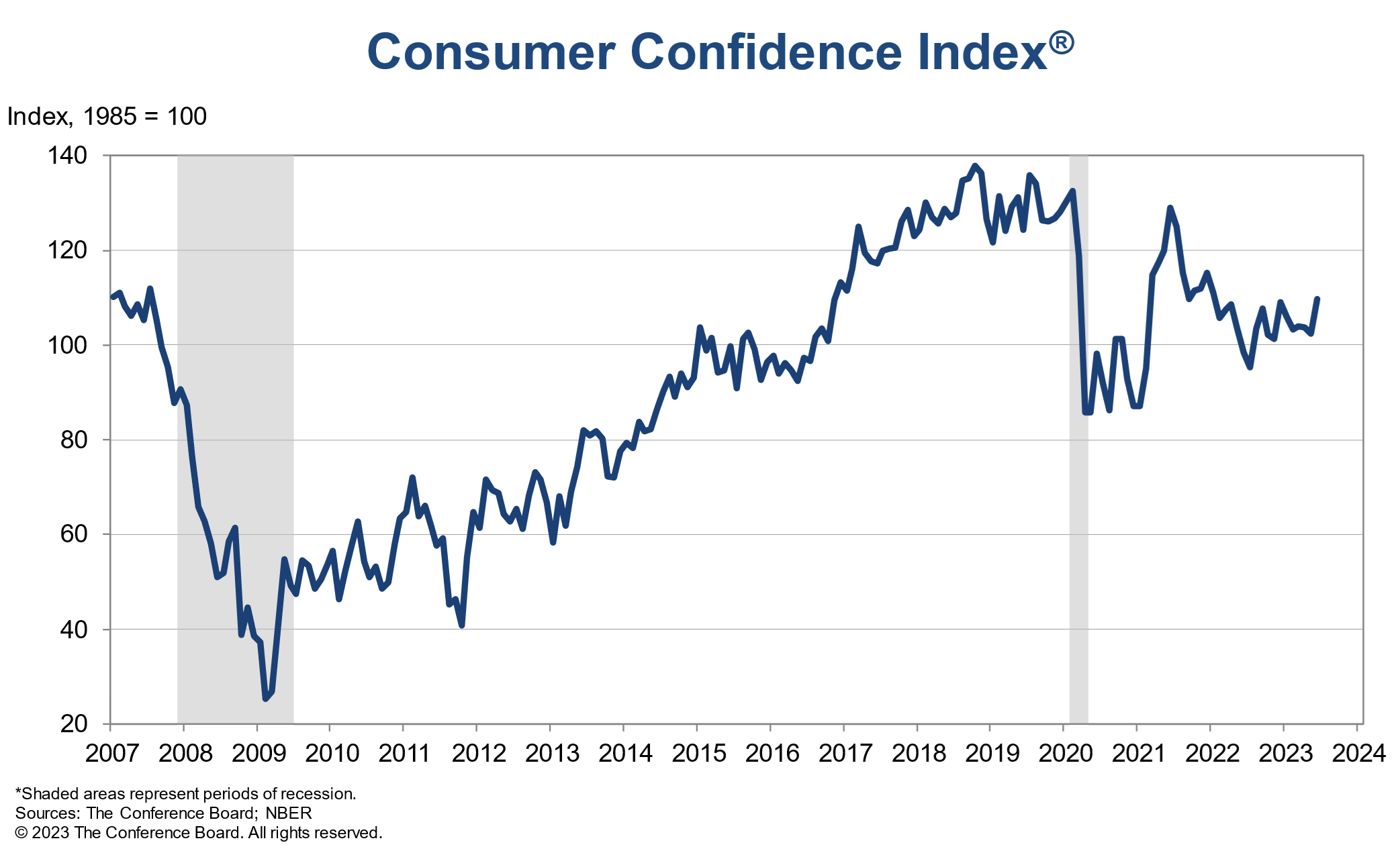

US consumer confidence rose to 109.7, highest since Jan 2022

US Conference Board Consumer Confidence rose from 102.5 to 109.7 in June, well above expectation of 103.6. Present Situation Index rose from 148.9 to 155.3. Expectations Index jumped from 71.5 to 79.3, but remained below 80 which was associated with a recession within the next year.

"Consumer confidence improved in June to its highest level since January 2022, reflecting improved current conditions and a pop in expectations," said Dana Peterson, Chief Economist at The Conference Board.

"Assessments of the present situation rose in June on sunnier views of both business and employment conditions."

"Although the Expectations Index remained a hair below the threshold signaling recession ahead, a new measure found considerably fewer consumers now expect a recession in the next 12 months compared to May."

Canada: Inflation Cools in May

Consumer price inflation cooled to 3.4% year-on-year (y/y) in May, down from 4.4% in April – right in line with market expectations. That marks the slowest pace of inflation in nearly two years.

