Sample Category Title

Economic Activity Has Cooled Euro

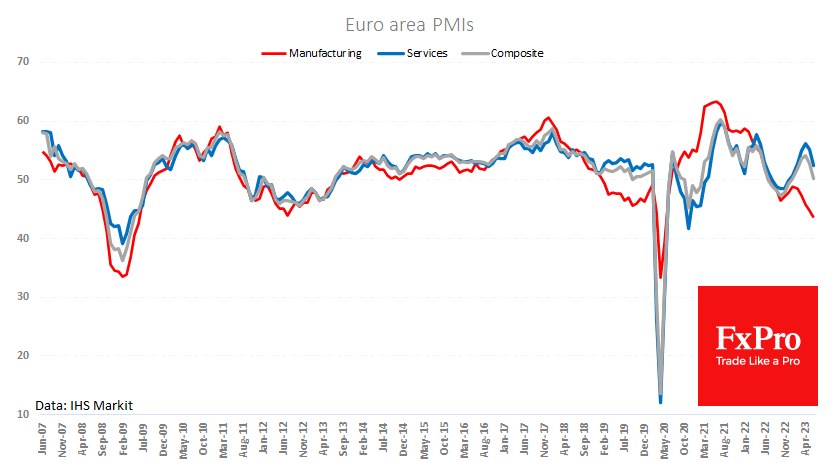

The Euro suffered a setback after the June PMIs revealed a slowdown in economic activity. Analysts were caught off guard by the contraction in French services, which dropped from 52.5 to 48.0 – far below the forecast of 52.2. Manufacturing also disappointed, staying below 50 for the tenth time in twelve months.

Germany followed with a grim report, showing a sharp decline in both manufacturing and services. The manufacturing PMI plunged from 43.2 to 41.0 (43.6 expected), and the services PMI slipped from 57.2 to 54.1 (56.3 expected).

These poor results weighed on the euro zone’s overall performance, where the composite business activity index fell to 50.3, its lowest level since January. The manufacturing PMI came in at 43.6, signalling a severe contraction in the region’s economy soon. Apart from the Covid dip, it has only been lower between October 2008 and May 2009, when the economy shrank by more than 5%. Although the current situation is not as dire, fears are mounting.

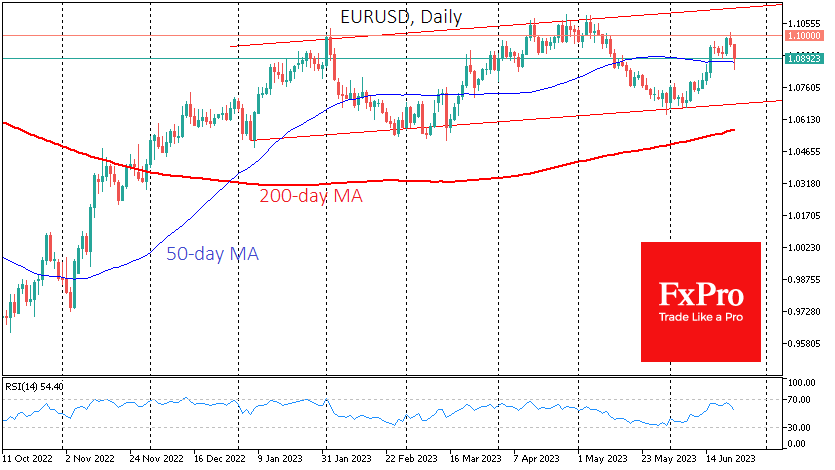

The EURUSD lost around 1.5% in less than a day after touching 1.10 in the middle of the European session on Thursday. It accelerated as it broke below 1.0920 on Friday morning following the release of the Eurozone PMI estimates.

Intraday, the EURUSD is hovering around its 50-day moving average. If it can hold above this level in the coming days, it could attract active buyers and further push the pair to test previous highs above 1.1070. However, weak macroeconomic data and dwindling risk appetite in global markets increase the odds of a downward move, at least to the lower border of the rising channel at 1.0700 or further to the previous local lows at 1.0550.

