Sample Category Title

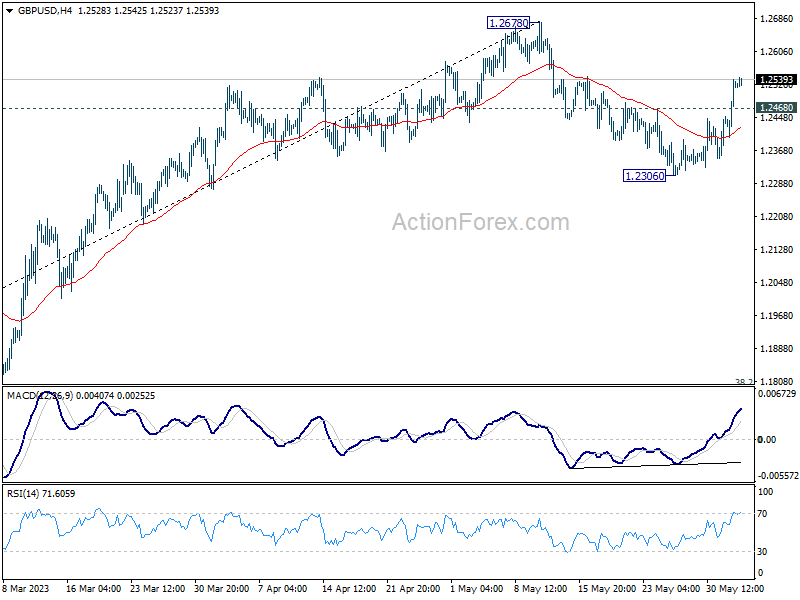

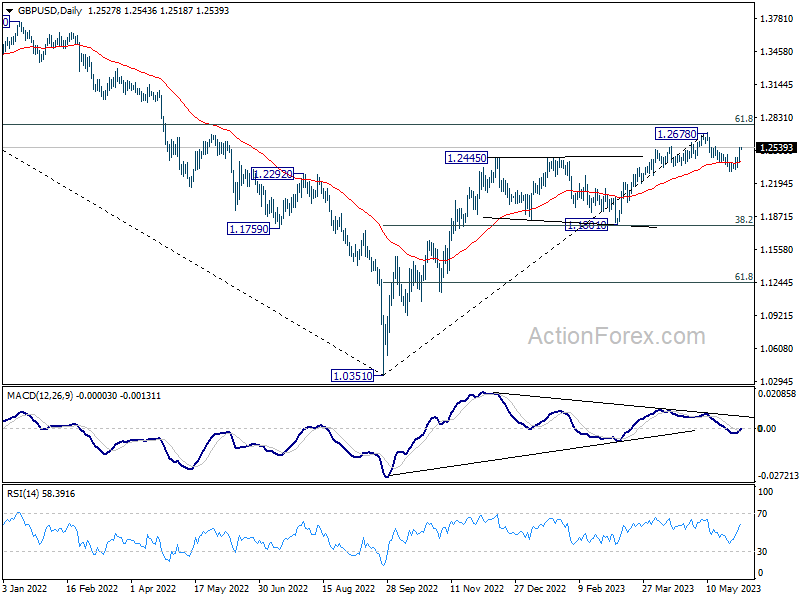

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2438; (P) 1.2489; (R1) 1.2577; More...

Intraday bias in GBP/USD remains mildly on the upside for the moment. Rebound from 1.2306 is in progress for retesting 1.2678 high. Decisive break there would resume larger up trend from 1.0351 to 1.2759 fibonacci level. Meanwhile, break of 1.2306 will resume the correction towards 1.1801 cluster support (38.2% retracement of 1.0351 to 1.2678 at 1.1789)

In the bigger picture, as long as 1.1801 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.1801 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.