Prices at the pump were the main story. Favourable base year effects leave gasoline prices down 18.3% lower than a year ago, an even sharper decline than -7.7% in April. Excluding gasoline, the CPI rose 4.4% in May, following a 4.9% increase in April.

Inflation at the grocery store remained firm, with prices up 9% y/y in May.

Shelter inflation eased slightly to 4.7%, down from 4.9% in April. Mortgage interest cost inflation keeps rising, up 29.9% versus a year ago in May. Statistics Canada cited that it is the largest single contributor to the year-on-year pace of inflation. Excluding higher mortgage costs, inflation would have been 2.5% y/y in May.

There were signs of easing price pressures for consumer goods. Clothing and footwear inflation was 0.7% y/y in May, down from 2.5% y/y in April and furniture prices were down 2.9% y/y, the smallest increase in three years. Overall durable goods inflation cooled to 1.0% y/y in May from 2.2% in April.

Services inflation cooled from 4.8% y/y in April to 4.6% y/y. Our measures of "supercore" inflation – a measure of core services inflation – remained elevated at 5.5% y/y, from 5.7% in April thanks to a sizeable increase in travel services prices.

The Bank of Canada's underlying inflation pressures cooled below the 4% mark in May. CPI-trim eased to 3.8% y/y versus 4.2% in April and CPI-median at 3.9% versus 4.3% y/y in April. Looking at the recent monthly trends, CPI- trim on a three-month annualized basis was at 3.8%, down from 3.9% and median at 3.6%, down from 3.8% in April.

Key Implications

Canadian inflation continued to cool in May, but progress is unlikely to be enough to prevent the Bank of Canada from raising rates in July. Improvements in core inflation are slow, particularly on the services side, with inflation picking up in discretionary areas like travel services and restaurant meals (6.8% y/y in May). Cooler goods inflation is welcome, but the BoC has likely been counting on that already as supply chain snarls improve.

Looking at the Bank's core measures, Governor Macklem may have a Bon Jovi earworm, humming, "whoa, we're half way there…". But, there is still a ways to go to get inflation all the way back to 2%. And the bank would rather not be "livin' on a prayer", and is likely to take rates another quarter point higher in July to ensure demand, and hence price pressures cool further.

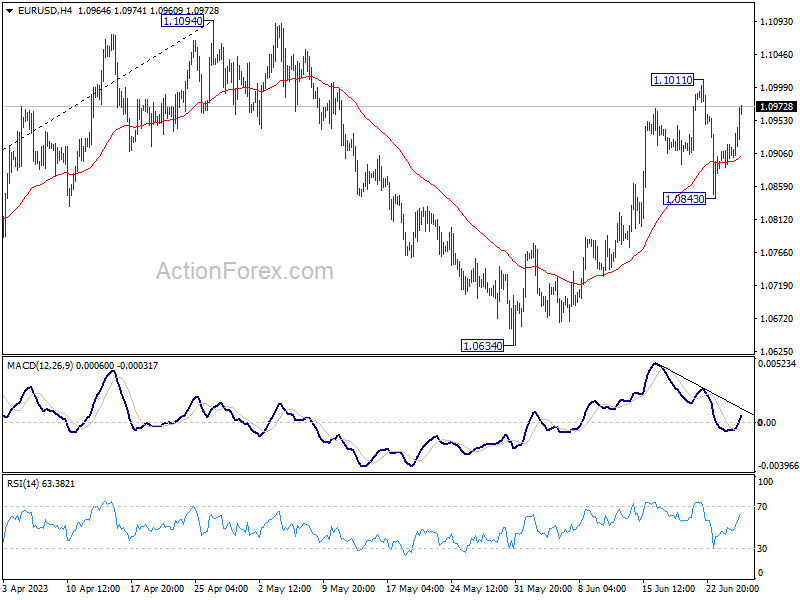

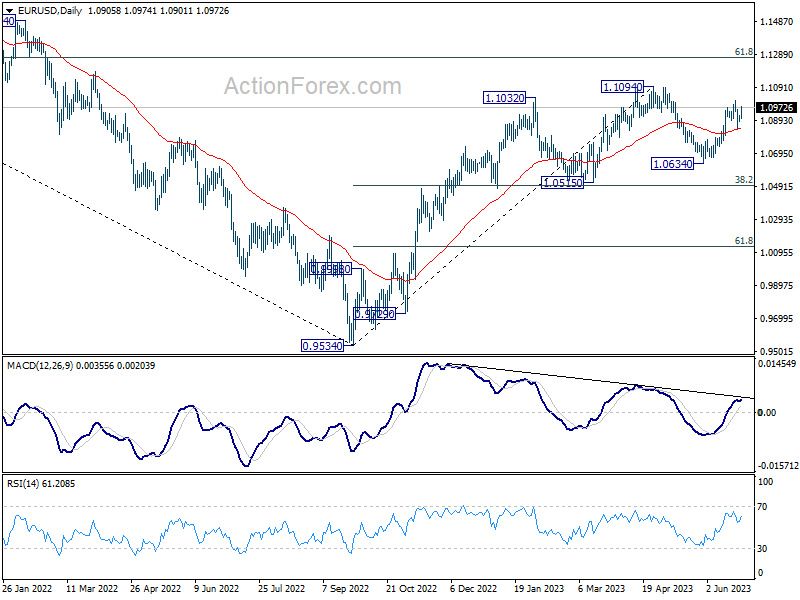

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0889; (P) 1.0904; (R1) 1.0921; More...