Sunset Market Commentary

Markets

European June PMIs disappointed on all accounts. The manufacturing rout continued, unexpectedly easing from 44.8 to 43.6. Services have long compensated but are now also showing a loss of momentum, retreating more than expected from 55.1 to 52.4. The composite series fell to 50.3 (-2.5 points) as a result. Diving into some details, new business inflows declined for the first time since January. This was driven by an increasingly sharp downturn in manufacturing. Services registered only a modest increase. Backlogs fell at the steepest rate for seven months. S&P Global considers this as a bad precursor for payroll numbers. Indeed, employment growth slowed again in June with the manufacturing sector cutting jobs for the first time since January 2021. Headcount in the services sector waned to the lowest since March though remains strong by historical standards. Factory input prices dropped for a fourth consecutive month. Those in the services sector continued to rise at a rate well above the long-term average, in particular due to wage pressures, though the pace moderated. Prices charged for goods fell the most in three years but rose sharply for services even as the rate cooled substantially. Concerns over demand growth and the broader impact of higher interest rates depressed optimism for the year ahead to the lowest level so far this year and below the long-run average. S&P Global concludes: " […] the probability has increased somewhat that the GDP change will again carry a negative sign in the current quarter, due in part to weak services activity in France. […] the downward trend in the Composite PMI points to a difficult second half of the year as companies across all sectors face deteriorating order books." The market reaction was textbook with German yields tumbling 11-17 bps across the curve, stocks under recessionary pressure and the euro down for the day. EUR/USD is testing minor support at 1.0893. Commodities and commodity-related currencies including the AUD, NOK and NZD face the recessionary fall-out. AUD/USD tumbles to 0.667 from 0.675, NZD/USD hits a weekly low around 0.613 and Norwegian krone erases the little that what was left from yesterday’s bigger-than-expected rate hike to trade 1.75% lower against the euro (EUR/NOK 11.82). US PMIs came in close to expectations for services. The sector held strong at 54.1. The pain for the manufacturing sector intensified (46.3) vs consensus hoping for a stabilization around 48.5. US yields hold on to (most) of their daily losses of about 6.4-8.2 bps.

British PMIs also missed the bar though showed a bit more resilience than in the EMU (composite PMI 52.8 from 54). The services gauge eased from 55.2 to 53.7. The manufacturing gauge dropped 0.9 points to 46.2. Service providers still reported solid new inflows, contrasting the steep and accelerated fall in manufacturing. Jobs were created for a third month straight, thanks to the services sector, and the pace of hiring was the fastest since September 2022. Input prices showed similar dynamics to the EU. Prices charged rose sharply in services, pushed by strong wage pressures while there was only a fractional decline in manufacturing. Private sector firms remain optimistic about their growth prospects 12 months ahead. The PMIs followed stronger-than-expected UK retail sales and give the pound a push in the back against an generally weak euro. EUR/GBP intraday lost almost a full big figure to trade in the 0.8545 area currently. UK yields rise 4.8 bps at the front but lose almost >10 bps at longer maturities as markets further boost BoE tightening bets and ponder its economic impact (6.25% at some point).

News & Views

Belgian Business confidence in June fell for the third consecutive month, the National bank of Belgium reported. The overall synthetic curve declined from -9.1 to -12.1. Business climate worsened sharply in business related services (-2.5 from 10.5). All components of the indicator declined. In addition to a more negative assessment of current activity, respondents expressed much more pessimistic expectations of future activity and market demand in general. All components in the trade sub-indicator (from -13.2 from -9.2) also fell as both demand and employment expectations and intentions of placing order with suppliers in the next three months deteriorated. The third consecutive drop in manufacturing (-15.6 from -14.3) reflects a more unfavourable assessment of total order books and stock levels which was partially offset by more positive demand expectations. The near stabilisation in the building industry (-6.6 from -6.0) was due to an improvement in the recent orders and increased equipment use. Other components deteriorated slightly.

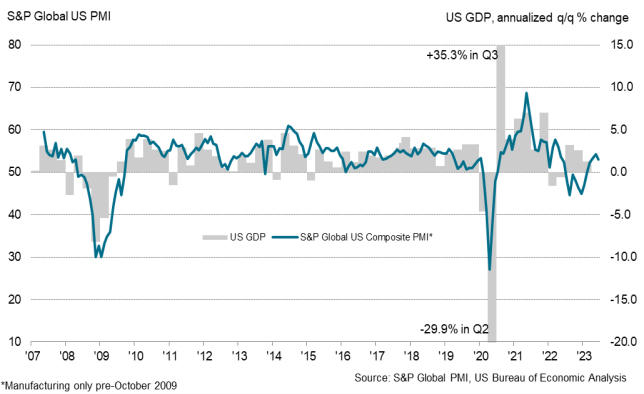

US PMI composite fell to 53.0, Q2 GDP growth in region of 2%

US PMI Manufacturing fell from 48.4 to 46.3 in June, a 6-month low. PMI Services fell from 54.9 to 54.1, a 2-month low. PMI Composite fell from 54.3 to 53.0, a 3-month low.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

"The overall rate of expansion of business activity in the US remained robust in June, consistent with GDP rising at a rate of 1.7% to put second quarter growth in the region of 2%.

"Growth remains dependent on service sector spending, however, with manufacturing slipping back into decline after three months of growth. While improving supply conditions had helped boost manufacturing production in prior months, an increasingly severe downturn in new orders mean factories are running out of work.

"The situation is brighter in the service sector, where demand is proving resilient and the recent pause in rate hikes appears to have helped boost business optimism for the year ahead.

"The question remains as to how resilient service sector growth can be in the face of the manufacturing decline and the lagged effect of prior rate hikes. Any further rate hikes will of course have a further dampening effect on this sector which is especially susceptible to changes in borrowing costs.