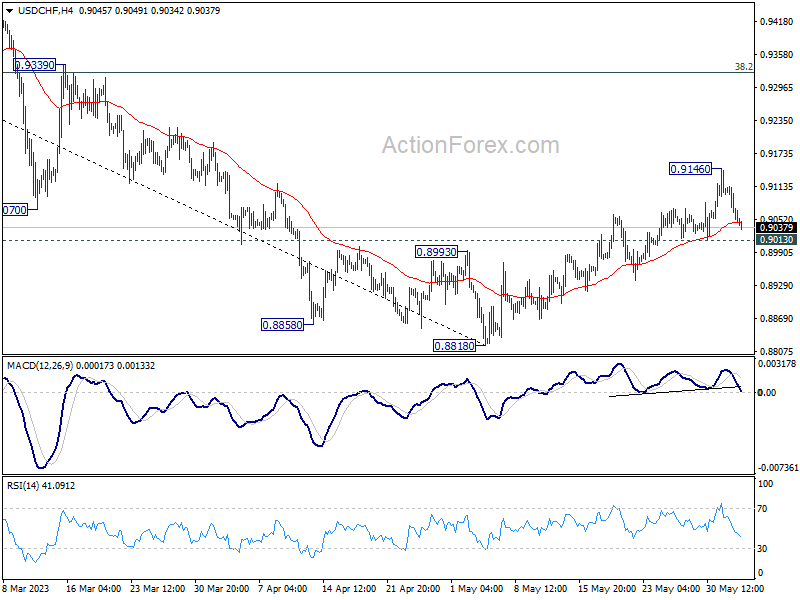

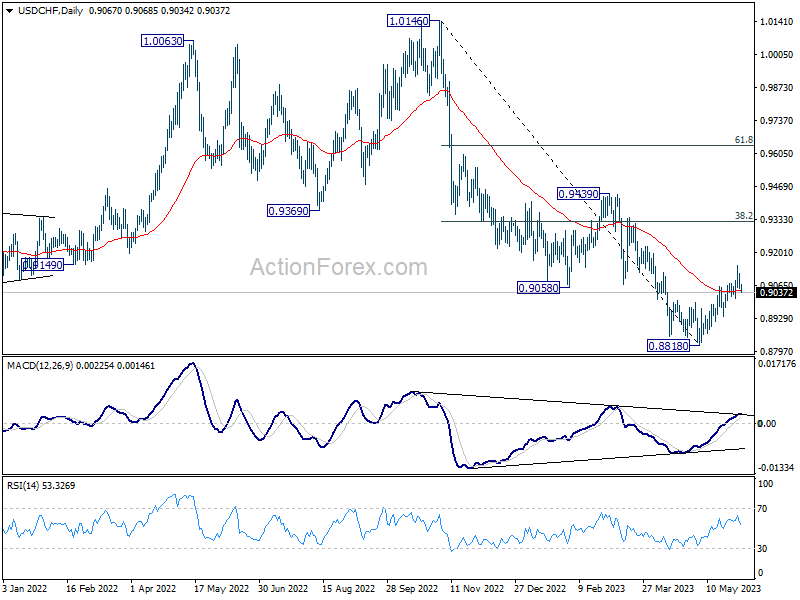

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9034; (P) 0.9076; (R1) 0.9097; More...

Intraday bias in USD/CHF remains neutral for the moment. break of 0.9146 will resume the rebound from 0.8818 to 38.2% retracement of 1.0146 to 0.8818 at 0.9325. On the downside, however, break of 0.9013 will turn bias back to the downside for retesting 0.8818 low instead.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high). So, downside should be contained by 0.8756 to bring reversal. Sustained break of 0.9058 support turned resistance will be the first sign of medium term bottoming. However, decisive break of 0.8756 will carry larger bearish implications.

