Sample Category Title

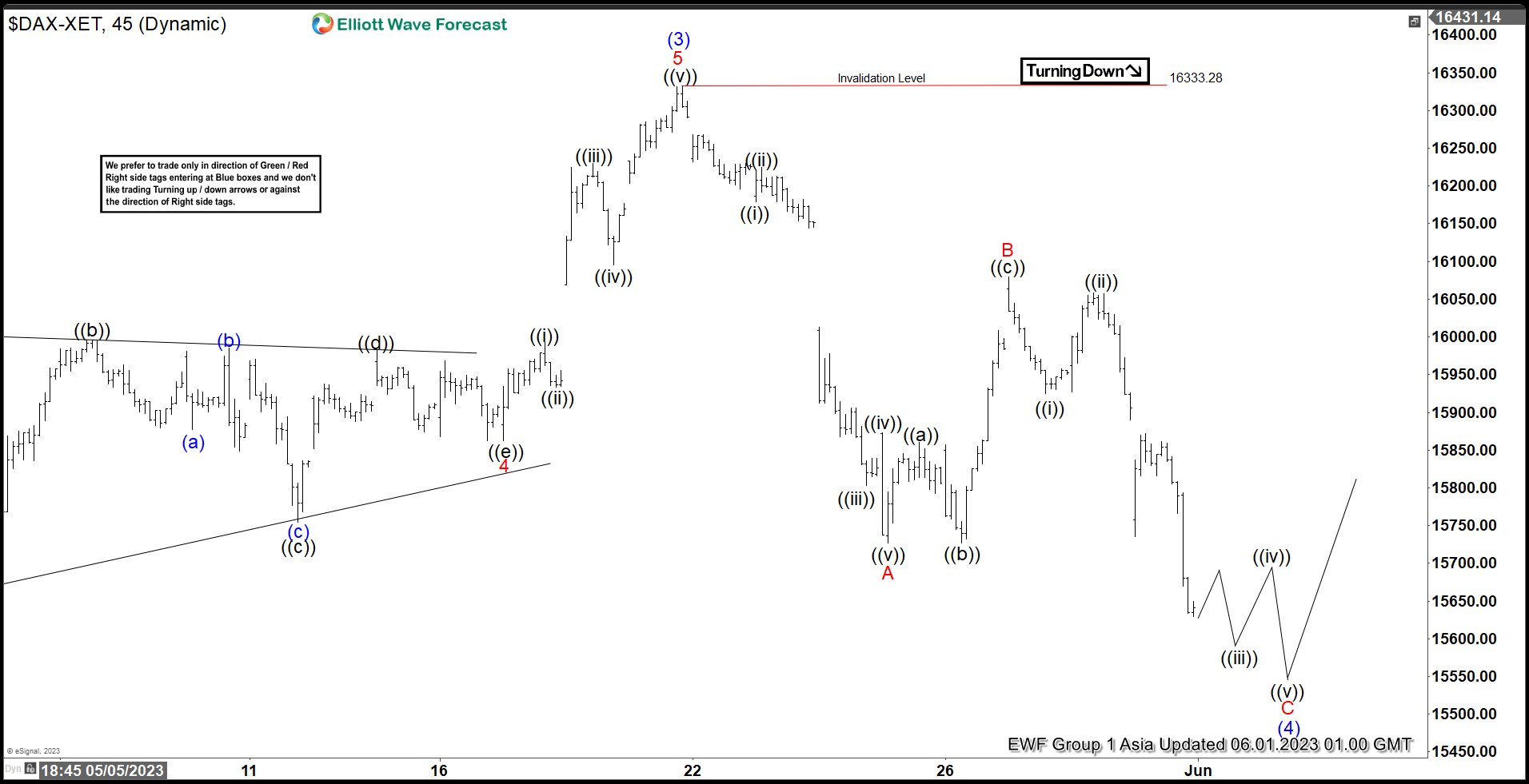

Elliott Wave View: DAX Pullback in Progress

Short term Elliott Wave View in DAX shows that the Index ended wave (3) at 16333.28. It is now pulling back in wave (4). Internal subdivision of the pullback is unfolding as a zigzag Elliott Wave structure. Down from wave (3), wave ((i)) ended at 16179.14 and rally in wave ((ii)) ended at 16224.32. Index then resumes lower in wave ((iii)) towards 15802.86 and rally in wave ((iv)) ended at 15872.60. Final leg wave ((v)) ended at 15726.5 which completed wave A.

Index then did a corrective wave B rally which unfolded as another zigzag in lesser degree. Up from wave A, wave ((a)) ended at 15860.37 and pullback in wave ((b)) ended at 15726.74. Index then rallied higher in wave ((c)) towards 16079.73. This completed wave B. Index then resumes lower in wave C with internal subdivision as 5 waves. Down from wave B, wave ((i)) ended at 15925.22 and wave ((ii)) rally ended at 16058.43. Expect Index to extend lower within wave ((iii)), then rally in wave ((iv)) followed by another leg lower in wave ((v)). This should complete wave C and (4). Potential target lower is 100% – 161.8% Fibonacci extension of wave A which comes at 15103.6 – 15476.8. Near term, as far as pivot at 16333.28 high stays intact, expect rally to fail in 3, 7, or 11 swing for further downside.

