Sample Category Title

FOMC Skips June, But Signals Hikes Not Done Yet

Summary

- As widely expected, the FOMC decided unanimously to refrain from raising rates at today's meeting.

- However, the Committee continued to say that "additional policy firming" may be appropriate. Furthermore, the median dot for 2023 shifted up by 50 bps. That is, most FOMC members believe that another 50 bps of tightening may be appropriate by the end of 2023. Prior to the meeting, the bond market was priced for only 25 bps of additional tightening.

- The Committee lowered its forecast of the unemployment rate at year-end 2023 and lifted its outlook for core PCE inflation at the end of the year.

- None of the 18 FOMC members at present think that a rate cut by the end of 2023 would be appropriate.

- In our view, the year-over-year rate of core PCE inflation does not need to be precisely at 2% to lead the Committee to ease policy. But, the FOMC does need to see evidence that it is heading back toward 2% on a sustained basis. We do not think that evidence will be forthcoming this year.

- We look for the FOMC to raise rates by another 25 bps at its next meeting on July 26 before calling it quits. But, we readily acknowledge that the risks to our fed funds rate forecast are skewed to the upside.

FOMC on Hold, But Leaning Toward More Tightening

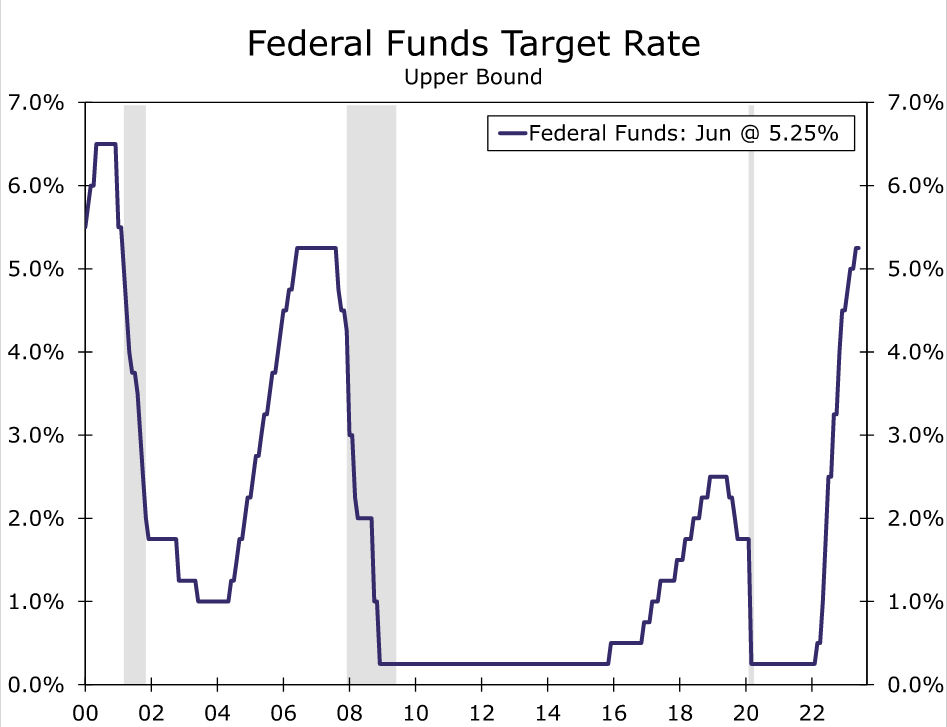

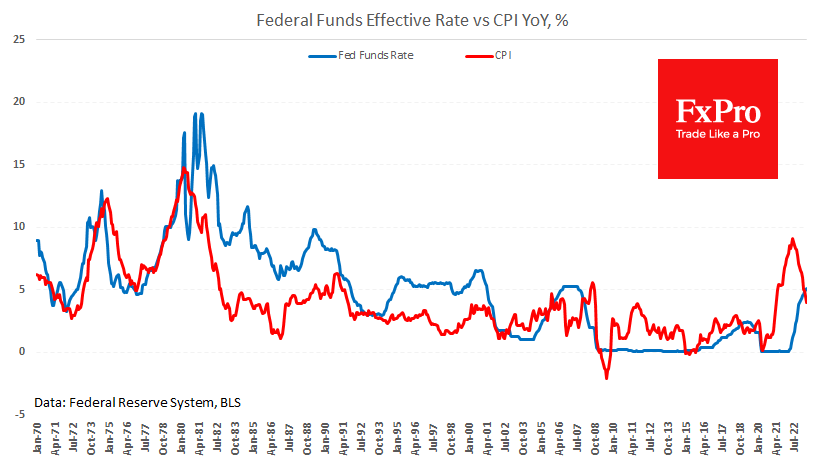

As widely expected, the Federal Open Market Committee (FOMC) refrained from hiking rates at its policy meeting today, which is the first time in 11 meetings that the Committee left the fed funds rate unchanged (Figure 1). The decision to keep the target range at 5.00%-5.25% was supported by all 11 members who were eligible to vote at this meeting. The FOMC also decided to keep its pace of quantitative tightening unchanged. That is, the Federal Reserve will allow up to $60 billion of Treasury securities and up to $35 billion of mortgage-backed securities to roll off its balance sheet every month.

