Sample Category Title

EUR/GBP Weekly Outlook

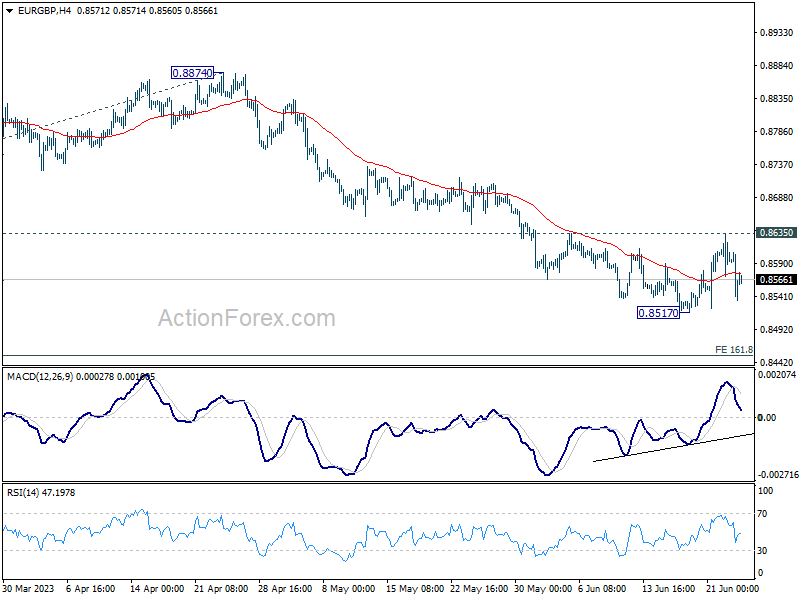

EUR/GBP's rebound was limited at 0.8635 last week and quickly reversed. The development keeps near term outlook bearish. Initial bias stays neutral this week first. Break of 0.8517 will resume the fall from 0.8977 to 161.8% projection of 0.8977 to 0.8717 from 0.8874 at 0.8453. Nevertheless, decisive break of 0.8635 will confirm short term bottoming, and bring stronger rebound to 55 D EMA (now at 0.8666) and above.

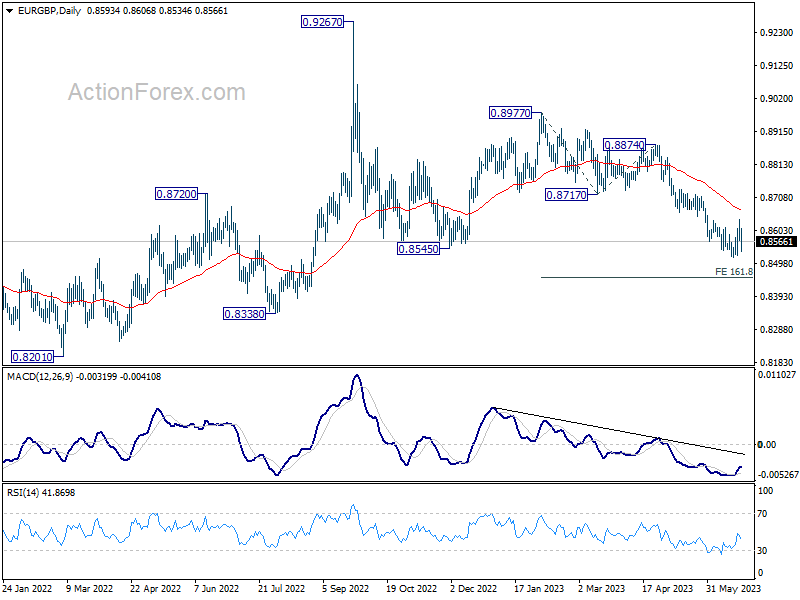

In the bigger picture, the down trend from 0.9267 (2022 high) is still in progress. It's seen as part of the long term range pattern from 0.9499 (2020 high). Deeper fall would be seen towards 0.8201 (2022 low). But strong support should be seen from there to bring reversal. This will now remain the favored case as long as 0.8717 support turned resistance holds.

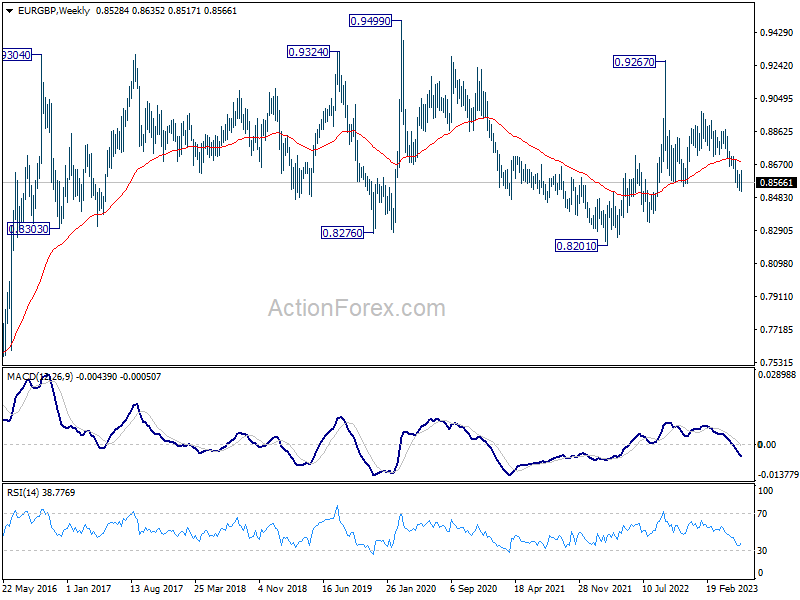

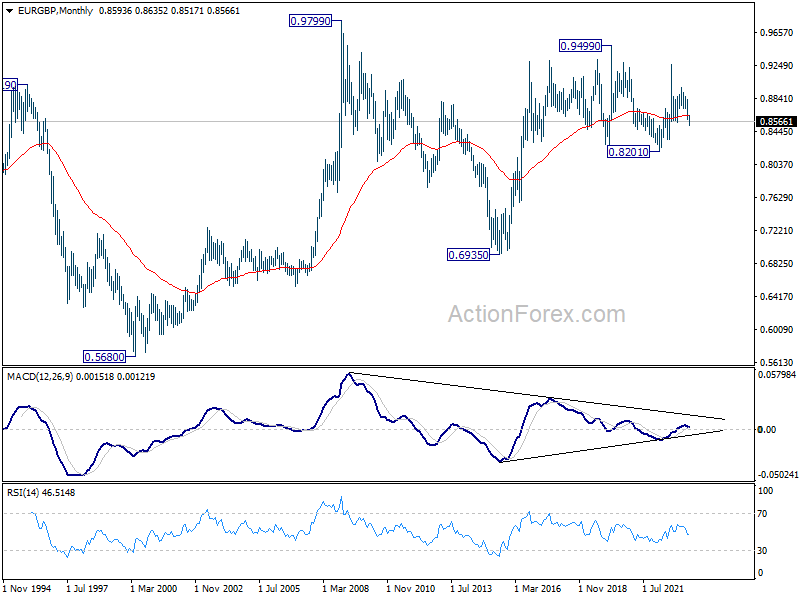

In the long term picture, long term range pattern is extending. But rise from 0.6935 (2015 low) is expected to extend at a later stage, to 0.9799 (2009 high).