DAX 45 Minutes Elliott Wave Chart

DAX Elliott Wave Video

https://www.youtube.com/watch?v=5i4WN4c4DUI

USD Consolidates Gains

EUR/USD drifts lower

The US dollar stays firm on bets of more interest rate hikes to come amid repeatedly hawkish Fed remarks. Rebounds have been limited so far which means that the bears still have full control of the direction. A slip below the immediate support of 1.0680 has renewed the selling pressure. With the RSI bouncing back into the neutral area, 1.0635 is the latest support to see buyers’ reaction. Stiff selling could be expected by trend-followers around 1.0745 and the bulls must clear this level first to turn the odds in their favour.

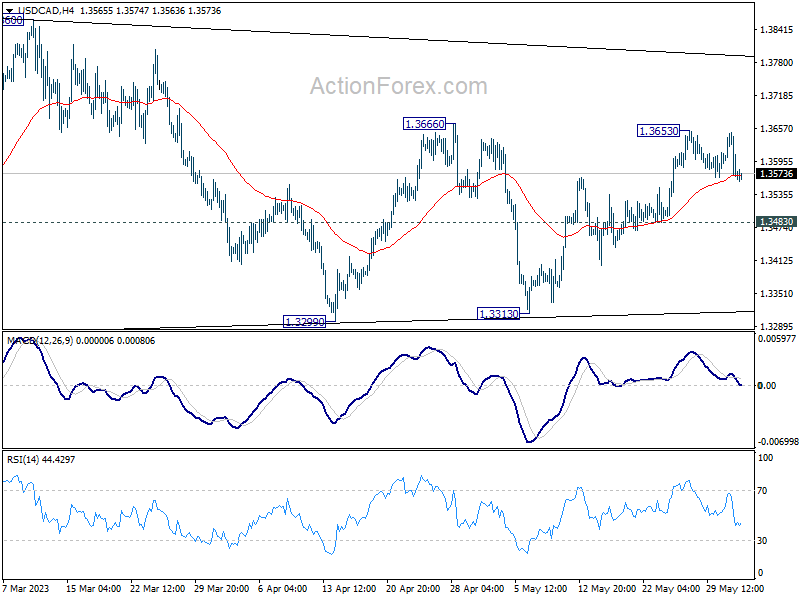

USD/CAD breaks support

The Canadian dollar clawed back losses over a strong GDP reading in Q1. Clearing the resistance of 1.3640 from early May has helped the recovery gain traction. After a bit of hesitation, the greenback had seemingly found support over 1.3570 only to see its advance capped by the recent high of 1.3650. A correction would expose 1.3500 next to the 30-day SMA which is a key floor to maintain the upward bias, and its breach may trigger a drop back to the daily demand zone around 1.3300. 1.3580 as a fresh hurdle in case of a bounce.

US Oil under renewed pressure

WTI crude slumps as weak Chinese manufacturing data fuel demand fears. The recent recovery has come to a halt at the 30-day SMA (74.50) and a two-leg sell-off below 72.00 and 70.00 was a sign of liquidation. Now that the bulls’ have thrown in the towel, the oil price could be vulnerable to a bearish continuation. As the RSI sinks into oversold territory, the swing low of 66.00 on the daily chart might be buyers’ last stand and its breach could open the door to 60.00. The psychological level of 70.00 has turned into a fresh resistance.

US and Taiwan Set to Sign the First Deal Under a New Trade Talks Framework

Markets

Core bonds enjoyed another solid bid yesterday, further unwinding ‘hawkish sentiment’ that reigned since mid-May. Chinese inspired risk-off and softer than expected national CPI data from Germany (HICP 6.3% Y/Y from 7.6%) and France (6.0% from 6.9M%) supported the move. Italian inflation (8.1% from 8.7%, but 7.5% expected) didn’t suffice for bond investors to change tactics. That said, German/European yields already reached intra-day lows early in the session, settling in a sideways pattern later. In the end, German yields lost between 3.8 bps (30-y) and 7.8 bps (5-y). US yields joined the broad bond market rebound, but the intraday pattern was a bit more choppy. Eco data were mixed with an awful Chicago PMI (40.4 from 48.6) and an unexpected rise in US April job openings (10 103k vs 9400k expected). While seen as important input for the Fed, JOLTS didn’t stop the decline in yields. Fed speak was at least partially to blame. Fed’s Harker and Jefferson both supported the idea of a Fed pause/skip in the rate hike cycle to assess incoming data before deciding about the extent of further policy firming. Market expectations on a June Fed hike dropped below 50%. US yields declined between 5.2 bps (5-y) and 2.9 bps (30-y). The Fed Beige book showed anecdotical evidence of employment and price growth slowing. The risk-off initially supported further USD gains but the US currency returned most of them late in US dealings (DXY 104.33, USD/JPY 139.34 from 139.79). The euro still underperformed (EUR/USD 1.0689). Sterling maintained its recent momentum (EUR/GBP 0.8592) even as UK yields corrected more than was the case in the US and Europe. US equities lost between 0.41% (Dow) and 0.63% (Nasdaq). Oil at first looked like going for a test of the YTD lows, but found a bottom intraday with brent closing at $72.66/b.