Today's post-meeting statement was little changed from the last statement on May 3. The Committee continued to note that economic activity is expanding at a "modest pace" and that unemployment remains low and inflation "remains elevated." The FOMC said that its decision to keep rates on hold would give it the ability "to assess additional information and its implications for monetary policy." The Committee re-iterated the phrase that it first used in the May 3 statement. That is, it will consider a number of factors to determine the extent that "additional policy firming may be appropriate to return inflation to 2 percent over time." These factors include "the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments."

Dot Plot Shifts Up

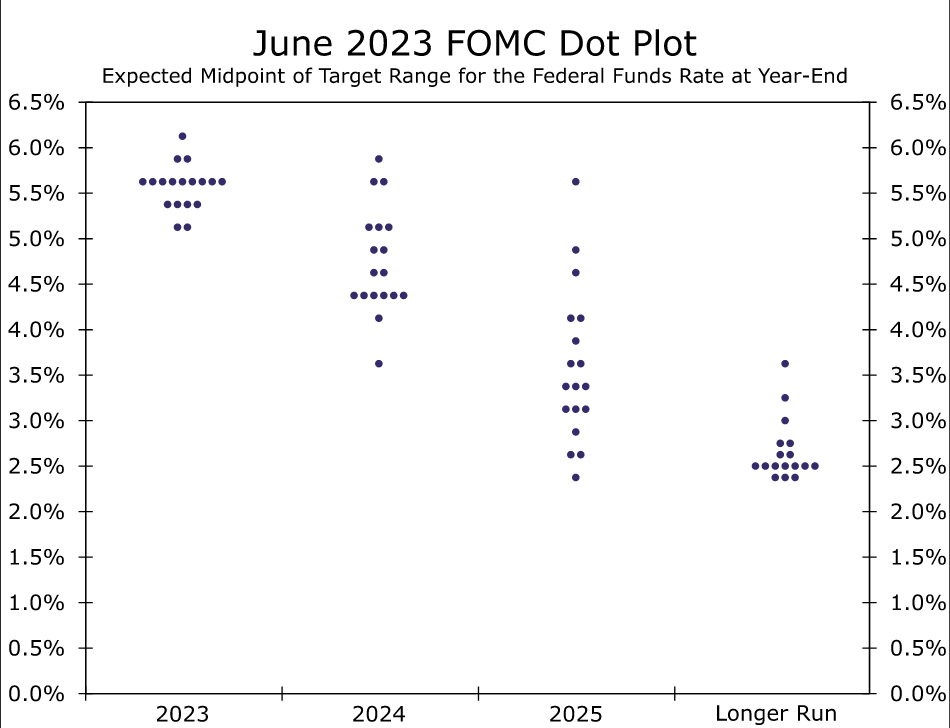

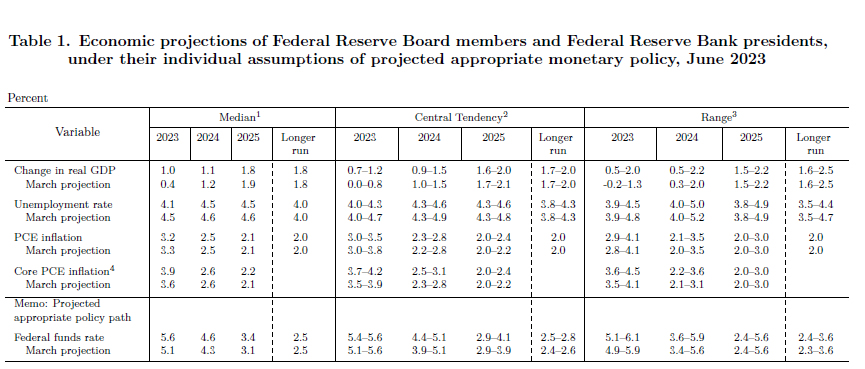

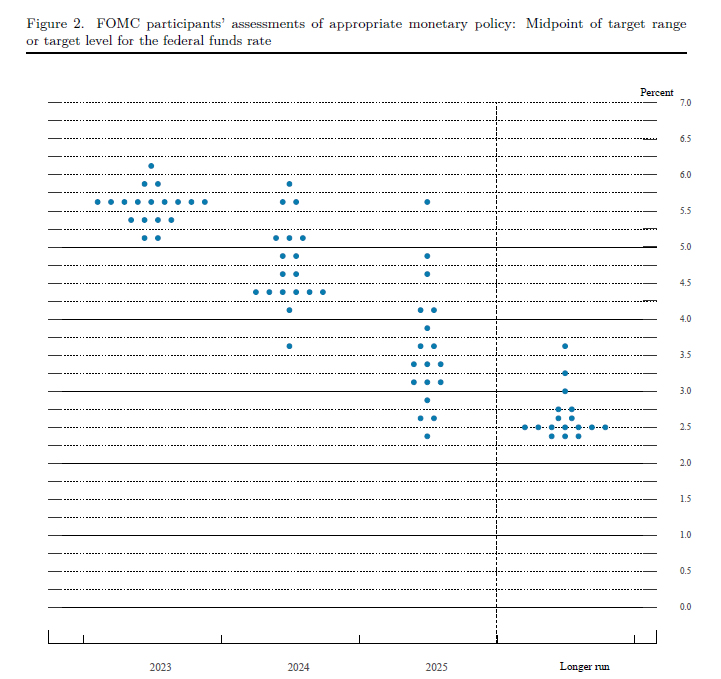

According to the Summary of Economic Projections (SEP), which the FOMC releases four times per year and outlines its macroeconomic forecasts, most members of the Committee believe that additional policy firming may be appropriate this year. That is, the so-called "dot plot" that was released following the March 22 meeting showed that the median FOMC member thought that a fed funds target range of 5.00%-5.25% would be appropriate at the end of 2023. The dot plot that was released today showed the median dot shifting up to a range of 5.50%-5.75% at the end of this year (Figure 2). In other words, the median FOMC member believes that another 50 bps of tightening will be needed by the end of the year "to return inflation to 2 percent over time." As we go to print, the bond market remains priced for only one more 25 bps rate hike by the end of 2023, most likely at the July meeting.

