Sample Category Title

Summary 6/5 – 6/9

Monday, Jun 5, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | AUD | TD Securities Inflation M/M May | 0.20% | |

| 01:30 | AUD | Company Gross Operating Profits Q/Q Q1 | 2.10% | 10.60% |

| 01:45 | CNY | Caixin Services PMI May | 55.2 | 56.4 |

| 06:00 | EUR | Germany Trade Balance (EUR) Apr | 16.1B | 16.7B |

| 06:30 | CHF | CPI M/M May | 0.40% | 0.00% |

| 06:30 | CHF | CPI Y/Y May | 2.10% | 2.60% |

| 07:45 | EUR | Italy Services PMI May | 53.7 | 57.6 |

| 07:50 | EUR | France Services PMI May F | 52.8 | 52.8 |

| 07:55 | EUR | Germany Services PMI May F | 57.8 | 57.8 |

| 08:00 | EUR | Eurozone Services PMI May F | 55.9 | 55.9 |

| 08:30 | EUR | Eurozone Sentix Investor Confidence Jun | -9.2 | -13.1 |

| 08:30 | GBP | Services PMI May F | 55.1 | 55.1 |

| 09:00 | EUR | Eurozone PPI M/M Apr | -2.70% | -1.60% |

| 09:00 | EUR | Eurozone PPI Y/Y Apr | 0.80% | 5.90% |

| 13:45 | USD | Services PMI May F | 55.1 | 55.1 |

| 14:00 | USD | ISM Services PMI May | 52.6 | 51.9 |

| 14:00 | USD | Factory Orders M/M Apr | 0.80% | 0.90% |

| 23:01 | GBP | BRC Like-For-Like Retail Sales Y/Y May | 5.20% | |

| 23:30 | JPY | Labor Cash Earnings Y/Y Apr | 1.90% | 0.80% |

| 23:30 | JPY | Overall Household Spending Y/Y Apr | -2.30% | -1.90% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | AUD | TD Securities Inflation M/M May | |

| Forecast: | Previous: 0.20% | ||

| 01:30 | AUD | Company Gross Operating Profits Q/Q Q1 | |

| Forecast: 2.10% | Previous: 10.60% | ||

| 01:45 | CNY | Caixin Services PMI May | |

| Forecast: 55.2 | Previous: 56.4 | ||

| 06:00 | EUR | Germany Trade Balance (EUR) Apr | |

| Forecast: 16.1B | Previous: 16.7B | ||

| 06:30 | CHF | CPI M/M May | |

| Forecast: 0.40% | Previous: 0.00% | ||

| 06:30 | CHF | CPI Y/Y May | |

| Forecast: 2.10% | Previous: 2.60% | ||

| 07:45 | EUR | Italy Services PMI May | |

| Forecast: 53.7 | Previous: 57.6 | ||

| 07:50 | EUR | France Services PMI May F | |

| Forecast: 52.8 | Previous: 52.8 | ||

| 07:55 | EUR | Germany Services PMI May F | |

| Forecast: 57.8 | Previous: 57.8 | ||

| 08:00 | EUR | Eurozone Services PMI May F | |

| Forecast: 55.9 | Previous: 55.9 | ||

| 08:30 | EUR | Eurozone Sentix Investor Confidence Jun | |

| Forecast: -9.2 | Previous: -13.1 | ||

| 08:30 | GBP | Services PMI May F | |

| Forecast: 55.1 | Previous: 55.1 | ||

| 09:00 | EUR | Eurozone PPI M/M Apr | |

| Forecast: -2.70% | Previous: -1.60% | ||

| 09:00 | EUR | Eurozone PPI Y/Y Apr | |

| Forecast: 0.80% | Previous: 5.90% | ||

| 13:45 | USD | Services PMI May F | |

| Forecast: 55.1 | Previous: 55.1 | ||

| 14:00 | USD | ISM Services PMI May | |

| Forecast: 52.6 | Previous: 51.9 | ||

| 14:00 | USD | Factory Orders M/M Apr | |

| Forecast: 0.80% | Previous: 0.90% | ||

| 23:01 | GBP | BRC Like-For-Like Retail Sales Y/Y May | |

| Forecast: | Previous: 5.20% | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Apr | |

| Forecast: 1.90% | Previous: 0.80% | ||

| 23:30 | JPY | Overall Household Spending Y/Y Apr | |

| Forecast: -2.30% | Previous: -1.90% | ||

Tuesday, Jun 6, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Current Account (AUD) Q1 | 15.0B | 14.1B |

| 04:30 | AUD | RBA Interest Rate Decision | 3.85% | 3.85% |

| 06:00 | EUR | Germany Factory Orders M/M Apr | 3.80% | -10.70% |

| 08:30 | GBP | Construction PMI May | 50.9 | 51.1 |

| 09:00 | EUR | Eurozone Retail Sales M/M Apr | 0.20% | -1.20% |

| 12:30 | CAD | Building Permits M/M Apr | 0.20% | 11.30% |

| 14:00 | CAD | Ivey PMI May | 57.2 | 56.8 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Current Account (AUD) Q1 | |

| Forecast: 15.0B | Previous: 14.1B | ||

| 04:30 | AUD | RBA Interest Rate Decision | |

| Forecast: 3.85% | Previous: 3.85% | ||

| 06:00 | EUR | Germany Factory Orders M/M Apr | |

| Forecast: 3.80% | Previous: -10.70% | ||

| 08:30 | GBP | Construction PMI May | |

| Forecast: 50.9 | Previous: 51.1 | ||

| 09:00 | EUR | Eurozone Retail Sales M/M Apr | |

| Forecast: 0.20% | Previous: -1.20% | ||

| 12:30 | CAD | Building Permits M/M Apr | |

| Forecast: 0.20% | Previous: 11.30% | ||

| 14:00 | CAD | Ivey PMI May | |

| Forecast: 57.2 | Previous: 56.8 | ||

Wednesday, Jun 7, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | GDP Q/Q Q1 | 0.30% | 0.50% |

| 03:00 | CNY | Trade Balance (USD) May | 94.2B | 90.2B |

| 05:00 | JPY | Leading Economic Index Apr P | 98.30% | 97.50% |

| 05:00 | JPY | Coincident Index Apr P | 98.8 | |

| 05:45 | CHF | Unemployment Rate M/M May | 1.90% | 1.90% |

| 06:00 | EUR | Germany Industrial Production M/M Apr | 0.80% | -3.40% |

| 06:45 | EUR | France Trade Balance (EUR) Apr | -7.7B | -8.0B |

| 07:00 | CHF | Foreign Currency Reserves (CHF) May | 732B | |

| 08:00 | EUR | Italy Retail Sales M/M Apr | 0.40% | 0.00% |

| 12:30 | USD | Trade Balance (USD) Apr | -75.3B | -64.2B |

| 12:30 | CAD | Labor Productivity Q/Q Q1 | 0.00% | -0.50% |

| 12:30 | CAD | Trade Balance (CAD) Apr | 0.1B | 1.0B |

| 14:00 | CAD | BoC Interest Rate Decision | 4.50% | 4.50% |

| 14:30 | USD | Crude Oil Inventories | 4.5M | |

| 22:45 | NZD | Manufacturing Sales Q1 | -0.40% | |

| 23:01 | GBP | RICS Housing Price Balance May | -37% | -39% |

| 23:50 | JPY | GDP Q/Q Q1 F | 0.40% | 0.40% |

| 23:50 | JPY | GDP Deflator Y/Y Q1 F | 2.00% | 2.00% |

| 23:50 | JPY | Bank Lending Y/Y May | 3.20% | |

| 23:50 | JPY | Current Account (JPY) Apr | 1.38T | 1.01T |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | GDP Q/Q Q1 | |

