Sample Category Title

USA: Tough Spell for the Manufacturing Sector Continues in May

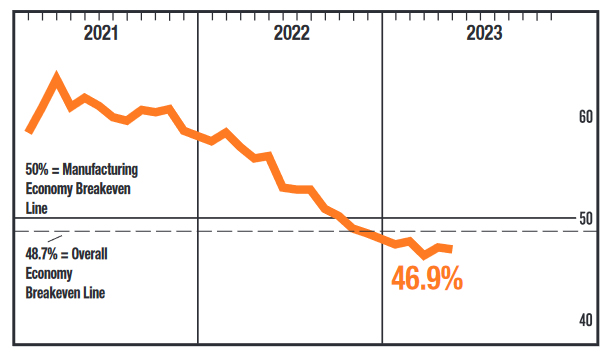

The May ISM Manufacturing Index registered 46.9, barely changed from April's 47.1 reading and roughly in line with expectations for a 47.0 print.

New orders pulled back 3.1 percentage points (pp) to 42.6, while new export orders ticked up 0.2 pp to 50.0.

The backlog of orders sub-index tumbled to 37.5, down 5.6 pp from April's 43.1 print. This is the lowest reading since March 2009.

The production and employment indexes both reflected growth, rising 2.2 pp and 1.2 pp, respectively, to 51.1 and 51.4.

The supplier deliveries sub-index fell to 43.5 from 44.6 in April, reflecting faster supplier deliveries. The prices index showed raw materials gave back some of their gains from April as the index pulled back 9.0 pp to 44.2.

Four of 18 manufacturing industries reported growth in May. The industries reporting growth are Nonmetallic Mineral Products; Furniture & Related Products; Transportation Equipment; and Fabricated Metal Products.

Key Implications

The slowdown in the manufacturing sector continues with little relief in sight. Nine consecutive months of falling new orders and order backlogs contracting at their fastest clip since the Great Recession reflect a sector whose near-term outlook is facing significant headwinds.

Looking forward, macroeconomic conditions are unlikely to improve the sector's prospects. Strong labor market data is lifting the odds that the Fed may have to extend its rate hiking cycle – prolonging the pain for the interest rate sensitive goods sector. That said, there is a silver lining to this report as the Transportation Equipment sector reported expansion in the month. With falling supplier delivery times, and clearing backlogs, the prospect of increased inventory in the automotive sector will be a welcome development for firms and households that have delayed purchases amidst historically tight supply conditions.

Stocks Waver as Traders Pare Back Expectations for Fed Rate Hikes

- Disinflation Trends might be back as prices paid plunged 9 points in the ISM manufacturing report

- ADP Report: Pay growth is slowing substantially

- Still waiting on layoff announcements to hit jobless claims data

US stocks are rising after some dovish Fed speak and as the House was able to advance the debt ceiling bill to the Senate. So far everything with the debt ceiling deal is going as planned after both the House Rules Committee and House of Representatives did their part to get this bill closer to President Biden’s desk. Last night’s House vote showed one of best bipartisan votes in history as 165 Democrats and 149 Republicans supported the bill. The deal is now in the Senate’s hands and the question is not if they will pass the bill but on when they will get it done. Majority Leader Schumer noted they are trying to get it done as soon as possible. A vote could happen today as lawmakers signal they are going to try to restrict amendments.

The latest Fed speak was rather dovish as Jefferson and Harker voiced support for skipping a rate hike at the June meeting. The Fed Whisperer Timiraos also noted that the FOMC is likely to hold rates steady in June.

Wall Street decided to shrug off a hot ADP report and another low jobless claims print and focus on a lower final reading on unit labor costs. The labor market is still looking strong, but perhaps we are seeing some signs that wage growth is gradually falling. Treasury yields rose on ADP, but tumbled after a near 2-point downward revision with labor costs.

US Data

Private payrolls posted another robust beat as employment increased by 278,000 in May, much higher than the 170,000 consensus estimate and slightly lower than revised 291,000 prior reading. The ADP report noted, ““Pay growth is slowing substantially, and wage-driven inflation may be less of a concern for the economy despite robust hiring.”

The 830am economic data drop showed jobless claims remain anchored for now and that first quarter unit labor costs were revised significantly lower.

The ISM manufacturing report was somewhat mixed as prices paid tumbled to contraction territory, export orders were stable, and new orders along with the backlog of orders remained rather depressed.

The key takeaway from the ADP report and unit labor costs is that wage pressures are showing clear signs of weakness, and this is supporting the argument for the Fed to skip the June meeting. The ISM report is showing that the manufacturing space is getting close to finding a bottom as commodity prices come down and as lower prices should bring back buyers.

The NFP report might not show a significant weakening in the labor market, but the downward trend should be in place.

