Sample Category Title

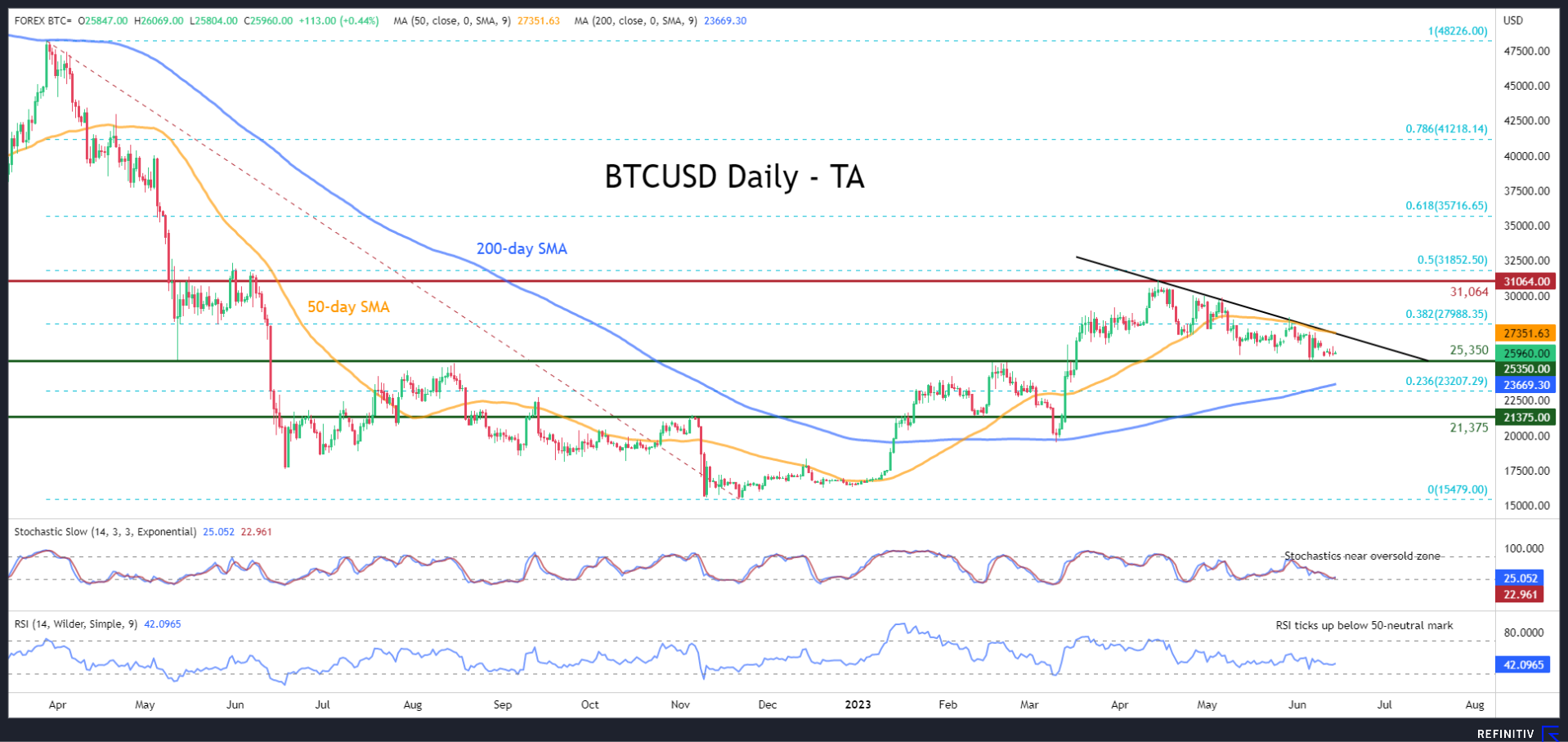

BTCUSD Trades Sideways, Bearish Pattern Remains Intact

BTCUSD (Bitcoin) has been generating a structure of lower highs and lower lows after peaking at the 11-month high of 31,064 in mid-April. However, the price has been rangebound in the past week, waiting for developments that could provide fresh directional impetus.

The momentum indicators are currently well within their negative territories, but they are also suggesting that positive momentum is picking up. Specifically, the stochastic oscillator posted a bullish cross just shy of the 20-oversold mark, while the RSI ticked up beneath its 50-neutral mark.

If the bulls manage to push the price above the restrictive trendline that connects the recent peaks, immediate resistance could be met at 27,988, which is the 38.2% Fibonacci retracement of the 48,226-15,479 downtrend. Surpassing that zone, Bitcoin could ascend to challenge the 11-month high of 31,064. Further advances could then cease at the 50.0% Fibo of 31,852.