Asian risk sentiment this morning turned positive with China and Japan gaining about 0.5%-1%. US yields trend 3-4 bps higher. The dollar gains, albeit modestly. Today’s calendar is well filled with the Flash EMU May CPI, US ADP employment change, weekly jobless claims and manufacturing ISM. EMU headline inflation is expected to ease from 7% to 6.3% with downside risks after this week’s national data. However, the focus will be on the core measure (expected at 5.5% from 5.6%). After this weeks correction in yields, a big negative surprise is needed to support further gains in European bonds. 2.17%/2.2% remains tough support for the German 10-y yield (currently 2.28%). Soft US data could fuel expectations for a Fed pause in June after yesterday’s ‘Fed-guidance’. A Fed wait-and-see approach combined with a better risk sentiment could in theory cap further USD gains. However no obvious support is currently in sight, especially in the EUR/USD cross rate. Also keep an eye at the EUR/GBP cross rate. Sub 0.86, probably quite some good news is discounted for sterling. Key support comes in at 0.8547 (Dec low).

News Headlines

The Hungarian central bank posted a record HUF 402bn loss for 2022, it said in its annual report. That’s up from HUF 57bn the year before. The main drag came from net interest income (HUF 1.06tn in the red) following a soaring policy rate to fight the EU’s highest inflation and other measures to mop up excess liquidity. The MNB brought the reference (base) rate to 13% before introducing an emergency policy rate of 18% (recently lowered to 17%). A weaker forint compensated the huge net interest losses through a HUF 798bn foreign currency gain. MNB equity as a result of the losses tanked to HUF 256bn and is poised to turn negative in 2023 as high interest rates still bite. This would have put the Hungarian government and its already-strained budget under additional stress were it not for the law change last year. It then extended the period during which the government must compensate/recapitalize the central bank from eight days to five years.

The US and Taiwan are set to sign the first deal under a new trade talks framework today. The so-called US-Taiwan Initiative on 21st Century Trade was founded after Washington excluded Taiwan from its larger pan-Asian Indo-Pacific Economic Framework. Aimed at boosting ties between the two amid heightened tensions with China, the deal today covers customs and border procedures, regulatory practices and other small business. After that, negotiations start on other more complex areas such as agriculture, digital trade, labour and environmental standards. Beijing has denounced the trade talks..

Fed to Hop?

The US dollar gained, and the euro fell yesterday, after data from the Eurozone countries showed a faster-than-expected easing in inflation, while the job openings data from the US hinted, yet again, at further resilience in the US jobs market.

Falling EZ inflation

Inflation in France fell from 6.9% to 6% in May, versus 6.4% expected by analysts. That was a nice beat. The French producer price inflation fell more than 5% over the same month, mostly thanks to the falling energy prices. Inflation in Germany fell from 7.6% to 6.3%, defying an uptick to 7.8% expected by analysts. Inflation in Italy eased as well, though not as much as analysts expected. The Eurozone’s aggregate inflation data is due this morning, with a chance of beating analysts’ expectations to the downside, maybe below 7%. This would be good news for softening the ECB rate hike expectations, but 7% is still more than twice the ECB’s policy target of 2% and will certainly not derail the ECB from its trajectory of at least two more rate hikes, if not three.

Fed to hop?

Across the Atlantic Ocean, the JOLTS data came in to support the Federal Reserve (Fed) hawks, yesterday. The US job opening made an unexpected U-turn in April and stepped back above the 10 million mark. Today, the ADP report is expected to reveal around 170K new private job additions in the US in May. But the negative surprises on the ADP front barely led to negative surprises in NFP print over the past months. Therefore, the chances are that we will continue seeing the Fed hawks fly low before Friday’s jobs data.

As a result of softer European inflation and stronger US job openings data, the EURUSD fell as low as 1.0635 yesterday, and the yield spread between the German and US 10-year bonds fell to the lowest levels since the end of February. The downside pressure in the EURUSD could extend to 1.05 mark, which is the major 38.2% Fibonacci retracement on September to April rebound, without damaging the positive trend building since September. But, for the 1.05 to serve as a defense to the bullish trend, we need a stronger signal that the Fed would pause hiking the rates.

And this is not the case for now. Even though, the Fed funds futures are back pricing in the possibility of no rate hike in June as the base case scenario, noises from the Fed members hint that a pause to rate hikes in June wouldn’t necessarily mean that there won’t be another 25bp increase by the end of July.

Profit taking

The US House cleared the debt limit bill despite critics both sides. With the bill now headed to the Senate, it’s almost certain that it will get approved before the June 5th deadline.