EUR/USD rebounds notably today but stays below 1.1011. Intraday bias remains neutral first. Nevertheless strong support from 55 D EMA (now at 1.0838) retains near term bullishness. Break of 1.1011 will resume the rally from 1.0634 and target 1.1094 resistance. Decisive break there will resume larger up trend from 0.9534.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

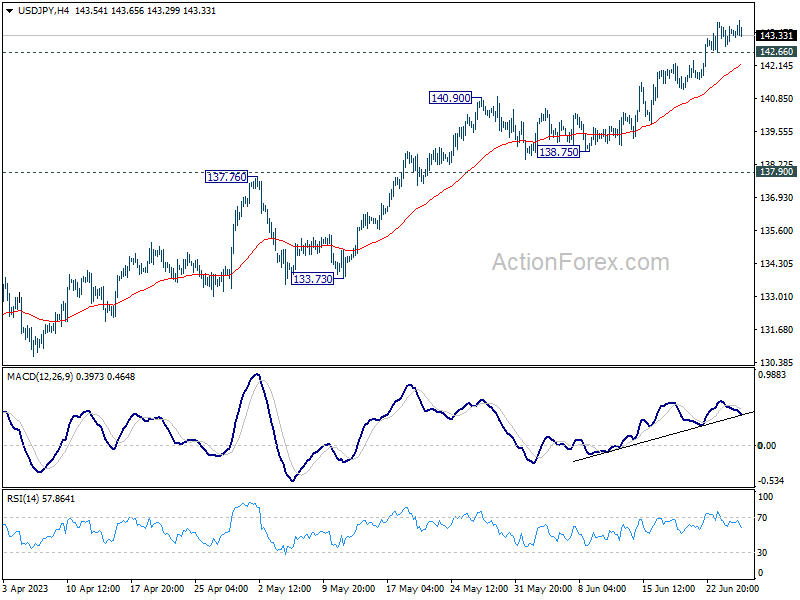

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.07; (P) 143.39; (R1) 143.84; More...

Further rise is expected in USD/JPY despite loss of upside momentum. Current rally from 127.20 should target 161.8% projection of 127.20 to 137.90 from 129.62 at 146.93. On the downside, below 142.66 minor support will turn bias neutral again and bring lengthier consolidations first.

In the bigger picture, rise from 127.20 is currently seen as the second leg of the corrective pattern from 151.93 high. Further rally is expected as long as 137.90 resistance turned support holds, to retest 151.93. But strong resistance could be seen there to limit upside. Break of 137.90 will indicate the the third leg has started back towards 127.20.