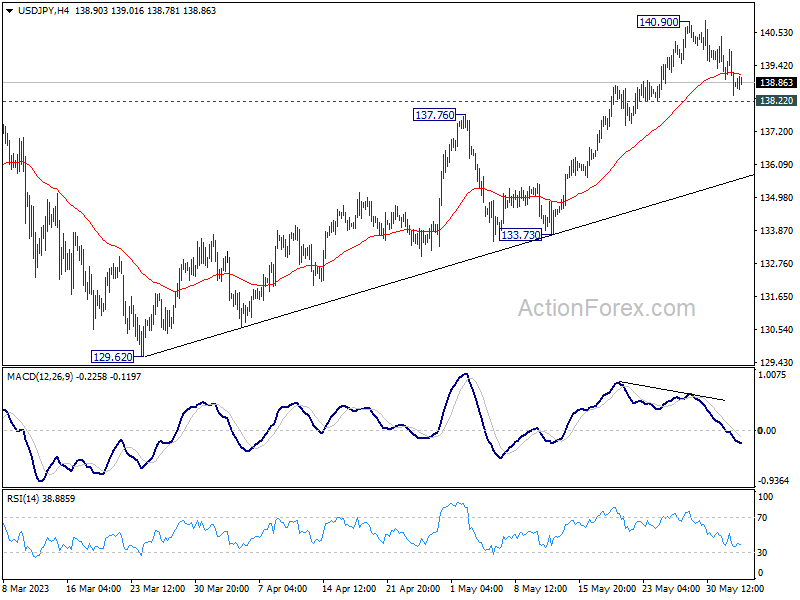

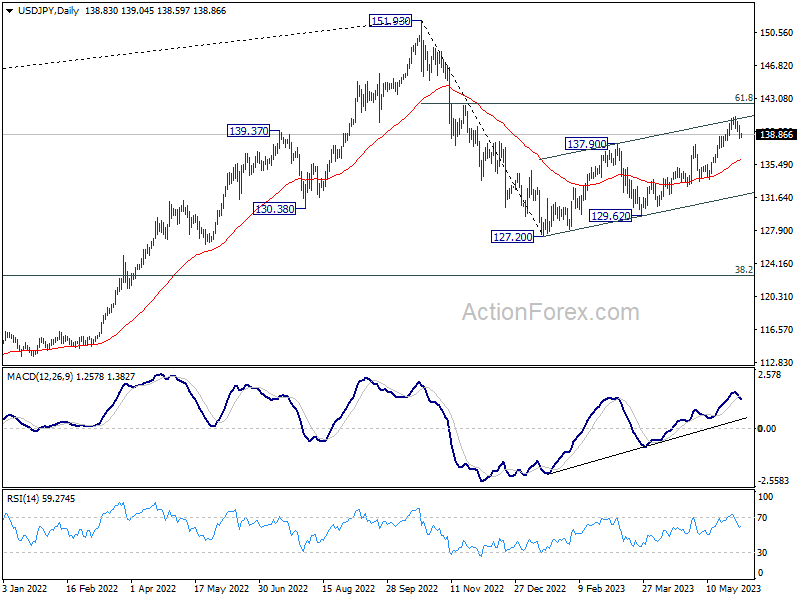

USD/JPY Daily Outlook

Daily Pivots: (S1) 138.19; (P) 139.07; (R1) 139.68; More...

USD/JPY is staying in range of 138.22/140.90 and intraday bias remains neutral for the moment. Downside of retreat should be contained above 138.22 support to bring another rally. Break of 140.90 will resume larger rise from 127.20 to 142.48 fibonacci level. However, considering bearish divergence condition in 4 hour MACD, break of 138.22 will confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 135.98).

In the bigger picture, rise from 127.20 is seen as the second leg of the corrective pattern from 151.93 high. Stronger rally would be seen to 61.8% retracement of 151.93 to 127.20 at 136.34. Sustained break there will pave the way back to retest 151.93. On the downside, however, break of 133.73 support will argue that the pattern could have started the third leg through 127.20 low.

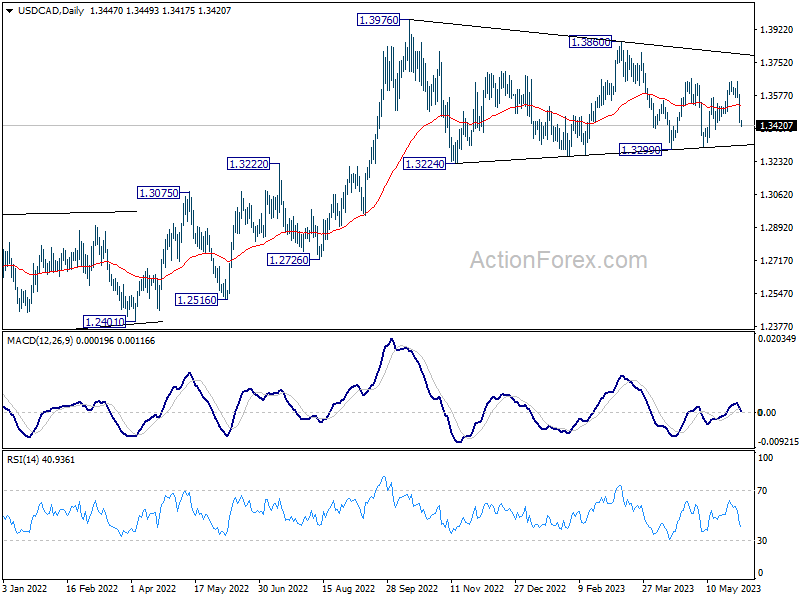

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3395; (P) 1.3490; (R1) 1.3543; More....

Intraday bias in USD/CAD is back on the downside with break of 1.3483 minor support. Deeper fall would be seen but downside should be contained by 1.3299 support to bring rebound. Overall, price actions from 1.3976 are seen as a triangle consolidation pattern, and more sideway trading is expected. Nevertheless, sustained break of 1.3229 will dampen this view and turn near term outlook bearish.

In the bigger picture, rise from 1.2005 (2021 low) is expected to resume through 1.3976 after consolidation from there completes. On decisive break of 1.3976, next target will be 1.4667/89 long term resistance zone. This will remain the favored case as long as 38.2% retracement of 1.2005 to 1.3976 at 1.3233 holds.

US Won’t Default, and Fed Will Likely Skip

The US Senate approved legislation to suspend the US debt ceiling through 2024, meaning that the US won’t default by next Monday. The bill now goes to President Joe Biden who will… sign it!

US yields fell and the dollar tanked on optimism that the US’ debt ceiling theater is over, and despite a big beat on ADP print.