"The tightness of the labor market remains a concern, and upward wage pressure remains a key driver of higher costs in the service sector. However, it is encouraging to see the overall rate of selling price inflation for goods and services drop to the lowest since late 2020 in a sign that the Fed is winning its fight against inflation."

Euro Skids After Soft PMI Data, Markets Eye ISM Mfg. PMI

- Eurozone and German PMIs weakened in June

- EUR/USD fell as much as 110 pips on Friday

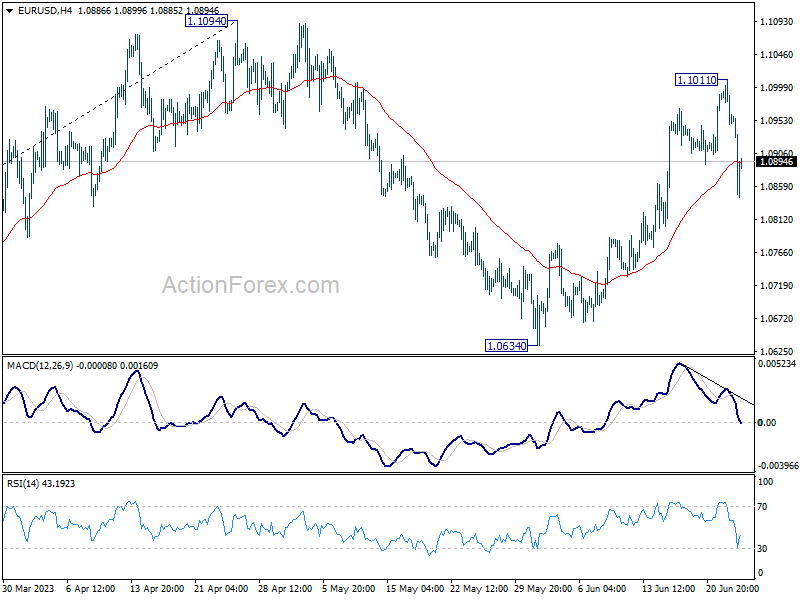

EUR/USD has taken a tumble on Friday. In the European session, the euro is trading at 1.0885, down 0.64%. The euro fell as low as 1.0844 earlier in the day. Later today, the US releases ISM Services PMI. The consensus stands at 54.0 for June, following 54.9 in May. The services sector is in solid shape and the ISM Services PMI has posted four straight readings over the 50 level, which separates expansion from contraction.

Eurozone, German PMIs fall in June

Eurozone PMIs for June pointed to weaker activity in the services and manufacturing sectors. The Services PMI eased to 52.4, down from 55.1 in May and below the consensus of 54.5 points. The Manufacturing PMI fell to 43.6, down from the May reading of 44.8 which was also the consensus. Germany, the largest economy in the eurozone, showed a similar trend, with Services PMI falling from 54.7 to 54.1 and Manufacturing PMI dropping from 43.5 to 41.0 points. The 50 line separates contraction from expansion.

The takeaway from these numbers is that the eurozone economy is cooling down. Business activity is still growing but at a weaker pace, while the manufacturing recession has deepened. The eurozone economy is yet to recover after negative growth in the past two quarters, as the ECB’s aggressive tightening makes its way through the economy.

At first glance, the weak PMI readings should be good news for the ECB, which is trying to dampen economic growth in order to wrestle inflation back down to the 2% target. However, inflation remains very high at 6% and further tightening could tip the weak eurozone economy into a recession.

The ECB’s efforts to push inflation lower have been made more difficult, as unemployment is at historic lows and wage growth is high. Germany, the bloc’s largest economy, isn’t the power locomotive that it once was and is still in recovery mode. The ECB has signalled that it will hike rates in July and another increase could be coming in September unless inflation decelerates more quickly.

EUR/USD Technical

- EUR/USD is testing support at 1.0882. The next support level is 1.0793

- 1.0976 and 1.1031 are the next resistance lines

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0933; (P) 1.0972; (R1) 1.0995; More...