S&P 500 Daily Chart

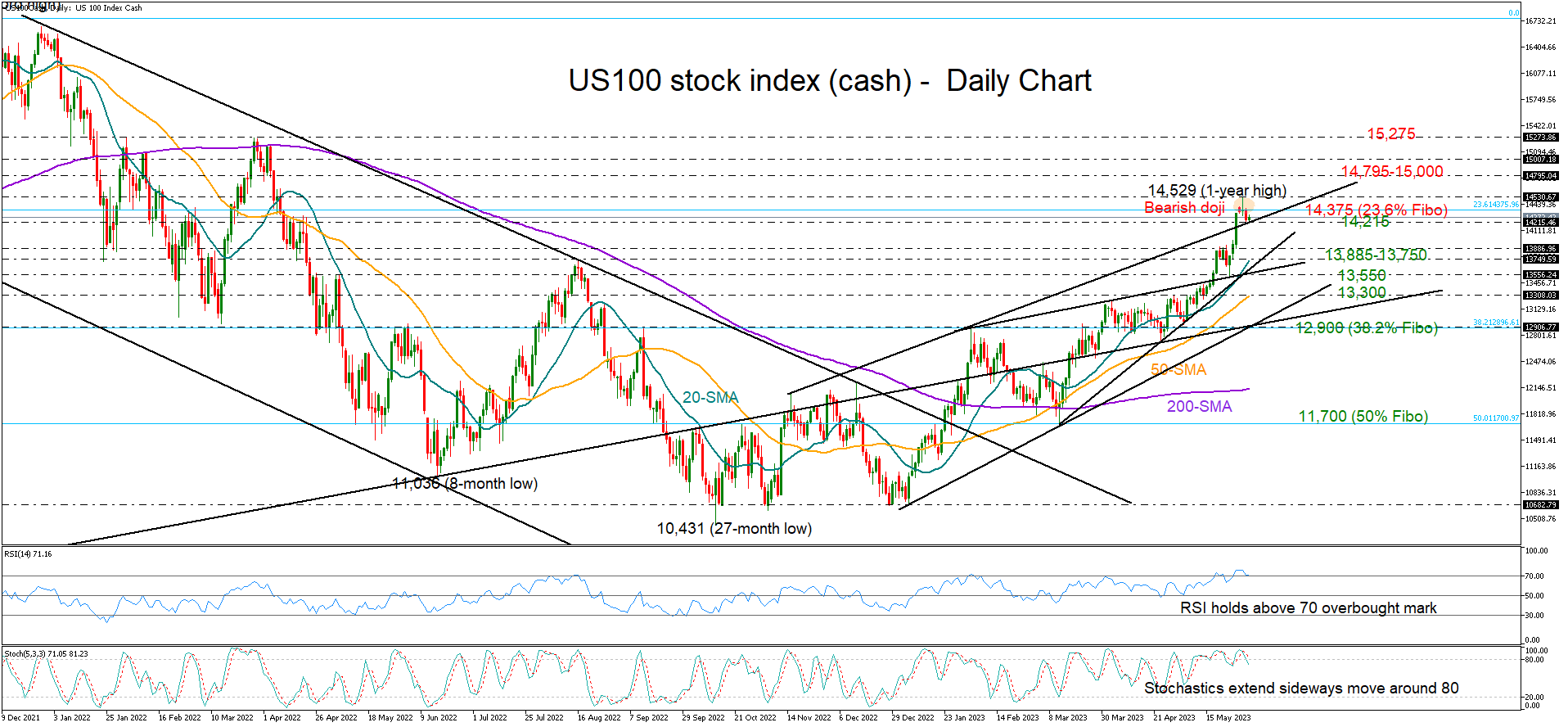

Will the US 100 Index Come Under Profit-Taking Pressure?

The US 100 stock index (cash) opened June’s trading session on a neutral note, though the formation of a bearish doji at the top of the uptrend keeps feeding speculation that the latest remarkable rally has probably peaked.

The RSI and the stochastic oscillator are witnessing overbought conditions. Yet, with the former standing above 70 and the latter preserving a horizontal trajectory around 80, upside pressures could last a bit longer, especially if the 14,215 nearby support area stands firm.

In the event the price heads lower, the next destination could be the 13,885-13,750 zone, where the 20-day simple moving average is converging. The 13,550 territory may attract greater interest as the resistance line from February’s high and the ascending trendline from March’s low intersect each other at this point. Failure to pivot here could shift the spotlight on the 50-day SMA at 13,300.

Conversely, if the index pivots near 14,215, the bulls will target the 14,375 barrier, which overlaps with the 23.6% Fibonacci retracement of the 6,634-16,767 uptrend. An extension beyond the 14,529 top could stall somewhere between 14,795 and 15,000, while higher, the next obstacle could pop up around the constraining region of 15,275.

All in all, the US 100 index might be on the verge of a new bear run. A close below 14,215 could extend the pullback from May’s one-year high.