The US economy added 278K new private jobs in May, versus 170K expected by analysts. But Challenger Job Cuts data revealed more than 80K layoffs in May, and the layoffs are up by more than 280% year-on-year. The tech layoffs jumped to the highest levels since the 2000 tech bubble since the beginning of the year, giving contradictory signals to higher JOLTS and solid ADP read.

Today, the official jobs data is expected to print 180K new nonfarm job additions, a slightly moderating wages growth, and a slight uptick in unemployment from 3.4% to 3.5%. But over the past year, the NFP prints tended to surprise to the upside, and by big chunks at some months. The last time the US printed a NFP figure below 200K was back in October 2021. And over the past year, the yearly NFP average was around 327K.

Therefore, yes, seeing a softer NFP figure, falling wages growth and higher unemployment ideally with a higher participation rate is what the Federal Reserve (Fed) needs to pause hiking. But the loosening in the US jobs market hasn’t materialized just yet.

ISM in the red

Yesterday’s strong ADP report was accompanied by a set of soft ISM figures. The ISM manufacturing PMI showed fastening contraction and more rapidly falling new orders in May, although the employment remained in the expansion zone (!)… As such, the third day retreat in the US 2-year yield to around 4.35% was certainly also driven by soft ISM figures – and not only by US debt ceiling resolution. Activity on Fed funds futures hints at an increased possibility of a rate hike skip at June meeting. The probability of a no rate hike is now at around 74%.

The US dollar fell sharply yesterday, pushing the EURUSD back above the 23.6% retracement level on September to April rally. While I am not confident that we will see soft US jobs data, a softer-than-expected figure could encourage a further recovery.

In the Eurozone, even though the latest inflation figures came in highly encouraging – with the CPI flash estimate falling to 6.1% versus 7% printed a month earlier and core CPI retreating to 5.3% - the European Central Bank (ECB) Chief Christine Lagarde didn’t see it as ‘evidence’ of peaking inflation and pledged to hike rates further. The decidedly hawkish ECB versus the rising voices hinting at a pause in Fed tightening in June could open an opportunity window for the EUR bulls to carry the pair back above the 200-DMA, which currently stands around the 1.0810 level.

And beyond the Fed’s June meeting? Well, we will see. The Fed clearly sends a message that they no longer see urgency in hiking the rates, while also letting investors know that their job fighting inflation is not done just yet. That’s a way of managing market expectations: pausing rate hikes, without however letting the market conditions loosen due to excess dovish speculation.

S&P 500 and Russell 200 tell different stories

Optimism regarding the US debt ceiling deal, and the falling yields sent the S&P500 1% up yesterday, Nasdaq jumped around 1.30%.

- The US debt ceiling crisis led to an accidental liquidity support,

- The banking crisis increased haven flows to Big Tech companies,

- The AI-craze attracted big inflows to Big Tech and,

- Softer US yields boosted the tech stock valuations.

As a result, Apple is up by around 45% since the start of the year, Alphabet rallied almost 50%, Microsoft and Amazon are both up by more than 50%, while Tesla more than doubled its price and Meta made an impressive U-turn. The stock price is up by 124% since the start of this year and more than 200% since the November dip. I am saying this because, as a result, the major US indices have been extremely biased by the Big Tech rally since the beginning of the year.

But without their contribution, the S&P500 would be up by just around 1.5% and would be much more vulnerable to … the tightening credit conditions, for example, due to the banking stress.

And if we compare the S&P500 to Russell 2000, we could clearly see that the recovery following the bank-stress selloff hasn’t been on the menu for small US stocks. On the contrary, the Russell 2000 index recorded a nice rally in tandem with the S&P500 stocks until the bank crisis, sold off along with the big stocks during the bank stress, but never recovered since then. The latter is proof that investors could be blindsided regarding the health of the US economy, if they only relied on the dynamics of the major US indices.

In this respect, Macy’s was one of the latest US retailers to release results yesterday, and the results were mixed. Sales tumbled below pre-pandemic levels and the company lowered its yearly forecast. However, Macy’s beat profit expectations, which helped the stock to recover from an initial 12% slump. But profits fell from $286 mio to $155 mio compared to a year earlier. So, it was a profit beat, yes, but on profits that almost halved in a year!

After EA Inflation, Focus Turns to the US Labour Market Report

Market movers today

Today, the traditional US Jobs Report will round of an eventful week of macro data. Consensus is looking for moderating non-farm payrolls growth (190k; from 253k), but we see some upside risks after most leading employment indicators and yesterday's ADP report have surprised to the upside.

The US congress is nearing the finish line with the debt ceiling discussions. We expect the Senate to pass the deal before Monday, when the Treasury has warned about a potential risk of a default.