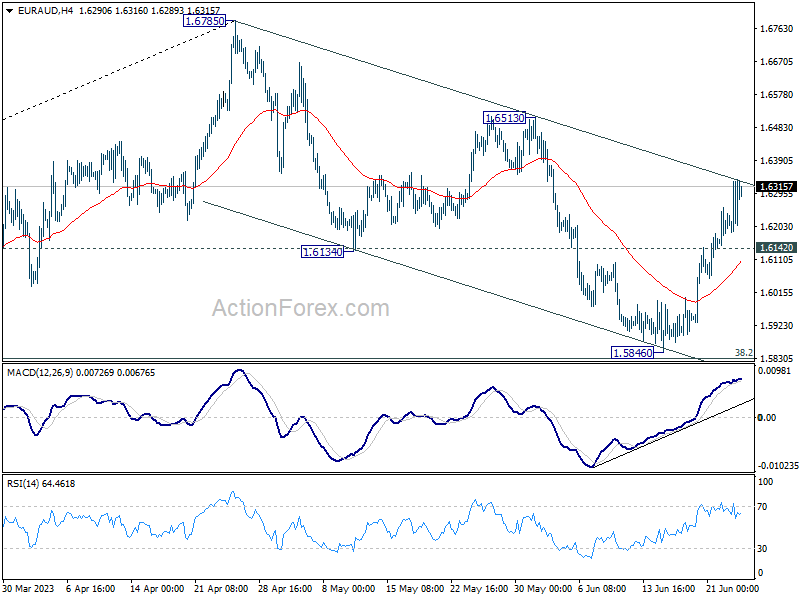

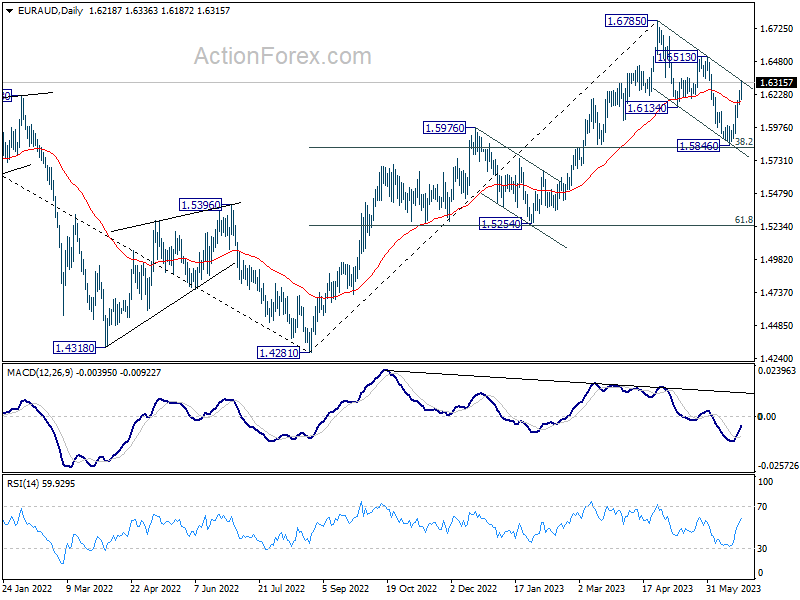

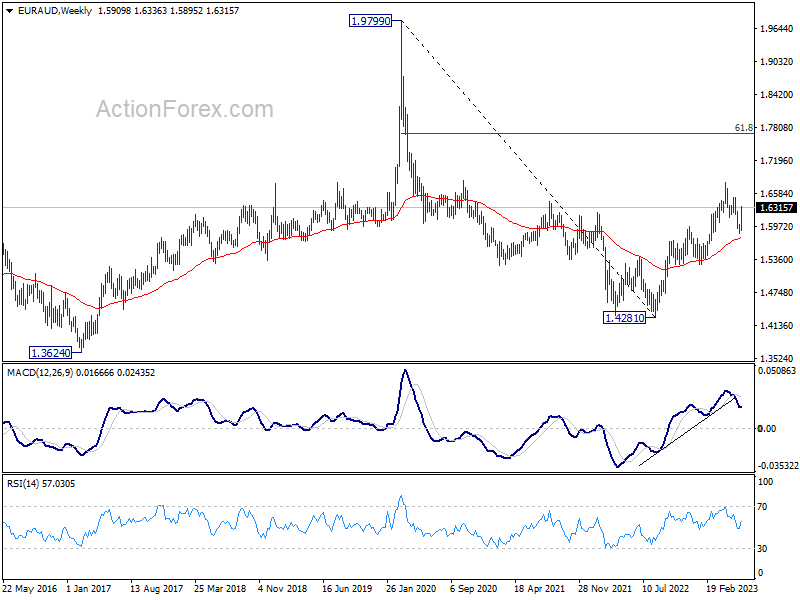

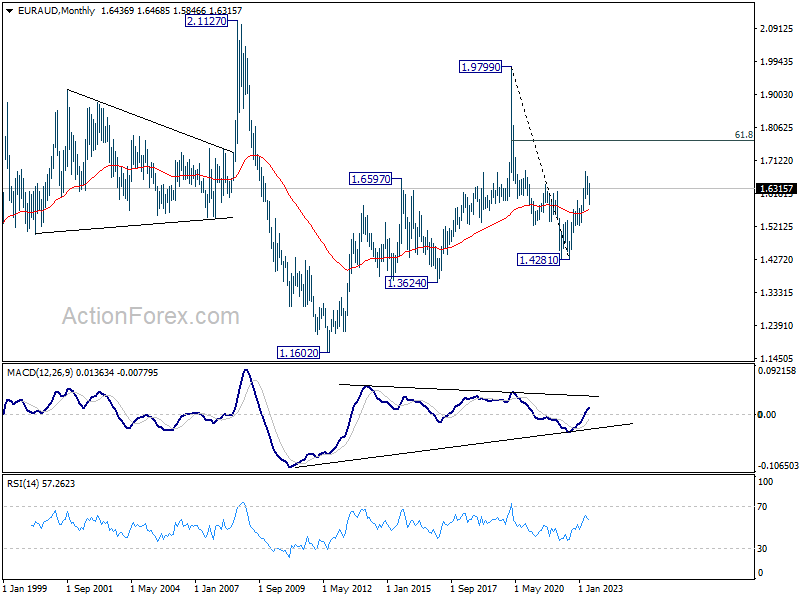

EUR/AUD Weekly Outlook

EUR/AUD's rally from 1.5846 continued last week and outlook is unchanged. Corrective fall from 1.6785 should have completed with three waves down to 1.5846. Initial bias remains on the upside this week for 1.6513 resistance. Firm break there will confirm this case and target 1.6785 high next. On the downside, though, break of 1.6142 minor support will mix up the outlook and turn intraday bias neutral first.

In the bigger picture, with 38.2% retracement of 1.4281 to 1.6785 at 1.5828 intact, rally from 1.4281 is still in progress. Firm break of 1.6785 will confirm rally resumption. Rejection by 1.6785 will extend the corrective pattern with another fall leg. But outlook will stay bullish as long as 1.5828 holds.

In the longer term picture, it's still early to decide if rise from 1.4281 is resuming whole up trend from 1.1602 (2012 low). But in either case, further rally is in favor as long as 1.5254 support holds. Next target is 61.8% retracement of 1.9799 to 1.4281 at 1.7691.