Alternatively, bearish actions could trigger a price retreat towards the recent 2½-month low of 25,350. Should that floor collapse, the spotlight could turn to the 23.6% Fibo of 23,207. Even lower, the 21,375 hurdle could provide downside protection.

Overall, BTCUSD has been trading sideways during the past week, but short-term oscillators are indicating that the bullish momentum is slowly intensifying. Thus, a clear break above the descending trendline is needed to revive bulls’ hopes for a trend reversal.

Gold Retains Sideways Move

Gold could not sustain its strength above the 1,965 bar on Tuesday, falling aggressively towards the 1,938 floor in the aftermath.

The previous metal switched to recovery mode on Wednesday, though the mixed technical signals in the four-hour chart provide no clear direction. Traders would like to see a close above the constraining falling line at 1,950 before they again turn their attention to the 1,965 barricade. Notably, the 23.6% Fibonacci retracement of the 2,079-1,932 downtrend is placed here too. If that wall collapses, the price may accelerate towards the 200-period simple moving average (SMA) and the 38.2% Fibonacci level of 1,987. Another bullish breakout there could clear the way towards the 2,000 psychological mark.

Failure to jump successfully above 1,950 may bring the 1,938 base back under the spotlight. If the bears exit the range below 1,930, the price may initially pause around the 1,900 number and then head towards the 1,887 region in order to meet the descending line from March 20.

In a nutshell, gold traders are in a wait-and-see mode. A significant move above 1,985 could brighten the short-term outlook, whilst a drop below 1,931 would re-activate May’s downfall.

Sunset Market Commentary

Markets

It’s Fed-day. And with the ECB following on Thursday and the Bank of Japan on Friday it might sound strange, but we’ve probably already faced the two key events for this week. First and foremost, the hot UK payrolls and wage inflation. They are a huge wake-up call for the hesitant Bank of England (BEHIND THE CURVE) and together with last week’s RBA and BoC hawkish rate hikes an omen on how the Indian summer in the US and Europe might look like. And trust us, El Nino won’t be the only one to blame. The second important event was the Chinese 7d reverse repo rate cut which probably heralds a cut in the key 1y MT lending facility rate tomorrow. Chinese monetary policy to save the local and help the global economy might eventually work… you guessed it… inflationary! We can be brief on today’s market moves. Core bonds and stocks gains some ground with the dollar suffering. Moves occur orderly. EUR/USD rises north of 1.0840. It’s probably a preview of what to expect after the Fed skips a meeting in its normalization cycle for the first time in 15 months tonight. After all, given the central bank data dependency it’s back to square one when it comes to the July meeting whatever current thinking/market pricing.

Fed preview: Yesterday’s more or less in-line CPI figures basically cemented the case for a skip in the tightening cycle. That said, we do expect the Fed to add a hawkish flavour because of - amongst others - ongoing economic resilience, especially in the labour market and stalling/insufficient progress in the core disinflationary process. The dot plot serves as the perfect tool for this. The updated version will include a higher terminal rate than the one in March (set back then at the current 5-5.25%). 2024 may also see a higher rate level than expected previously. We don’t expect chair Powell to sound outright hawkish in the press conference afterwards though. He’ll stick to a data-dependent approach instead. With another rate hike almost fully priced in for either July or September, we think the dollar’s room for appreciation against the euro is limited. We might even be getting some buy-the-rumour, sell-the-fact. The US yield rally lost some steam at key technical references, likely triggering rebound action lower. The downside should be protected by the higher-for-longer strategy though. Unless markets take a skip for a pause and the pause eventually for a pivot…

News & Views

Swedish inflation followed the Norwegian example of last week by beating most estimates. Headline inflation using a fixed interest rate (CPIF) rose 0.1% m/m vs. expectations for flatlining. The yearly figure fell sharply from 7.6% to 6.7%. That was bang in line with consensus and even lower than the 7.1% the Riksbank had projected in April. It is by no means a relief though, as core CPIF only eased from 8.4% to 8.2%. That topped both analyst (7.8%) and Riksbank (8.1%) forecasts. Sticky prices make the disinflationary process a painstakingly slow one. In addition, the Swedish krone since the April policy meeting weakened another 2%+, posing upside inflation risks. The central bank last time around hinted at one more 25 bps rate hike either on June 29 or September 21 with odds clearly in favour of the former. But today’s data and the weak SEK suggest that even the level reached then (3.75%) may not suffice. The Swedish krone quickly erased a kneejerk leg higher after the data. EUR/SEK is trading higher for the day around 11.56 even as swap yields in the country rise up to 5.4 bps at the front.