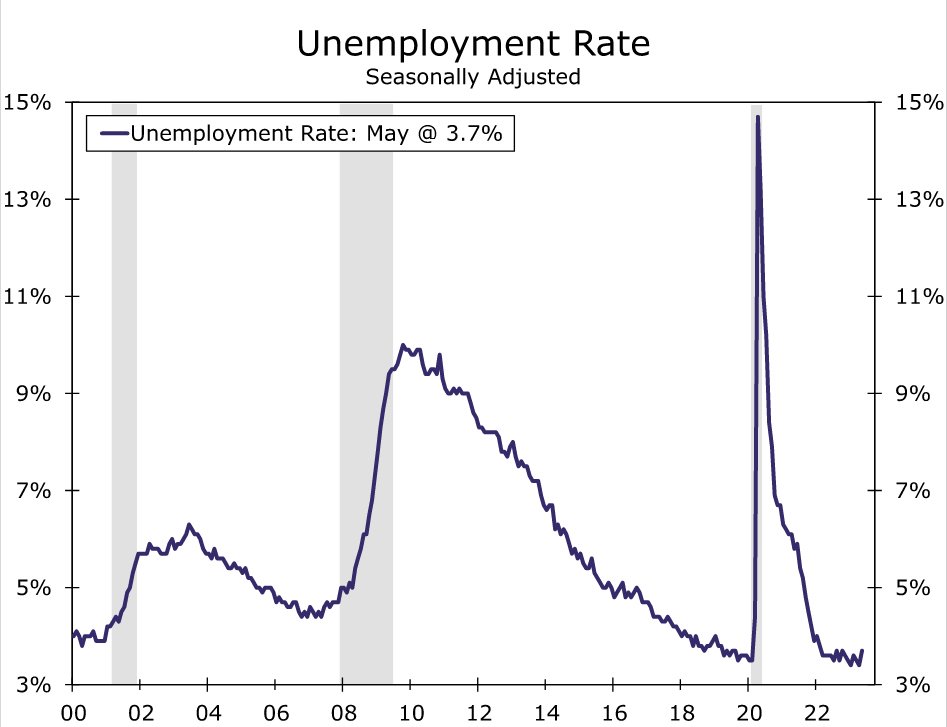

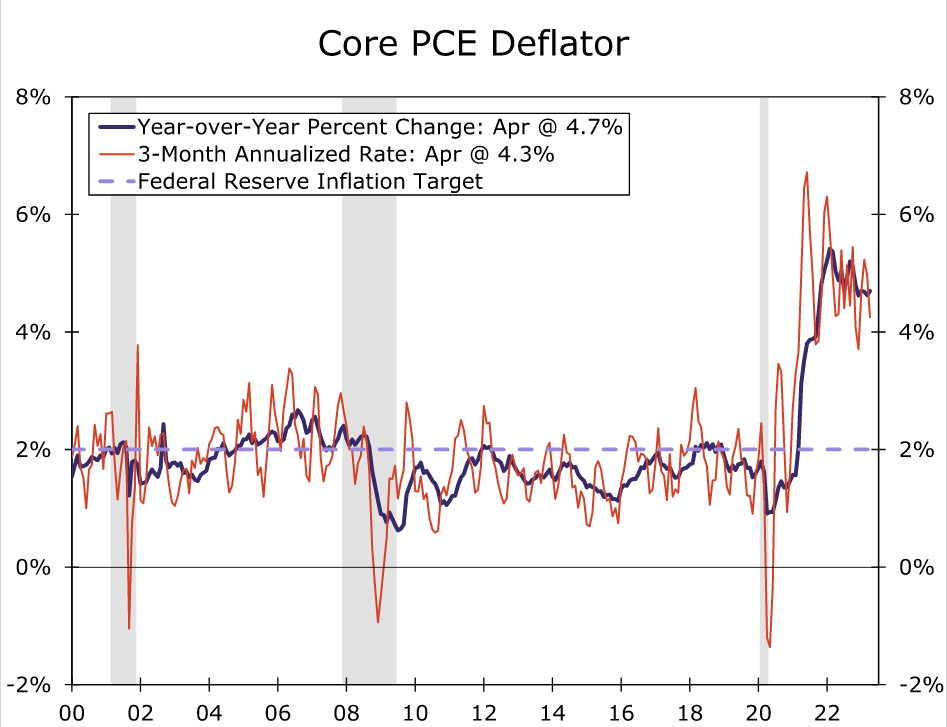

Why the change in the dots? The answer: the FOMC changed its forecasts of unemployment and inflation. As shown in Figure 3, the unemployment rate remains exceptionally low at present, and the Committee nows sees it rising to only 4.1% by the end of 2023 (the median participant in March forecasted it rising to 4.5% at the end of the year.) Additionally, the median forecast for the core rate of PCE inflation at year-end 2023 was lifted from 3.6% in March to 3.9% today. Interestingly, none of the 18 FOMC members at present thinks that a rate cut by the end of the year would be appropriate.