Sunset Market Commentary

Markets

The bond market rally from earlier this week took a breather this morning. With no more than two 25 bps ECB interest rate hikes discounted through summer and expectations for an additional Fed hike pushed back to July, one might have expected the case to push for more dovishness to have become less compelling, unless it would be backed by outspoken soft data. Indeed, EMU May headline inflation dropped from 7.0% to 6.1%. Core inflation also slowed more than (initially) expected from 5.6% to 5.3%. However, this was no big surprise after national data released earlier this week. Still, 5%+ core inflation is far from a guarantee for the ECB to be sure it is on track to sustainably return inflation back to 2.0%. In the accounts of the early May ECB meeting, developments on core inflation was still seen as a major source of concern. In this respect, ECB ‘hawks’ wanted a directional bias, clarifying that, despite slowing down the pace of hikes to 25 bps, further steps would be warranted. The EMU CPI release left few traces on (interest rate markets). However early in US dealings, yields reversed the early rise, probably as markets still pondered yesterday’s guidance from Fed governors Harker and Jefferson to ‘skip’ a June rate hike and take time to asses incoming data. The ADP labour market report at least didn’t bring much of a strong case for the ‘skip’. 278k of additional US private sector jobs in May again beat the consensus by a wide margin. Jobless claims at 232k also suggested persistent labour market strength. However, a downward revision of the Q1 US unit labour costs from 6.0% to 4.2% was enough to push daily yield changes back in red. Whether this ‘outdated’ series is important input for the Fed’s assessment is subject to discussion. Even so, US yields currently are ceding between 3.5 bps (2-y) and 6 bps (5-y). After finishing this report, the US manufacturing ISM still has to published. The price action on the early morning data at least suggests a tentative dovish bias going into the release. German yields also reversed an initial rise to currently cede up to 3 bps (10-y). Better than expected Chinese data (Caixin PMI) and a (potentially/hoped for) more benign inflation environment initially supported a comeback of European equities. However, the intraday dynamics is far from convincing. The Eurostoxx 50 only gains 0.45% after yesterday’s 1.7% decline. US indices open little changed.

On FX markets, the dollar eases off recent peak levels. DXY is at risk of falling below the 104 big figure. EUR/USD tries to regain the 1.07 barrier mainly on USD weakness rather than on outright euro strength. It’s too early to call off the downward alert. USD/JPY is further drifting off the 140 barrier (139.10). Sterling continues outperforming both the dollar (Cable 1.2475) and the euro. At EUR/GBP 0.858, key 0.8547 December low is coming with reach.

News & Views

The National Bank of Belgium upwardly revised the Q1 GDP figure from 0.4% Q/Q to 0.5% Q/Q (1.4% Y/Y from 1.3% /Y). Details were constructive. Household consumption rose by 0.6% Q/Q, with the increase driven by purchases of non-durable goods. Business investment grew by 1.9% Q/Q while government consumption declined by 0.7% Q/Q. Inventories decreased by 0.2% Q/Q. Imports and exports of goods and services both contracted 1% in Q1 (net export 0%). In the supply-side breakdown, value added in the manufacturing industry declined by 0.6% Q/Q. The services sector grew by 0.8% Q/Q and the building industry by 0.3% Q/Q. Domestic employment rose by 0.3% Q/Q (1.3% Y/Y). Separately, StatBel reported a 9.8% annualized increase in the hourly labour cost in Q1 2023, which is the strongest since the start of the series in 2000. The sharpest increase is registered in Accommodation and food service activities with 10.5%, while the lowest increase was observed in Electricity, gas, steam and air conditioning supply with +7.7%.

The Slovak Republic raised €2bn today via a new 10yr syndicated deal. Order books totaled over €7.7bn, resulting in a significant price concession compared to initial price takings in the MS +95 bps area and revised guidance at MS +85 bps. The bond was eventually priced at MS + 80 bps. Slovak debt agency Ardal is well-advanced with this year’s funding. YTD, they now raised €8.26bn. The lion share of the amount came from today’s syndication and from two other benchmark deals in February (€2bn Feb2035 & €1.5bn Feb2043). In its official funding plans, Ardal estimated this year’s gross borrowing requirement at €13bn, but they aimed for only €8bn of bond issuance with EU funds and the cash buffer doing the rest of the job.