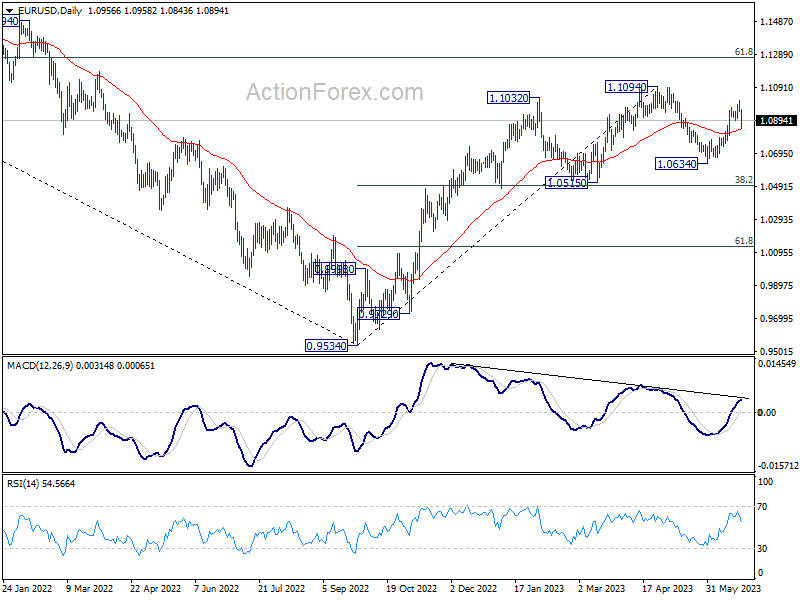

Intraday bias in EUR/USD remains mildly on the downside at this point. Fall from 1.1011 is seen as the third leg of the corrective pattern from 1.1094. Sustained break of 55 D EMA (now at 1.0838) will target 1.0634 support and below. Nevertheless, rebound from current level, followed by break of 1.1011 will target a test on 1.1094 high instead.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2707; (P) 1.2767; (R1) 1.2809; More...

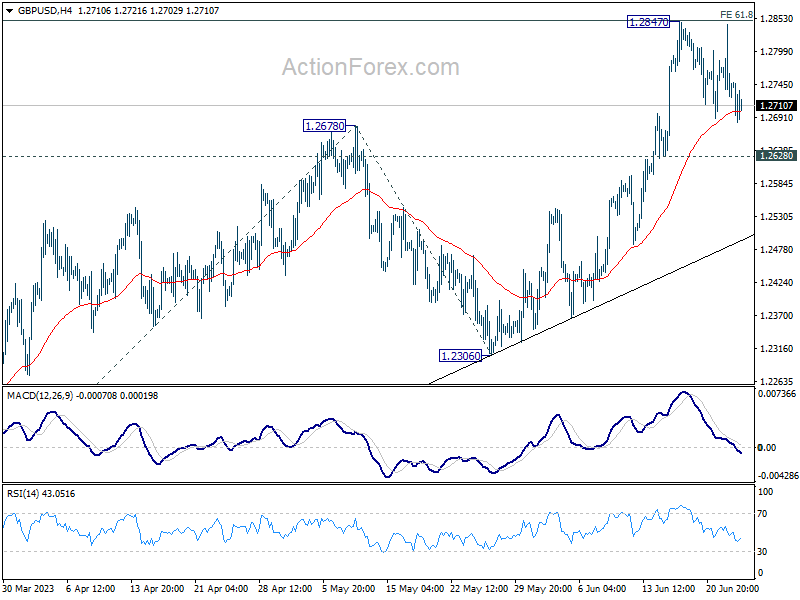

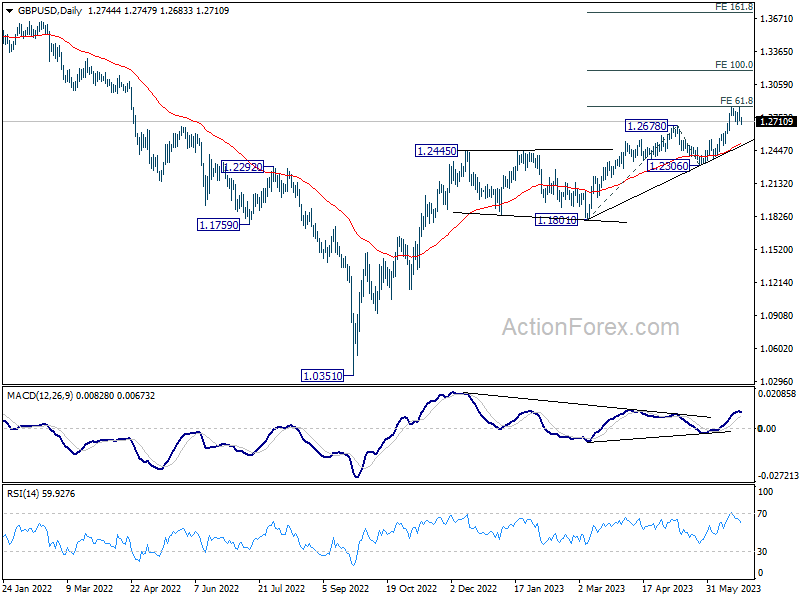

GBP/USD is still bounded in consolidation from 1.2847 and intraday bias stays neutral. On the upside, firm break of 1.2847 will resume larger up trend and target 100% projection of 1.1801 to 1.2678 from 1.2306 at 1.3183 next. However, firm break of 1.2628 will turn bias to the downside, for deeper fall to 1.2306 support instead.

In the bigger picture, the strong support from 55 W EMA (now at 1.2345) is a medium term bullish sign. Outlook will stay bullish as long as 1.2306 support holds. Rise from 1.0351 medium term bottom (2022 low) is expected to extend further to retest 1.4248 key resistance (2021 high).