What will the FOMC need to see to start easing policy? Barring some unforeseen negative shock to the economy in the near term, the Committee wants to see evidence that inflation is returning to 2% on a sustained basis. As shown in Figure 4, the rate of inflation has eased marginally in recent months but only an optimist would look at that chart and see evidence that inflation is returning to 2%. In our view, the year-over-year rate of inflation does not need to be precisely at 2% before the Committee begins to ease policy. But, our forecast is that the core PCE deflator will increase at an annualized rate of 2.8% in Q4-2023 relative to Q3-2023, which we think is still too hot to induce the FOMC to cut rates. Consequentially, we do not look for a rate cut this year, which is consistent with the FOMC's thinking at present.

The next FOMC meeting is scheduled for July 26. We expect that the continued resilience of the economy and the elevated rate of inflation will lead the Committee to hike by another 25 bps at that meeting. Indeed, Chair Powell stated in his post-meeting press conference that the July FOMC meeting will be a "live meeting." We then look for the Committee to remain on hold for the remainder of the year. However, given today's dot plot, we readily acknowledge that the risks to our fed funds forecast are skewed to the upside. We think it will take a modest recession early next year, which will help to bring inflation lower, to induce the FOMC to ease policy. See our most recent U.S. Economic Outlook for details of our forecast.

Fed Chair Powell press conference live stream

https://www.youtube.com/watch?v=L61NSlLRGe8

Fed stands pat, but projections two more hikes this year, on stronger growth and core inflation

Fed keeps interest rate unchanged at 5.00-5.25% as widely expected, by unanimous vote. The new economic projections are rather hawkish, with 2023 median rate projections raised to 5.6% (two more 25bps hikes). GDP growth and core PCE inflation were revised higher while unemployment rate was revised lower.

FOMC leaves the door open for more tightening, as "the Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals.:

Fed added that the assessments will take into account information including "readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.".

In the new economic projections, median federal funds rates for 2023 is raised from 5.1% to 5.6%, indicating two more 25bps hike. Median projections for 2024 was raised from 4.3% to 4.6%, for 2025 raised from 3.1% to 3.4%.

Regarding 2023 median economic projections, real GDP growth was raised sharply higher from 0.4% to 1.0%, unemployment rate sharply lower from 4.5% to 4.1%, core PCE inflation from 3.6% to 3.9%.

In the new dot plot, twelve members penciled in rate hikes to 5.50-5.75% this year, with four expecting rate at 5.25-5.50%, and only two at the current 5.00-5.25%.

(FED) Federal Reserve Issues FOMC Statement

Recent indicators suggest that economic activity has continued to expand at a modest pace. Job gains have been robust in recent months, and the unemployment rate has remained low. Inflation remains elevated.

The U.S. banking system is sound and resilient. Tighter credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. The extent of these effects remains uncertain. The Committee remains highly attentive to inflation risks.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to maintain the target range for the federal funds rate at 5 to 5-1/4 percent. Holding the target range steady at this meeting allows the Committee to assess additional information and its implications for monetary policy. In determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Lisa D. Cook; Austan D. Goolsbee; Patrick Harker; Philip N. Jefferson; Neel Kashkari; Lorie K. Logan; and Christopher J. Waller.

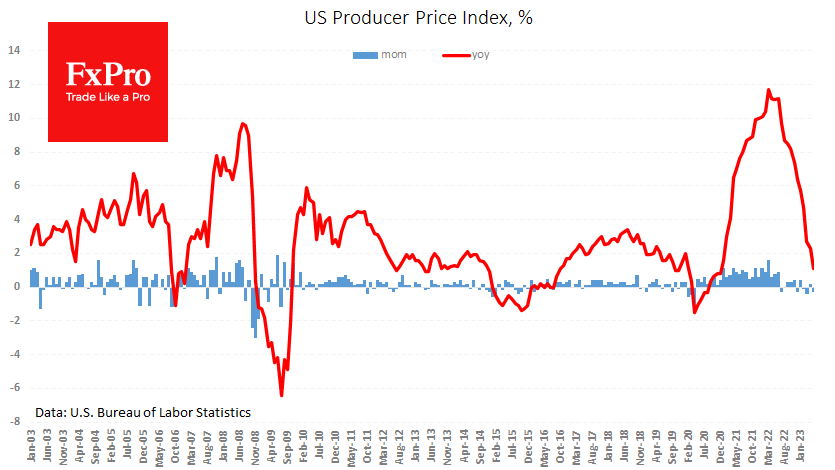

US PPI Confirm Disinflationary Trends

US producer prices fell stronger than expected, potentially reinforcing the dovish argument at the Fed. For May, PPI declined by 0.3% m/m, more than the expected 0.1%, and the index gained a modest 1.1% y/y after 2.3% a month earlier.

In contrast to the core CPI, the PPI shows a return to desired inflation numbers, with the monthly price growth rate well within the Central Bank target.