One would’ve expected a relief rally on the back of the news that the debt ceiling crisis is almost over, but the stock markets gave a muted reaction. The more than 5.5% slump in Nvidia shares outweighed the debt ceiling optimism.

As a result, the S&P500 closed 0.60% lower and Nasdaq 100 fell 0.70% as a sign that we will probably see profit taking after the massive AI-triggered tech rally, and after the debt ceiling is raised.

Equity traders will shift their focus back to more hawkish Fed expectations and rising yields, while the Treasury will suck liquidity back to refill its General Account that has almost emptied with the extended debt ceiling crisis.

The US 2-year yield is up this morning after a two-session fall, while the 2-10-year portion remains severely inverted keeping recession odds well alive. Today, the ISM manufacturing data is expected to confirm further contraction in activity in May.

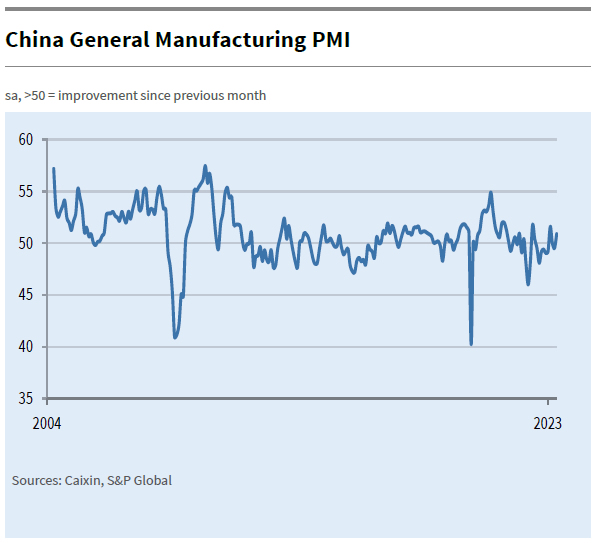

Caixin optimism

In China, the Caixin manufacturing index printed a number above 50 for May, in the expansion zone, in contradiction with the official PMI which unexpected showed a faster contraction the same month earlier this week. The latter may have helped halting bleeding in crude oil, which lost more than 2.50% yesterday, and more than 10% since the May 24 peak, when the Saudi Prince Bin Salman had warned sellers that it would ouch at the next OPEC meeting.

The barrel of US crude tipped a toe below $67pb yesterday, and trades a touch above the $68pb this morning, with sellers showing their teeth to Saudi Prince and his warnings. The dynamics in oil prices gives a solid indication that any OPEC-led rally will serve as opportunity to sell a top.

Zooming into the Chinese stocks, today’s better-than-expected Caixin data gave a little boost to Hang Seng index, which tracks a number of mainland stocks, but the index fell 20% since the beginning of this year, and is at the door of the bear market, whereas the US and European stocks were well bid since the start of this week.

European stocks sputter

The European stocks fell off the race in the second half of May, at about the same time the euro peaked against the US dollar.

The Stoxx 600 index follows the EURUSD very closely, hinting that a further weakness in the EURUSD should continue weighing on European stocks. The soft rebound in Chinese economy, and rising recession odds in the US weigh on European luxury goods makers, which have been carrying the rally on their shoulders since last year. Hermes, which doubled its share price in about a year gives toppish signs near the 2000 mark, while LVMH is testing the minor 23.6% Fibonacci support on the past year’s rally. The current levels look good for further correction in European luxury stocks.

Deal on the US Debt Ceiling

Market movers today

Today's main data release from euro area will be the May flash HICP. While consensus was originally looking for only a slight moderation in core inflation, preliminary figures from individual countries have so far come out clearly below expectations.

From the US, ADP private sector employment report and ISM manufacturing index are due for release. Consensus is looking for moderating employment growth, although leading indicators have so far pointed towards fairly upbeat development in May. ISM is expected to decline modestly following a downtick in the flash PMIs earlier.

From central banks, ECB's Lagarde and the Fed's Harker are scheduled to give speeches today.

The 60 second overview

The House of Representatives passed the deal between President Biden and the Republicans on the debt ceiling yesterday and thus averting a default on US Treasuries. The bill now goes to the Senate where it is also expected to be passed. This signals the end to debt ceiling uncertainty for now.

The deal has lifted Asian equity markets this morning, there has been a modest rise in US Treasury yields in the Asian trading, while the dollar has been stable. The oil price continues to decline.

There has been several comments from Federal Reserve signalling a pause to the hikes, but also that the Federal Reserve has not yet reached its peak. The positive surprise in US jobs data yesterday gave support to this view, but inflation is coming down as we saw in the string of European inflation data released yesterday.

The Chinese manufacturing PMI - Caixin, released this morning, rose unexpectedly to 50.9.