Slovakia’s prime minister Odor in an interview with Bloomberg said his country risks being punished by financial markets if it doesn’t take steps to cut spending. Slovakia is running a projected 6%+ deficit this year, the biggest in over a decade as well as the eurozone’s widest gap. Public debt is expected to hit 58.5% of GDP in 2023. This compares to the 48% in 2019, prior to the spending done to cushion the impact from the pandemic and the Russian war in Ukraine. The government also introduced measures to soften the cost-of-living crisis. Inflation peaked at a 23-year high of 15.4% in February before easing to a still lofty 11.9% in May, according to data published this morning. Odor and his caretaker administration in the runup to the September 30 elections will prepare a set of measures to address the matter. These include a shift to targeted state aid and social payments, higher taxes on consumption and abandoning various tax exceptions.

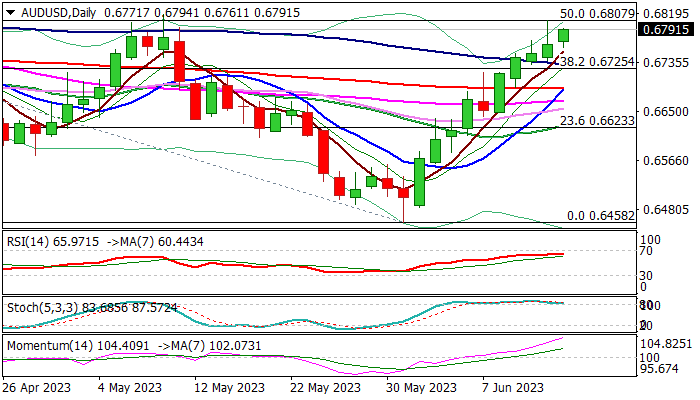

AUD/USD: Bulls Crack Pivotal Resistance Zone as Fed Expected to Stay on Hold

Australian dollar remains bid in Asia / early Europe on Wednesday, underpinned by weaker dollar and rise in Dalian iron ore.

Bulls cracked the lower boundary of strong resistance zone at 0.6807/18 (50% retracement of 0.7157/0.6458 / May 10 high) on Tuesday but was unable to break on the first attempt.

Daily studies are firmly bullish but overbought which may produce additional headwinds and make attempts through pivotal barriers more difficult, however, FOMC decision is likely to be key driver today.

The Fed is widely expected to pull the brake and keep interest rates unchanged for the first time in more than one year of aggressive policy tightening.

Market observers expect a pause in rate raising cycle but with hawkish rhetoric, while focus will be on central bank’s forward guidance, which is likely to determine greenback’s short-term fate.

Sustained break of 0.6807/18 pivots would open way for fresh extension towards 0.6890/0.6915 Fibo 61.8% / weekly cloud top).

Broken 100DMA and Fibo 38.2% offer initial supports at 0.6731/25, followed by converged 10/200DMA’s (0.6689) which are about to form a golden-cross.

Res: 0.6818; 0.6864; 0.6890; 0.6915.

Sup: 0.6761; 0.6725; 0.6689; 0.6668.