| Forecast: 0.30% | Previous: 0.50% | ||

| 03:00 | CNY | Trade Balance (USD) May | |

| Forecast: 94.2B | Previous: 90.2B | ||

| 05:00 | JPY | Leading Economic Index Apr P | |

| Forecast: 98.30% | Previous: 97.50% | ||

| 05:00 | JPY | Coincident Index Apr P | |

| Forecast: | Previous: 98.8 | ||

| 05:45 | CHF | Unemployment Rate M/M May | |

| Forecast: 1.90% | Previous: 1.90% | ||

| 06:00 | EUR | Germany Industrial Production M/M Apr | |

| Forecast: 0.80% | Previous: -3.40% | ||

| 06:45 | EUR | France Trade Balance (EUR) Apr | |

| Forecast: -7.7B | Previous: -8.0B | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) May | |

| Forecast: | Previous: 732B | ||

| 08:00 | EUR | Italy Retail Sales M/M Apr | |

| Forecast: 0.40% | Previous: 0.00% | ||

| 12:30 | USD | Trade Balance (USD) Apr | |

| Forecast: -75.3B | Previous: -64.2B | ||

| 12:30 | CAD | Labor Productivity Q/Q Q1 | |

| Forecast: 0.00% | Previous: -0.50% | ||

| 12:30 | CAD | Trade Balance (CAD) Apr | |

| Forecast: 0.1B | Previous: 1.0B | ||

| 14:00 | CAD | BoC Interest Rate Decision | |

| Forecast: 4.50% | Previous: 4.50% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 4.5M | ||

| 22:45 | NZD | Manufacturing Sales Q1 | |

| Forecast: | Previous: -0.40% | ||

| 23:01 | GBP | RICS Housing Price Balance May | |

| Forecast: -37% | Previous: -39% | ||

| 23:50 | JPY | GDP Q/Q Q1 F | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 23:50 | JPY | GDP Deflator Y/Y Q1 F | |

| Forecast: 2.00% | Previous: 2.00% | ||

| 23:50 | JPY | Bank Lending Y/Y May | |

| Forecast: | Previous: 3.20% | ||

| 23:50 | JPY | Current Account (JPY) Apr | |

| Forecast: 1.38T | Previous: 1.01T | ||

Thursday, Jun 8, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) Apr | 14.0B | 15.27B |

| 05:00 | JPY | Eco Watchers Survey: Outlook May | 54.1 | 54.6 |

| 09:00 | EUR | Eurozone GDP Q/Q Q1 F | 0.00% | 0.10% |

| 09:00 | EUR | Eurozone Employment Change Q/Q Q1 F | 0.60% | 0.60% |

| 12:30 | USD | Initial Jobless Claims (Jun 2) | 235K | 232K |

| 14:00 | USD | Wholesale Inventories Apr F | -0.20% | -0.20% |

| 14:30 | USD | Natural Gas Storage | 110B | |

| 23:50 | JPY | Money Supply M2+CD Y/Y May | 2.50% | 2.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) Apr | |

| Forecast: 14.0B | Previous: 15.27B | ||

| 05:00 | JPY | Eco Watchers Survey: Outlook May | |

| Forecast: 54.1 | Previous: 54.6 | ||

| 09:00 | EUR | Eurozone GDP Q/Q Q1 F | |

| Forecast: 0.00% | Previous: 0.10% | ||

| 09:00 | EUR | Eurozone Employment Change Q/Q Q1 F | |

| Forecast: 0.60% | Previous: 0.60% | ||

| 12:30 | USD | Initial Jobless Claims (Jun 2) | |

| Forecast: 235K | Previous: 232K | ||

| 14:00 | USD | Wholesale Inventories Apr F | |

| Forecast: -0.20% | Previous: -0.20% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 110B | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y May | |

| Forecast: 2.50% | Previous: 2.50% | ||

Friday, Jun 9, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | CNY | CPI Y/Y May | 0.10% | 0.10% |

| 01:30 | CNY | PPI Y/Y May | -3.90% | -3.60% |

| 08:00 | EUR | Italy Industrial Output M/M Apr | 0.10% | -0.60% |

| 12:30 | CAD | Capacity Utilization Q1 | 82.20% | 81.70% |

| 12:30 | CAD | Net Change in Employment May | 41.4K | |

| 12:30 | CAD | Unemployment Rate May | 5.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | CNY | CPI Y/Y May | |

| Forecast: 0.10% | Previous: 0.10% | ||

| 01:30 | CNY | PPI Y/Y May | |

| Forecast: -3.90% | Previous: -3.60% | ||

| 08:00 | EUR | Italy Industrial Output M/M Apr | |

| Forecast: 0.10% | Previous: -0.60% | ||

| 12:30 | CAD | Capacity Utilization Q1 | |

| Forecast: 82.20% | Previous: 81.70% | ||

| 12:30 | CAD | Net Change in Employment May | |

| Forecast: | Previous: 41.4K | ||

| 12:30 | CAD | Unemployment Rate May | |

| Forecast: | Previous: 5.00% | ||

Week Ahead – RBA and BoC to Hold Rates But Might be Tempted to Hike, OPEC+ Meets

Policy decisions from the RBA and the Bank of Canada will be taking centre stage next week amid an otherwise light agenda. In the United States, the ISM services PMI will be the only top-tier release and now that Congress has averted a default by suspending the debt ceiling, the dollar might spend the week drifting lower. Before all that however, OPEC and non-OPEC countries will meet on Sunday to discuss whether to make further cuts to oil output.

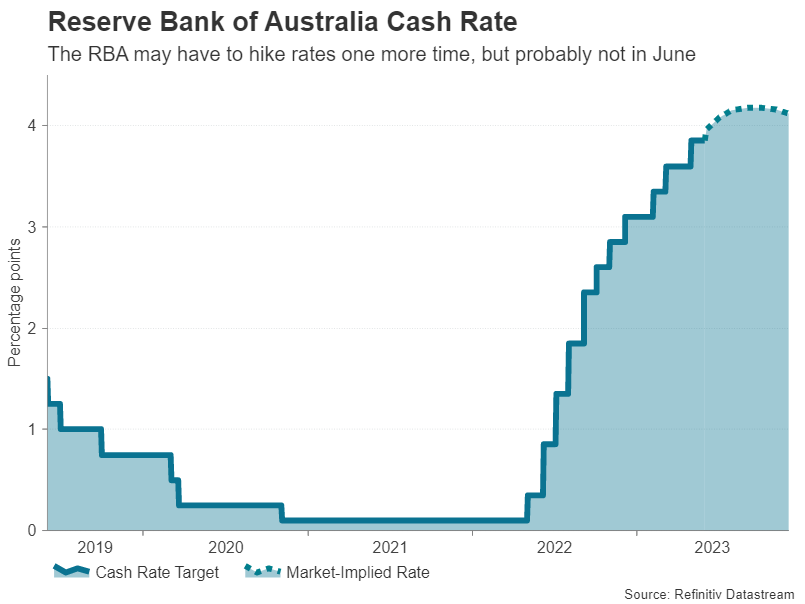

Will the RBA deliver another surprise hike?