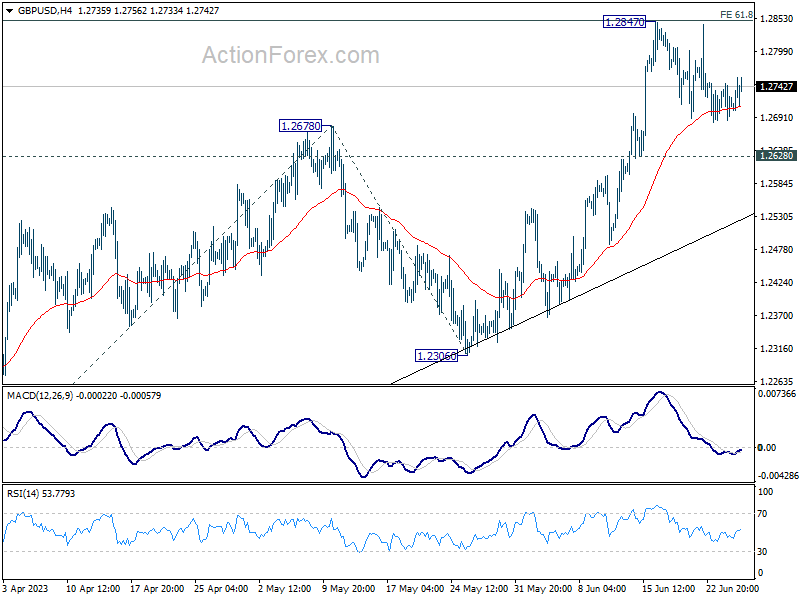

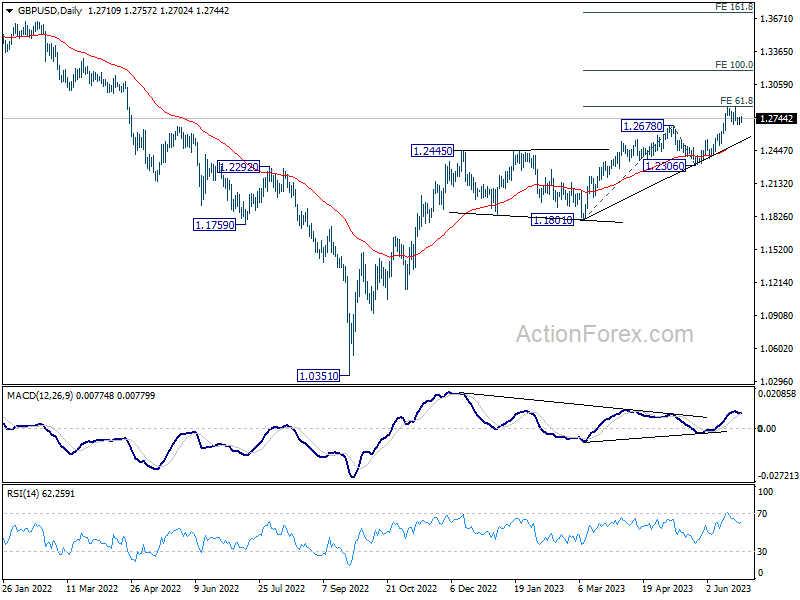

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2683; (P) 1.2716; (R1) 1.2744; More...

Intraday bias in GBP/USD stays neutral as consolidation continues. On the upside, firm break of 1.2847 will resume larger up trend and target 100% projection of 1.1801 to 1.2678 from 1.2306 at 1.3183 next. However, firm break of 1.2628 will turn bias to the downside, for deeper fall to 1.2306 support instead.

In the bigger picture, the strong support from 55 W EMA (now at 1.2341) is a medium term bullish sign. Outlook will stay bullish as long as 1.2306 support holds. Rise from 1.0351 medium term bottom (2022 low) is expected to extend further to retest 1.4248 key resistance (2021 high).