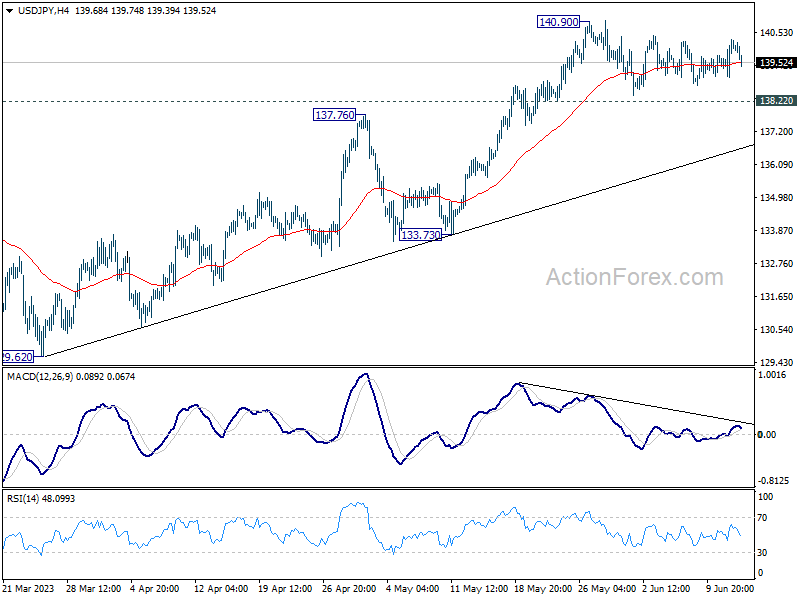

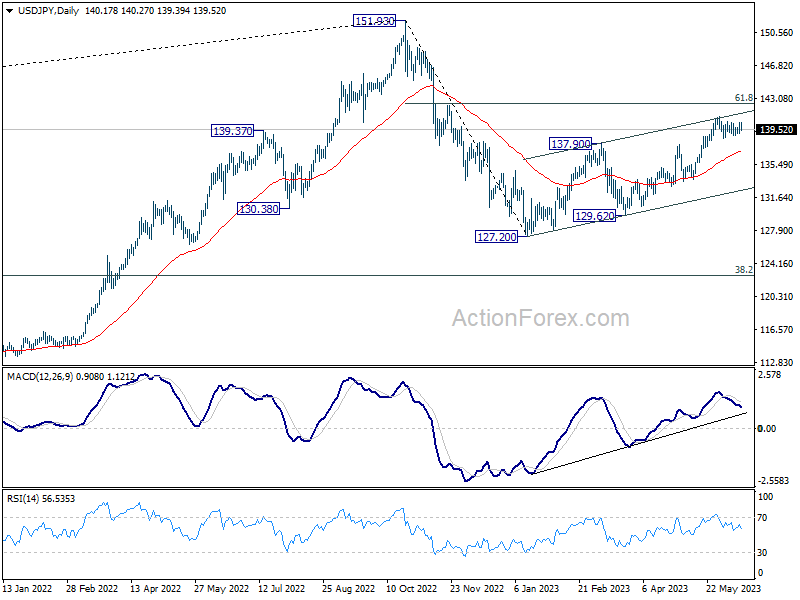

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 139.39; (P) 139.85; (R1) 140.69; More...

Range trading continues in USD/JPY and intraday bias stays neutral at this point. Further rally is expected as long as 138.22 minor support holds. On the upside, break of 140.90 will resume larger rise from 127.20 to 142.48 fibonacci level. However, considering bearish divergence condition in 4 hour MACD, break of 138.22 will confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 137.02).

In the bigger picture, rise from 127.20 is seen as the second leg of the corrective pattern from 151.93 high. Stronger rally would be seen to 61.8% retracement of 151.93 to 127.20 at 142.48. Sustained break there will pave the way back to retest 151.93. On the downside, however, break of 133.73 support will argue that the pattern could have started the third leg through 127.20 low.