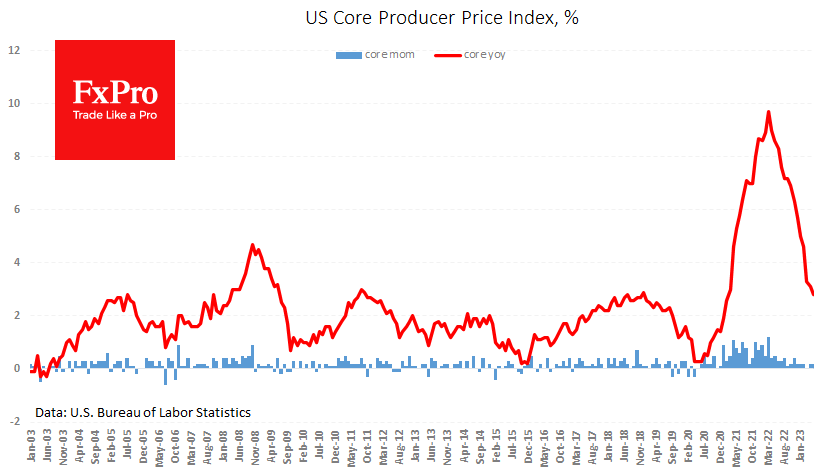

The core PPI, which excludes food and energy, added 0.2% m/m and 2.8% y/y. The annual rate was lower than 3.2% a month earlier and the expected 2.9%.

Were it not for a strong labour market and the resulting robust consumer demand, the producer price development should have been regarded as a leading indicator for the CPI. However, in a full employment environment, retailers can use the situation to support their margins by justifying it with increased interest expenses.

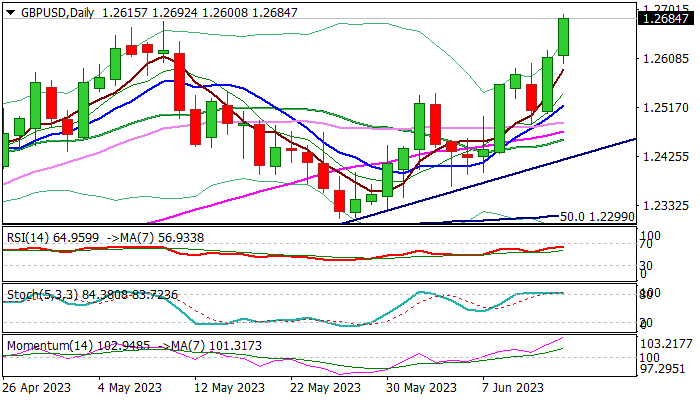

GBP/USD Outlook: Cable Hits New 2023 High

Cable hit new 2023 high on Tuesday on fresh bullish acceleration which extends into the second consecutive day.

Sterling received fresh support from weaker than expected US producer prices in May, which showed the smallest annual increase in 2 ½ years, adding to expectations that the Fed will stay on hold in June meeting which ends today.

Pound was also underpinned by hawkish rate outlook, as the Bank of England remains on track for further rate hikes, in a battle with inflation which is currently more than four times higher than BoE’s target, while economists remain optimistic and say that the economy is unlikely to enter recession.

The central bank is widely expected to raise interest rates by additional 25 basis points to 4.75% in June 22 meeting, with economists being divided about terminal rate, expecting peak at 5.00% and 5.50% range, while markets see rates climbing to 5.75% before start to turn lower.

Strongly hawkish stance of UK policymakers fuels pound’s latest rally, which broke through previous peak and turning focus towards next targets at 1.2759 (Fibo 61.8% of 1.4249/1.0348 downtrend) and 1.2874 (200WMA) which guards psychological 1.30 barrier.

Bulls require daily close above 1.2679 (former annual top of May 10) to be confirmed, with all eyes being on Fed.

The US central bank is likely to pause this time, but markets will be closely watching comments from Fed Chair Powell, for more clues about their next steps.

Initial supports lay at 1.2600/1.2590 zone (session low / rising 5DMA) followed by 1.2534 (daily cloud top) and 1.2521 (10DMA).

Res: 1.2700; 1.2759; 1.2874; 1.3000.

Sup: 1.2600; 1.2534; 1.2487; 1.2457.

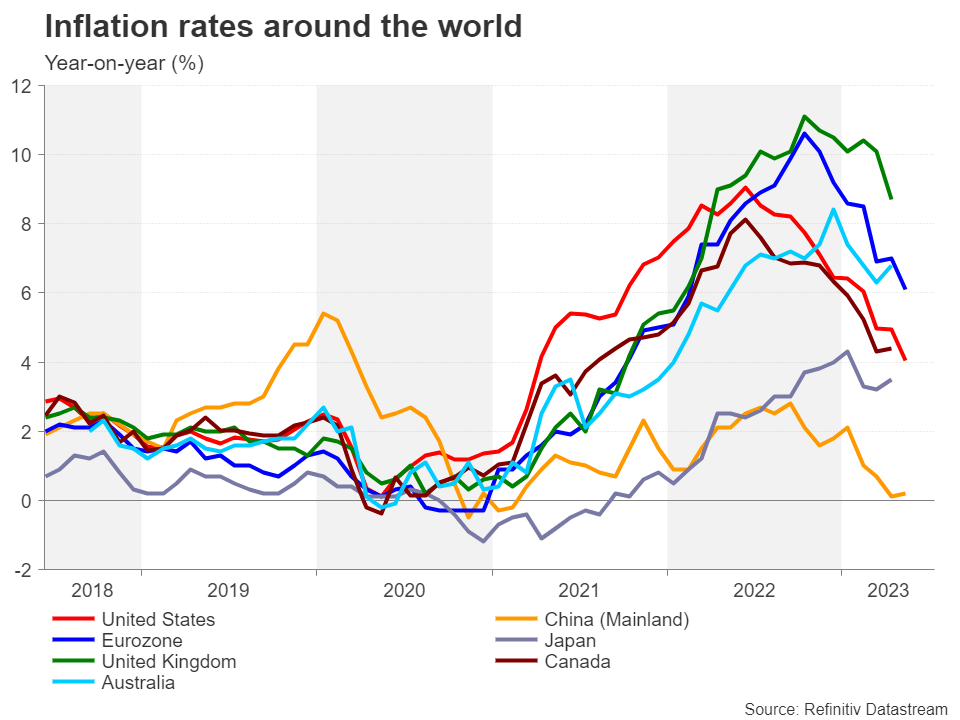

Is Inflation About to Fall Off a Cliff?