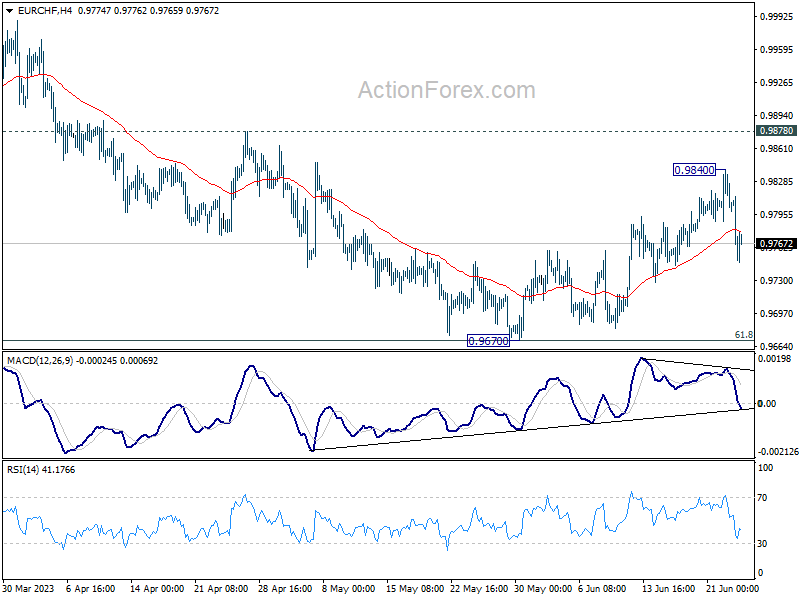

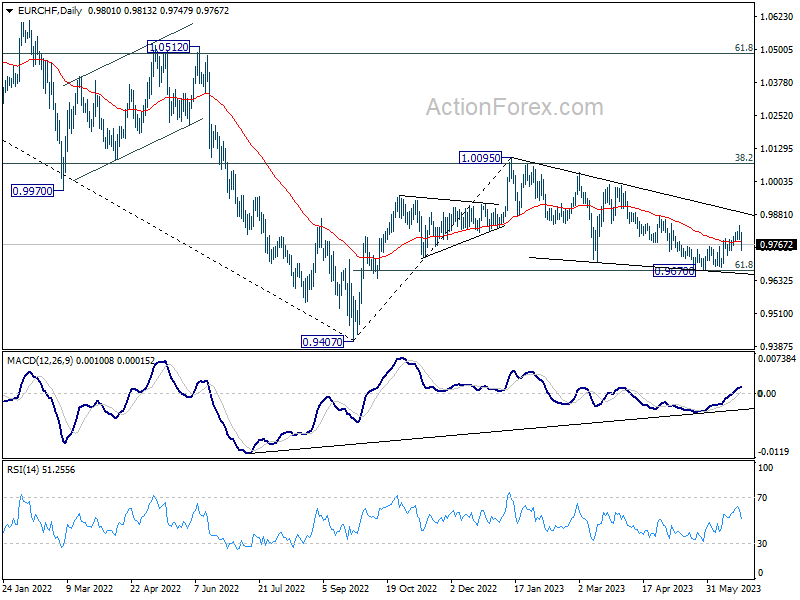

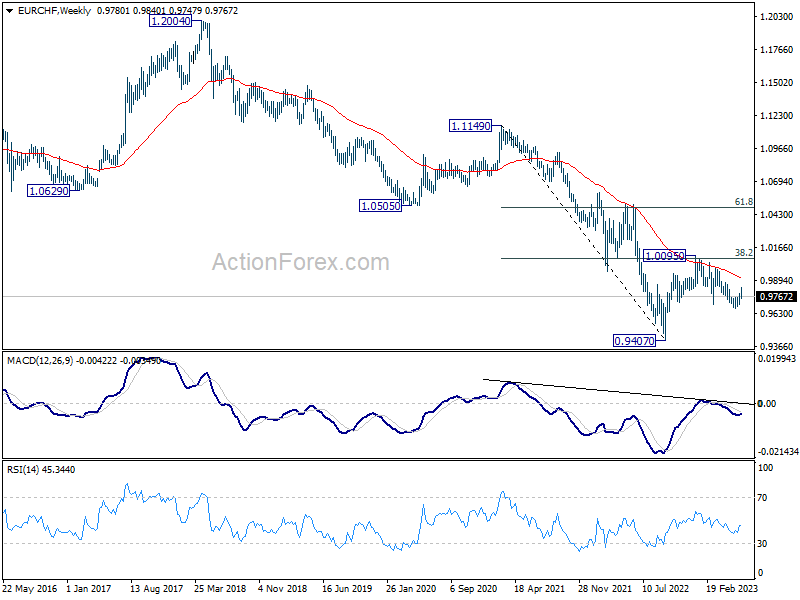

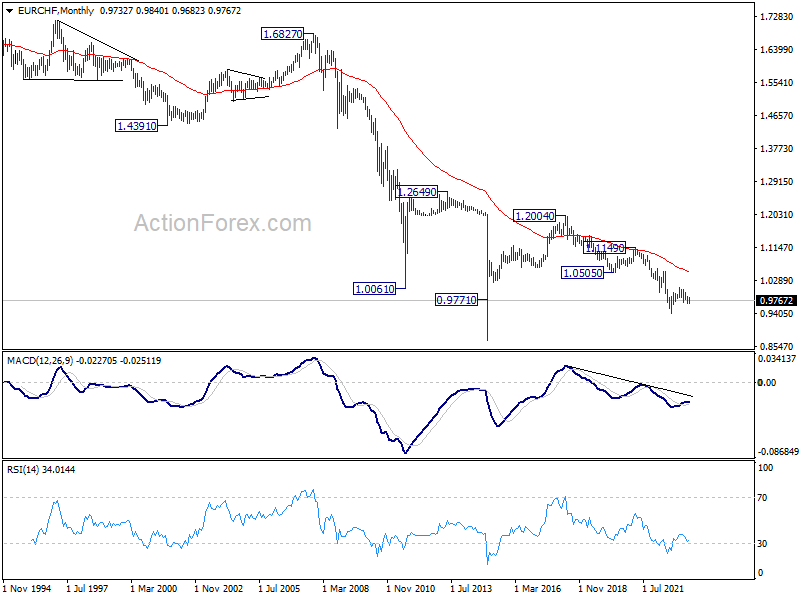

EUR/CHF Weekly Outlook

While EUR/CHF's rebound from 0.9670 extended to 0.9840 last week, subsequent reversal suggests that it has completed already. Initial bias stays on the downside this week for retesting 0.9670 low. Sustained break there will resume the whole fall from 1.0095. Nevertheless, break of 0.9840 will resume the rebound to 0.9878 resistance.

In the bigger picture, medium term outlook is staying bearish as the pair is capped below falling 55 W EMA (now at 0.9918). Down trend form 1.2004 (2018 high) is in favor to extend through 0.9407 at a later stage. Nevertheless, decisive break of 38.2% retracement of 1.1149 to 0.9407 will raise the chance of bullish trend reversal.

In the long term picture, it's still way too early too call for bullish trend reversal with upside capped well below 55 M EMA (now at 1.0484) and 1.0505 support turned resistance (2020 low). The multi-decade down trend could still continue.

Week Ahead – Inflation and Recession Risks

US

While Europe appears at great risk for a recession as traders bet on aggressive rate rises by all the European central banks, the Fed is still expected to be nearing the end of their respective rate hiking campaign. The focus in the US will fall on the PCE readings. If inflation comes down as expected, the swap futures might grow even more confident that the Fed will only deliver one more rate hike. Wall Street will also pay close attention to the Conference Board’s consumer confidence reading, which is expected to show a modest rebound. Friday’s Personal income and spending data will also be closely watched as incomes continue to grow, while spending softens.

Fed’s Williams speaks at the Bank for International Settlements on Sunday. Fed Chair Powell heads to Europe and speaks at the ECB’s global banking forum in Portugal. The Fed will also release the results of their annual banking stress tests.

Eurozone

There’ll be a lot of attention on ECB President Christine Lagarde’s appearances early in the week, particularly in light of what we’ve seen recently with central banks continuing to raise interest rates amid stubborn inflation. But it’s the flash HICP data on Friday that investors will be most interested in. The ECB recently warned that it will take a significant improvement in the data to avoid another rate hike next month and another repeat performance of the May report could be just that. Instead, we’re expected to see a small move in the other direction as base effects become less favourable for a couple of months, enabling the ECB to hike again in July before reassessing the situation in September. Inflation data from individual countries earlier in the week may offer some insight into what we can expect on Friday.

UK

In light of the Bank of England decision to hike interest rates by 50 basis points last week, focus will be on what MPC members have to say. There’s been a lack of unity for months but that was increasingly evident at the June meeting. Going forward, the decisions aren’t going to get easier which means there’s likely to be less unity, rather than more. It won’t take many votes to pause the tightening cycle and so, despite the clear inflation problem, comments from MPC members will become increasingly scrutinized.

Russia

A few data releases on the agenda next week including unemployment, retail sales, industrial output and monthly GDP.

South Africa

A very quiet week with PPI the only notable release. Inflation is falling back towards target and the PPI may offer insight into whether those pressures are continuing to head in the right direction.

Turkey

Thursday’s 6.5% rate hike suggests Turkey is on the path back to a conventional monetary policy approach. Markets were pricing in a lot more but with President Erdogan openly against hiking rates – despite replacing the Governor who was happy to cut on his behalf – the CBRT may be treading a little carefully. As we’ve seen before, Erdogan will not hesitate to sack a Governor so perhaps his new appointment simply has ambitions to still be employed in September. No major economic releases next week.

Switzerland

There are a few data releases next week, but SNB Chair Thomas Jordan’s appearance will probably be the highlight. The SNB hiked rates by 25 basis point this past week and markets believe there’s another in the pipeline. Jordan previously hinted at the neutral rate being 2% and the SNB indicated on Thursday that another hike may follow. With inflation forecast to stay above 2% for the next couple of years, only a drop in it over the next couple of months may change the SNBs mind.

China

Not much action on the economic data front with the only key data on manufacturing and services activities to digest.

On Friday, we will have the release of the NBS Manufacturing and Non-Manufacturing PMIs for June. Manufacturing PMI is forecasted to rebound slightly to 49.0 after it contracted to a five-month low of 48.8 in May.

In contrast, the growth trajectory of Non-Manufacturing PMI is forecasted to dip to 53.7 in June from 54.5 in May. If it turns out as expected, it will be the third consecutive month of a growth slowdown in services activities. These data will be closely watched to determine and gauge the next move from China’s top policymakers as market participants wait eagerly for the amount and scope of an impending new fiscal stimulus measure that the State Council stopped short of giving out any details about it last week.

India

A couple of key data to take note of on Friday; bank loan growth, Q1 current account where its deficit is forecasted to narrow to -$16 billion from $-18.2 billion recorded in Q4 2022, and Q1 external debt that is forecasted to edge lower to US$602 billion from $613.1 billion recorded in Q4 2022.

Australia

Two key data to focus on to gauge the next move on RBA’s monetary policy stance where it has reiterated its current tightening mode on last week’s release of RBA June meeting minutes.

On Wednesday, the monthly CPI Indicator for May is expected to come in at a slower growth rate of 6.1% year-on-year from 6.8% in April. If it turns out as expected, it will be the lowest level of inflation growth since March 2023.

On Thursday, preliminary retail sales for May is expected to show a growth of 0.1% month-on-month after zero growth recorded in April.

As of 23 June, the pricing on the ASX 30-day Interbank Cash Rate futures July contract has indicated a 32% chance of a 25-bps hike in the next RBA monetary policy meeting on 4th July 2023 to bring the cash rate up to 4.35%.

New Zealand

2 key data to focus on; Business Confidence for June out on Thursday where the forecast is calling for a slight improvement to -28 from -31.1 in May.

On Friday, Consumer Confidence for June is forecasted to dip to 77 from 79.2 recorded in May, if it turns out as expected, it will be the lowest level since December 2022.

Japan

Several key data to pay attention to. On Monday, the Bank of Japan (BoJ)’s Summary of Opinions. Retail sales for May will be released on Thursday where the consensus estimates are calling for a rebound to 5.4% year-on-year from 5% in April. Consumer confidence for June will also be released on the same day with an improvement to 38 being forecasted from 36 recorded in May. If it turns out as forecasted, it will be the 5th consecutive month of improvement in Japanese consumer sentiment.

Lastly, on Friday, we will have the all-important leading Tokyo area inflation data for June. Pay close attention to Tokyo’s core-core inflation rate (excluding fresh food & energy) that accelerated in May to 2.4% year-on-year, close to a 31-year high. If it continues to surge higher in June, it will run counter to BoJ’s latest guidance that has indicated that Japan’s inflation growth is at risk of a slowdown in the second half of the current fiscal year.

Singapore

Industrial production for May will be released on Monday, a further deceleration is expected to -7.2% year-on-year from -6.9% printed in April. If it turns out as expected, it will mark eight consecutive months of contraction of industrial production given the slowing external demand environment.

On Thursday, we will have PPI for May for a further deflationary spiral in producers’ prices is being forecasted at -12.4% year-on-year from -11.4% in April.

Economic Calendar

Saturday, June 24

Economic Events:

- ECB’s Schnabel participates in panel discussion at Petersberger Sommer-Dialog 2023.

- Austrian Chancellor Nehammer and Italian PM Meloni speak at Europa Forum Wachau

Sunday, June 25

Economic Events:

- Greece holds national elections.

- New Zealand PM visits China to meet with President Xi Jinping

- Fed’s Williams speaks at the Bank for International Settlements in Switzerland.

Monday, June 26

Economic Data/Events:

- Germany IFO business climate

- Israel unemployment

- Singapore industrial production

- Taiwan industrial production

- ECB forum in Sintra, Portugal

- SNB President Jordan speaks at Point Zero Forum in Zurich.

- EU foreign affairs ministers meet in Luxembourg.

- NATO Secretary General Stoltenberg meets Lithuanian President Nausėda in Vilnius

- French finance minister Le Maire and German economy minister Habeck meet in Berlin.

- Bank of Japan summary of opinions.

Tuesday, June 27

Economic Data/Events:

- US new home sales, durable goods, Conference Board consumer confidence

- Canada CPI

- Mexico international reserves, trade

- Taiwan jobless rate

- China’s Premier Li Qiang speaks at The World Economic Forum’s Annual Meeting

- ECB President Lagarde speaks in Sintra.

- BOE’s policymaker Tenreyro is a panelist at ECB forum in Sintra on “Monetary policy in the face of multiple supply shocks.”