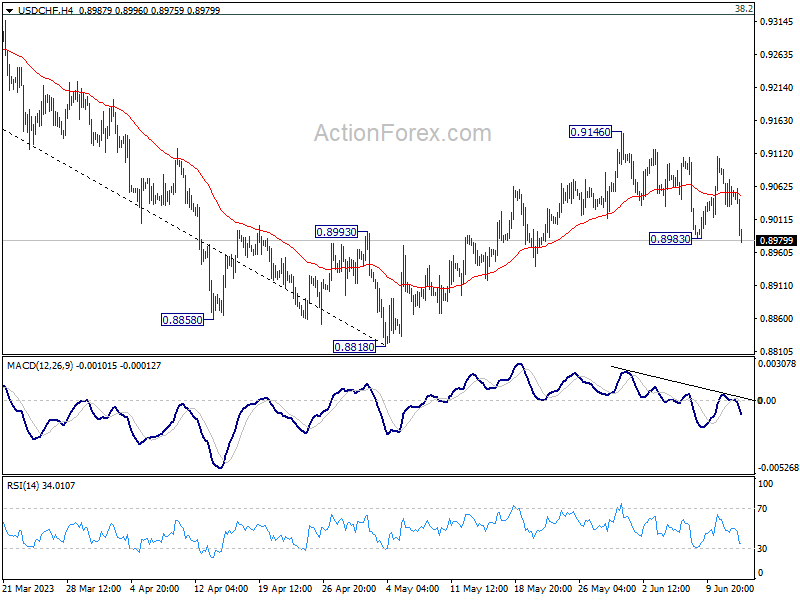

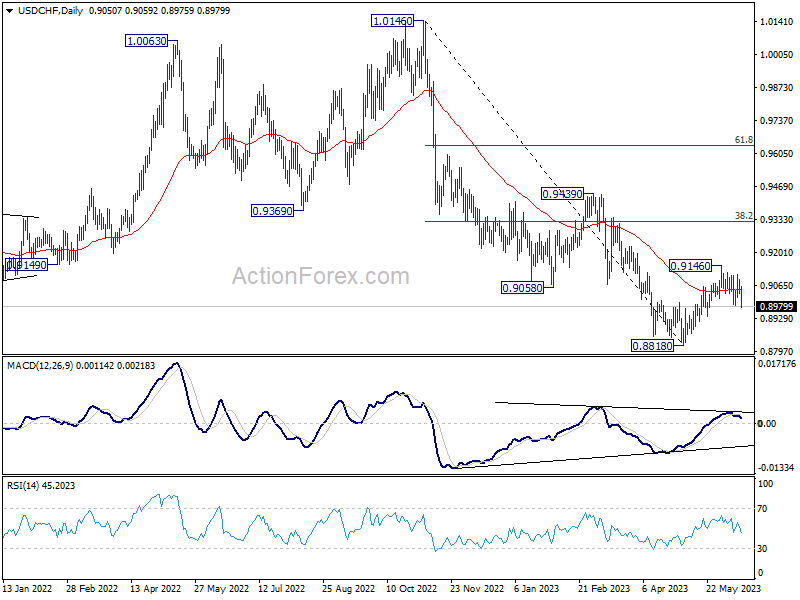

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9024; (P) 0.9059; (R1) 0.9087; More...

USD/CHF's break of 0.8983 support indicate resumes of fall from 0.9146. The development also revives that case that corrective rebound from 0.8818 has completed at 0.9146. Intraday bias is back on the downside for retesting 0.8818 low. For now, risk will stay on the downside as long as 0.9146 resistance holds.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high), which might have completed at 0.8818 already, just ahead of 0.8756 long term support. Sustained trading above 0.9058 support turned resistance should confirm medium term bottoming. Further break of 0.9439 resistance will confirm bullish trend reversal.

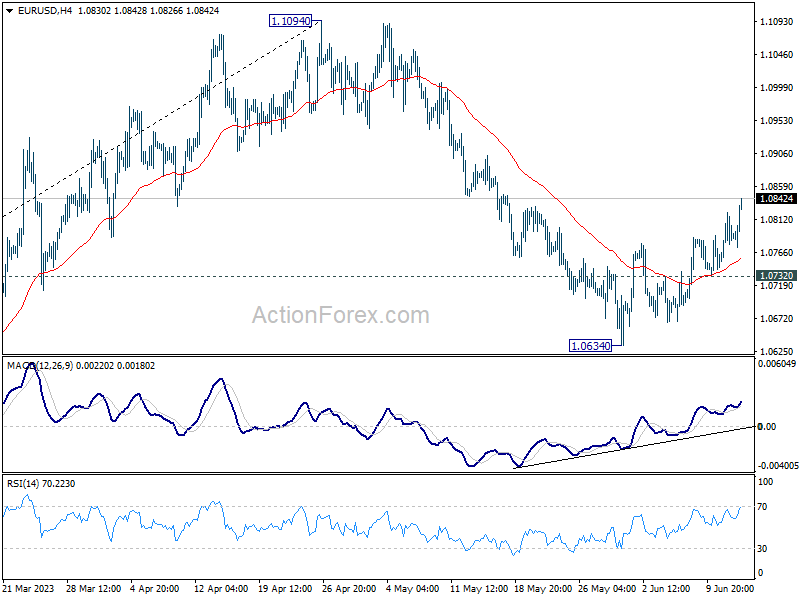

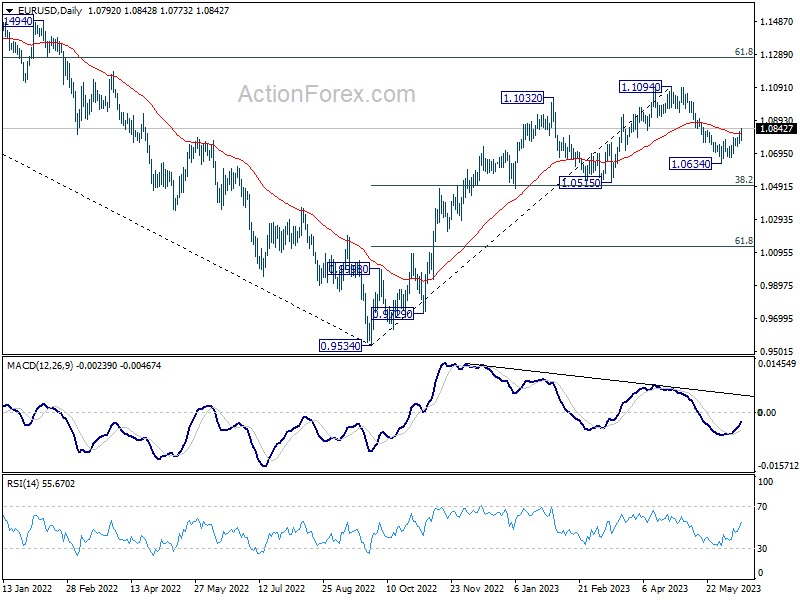

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0757; (P) 1.0790; (R1) 1.0827; More...

