Sample Category Title

Fed Jefferson: A pause in June doesn’t mean rates have peaked

Comments from top officials from Fed suggested a pause in interest rate hikes in June while possible, shouldn't be misinterpreted as a sign that peak rates for the cycle have been reached.

Fed Governor, Philip Jefferson, clarified, "A decision to hold our policy rate constant at a coming meeting should not be interpreted to mean that we have reached the peak rate for this cycle."

Jefferson, suggested that skipping a rate hike at an upcoming meeting would provide an opportunity for the committee to review more data before deciding on the extent of any further policy tightening.

Philadelphia Fed President, Patrick Harker, echoed this sentiment, albeit with a more forceful argument for the need to 'skip' rather than 'pause'. "I am in a camp increasingly coming into this meeting of thinking that we really should skip, not pause," he remarked.

Harker believes the current policy is nearing, if not already at, a restrictive level and suggests a period of careful reflection before further action is taken.

Harker added, "I think we have to be ready that we might have to do more and I'm fully aware we have to do that and willing to do that, but I want to give it a little bit of time."

BoE Mann: Inflation gap in the UK more persistent than others

BoE policymaker, Catherine Mann, has highlighted the unique and mounting inflation problem that Britain is facing in comparison to the United States and the Eurozone.

Mann pointed to both large-scale price increases and the rising persistence of these underlying pressures as causes for concern. She emphasized, "The gap (between headline and core CPI) that I have in my country is more persistent than the gaps that we see in either of my neighbours, the U.S. or the euro area."

The gap she refers to is the disparity between headline inflation (which includes volatile commodities like food and energy) and core inflation (which excludes these commodities).

Notably, Mann underscored the role of British businesses and increased wages in maintaining high core inflation. She explains that businesses in the UK have been successful in passing on price rises, contributing to this persistent inflation gap. This, coupled with increased wages, suggests that headline inflation has been slower to recede towards the core rate than it has in other regions.

"There is a gap between the headline, which is incorporating energy which went up really high and now has come down, and core where we do start to see the implications coming through pricing channels, through wage negotiations, into something that is persistent," Mann explained.

SNB Jordan: We don’t see a big risk in over-tightening monetary policy

SNB Chairman Thomas Jordan recently warned yesterday that the more inflation is entrenched in the perception of companies and households, the harder it is to bring it down. He highlighted the urgency of the situation, stating, "We have to bring it back below 2% as soon as possible."

Discussing the bank's approach towards interest rates, Jordan assured that Switzerland's are "still very low". "We don't see a big risk in over-tightening monetary policy. It is not something that will damage financial stability in general in Switzerland," he affirmed.

Regarding the financial stability issues surrounding Credit Suisse, Jordan clarified that it was an individual case where the problem was not interest rates, but rather a "lack of trust of market participants in an institution."

Looking ahead, market expectations suggest a 25bps rise from the current 1.5% level when the central bank delivers its next assessment in June.