The 60 second overview

Euro area inflation print released yesterday confirmed the disinflationary prints from country releases in previous days. HICP came in at 6.1%, a sharp drop from 7% in April. Core inflation also slowed more than anticipated to 5.3% from 5.6% in April. For now, the introduction of the EUR49m German transport ticket is likely to have been a key reason for this decline and hence we should be careful interpreting this core print. A detailed look at the breakdown showed that services eased to 5.0% from 5.2% in April. The non-energy industrial goods continued its decline from the peak reached last year and printed at 5.8% (from 6.20% in April). Food eased at 12.5% from 13.5% in April. Energy contributed again with a negative print of -1.7% yoy.

Sweden PMI print comparably low at 40.6. All sub-indices weighed, especially orders. Even export orders dropped sharply to 37.5 (44.9) - despite the weaker SEK one might add. This increases the dilemma for the Riksbank not least given that the domestic economy is already down for the count (households and housing), while on the other hand inflation is too high and SEK weak.

US debt ceiling discussion is coming to an end for now as the Senate approved the legislation, which means that now only Biden needs to sign it off.

US data, with ISM coming in weaker and unit labour costs lower than anticipated, were a catalyst for a minor reaction in markets yesterday. The particularly surprising part of the ISM release was the significant drop in prices paid to 44.2, well below the consensus of 52.3, which now means that we may start to talk about falling goods prices.

Equities: Global equities higher yesterday in broad based gains and a risk-on tone with cyclicals leading the advances. Macro data as always overwhelming the first day of a new month and we honestly admit we would not have been surprised if equity markets had looked very different based on the data releases.

In US Dow +0.5%, S&P 500 +1.0%, Nasdaq +1.3% and Russell 2000 +1.1%. Asian markets are continuing the positive tone this morning. China (Hang Seng) in strong advances after a period where it has underperformed much of the rest of the world. Performance in China today looks more like a technical one after the long sell-off rather than driven by new information or data releases. Futures are higher in Europe and US.

FI: It was a tale of two stories yesterday. The European inflation print did not change the market pricing, which was broadly unchanged until the US data release led to a lower yield environment. Jobless claims, unit labour costs and ISM (in particular prices paid), initiated a minor rally in the belly of the curve. The front end and long end respectively were broadly unchanged on the day. Markets are still focusing on two additional hikes from the ECB, while Fed's Harker (voter) said that they should skip this June meeting for rate hikes. Yesterday afternoon Villeroy said that the remaining hikes will be 'relatively marginal'.

FX: The weaker-than-expected ISM data yesterday shifted money market pricing back towards a Fed pause at the June meeting, and sent both stocks and bonds higher on the day. The USD however weakened broadly, with EUR/USD rising close to a full figure on the day. Scandi FX gave back some of Wednesday's gains in volatile trading. EUR/GBP posted a new 6M low and we expect Sterling momentum to continue in the near-term.

Credit: It was an active day in the EUR corporate segment with issuance from Italgas, RCI Banque, Statnett and Unilever, while in financials BFCM placed a dual-tranche senior preferred transaction. CDS indices tightened with iTraxx Main closing at 79bp (-3bp) and Xover at 424bp (-10bp).

Nordic macro

The Norwegian labour market remains tight but is showing some signs of weakening. New job openings are down, and the number of jobless has begun to edge up. Short-term unemployment too has started to climb, which is often an indication of rising unemployment further ahead. We expect this trend to have continued in May, but with the seasonally adjusted jobless rate unchanged at 1.8%.