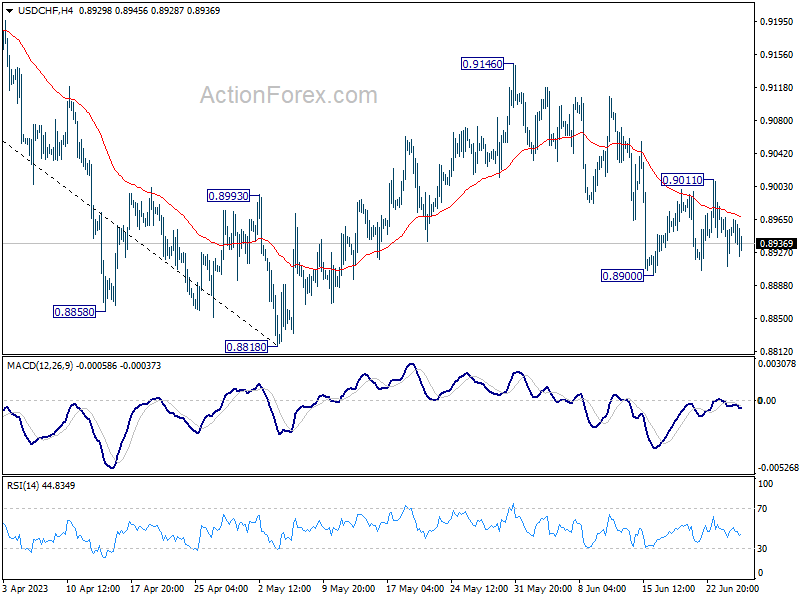

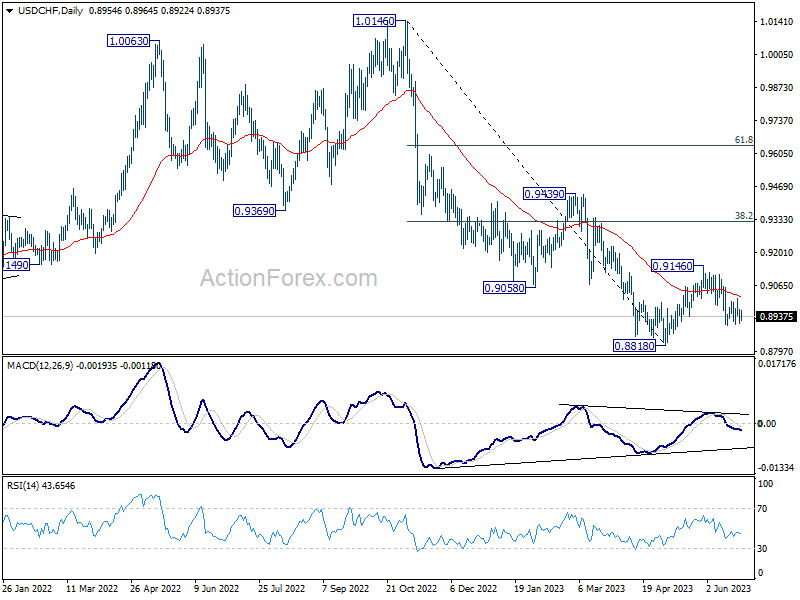

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8921; (P) 0.8948; (R1) 0.8985; More...

Range trading continues in USD/CHF and intraday bias remains neutral. Break of 0.8900 will resume the fall from 0.9146 to 0.8818 low or below. But for now, strong support is still expected from 0.8756 long term support to bring rebound. On the upside, above 0.9011 will bring stronger rise towards 0.9146 resistance.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high), which might have completed at 0.8818 already, just ahead of 0.8756 long term support. Sustained trading above 0.9058 support turned resistance should confirm medium term bottoming.

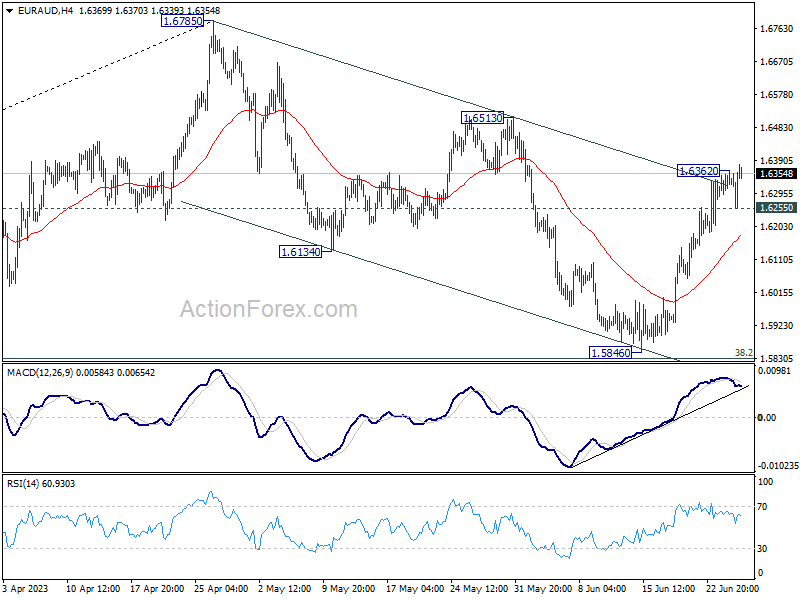

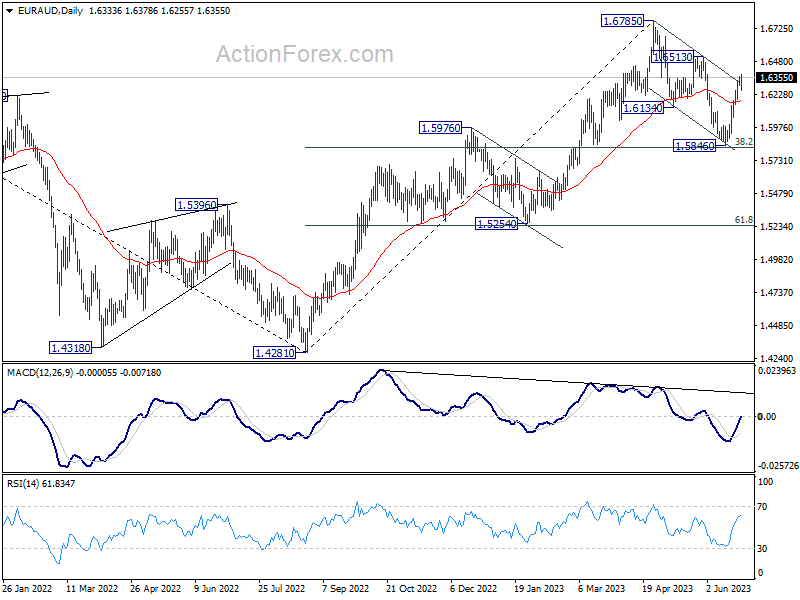

EUR/AUD Mid-Day Outlook

Daily Pivots: (S1) 1.6301; (P) 1.6333; (R1) 1.6369; More...