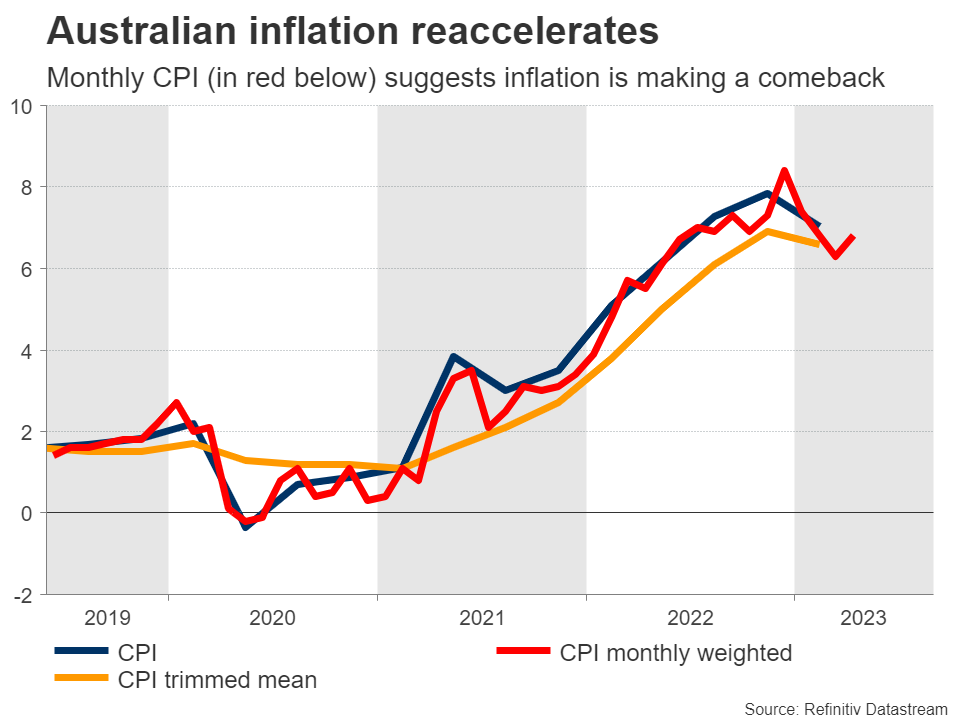

The Reserve Bank of Australia caught markets off guard when it hiked rates last month and there’s a risk that policymakers could again lift borrowing costs higher by 25 basis points when they hold their June meeting on Tuesday.

However, the economic data has been somewhat mixed lately so the RBA might decide to pause again to get a better picture of what is happening in the economy. The jobless rate edged up slightly in April and the flash PMIs pointed to a modest softening in economic activity in May. However, monthly inflation readings for April were hotter-than-expected.

First quarter GDP growth figures are due on Wednesday but might come too late for the RBA to fully factor the data into its decision. Also out on Wednesday is the AIG manufacturing index.

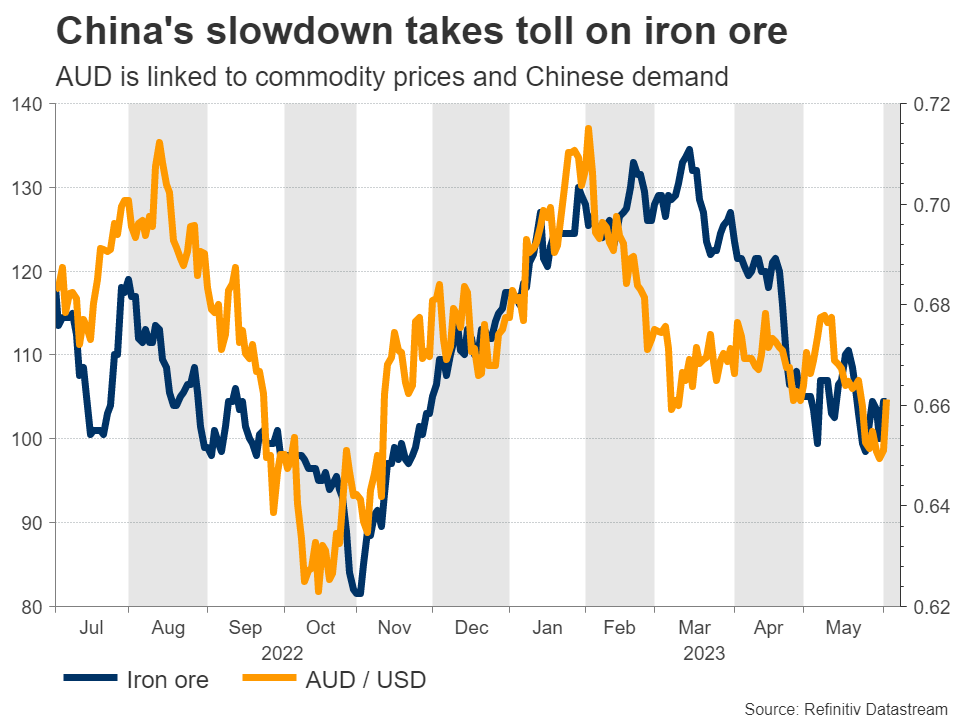

Another consideration for policymakers is the faltering recovery in China. The slowing demand for industrial metals and other resources from the world’s largest consumer of such commodities is bad news for Australian exporters whose number one market is China.

Hence, the RBA has more incentive to skip a hike, while maintaining a tightening bias and investors appear to be converging with this view as they’ve currently assigned around 55% probability of no change in June but a 25-bps hike is fully priced in for August.

The Australian dollar has tumbled to more than six-month lows versus its US counterpart but could receive support from a hawkish RBA. Aussie traders will also be keeping an eye on some Chinese indicators coming up next week.

The trade balance will be important on Wednesday to see how exports and imports fared in May, and on Friday, the latest consumer and producer price indices will provide fresh clues on the strength of domestic demand.