Equities: Global equities lower yesterday across regions and with a defensive tilt. Please note that cyclicals massively outperformed defensives in May despite equities in general being flat for the month. This fits our strategy fine, but we admit that most of our coinciding macro models ertr not as strong as the cyclical outperformance suggest and hence opening a negative reality gap. Banks came under pressure yesterday due to increased focus on potential liquidity drain in the aftermath of a US debt ceiling. As covered in the Morning Espresso earlier this week, we will see hefty bond issuance and QT the next six months in the US, leaving a potential liquidity risk. In US yesterday, Dow -0.4%, S&P 500 -0.6%, Nasdaq -0.6% and Russell 2000 -1.0%. Asian markets are positive this morning, Caixin PMI way better than NBS yesterday sending most indices higher in Asia. European futures higher as well while US futures are flat this morning.

FI: Yesterday, the global bond yields and interest rates continued to decline on the back of softer inflation data from euro area as both French and German inflation declined. The positive surprise in the US jobs market data - the JOLTs report, however sent rates a bit higher, but they ended the day lower as 10Y Bunds declined some 6bp. The spread between the periphery and core-EU remained stable.

FX: EUR/USD multi-week down trend intact with the cross slightly below 1.07. USD/JPY below 140 mark as we entered a short position based on relative monetary policy. Massive drop in EUR/NOK yesterday, close to 20 figures, on the back of Norges Bank's FX sales announcement. The cross has paused just above 11.80. Also SEK had a good day with EUR/SEK down around 10 figures.

Credit: CDS indices were slightly wider yesterday with iTraxx Main closing at 82bp (+2bp) while Xover widened by 7bp to 434bp. In financials there was more senior supply with Ibercaja Banco in the market, while in covereds both Rabobank and Arkéa brought new 10y deals.

Nordic macro

The Norwegian manufacturing PMI has rallied over the past couple of months and was back above 50 in April, pointing to increasing activity. This contrasts with global PMIs, which have generally fallen further into recessionary territory in recent months. This could be down to higher activity in oil services in Norway, but could also just be noise. Our best guess is that the PMI will hold steady around 51.0.

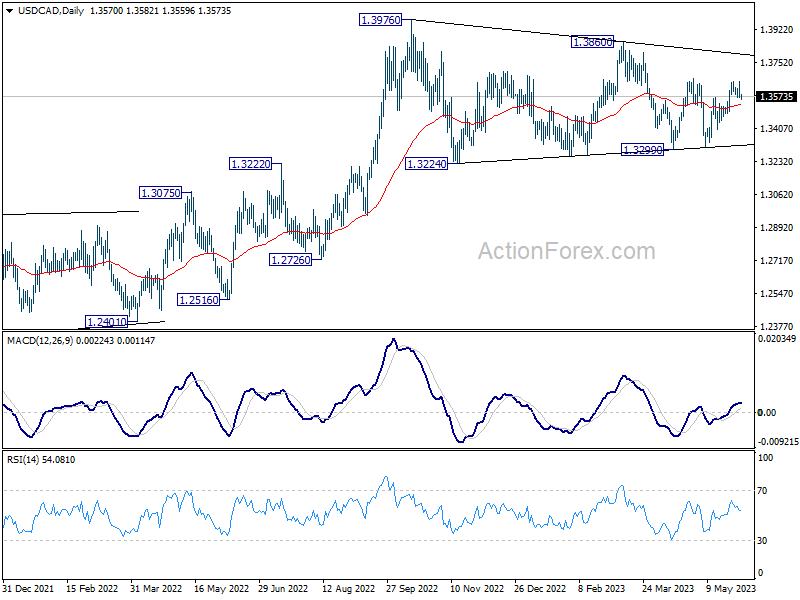

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3545; (P) 1.3599; (R1) 1.3629; More....

USD/CAD is staying in range below 1.3653 and intraday bias remains neutral. Price actions from 1.3976 are seen as a triangle consolidation pattern. Above 1.3666 will target 1.3860 resistance first. Firm break of 1.3860 will argue that larger up trend is ready to resume through 1.3976 high.

In the bigger picture, rise from 1.2005 (2021 low) is expected to resume through 1.3976 after consolidation from there completes. On decisive break of 1.3976, next target will be 1.4667/89 long term resistance zone. This will remain the favored case as long as 38.2% retracement of 1.2005 to 1.3976 at 1.3233 holds.

Dollar Mixed Ahead of ADP and ISM, Euro Eyes CPI

Dollar turned mixed in Asian session as traders are awaiting fresh inspirations from economic data and comments from Fed officials. The FOMC is clearly split in way with some policymakers advocating a "hold" in June. Nevertheless, they're unified in another way that even a "hold" doesn't necessarily means a "pause", not to mention a "peak". The greenback, in any case, will look into today's ADP employment and ISM manufacturing, as well as tomorrow's non-farm payroll data for more guidance.

Australian Dollar is recovering mildly, with help from China's manufacturing data, but upside is limited. Yen is turning softer again after this week's rebound is losing momentum. Sterling is holding on to gains against Euro and Swiss Franc, as well as Dollar. Meanwhile, Canadian Dollar is sluggish together with New Zealand Dollar.