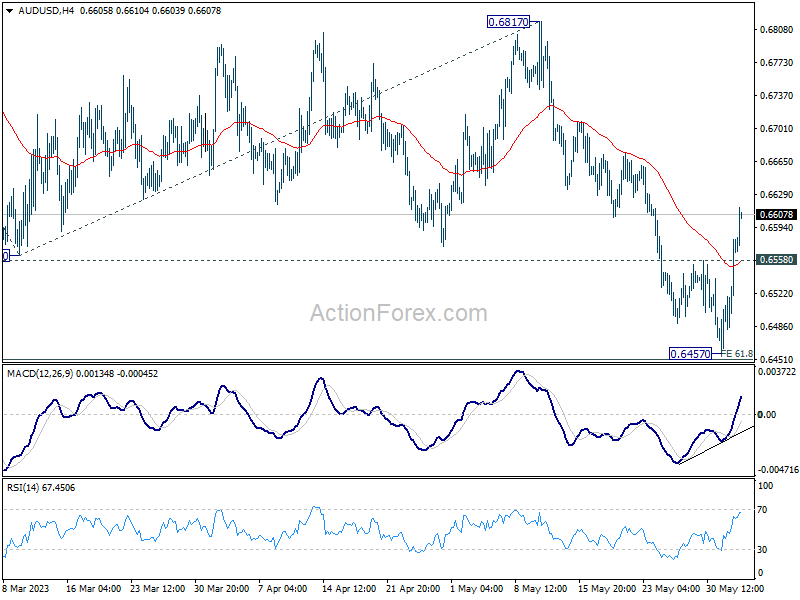

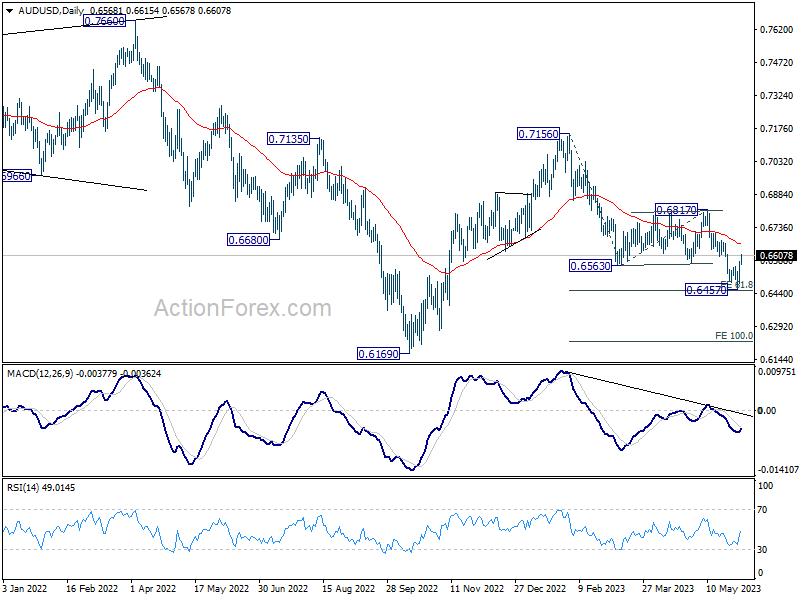

AUD/USD Daily Report

Daily Pivots: (S1) 0.6511; (P) 0.6547; (R1) 0.6608; More...

AUD/USD's strong break of 0.6558 minor resistance confirm short term bottoming at 0.6457, just ahead of 61.8% projection of 0.7156 to 0.6563 from 0.6817 at 0.6451. Intraday bias is back on the upside for 55 D EMA (now at 0.6659). Sustained break there will target 0.6817 resistance next. Nevertheless, rejection by 55 D EMA will keep near term outlook bearish. Firm break of 0.6451 will resume the fall from 0.7156 to 100% projection at 0.6224.

In the bigger picture, rejection by 55 W EMA (now at 0.6822) keeps medium term outlook bearish. Current development suggests that down trend from 0.8006 (2021 high) is possibly still in progress. Retest of 0.6169 (2022 low) should be seen next. Firm break there will confirm down trend resumption. For now, this will remain the favored case as long as 0.6817 resistance holds.

Dollar Pullback Continues; Focus Turns to Non-Farm Payroll Data

Dollar is extending the near term pull back in Asian session today, driven by a combination of factors including a risk-on market sentiment, falling Treasury yields, and growing market expectations of a Federal Reserve "skip" in June. However, the greenback, along with other currencies, will be closely watching today's non-farm payroll data for further direction. As it stands, Swiss Franc is trailing Dollar as the week's second worst performer, followed by Euro. On the other hand, Sterling is actually the quiet star of the week, followed by Aussie and Loonie. Yen is currently mixed as near term consolidation extends.

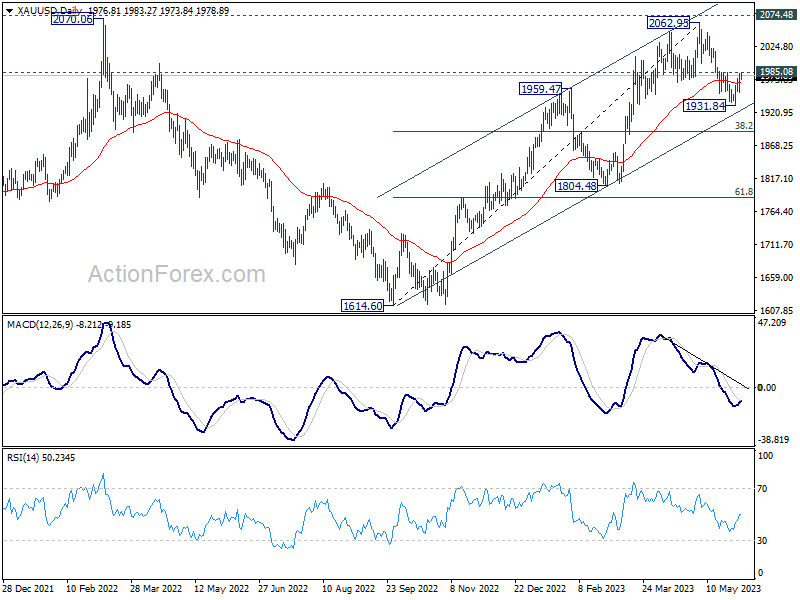

Technically, Gold is now eyeing 1985.08 minor resistance with current rebound. Break there will indicate that a short term bottoming is formed at 1931.84. More importantly, such development will keep the medium term rising channel intact. That is, rise from 1614.60 is indeed not over yet. Retest of 2062.95 or even 2074.48 record high could be seen soon, which could also correspond to near term selloff in Dollar.