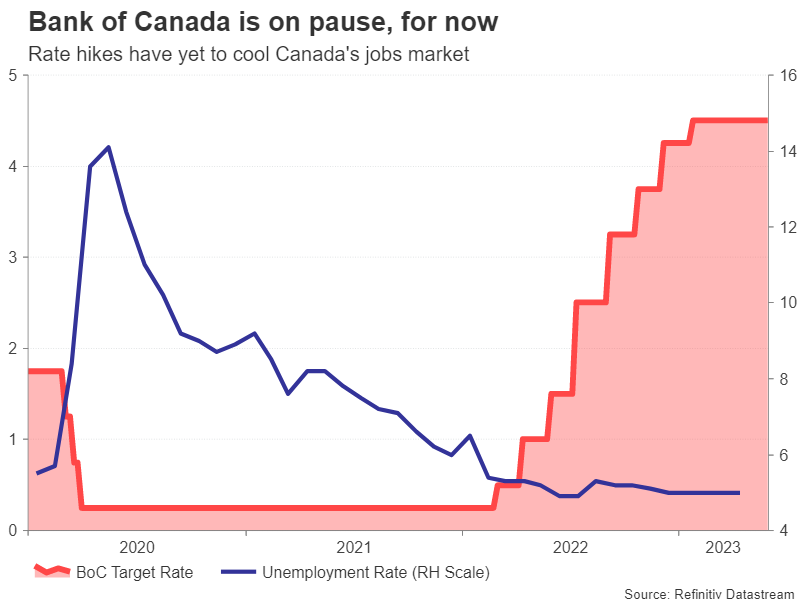

BoC may not be done with rate hikes

The Bank of Canada has been on pause since March but like the RBA, a rate hike is back on the table. The Canadian economy enjoyed a strong rebound in GDP growth in the first quarter, expanding by 0.8% q/q. The labour market is heating up again, while headline inflation unexpectedly accelerated in April.

However, underlying measures of inflation continued to decline and this may convince enough policymakers to stay on pause for another meeting in case the increase in headline CPI was a blip.

Markets are expecting the BoC to remain on hold at least until September before resuming its tightening cycle. But should policymakers display a strong inclination to hike soon, this would likely increase the focus on Friday’s employment report for May.

Another strong set of jobs numbers could bring rate hike bets forward, boosting the Canadian dollar.

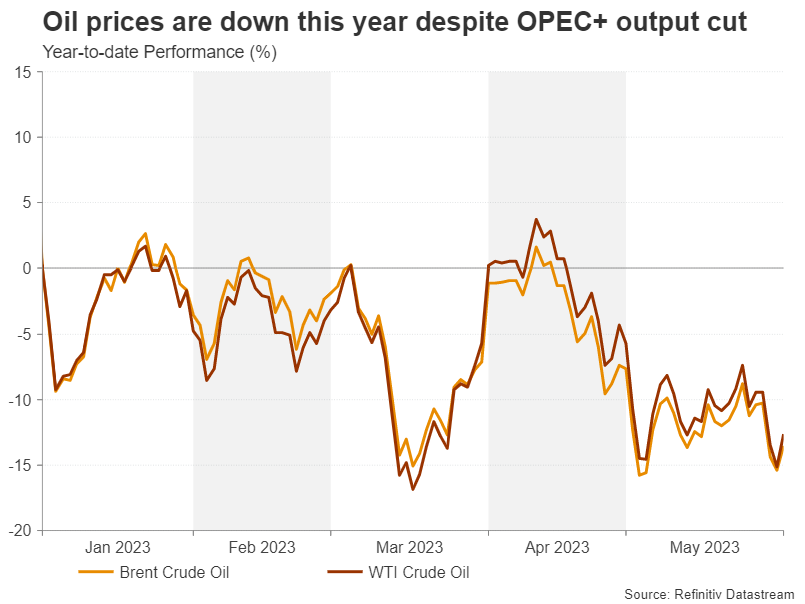

OPEC+ has a tough balance to strike

The oil-sensitive loonie will also be watching developments with OPEC+. The oil cartel will gather on Sunday to decide whether to follow up April’s surprise cut with a further reduction in output quotas. Russia has signalled it does not favour more cuts but the de-facto leader of the pact, Saudi Arabia, is more mindful about the lacklustre performance of oil prices over the last couple of months.

Indeed, Saudi Arabia is in a difficult position. By slashing production yet again it could end up conceding more market share to Russia, who is selling oil on the cheap to Asian countries that are able to evade Western sanctions slapped on Moscow over the war in Ukraine.

The other problem for the Saudis is that another output cut might send the message that oil producers are becoming more worried about the weakening outlook for oil prices and this could trigger the opposite reaction in oil futures, unless they decide on a very large reduction.

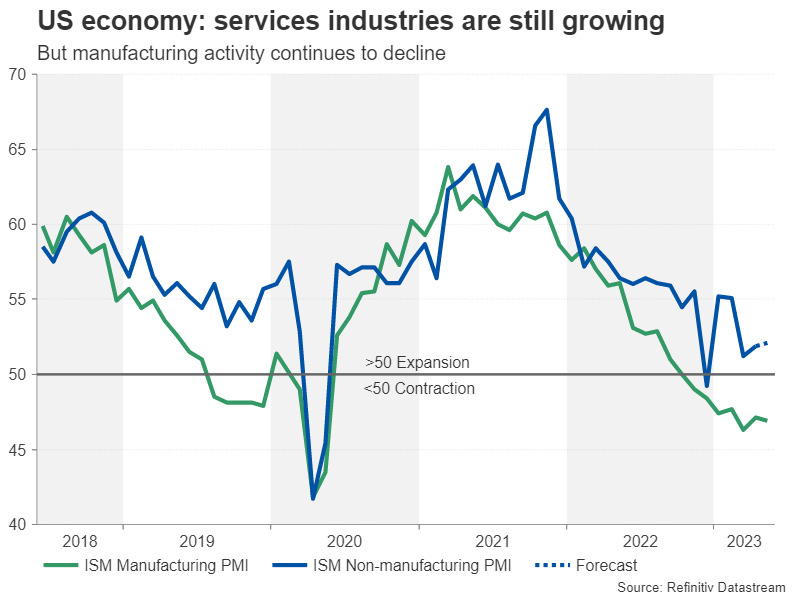

Quieter week looms for the dollar

In the United States, the main highlight is the ISM non-manufacturing PMI on Monday, and April factory orders due the same day might attract some interest too.

Although the American economy has lost some steam lately, it is far from being out of momentum and the ISM survey should offer a glance as to how things stood in May in the services sector.

Communication from the Fed has been rather conflicting heading into the June 14 FOMC decision, but more recently, it appears that the doves, likely led by Chair Powell himself, are building a case to sit out the next meeting.

There is still one more CPI report on the way before then, but the ISM PMI will have some significance given the growing divisions within the Fed.

If the odds start to shift again in favour of a June hike, the US dollar could find itself back on the front foot.

Can the yen extend its rebound?

One of the beneficiaries of the dollar’s recent setback has been the Japanese yen, which is recovering from six-month lows. Next week’s data out of Japan are unlikely to have too much of an impact but they could nevertheless aid the recovery if they are broadly positive.

Kicking things off on Tuesday are household spending stats for April, along with cash earnings for the same period. A pick up in wage growth might add to bets that the Bank of Japan will abandon its yield curve control policy sooner rather than later. On Thursday, the Q1 GDP estimate is likely to get revised up following the positive revision to capital expenditure.

Finally, in the euro area, German industrial orders and output numbers for April (Tuesday and Wednesday, respectively) will probably grab the most attention amid a manufacturing-led technical recession in Europe’s largest economy.

Will RBA Surprise Traders and Raise Rates Again?