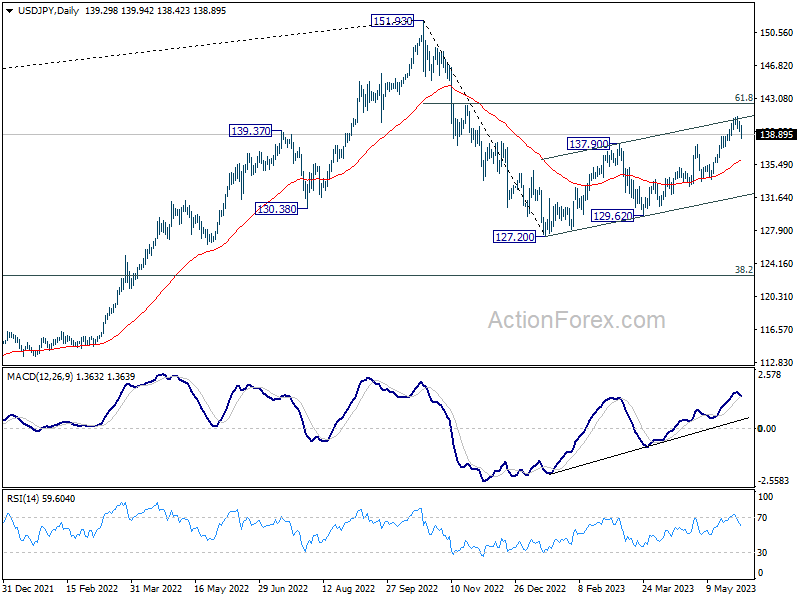

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 138.93; (P) 139.66; (R1) 140.07; More...

Intraday bias in USD/JPY remains neutral for the moment. Downside of retreat should be contained above 138.22 support to bring another rally. Break of 140.90 will resume larger rise from 127.20 to 142.48 fibonacci level. However, considering bearish divergence condition in 4 hour MACD, break of 138.22 will confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 135.89).

In the bigger picture, rise from 127.20 is seen as the second leg of the corrective pattern from 151.93 high. Stronger rally would be seen to 61.8% retracement of 151.93 to 127.20 at 136.34. Sustained break there will pave the way back to retest 151.93. On the downside, however, break of 133.73 support will argue that the pattern could have started the third leg through 127.20 low.

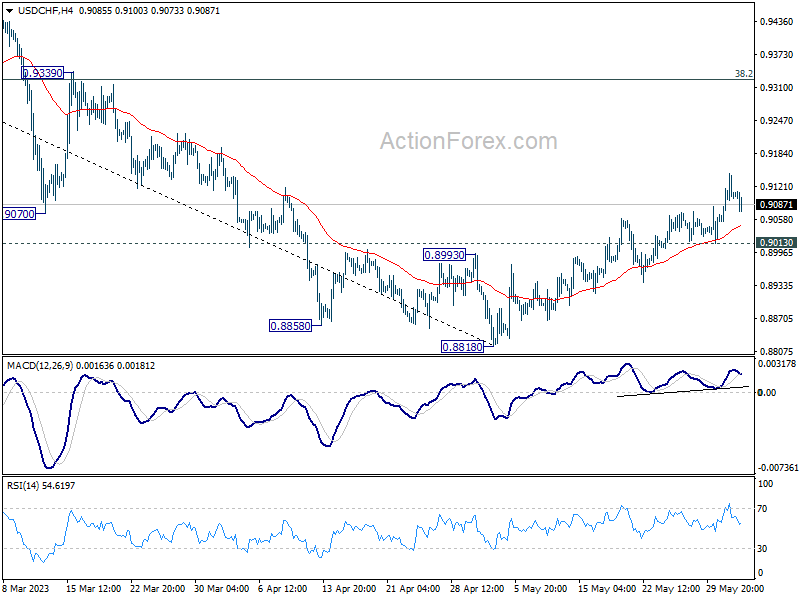

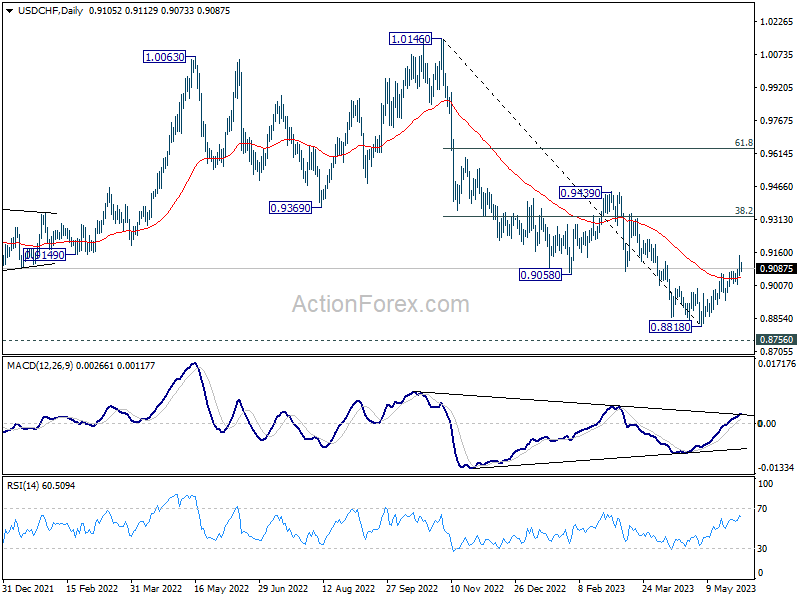

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9055; (P) 0.9102; (R1) 0.9153; More...