Wednesday, June 28

Economic Data/Events:

- Australia monthly CPI

- China industrial profits

- Italy CPI

- Russia unemployment, industrial production

- US wholesale inventories, goods trade balance

- Fed reveals results of annual banking industry stress test.

- Policy panel with ECB’s Lagarde, Fed Chair Powell, BOJ’s Ueda and BOE’s Bailey at ECB bank forum in Sintra, Portugal.

- BOE chief economist Pill on panel at ECB bank forum focused on macroeconomic forecasting.

- ECB’s Villeroy speaks at Paris School of Economics conference.

- ECB’s Enria makes an introductory statement at a hearing of the European Parliament’s economic and monetary affairs committee in Brussels.

Thursday, June 29

Economic Data/Events:

- US Final Q1GDP report, initial jobless claims

- Australia retail sales

- Chile unemployment

- Eurozone economic confidence, consumer confidence

- Germany CPI

- Japan retail sales

- Spain CPI

- Sweden rate decision: Expected to raise repo rate 25bs to 3.75%

- The EU leaders summit opens in Brussels.

- Fed’s Bostic speaks on the US economic outlook at Irish Association of Investment Managers dinner in Dublin.

- BOE’s Tenreyro speaks at a Society of Professional Economists event in London

- BOE’s Cleland gives keynote speech at Global Bank Payments Summit in Cape Town.

Friday, June 30

Economic Data/Events:

- US May PCE deflator M/M: 0.1%e v 0.4% prior;; core PCE deflator M/M: 0.3%e v 0.4% prior, personal income and spending, University of Michigan consumer sentiment

- Canada GDP

- China June manufacturing PMI: 49.0e v 48.8 prior, non-manufacturing PMI, balance of payments

- Czech Republic GDP

- Eurozone June CPI M/M: 0.3%e v 0.0% prior; Core CPI Y/Y: 5.5%e v 5.3% prior, CPI Estimate Y/Y: 5.6%e v 6.1% prior, unemployment rate

- France CPI

- Germany unemployment

- India fiscal deficit

- Italy unemployment

- Japan unemployment, industrial production, Tokyo CPI

- Mexico unemployment

- Poland CPI

- South Africa trade balance

- Thailand trade, balance of payments

- UK GDP

- Bank of Canada releases business outlook survey and survey of consumer expectations.

Sovereign Rating Updates:

- None scheduled

Summary 6/26 – 6/30

Monday, Jun 26, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y May | 1.80% | 1.60% |

| 23:50 | JPY | BoJ Summary of Opinions | ||

| 08:00 | EUR | Germany IFO Business Climate Jun | 91.2 | 91.7 |

| 08:00 | EUR | Germany IFO Current Assessment Jun | 93.5 | 94.8 |

| 08:00 | EUR | Germany IFO Expectations Jun | 88 | 88.6 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y May | |

| Forecast: 1.80% | Previous: 1.60% | ||

| 23:50 | JPY | BoJ Summary of Opinions | |

| Forecast: | Previous: | ||

| 08:00 | EUR | Germany IFO Business Climate Jun | |

| Forecast: 91.2 | Previous: 91.7 | ||

| 08:00 | EUR | Germany IFO Current Assessment Jun | |

| Forecast: 93.5 | Previous: 94.8 | ||

| 08:00 | EUR | Germany IFO Expectations Jun | |

| Forecast: 88 | Previous: 88.6 | ||

Tuesday, Jun 27, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 12:30 | CAD | CPI M/M May | 0.50% | 0.70% |

| 12:30 | CAD | CPI Y/Y May | 3.40% | 4.40% |

| 12:30 | CAD | CPI Median Y/Y May | 4.00% | 4.20% |

| 12:30 | CAD | CPI Trimmed Y/Y May | 4.00% | 4.20% |

| 12:30 | CAD | CPI Common Y/Y May | 5.40% | 5.70% |

| 12:30 | USD | Durable Goods Orders May | -1.00% | 1.10% |

| 12:30 | USD | Durable Goods Orders ex Transportation May | 0.10% | -0.30% |

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Apr | -0.70% | -1.10% |

| 13:00 | USD | Housing Price Index M/M Apr | 0.30% | 0.60% |

| 14:00 | USD | Consumer Confidence Jun | 103.6 | 102.3 |

| 14:00 | USD | New Home Sales Change M/M May | 0.50% | 4.10% |

| 14:00 | USD | New Home Sales M/M May | 663K | 683K |

| GMT | Ccy | Events | |

|---|---|---|---|

| 12:30 | CAD | CPI M/M May | |

| Forecast: 0.50% | Previous: 0.70% | ||

| 12:30 | CAD | CPI Y/Y May | |

| Forecast: 3.40% | Previous: 4.40% | ||

| 12:30 | CAD | CPI Median Y/Y May | |

| Forecast: 4.00% | Previous: 4.20% | ||

| 12:30 | CAD | CPI Trimmed Y/Y May | |

| Forecast: 4.00% | Previous: 4.20% | ||

| 12:30 | CAD | CPI Common Y/Y May | |

| Forecast: 5.40% | Previous: 5.70% | ||

| 12:30 | USD | Durable Goods Orders May | |

| Forecast: -1.00% | Previous: 1.10% | ||

| 12:30 | USD | Durable Goods Orders ex Transportation May | |

| Forecast: 0.10% | Previous: -0.30% | ||

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Apr | |

| Forecast: -0.70% | Previous: -1.10% | ||

| 13:00 | USD | Housing Price Index M/M Apr | |

| Forecast: 0.30% | Previous: 0.60% | ||

| 14:00 | USD | Consumer Confidence Jun | |

| Forecast: 103.6 | Previous: 102.3 | ||

| 14:00 | USD | New Home Sales Change M/M May | |

| Forecast: 0.50% | Previous: 4.10% | ||

| 14:00 | USD | New Home Sales M/M May | |

| Forecast: 663K | Previous: 683K | ||

Wednesday, Jun 28, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Monthly CPI Y/Y May | 6.80% | |

| 06:00 | EUR | Germany Gfk Consumer Confidence (Jul) | -23 | -24.2 |

| 08:00 | CHF | Credit Suisse Economic Expectations Jun | -32.2 | |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y May | 1.50% | 1.90% |

| 12:30 | USD | Goods Trade Balance (USD) May P | -92.3B | -96.8B |

| 12:30 | USD | Wholesale Inventories May P | 0.10% | -0.10% |

| 14:30 | USD | Crude Oil Inventories | -3.8M | |

| 23:50 | JPY | Retail Trade Y/Y May | 5.20% | 5.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Monthly CPI Y/Y May | |

| Forecast: | Previous: 6.80% | ||

| 06:00 | EUR | Germany Gfk Consumer Confidence (Jul) | |

| Forecast: -23 | Previous: -24.2 | ||

| 08:00 | CHF | Credit Suisse Economic Expectations Jun | |

| Forecast: | Previous: -32.2 | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y May | |

| Forecast: 1.50% | Previous: 1.90% | ||

| 12:30 | USD | Goods Trade Balance (USD) May P | |

| Forecast: -92.3B | Previous: -96.8B | ||

| 12:30 | USD | Wholesale Inventories May P | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -3.8M | ||

| 23:50 | JPY | Retail Trade Y/Y May | |

| Forecast: 5.20% | Previous: 5.00% | ||

Thursday, Jun 29, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | NZD | ANZ Business Confidence Jun | -31.1 | |

| 01:30 | AUD | Retail Sales M/M May | 0.10% | 0.00% |

| 05:00 | JPY | Consumer Confidence Jun | 36.2 | 36 |

| 08:00 | EUR | ECB Economic Bulletin | ||

| 08:30 | GBP | Mortgage Approvals May | 50K | 49K |

| 08:30 | GBP | M4 Money Supply M/M May | -0.10% | 0.00% |

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Jun | 96 | 96.5 |

| 09:00 | EUR | Eurozone Industrial Confidence Jun | -5.5 | -5.2 |

| 09:00 | EUR | Eurozone Services Sentiment Jun | 5.5 | 7 |

| 09:00 | EUR | Eurozone Consumer Confidence Jun F | -16.1 | -16.1 |

| 12:00 | EUR | Germany CPI M/M Jun P | 0.20% | -0.10% |

| 12:00 | EUR | Germany CPI Y/Y Jun P | 6.30% | 6.10% |

| 12:30 | USD | Initial Jobless Claims (Jun 23) | 265K | 264K |

| 12:30 | USD | GDP Annualized Q1 F | 1.30% | 1.30% |

| 12:30 | USD | GDP Price Index Q1 F | 4.20% | 4.20% |

| 14:00 | USD | Pending Home Sales M/M May | -0.30% | 0.00% |

| 14:30 | USD | Natural Gas Storage | 95B | |

| 23:30 | JPY | Tokyo CPI Y/Y Jun | 3.80% | 3.20% |

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Jun | 3.30% | 3.20% |

| 23:30 | JPY | Tokyo CPI ex Food Energy Y/Y Jun | 4.40% | 3.90% |

| 23:30 | JPY | Unemployment Rate May | 2.60% | 2.60% |

| 23:50 | JPY | Industrial Production M/M May P | -1.00% | 0.70% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | NZD | ANZ Business Confidence Jun | |

| Forecast: | Previous: -31.1 | ||

| 01:30 | AUD | Retail Sales M/M May | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 05:00 | JPY | Consumer Confidence Jun | |

| Forecast: 36.2 | Previous: 36 | ||

| 08:00 | EUR | ECB Economic Bulletin | |

| Forecast: | Previous: | ||

| 08:30 | GBP | Mortgage Approvals May | |

| Forecast: 50K | Previous: 49K | ||

| 08:30 | GBP | M4 Money Supply M/M May | |

| Forecast: -0.10% | Previous: 0.00% | ||

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Jun | |

| Forecast: 96 | Previous: 96.5 | ||

| 09:00 | EUR | Eurozone Industrial Confidence Jun | |

| Forecast: -5.5 | Previous: -5.2 | ||

| 09:00 | EUR | Eurozone Services Sentiment Jun | |

| Forecast: 5.5 | Previous: 7 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Jun F | |