The Reserve Bank of Australia will announce its next rate decision at 04:30 GMT on Tuesday. Markets are pricing in a 45% probability for another rate increase, as inflation has been hotter than anticipated lately. If the RBA raises rates, the Australian dollar could benefit, although it’s questionable whether the currency can sustain a rally with the Chinese economy losing steam.

Hotter inflation, slower growth

It will be a difficult decision for Australian central bank officials next week, as there are solid arguments both for raising interest rates and for pausing. The prospect of another rate increase is supported mainly by the recent trend in inflation.

After several months of declines, inflation fired up again in April and is currently on track to overshoot the Reserve Bank’s forecasts for this quarter. Similarly, the latest quarterly data on wages showed an acceleration, fanning concerns of a wage-price spiral that keeps inflation burning for some time.

Reinforcing such concerns was this week’s decision by the Fair Work Commission to raise the minimum wage by 5.75%, providing another boost to wage growth that could lead the RBA to adopt a more aggressive stance.

However, other elements suggest the RBA should take a cautious approach and do nothing next week. The labor market weakened in April, with the unemployment rate rising noticeably. Meanwhile, retail sales stagnated as consumers turned more defensive. Combined, these suggest economic growth has started to lose momentum.

Similarly, the slowdown in China’s manufacturing sector continues to intensify, which spells bad news for an Australian economy that relies on Chinese demand to absorb its commodity exports.

RBA decision is a close call

Hence, the question heading into next week’s rate decision is whether the RBA will prioritize fighting inflation or supporting economic growth. So far, policymakers have been laser-focused on bringing inflation down, and with inflationary forces regaining strength, it will be hard for the RBA to do nothing.

Markets are pricing in a 45% probability for a quarter-point rate increase, which seems relatively low considering the inflation dynamics. Nonetheless, a rate hike is almost fully priced in by July, so traders are betting it’s only a matter of time before the RBA hits the tightening button again.

Since investors view this decision as a coin toss, there is scope for the Australian dollar to gain if rates are raised. From a chart perspective, any advances in aussie/dollar could encounter initial resistance around the 0.6710 zone, which roughly encapsulates the 200-day moving average, currently at 0.6694.

On the flipside, if the RBA pauses and signals it will be patient while it examines incoming data, the pair could resume its downward trajectory, turning the spotlight towards the 0.6560 support region.

Rallies might be short-lived

Looking beyond this meeting, the trajectory in the Australian dollar might depend mostly on how the Chinese economy evolves in the coming months, and how global risk sentiment fares.

Admittedly, it’s tough to be optimistic about the aussie when Chinese demand is rolling over and commodity prices are struggling, against the backdrop of slowing global growth. The charts tell a similar story as the aussie has been trapped in a downtrend for over two years now.

One potential game-changer for the aussie would be an announcement from China that serious stimulus measures are on the way. This has been widely speculated, as it seems almost impossible for Chinese authorities to hit their growth targets without juicing up the economy.

A deluge of Chinese stimulus would be good news for the aussie, but whether it will be enough to turn the tide for good is another question. Ultimately, that might depend on the scale and scope of any measures.

Note that GDP growth numbers for Q1 will be released Wednesday, after the RBA meeting.

Stronger Earnings Growth Could be Signal BoJ Has Been Waiting For

Another month has started but the discussion about the BoJ still revolves around the same issues. With the largest central banks globally ready to pause their hiking cycle, can the BoJ map a way out of its ultra-loose monetary policy and finally boost the ailing yen?

What has been happening lately?

As we have been highlighting in recent previews, the BoJ remains in an uncomfortable position. With the largest central banks being very close to completing their rate hiking cycle, the BoJ is still looking for the light at the end of the decade-long tunnel. Its outlook was looking brighter a couple of months ago but, unfortunately for the BoJ, inflationary pressures globally appear to be abating. This was also evident at the recent Tokyo CPI print for May that surprised on the downside. So, how can the BoJ embark on some sort of monetary tightening with inflation on a downwards path?

BoJ Governor Ueda has repeatedly highlighted the fact that the Japanese inflation rise is due to external, cost-push factors. Domestic demand has been playing a secondary, much weaker role, compared to what we have seen in other countries, tying the BoJ’s hands. The way out of the current deadlock is the consumer sector, thus raising the importance of the recent strong, above-inflation wage increases. The BoJ is expecting these increases to have a material impact on consumer spending and consumer sentiment going forward.

Amidst this challenging environment, there is increased nervousness about the BoJ’s next move. The market has gotten used to the ultra-loose monetary stance with the yen being the traditional funding currency for carry trades. Therefore, a change of policy by the BoJ or even adoption of a more hawkish stance is expected to have a stronger impact, especially on the FX markets. The ECB was quite vocal about this possibility at its most recent Financial Stability review. It was also highlighted that a wave of yen repatriation could create an investment gap in the European and US bond markets.

Plethora of data but two releases stand out next week

Understandably, next week's focus will be on Tuesday’s figures and, to a lesser extent, on Thursday’s releases. The final GDP print for the first quarter of 2023 and the current account figures for April, both released on Thursday, are critical pieces of the economic puzzle, but as described above the focus is squarely on domestic earnings and spending.

The year-on-year change in the labour cash earnings is forecast to moderate even further to 0.5%. If confirmed, this would be the lowest print since February 2022, and a potential signal that the optimism after the recent wage agreements might have been premature. Similarly, the overall household spending data for April is expected to show some improvement but remain in negative territory. A positive set of data figures on Tuesday would be greatly welcomed at the BoJ halls, but probably not by the bond markets.

Can the yen finally recover some of its 2023 losses?

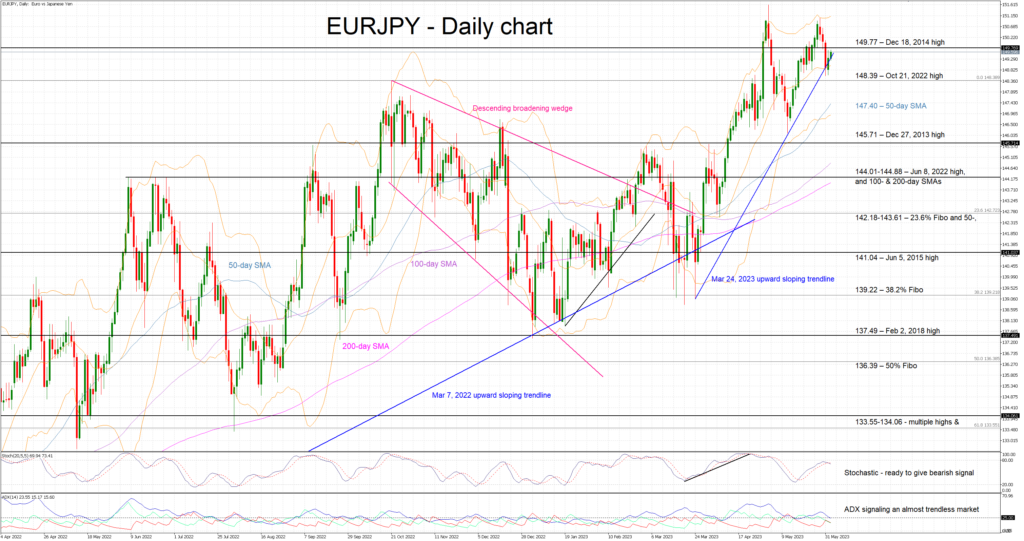

The 15-year high at 151.61 in euro/yen appears to have somewhat energized the yen bulls as they have been trying to stop this pair’s advance. Their effort has been fruitless up to now, but the formation of a double top pattern could be the answer to their prayers.