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8914; (P) 0.8943; (R1) 0.8979; More...

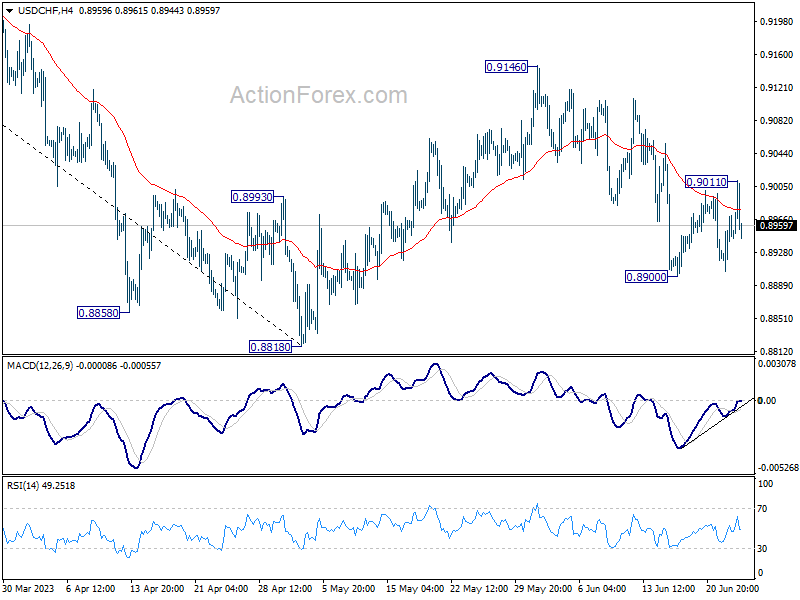

Intraday bias in USD/CHF is turned neutral again with current retreat. On the upside, above 0.9011 will bring stronger rise towards 0.9146 resistance. On the downside, through, break of 0.8900 will target 0.8818 and possibly below.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high), which might have completed at 0.8818 already, just ahead of 0.8756 long term support. Sustained trading above 0.9058 support turned resistance should confirm medium term bottoming.

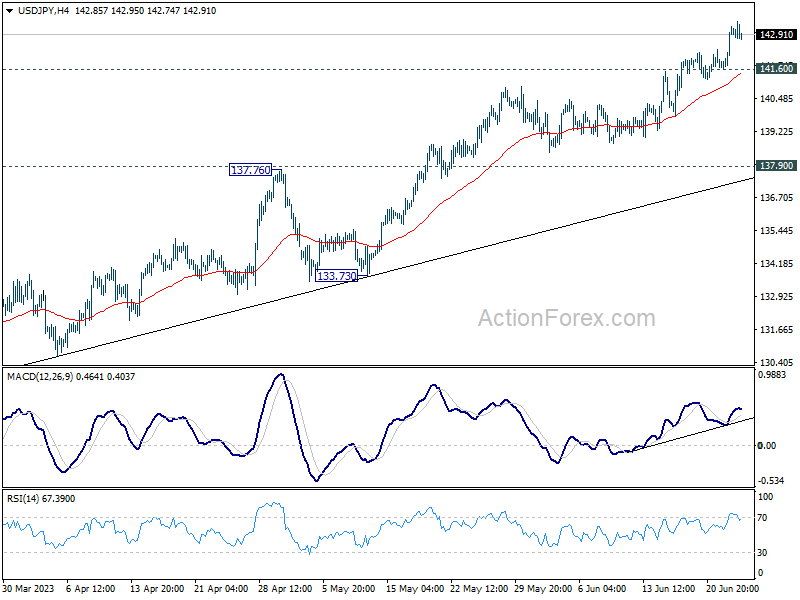

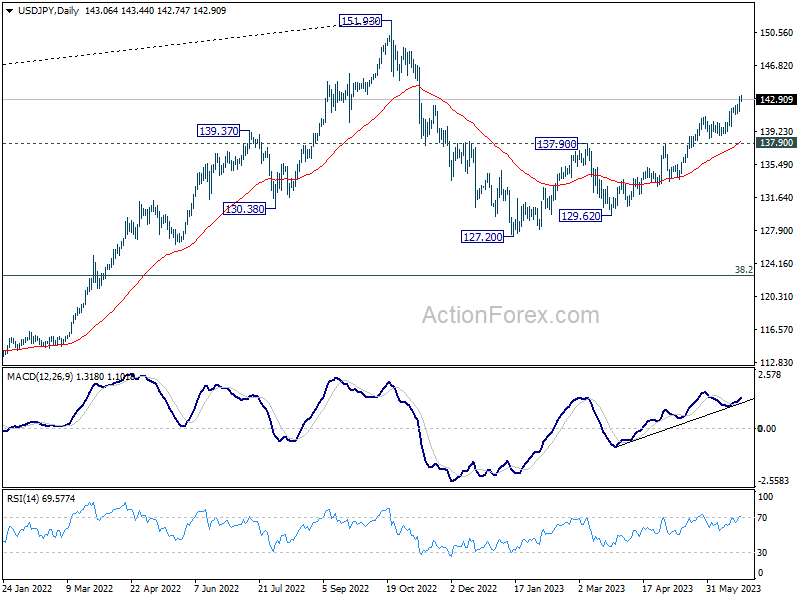

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.07; (P) 142.65; (R1) 143.69; More...