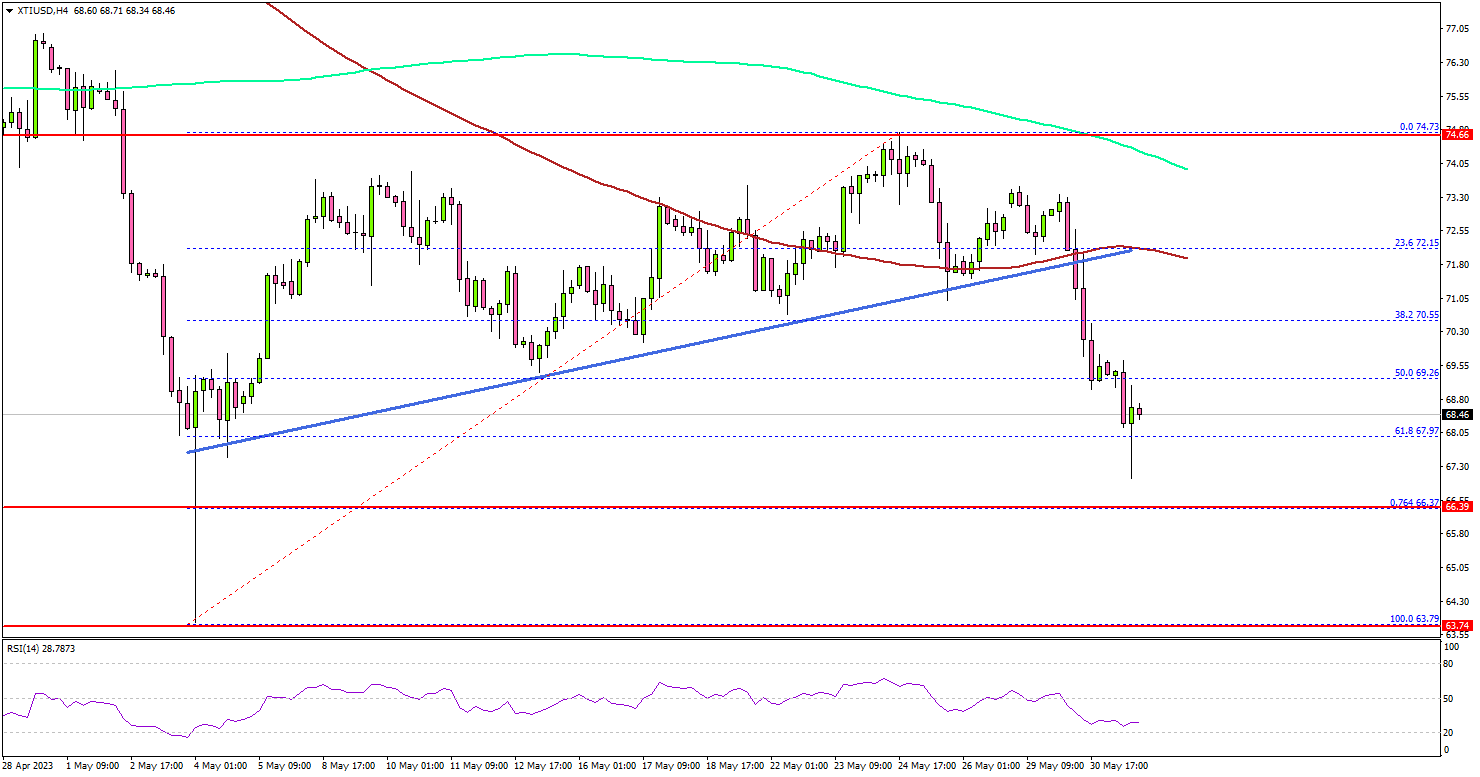

Crude Oil Price Dives Below $70, US ADP Employment Report Next

Key Highlights

- Crude oil price started a fresh decline below the $72 support.

- It traded below a key bullish trend line with support near $71.80 on the 4-hour chart.

- EUR/USD is still at risk of a move toward 1.0620.

- The US ADP employment could change by 170K in May 2023, down from 296K.

Crude Oil Price Technical Analysis

Crude oil price struggled to clear the $75 resistance against the US Dollar. The price started a fresh decline and traded below the key $72 support.

Looking at the 4-hour chart of XTI/USD, the price traded below a key bullish trend line with support near $71.80. There was a close below the $70 support, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour).

The price spiked below the 61.8% Fib retracement level of the upward move from the $63.79 swing low to the $74.73 high. On the downside, initial support is near the $66.40 level.

The next major support sits near the $65.00 level. Any more losses might call for a test of the $62.00 support zone in the coming days.

On the upside, the first major resistance is near the $70.50 level. The next key resistance is near $72.00 and the 100 simple moving average (red, 4-hour), above which the price may perhaps accelerate higher.

Looking at EUR/USD, the pair is moving lower and there is now a risk of a downside break below the 1.0620 support zone.

Economic Releases to Watch Today

- US Initial Jobless Claims - Forecast 235K, versus 229K previous.

- US ISM Manufacturing Index for May 2023 – Forecast 47.0, versus 47.1 previous.

- US ADP Employment Change for May 2023 - Forecast 170K, versus 296K previous.