Should the data releases surprise to the upside and sentiment turn in favour of the yen, we would see a retreat towards the 148.39 level and a retest of the 147.22 level. A break of the neckline of the formed pattern at 146.13 could result in an even stronger correction. On the other hand, an upwards break of the 149.77 level could open the door for a higher high, above the recent 151.61.

Weekly Focus – Softer Inflation Prints Drive Yields Lower

Hopes for inflation coming down faster than expected drove market sentiment towards the end of the week. The euro area inflation print released on Thursday confirmed the disinflationary prints from country releases in previous days. HICP came in at 6.1%, which is a sharp drop from 7% in April. Core inflation also slowed more than anticipated to 5.3% from 5.6% in April. For now, the introduction of the EUR49 German transport ticket is likely to have been a key reason for this decline and hence we should be careful interpreting this core print. Nevertheless, stock markets cheered inflation coming lower faster than expected while yields drifted lower. The German 10y yield is trading almost 30bp lower compared to a week ago and the ECB peak rate is priced 9bp lower at 3.64%.

A financial market apocalypse in the US was avoided as the policymakers agreed on a deal to raise the country's debt ceiling. The bill passed the senate with 46 Democrats and 17 Republicans supporting it while five Democrats and 31 Republicans opposed the legislation. The debt ceiling driven drain in the Treasury General Account has supported liquidity, and hence, contributed to easing financial conditions lately, a development which we now expect to reverse.

Chinese PMI from NBS on Wednesday was weaker than expected across the board and pointed to new stimulus soon from the government and PBOC. The NBS PMI manufacturing PMI dropped from 49.2 to 48.8 (consensus 49.5) with details also being soft. Both new orders and export orders dropped. Then again, Caixin manufacturing PMI came out better than expected and in the expansionary territory. We still conclude that recovery in China is losing steam. Markets turning positive on Friday is more related to positioning and unlikely to be a sustainable phenomenon.

In Turkey's presidential run-off, Erdogan secured 52.2% of the votes and sealed his iron grip on power for the next five years. We think that in the absence of a turnaround in economic policy, Turkey could eventually end up in a currency crisis where lira's value would collapse, inflation would explode and even goods shortages could occur. Turkish corporates with large foreign liabilities would face substantial rollover risks. Read more in our election review Research Turkey - Time to fasten seat belts as Erdogan secures another term, 29 May.

Next week, we get the ISM services index from the US. Service PMI was fairly strong in May, so it will be interesting to see whether this is being reflected in the ISM as well. We are expecting the RBA to maintain rates unchanged on Tuesday. Markets are pricing a small (30-35%) risk of a 25bp hike. German factory orders for April are out on Tuesday as well. Orders fell a lot in March and now we are looking into more signals of whether this was a temporary thing or a sign of a more severe contraction. China will publish CPI data for May out on Friday. Inflation was 0.1% y/y in April, and a below zero print would create some headlines. On the geopolitical front, we continue to follow the events in Ukraine as the spring offensive is looming.

Sunset Market Commentary

Markets

The US jobs report delivered yet another big beat in the headline figure, the 14th in a row. Employment grew a whopping 339k in May with the previous two months revised up by 93k. That brings about a total upward surprise of 237k. Average hourly earnings were more or less as expected, coming in at 0.3% m/m to be up 4.3% y/y. That’s one tenth below consensus and the April figure. There are some inconsistencies though with the unemployment rate rising from 3.4% to 3.7% vs 3.5% expected despite the bumper payrolls growth and a stable participation rate (62.6%). This is because the number is derived from a separate household survey where employment instead of rising, dropped by no less than 310k. After a kneejerk rate move higher which went to 10 bps and more at the front, gains were cut a bit to 2.9-7.5 bps across the curve as investors stick to the idea of a Fed June rate skip. There’s only one chance in three discounted for a hike. Fed governors including Jefferson and Harker in the run-up did their best to cement such a scenario in market thinking before the blackout period kicks in this weekend. The case for a July hike does strengthen again (about 80% chance). German Bund yields were rising a few bps earlier in the day before temporarily extending gains in sympathy with the US. They remain near the lows of this week though. Current changes vary between 2.3 (30-y) to 6.3 bps (2-y, 5-y).

Strong payroll growth and the yield advance has little effect on the US dollar. An attempt to recoup some of losses incurred against the euro yesterday was in vain. EUR/USD trades around opening levels in the 1.076/1.077 area. The trade-weighted index goes nowhere (103.58). Capping the dollar’s appeal except from US yields quickly retreating from intraday highs is the broad risk-on mood on equity markets. Stocks easily gain 1% and more. Markets cheer at a Bloomberg report citing people familiar with the matter that China is working on a new basket of measures to support the property market. Existing/previous plans including the 16-point rescue package have clearly failed to do the trick. The Chinese yuan rallied against the USD. USD/CNY trades at 7.072, down from 7.103. Commodities including Brent oil (+2.2%), copper (+1.5%) and iron (+2.55%) rally. The likes of the CAD and NZD eke out a small gain. AUD outperforms G10 peers following reports of a 5.75% minimum wage increase this morning.

News & Views

In May, the food price index of the UN Food and Agricultural Organization dropped another 2.6 M/M and stands 22.1% below the all-time high reached in March 2022. The May decline was driven by significant drops in the indices of vegetable oils, cereals and dairy which were partially counterbalanced by increases in the sugar and meat indices. The cereal price index dropped 4.8% M/M. Wheat prices declined 3.5% reflecting the prospects for ample global supplies in the 2023/24 season and the extension of the Black Sea initiative. Prices of maize dropped 9.8% on higher expected production in the US and Brazil. The price of rice was an exception to the broader decline. Vegetable oil price extended their downtrend (-9.8% M/M and 48.2% Y/Y). The decline in dairy prices was more modest (3.2% M/M) with milk powders even rebounding. Meat prices were up a modestly (1.0% M/M), the fourth consecutive monthly increase to be only 4.1% lower Y/Y. The sugar price remains on a sustained uptrend (5.5% M/M, fourth consecutive monthly rise) standing 30.9% higher compared to the same month last year. Rising concerns over the development of the El Niño phenomenon on 2023/24 crops, together with lower-than-earlier-expected availabilities in 2022/23 and shipping delays are said as causing the rise.