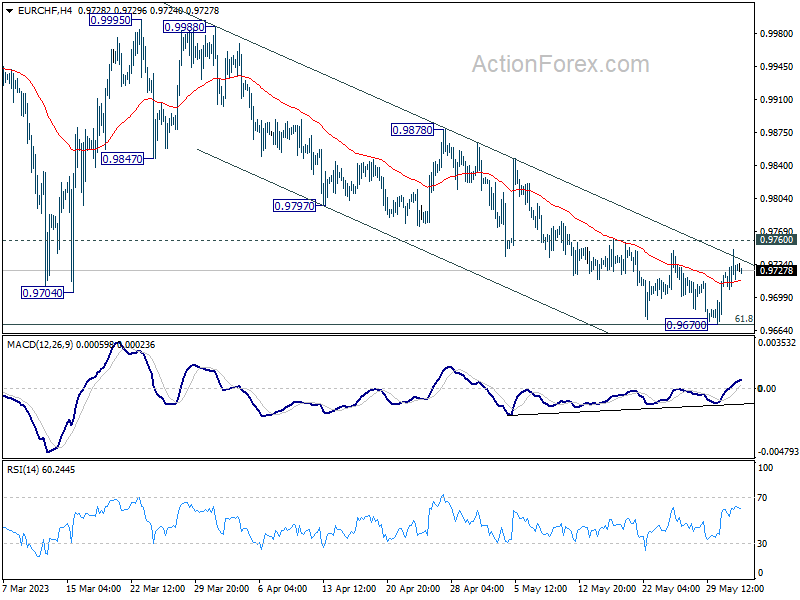

Technically, Euro is clearly weaker this week after downside surprising in France and Germany inflation data. Yet, EUR/CHF is still working hard to form a bottom and focuses will be on 0.9760 minor resistance today. Firm break there should confirm short term bottoming at 0.9670 and bring stronger rebound back to 0.9797/9878 resistance zone. The next move will depend on markets' reaction to today's Eurozone CPI data.

In Asia, Nikkei closed up 0.84%. Hong Kong HSI is up 0.54%. China Shanghai SSE is up 0.28%. Singapore Strait Times is up 0.12%. Japan 10-year JGB yield is down -0.0081 at 0.425. Overnight, DOW dropped -0.41%. S&P 500 dropped -0.61%. NASDAQ dropped -0.63%. 10-year yield dropped -0.063 to 3.637.

SNB Jordan: We don't see a big risk in over-tightening monetary policy

SNB Chairman Thomas Jordan recently warned yesterday that the more inflation is entrenched in the perception of companies and households, the harder it is to bring it down. He highlighted the urgency of the situation, stating, "We have to bring it back below 2% as soon as possible."

Discussing the bank's approach towards interest rates, Jordan assured that Switzerland's are "still very low". "We don't see a big risk in over-tightening monetary policy. It is not something that will damage financial stability in general in Switzerland," he affirmed.

Regarding the financial stability issues surrounding Credit Suisse, Jordan clarified that it was an individual case where the problem was not interest rates, but rather a "lack of trust of market participants in an institution."

Looking ahead, market expectations suggest a 25bps rise from the current 1.5% level when the central bank delivers its next assessment in June.

BoE Mann: Inflation gap in the UK more persistent than others

BoE policymaker, Catherine Mann, has highlighted the unique and mounting inflation problem that Britain is facing in comparison to the United States and the Eurozone.

Mann pointed to both large-scale price increases and the rising persistence of these underlying pressures as causes for concern. She emphasized, "The gap (between headline and core CPI) that I have in my country is more persistent than the gaps that we see in either of my neighbours, the U.S. or the euro area."

The gap she refers to is the disparity between headline inflation (which includes volatile commodities like food and energy) and core inflation (which excludes these commodities).

Notably, Mann underscored the role of British businesses and increased wages in maintaining high core inflation. She explains that businesses in the UK have been successful in passing on price rises, contributing to this persistent inflation gap. This, coupled with increased wages, suggests that headline inflation has been slower to recede towards the core rate than it has in other regions.

"There is a gap between the headline, which is incorporating energy which went up really high and now has come down, and core where we do start to see the implications coming through pricing channels, through wage negotiations, into something that is persistent," Mann explained.

Fed Jefferson: A pause in June doesn't mean rates have peaked

Comments from top officials from Fed suggested a pause in interest rate hikes in June while possible, shouldn't be misinterpreted as a sign that peak rates for the cycle have been reached.

Fed Governor, Philip Jefferson, clarified, "A decision to hold our policy rate constant at a coming meeting should not be interpreted to mean that we have reached the peak rate for this cycle."

Jefferson, suggested that skipping a rate hike at an upcoming meeting would provide an opportunity for the committee to review more data before deciding on the extent of any further policy tightening.

Philadelphia Fed President, Patrick Harker, echoed this sentiment, albeit with a more forceful argument for the need to 'skip' rather than 'pause'. "I am in a camp increasingly coming into this meeting of thinking that we really should skip, not pause," he remarked.

Harker believes the current policy is nearing, if not already at, a restrictive level and suggests a period of careful reflection before further action is taken.