| Forecast: -16.1 | Previous: -16.1 | ||

| 12:00 | EUR | Germany CPI M/M Jun P | |

| Forecast: 0.20% | Previous: -0.10% | ||

| 12:00 | EUR | Germany CPI Y/Y Jun P | |

| Forecast: 6.30% | Previous: 6.10% | ||

| 12:30 | USD | Initial Jobless Claims (Jun 23) | |

| Forecast: 265K | Previous: 264K | ||

| 12:30 | USD | GDP Annualized Q1 F | |

| Forecast: 1.30% | Previous: 1.30% | ||

| 12:30 | USD | GDP Price Index Q1 F | |

| Forecast: 4.20% | Previous: 4.20% | ||

| 14:00 | USD | Pending Home Sales M/M May | |

| Forecast: -0.30% | Previous: 0.00% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 95B | ||

| 23:30 | JPY | Tokyo CPI Y/Y Jun | |

| Forecast: 3.80% | Previous: 3.20% | ||

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Jun | |

| Forecast: 3.30% | Previous: 3.20% | ||

| 23:30 | JPY | Tokyo CPI ex Food Energy Y/Y Jun | |

| Forecast: 4.40% | Previous: 3.90% | ||

| 23:30 | JPY | Unemployment Rate May | |

| Forecast: 2.60% | Previous: 2.60% | ||

| 23:50 | JPY | Industrial Production M/M May P | |

| Forecast: -1.00% | Previous: 0.70% | ||

Friday, Jun 30, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | CNY | Manufacturing PMI Jun | 49.5 | 48.8 |

| 01:00 | CNY | Non-Manufacturing PMI Jun | 53.7 50.8 | 54.5 |

| 01:30 | AUD | Private Sector Credit M/M May | 0.40% | 0.60% |

| 05:00 | JPY | Housing Starts Y/Y May | -2.20% | -11.90% |

| 06:00 | EUR | Germany Import Price Index M/M May | -2.00% | -1.70% |

| 06:00 | EUR | Germany Retail Sales M/M May | 0.20% | 0.80% |

| 06:00 | GBP | GDP Q/Q Q1 F | 0.10% | 0.10% |

| 06:00 | GBP | Current Account (GBP) Q1 | -7.7B | -2.5B |

| 06:30 | CHF | Real Retail Sales Y/Y May | -2.50% | -3.70% |

| 06:45 | EUR | France Consumer Spending M/M May | 0.70% | -1.00% |

| 07:00 | CHF | KOF Economic Barometer Jun | 89.2 | 90.2 |

| 07:55 | EUR | Germany Unemployment Change May | 15K | 9K |

| 07:55 | EUR | Germany Unemployment Rate May | 5.60% | 5.60% |

| 08:00 | EUR | Italy Unemployment May | 7.90% | 7.80% |

| 09:00 | EUR | Eurozone Unemployment Rate May | 6.50% | 6.50% |

| 09:00 | EUR | CPI Y/Y Jun P | 5.60% | 6.10% |

| 09:00 | EUR | CPI Core Y/Y Jun P | 5.40% | 5.30% |

| 12:30 | CAD | GDP M/M Apr | 0.20% | 0.00% |

| 12:30 | USD | Personal Income M/M May | 0.40% | 0.40% |

| 12:30 | USD | Personal Spending May | 0.20% | 0.80% |

| 12:30 | USD | PCE Price Index M/M May | 0.40% | |

| 12:30 | USD | PCE Price Index Y/Y May | 4.40% | |

| 12:30 | USD | Core PCE Price Index M/M May | 0.40% | 0.40% |

| 12:30 | USD | Core PCE Price Index Y/Y May | 4.70% | 4.70% |

| 13:45 | USD | Chicago PMI Jun | 44.5 | 40.4 |

| 14:00 | USD | Michigan Consumer Sentiment Index Jun F | 63.9 | 63.9 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | CNY | Manufacturing PMI Jun | |

| Forecast: 49.5 | Previous: 48.8 | ||

| 01:00 | CNY | Non-Manufacturing PMI Jun | |

| Forecast: 53.7 50.8 | Previous: 54.5 | ||

| 01:30 | AUD | Private Sector Credit M/M May | |

| Forecast: 0.40% | Previous: 0.60% | ||

| 05:00 | JPY | Housing Starts Y/Y May | |

| Forecast: -2.20% | Previous: -11.90% | ||

| 06:00 | EUR | Germany Import Price Index M/M May | |

| Forecast: -2.00% | Previous: -1.70% | ||

| 06:00 | EUR | Germany Retail Sales M/M May | |

| Forecast: 0.20% | Previous: 0.80% | ||

| 06:00 | GBP | GDP Q/Q Q1 F | |

| Forecast: 0.10% | Previous: 0.10% | ||

| 06:00 | GBP | Current Account (GBP) Q1 | |

| Forecast: -7.7B | Previous: -2.5B | ||

| 06:30 | CHF | Real Retail Sales Y/Y May | |

| Forecast: -2.50% | Previous: -3.70% | ||

| 06:45 | EUR | France Consumer Spending M/M May | |

| Forecast: 0.70% | Previous: -1.00% | ||

| 07:00 | CHF | KOF Economic Barometer Jun | |

| Forecast: 89.2 | Previous: 90.2 | ||

| 07:55 | EUR | Germany Unemployment Change May | |

| Forecast: 15K | Previous: 9K | ||

| 07:55 | EUR | Germany Unemployment Rate May | |

| Forecast: 5.60% | Previous: 5.60% | ||

| 08:00 | EUR | Italy Unemployment May | |

| Forecast: 7.90% | Previous: 7.80% | ||

| 09:00 | EUR | Eurozone Unemployment Rate May | |

| Forecast: 6.50% | Previous: 6.50% | ||

| 09:00 | EUR | CPI Y/Y Jun P | |

| Forecast: 5.60% | Previous: 6.10% | ||

| 09:00 | EUR | CPI Core Y/Y Jun P | |

| Forecast: 5.40% | Previous: 5.30% | ||

| 12:30 | CAD | GDP M/M Apr | |

| Forecast: 0.20% | Previous: 0.00% | ||

| 12:30 | USD | Personal Income M/M May | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 12:30 | USD | Personal Spending May | |

| Forecast: 0.20% | Previous: 0.80% | ||

| 12:30 | USD | PCE Price Index M/M May | |

| Forecast: | Previous: 0.40% | ||

| 12:30 | USD | PCE Price Index Y/Y May | |

| Forecast: | Previous: 4.40% | ||

| 12:30 | USD | Core PCE Price Index M/M May | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 12:30 | USD | Core PCE Price Index Y/Y May | |

| Forecast: 4.70% | Previous: 4.70% | ||

| 13:45 | USD | Chicago PMI Jun | |

| Forecast: 44.5 | Previous: 40.4 | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Jun F | |

| Forecast: 63.9 | Previous: 63.9 | ||

The Weekly Bottom Line: Consumer Updraft Supports Hawkish BoC

U.S. Highlights

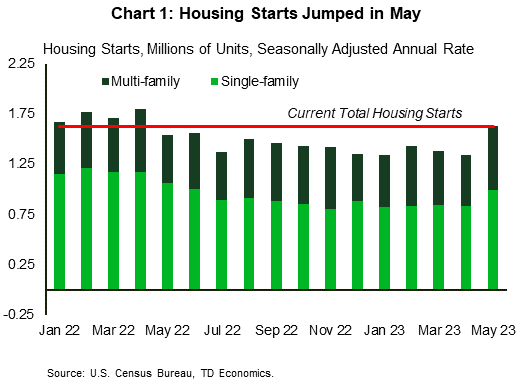

- Housing starts rose 21.7% month-on-month (m/m) in May, hitting its highest level in 13 months as both single-family and multi-family construction picked up.

- Existing home sales grew 0.2% m/m in May with elevated mortgage rates and limited supply continuing to act as headwinds.

- FOMC Chair Powell reiterated his expectation that rates would need to rise further this year during his semi-annual Congressional hearing.

Canadian Highlights

- Equity market sentiment soured this week, as more global central banks followed the Bank of Canada in ratcheting up rate hikes. Markets are worried about the coming economic slowdown in the wake of tighter monetary policy.

- April retail sales was the key Canadian data point in a relatively quiet week. Consumers ramped up spending in a wide variety of categories during the month, putting upside risk on Q2 consumer spending.

- All eyes will turn to next week’s inflation report for May along with the BoC’s Business Outlook Survey. Both will provide key information for the Bank to weigh ahead of it’s mid-July rate decision.

U.S. – Housing Up, Rates to Follow

The holiday-shortened, first week of summer was relatively quiet on the economic data front. However, we did get to hear from several FOMC members on the heels of last week’s meeting, including Chair Powell who was before Congress this week for the Fed’s semi-annual hearing. We also got a pulse check on housing this week which showed more homes being built and sold. Equity markets drifted lower on the week, as the S&P 500 fell 1.4% and the yield curve inversion steepened as the 10-Year Treasury yield fell by 5 basis-points (bps) to 3.72% as of the time of writing.

The week kicked off on Tuesday with a notable upside surprise in homebuilding activity, as housing starts came in at 1.63 million units (annualized) in May, 231k units higher than expected. Starts rose by 5.5% year-on-year (y/y), marking the first time in 13 months that starts were higher than their year-ago level (Chart 1). Most of the surprise can be attributed to an atypically large jump in single-family starts, while multi-family starts continued to fluctuate near elevated levels. With the prospect of higher for longer rates likely keeping existing home inventory relatively low for the foreseeable future, near-term tailwinds have formed behind residential construction.