EUR/AUD's rise resumed after brief retreat and intraday bias is back on the upside. Outlook is unchanged that corrective fall from 1.6785 should have completed with three waves down to 1.5846. Further rise should be seen to 1.6513 resistance first. Firm break there will confirm this case and target 1.6785 high next. On the downside, below 1.6255 minor support will turn intraday bias neutral.

In the bigger picture, with 38.2% retracement of 1.4281 to 1.6785 at 1.5828 intact, rally from 1.4281 is still in progress. Firm break of 1.6785 will confirm rally resumption. Rejection by 1.6785 will extend the corrective pattern with another fall leg. But outlook will stay bullish as long as 1.5828 holds.

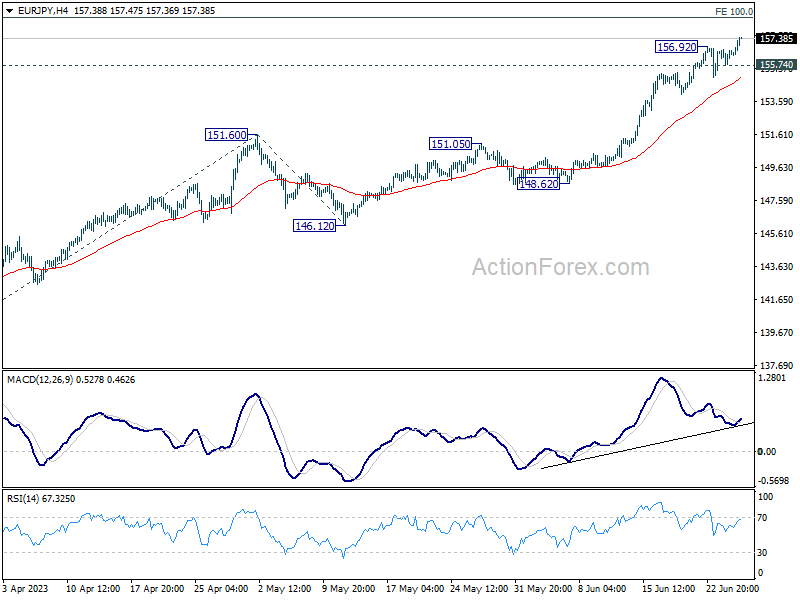

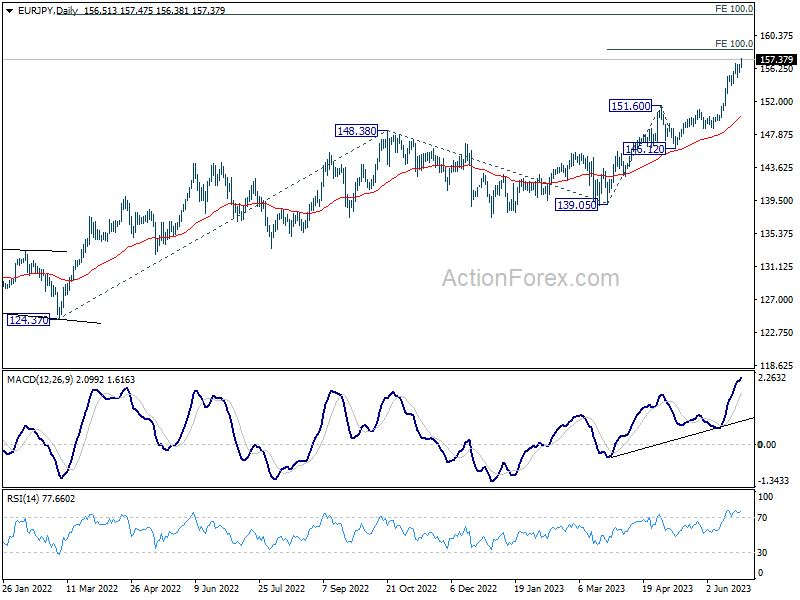

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.92; (P) 156.33; (R1) 156.90; More....

EUR/JPY's rally resumed after brief consolidations and intraday bias is back on the upside. Current up trend should target 100% projection of 139.05 to 151.60 from 146.12 at 158.67. On the downside, break of 155.74 minor support will turn intraday bias neutral and bring consolidations first, before staging another rise.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 100% projection of 124.37 to 148.38 from 138.81 at 162.82. For now, medium term outlook will remain bullish as long as 151.60 resistance turned support holds, even in case of deep pull back.