Harker added, "I think we have to be ready that we might have to do more and I'm fully aware we have to do that and willing to do that, but I want to give it a little bit of time."

IMF sees opportunity for Japan to re-anchoring Inflation Expectations

IMF chief economist, Pierre-Olivier Gourinchas, suggested that a unique opportunity may be presenting itself in Japan to re-anchor inflation expectations to BoJ's target. However, he cautioned that the process won't be instantaneous.

"There's an opportunity right now," Gourinchas said, "but it will take time. It won't happen overnight." Achieving this re-anchoring requires convincing the public that Japan won't slide back into deflation - a challenge given the country's prolonged struggle with price stagnation. Gourinchas believes it's "too early" for the BoJ to tighten policy, stressing the need for careful handling of the situation.

Pointing to the global trend of persistent inflation despite initial expectations of transitory dynamics, Gourinchas warned, "Obviously, the history of the last two years is one where inflation that was supposed to be transitory, turned out to be not transitory. We could have similar dynamics in Japan." Given this possibility, he underscored the need for vigilance and readiness to tighten monetary policy if inflation remains too high.

Regarding potential strategies for policy tightening, Gourinchas suggested a cautious approach. "It's probably safer to first move away from the control of long-term yields. And then, if the need arises to tighten monetary policy, it can do so as part of the usual tightening of the policy rate," he proposed. However, he acknowledged that executing this transition would be technically complex.

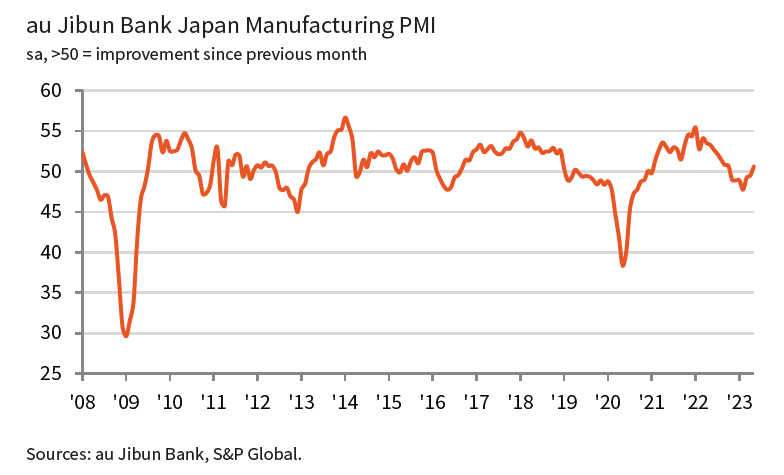

Japan PMI manufacturing finalized at 50.6, a decisive turnaround

Japan PMI Manufacturing was finalized at 50.6 in May, up from April's 49.5. That's the first expansionary reading since October 2022, signalling a modest overall improvement in operating conditions. Also, business optimism reached highest level since January 2022, while supplier performance stabilized.

Tim Moore, Economics Director at S&P Global Market Intelligence, said: "The latest au Jibun Bank PMI survey highlights a decisive turnaround in manufacturing sector performance during May and brings to an end a six-month period of weakening business conditions."

China Caixin PMI manufacturing rose to 50.9, activity improved

China Caixin PMI Manufacturing rose from 49.5 to 50.9 in May, signaling the first improvement in the health of the sector since February. Caixin noted stronger increase in output as firms saw fresh upturn in new business. Input costs fell solidly. Employment, however, continued to decline as business confidence softened.

Wang Zhe, Senior Economist at Caixin Insight Group said: "In a nutshell, manufacturing activity improved in May. Both supply and demand expanded, but employment sank to a three-year low. Businesses stepped up purchasing, inventories of raw materials grew marginally, logistics picked up, prices continued to slump, and manufacturers' optimism wavered."

Looking ahead

Eurozone CPI flash and ECB meeting accounts are the main feature in European session. Eurozone will also release unemployment rate and PMI manufacturing final. UK will release PMI manufacturing final, M4 money supply and mortgage approvals.

Later in the day, US ISM manufacturing and ADP employment will take center stage. Weekly jobless claims will also be released.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3545; (P) 1.3599; (R1) 1.3629; More....

USD/CAD is staying in range below 1.3653 and intraday bias remains neutral. Price actions from 1.3976 are seen as a triangle consolidation pattern. Above 1.3666 will target 1.3860 resistance first. Firm break of 1.3860 will argue that larger up trend is ready to resume through 1.3976 high.