Further rise is expected in USD/CHF as long as 0.9013 minor support holds. Current rally is seen as correcting whole down trend from 1.0146. Further rise should then be seen to 38.2% retracement of 1.0146 to 0.8818 at 0.9325. On the downside, below 0.9013 minor support will turn intraday bias neutral first.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high). So, downside should be contained by 0.8756 to bring reversal. Sustained break of 0.9058 support turned resistance will be the first sign of medium term bottoming. However, decisive break of 0.8756 will carry larger bearish implications.

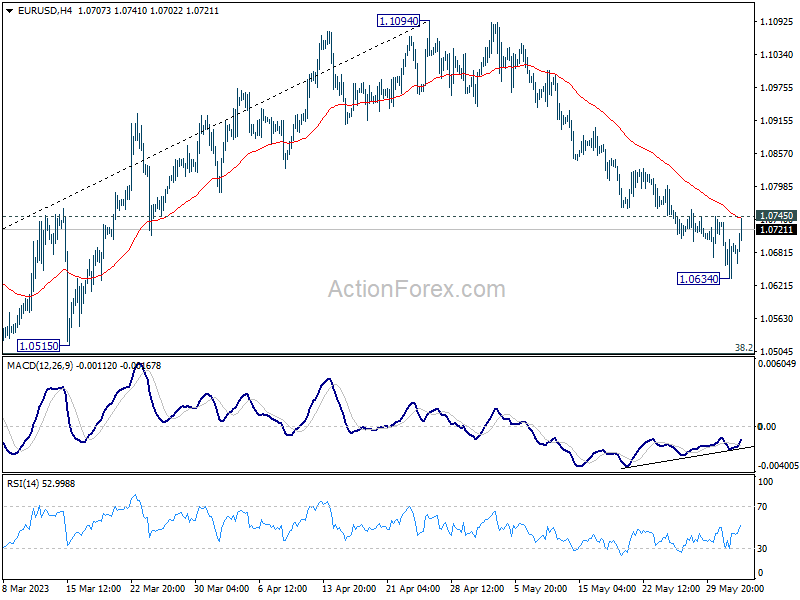

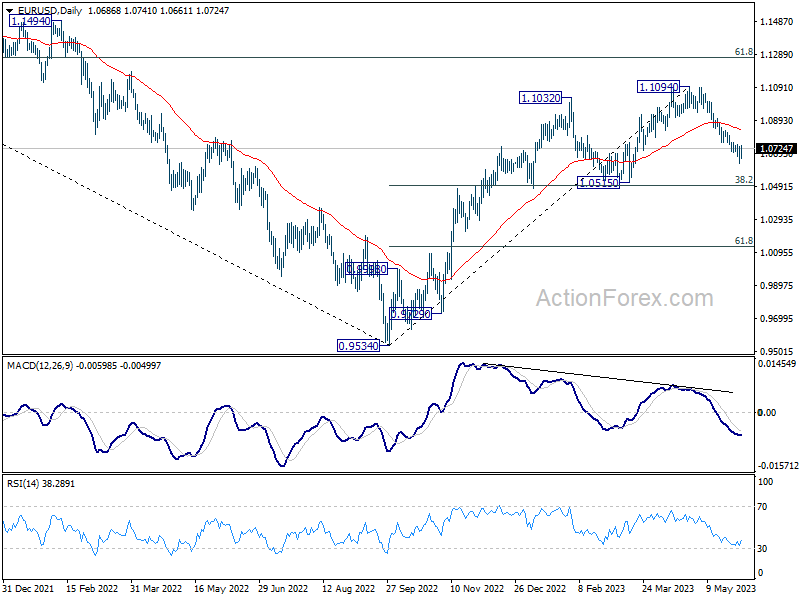

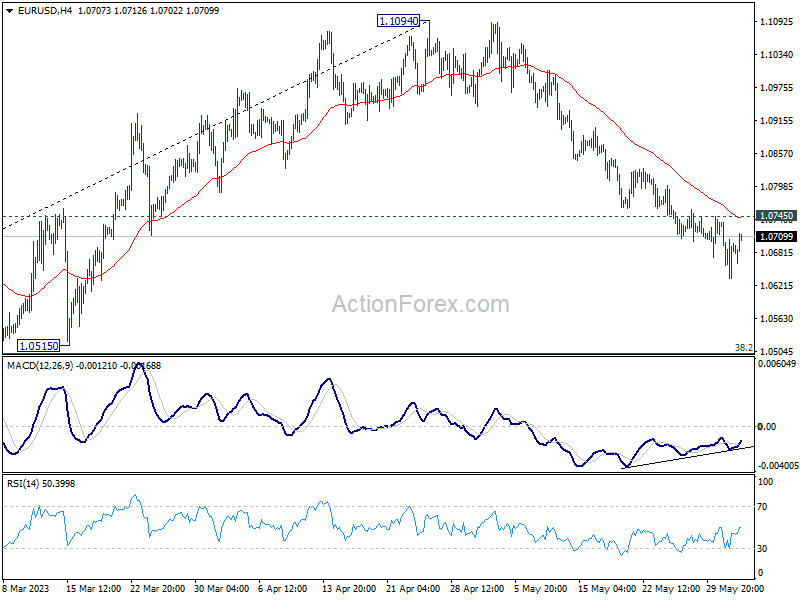

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0637; (P) 1.0687; (R1) 1.1.0739; More...