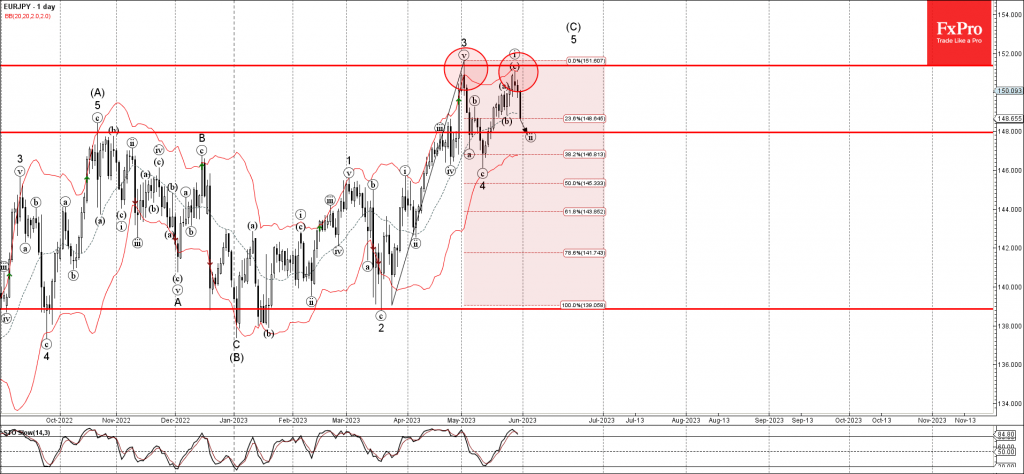

EURJPY Wave Analysis

- EURJPY reversed from resistance level 151.35

- Likely to fall to support level 148.00

EURJPY currency pair recently reversed down with the daily Shooting Star from the key resistance level 151.35 (top of the previous minor impulse wave 3 from the start of May).

The downward reversal from the resistance level 151.35 started the active short-term correction (ii), which belongs to the higher impulse waves 5 and (C).

Given the still overbought daily Stochastic , EURJPY can be expected to fall toward the next support level 148.00, target price for the completion of the active correction (ii).

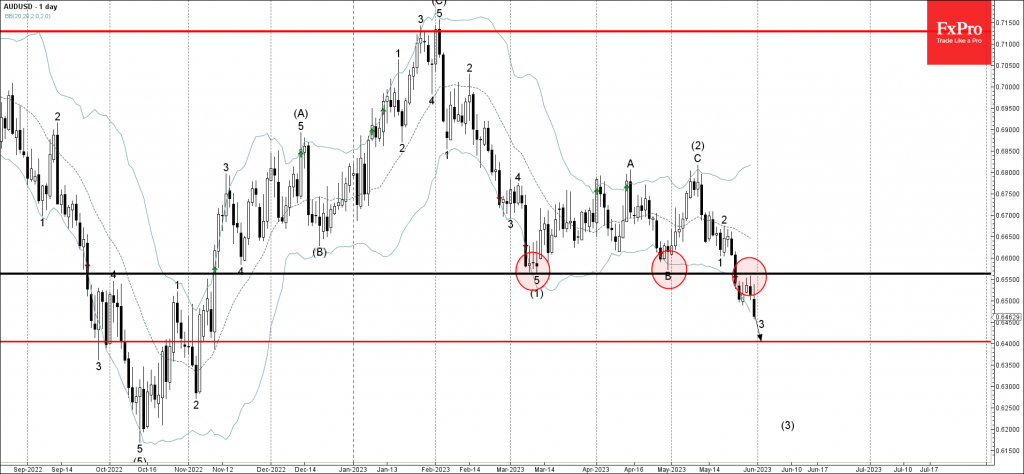

AUDUSD Wave Analysis

- AUDUSD reversed from resistance level 0.6565

- Likely to fall to support level 0.6400

AUDUSD currency pair recently reversed down from the key resistance level 0.6565 (former strong support from March and April, acting as the resistance after it was broken).

The downward reversal from the resistance level 0.6565 continues the impulse wave 3 of the intermediate downward impulse sequence (3) from the start of May.

AUDUSD can be expected to fall further toward the next support level 0.6400, target price for the completion of the active impulse wave 3.