Intraday bias in EUR/USD stays on the upside at this point. Rebound from 1.0634 is still in progress. Sustained trading above 55 EMA (now at 1.0810) will pave the way back to retest 1.1094 high. Nevertheless, break of 1.0732 minor support should resume the fall from 1.1094 through 1.0634 support.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

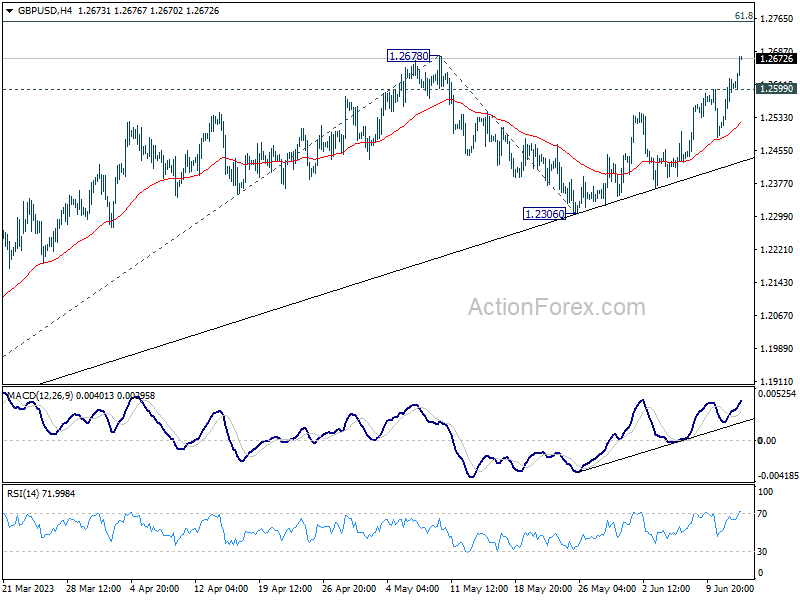

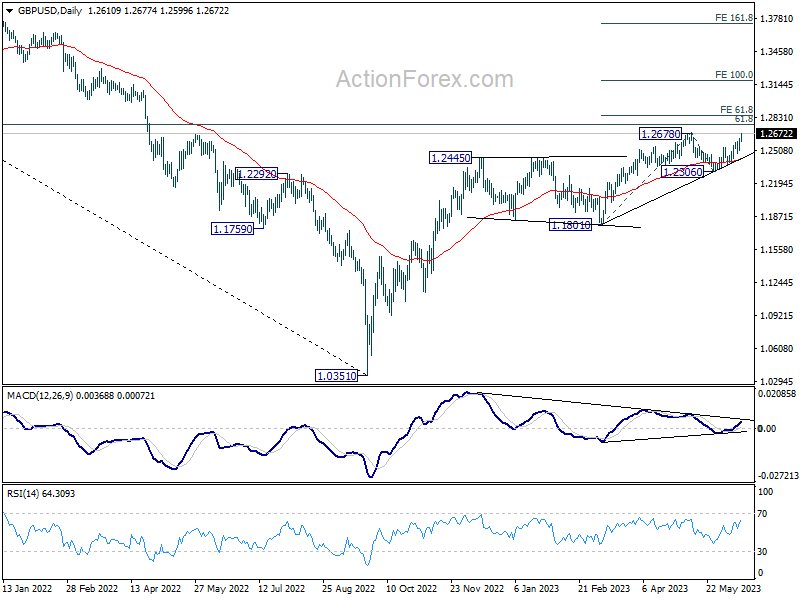

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2532; (P) 1.2579; (R1) 1.2657; More...

Intraday bias in GBP/USD remains on the upside with focus on 1.2678 resistance. Decisive break there will confirm resumption of whole up trend from 1.0351. Further rally should then be seen through 1.2759 fibonacci level to 61.8% projection of 1.1801 to 1.2678 from 1.2306 at 1.2848. On the downside, below 1.2599 minor support will turn intraday bias neutral first.

In the bigger picture, as long as 1.2306 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.2306 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.

Dollar Sell-Off Resumes after PPI; Spotlight Shifts to FOMC Hold

Dollar is facing renewed selling in early US session as data reveals a further slowdown in upstream inflation via PPI. All eyes are now on the much-anticipated FOMC rate decision where a 'hold' is broadly expected. However, the possibility of an upside surprise in both inflation projections and the dot plot remains, suggesting that we could be in for some choppy waters ahead.

Indeed, the overall market reaction could be multifaceted, especially when the equities and bond markets are added to the equation. So, market participants should buckle up for potential volatility.

In the meantime, Aussie and Kiwi dollars continue to flex their muscles, being the day's strongest performers. A noticeable rebound the Swiss Franc is also evident. British Pound isn't too far behind after GDP data matched expectations. Canadian dollar trails Dollar as the next weakest performer, followed by Euro and Yen.