Intraday bias in EUR/USD is turned neutral again with today's recovery. Considering bullish convergence condition in 4H MACD, break of 1.0745 minor resistance will indicate short term bottoming at 1.0634. Intraday bias will then be back on the upside for rebound to 55 D EMA (now at 1.0836). Nevertheless, break of 1.0634 will resume the fall from 1.1094 to 1.0515 cluster support, 38.2% retracement of 0.9534 to 1.1094 at 1.0498.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

US ISM manufacturing dropped to 46.9, corresponds to -0.6% GDP annualized GDP contraction

US ISM Manufacturing PMI dropped from 47.1 to 46.9 in May, below expectation of 47.0. Looking at some details, new orders dropped from 45.7 to 42.6. Production rose from 48.9 to 51.1. Employment rose from 50.2 to 51.4. Prices dropped sharply from 53.2 to 44.2.

ISM said: " "This is the seventh month of contraction and continuation of a downward trend that began in June 2022. That trend is reflected in the Manufacturing PMI's 12-month average falling to 49.4 percent."

"The past relationship between the Manufacturing PMI and the overall economy indicates that the May reading (46.9 percent) corresponds to a change of minus-0.6 percent in real gross domestic product (GDP) on an annualized basis."

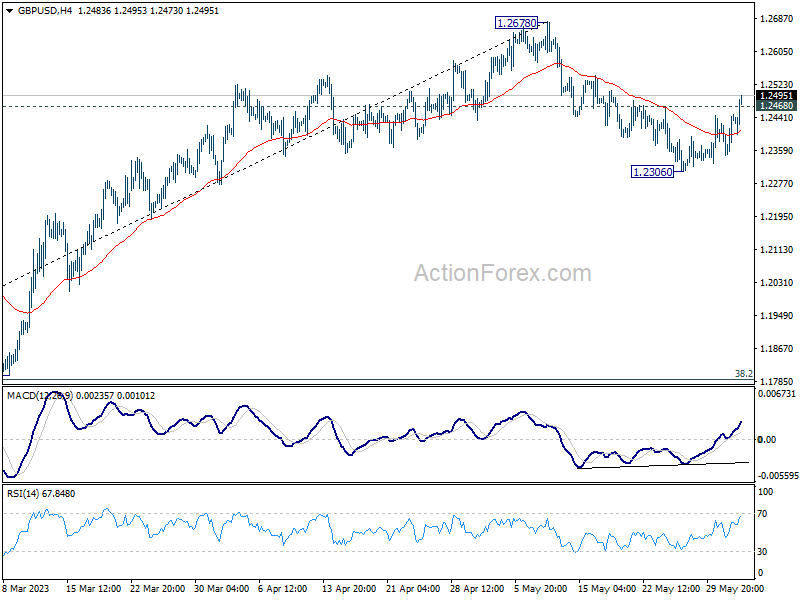

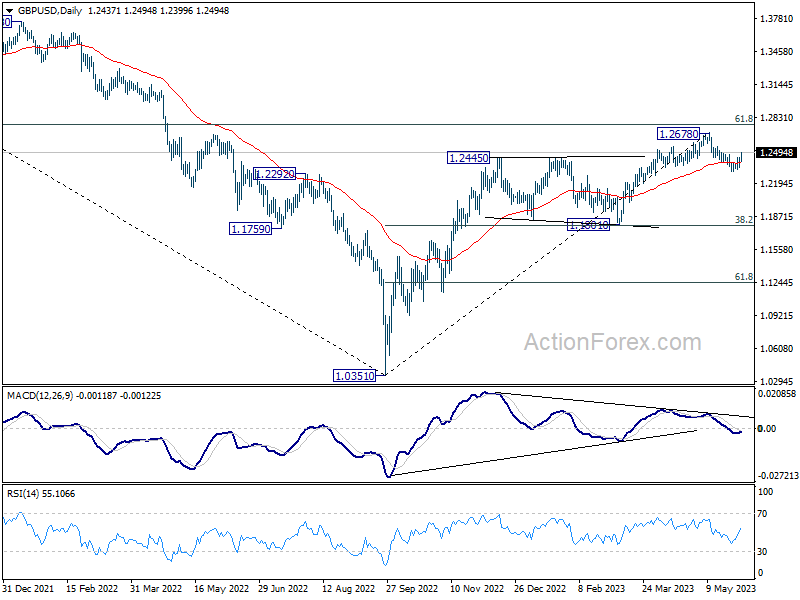

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2378; (P) 1.2411; (R1) 1.2474; More...