Inflation may have finally peaked around the world, but central banks remain on alert amid an uptick in some countries and the stickiness of underlying price measures in others. Whilst the view that inflation will continue to decline in the coming months hasn’t changed, policymakers are concerned that it’s not coming down fast enough, and this raises the risk that inflation expectations may start to become unanchored. But what if the risk of that happening isn’t very high at all and the real danger for central banks is inflation falling off a cliff?

Overcompensating for a policy mistake?

It goes without saying that inflation is one of the most important economic indicators that policymakers, analysts and investors, as well as the wider public, watch. But that doesn’t detract from the fact that inflation is a lagging indicator, meaning that it measures the changes in price levels after they have occurred and not before it. This makes the job for central banks quite difficult as they have to base their decisions on interest rates on the predicted path of inflation, often leading to policy mistakes, such as in 2021 when the initial warning signs of simmering prices were deemed to be transitory.

Scarred by that misjudgement, central banks took a very hard line on inflation in 2022 and even now when CPI rates are headed down globally, the likes of the Federal Reserve and European Central Bank are only slowly letting their guards down. This caution seems warranted when considering that consumer demand in just about every region has remained resilient against the rising cost of living and higher borrowing costs, many economies are still experiencing widespread labour shortages and the overall economic pain of the most aggressive tightening cycle in decades has been surprisingly small.

Guided by inflation expectations

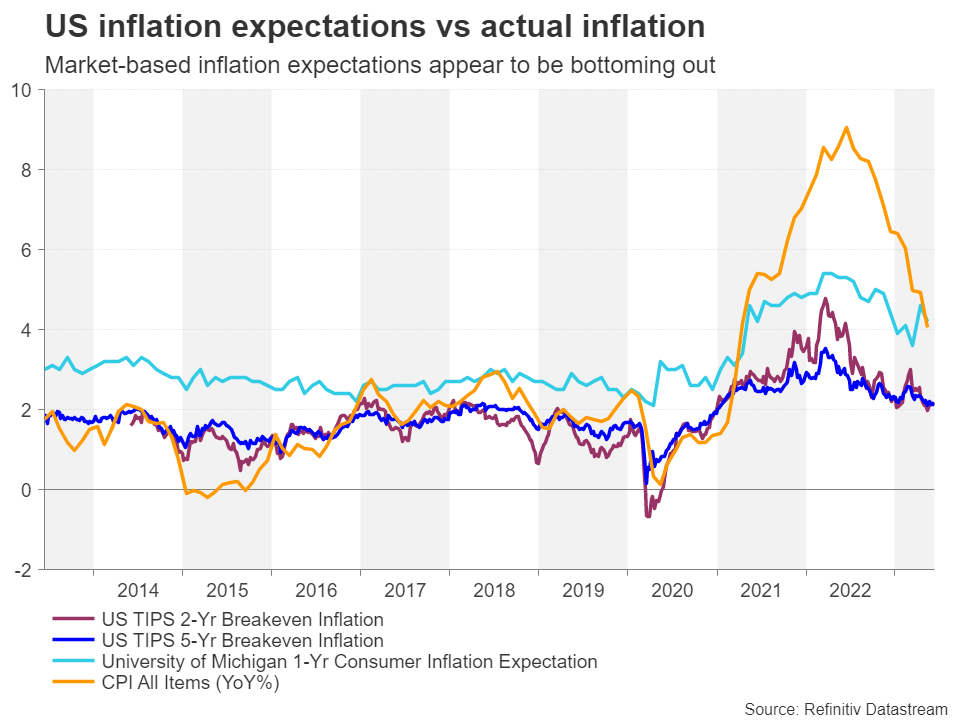

However, the fight against high inflation has probably reached its most crucial stage as policymakers have to factor in the substantial policy tightening that’s already in the pipeline against the need for additional rate hikes amid the sticky price pressures. Hence, there is increasing attention on the various leading indicators of inflation for clues on its future trend.

Measures of expected inflation are the foremost leading indicators that central bankers keep an eye on. For the US, there are some very encouraging signals from the two- and five-year breakeven inflation rates as these market-based gauges have settled just above 2%. But this is not a very conclusive sign as they were not particularly great at predicting the extent of the price surges in 2021 and 2022 and they should ideally be hovering slightly below 2% rather than above it, as was the case in the decade before the pandemic.

Moreover, a closely watched consumer-based expectation of inflation – the University of Michigan’s one-year inflation expectation – has edged up lately. Taken together, they could be interpreted as suggesting that the decline in inflation has stalled. In the euro area, inflation expectation based on the 5-year/5-year swap rate may not have even peaked yet and remains elevated near the all-time high of 2.58% set in May.