Intraday bias in USD/JPY remains on the upside for the moment. Current rise from 127.20 would target a retest on 151.93 high. On the downside, below 141.20 minor support will turn intraday bias neutral first. But further rally will now remain in favor as long as 137.90 resistance turned support holds.

In the bigger picture, rise from 151.93 are seen as a corrective pattern to up trend from 102.58. The first leg has completed at 127.20. Rebound from there is seen as the second leg, and should be limited below 151.93. Sustained trading below 55 D EMA (now at 137.93) will argue that the third leg has started back to 127.20 and possibly below.

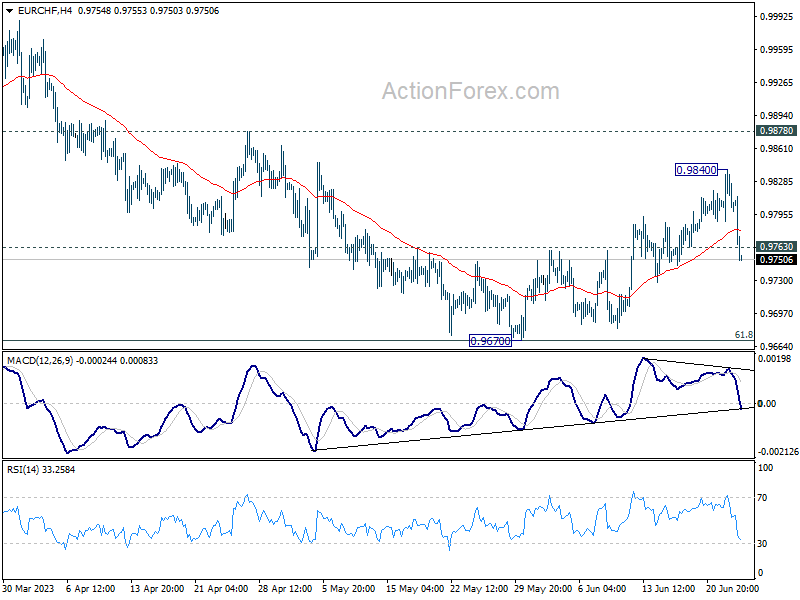

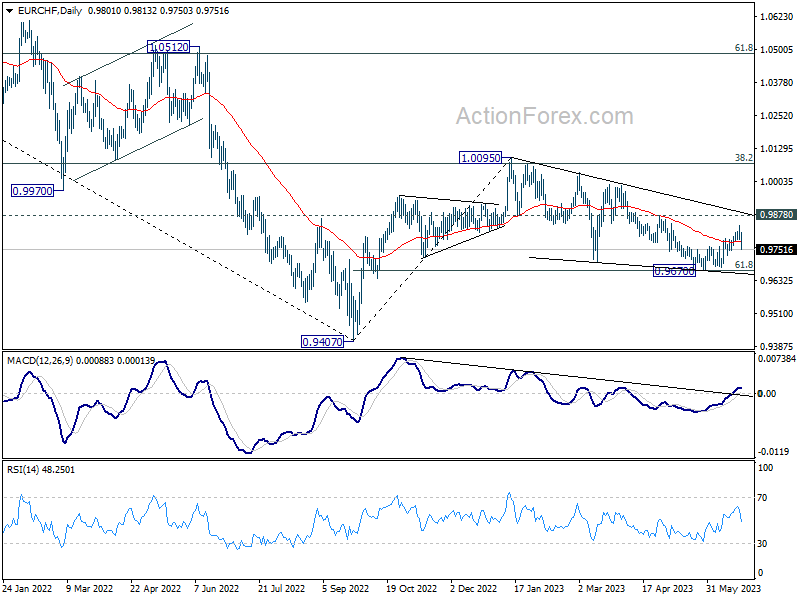

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9783; (P) 0.9812; (R1) 0.9834; More...

EUR/CHF's break of 0.9763 minor support argues that recovery from 0.9670 has completed as a correction to 0.9840 Intraday bias is back on the downside for retesting 0.9670 low. Sustained break there will resume the whole fall from 1.0095. Nevertheless, break of 0.9840 will resume the rebound to 0.9878 resistance.

In the bigger picture, prior rejection by 38.2% retracement of 1.1149 to 0.9407 at 1.0072 suggests that medium term outlook is staying bearish. The pair is also capped below 55 W EMA (now at 0.9924). Down trend from 1.2004 (2018 high) is not complete yet and is in favor to resume through 0.9407 at a later stage. However, decisive break of 1.0095 resistance will raise the chance of bullish trend reversal. Rise from 0.9407 should then target 1.0505 cluster resistance (2020 low at 1.0505, 61.8% retracement of 1.1149 to 0.9407 at 1.1484).