GBP/USD's break of 1.2468 minor resistance today argues that corrective pull back from 1.2678 has completed at 1.2306. Intraday bias is back on the upside for retesting 1.2678 high next. But strong resistance could be seen there to limit upside on the first attempt. Meanwhile, break of 1.2306 will resume the correction towards 1.1801 cluster support (38.2% retracement of 1.0351 to 1.2678 at 1.1789)

In the bigger picture, as long as 1.1801 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.1801 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.

Dollar Dips Despite Strong Jobs Data; Sterling Strengthens

Dollar falls broadly today, despite strong job data, as near term consolidations continues. The odds of a June Federal Reserve rate hike seem to be dwindling, following recent comments that emphasized the likelihood of a hold. However, the overall landscape could alter significantly following tomorrow's non-farm payroll report. Notably, the greenback still retains its position above near-term support levels against most major currencies, with the exception of the British Pound.

Staying in the currency markets, overall development is indeed mixed. Sterling is emerging as one of the day's strongest currencies, largely propelled by purchases against Euro and Swiss Franc. Australian Dollar stands out as the top performer, while its trans-Tasman cousin, New Zealand dollar, ranks among the worst. Japanese Yen is fluctuating, still attempting to prolong this week's corrective recovery.

Technically, levels to watch in Dollar pairs include 1.0745 resistance in EUR/USD, 0.6558 resistance in AUD/USD, 0.9013 support in USD/CHF, 138.22 support in USD/JPY, and 1.3483 support in USD/CAD. As long as these levels hold, Dollar's rally could resume any time.

In Europe, at the time of writing, FTSE is up 0.21%. DAX is up 0.66%. CAC is up 0.16%. Germany 10-year yield is down -0.0263 at 2.258. Earlier in Asia, Nikkei rose 0.84%. Hong Kong HSI dropped -0.10%. China Shanghai SSE rose 0.00%. Singapore Strait Times rose 0.24%. Japan 10-year JGB yield dropped -0.0123 to 0.420.

US ADP jobs grew 278k, pay growth slowing substantially

US ADP private employment grew 278k in May, well above expectation of 167k. By sector, goods-producing jobs grew 110k while service-providing jobs grew 168k. By establishment size, small companies added 235k jobs, medium companies added 140k, large companies cut -106k.

Job changers saw a gain of 12.1% yoy, down a full percentage point from April. For job stayers, the increase was 6.5% yoy in May, down from 6.7% yoy.

"This is the second month we've seen a full percentage point decline in pay growth for job changers. Pay growth is slowing substantially, and wage-driven inflation may be less of a concern for the economy despite robust hiring." Nela Richardson, Chief Economist, ADP said.

US jobless claims rose to 232k, slightly below expectations

US initial jobless claims rose 2k to 232k in the week ending May 27, slightly below expectation of 236k. Four-week moving average of initial claims dropped -2.5k to 229.5k.

Continuing claims dropped -6k to 1795k in the week ending May 20. Four-week moving average of continuing claims dropped -1.5k to 1789k.

Eurozone CPI slowed to 6.1% yoy in May, core CPI down to 5.3% yoy

Eurozone CPI slowed from 7.0% yoy to 6.1% yoy in May, below expectation of 6.3% yoy. CPI core (ex-energy, food, alcohol & tobacco) slowed from 5.6% yoy to 5.3% yoy, below expectation of 5.3% yoy.

Looking at the main components, food, alcohol & tobacco is expected to have the highest annual rate in May (12.5%, compared with 13.5% in April), followed by non-energy industrial goods (5.8%, compared with 6.2% in April), services (5.0%, compared with 5.2% in April) and energy (-1.7%, compared with 2.4% in April).

Eurozone PMI manufacturing finalized at 44.8, weakness in demand increasingly evident

Eurozone PMI Manufacturing was finalized at 44.8 in May, down from April's 45.8, hitting the worst level in 36 months. PMI Manufacturing output dropped from 58.5 to 46.4, a 6-month low. Factor gate prices declined fro the first time since September 2020.

Looking at some member states, Ireland (47.5), Italy (45.9), the Netherlands (44.2) and Germany (43.2) were all at 36-month low. Austria hit 37-month low at 39.7. France recovered to 2-month high at 45.7.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, said: "The weakness in demand in the manufacturing sector, which has become increasingly evidence since the beginning of the year in falling PMI readings, has now led the surveyed companies to reduce their production for the second month in a row".

UK PMI manufacturing finalized at 47.1, downturn deepened

UK PMI Manufacturing was finalized at 47.1 in May, down from April's 47.8, hitting the lowest level in four-months. S&P Global noted the output contracted in investment and intermediate goods sectors. Input costs fell and supply chain pressured subsided.

Rob Dobson, Director at S&P Global Market Intelligence, said:

"The UK manufacturing downturn deepened in May, with output, new orders and employment all falling at increased rates. Manufacturers are finding that any potential boost to production from improving supply chains is being completely negated by weak demand, client destocking and a general shift in spending in the UK away from goods to services.