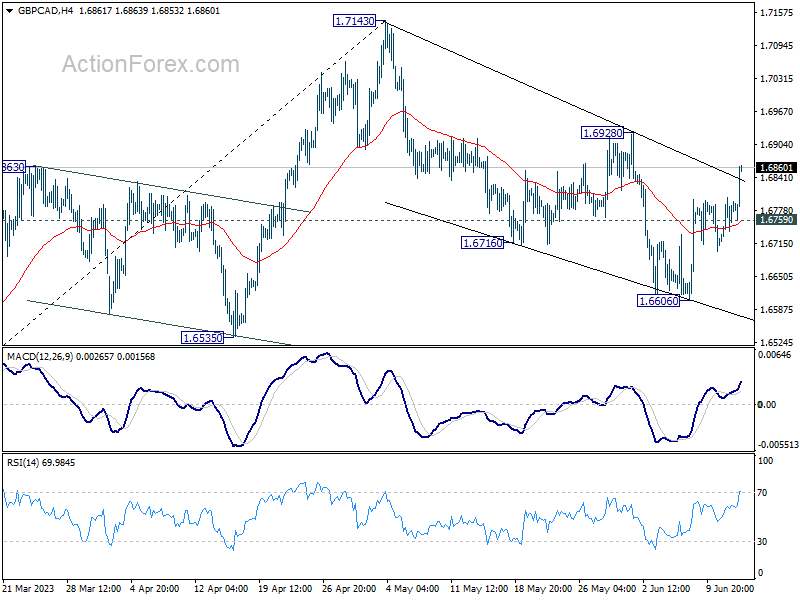

Technically, GBP/CAD's break of near term falling trend line today is taken as the first signal that whole correction from 1.7143 has completed with three waves down to 1.6606. Further rally is now expected as long as 1.6759 support holds. Firm break of 1.6928 will solidify the case of larger up trend resumption through 1.7143 high. Let's see if that will happen before BoE rate decision next week.

In Europe, at the time of writing, FTSE is up 0.38%. DAX is up 0.47%. CAC is up 0.74%. Germany 10-year yield is up 0.0140 at 2.439. Earlier in Asia, Nikkei rose 1.47%. Hong Kong HSI dropped -0.58%. China Shanghai SSE dropped -0.14%. Singapore Strait Times rose 0.90%. Japan 10-year JGB yield rose 0.0099 to 0.431.

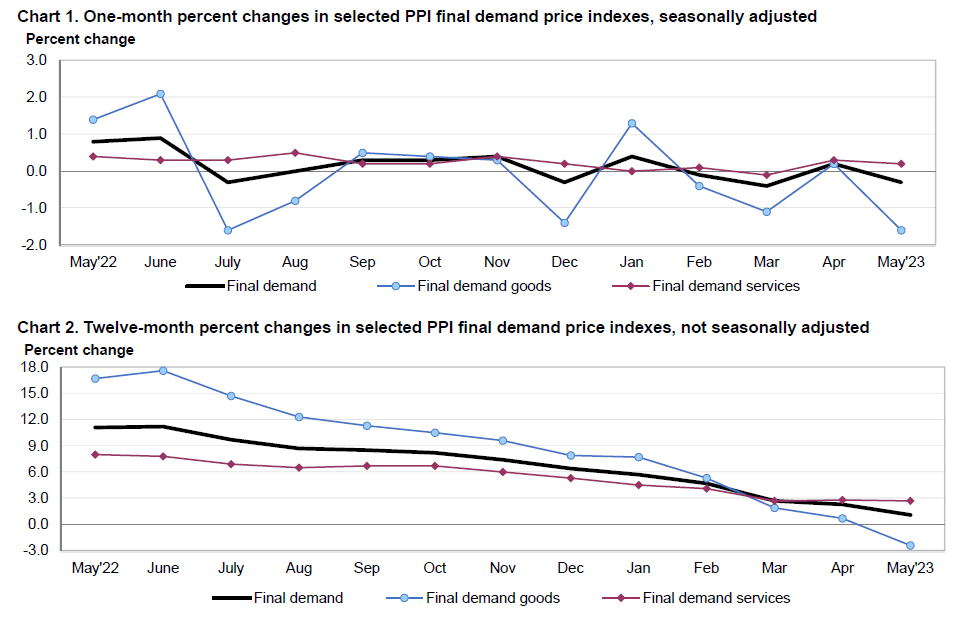

US PPI at -0.3% mom, 2.8% yoy in May

US PPI for final demand fell -0.3% mom in May, below expectation of -0.1% mom rise. PPI goods fell -1.6% mom while PPI services rose 0.2% mom. PPI less foods, energy, and trade services was flat mom.