In the bigger picture, rise from 1.2005 (2021 low) is expected to resume through 1.3976 after consolidation from there completes. On decisive break of 1.3976, next target will be 1.4667/89 long term resistance zone. This will remain the favored case as long as 38.2% retracement of 1.2005 to 1.3976 at 1.3233 holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Capital Spending Q1 | 11.00% | 5.50% | 7.70% | |

| 00:30 | JPY | Manufacturing PMI May F | 50.6 | 50.8 | 50.8 | |

| 01:30 | AUD | Private Capital Expenditure Q1 | 2.40% | 1.10% | 2.20% | 3.00% |

| 01:45 | CNY | Caixin Manufacturing PMI May | 50.9 | 49.5 | ||

| 06:00 | CHF | Trade Balance (CHF) Apr | 2.6B | 3.73B | 4.53B | |

| 06:00 | EUR | Germany Retail Sales M/M Apr | 0.80% | 0.90% | -2.40% | -2.20% |

| 07:30 | CHF | Manufacturing PMI May | 44.5 | 45.3 | ||

| 07:45 | EUR | Italy Manufacturing PMI May | 45.8 | 46.8 | ||

| 07:50 | EUR | France Manufacturing PMI May F | 46.1 | 46.1 | ||

| 07:55 | EUR | Germany Manufacturing PMI May F | 42.9 | 42.9 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI May F | 44.6 | 44.6 | ||

| 08:30 | GBP | Manufacturing PMI May F | 46.9 | 46.9 | ||

| 08:30 | GBP | Mortgage Approvals Apr | 54K | 52K | ||

| 08:30 | GBP | M4 Money Supply M/M Apr | -0.20% | -0.60% | ||

| 09:00 | EUR | Eurozone Unemployment Rate Apr | 6.50% | 6.50% | ||

| 09:00 | EUR | Eurozone CPI Y/Y May P | 6.30% | 7.00% | ||

| 09:00 | EUR | Eurozone CPI Core May P | 5.50% | 5.60% | ||

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 11:30 | USD | Challenger Job Cuts May | 175.90% | |||

| 12:15 | USD | ADP Employment Change May | 167K | 296K | ||

| 12:30 | USD | Initial Jobless Claims (May 26) | 236K | 229K | ||

| 12:30 | USD | Nonfarm Productivity Q1 | -2.70% | -2.70% | ||

| 12:30 | USD | Unit Labor Costs Q1 | 6.30% | 6.30% | ||

| 13:30 | CAD | Manufacturing PMI May | 50.2 | |||

| 13:45 | USD | Manufacturing PMI May F | 48.5 | 48.5 | ||

| 14:00 | USD | ISM Manufacturing PMI May | 47 | 47.1 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid May | 52.5 | 53.2 | ||

| 14:00 | USD | ISM Manufacturing Employment Index May | 50.2 | |||

| 14:00 | USD | Construction Spending M/M Apr | 0.10% | 0.30% | ||

| 14:30 | USD | Natural Gas Storage | 106B | 96B | ||

| 15:00 | USD | Crude Oil Inventories | -1.4M | -12.5M |

China Caixin PMI manufacturing rose to 50.9, activity improved

China Caixin PMI Manufacturing rose from 49.5 to 50.9 in May, signaling the first improvement in the health of the sector since February. Caixin noted stronger increase in output as firms saw fresh upturn in new business. Input costs fell solidly. Employment, however, continued to decline as business confidence softened.

Wang Zhe, Senior Economist at Caixin Insight Group said: "In a nutshell, manufacturing activity improved in May. Both supply and demand expanded, but employment sank to a three-year low. Businesses stepped up purchasing, inventories of raw materials grew marginally, logistics picked up, prices continued to slump, and manufacturers' optimism wavered."

Japan PMI manufacturing finalized at 50.6, a decisive turnaround

Japan PMI Manufacturing was finalized at 50.6 in May, up from April's 49.5. That's the first expansionary reading since October 2022, signalling a modest overall improvement in operating conditions. Also, business optimism reached highest level since January 2022, while supplier performance stabilized.

Tim Moore, Economics Director at S&P Global Market Intelligence, said: "The latest au Jibun Bank PMI survey highlights a decisive turnaround in manufacturing sector performance during May and brings to an end a six-month period of weakening business conditions."

IMF sees opportunity for Japan to re-anchoring Inflation Expectations

IMF chief economist, Pierre-Olivier Gourinchas, suggested that a unique opportunity may be presenting itself in Japan to re-anchor inflation expectations to BoJ's target. However, he cautioned that the process won't be instantaneous.

"There's an opportunity right now," Gourinchas said, "but it will take time. It won't happen overnight." Achieving this re-anchoring requires convincing the public that Japan won't slide back into deflation - a challenge given the country's prolonged struggle with price stagnation. Gourinchas believes it's "too early" for the BoJ to tighten policy, stressing the need for careful handling of the situation.

Pointing to the global trend of persistent inflation despite initial expectations of transitory dynamics, Gourinchas warned, "Obviously, the history of the last two years is one where inflation that was supposed to be transitory, turned out to be not transitory. We could have similar dynamics in Japan." Given this possibility, he underscored the need for vigilance and readiness to tighten monetary policy if inflation remains too high.

Regarding potential strategies for policy tightening, Gourinchas suggested a cautious approach. "It's probably safer to first move away from the control of long-term yields. And then, if the need arises to tighten monetary policy, it can do so as part of the usual tightening of the policy rate," he proposed. However, he acknowledged that executing this transition would be technically complex.