In Asia, at the time of writing, Nikkei is up 1.03%. Hong Kong HSI is up 3.79%. China Shanghai SSE is up 0.78%. Singapore Strait Times is up 0.24%. 10-year JGB yield is down -0.0074 at 0.413. Overnight, DOW rose 0.47%. S&P 500 rose 0.99%. NASDAQ rose 1.28%. 10-year yield dropped -0.029 to 3.608.

Fed Harker: We are clearly in restrictive, we can sit there for a while

Philadelphia Fed President Patrick Harker recommended a pause in interest rate hikes at the upcoming FOMC meeting, stating. "It's time to at least hit the stop button for one meeting and see how it goes," he said yesterday.

Harker also noted, "I think we are at the point, or very close to the point now, where we are clearly in restrictive territory, and we can sit there for a while," he explained. "We don't have to keep moving rates up, and then have to reverse course quickly."

Looking ahead, Harker expects the US economy to grow less than 1% this year, and anticipates unemployment rate, currently at 3.4%, to increase to around 4.4%. Additionally, he forecasts a decrease in inflation to 3.5% this year and 2.5% next year, predicting it to reach Fed's 2% target only by 2025.

BoJ Ueda: No time frame to achieve inflation target, but not so long as 10 years

In a parliamentary address today, BoJ Governor Kazuo Ueda said "The time it takes for the impact of monetary policy to appear on the economy could move around a lot depending on circumstances."

"We therefore do not have any time frame in mind" in achieving the inflation target, he added.

"Having said that, our baseline view is that it won't take so long as over 10 years. We'll still seek to hit the target at the earliest date possible," he remarked.

Ueda reiterated that the Bank of Japan's purchases of Real Estate Investment Trusts (REITs) form part of their expansive monetary easing strategy. He noted, "We are conducting the purchases (of REITs) as part of our massive monetary easing program. Given it will take more time to achieve our price target, we will maintain the easy policy."

US non-farm payroll in spotlight, NASDAQ presses key resistance

Today, market watchers are turning their attention to US non-farm payroll report, a key indicator of the health of the American labor market. Economists are forecasting job growth of around 180k in May, with the unemployment rate predicted to slightly increase from 3.4% to 3.5%. Meanwhile, average hourly earnings are expected to continue a trend of robust growth with another 0.3% mom rise.

Looking at some related economic data, ISM manufacturing employment index showed a modest rise from 50.2 to 51.4, while ADP private job data indicated a strong increase of 278k. The four-week moving average of initial jobless claims saw a slight dip from 239k to 230k. All these numbers suggest a job market that remains steady, showing no significant signs of weakening.

In terms of monetary policy, Fed funds futures are currently pricing in 76% probability that Fed will opt to "skip" a rate hike at the upcoming FOMC meeting on June 14. Nevertheless, there is still around a 60% chance of another 25bps increase in June to a range of 5.25-5.50%. Today's data could significantly alter this picture if it brings any surprises.