" These factors are also driving a broad decrease in demand from overseas amid reports of lost orders from the US and mainland Europe. The retrenchment in export demand is also being exacerbated by some EU clients switching to more local sourcing to avoid post-Brexit trade complications."

Japan PMI manufacturing finalized at 50.6, a decisive turnaround

Japan PMI Manufacturing was finalized at 50.6 in May, up from April's 49.5. That's the first expansionary reading since October 2022, signalling a modest overall improvement in operating conditions. Also, business optimism reached highest level since January 2022, while supplier performance stabilized.

Tim Moore, Economics Director at S&P Global Market Intelligence, said: "The latest au Jibun Bank PMI survey highlights a decisive turnaround in manufacturing sector performance during May and brings to an end a six-month period of weakening business conditions."

China Caixin PMI manufacturing rose to 50.9, activity improved

China Caixin PMI Manufacturing rose from 49.5 to 50.9 in May, signaling the first improvement in the health of the sector since February. Caixin noted stronger increase in output as firms saw fresh upturn in new business. Input costs fell solidly. Employment, however, continued to decline as business confidence softened.

Wang Zhe, Senior Economist at Caixin Insight Group said: "In a nutshell, manufacturing activity improved in May. Both supply and demand expanded, but employment sank to a three-year low. Businesses stepped up purchasing, inventories of raw materials grew marginally, logistics picked up, prices continued to slump, and manufacturers' optimism wavered."

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2378; (P) 1.2411; (R1) 1.2474; More...

GBP/USD's break of 1.2468 minor resistance today argues that corrective pull back from 1.2678 has completed at 1.2306. Intraday bias is back on the upside for retesting 1.2678 high next. But strong resistance could be seen there to limit upside on the first attempt. Meanwhile, break of 1.2306 will resume the correction towards 1.1801 cluster support (38.2% retracement of 1.0351 to 1.2678 at 1.1789).

In the bigger picture, as long as 1.1801 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.1801 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Capital Spending Q1 | 11.00% | 5.50% | 7.70% | |

| 00:30 | JPY | Manufacturing PMI May F | 50.6 | 50.8 | 50.8 | |

| 01:30 | AUD | Private Capital Expenditure Q1 | 2.40% | 1.10% | 2.20% | 3.00% |

| 01:45 | CNY | Caixin Manufacturing PMI May | 50.9 | 49.5 | ||

| 06:00 | CHF | Trade Balance (CHF) Apr | 2.6B | 3.73B | 4.53B | |

| 06:00 | EUR | Germany Retail Sales M/M Apr | 0.80% | 0.90% | -2.40% | -2.20% |

| 07:30 | CHF | Manufacturing PMI May | 43.2 | 44.5 | 45.3 | |

| 07:45 | EUR | Italy Manufacturing PMI May | 45.9 | 45.8 | 46.8 | |

| 07:50 | EUR | France Manufacturing PMI May F | 45.7 | 46.1 | 46.1 | |

| 07:55 | EUR | Germany Manufacturing PMI May F | 43.2 | 42.9 | 42.9 | |

| 08:00 | EUR | Eurozone Manufacturing PMI May F | 44.8 | 44.6 | 44.6 | |

| 08:30 | GBP | Manufacturing PMI May F | 47.1 | 46.9 | 46.9 | |

| 08:30 | GBP | Mortgage Approvals Apr | 49K | 54K | 52K | 51K |

| 08:30 | GBP | M4 Money Supply M/M Apr | 0.00% | -0.20% | -0.60% | |

| 09:00 | EUR | Eurozone Unemployment Rate Apr | 6.50% | 6.50% | 6.50% | |

| 09:00 | EUR | Eurozone CPI Y/Y May P | 6.10% | 6.30% | 7.00% | |

| 09:00 | EUR | Eurozone CPI Core May P | 5.30% | 5.50% | 5.60% | |

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 11:30 | USD | Challenger Job Cuts May | 286.70% | 175.90% | ||

| 12:15 | USD | ADP Employment Change May | 278K | 167K | 296K | 291K |

| 12:30 | USD | Initial Jobless Claims (May 26) | 232K | 236K | 229K | |

| 12:30 | USD | Nonfarm Productivity Q1 | -2.10% | -2.70% | -2.70% | |

| 12:30 | USD | Unit Labor Costs Q1 | 4.20% | 6.30% | 6.30% | |

| 13:30 | CAD | Manufacturing PMI May | 50.2 | |||

| 13:45 | USD | Manufacturing PMI May F | 48.5 | 48.5 | ||

| 14:00 | USD | ISM Manufacturing PMI May | 47 | 47.1 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid May | 52.5 | 53.2 | ||

| 14:00 | USD | ISM Manufacturing Employment Index May | 50.2 | |||

| 14:00 | USD | Construction Spending M/M Apr | 0.10% | 0.30% | ||

| 14:30 | USD | Natural Gas Storage | 106B | 96B | ||

| 15:00 | USD | Crude Oil Inventories | -1.4M | -12.5M |