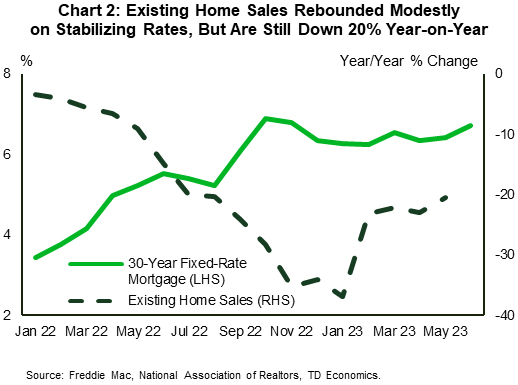

On the demand side of the housing equation, we saw existing home sales rise by 0.2% month-on-month (m/m) in May. All of that growth was found in the condo/co-op segment which grew by 4.7% m/m, while single-family sales declined by 0.3% m/m. While existing home sales have rebounded modestly in recent months, they are still down 20% y/y (Chart 2). Stabilizing mortgage rates have helped sales to experience a moderate near-term rebound, but with the Fed eyeing further rate hikes a sustainable rebound is unlikely to materialize this year.

Last week’s FOMC meeting brought a long-awaited pause to one of the most aggressive rounds of monetary policy tightening in decades, but it also came with the caveat that the FOMC expects an additional 50bps of rate hikes will be necessary this year. At his Congressional hearing this week, Chair Powell reiterated his comments from last week that inflation remained too high and that the Fed had more work to do. Other Fed speakers this week diverged, with Bostic seeing current rates as sufficiently restrictive, Goolsbee emphasizing a wait-and-see approach, and Bowman echoing Powell that more work needs to be done.

Across the pond, the Bank of England surprised markets with a 50bps hike on Thursday after core inflation accelerated in recent months. In the U.S., core PCE inflation – the Fed’s preferred inflation measure – has not accelerated, but roughly flatlined since the start of the year. This is why the Fed has favored 25bps hikes as it fine-tunes its approach to the terminal rate, but it is also why last week’s pause was conditional on further policy tightening. Next week we will receive an update on core PCE, and although it is unlikely to shift market expectations for a 25bps hike in July, it will help shape expectations for the rest of the FOMC meetings this year.

Canada – Consumer Updraft Supports Hawkish BoC

Sentiment on equity markets soured this week as more global central banks raised rates to cool inflation that remains overheated across much of the world. In Canada, April retail sales data was the headliner in a relatively quiet week for data. The report underscored the solid momentum on the consumer front. Despite high inflation, increased borrowing costs and uncertainty about recession, consumer spending has held up relatively well this spring.

April retail sales rose an impressive 1.1% month/month, coming in above Statistics Canada's advance estimate. Inflation was part of the story, but sales in real terms were still up a healthy 0.3% m/m, albeit coming after a couple of months of declines. Sales were up broadly across categories as well: general merchandise (+3.3% m/m), clothing and accessories (+3.1% m/m), food and beverages (+1.5% m/m), health and personal care retailers (+1.0% m/m), sporting goods, hobby items, musical instruments, and books stores (+1.0% m/m) and building material and garden equipment and supplies dealers (+0.7% m/m). Notable exceptions included furnishings, and electronics and appliances.

Consumer momentum looks to have carried through to May. Statistics Canada's advance estimate for May retail sales points to a solid 0.5% m/m follow through. However, with April's advance estimate falling well short of the actual data, this must be taken with several grains of salt. The firm retail data puts upside risk to our recent quarterly forecast for consumer spending, which is now tracking closer to a 1% annualized gain for Q2, versus our initial expectation for a relatively flat quarter following a healthy Q1.

This data vindicates the Bank of Canada's decision to raise the policy rate in early June. Strength in consumer spending had been a key factor in the Bank's decision to step off the sidelines and raise rates a quarter point. The BoC released its summary of deliberations leading up to its June 7th rate hike this week, and there was little new. The summary expanded on the factors outlined in the Bank's statement. Attention turns now to what the Bank is likely to do at its July 12th decision.

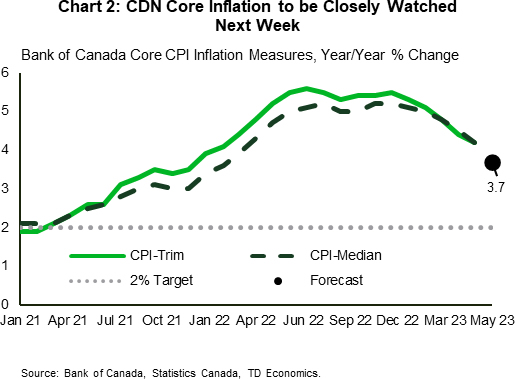

Next week's inflation data for May will be key. The BoC's preferred core inflation metrics – CPI trim and CPI median – had not eased as much as the Bank had hoped in recent months, another key factor in their rate hike. We expect the measures to decelerate to an average 3.7% year/year in May (Chart 2). If inflation cools far more than we expect, our confidence that the BoC is likely to hike again will be reduced.

However, the Bank will be assessing the totality of the data and may not be dissuaded from taking their policy rate higher with one soft inflation report, particularly given ongoing strength in housing, which has knock on effects for spending. Another key indicator is their quarterly Business Outlook Survey, due out next Friday. Last quarter's survey suggested businesses expected inflation pressures to ease, which hasn't panned out quite as the Bank would have liked. Nevertheless, business sentiment will be another piece of the data puzzle in their decision.

Critical Data Releases to Set Course for BoC Interest Rate Plans

The Bank of Canada will scrutinize a number of top-tier economic data releases next week as it contemplates how much higher to push interest rates.