Euro Rides the High Wave, Soaring Against Yen and Others

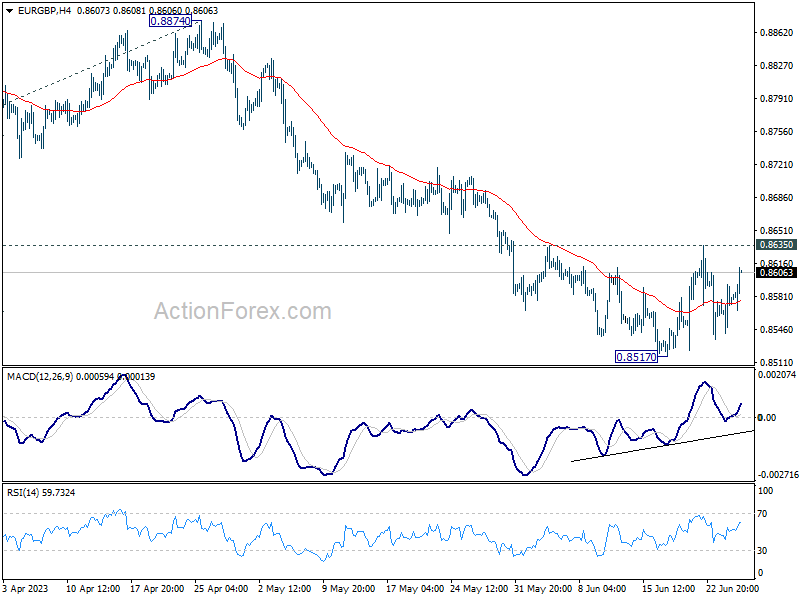

In today's trading, Euro takes the limelight, soaring broadly and reaching new heights against the frail Yen. While comments from ECB officials continued to be hawkish, there was basically nothing substantially new. The rationale propelling the shared currency is yet unclear. Following closely behind, Aussie and Kiwi mark themselves as the second and third strongest, respectively. Dollar, on the other hand, trails as the day's weakest performer, shadowed by Yen and Swiss Franc. Meanwhile, Sterling and Canadian Dollar deliver a mixed performance.

Technically, some focuses will be on 0.8635 resistance in EUR/GBP. Firm break there should indicate short term bottoming at 0.8517 and bring stronger rebound. If realized. that might help EUR/CHF rises through 0.9840 resistance, and push EUR/USD towards 1.1094 high. Let's see how it goes.

In Europe, at the time of writing, FTSE is down -0.17%. DAX is down -0.14%. CAC is down -0.19%. Germany 10-year yield is up 0.007 at 2.321. Earlier in Asia, Nikkei dropped -0.49%. Hong Kong HSI rose 1.88%. China Shanghai SSE rose 1.23%. Singapore Strait Times rose 0.49%. Japan 10-year JGB yield rose 0.0205 to 0.374.

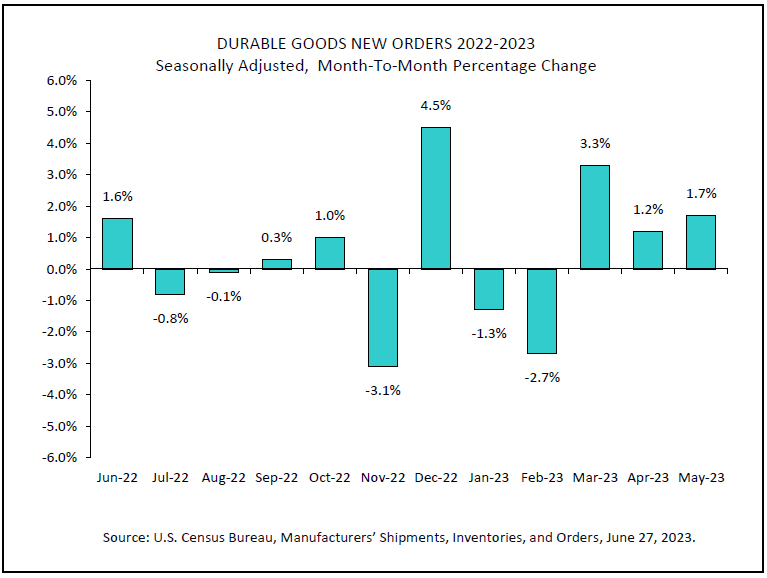

US durable goods orders up 1.7% mom in may

US durable goods orders rose 1.7% mom to USD 288.2B in May, much better than expectation of -1.0% mom decline. Ex-transport orders rose 0.6% mom to 185.6B. Ex-defense orders rose 3.0% mom to 269.9B. Transportation equipment rose USD 3.9% mom to USD 102.6B.

Canada CPI slowed to 3.4% yoy, lowest since Jun 2021

Canada CPI slowed from 4.4% yoy to 3.4% yoy in May, matched expectations. That's the lowest reading since June 2021, largely driven by lower year-over-year prices for gasoline (-18.3% ) resulting from a base-year effect.

Excluding gasoline, CPI also slowed from 4.9% yoy to 4.4% yoy. Mortgage interest cost index (+29.9%) remained the largest contributor to year-over-year CPI increase. Excluding mortgage interest cost, CPI rose slowed from 3.7% yoy to 2.5% yoy.