Euro Dips on Poor PMI Data, Dollar Losing Some Momentum

Dollar has launched a broad-based rebound in today's market. However, momentum appears to be faltering against its European counterparts in early U.S. trading session. Although it continues to perform strongly against Yen and Australian dollar, the greenback has been struggling to break last week's high against other key currencies. Consequently, this rebound seems to be more of a corrective move than a robust up trend. Nevertheless, today's surge could potentially signal a period of consolidation that might extend through the remainder of the month.

Meanwhile, Euro has suffered broad losses today, driven by disappointing PMI data. While a July rate hike by ECB seems almost certain, the outlook beyond that point is clouded in uncertainty. Australian and New Zealand Dollars, have taken a severe hit following sell-off in Hong Kong stocks and continuous decline in Chinese Yuan. Despite being among the week's worst performers, Yen is experiencing a slight recovery against other currencies, with the notable exception of Dollar.

In Europe, at the time of writing, FTSE is down -0.57%. DAX is down -1.20%. CAC is down -0.60%. Germany 10-year yield is down -0.165 at 2.335. Earlier in Asia, Nikkei fell -1.45%. 10-year JGB yield dropped -0.0072 to 0.372. Hong Kong HSI fell -1.71%. Singapore Strait Times fell -0.96%.

ECB de Cos: Not appropriate to forecast rates after July hike

ECB Governing Council member Pablo Hernandez de Cos conveyed his anticipation of another interest rate hike. He underscored that ECB's decisions would continue to rely on key data and inflation outlook.

He stated today, "If the central scenario of our forecasts published by the ECB last week materialises, we will also have to raise 25 basis points again in July." However, "beyond that it is not appropriate to make any forecasts."

De Cos highlighted the essential role of key data and inflation dynamics in shaping ECB's decisions. He added, "we will continue to take our decisions depending on the data and, in particular, on the aggregate assessment of the inflation outlook, the dynamics of underlying inflation."

Eurozone PMI manufacturing down to 43.6, services down to 52.4

Eurozone PMI Manufacturing fell from 44.8 to 43.6 in June, a 37-month low. PMI Services dropped from 52.4 to 55.1, a 5-month low. PMI Composite tumbled from 52.8 to 50.3, a 5-month low.

HCBO Bank noted in the release that there are diverging trends in the manufacturing and service sectors. Despite falling prices in manufacturing that would typically herald rate cuts, persistent price hikes in the larger service sector continue to slow down core inflation's decline.

Adding to the complexity are regional differences: France's service sector contracted in June while Germany's continues to expand. With Eurozone GDP potentially falling for a third consecutive quarter, the Composite PMI predicts a challenging second half of the year for businesses.

In France, PMI Manufacturing ticked down from 45.7 to 45.5 in June, a 37-month low. PMI Services dropped sharply from 52.5 to 48.0, a 28-month low. PMI Composite fell from 51.2 to 47.3, a 28-month low.

In Germany, PMI Manufacturing fell from 43.2 to 41.0, a 27-month low. PMI Services dropped from 57.2 to 54.1, a 3-month low. PMI Composite declined from 53.9 to 50.8, a 4-month low.

UK PMI manufacturing down to 46.2, Services down to 53.7

UK PMI Manufacturing fell from 47.1 to 46.2 in June, a 6-month low. PMI Services dropped from 55.2 to 53.7, a 3-month low. PMI Composite lowered from 54.0 to 52.8, a 3-month low.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

"June's flash PMI survey indicates that the UK economy has lost momentum again after a brief growth spurt in the spring, and looks set to weaken further in the months ahead.

"Most notably, consumer spending on services, which was a core growth driver in the spring, is now showing signs of faltering… The manufacturing sector meanwhile continues to report recessionary conditions.

"One notable area of resilience in the economy is the labour market…While falling backlogs of work suggest this hiring trend could also fade in the coming months as the economy weakens.

"The survey's price gauges point to consumer price inflation remaining well above the Bank of England's target into 2024, which will add to the case for further interest rate hikes…

"Stubbornly elevated price growth in the service sector suggests the Bank of England will consider its fight against inflation as still a work in progress.

Japanese Finance Minister speaks out amid rapid Yen depreciation

As Yen continues to face intense selling pressure, Japanese Finance Minister Shunichi Suzuki reiterated the importance of market-determined exchange rates and the undesirability of abrupt currency movements.

Suzuki stated, "Currency rates should be set by the market, reflecting fundamentals." He also emphasized the need for stability, saying, "Sharp moves are undesirable, currencies should move stably reflecting fundamentals. With that in mind, we will continue to keep firm watch on market moves."