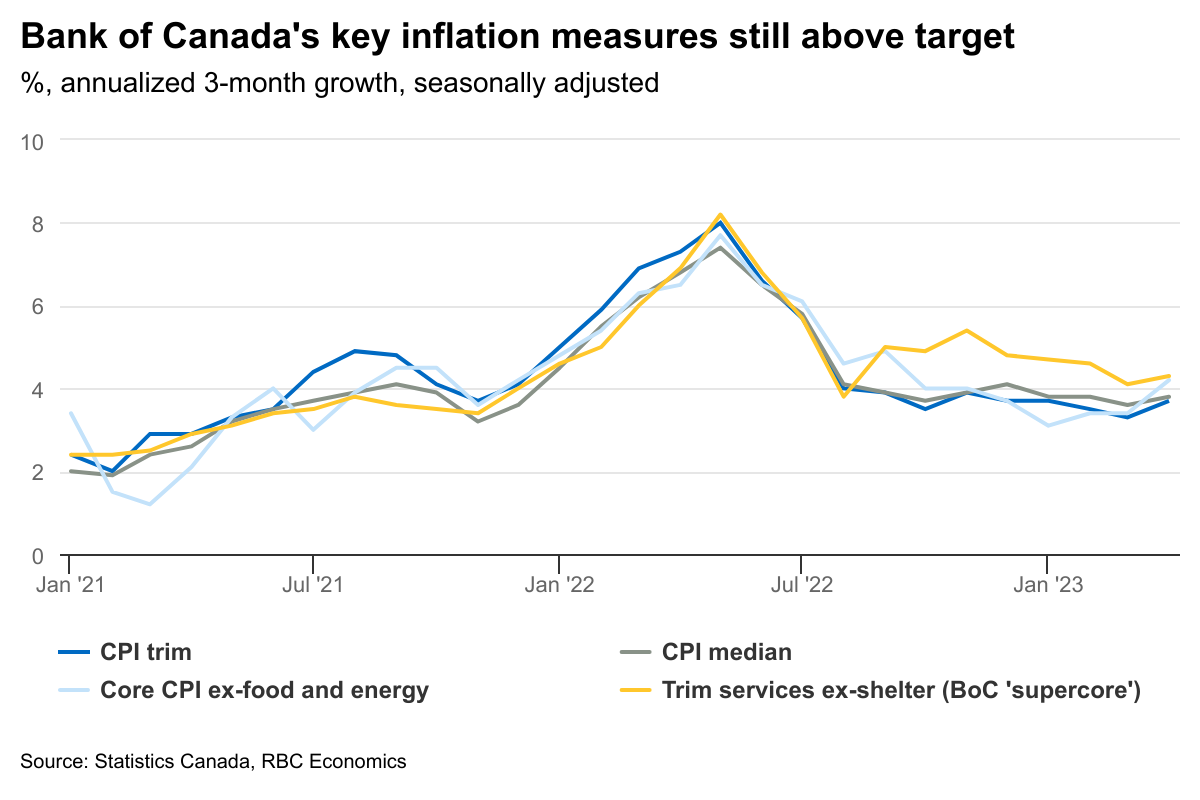

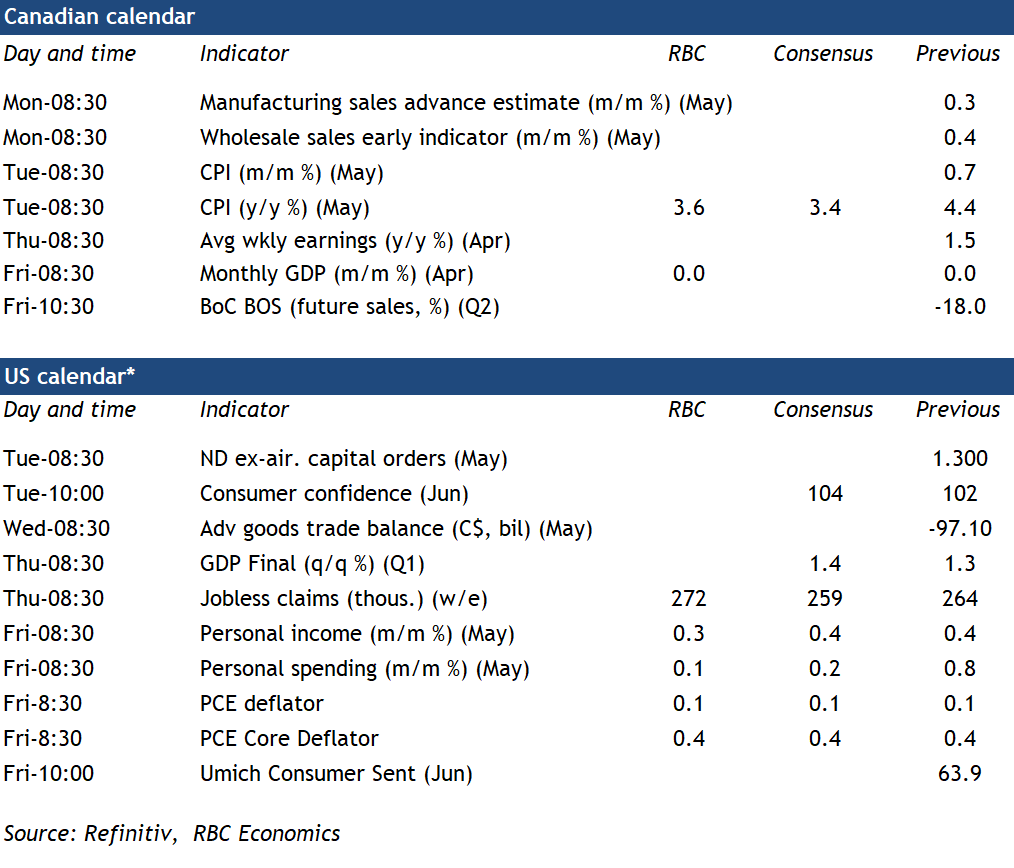

Canadian CPI inflation data should look better in May after surprising on the upside in April. We look for ‘headline’ price growth to slow—falling to 3.6% annually from 4.4% in April. Lower energy prices (gasoline and fuel oil prices were down 18% and 36%, respectively, from year-ago levels in May) explain most of that slowdown. And food price inflation is expected to edge lower again after peaking in January. More important for the Bank of Canada will be further signs that the pressures fueling inflation across other products and services continue to narrow. Annual growth in the BoC’s preferred ‘core’ measures will very likely slow due to favorable ‘base effects’ (that is, unusually large month-over-month increases a year ago not expected to be repeated this year). More recent month-over-month increases in those measures are down sharply from peak levels last summer. But they’ve been sticky, hovering at around a 4% annual rate (still well above the 2% inflation target).

The central bank’s own quarterly Business Outlook Survey (BOS) will be watched closely for signs that weaknesses are emerging in what has been a resilient economic backdrop so far in 2023. The last BOS flagged an unexpected easing in the intensity of labour shortages. And the number of job openings has continued to trend lower into June. Future sales growth will likely remain soft and investment plans have moderated in recent quarterly surveys. Economic data releases for Q2 have so far remained relatively resilient, but we are tracking a flat reading for April GDP next week. That’s still firm given the federal worker’s strike that month likely subtracted 0.2 to 0.3 percentage points from growth—but it’s below StatCan’s 0.2% preliminary estimate a month ago. We continue to see signs of cracks forming in the economic backdrop, but it’s highly unlikely that the BoC ended its pause in interest rate hikes in June for just one additional 25 basis point increase. It would likely take substantial downside surprises in data releases (i.e., lower inflation and / or GDP data) to prevent another hike at the next meeting in July.

Week ahead data watch

We expect Canadian April GDP to hold unchanged at March’s level—softer than the 0.2% prelim estimate from StatCan a month ago. The federal worker’s strike likely subtracted 0.2 to 0.3 percentage points from GDP growth in April. But retail and manufacturing sale volumes rose, and an 11% surge in home resales increased activity in real estate offices. The return of those federal workers to the job will boost May GDP growth but forest fires disrupted oil activity and hours worked (not including the strike impact) declined by 0.4% in May.

U.S. personal income likely edged up 0.3% in May alongside a smaller 0.1% rise in spending. Wage incomes likely rose 0.2% with higher hourly wage rates offsetting a tick down in hours worked, and household rental income has been rising strongly in recent months.

The Canadian SEPH employment report will be watched closely for further easing in labour demand. Job vacancies are already down almost 20% from their peak as of March and data from indeed.com are pointing to further declines in April.

Weekly Economic & Financial Commentary:

Summary

United States: Economic Resilience Suggests the Fed Has More Work to Do

- Chair Powell noted this week in Congressional testimony that economic activity has been resilient in the face of higher interest rates, suggesting there is more work to be done by policymakers in order to achieve their 2% inflation target. Housing was the dominant theme this week and intimated the housing market is holding up reasonably well in the face of higher interest rates and the potential for recession early next year.

- Next week: Durable Goods (Tue.), New Home Sales (Tue.), Personal Income & Spending (Fri)

International: Bank of England Revs Up Rate Hikes

- In the wake of disappointing inflation news in recent months, the Bank of England (BoE) this week decided to deliver a large 50 bps policy rate hike to 5.00%. The BoE's hand was essentially forced by especially rapid inflation in recent months, including a May CPI that quickened to 7.1% year-over-year. We doubt wage or price inflation will cool substantially by the time of the Bank of England's August announcement, and expect the U.K. central bank to deliver another 50 bps rate increase, to 5.50%, at that meeting. Beyond that, we also see a 25 bps hike to 5.75% in September, which we expect to be the peak for the current cycle.

- Next week: Riksbank Policy Rate (Thu.), China PMIs (Fri.), Eurozone CPI (Fri.)

Credit Market Insights: H8 to See You Go, Commercial Bank Loans Are Declining

- Credit conditions have tightened in the weeks since the advent of turmoil in the U.S. financial sector and giving the Fed more to consider in its deliberations over the future path of interest rates. Recently released H8 data depict a downward trend in the loans and leases of commercial banks in the U.S. during the weeks since these events, driven primarily by a deceleration in C&I loans.

Topic of the Week: Chairman Powell Reveals a Touch of Grey

- As mandated by the Federal Reserve Reform Act of 1977, Chair Jerome Powell presented the Federal Reserve's semiannual monetary policy report to the House of Representatives and Senate this week.

Week Ahead – Euro and Bleeding Yen Brace for Inflation Tests

With all the major central bank decisions behind us, the spotlight next week will turn to a new round of inflation releases. The euro has been riding high this month, but whether it still has some miles left in the tank will depend on what the inflation data spells for ECB policy. Meanwhile, the yen has been demolished and since FX intervention seems unlikely, it might take a serious acceleration in Japanese inflation to stop the bleeding.

Can the euro keep going?

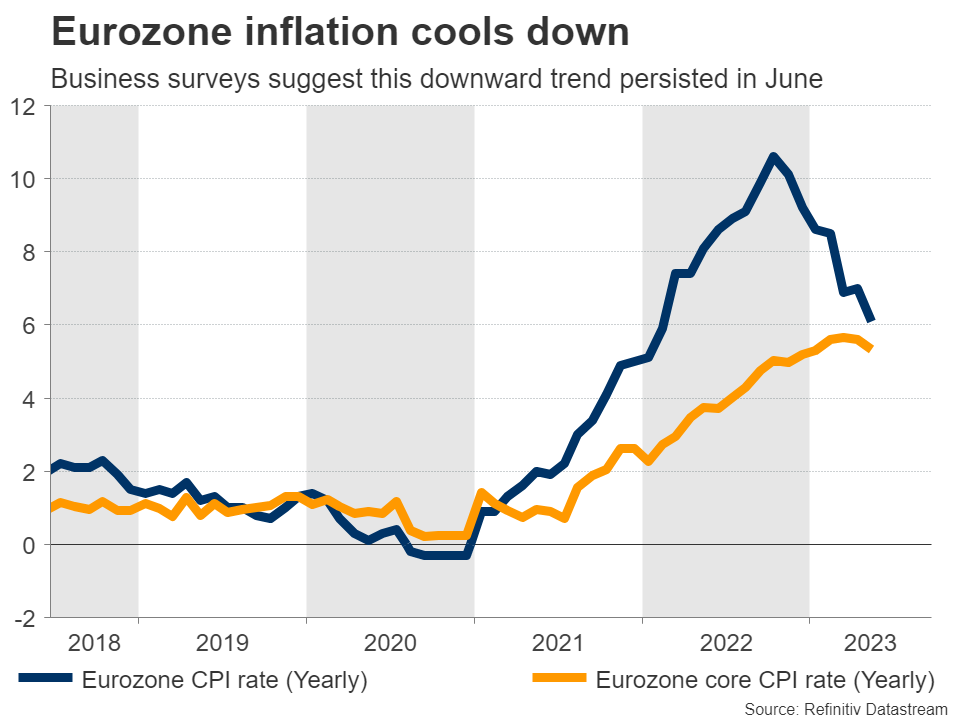

It’s been a solid month for the euro, which has capitalized on bets that the European Central Bank will raise interest rates further than previously expected. Despite mounting signs that inflation is cooling off and economic activity is stagnating, the ECB still decided to telegraph its intentions for higher rates.