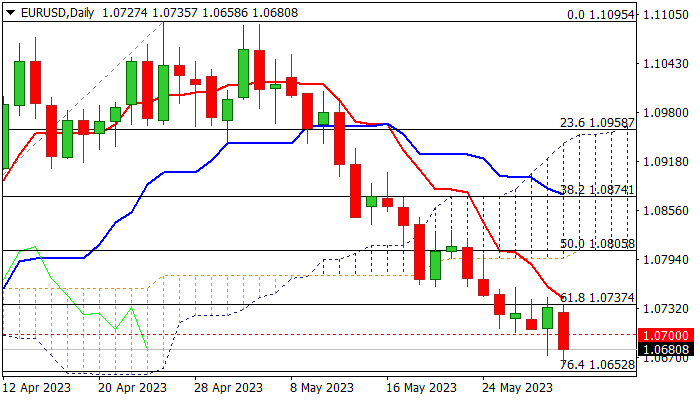

EUR/USD: Firm Break of Psychological 1.07 Support to Open Way for Further Weakness

The Euro came under renewed pressure and fell to new nine-week low on Wednesday, bringing larger bears back to play after brief consolidation above 1.07 support.

Fresh weakness so far shapes Wednesday’s action in large bearish candle, which is on track to offset initial reversal signal on Monday’s inverted hammer and Tuesday’s bullish candle, along with false break below 1.07.

Today’s close below 1.07 level would add to fresh signals of bearish continuation, with violation of nearby Fibo support at 1.0652 (76.4% of 1.0516/1.1095) to open way for possible full retracement of 1.0516/1.1095 rally.

Bearish daily studies contribute to negative near-term outlook, though caution is still required, as repeated failure to register close below 1.07 mark would signal prolonged consolidation.

Immediate bears are expected to remain fully in play while falling daily Tenkan-sen (1.0744) caps, while break higher would ease downside pressure and open door for bounce towards strong barrier at 1.0805 (base of thick daily Ichimoku cloud).

Res: 1.0700; 1.0744; 1.0759; 1.0805.

Sup: 1.0652; 1.0631; 1.0600; 1.0551.

Sunset Market Commentary

Markets

Core bonds extended this week’s gains during European trading hours as the data drum echoed yesterday’s sound. Additionally, risk sentiment soured following dismal Chinese figures this morning. French inflation fell by 0.1% M/M in May (vs 0.3% consensus) with the Y/Y-figure come down from 6.9% to 6% (vs 6.4% expected). As was the case in yesterday’s Spanish and Belgian figures, energy prices were the main culprit though the inflation decline was more broad-based. German regional data soon pointed to a similar story with M/M inflation effectively down 0.2% and the Y/Y figure sliding more than expected from 7.6% to 6.3%. Again, energy inflation was the prime driver of this decline. Italian inflation, rising by 0.3% M/M and falling less than expected from 8.7% Y/Y to 8.1% was today’s exception to the rule. Data suggest downside risks for EMU headline inflation tomorrow, though the jury remains out on the core issue. They nevertheless don’t question the ECB’s drive to hike policy rates by another 25 bps mid-June while sticking to their hawkish guidance. The intraday bond rally grinded to a halt in the run-up to US trading. We don’t draw any firm conclusions yet though with monthly JOLTS job openings still to be released. We retain comments by Fed Bowman who said that “the residential real estate market appears to be rebounding, with home price leveling out recently, which has implications for our fight to lower inflation”. Earlier today, Cleveland Fed Mester in an interview with the FT argued in favour of another 25 bps rate hike at the June FOMC meeting. Changes on the US yield curve currently range between -3.8 bps (2-yr) and +0.3 bps (30-yr). German Bunds outperform with yield changes varying between -5.7 bps (5-yr) and -2 bps. In the sovereign scope, the Slovak Republic mandated banks to launch a new 10y benchmark in the near future (likely tomorrow). Existing trends in major FX crosses weren’t questioned with EUR/USD losing 1.07 on the combination of EMU CPI and risk aversion. EUR/GBP copied the move south in EUR/USD, testing yesterday’s low around 0.8630. In smaller currencies, the Turkish lira is the standout loser (EUR/TRY>22) while Scandinavian currencies try to fight back after recently setting multi-annual lows.