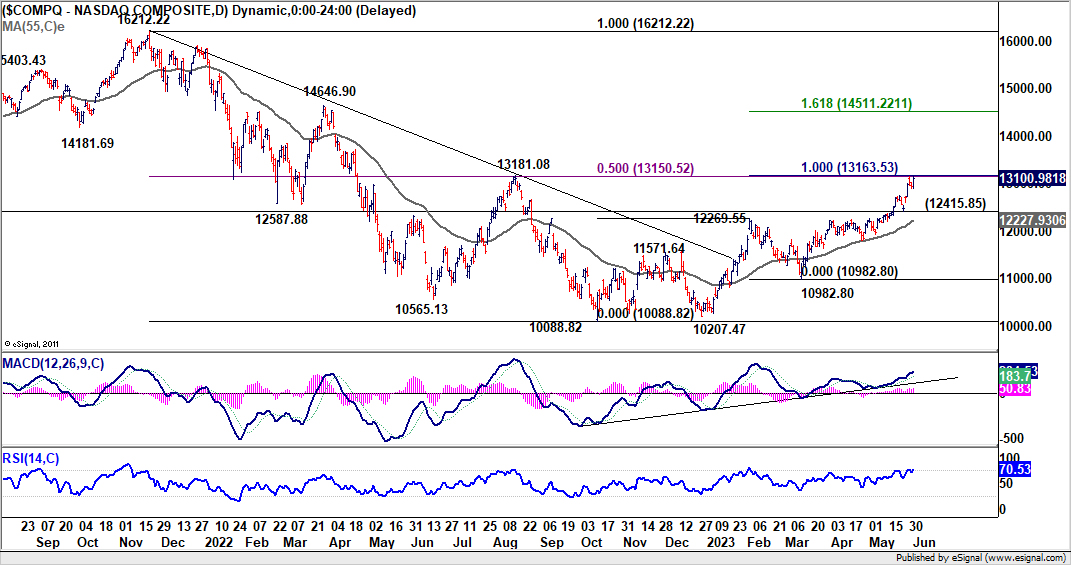

Over in the equity markets, NASDAQ is once again testing a crucial cluster resistance level at 13181.08, following a brief retreat earlier this week. The level represents 100% projection of 10088.82 to 12269.55 from 10982.80 at 13163.53, as well as 50% retracement of 16212.22 to 10088.82 at 13150.52.

Decisive breakthrough above this 13150/80 range would confirm underlying medium term bullish momentum in NASDAQ, potentially sparking upward acceleration towards 161.8% projection at 14511.22. Let's see how NASDAQ reacts to today's data.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6511; (P) 0.6547; (R1) 0.6608; More...

AUD/USD's strong break of 0.6558 minor resistance confirm short term bottoming at 0.6457, just ahead of 61.8% projection of 0.7156 to 0.6563 from 0.6817 at 0.6451. Intraday bias is back on the upside for 55 D EMA (now at 0.6659). Sustained break there will target 0.6817 resistance next. Nevertheless, rejection by 55 D EMA will keep near term outlook bearish. Firm break of 0.6451 will resume the fall from 0.7156 to 100% projection at 0.6224.

In the bigger picture, rejection by 55 W EMA (now at 0.6822) keeps medium term outlook bearish. Current development suggests that down trend from 0.8006 (2021 high) is possibly still in progress. Retest of 0.6169 (2022 low) should be seen next. Firm break there will confirm down trend resumption. For now, this will remain the favored case as long as 0.6817 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Terms of Trade Index Q1 | -1.50% | -1.10% | 1.80% | 1.50% |

| 23:50 | JPY | Monetary Base Y/Y May | -1.10% | -1.40% | -1.70% | |

| 06:45 | EUR | France Industrial Output M/M Apr | 0.30% | -1.10% | ||

| 12:30 | USD | Nonfarm Payrolls May | 180K | 253K | ||

| 12:30 | USD | Unemployment Rate May | 3.50% | 3.40% | ||

| 12:30 | USD | Average Hourly Earnings M/M May | 0.30% | 0.50% |

US non-farm payroll in spotlight, NASDAQ presses key resistance

Main focus now turns to US non-farm payroll report today. Markets are expecting 180k job growth in May. Unemployment rate is expected to tick up from 3.4% to 3.5%. Meanwhile, average hourly earnings are expected to show another month of robust 0.3% mom growth.

Looking at some related economic data, ISM manufacturing employment rose slightly from 50.2 to 51.4, but ISM services data is not released yet. ADP private job data showed strong 278k growth. Four-week moving average of initial jobless claims fell slightly from 239k to 230k. There is nothing in these data that show significant loosening in the job market, not to mention weakness.

Fed funds futures are now pricing in 76% chance of a "skip" at upcoming FOMC meeting on June 14. Meanwhile, there is around 60% chance of another 25bps hike in June to 5.25-5.50%. The landscape could change quite notably if there is surprises in today's data.

NASDAQ is back pressing key cluster resistance at 13181.08 after brief retreat earlier in the week. The level represents 100% projection of 10088.82 to 12269.55 from 10982.80 at 13163.53, as well as 50% retracement of 16212.22 to 10088.82 at 13150.52.

Decisive break of this 13150/80 handle will confirm underlying bullish momentum in NASDAQ, and could prompt upside acceleration to 161.8% projection at 14511.22. Let's see how NASDAQ reacts to today's data.

BoJ Ueda: No time frame to achieve inflation target, but not so long as 10 years

In a parliamentary address today, BoJ Governor Kazuo Ueda said "The time it takes for the impact of monetary policy to appear on the economy could move around a lot depending on circumstances."

"We therefore do not have any time frame in mind" in achieving the inflation target, he added.

"Having said that, our baseline view is that it won't take so long as over 10 years. We'll still seek to hit the target at the earliest date possible," he remarked.

Ueda reiterated that the Bank of Japan's purchases of Real Estate Investment Trusts (REITs) form part of their expansive monetary easing strategy. He noted, "We are conducting the purchases (of REITs) as part of our massive monetary easing program. Given it will take more time to achieve our price target, we will maintain the easy policy."