According to Reuters reporting, Vice Chairman of the Swiss National Bank (SNB), Martin Schlegel said the SNB remains ready to tighten policy further as it sees inflation spreading across the economy to other goods and services that are not linked to energy and supply bottlenecks. The Vice Chairman also mentioned the potential impact of higher interest rates on rents which could add to inflation later this year. Swiss inflation in April slowed to 0.0% M/M and 2.6% Y/Y. Core inflation was unchanged at 2.2%. The SNB aims to keep inflation between 0.0% and 2.0%. In its March quarterly Bulletin it forecasted inflation to ease for 2.6% this year to just the 2.0% top of the policy range in 2024/2025. The SNB holds its next policy meeting on 22 June, with May CPI data to be published Monday next week. The Swiss franc this week eased off the highest level in more than six months against the euro (EUR/CHF 0.9672) to currently trade near 0.976.

US: Strong May Payrolls Print Keeps Summer Rate Hike in Play

The U.S. economy added 339k jobs in May, well above the consensus forecast of 195k. Revisions to the two prior months were positive, adding a meaningful 93k from the previously reported figures. Hiring over the last three-months averaged 283k jobs per-month, an uptick from the 253k recorded in April.

Employment gains on the service side (+257k) were relatively broad based, with healthcare (+75k), professional & business services (+64k), leisure & hospitality (+48k) and transportation & warehousing (+24k) leading the charge. The goods sector (+26k) also added jobs last month, though gains were almost entirely concentrated in construction (+25k), while manufacturing shed 2k jobs. Hiring across government remained very strong, adding 56k jobs in May.

In the household survey, civilian employment fell by 310k while the labor force gained 130k – resulting in a sharp 0.3% percentage point (ppt) uptick in the unemployment rate to 3.7%. Meanwhile, the participation rate held steady at its cyclical high of 62.6%.

Average hourly earnings rose 0.3% month-on-month (m/m) – a deceleration from April's downwardly revised gain of 0.4% m/m. Relative to last May, hourly earnings slowed a tenth of a percentage point to 4.3%, though the more truncated three-month annualized change rose to 4.0% (from 3.8% in April).

Key Implications

Another strong reading on U.S. job creation! Over the last three months, job growth has averaged 283k jobs per-month. This marks an uptick from the steady downward trend seen over the last several months. At its current pace, job growth continues to run at a clip that's more than three-times what's required to meet trend growth in the labor force.

Beyond the healthy gain in employment, this morning's report also offered other evidence that the labor market remains hot. The breadth of hiring remained reasonably strong – with only two industries shedding jobs – while revisions to the two prior months were significantly higher, adding an additional 93k jobs. And while the unemployment rate jumped by 0.3 ppts, we will discount that for now given the inherent volatility in the household survey. Moreover, at 3.7%, the unemployment remains at the upper end of the very narrow range (3.4%-3.7%) where it has oscillated over the past 15 months.

While most Fed officials seem to support skipping a June rate hike to better assess the data flow, this morning's employment report certainly keeps the possibility of another 25-basis point (bps) hike in play later this summer. Irrespective of whether the Fed does eventually push ahead with another hike, the theme of 'higher for longer' seems to be reverberating through financial markets. Just a month ago, investors were pricing in 75 bps of rate cuts by year-end. Today, virtually no cuts are priced for 2023. With the labor market continuing to show incredible resilience and inflationary pressures persisting, we don't expect the Fed to begin easing the policy rate until at least Q1 of next year.

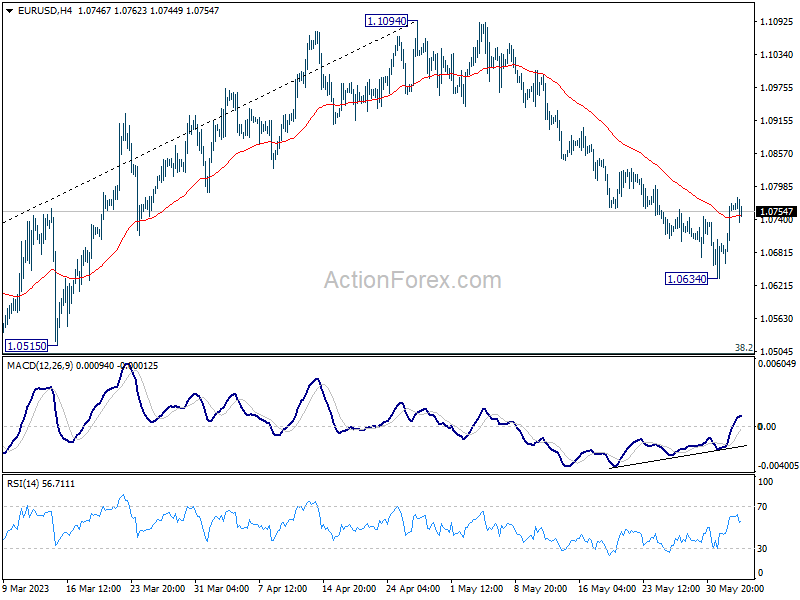

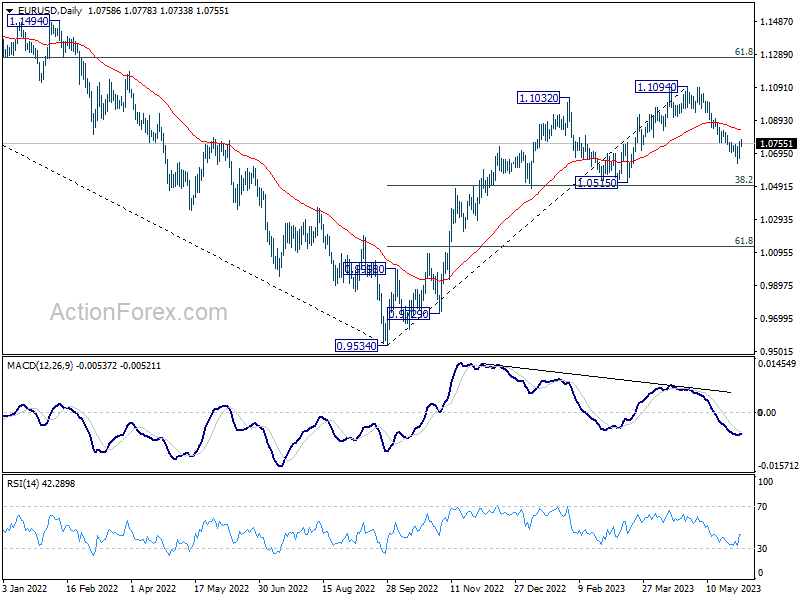

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0694; (P) 1.0731; (R1) 1.0800; More...