News & Views

The ECB published its semi-annual financial stability report today. Among the key findings are that uncertain growth prospects, persistent inflation and tightening financing conditions continue to weigh on the balance sheets of (especially debt-laden) firms, households and governments. Sector wise, the ECB singled out the real estate market with a particular focus on commercial property. House prices have cooled considerably though orderly. That could turn disorderly, however, if higher mortgage rates increasingly reduce demand. The ECB said that financial markets remain vulnerable to asset price adjustments. “Stretched valuations, tighter financing conditions and lower market liquidity might increase the risk of any adjustment becoming disorderly, particularly in the event of renewed recession fears.” The ECB also found that euro area banks proved resilient to stresses in the US and Swiss banks, thanks to strong capital and liquidity positions. It added that it is essential to preserve this resilience.

Polish prices stabilized in May. The 0.0% m/m outcome undershot a 0.3% estimate, delivering a downside y/y surprise as well: 13% vs 13.4% expected, coming from 14.7% in April. Fuel prices and utilities (electricity, gas & other) exerted a strong downward force with monthly declines of 4.8% and 0.5% respectively. Excluding this suggests that core inflation (to be released June 16) might be much more sticky. KBC Economics estimates it to be above 11% y/y, from 12.2% in April, leaving the central bank in the country no room to cut rates (6.75% today) anytime soon. NBP’s Kotecki, one of the few hawks in the monetary policy committee, in an interview on Monday said rates might not be slashed this year and even the next. Other members, including Maslowska, are using the recent zloty appreciation as an argument to bring forward a rate cut. The NBP governor Glapinski has repeatedly expressed hope for a first move by the end of the year. The Polish zloty today trades unchanged around EUR/PLN 4.53. In a broader perspective, the zloty appreciation recently hit strong resistance around EUR/PLN 4.50.

Canada’s GDP Rebounds in First Quarter of 2023

The Canadian economy expanded by 3.1% quarter/quarter annualized (q/q) in 2023 Q1. Furthermore, the flash estimate for April showed a 0.2% month-on-month increase.

Consumer spending drove the first quarter gains, up 5.7% q/q. This was led by spending on durable goods, including "new trucks, vans, and sport utility vehicles". Spending on services also rose, led by Canadians' desire to go out to dinner and bars.

Exports also rose by 10.1% q/q, led by sales of "passenger cars and light trucks, unwrought gold, silver, and platinum group metals and their alloys, other crop products, and wheat." At the same time, imports were flat at 0.9% q/q, as increases in oil imports "were largely offset by declines in imports of passenger cars and light trucks, unwrought gold, silver, and platinum group metals and their alloys, and clothing, footwear, and accessories."

Investment was a drag once again, as housing investment (-14.6% q/q) led the decline. Statcan noted that the "decline in investment was widespread—as new construction (-6.0%), renovations (-2.1%), and ownership transfer costs (-1.5%), which represents resale activity, were all down. The decline in new construction was observed in every province and territory except Yukon."

The incomes of Canadians also rose, as employee compensation rose 7.2% q/q – "the largest quarterly growth in compensation of employees since the second quarter of 2022." This was driven by higher wages and employment gains over the quarter. The savings rate hit 2.9%, down from 5.8% in 2022 Q4.

Key Implications

Canada's economy bounced back in a meaningful way in the first quarter of 2023. Growth was driven by an acceleration in consumer spending, supported by a record-breaking increase in employment during the first quarter and wage growth that now outpaces inflation. This labour market strength enabled final domestic demand to surge by 2.6% q/q, well above the trend rate of growth. The encouraging flash estimate for April GDP points to less of a deceleration heading into the second quarter than previously expected, with 2023 Q2 now tracking around 1% q/q.

The Bank of Canada's (BoC) next interest rate decision is next week, and while today's report might not force a move off the sidelines, it may be used as rationale for a hike later this summer. Thus far, the BoC's rhetoric has focused on its expectation for a quick deceleration in economic growth over the remainder of the year. That slowdown still seems likely, but if the data keep coming in hot, the BoC may be compelled to move once again.