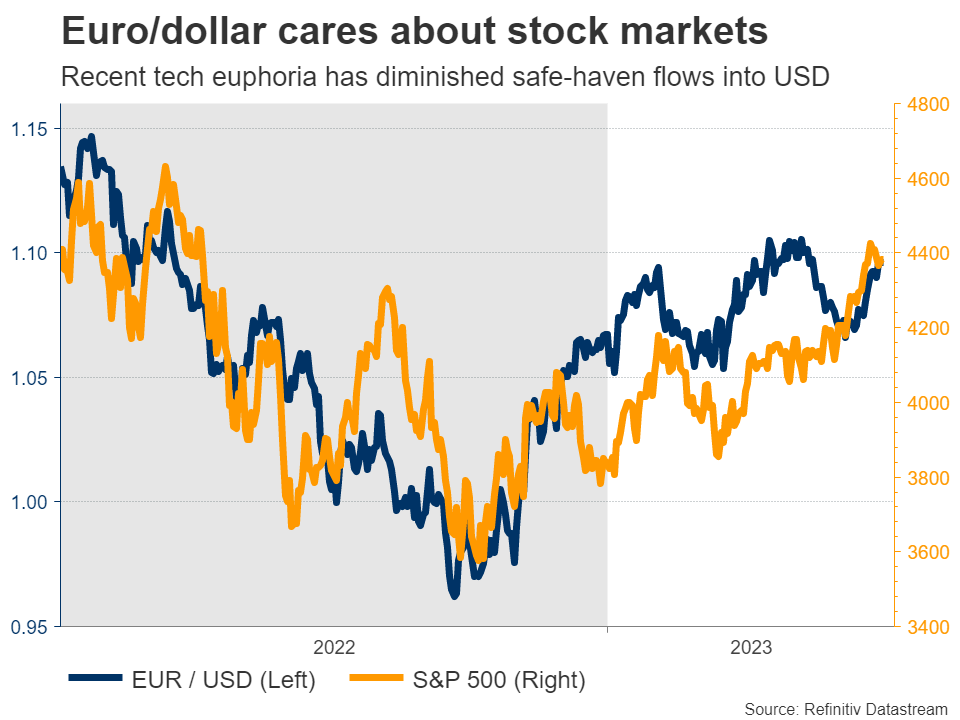

Ultimately this precommitment might prove to be a mistake since it ties the ECB’s hands, but for now, the rally in European yields has turned the euro into a more attractive investment destination. Another blessing for the euro has been the weakness in the US dollar, and even more so in the Japanese yen lately. After all, FX is a relative game.

Looking ahead, the question is whether there is still some juice left in the euro’s rally. That might be decided by the inflation report on Friday and what it implies for the ECB’s path. Inflation has been steadily declining this year and the latest business surveys suggest this trend continued in June, with selling prices rising at the slowest pace in over two years.

Markets are already pricing in another two rate increases over the coming months, and admittedly, it will be extremely difficult for the ECB to exceed those expectations amid slowing inflation and with the economy already in a mild technical recession.

Therefore, the euro might not be able to count on any further support from monetary policy. It could still advance if other major currencies keep depreciating, but the rally is unlikely to receive any more ‘fuel’ from the euro side of the equation.

Ahead of the Eurozone-wide flash CPI print on Friday, investors will get a taste of what to expect from the German numbers on Thursday.

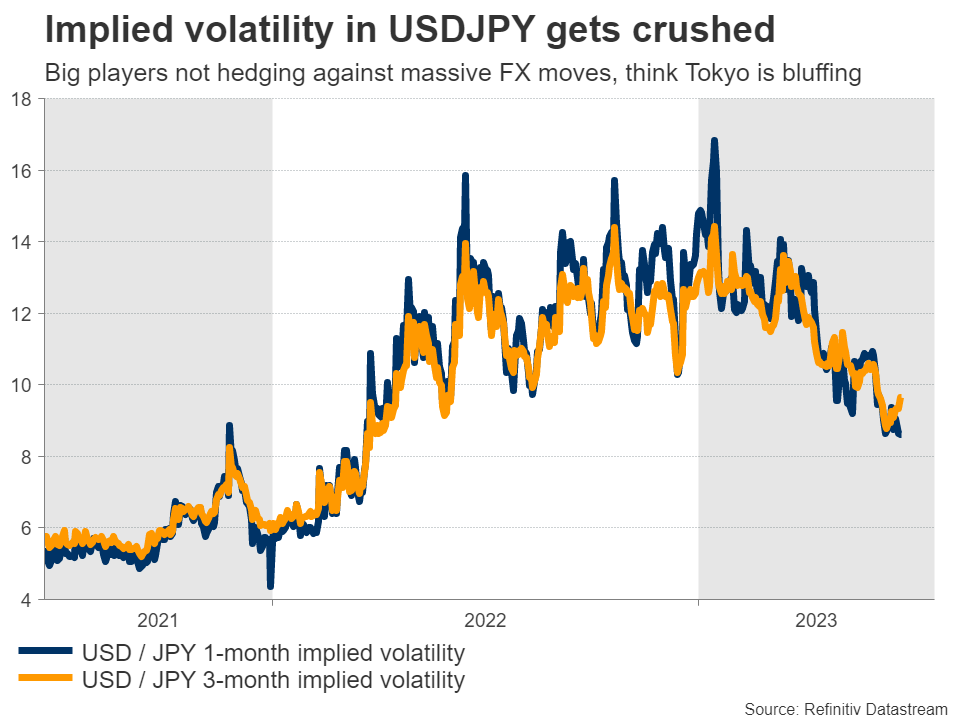

Sinking yen turns to inflation data for help

Over in Japan, the yen has been devastated by the Bank of Japan’s refusal to tighten monetary policy. Naturally, the yen’s losses have been heavier against currencies that are backed up by hawkish central banks, hence the parabolic moves in euro/yen and pound/yen.

With the currency in freefall, Japanese authorities have stepped up their warnings about FX intervention, but market participants don’t seem to believe them. Implied volatility in dollar/yen has been falling for months now, so bank dealers and investment managers are not panic-hedging against any massive movements in the yen.

Indeed, the intervention rhetoric from Japanese officials has not reached ‘peak levels’ either. So far, the finance minister has refrained from using phrases that would suggest intervention is imminent. Instead, he has been more measured with his comments, which makes the risk of FX intervention appear relatively low for now.

As such, for the yen to stand any chance of a comeback, it would need to rely on speculation that the Bank of Japan might adjust its policy settings next month. This puts extra emphasis on the CPI inflation numbers for Tokyo, which will hit the markets on Friday.

The Tokyo core CPI rate is projected to have risen in June, although just barely. Such an increase probably wouldn’t be enough to get the markets excited about a BoJ policy shift in July, which suggests the yen might continue to suffer for a while longer.

Dollar eyes PCE inflation

In the United States, the show will get started on Tuesday with the release of durable goods orders and new home sales for May, ahead of the core PCE price index on Friday, which will be released alongside personal consumption and income numbers for the same month.

There is a game of chicken being played between Fed officials and market participants in recent weeks, with policymakers telegraphing another two rate increases for this year but investors only pricing in one. As such, the persistence of inflationary pressures will decide who is right, driving the dollar accordingly.

Overall, the greenback has been under some pressure this month, partly because of the market’s skepticism about the Fed’s hawkish signals and partly because of the euphoric tone in stock markets that has diminished safe-haven flows.

Yet, there is some scope for a dollar recovery moving forward, since the US economy seems much more resilient than its competitors and the summer months could be marked by tighter liquidity conditions as the Treasury continues to raise its cash levels.

Finally in neighboring Canada, inflation stats for May are out on Tuesday. The loonie has advanced lately despite the decline in oil prices, mostly on the back of hawkish signals from the Bank of Canada, so the inflation report will be crucial in deciding the longevity of this rally.

Weekly Focus – Hawkish Surprise

Rates markets prepare for recession as yields curves inverted further this week. With a hawkish tilt to central bank decisions this week, Bank of Japan (BoJ) continues to stand in stark contrast supported by several dovish messages from BoJ, leaving yen as one of the big losers in FX markets. Scandi currencies have also seen some headwinds with EUR/SEK hitting the highest level ever. European yields moved lower as PMI data ticked in significantly weaker than expected, with service sector growth easing and further weakness in manufacturing. Oil and energy in general took a leg lower following the weak PMIs and as the US inventory report showed continued selling of strategic oil reserves.

Another key market events this week was Fed chair Powell's semi-annual testimony in the House Financial Services Committee. Powell said, it might make sense to hike further at a more moderate pace; nothing new compared to last week's FOMC meeting. Fed pricing was little changed and markets price in one additional hike this year. We still think this hiking cycle is done.

Thursday brought a flurry of rate hikes, with hawkish surprises from Norges Bank and Bank of England, both hiking by 50 bps. While expectations were split between a 25 and 50 bps hike for the former, the latter was a big surprise with 31 bps priced in ahead of the meeting. Both decisions come on the back of further surge in inflation in May. FX markets strengthened Sterling on announcement but quickly reversed the move and rates curves inverted further. As expected, the Turkish central bank U-turned as the new governor Erkan hiked the key interest rate by 650 basis points to 15%. Analyst expectations were dispersed to say the least. That said, the hike was significantly smaller than priced in by markets, and the lira tumbled to new lows despite a promise to tighten further.

We have published a new Nordic Outlook this week. The news have mostly been good in recent months when it comes to inflation, employment and the near-term growth outlook in most major economies. However, we have yet to see the full effect of the monetary and fiscal tightening that has already happened, and inflation is still not sufficiently under control. We expect prolonged slowdown and moderately higher unemployment, with the risk of a deeper recession still present. This is also true in the Nordic countries, even though the outcome so far has surprised positively in Denmark and Sweden.

Next week, focus turns back to inflation data, as euro area figures are released Friday. We expect headline inflation continued to slide rapidly to 5.3% from 6.0% in May. Core inflation on the other hand is stickier and we forecast a small decline from 5.3 to 5.1%. We will also keep an eye on ECB president Lagarde's speech at Sintra. In the US, May PCE data will be in focus along with Powell, who is scheduled to speak again Wednesday.

In China, focus will be on whether we get any concrete announcements on new stimulus. We also get the official PMI release for June, look for a small lift to the manufacturing PMI and further moderation in the service PMI from still high levels.