Intraday bias in EUR/USD stays mildly on the upside at this point. Rebound from 1.0634 short term bottom is in progress for 55 D EMA (now at 1.0836). On the downside, though, break of 1.0634 will resume the fall from 1.1094 to 1.0515 cluster support, 38.2% retracement of 0.9534 to 1.1094 at 1.0498.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

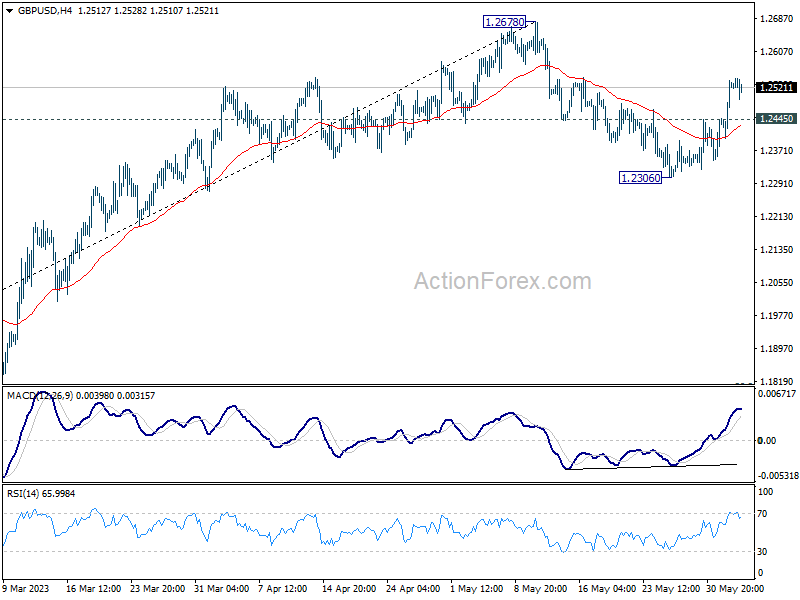

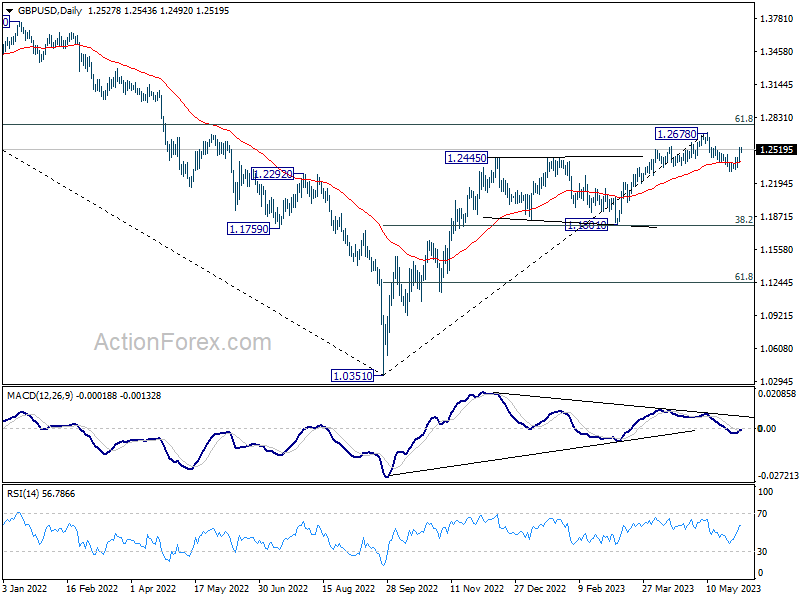

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2438; (P) 1.2489; (R1) 1.2577; More...

Intraday bias in GBP/USD stays mildly on the upside at this point. Rebound from 1.2306 is in progress for retesting 1.2678 high. Decisive break there would resume larger up trend from 1.0351 to 1.2759 fibonacci level. Meanwhile, below 1.2445 minor support will turn intraday bias neutral first. Further break of 1.2306 will resume the correction towards 1.1801 cluster support (38.2% retracement of 1.0351 to 1.2678 at 1.1789)

In the bigger picture, as long as 1.1801 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.1801 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.

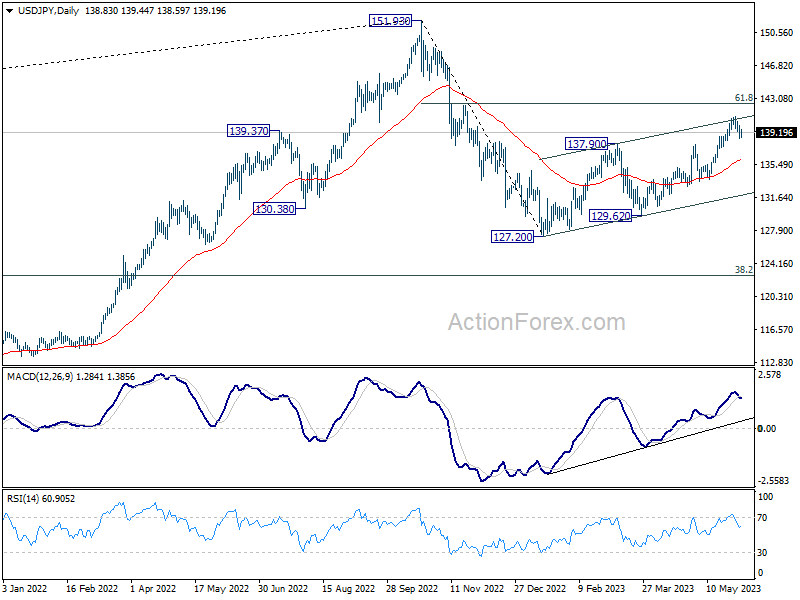

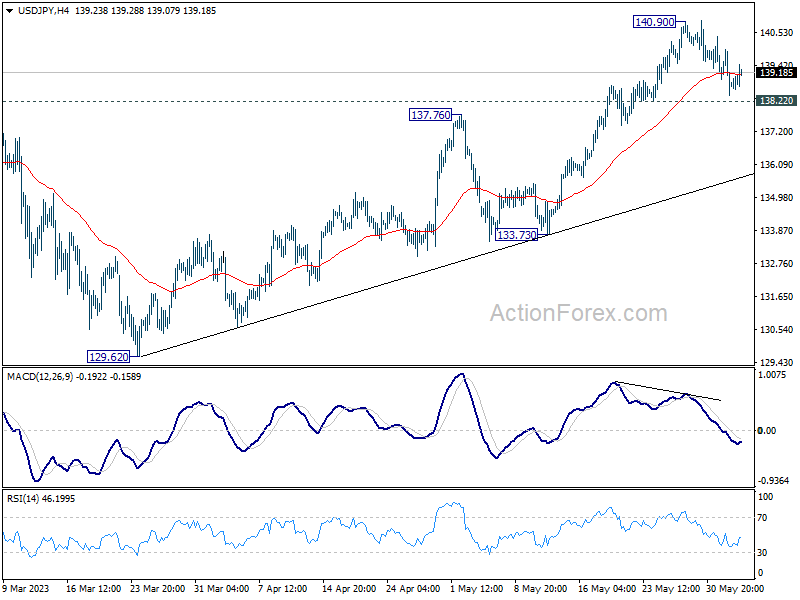

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 138.19; (P) 139.07; (R1) 139.68; More...

Intraday bias in USD/JPY remains neutral as range trading continues. Downside of retreat should be contained above 138.22 support to bring another rally. Break of 140.90 will resume larger rise from 127.20 to 142.48 fibonacci level. However, considering bearish divergence condition in 4 hour MACD, break of 138.22 will confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 135.98).

In the bigger picture, rise from 127.20 is seen as the second leg of the corrective pattern from 151.93 high. Stronger rally would be seen to 61.8% retracement of 151.93 to 127.20 at 136.34. Sustained break there will pave the way back to retest 151.93. On the downside, however, break of 133.73 support will argue that the pattern could have started the third leg through 127.20 low.