His comments come as the USD/JPY surged past the 143 handle, marking a significant acceleration in Yen's recent depreciation. The slide began last week following BoJ's decision to maintain its ultra-loose monetary policy stance. Today's strong inflation data, rather than tempering Yen's decline, seemed to have had little impact in averting its downtrend.

The verbal intervention from Suzuki underscores the growing concern over the pace and extent of Yen's depreciation. It also signals the government's readiness to monitor market trends closely, and possibly intervene should the currency's movements threaten to undermine the economic fundamentals.

Japan PMI manufacturing fell to 49.8, services down to 54.2

Japan PMI Manufacturing declined from 50.6 to 49.8 in June, below expectation of 50.2. PMI Manufacturing Output fell from 50.9 to 48.3. PMI Services dropped from 55.9 to 5.4.2. PMI Composite decreased from 54.3 to 52.3.

Annabel Fiddes, Economics Associate Director at S&P Global Market Intelligence, said:

"A fresh fall in manufacturing output coincided with a softer rise in services activity, leading to the weakest expansion of overall output for four months....

"The softening of growth momentum fed through to reduced optimism around the outlook, with business confidence slipping to a five-month low...

"However, there was some better news in terms of inflationary pressures, which showed further signs of easing. Notably, input price inflation softened to a 22-month low in June, while output charges increased at the softest pace since January."

Australia PMI composite fell to 50.5, RBA has time on their side

Australia PMI Manufacturing ticked up from 48.4 to 48.6 in June. PMI Services fell from 52.1 to 50.7. PMI Composite declined from 51.6 to 50.5.

Warren Hogan, Chief Economic Advisor at Judo Bank said:

"The loss of momentum in recent months will probably give the RBA some comfort that economic activity is slowing down across the economy in 2023, following their consecutive rate hikes in May and June...

"The survey suggests that the RBA has time on their side and does not necessarily need to hike rates again in July. The slowdown taking place across the economy provides further evidence that the point at which the RBA can undertake a genuine pause in their tightening cycle is getting closer.

"We cannot rule out a further hike in the next few months, but we are close to a level of interest rates whereby the RBA can sit back for 4-6 months and observe the effects of past interest rate increases."

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9783; (P) 0.9812; (R1) 0.9834; More...

EUR/CHF's break of 0.9763 minor support argues that recovery from 0.9670 has completed as a correction to 0.9840 Intraday bias is back on the downside for retesting 0.9670 low. Sustained break there will resume the whole fall from 1.0095. Nevertheless, break of 0.9840 will resume the rebound to 0.9878 resistance.

In the bigger picture, prior rejection by 38.2% retracement of 1.1149 to 0.9407 at 1.0072 suggests that medium term outlook is staying bearish. The pair is also capped below 55 W EMA (now at 0.9924). Down trend from 1.2004 (2018 high) is not complete yet and is in favor to resume through 0.9407 at a later stage. However, decisive break of 1.0095 resistance will raise the chance of bullish trend reversal. Rise from 0.9407 should then target 1.0505 cluster resistance (2020 low at 1.0505, 61.8% retracement of 1.1149 to 0.9407 at 1.1484).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:00 | AUD | Manufacturing PMI Jun P | 48.6 | 48.4 | ||

| 23:00 | AUD | Services PMI Jun P | 50.7 | 52.1 | ||

| 23:01 | GBP | GfK Consumer Confidence Jun | -24 | -26 | -27 | |

| 23:30 | JPY | National CPI Y/Y May | 3.20% | 3.50% | ||

| 23:30 | JPY | National CPI Core Y/Y May | 3.20% | 3.10% | 3.40% | |

| 23:30 | JPY | National CPI Core-Core Y/Y May | 4.30% | 4.10% | ||

| 00:30 | JPY | Manufacturing PMI Jun P | 49.8 | 50.2 | 50.6 | |

| 06:00 | GBP | Retail Sales M/M May | 0.30% | -0.20% | 0.50% | |

| 07:15 | EUR | France Manufacturing PMI Jun P | 45.5 | 45.2 | 45.7 | |

| 07:15 | EUR | France Services PMI Jun P | 48 | 52.1 | 52.5 | |

| 07:30 | EUR | Germany Manufacturing PMI Jun P | 41 | 43.6 | 43.2 | |

| 07:30 | EUR | Germany Services PMI Jun P | 54.1 | 56.3 | 57.2 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Jun P | 43.6 | 44.9 | 44.8 | |

| 08:00 | EUR | Eurozone Services PMI Jun P | 52.4 | 54.5 | 55.1 | |

| 08:30 | GBP | Manufacturing PMI Jun P | 46.2 | 46.8 | 47.1 | |

| 08:30 | GBP | Services PMI Jun P | 53.7 | 54.9 | 55.2 | |

| 13:45 | USD | Manufacturing PMI Jun P | 48.5 | 48.4 | ||

| 13:45 | USD | Services PMI Jun P | 54 | 54.9 |