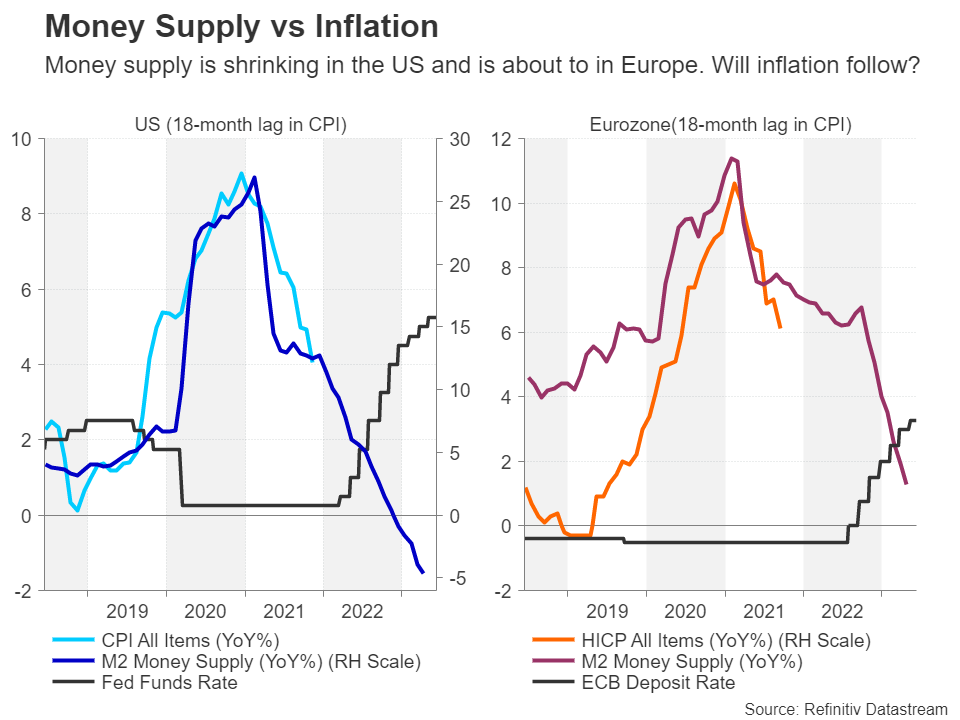

Money supply growth is plunging

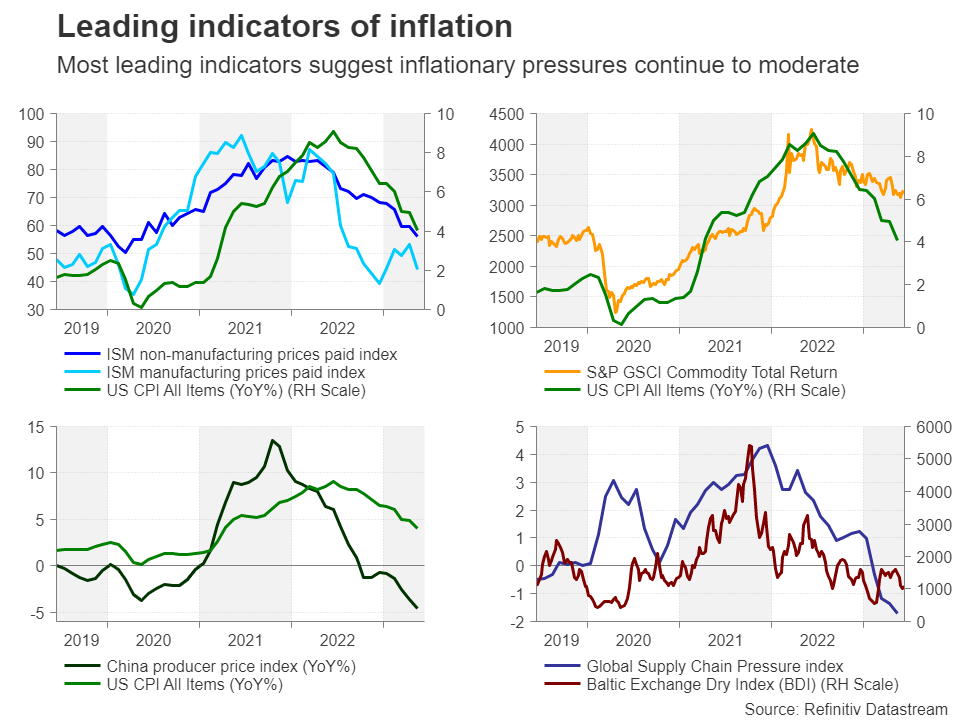

But other leading indicators paint a much more promising picture, and in some extreme cases, even a worrying one of disinflation going too far. One major red flag is the sharp drop in money supply growth in both the US and Eurozone. M2 growth in the US turned negative for the first time on record at the end of 2022 and European M2 growth is headed in the same direction. Although the pandemic stimulus is likely distorting these readings, the implied path does nevertheless point to further dramatic falls in inflation over the next 12 months.

As demonstrated in the charts above, the series of rate hikes on both sides of the Atlantic are having a clear impact in contraining money supply, though this should not be confused with net liquidity changes in the economy.

The only way is down

Another key indicator, one that is popular with investors, is the ISM prices paid index. Again, the trend here is downwards, particularly for non-manufacturing prices, and while manufacturing prices may have started to creep slightly higher, the drop in services inflation carries a lot more weight for the Fed as this has been its primary focus this year.