CPI median fell from 4.2% yoy to 3.9% yoy. CPI trimmed fell from 4.2% yoy to 3.8% yoy. CPI common fell from 5.7% yoy to 5.2% yoy.

On a monthly basis, CPI rose 0.4% mom, matched expectations.

ECB Lagarde reiterates further tightening in July

ECB President Christine Lagarde, while speaking at the ECB Forum today , emphasized that the bank"s job was far from over. She reiterated that "barring a material change to the outlook, we will continue to increase rates in July."

As ECB treads further into restrictive territory, Lagarde indicated that the central bank would be paying close attention to two aspects of its policy - the "level" of rates and the communication around future decisions, particularly in terms of "length" of time rates are expected to stay at that level.

She underscored the presence of two main uncertainties affecting the "level" and "length" of the bank"s interest rate policies.

The first is the uncertainty about inflation persistence, which makes the peak level of rates state-contingent. The second involves the uncertainty around monetary policy transmission, an issue heightened by the fact that Eurozone has not experienced a sustained phase of rate hikes since the mid-2000s and has never witnessed such swift rate rises.

ECB Kazaks: Rates will need to be raised past July

ECB Governing Council member Martins Kazaks expressed concerns about the persistent high inflation, indicating that an economic slowdown may not be enough to counter it. He also pushed back against market expectations of an ECB rate cut in the first half of next year.

Kazaks stated, "The softness of the economy is unlikely to deal with inflation, which is still very high, with strong risks of persistence."

Further suggesting the need for rate hikes beyond July, Kazaks said, "In my view, we will still need to raise rates and I don't think that in July we'll be comfortable enough to say: 'we're done'. I think rates will need to be raised past July but when and by how much will be data-dependent."

Highlighting the divergence between his stance and market sentiments, he remarked, "The major problem with market pricing is the expectation of rates coming down so quickly. In my view, it's wrong and the reason is that the market must be pricing in a different macro scenario with inflation coming down much more quickly."

His views on potential rate cuts were very clear. Kazaks sees the need for rate cuts only when "it becomes quite certain that inflation is about to start significantly and persistently undershooting our target of 2%. And not at the end of the forecast period but towards the middle of the forecast period."

China steps up efforts to curb yuan's decline, defends 7.25

The Offshore Chinese Yuan (CNH) is witnessing a revival today, as China appears to be intensifying its efforts to curb the currency's recent slump. Market participants view 7.25 level against Dollar as a significant psychological threshold to uphold.

According to a report by Reuters, there's evidence that major state-owned Chinese banks are selling dollars in the offshore spot foreign exchange market. This activity suggests that authorities are keen to slow the yuan's precipitous decline in recent times.

In an additional bid to temper the yuan's slide, China set its daily reference rate for the managed currency at a stronger-than-anticipated level for a second consecutive day. This move underscores PBoC's dissatisfaction with the currency's recent rapid and unilateral depreciation, particularly the swift move from 7.25.

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.92; (P) 156.33; (R1) 156.90; More....

EUR/JPY's rally resumed after brief consolidations and intraday bias is back on the upside. Current up trend should target 100% projection of 139.05 to 151.60 from 146.12 at 158.67. On the downside, break of 155.74 minor support will turn intraday bias neutral and bring consolidations first, before staging another rise.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 100% projection of 124.37 to 148.38 from 138.81 at 162.82. For now, medium term outlook will remain bullish as long as 151.60 resistance turned support holds, even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 12:30 | CAD | CPI M/M May | 0.40% | 0.50% | 0.70% | |

| 12:30 | CAD | CPI Y/Y May | 3.40% | 3.40% | 4.40% | |

| 12:30 | CAD | CPI Median Y/Y May | 3.90% | 4.00% | 4.20% | |

| 12:30 | CAD | CPI Trimmed Y/Y May | 3.80% | 4.00% | 4.20% | |

| 12:30 | CAD | CPI Common Y/Y May | 5.20% | 5.40% | 5.70% | |

| 12:30 | USD | Durable Goods Orders May | 1.70% | -1.00% | 1.10% | 1.20% |

| 12:30 | USD | Durable Goods Orders ex Transportation May | 0.60% | 0.10% | -0.30% | -0.60% |

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Apr | -1.70% | -0.70% | -1.10% | |

| 13:00 | USD | Housing Price Index M/M Apr | 0.70% | 0.30% | 0.60% | 0.50% |

| 14:00 | USD | Consumer Confidence Jun | 103.6 | 102.3 | ||

| 14:00 | USD | New Home Sales M/M May | 663K | 683K |

US durable goods orders up 1.7% mom in may

US durable goods orders rose 1.7% mom to USD 288.2B in May, much better than expectation of -1.0% mom decline. Ex-transport orders rose 0.6% mom to 185.6B. Ex-defense orders rose 3.0% mom to 269.9B. Transportation equipment rose USD 3.9% mom to USD 102.6B.