For the 12 months ended in May, PPI slowed from 3.1% yoy to 2.8% yoy, below expectation of 2.9% yoy. PPI for less foods, energy, and trade services slowed from 3.3% yoy to 2.8% yoy.

UK GDP grew 0.2% mom in Apr led by 0.3% growth in services

UK GDP grew 0.2% mom in April, matched expectations. Services rose 0.3% mom. Production declined by -0.3% mom. Construction fell -0.6% mom. In the three months to April, GDP grew 0.1%, compared with the three months to January 2023, with falls in 8 of the 14 sub-sectors.

Also released, industrial production fell -0.3% mom, -1.9% yoy in April, versus expectation of -0.1% mom, -2.6% yoy. Manufacturing production declined -0.3% mom, -0.9% yoy, versus expectation of -0.1% mom, -1.8% yoy. Goods trade deficit narrowed from GBP -16.4B to GBP -15.0B, versus expectation of GBP -16.5B.

NIESR forecasts anemic UK growth amid BoE rate hikes

NIESR projects that UK monthly GDP will "remain flat" in May compared to April. The institute added "Higher-frequency data suggest that continued growth in services in May be partially offset by a further decline in manufacturing activity."

For the second quarter, NIESR anticipates a rather lukewarm GDP growth of merely 0.1%, a pace that "broadly consistent with the longer-term trend of low economic growth".

Paula Bejarano Carbo, Associate Economist, NIESR, noted, "With the Bank Rate set to rise further over the coming months, curbing demand, it is likely that UK growth will continue to be anaemic at best."

Eurozone industrial production rose 1.0% mom, EU up 0.7% mom

Eurozone industrial production rose 1.0% mom in April, below expectation of 1.2% mom. Production of capital goods grew by 14.7% mom and energy by 1.0% mom, while production of intermediate goods fell by -1.0% mom, durable consumer goods by -2.6% mom and non-durable consumer goods by -3.0% mom.

EU industrial production rose 0.7% mom. Among Member States for which data are available, the highest monthly increases were registered in Ireland (+21.5%), Lithuania (+2.8%) and Sweden (+1.4%). The largest decreases were observed in Slovenia (-7.9%), Portugal (-5.5%) and the Netherlands (-3.5%).

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2532; (P) 1.2579; (R1) 1.2657; More...

Intraday bias in GBP/USD remains on the upside with focus on 1.2678 resistance. Decisive break there will confirm resumption of whole up trend from 1.0351. Further rally should then be seen through 1.2759 fibonacci level to 61.8% projection of 1.1801 to 1.2678 from 1.2306 at 1.2848. On the downside, below 1.2599 minor support will turn intraday bias neutral first.

In the bigger picture, as long as 1.2306 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.2306 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Current Account Q1 | -5.22B | -6.95B | -9.46B | |

| 06:00 | GBP | GDP M/M Apr | 0.20% | 0.20% | -0.30% | |

| 06:00 | GBP | Industrial Production M/M Apr | -0.30% | -0.10% | 0.70% | |

| 06:00 | GBP | Industrial Production Y/Y Apr | -1.90% | -2.60% | -2.00% | |

| 06:00 | GBP | Manufacturing Production M/M Apr | -0.30% | -0.10% | 0.70% | |

| 06:00 | GBP | Manufacturing Production Y/Y Apr | -0.90% | -1.80% | -1.30% | |

| 06:00 | GBP | Goods Trade Balance (GBP) Apr | -15.0B | -16.5B | -16.4B | |

| 09:00 | EUR | Eurozone Industrial Production M/M Apr | 1.00% | 1.20% | -4.10% | |

| 12:30 | USD | PPI M/M May | -0.30% | -0.10% | 0.20% | |

| 12:30 | USD | PPI Y/Y May | 1.10% | 1.50% | 2.30% | |

| 12:30 | USD | PPI Core M/M May | 0.20% | 0.20% | 0.20% | |

| 12:30 | USD | PPI Core Y/Y May | 2.80% | 2.90% | 3.20% | 3.10% |

| 14:30 | USD | Crude Oil Inventories | -1.3M | -0.5M | ||

| 18:00 | USD | Fed Interest Rate Decision | 5.25% | 5.25% | ||

| 18:30 | USD | FOMC Press Conference |

US PPI at -0.3% mom, 2.8% yoy in May

US PPI for final demand fell -0.3% mom in May, below expectation of -0.1% mom rise. PPI goods fell -1.6% mom while PPI services rose 0.2% mom. PPI less foods, energy, and trade services was flat mom.

For the 12 months ended in May, PPI slowed from 3.1% yoy to 2.8% yoy, below expectation of 2.9% yoy. PPI for less foods, energy, and trade services slowed from 3.3% yoy to 2.8% yoy.