In addition, manufacturing prices in the US and globally have a close correlation with the price of goods coming out of China’s factories, which have been declining year-on-year since late 2022, signalling more disinflation is on the way. Reinforcing this view are the decreases in other industry indicators such as freight costs and supply pressures. One area of disappointment is commodity prices, which have yet to fully reverse their gains from the Ukraine war and crude oil is one of the few exceptions.

Overtightening fears

But on the whole, everything is pointing to inflation decelerating further this year and this raises the question, have central banks overtightened? Well, the jury is out on that and it will probably be a while before the outcome of the past year’s policy actions emerges.

However, with the rate-hike cycle now nearing the end in most Western economies, the angst about overtightening won’t simply vanish for investors when central banks go on a permanent pause and will linger on for the duration that they decide to hold rates at peak levels. The longer that rates are kept high, the greater the risk of recession fears eventually materializing.

FOMC: What Next For The US Dollar?

Get ready for the latest on the Federal Reserve's upcoming decision. In a surprising move, the Fed is expected to keep interest rates unchanged for the first time since embarking on an aggressive tightening cycle. But hold your horses. It's not a pivot or a pause!

The Fed may use this opportunity to signal that more rate hikes are on the horizon, depending on how the economy evolves, financial stability, and inflation trajectory. With a mixed bag of economic data and lingering uncertainties, caution is the name of the game. While the Fed will likely skip a rate increase this time, they may hint at the need for one or two more hikes by the end of 2023. It's a delicate policy compromise amid strong employment and inflation concerns. Stay tuned for the Fed's policy statement and projections, and listen out for Chairman Powell's press conference. Remember, no extended pause or rate cuts are expected for now. So buckle up and keep an eye on the ever-changing forex landscape!

US DOLLAR - Daily Timeframe

In line with my analysis last week, the US Dollar declined heavily from the pivot zone and resistance trendline. From all indications, the price is expected to continue on that downward path until it reaches the demand zone I’ve marked out - which would be the case if the Fed keeps the interest rate steady at the end of the day. I will watch for a sharp reaction from the marked demand zone before halting my hopes of a bearish continuation.

Analyst’s Expectations:

- Direction: Bearish

- Target: 102.660

- Invalidation: 103.646

EURUSD - Daily Timeframe

The bullish movement on EURUSD is yet to reach an efficient resistance level. Therefore, as highlighted in the chart above, the only logical poise is to expect a continuation of the bullish movement until the supply zone is reached. If the FOMC rates decision turns out to be dovish, the outlined direction would be the most likely outcome.

Analyst’s Expectations:

- Direction: Bullish

- Target: 1.08595

- Invalidation: 1.07501

GBPUSD - Daily Timeframe

GBPUSD has reached a crucial resistance level after commencing a solid rally from the 100-Day moving average, which on a regular day would imply a possibility of a bearish movement. However, in this case, we may see the price break clearly above that resistance level owing to the press release from the FOMC meeting later today. The interest rate is expected to play a vital role in the eventual outcome of the GBPUSD forecast.

Analyst’s Expectations:

- Direction: Bullish

- Target: 1.27401

- Invalidation: 1.25084

USDJPY - Daily Timeframe

USDJPY is inching closer to a major rally-base-drop supply zone and has been rejected from that area recently. Pending the release of the Fed interest rates figures, I believe we will see a decline of buying pressure from the USD, leading to a bearish momentum overall.

The confluences for this position include;

The resistance trendline

The rally-base-drop supply zone, and

The previous rejection from the supply zone

Analyst’s Expectations:

- Direction: Bearish

- Target: 136.494

- Invalidation: 141.014

CONCLUSION

The trading of CFDs comes at a risk. Thus, to succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.

Fed Could Signal the End of the Hike Cycle

The Fed’s rate decision is the most anticipated event of the day and possibly the coming weeks. As usual, the markets have a strong consensus on what the central bank will do in the short term, but they are more uncertain about its future moves. The tone of the statement and the assessment of the latest economic data are the primary sources of potential market volatility.

Rate futures indicate a 95% probability of keeping the key rate unchanged in the current 5.00-5.25% range, leaving only 5% for a chance of a policy tightening. However, the same FedWatch tool shows a 63% likelihood of a new 25-point rate hike at the end of July. Interestingly, the expected rates shift downward significantly further ahead, with only 35% betting that there will be no rate cut before the end of the year.

Since the beginning of the year, the markets have been consistently expecting a policy reversal – a sentiment that the Fed has been trying to counter by reassuring that it will not cut rates anytime soon. This divergence of view promises to be the most heated topic at Powell’s press conference later today and in his subsequent speeches.

The annual rate of overall inflation has declined for 11 consecutive months and is already below the key rate in May and June. The base effect (a 1.2% price increase for June 2022) suggests an even bigger drop in inflation, which would favour the Fed’s stance. A further rate hike seems unnecessary and risky for the banking system, which faced severe stress in March. It could also trigger a sharp policy reversal, worsening the financial sector’s problems and causing a steep economic slowdown.

On the other hand, a rate cut is not likely either. Higher monthly core CPI growth, on top of a tight labour market and relatively solid business reports, are reasons to maintain restrictive monetary conditions but not enough to tighten them.

If the Fed shares this view, it will signal a readiness to pause rate hikes while trying to change market expectations in favour of keeping current rates for the following quarters.